asset/liability management for life insurers contractual savings conference – supervisory and...

TRANSCRIPT

Asset/Liability Management for Life Insurers

Contractual Savings Conference – Supervisory and Regulatory Issues in Private Pensions and Life Insurance

Presentation by

David F. Babbel, Professor

Department of Insurance and Risk Management

Department of Finance

Wharton School, University of Pennsylvania

Philadelphia, Pennsylvania USA 19104-6218

The limited imagination of courts…

• Baldwin United• Executive Life Companies

– Executive Life of California– Executive Life of NY

• First Capital Holdings - SLH– First Capital Life– Fidelity Bankers Life– E. F. Hutton Life

• Mutual Benefit Life• Confederation Life• National Heritage Life• ARM Financial

– Integrity Life– National Integrity Life

• General American Life• Mutual Fidelity

• $4 billion• $20 billion

– $16 billion– $4 billion

• $12 billion– $5 billion– $5 billion– $2 billion

• $16 billion• $17 billion• $2 billion• $10 billion

– $5 billion– $5 billion

• $15 billion• $1 billion

Near misses…

• Equitable Life Assurance

• Mutual of New York MONY

• Presidential Life

• Colonial Penn

• and many, many more…

• $80 billion

• $24 billion

• $2 billion

• $8 billion

• $XXX billion

Two Observations...

• Insurers will act according to the economic incentives they face– To maximize share value– To maximize value of owners’ equity– To fulfill managements’ desires

• An insurance policy is a contingent claim to the policyowner– Life insurance cash flows are contingent upon an “event”– “Event” can be precipitated by:

• Policyholder choice• Chance

Market Value of Insurance Stock:

The Static View

MarketValue

of Stock

= FranchiseValue

Net TangibleValue

PutOption

+ +

Components of Insurance Stock Market Value– “Economic rents,” present value of future profits– Charter value– Reputation– Distribution network– Personnel

– Market value of tangible assetsless

– Present value of liabilities– Closely related to liquidation value

– The value of issuing debt (i.e., policies) at below-market rates due to the insurance insolvency guarantee programs– The value to equity holders of capturing the upside earnings while not incurring all of the costs of default

Franchise Value

Net Tangible Value

Put Option

{

{{

Risk and the Components of Value

Firm Risk

Firm Risk

Firm Risk

Franchise Value

Market value of tangible assets

Put Option Value

Present value of liabilities

Net Tangible Value

Components of Value Combined

1.0 -

Net Tangible Value

Firm Risk

Franchise Value

Put Option ValueMarket

Value

Net Tangible Value

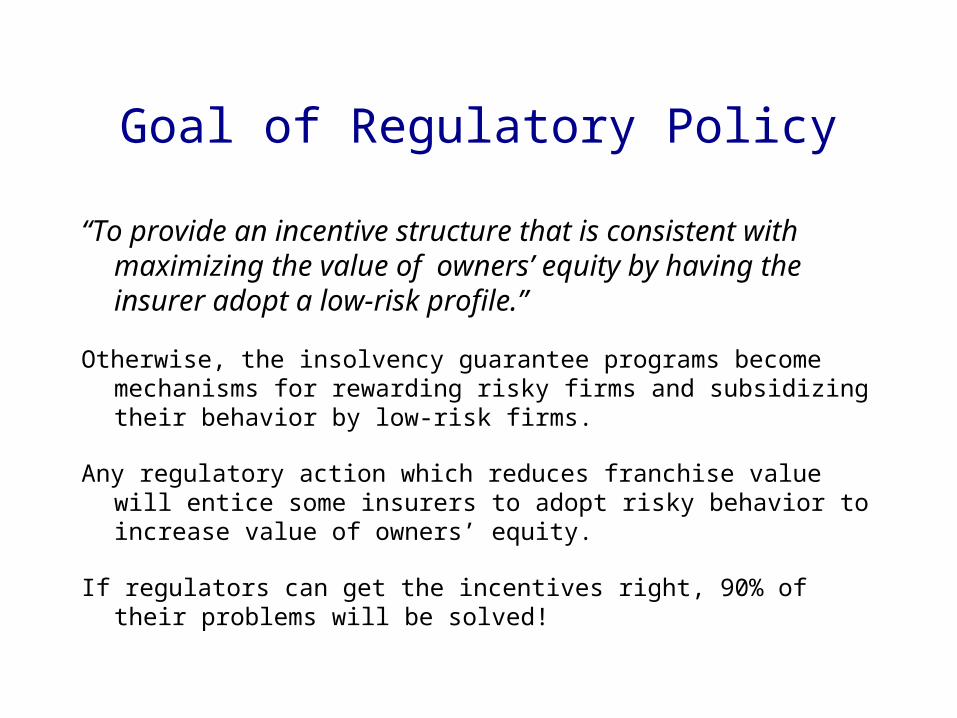

Goal of Regulatory Policy

“To provide an incentive structure that is consistent with maximizing the value of owners’ equity by having the insurer adopt a low-risk profile.”

Otherwise, the insolvency guarantee programs become mechanisms for rewarding risky firms and subsidizing their behavior by low-risk firms.

Any regulatory action which reduces franchise value will entice some insurers to adopt risky behavior to increase value of owners’ equity.

If regulators can get the incentives right, 90% of their problems will be solved!

Betting the Bank

Insurers most likely to bet the bank have:

– Low franchise value

– Minimal liquidation value

With little to lose, the insurer will bet the bank

– If the bet is won, the owners benefit

– If the bet is lost, others (policyholders, contributors to the various state insolvency guarantee programs, and tax-payers) pick up the tab

The ability to bet the bank will be enhanced if the insurer can hide its true capital situation by inflating statutory surplus

Capital or Crapital?

Substitute future profits for surplus surplus relief reinsurance commission financing

Front load earnings commission financing asset yields higher than expected returns

• negative convexity instruments• duration mismatch, foreign currencies• low quality, low liquidity

Engage in actuarial subterfuge high discount rates, aggressive reserving methods low lapse, aggressive mortality & morbidity assumptions

Run up the sales offer high crediting rates, low surrender charges engage in lax underwriting, misprice policies

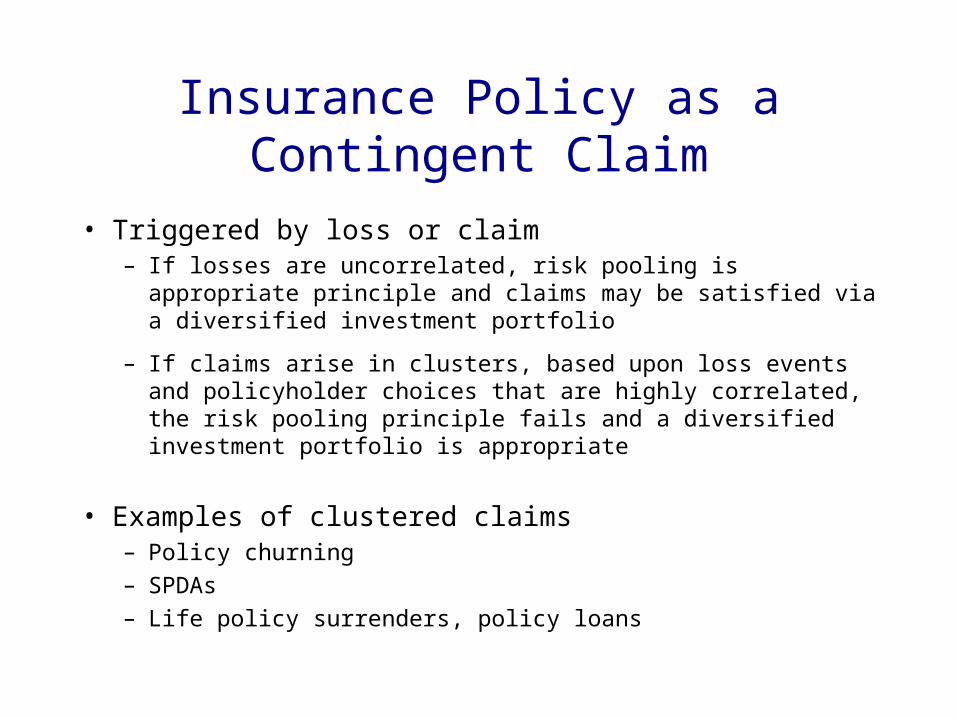

Insurance Policy as a Contingent Claim

• Triggered by loss or claim– If losses are uncorrelated, risk pooling is appropriate principle and

claims may be satisfied via a diversified investment portfolio

– If claims arise in clusters, based upon loss events and policyholder choices that are highly correlated, the risk pooling principle fails and a diversified investment portfolio is appropriate

• Examples of clustered claims– Policy churning

– SPDAs

– Life policy surrenders, policy loans

Simple Rules of ThumbMay do more harm than good

– MIL and MBS

– Prohibitions of certain investment classes

– Slow to incorporate new investment vehicles

– Duration matching• Basis risk

– Long vs. short-term interest rates– Domestic vs. foreign currencies– Liquid vs. illiquid investments– Taxable vs. tax-free status– Credit quality

• Taking options into account

– Ignoring one side of balance sheet

– Focus on earnings

Market Value of Insurance Stock: The Dynamic View

• Increments to Economic of Surplus depend on gaining positive Net Present Value

• Net present value may arise from asset or liability side of balance sheet

Where does NPV come from?(Developed Countries Version)

• Asset Side?– Very unlikely

– Perhaps after the fact• Unrealized credit risk

• Economic environment changed

• Liability Side?– Theoretically likely– Depends on pricing

• Tax preference• Guarantee programs• Translucency• Imperfect competition

MV[NW] = MV[A] MV[L]

Where does NPV come from?(Developing Countries Version)

• Asset Side?– Possible

– Possibly negative NPV• If domestic investors have no external

outlets• If foreign investors have no access

– Perhaps after the fact• Unrealized credit risk• Economic environment changed

• Liability Side?– Theoretically likely– Depends on pricing

• Tax preference• Minimum embedded interest

rate requirements• Guarantee programs• Translucency• Imperfect competition

But doesn’t NPV come from actuaries?

Netting Expected Cash Flows

Assets = $100 million Liabilities = $100 million Economic Surplus = 0

Asset cash flows(in $millions)

Liabilities cash flows(in $millions)

Interestpayments@ 10%

promisedyield

Interestpayments

adjusted for1%

historicaldefault risk

Liability expectedpayments

@ 8%embedded interest

Expectednet cash flow

Year 1 10 9 8 1Year 2 10 9 8 1Year 3 10 9 8 1Year 4 10 9 8 1Year 5 10 9 8 1Year 6 10 9 8 1. . . . .. . . . .. . . . .Year n 10 9 8 1

. . . . .

. . . . .

. . . . .

Surplus Value of perpetual business = $1 million ÷ 10% = $10 million

Voila!

In summary...

Regulators should ensure that the economic incentives faced by insurers are consistent with preserving franchise value and liquidation value.

Best accomplished if insurers have something of value -- net tangible value -- to lose by pursuing risky investment strategies and other risky insurance operations.

Need to redefine “risky.”

Insurance regulators have considered applying various

asset/liability management tools to measure, monitor and

regulate insurer insolvency…

Don’t do it!

A / L MTools

(for regulatorypurposes)

Why not??

Everybody else is doing it!

Early History of A/L M

• Macaulay 1938• Hicks 1939• Reddington 1952• Duration enhancements

– Fisher-Weil– Bierwag, Kaufman, Toevs– Khang– Babbel, Nelson, Schaefer– Effective Duration– Convexity

• Focus was always on value and changes in value

• Tools fixated on interest rate risks

• Each risk measure was generally consistent with the assumed underlying interest rate process

A Dubious Turn

• Insurance regulation– NY Reg. 126

– Seven interest rate scenarios

– NY Reg. 128

• Software vendors got into the act

• CALMS, TAS

• PTS

• Polysystems

• Focus turned to:– income

– cash flows

– yield spreads

– statutory surplus

Asset/Liability Management: Recent “Advances”

Earlier A/L M Models– Immunization Model– Dedication Model– Mean-variance models– Expected utility models– Multicriteria decision models

More Recent A/L M Models• Stochastic Control A/L M

Models• Multistage Stochastic A/L M

Programming with Decision Rules

• Capital Growth

• Stochastic Programming A/L M Models– Chance Constrained Model– Dynamic Programming– Sequential Decision

Analysis– Stochastic Linear

Programming with Recourse– Dynamic Generalized

Networks– Scenario Optimization– Robust Optimization

The 12 “new” objective functions…

• Maximize asset portfolio yield• Minimize purchase price of asset portfolio• Minimize initial cash holdings• Minimize variance s.t. a target return• Maximize expected utility• Minimize a function of deviations from targets set for goals• Minimize cost of funding s.t. acceptable levels of insolvency risk• Maximize expected terminal wealth s.t. no shorts, limits on particular

asset holdings• Maximize E[V] of firm at horizon subject to penalties of shortfalls• Maximize E[U] of surplus at end of planning horizon• Minimize downside risk for a given average contribution rate• Maximize the expected log of asset wealth

109 papers cited…• Operations Research• European Journal of Operations

Research• Annals of Operations Research• Journal of Operations Research• Journal of the Operations Research

Society• Mathematics of Operations

Research• ORSA Journal of Computing • Journal of Applied Econometrics• Journal of Econometrics• Econometrics Review• Journal of Economic Dynamics

and Control

• Applied Mathematics and Optimization

• Mathematical Programming • Journal of Applied Mathematics• Informs Journal on Computing• Annals of Statistics• Journal of Information and

Optimization Sciences• Transactions of the Faculty of

Actuaries• International Journal of Forecasting• Management Science• Interfaces• Risk

A Commonly Used Model

Asset TypesAsset Types

TYPE A TYPE B TYPE C

Foreign Exchange Interest Credit Risk

TYPE A TYPE B TYPE C

Key Driving

Factors

Key Driving

Factors

TYPE A TYPE B TYPE C

Model 1 Model 2 Model 3

Each different model is specialized to focus on key factor.

This specialization is aimed at speeding solutions.

Problem: how can you measure portfolio exposure to risk factors?

TYPE A TYPE B TYPE C

Model 1 Model 2 Model 3

Unified

Valuation

Model

Recommendations…

Developed Countries• Focus on economic

incentives• Focus on valuation• Focus on net tangible

value• A/L M measures are not

ready to be useful; indeed, they provide false comfort

Developing Countries• Focus on economic

incentives• Valuation tools are not

useful at this point• Focus on contributed

tangible capital• A/L M measures are not

ready to be useful at all for regulatory purposes

But what if our goal is to develop internal capital markets?

• Distinction between number of companies and amount of capital formation

• Confidence is a major concern

• Government guarantees cannot alone answer this concern

• Fostering small company entry into the market could destroy confidence and ultimately worsen capital formation