lecture 10: capital structure by c. l. mattoli 1

TRANSCRIPT

Lecture 10: Capital Structure

By C. L. Mattoli

1

Intro Assets are, in a sense, independent of

capital structure, although capital structure will affect our future WACC and project decisions.

In this lecture, we assume that asset and liability decisions are independent.

The importance of debt is how it can be used to enhance shareholder value.

We shall examine elements of the capital structure decision (Chapter 13).

2

The Question Shareholder value is the individualized

value of the firm, so we shall talk of firm value, here.

Thus, our job becomes to choose the capital structure that will maximize firm value.

The value of anything is its discounted cash flow value, and, in the case of a company, CF’s are discounted at the WACC.

3

The Question

The WACC, in turn, contains, in its construction, capital structure, in the weights.

Moreover, value is inversely related to the discounting rate.

Therefore, we might, alternatively, pose the question: what is the capital structure that will minimize the WACC?

4

The Question

Then, we will say that one capital structure is preferable to another, if the resulting WACC is smaller.

We call the optimal capital structure the one that will absolutely minimize WACC.

This optimal capital structure is sometimes called the target capital structure of the firm.

5

Consequences of Financial Leverage Financial leverage refers to the use of debt

in the capital mix of the firm. Although, as students of finance, we know

that we should look at cash flows, for our purposes, we focus on earnings and book equity for a demonstration of the effects of financial leverage.

The bottom line is that debt has interest payments that must be paid: they are fixed costs.

6

Consequences of Financial Leverage More debt means more fixed costs. Thus, in a good year, there will be enough

to pay off the fixed costs and leftovers for the shareholders.

In a bad year, we might not make enough to pay debt service, and we could be in trouble.

Effectively, variation of income and ROE will increase with increasing debt.

7

Textbook Leverage Example Eagle Air Services currently has no debt but

is considering restructuring (changing capital structure).

In the restructure, it would issue debt and buy back some shares of common stock.

The company has 400,000 shares issued and outstanding, and the market value is $8 million ($20/share).

In the restructure, the company will issue $4 million of debt with 10% annual interest.

8

Textbook Leverage Example With the proceeds, it will buy back $4 million

= $20/share x 200,000 shares of stock. Then, in the new structure, it will have a

debt/equity ratio of 1, with 200,000 shares issued and out.

We assume, for now, that the share market price will remain at $20/share

The figures for current and proposed capital structure are shown in the next slide.

9

Textbook Leverage Example Figure 13.1: Capital Structure

Current ProposedAssets $8,000,000 $8,000,000 Debt $0 $4,000,000 Equity $8,000,000 $4,000,000 Debt/Equity Ratio 0 1 Share Price $20 $20 Shares Outstanding 400,000 200,000Interest rate 10% 10%

10

Textbook Leverage Example To study the affect of changed capital

structure, the CFO has prepared simple financials under 3 different macroeconomic scenarios: expected, recession, and expansion.

Under the 3 scenarios, EBIT will be $1 million in the neutral, expected case; $500,000 in the bad, recessionary scenario; and $1.5 million in the optimistic, expansionary scenario.

We summarize figure in the next slide.

11

Textbook Leverage Example Figure 13.2

Current Capital Structure: No Debt Recession Expected ExpansionEBIT $500,000 $1,000,000 $1,500,000 Interest 0 0 0Net Income $500,000 $1,000,000 $1,500,000 ROE 6.25% 12.50% 18.75%EPS $1.25 $2.50 $3.75

Proposed Capital Structure: Debt = $4 million Recession Expected ExpansionEBIT $500,000 $1,000,000 $1,500,000 Interest 400,000 400,000 400,000Net Income $100,000 $600,000 $1,100,000 ROE 2.50% 15.00% 27.50%EPS $0.50 $3.00 $5.50

12

Textbook Leverage Example As it is now, under the three scenarios, EPS

(B Tax) is $2.50, normal; $1.25 worst case; and $3.75 best case.

Also, in present structure, ROE is 12.5%, normal; ranging from 8.28% to 18.75%.

The whole idea behind leverage is enhancing shareholder income and returns: we borrow money at a rate that is less than our business returns, and we make extra money.

In the restructured case, we will have an extra expense of interest = $400,000/year.

13

Textbook Leverage Example Then, normal EPS = $3.00, an enhanced

number from the cheap debt. Normal ROE = 15%, again enhanced.

In the best case scenario, we also gain over the unlevered results with EPS = $5.50 and ROE = 27.5%.

However, in the bad economy scenario, EPS = $0.50 and ROE = 2.5%.

Thus, leverage is a double-edged sword. It can enhance when times are good, but it can devastate, even force bankruptcy, in bad times because fixed interest expense must be paid no matter what happens in the business.

14

Textbook Leverage Example As we have done in many situations, in this

course, we can perform a break-even (BE) analysis.

In terms of returns, of course, the objective is for return on assets to be above the cost of debt. Then, we will enhance ROE. The cost of debt (%) is the BE.

In the next slide, we show plots of EPS vs. EBIT from zero to expansion EBIT.

15

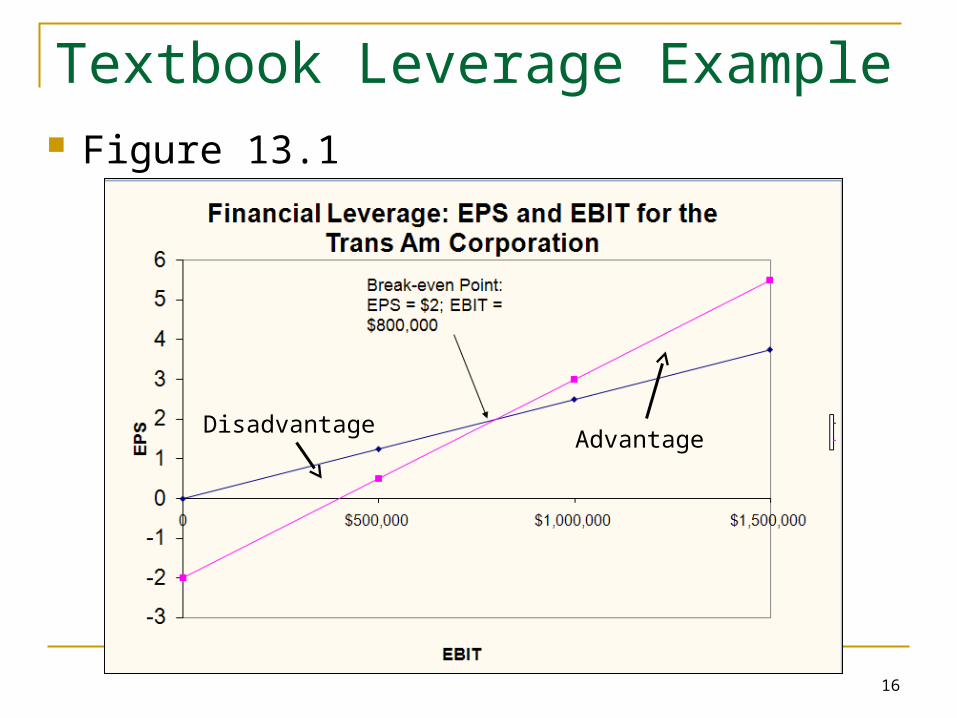

Textbook Leverage Example Figure 13.1

Disadvantage Advantage

16

Textbook Leverage Example The line starting at zero EBIT is EPS (BT)

for the unrestructured firm. The other line is the line with debt. The restructured line has a higher slope

than the other: it is levered up: that’s why we call it leverage.

In this BE analysis, we also consider the case that the firm has no EBIT, which will give it a loss for paying the interest on the debt.

17

Textbook Leverage Example

The lines cross, the lever point, at the BE point for the two capital structures.

The BE is where EPS is neutral to Capital Structure.

At that point ROE will equal the COC debt interest rate.

Below that point, i.e., ROE less than COCD, the levered firm impairs EPS.

18

Textbook Leverage Example Above the BE, the use of cheaper debt

allows the firm to make a marginal return on debt, add it to the ROE and enhance both ROE and EPS.

Thus, financial leverage is a double-edged sword: it can enhance firm value but it can also detract.

It can even result in legal issues, from default on legally-binding loan covenants, as we shall discuss, later.

19

Further Conclusions about Leverage Certainly, leverage has enhanced the

volatility of EPS and returns. Will shareholders, therefore, reassess

their risk in the firm? Surprisingly, they will not. The argument

is that shareholders can create their own leverage, called homemade leverage by splitting their money between shares and lending/borrowing, on their own.

20

Shareholder-Equivalent Restructuring The concept of replication is a major tool in

financial analysis. It has its basis in behavioral finance as the

concept of framing, which is how something is “looked at”.

As an example of the use of replication, we shall illustrate how the shareholder, through homemade leverage can replicate the levered firm, on her own.

21

Shareholder-Equivalent Restructuring Consider 2 alternatives: buy 100 shares in

the originally structured company for $2,000 or borrow $2,000 @ 10% and buy 200 shares in the company for $4,000.

In the next slide, which is from table 13.3, in the text, we show the payoffs of one year’s investment in the two alternatives, using the low, medium and high earnings scenarios that we used before.

22

Shareholder-Equivalent Restructuring Table 13.3

23

Proposed Capital Structure: Debt = $4 million

Recession Expected Expansion

EBIT $0.50 $3.00 $5.50Earnings 100 shares $50.00 $300.00 $550.00Net cost = $20x100 = $2,000

Current Capital Structure + Homemade Leverage

Recession Expected Expansion

EBIT $1.25 $2.50 $3.75 Earnings 100 shares $250.00 $500.00 $750.00

less interest on $2000 $200.00 $200.00 $200.00

Net eranings $50.00 $300.00 $550.00

Net cost = $20x200 = $4,000 - $2,000 borrowed = $2,000

Shareholder-Equivalent Restructuring As is demonstrated in the previous slide, the

payoffs are exactly the same for both positions.

The shareholder has leveraged her stock position by borrowing $2,000, the same amount as her original equity investment in the shares.

Thus, now, the shareholder’s debt equity ratio is 1:1, the same as the debt-equity ratio that the company would have chosen for itself in the restructuring.

24

Shareholder-Equivalent Restructuring In that regard, it does not matter whether

the company or the shareholder creates the leverage.

Shareholders can decided how much leverage they want in their company investments, the company does not have to.

In fact, the same technique can be used by a shareholder to unlever a company in their own portfolio.

25

Shareholder-Equivalent Restructuring Students can continue with this example, on

their own by staring with the levered company, buying only 50 shares, and investing the other $1,000 in money market at 10%.

The effect will be to get the same payoffs as those for the originally unlevered firm.

In the end, the price of the stock of a company, according to these arguments, should not be affected by company leverage.

26

Cap Structure & COC Equity Our preceding arguments about the stock

price and leverage are just a special case of the Miller-Modigliani (MM) Proposition I, which states that a firm’s capital structure is irrelevant.

MM Prop 1, the Pie Model, says if the asset side of two companies’ balance sheets are the same, then, it must equal the right hand side, the capital.

Then, capital structure is simply the way that the pie (pie chart) is sliced, but the size of the pie is the same.

27

Cap Structure & COC Equity

Even though, according to MM I, the cap structure has no affect on firm value, the capital changes, so we should look at the WACC.

We can write WACC = RA = (D/V)RD + (E/V)RE

We can rearrange this equation as RE = RA + (RA – RD)(D/E).

28

Cap Structure & COC Equity

This is MM Proposition II, which says that the COCE depends on: (1) ROA, (2) the cost of debt, and (3) the D/E.

That equation says RE is a straight line with slope (RA – RD) versus (D/E).

That says that RE increases as D/E increases: the risk of equity returns increases with increasing leverage, which increases the RRR.

29

Cap Structure & COC Equity

Some simple calculations will show that RA = (D/V)RD + (E/V)RE = (D/V)RD + (E/V)[RA + (RA – RD)(D/E)] = (E/V)RA + (D/V)RA =RA.

In other words, WACC is independent of capital structure (MM I, restated).

The mechanism is that the increased benefit of more and more lower cost debt is exactly offset by the increasing COCE from the addition of leverage.

30

Figure 13.3

31

The CAPM, the SML and Proposition II How does financial leverage affect

systematic risk? CAPM: RA = Rf + A(RM – Rf)

Where A is the firm’s asset beta and measures the systematic risk of the firm’s assets

Proposition II Replace RA with the CAPM and assume that the

debt is riskless (RD = Rf)

RE = Rf + A(1+D/E)(RM – Rf)

32

Case I – Example Data

Required return on assets = 16%, cost of debt = 10%, percent of debt = 45%

What is the cost of equity?

RE = .16 + (.16 - .10)(.45/.55) = .2091 = 20.91%

Suppose instead that the cost of equity is 25%, what is the debt-to-equity ratio? .25 = .16 + (.16 - .10)(D/E) D/E = (.25 - .16) / (.16 - .10) = 1.5

Based on this information, what is the percent of equity in the firm? E/V = 1 / 2.5 = 40%

33

Business & Financial Risk

There is another way to look at MM II. The firm has risk because of the business

it is in and how it operates it. That is the business risk of the firm, and

is represented by the first term in the MM II equation.

The business risk depends on the systematic risk of the firm’s assets.

34

Business & Financial Risk

The second term in the equation depends on cap structure and is dependent on the firm’s financial risk.

The financial risk of equity is increased by the addition of debt to the capital structure.

This financial risk term increases even though the business risk is constant, and it leads to increasing COCE.

35

The Affect of Taxes The preceding analysis was under the

idealization that there are no corporate taxes. Taxes have a real affect, in that debt service

payments, interest, are a tax deductible expense and get a tax shield.

This is an added benefit of debt financing. On the negative side of debt financing is the

absolute obligation to meet promises of debt service payments.

Not meeting them could result in bankruptcy.36

Case II – ExampleUnlevered Firm Levered Firm

EBIT 5000 5000

Interest 0 500

Taxable Income

5000 4500

Taxes (30%) 1500 1350

Net Income 3500 3150

CFFA 3500 3650

37

Interest Tax Shield Example Annual interest tax shield

Tax rate times interest payment 6250 in 8% debt = 500 in interest expense Annual tax shield = .30(500) = 150

PV of annual interest tax shield Assume perpetual debt for simplicity PV = 150 / .08 = 1875 (same risk as debt) PV = D(RD)(TC)/RD = DTC = 6250(.30) =

1875

38

MM I with Taxes We can summarize the results as follows: The value of the firm increases by the PV

of the interest tax shield. Value of a levered firm = value of an

unlevered firm + PV of interest tax shield Value of equity = Value of the firm – Value

of debt. For perpetual debt service cash flows: VU

= EBIT(1-T)/RU; VL = VU + DTC

39

Textbook Figure 13.4

40

MM II with taxes

The WACC also decreases as D/E increases due to the effective government subsidy on interest payments

We have RA = (E/V)RE + (D/V)(RD)(1-TC)

So, RE = RU + (RU – RD)(D/E)(1-TC)

41

MM II with taxes Example

Consider a firm with D/E = 0.865 Then, from the equations: RE = .12 +

(.12-.09)(0.865)(1-.35) = 13.69%; And RA = (86.67/161.67)(.1369) +

(75/161.67)(.09)(1-.35) = 10.05%.

42

MM II with taxes Example

Suppose it changes it D/E to 1. Then, RE = .12 + (.12 - .09)(1)(1-.35)

= 13.95% And the weighted average cost of

capital is RA = .5(.1395) + .5(.09)(1-.35) = 9.9%.

We summarize graphically, in the next slide.

43

Graphical MM II + T

44

Default on Debt

The unrealistic conclusion of MM with taxes is that we should lever the firm to almost 100% debt.

However, realistically, the more debt we have, the more obligated we are to make payments.

Then, the risk that we cannot meet these fixed obligations increases.

45

Default on Debt

When a debtor defaults on payments, the lenders can take him to court and lay claim to assets.

In addition, a firm becomes bankrupt, in principle, when A = L, so E = 0, and transfer of control goes from owners to creditors.

Bankruptcy has its costs.

46

Costs of Bankruptcy

Bankruptcy can result from default on debt obligations: it is a legal process.

In addition, someone is appointed to oversee the liquidation of the firm.

The formal legal and administrative costs are real and subtract from what debtors will actually get after the liquidation of all assets and liabilities.

47

Costs of Bankruptcy The precursor to bankruptcy is financial

distress when the company is having difficulty meeting its debt obligations but has not yet tipped into default.

At that point the company will spend time and energy in avoiding bankruptcy.

Moreover, as the firm fights for its life, customers might beg off, good employees might quit, and potentially lucrative projects might be shelved.

These indirect costs of bankruptcy are called financial distress costs.

48

Optimal Capital Structure.

Thus, the ever-increasing benefit of leverage a la MM + T is moderated by the ever-increasing probability of distress, default and bankruptcy.

The result is that instead of the increasing line, in figure 13.4, it will be humped with a peak at the optimal capital structure, thereafter decreasing with increasing leverage.

We show this combined picture in the next slide.

49

Figure 13.5

= Value of firm with debt

50

Op Cap Structure & COC The theory that we are discussing is called

the static theory because only D/E is changed, not assets or operations.

Hand in hand with the upside down cup shape for cap structure will be an upright cup shape for WACC.

The minimum of the WACC curve will correspond to the max of cap structure.

We show the situation in the next slide.

51

Figure 13.6

52

Further Recommendations

Although the static theory of cap structure cannot produce a definite optimal cap structure, it can give us some guidance.

Firms with accumulated losses will get little benefit from the interest tax shield, especially since their benefits will come later, after the losses carry forward and are finally offset by gains (loss of PV of tax benefits).

53

Further Recommendations Also, firms with other large tax shield from,

e.g., depreciation and amortization, will benefit less from debt.

If firms can fully utilize franking and their shareholders can use it, equity will gain in relative benefit for the company.

Concerning distress and the way out, firms with hard assets that can be sold will better be able to dig their way out of distress by borrowing more than firm’s whose assets are mostly intangible.

54

Observed capital structure First off, in Australia, firms tend to have low D/E

ratios. There is variation along broad industry lines. Energy companies tend to have no debt, where

as food, staples and retail tend to have high debt levels.

First, debt markets only began ion Australia in the 1980’s, but the major reason that people assume the low debt level is the dividend imputation system.

We show some examples in the next slide.

55

From table 13.5 (D/E)

56

Bankruptcy: the Process Distress can be characterized in a number of

ways:1. Business failure, meaning business terminated

with a loss to creditors.2. Legal bankruptcy involves a petition to federal

court to appoint a liquidator and either over see complete liquidation or reorganization of assets/liabilities.

3. Technical insolvency means the firm cannot meet its financial obligations, i.e., can’t pay its bills on a going basis.

4. Accounting insolvency occurs when L > A (W=0).

57

Liquidation & Reorganization The steps for bankruptcy liquidation are:

1. Petition filed voluntarily by company or involuntary petition by creditors.

2. Administrator is appointed to assume control of assets and oversee liquidation.

3. After liquidation and payment of administrative costs, proceeds are distributed to creditors.

4. Any leftovers go to the owners.

58

Order of liquidation payments The order of payments are set out in

Australian Government Corporation Law §556

1. Bankruptcy admin expenses.

2. Other expenses arising from filing before appointment of admin.

3. Wages, salaries and superannuation owed before entering liquidation.

4. Injury compensation owed before.

59

Order of liquidation payments5. Due employees on leave.6. Retrenchment payments due employees.7. Payment to unsecured creditors.8. Payment to pfd shareholders9. Payment to common shareholders. This is according to the absolute priority rule

(APR). Secured creditors are outside the process

and lay separate claim to assets, unless their assets were insufficient to cover obligations.

60

Fin Management & Bankruptcy The reason that a firm might file voluntary

bankruptcy is that when the filing is made, there is a stay on all payments to creditors.

In that manner, the company gives itself breathing room to plan a reorganization or to begin to negotiate with creditors who are then at a slight disadvantage and cannot themselves file the petition and be in control of the situation.

Commonly called filing for protection under bankruptcy.

61

Agreements to avoid bankruptcy. Instead of letting things go too far once a

default event has occurred, it is better for all parties to sit down and negotiate a way to avoid bankruptcy and liquidation.

Then, debt might be rescheduled, and the firm’s capital might be reorganized voluntarily with the help of creditors and company.

Terms that apply here, are extension, postponing payment, or composition, allowing for a reduced payment.

62

Homework

Learning activity ● Attempt all of the critical thinking and

concepts review section ● Attempt questions and problems 1, 2, 4, 5,

6, 8, 10, 11, 12, 13

See pages 80-82 of Study Guide for an example of trying to find optimal capital structure.

63

END

64