lecture 24: risk premium portfolio diversification risk.pdf · 24: risk premium & portfolio...

TRANSCRIPT

Lectures 24 & 25: Risk

• Lecture 24: Risk Premium & Portfolio Diversification • Bias in the forward exchange market

as a predictor of the future spot exchange rate

• What makes an asset risky?

• The gains from international diversification

• The portfolio balance model

• Appendix: Intervention in the FX Market

• Lecture 25: Sovereign Risk

• Lecture 26 – Possible topics: • Procyclical fiscal policy

• Greece & the euro crisis

• Recent macro history of China ITF220 - Prof.J.Frankel

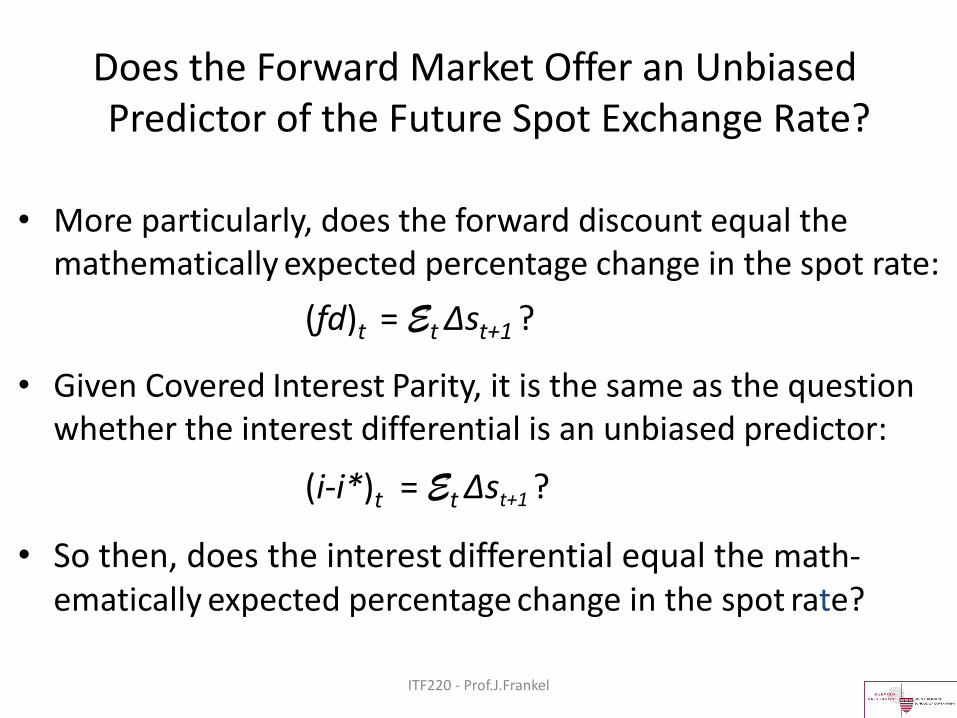

Does the Forward Market Offer an Unbiased Predictor of the Future Spot Exchange Rate?

ITF220 - Prof.J.Frankel

• More particularly, does the forward discount equal the mathematically expected percentage change in the spot rate:

(fd)t = Et Δst+1 ?

• Given Covered Interest Parity, it is the same as the question whether the interest differential is an unbiased predictor:

(i-i*)t = Et Δst+1 ?

• So then, does the interest differential equal the math-ematically expected percentage change in the spot rate?

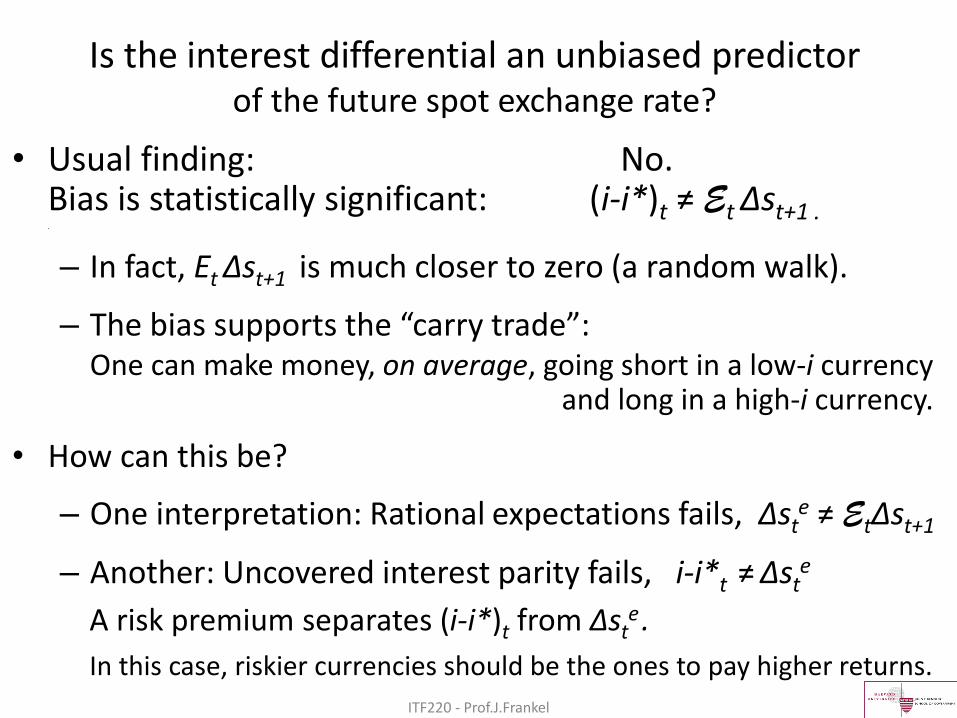

Is the interest differential an unbiased predictor of the future spot exchange rate?

• Usual finding: No. Bias is statistically significant: (i-i*)t ≠ Et Δst+1 . .

– In fact, Et Δst+1 is much closer to zero (a random walk).

– The bias supports the “carry trade”:

One can make money, on average, going short in a low-i currency and long in a high-i currency.

• How can this be?

– One interpretation: Rational expectations fails, Δste ≠ EtΔst+1

– Another: Uncovered interest parity fails, i-i*t ≠ Δste

ITF220 - Prof.J.Frankel

A risk premium separates (i-i*)t from Δste

.

In this case, riskier currencies should be the ones to pay higher returns.

What makes an asset risky to a portfolio investor?

• If uncertainty regarding the value of the currency (variance) is high.

• If you already holds a lot of assets in that currency.

• If currency is highly correlated with other assets you hold. What matters is how much risk the currency adds to your overall portfolio.

ITF220 - Prof.J.Frankel

The gains from international diversification

• James Tobin: The theory of optimal portfolio diversification

• “Don’t put all your eggs in one basket.”

• The theory was worked out for stocks in the Capital Asset Pricing Model (CAPM).

• Applies to all assets: bonds, equities; domestic, foreign.

• International markets offer a particular opportunity for diversification, because they move independently to some extent.

ITF220 - Prof.J.Frankel

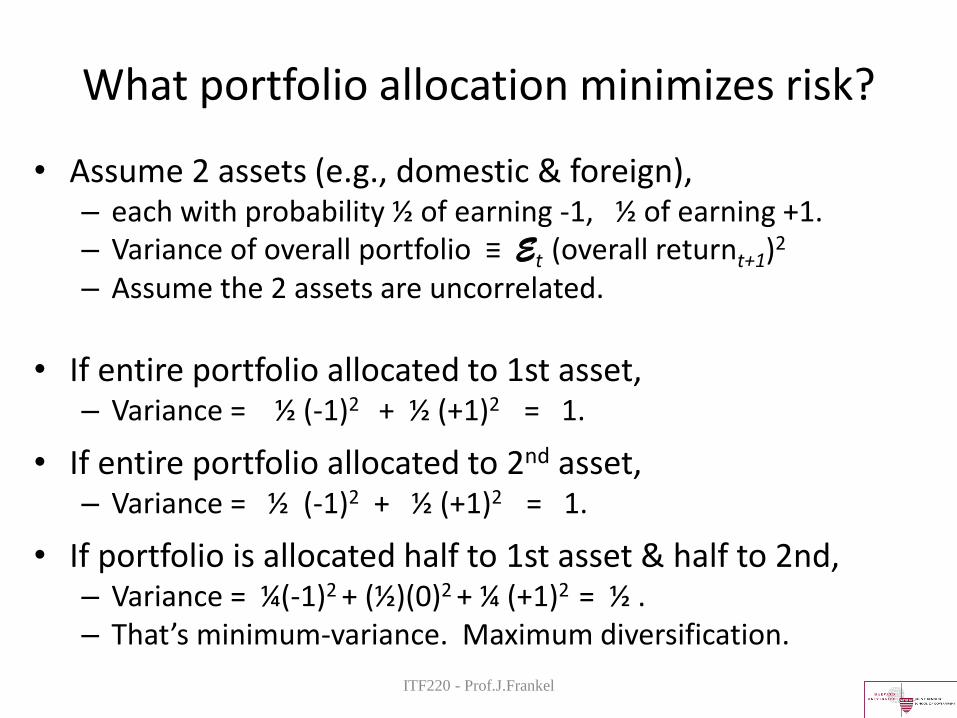

What portfolio allocation minimizes risk?

• Assume 2 assets (e.g., domestic & foreign), – each with probability ½ of earning -1, ½ of earning +1. – Variance of overall portfolio ≡ Et (overall returnt+1)2

– Assume the 2 assets are uncorrelated.

• If entire portfolio allocated to 1st asset, – Variance = ½ (-1)2 + ½ (+1)2 = 1.

• If entire portfolio allocated to 2nd asset, – Variance = ½ (-1)2 + ½ (+1)2 = 1.

• If portfolio is allocated half to 1st asset & half to 2nd, – Variance = ¼(-1)2 + (½)(0)2 + ¼ (+1)2 = ½ . – That’s minimum-variance. Maximum diversification.

ITF220 - Prof.J.Frankel

Diversification lowers risk to the overall portfolio.

The investor can achieve a lower level of risk by diversifying internationally.

Standard deviation of return to portfolio

ITF220 - Prof.J.Frankel

Investors want to minimize risk and maximize expected return.

• To get them to hold assets that add risk to the portfolio, you have to offer them a higher expected return.

• That is why stocks pay a higher expected return than treasury bills.

• Do foreign assets pay a higher expected return than domestic assets?

ITF220 - Prof.J.Frankel

Placing 20% of your portfolio abroad reduces risk (diversification). After that point, the motive for going abroad is higher expected return;

investors who are more risk averse won’t go much further.

Risk →

↑ Return

Medium risk- aversion

High risk- aversion

Low risk- aversion

Purely US

ITF220 - Prof.J.Frankel

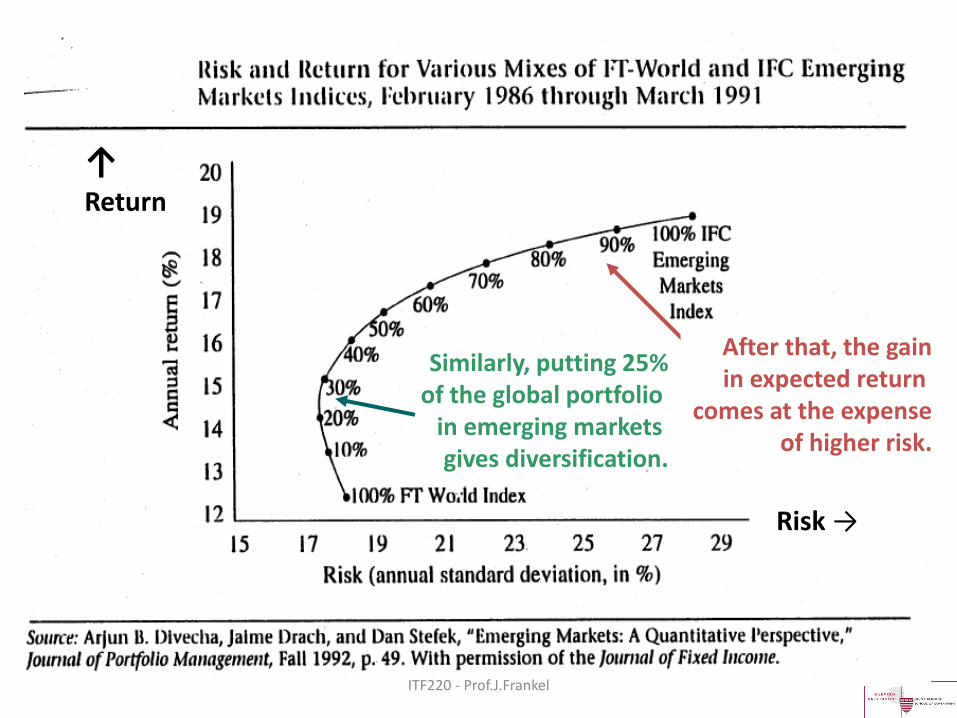

Similarly, putting 25% of the global portfolio

in emerging markets gives diversification.

Risk →

↑ Return

After that, the gain in expected return

comes at the expense of higher risk.

ITF220 - Prof.J.Frankel

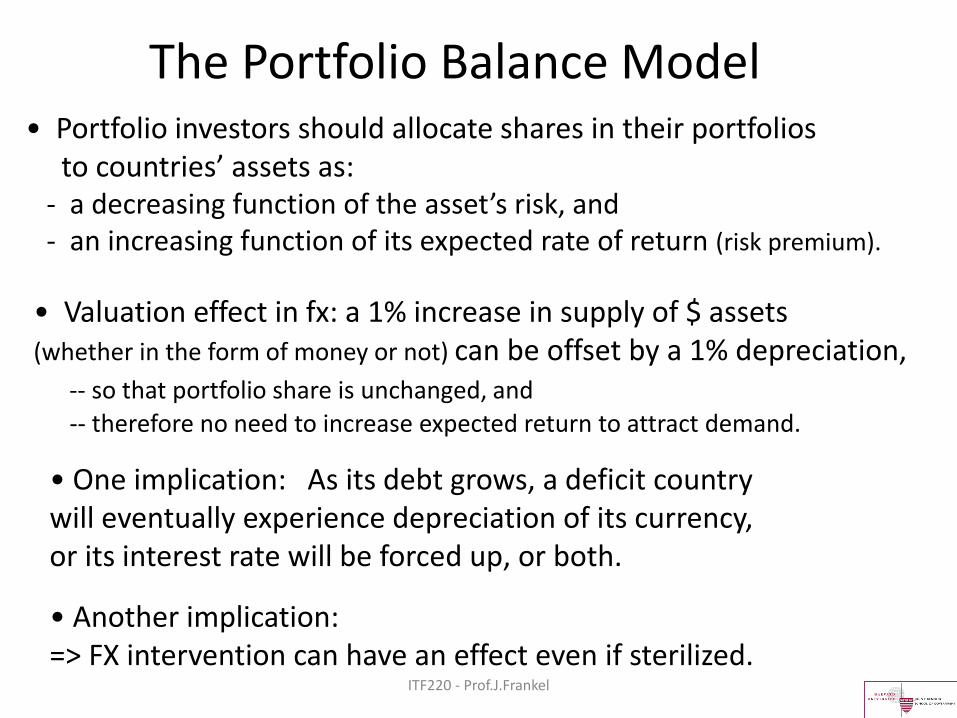

The Portfolio Balance Model • Portfolio investors should allocate shares in their portfolios to countries’ assets as: - a decreasing function of the asset’s risk, and - an increasing function of its expected rate of return (risk premium).

• Valuation effect in fx: a 1% increase in supply of $ assets (whether in the form of money or not) can be offset by a 1% depreciation, -- so that portfolio share is unchanged, and

-- therefore no need to increase expected return to attract demand.

• Another implication: => FX intervention can have an effect even if sterilized.

• One implication: As its debt grows, a deficit country will eventually experience depreciation of its currency, or its interest rate will be forced up, or both.

ITF220 - Prof.J.Frankel

APPENDIX: Intervention in the foreign exchange market

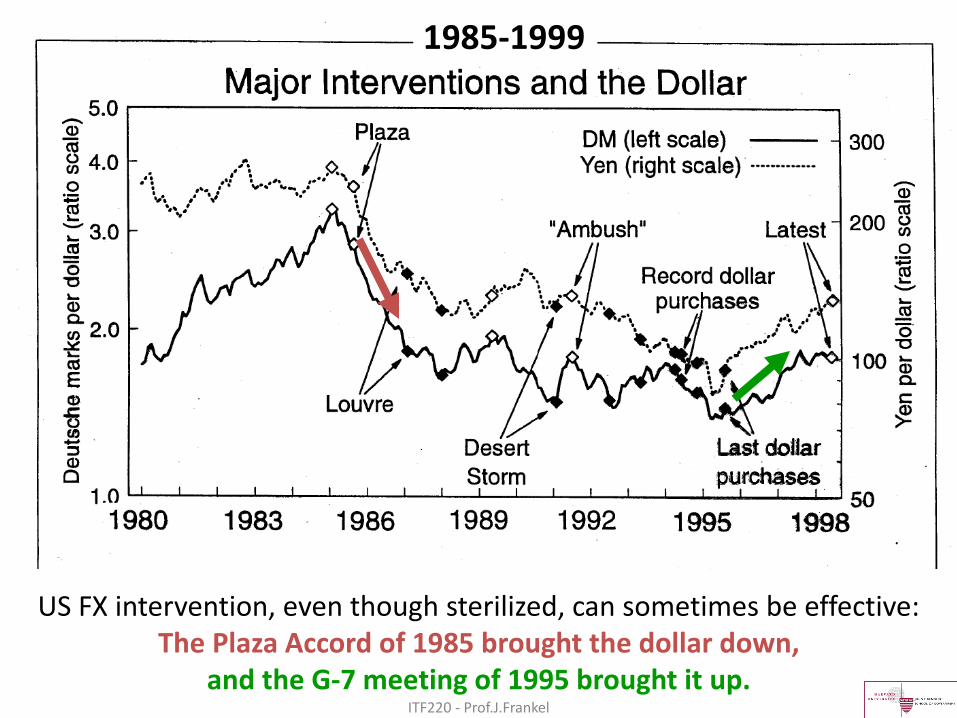

• was effective in 1985, to bring down the $, represented by the G-5 agreement at the Plaza Hotel;

• and was effective at times subsequently (though not always).

• Since 2001, the ECB, Fed, & BoJ have intervened very little;

• In 2013 the G-7 agreed not to intervene, – to avoid currency wars.

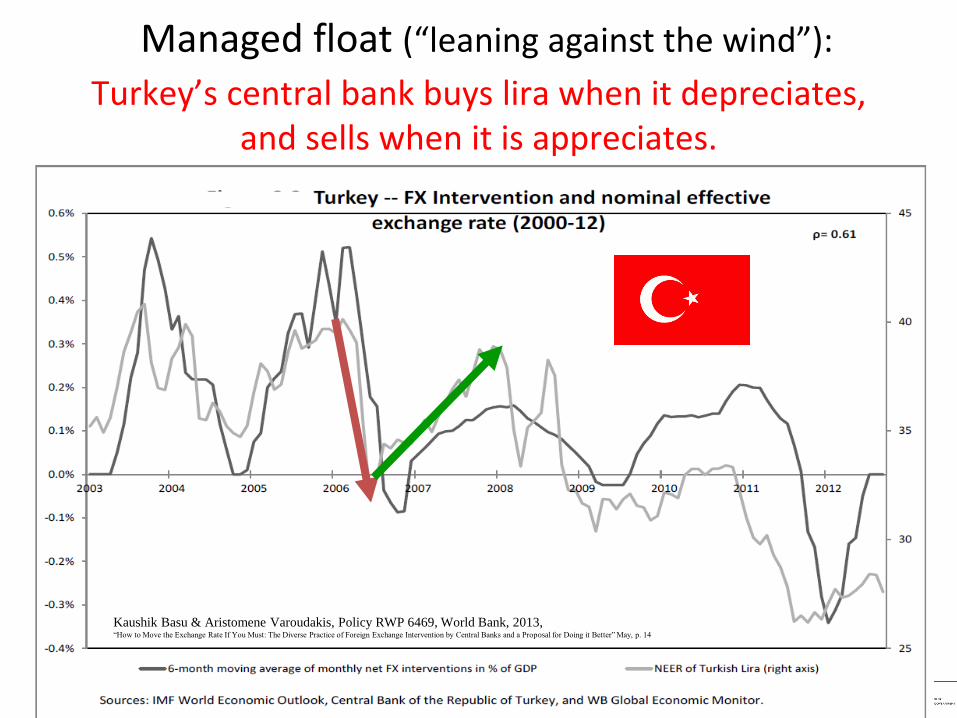

• But other floaters intervene more often, – Esp., major emerging market countries,

ITF220 - Prof.J.Frankel

US FX intervention, even though sterilized, can sometimes be effective: The Plaza Accord of 1985 brought the dollar down,

and the G-7 meeting of 1995 brought it up.

1985-1999

ITF220 - Prof.J.Frankel

Managed float (“leaning against the wind”):

Kaushik Basu & Aristomene Varoudakis, Policy RWP 6469, World Bank, 2013, “How to Move the Exchange Rate If You Must: The Diverse Practice of Foreign Exchange Intervention by Central Banks and a Proposal for Doing it Better” May, p. 14

Turkey’s central bank buys lira when it depreciates, and sells when it is appreciates.