lecture 5 money, credit and banking in history. coincidence of wants with coincidence of wants...

Post on 22-Dec-2015

227 views

TRANSCRIPT

Lecture 5

Money, credit and banking in history

Coincidence of wants

• With coincidence of wants barter trades match perfectly.

• Barter is exchange of, say, wheat for shoes• Coincidence of wants is the exception rather

than the rule.• Could modern web based search machines

help? • Perhaps but transaction cost would probably be

high. • Think of examples….

A case of coincidence of wants

The origin of money

• Money opens up for trade in situations of non-coincidence of wants by direct barter.

• It is wanted by all because it is possible to purchase all sorts of goods from all sorts of people.

• Commodity money restores the coincidence of wants if money is wanted by all

• It makes it possible to postpone a purchase into the future

• It provides a unit to express the prices of all other goods

A case of non-coincidence of wants

A mix of barter and money sometimes helps

Three basic functions of money

• As a means of payment, it should be easy and quick to evaluate on inspection, to be divisible into small units and to carry in your pocket, which excludes…used cars

• As a store of value it should be made of a non-perishable good, which excludes…

• As a unit of account it should be divisible into small units, which excludes…

Why commodity money?

• Commodity money has an intrinsic value: a silver coin can be melted and the silver can be sold at a price close to the face value of the (melted) coin.

• It is therefore not profitable for counterfeiters to make coins because professional money changers can easily detect if the fineness of the metal has decreased.

A day at the job: making money

Varieties of medieval coins

Seigniorage & debasement

• The mint claims a fee, 5-15 percent to mint coins.

• If a merchant comes to the mint with 200 g of silver he will get 100 to 110 Carolingian pennies each with a silver weight of 1.7 g.

• The Crown was often tempted to lower the silver content in coins by increasing seigniorage.

Debasement in Italy

The spectacular diffusion of mints, before 973

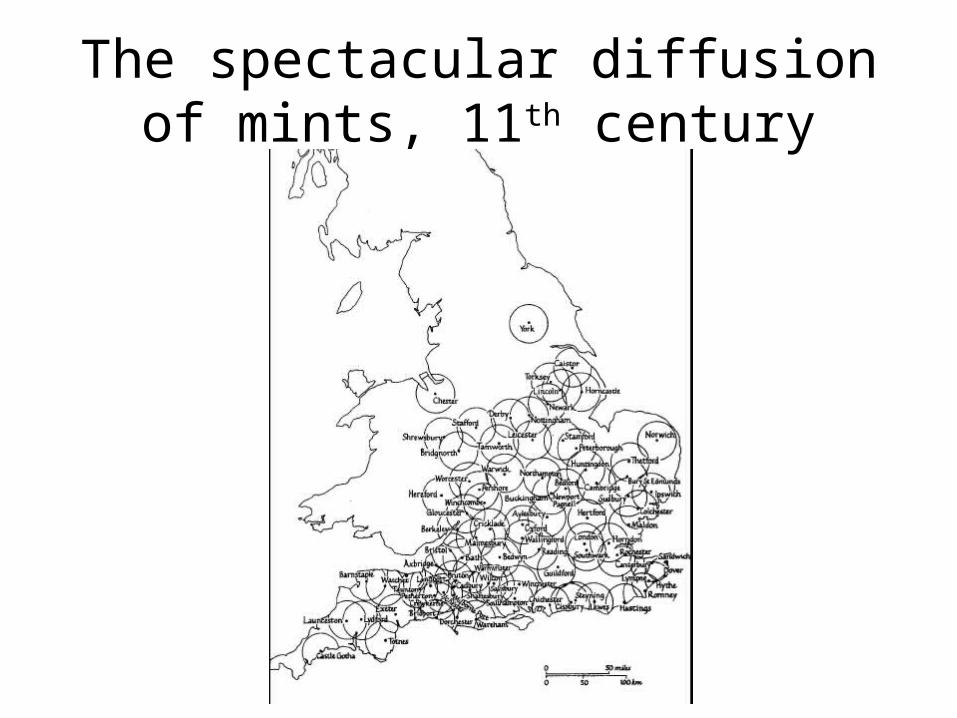

The spectacular diffusion of mints, 11th century

Why not paper money?

• Spontaneous development of paper money: Goldsmiths’ receipts.

• Fractional banking (banks which hold only a fraction of deposits as reserves) and note-issue: a difficult balance.

• Banks create money but tend to overextend lending and become victims of bank-runs.

• Bank-runs can ruin banks which are fundamentally sound.

Governments and paper money

• Governments often misused its monopoly over money supply. ’Printing money’

• Paper money convertible to gold was the rule until early 20th century.

• Non-convertible paper money is based on trust and the belief that fiat money is accepted as a means of payment by all.

• Historic trend towards independent national banks reveal public mistrust of governments.

What do Banks do?

• Banks do ‘delegated monitoring’ over borrowers on behalf of savers.

• Banks solve information asymmetries.

• Banks transform savers’ preferences for liquid assets to long term commitments to firms.

Banks and growth

• By reducing risk and increase rewards for savers banks can increase the savings ratio – and plausible the investment ratio.

• Banks can improve the efficiency of allocation of savings : picking the winners, since banks specialize in processing information.

What banks doSavers’ Problem What Banks do Entrepreneurs/Borrowers’

Problem

Costly to assess Investors Exploit economies of scale in information processing

Finding willing investors(High search cost; cash constraints)

Risky not to diversify saving Hold diversified asset portfolios

Relationship of banking

Savers want liquid assets Banks have (fractional) reserves

Need long term commitment for investment in fixed capital

Asymmetric informationSavers do not have the access to Borrowers’ private information

Banks practice delegated monitoring of firms

Entrepreneurs exploit private information

England - Germany: 0 -1?

• Relationship banking vs. transaction banking.

• Did England fail because banks did not commit to firms’ need for long term capital?

• Hypothesis: English firms were strangled by cash constraints and deficient information generated by transaction type banking.

Banks and Stock markets

• Two (complementary?) ways of monitoring firms.

• Historically stock market traders more exclusive group than bank customers – an information and trust problem.

• Stock market traders might under-invest in information gathering, which might create bubbles.

The lecture in one single graph!

Conclusion

• Financial history

• is a story of the development of less risky and less costly

• it highlights the importance of trust for stable institutions,

• it demonstrates that institutions (banks) develop to solve asymmetries between savers and borrowersI