ldsf ;lk; dfssdfsdf ldfljd kljkdfjsdfsdfsdf

TRANSCRIPT

DE–5293

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

BUSINESS COMMUNICATION

(1999 onwards)

Time : Three hours Maximum : 100 marks

Answer should not exceed more than 200 words.

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions.

All questions carry equal marks.

1. List out the various objectives of communication.

2. Briefly explain the various components of a business letter.

3. Briefly explain the letters of enquiry.

4. List out the various contents of an order letter.

5. Explain the various source of information.

6. Write to your bankers, requesting them to open an irrevocable letter of credit in favour in your foreign supplier.

7. Write a note on the various types of secretarial correspondence.

8. Describe the importance of reports.

11

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

All questions carry equal marks.

9. List out the various barriers to communication? How will you overcome them?

10. Define quotation. Explain the various terms used in quotations.

11. Draft an application for the post of an accountant in an export organisation.

12. What are the various kinds of meeting? Discuss the duties of the secretary in such meetings.

13. Enumerate the various parts of a report along with the contents in a detailed manner.

14. What are the various components of a speech? Explain each one of them briefly.

15. Draft a suitable reply to the manager of a firm who expressed a desire to open a current account with your bank.

––––––––––––––––

2

DE–5294

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

BASIC FINANCIAL ACCOUNTING

(1999 onwards)

Time : Three hours Maximum : 100 marks

SECTION A — (5 × 8 = 40 marks)

Answer any FIVE questions.

1. Ramesh keeps his books on single entry basis. Prepare a statement of affairs as on 31.10.2002 and a statement of profit (or) loss for the period ending 31.10.2002.

1.11.2001 1.10.2002

Rs. Rs.

Bank Balance 560 (Cr) 350 (Dr)

Cash on hand 10 50

Debtors 4,500 3,600

Stock 2,700 2,900

Plant 4,000 4,000

Furniture 1,000 1,000

Ramesh had withdrawn Rs. 1,000 during the year and had introduced fresh capital of Rs. 4,200 on 1.7.2002. A provision of 5% on debtors is necessary. Write off Depreciation on plant at 10% and furniture at 15%. Interest on capital is to be allowed at 5%.

3

12

2. A plant is purchased for Rs. 20,000. It is depreciated at 5% p.a. on reducing balance for five years when it becomes obsolete due to new method of production and is scrapped. The scrap produces Rs. 5,385. Show the plant account in the ledger.

3. What are the differences between Income and Expenditure account and a Receipts and Payments account?

4. Explain on the three important ledgers prepared under the self-balancing system.

5. Distinguish consignment from Sale. What are the differences between the consignment and joint venture?

6. Distinguish between Double Entry & Single Entry System.

7. Distinguish between :

(a) Balance Sheet & Trial Balance

(b) Balance Sheet & Profit & Loss A/c.

8. Deva owes Rs. 1,000 to Krishnan. On 1st May 2002, he sent his promissory notes for the amount payable after

3 months. On 1st June 2002 Krishnan endorsed the promissory note in favour of Ravi to whom he owed a like amount. On the due date, Deva paid the amount. Give journal entries in the books of Krishnan, Deva and Ravi.

SECTION B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. A & Co. of Calcutta sent goods on consignment to B & Co. of Bombay at an invoice price of Rs. 29,675 and paid freight Rs. 762, cartage Rs. 231 and insurance Rs.700. Half the goods were sold by the agents for Rs. 17,500 subject to

4

an agent’s commission of Rs. 875, storage expenses of Rs. 200 and other selling expenses of Rs. 350. One fourth of the consignment was lost by fire and a claim of Rs. 5,000 was recovered. Draw up the necessary accounts in the books of A & Co., and ascertain the profit or loss assuming stock to be one-fourth of the consignment. The agent reported that rest of the goods were also damaged and would need Rs. 700 for repairs.

10. Bachan and Charan enter into a Joint Venture to prepare a film for the Government. The Government agrees to pay Rs. 1,00,000. Bachan contributes Rs. 10,000 and Charan contributes Rs. 15,000. These amounts are paid into a Joint Bank. Payments made out of the Joint account were :

Rs.

Purchase of equipment 6,000

Hire of equipment 5,000

Wages 45,000

Materials 10,000

Office expenses 5,000

Bachan paid Rs. 2,000 as licensing fees. On completion, the film was found defective and Government made a deduction of Rs. 10,000. The equipment was taken over by Charan 3/5. Give ledger accounts.

11. What are the types of Accounts? Explain its principles. What are the objectives of Accounting?

12. From the following particulars extracted from the books of a trader kept under the Single Entry System, you are required to find out the figures for credit sales and credit purchases by showing the Total Debtors Account and Total Creditors Account.

Rs.

Balance, 1st January, 1988 :

Total debtors 57,200

5

Rs.

Bills receivable 4,000

Total creditors 26,400

Bills payable 2,500

Cash paid to creditors 70,250

Discount allowed by suppliers 2,650

Cash received from customers 1,35,400

Discount allowed to customers 4,200

Returns from customers 1,625

Returns to suppliers 1,330

Bad debts written off 3,540

Cash received against bills receivable 14,200

Payments made against bills payable 7,000

Bills receivable dishonoured 1,100

Bad debts previously written off now recovered

1,000

Cash sales during the year 15,800

Cash purchases during the year 12,300

Total debtors on 31.12.88 55,600

Total creditors on 31.12.88 28,400

Bills receivable on 31.12.88 1,000

Bills payable on 31.12.88 3,000

13. From the following Receipts & Payments account of the Priya Club for the year ended 31st March 1998, prepare Income & Expenditure account :

Receipts & Payments A/C for the year ended 31.03.1998.

6

Receipts Rs. Payments Rs.

To Balance (1.4.97) 3,485 By Books 6,150

To Entrance Fee 650 By Printing & Stationery 465

To Donations 6,000 By Newspapers 1,110

To Subscriptions 6,865 By Sports Materials 5,000

To Interest on Investment

1,900 By Repairs 650

To Sale of furniture 685 By Investments 2,000

To Sale of old news papers

465 By Furniture 1,000

To Proceeds from entertainment

865 By Salary 1,500

To Sundry Receipts 125 By Balance on 31.3.98 3,165

21,040 21,040

The entrance fees and donations are to be capitalized; Sports materials are valued at Rs. 4,000 as on 31.3.1998.

14. From the following particulars prepare debtors ledger adjustment a/c and purchase ledger adjustment a/c in the general ledger for the year ended 31.12.1999.

Particulars Rs.

Purchase ledger (Cr) 2,00,000

Purchase ledger (Dr) 22,700

Sales ledger (Cr) 2,400

Sales ledger (Dr) 4,21,000

Credit Purchase 20,00,000

Cash Purchase 2,00,000

Credit Sales 18,00,000

Cash Sales 7,00,000

Closing balances :

7

Purchase ledger (Dr) 17,000

Sales ledger (Cr) 9,000

Purchase Returns 1,00,000

Sales Returns 80,000

B/R received 3,00,000

Particulars Rs.

B/P accepted 2,00,000

Bad debts written off 10,000

Provision for bad debts 10,000

B/R dishonored 40,000

Cash received from debtors 12,00,000

Cash paid to creditors 16,00,000

15. From the following Trial Balance of Sri. Narayanan, you are required to prepare a Trading and Profit & Loss a/c for the year ended 31st December 1997 and a Balance Sheet as on that date.

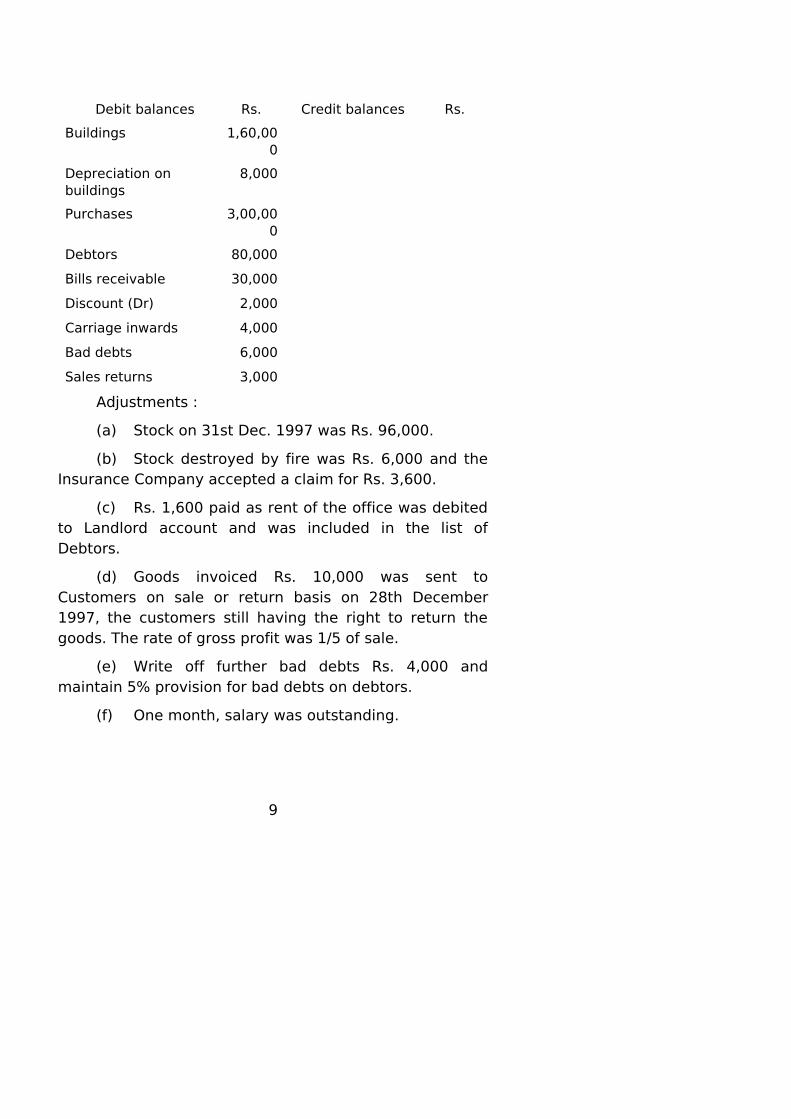

Debit balances Rs. Credit balances Rs.

Stock on 1st Jan, 1997 70,000 Capital 2,00,000

Plant & Machinery 50,000 Wages outstanding 4,000

Rent 3,000 Sales 5,00,000

Depreciation on Plant & Creditors 45,000

Machinery 5,000 Bills Payable 16,000

Drawings 40,000 Discount (Cr) 12,000

Wages 20,000 Bank overdraft 9,000

Income tax 2,000 Commission (Cr) 8,000

Salary for 11 months 11,000 Purchase returns 5,000

Cash 5,000

8

Debit balances Rs. Credit balances Rs.

Buildings 1,60,000

Depreciation on buildings

8,000

Purchases 3,00,000

Debtors 80,000

Bills receivable 30,000

Discount (Dr) 2,000

Carriage inwards 4,000

Bad debts 6,000

Sales returns 3,000

Adjustments :

(a) Stock on 31st Dec. 1997 was Rs. 96,000.

(b) Stock destroyed by fire was Rs. 6,000 and the Insurance Company accepted a claim for Rs. 3,600.

(c) Rs. 1,600 paid as rent of the office was debited to Landlord account and was included in the list of Debtors.

(d) Goods invoiced Rs. 10,000 was sent to Customers on sale or return basis on 28th December 1997, the customers still having the right to return the goods. The rate of gross profit was 1/5 of sale.

(e) Write off further bad debts Rs. 4,000 and maintain 5% provision for bad debts on debtors.

(f) One month, salary was outstanding.

9

———————

10

DE 5295

B.C.S. DEGREE EXAMINATION, MAY 2009.

PRINCIPLES OF MANAGEMENT

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions in about 200 words each.

All questions carry equal marks.

1. Define the term Management. Bring out it’s importance.

2. Explain the different types of decisions.

3. Discuss the various principles of delegation.

4. What are the forms of verbal communication?

5. What are the steps in control process?

6. Write a note on:

(a) Authority

(b) Responsibility

(c) Accountability.

7. Explain Management By Objectives.(MBO)

11

13

8. What do you mean by line organisation? State it’s merits and demerits.

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions in about 400 words each.

All questions carry equal marks.

9. Define the term management. Discuss briefly the various functions of management.

10. What is planning? What are the steps in planning process?

11. State the barriers to communication and how they should be overcome?

12. What is span of control? What factors determine the span of supervision?

13. Enumerate the principles of a good organisation.

14. Discuss briefly the different control techniques.

15. Define motivation. Write a note on monetary and non-monetary incentives provided to motivate the employees of an organisation.

–––––––––––––

12

DE–5296

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

COMPANY LAW

(1999 Onwards)

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions in about 200 words each.

All questions carry equal marks.

1. Define a Company. Explain its features.

2. Who are liable for mis-statement in a prospectus?

Discuss their civil and criminal liabilities.

3. Explain the legal provisions relating to the Extra-

ordinary General Meeting.

4. State the procedure for reduction of share capital of

a company.

5. What are the legal requirements which a company

must comply with while borrowing?

6. Who is a promoter of a company? Discuss his legal

position in relation to the company he promotes.

7. When does a person cease to be a director of a

company?

13

14

8. Explain the various types of debentures.

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions in about 400 words each.

All questions carry equal marks.

9. Explain the concept of ‘‘Corporate veil’’ and state

the circumstances when it can be lifted.

10. What is meant by register of members? State the

provisions regarding acquisition and cessation of

membership.

11. How a company is incorporated? What documents

are required to be filed with the Registrar of companies

for this purpose?

12. Explain special resolution and ordinary resolution of

a company registered under the Companies Act.

13. Explain the provisions on company deposits.

14. What is ‘Articles of Association’? What are its

contents? How can articles of association be altered?

15. How a Managing Director of a company is

appointed? What are the disqualifications of a Managing

Director?

———————

14

DE-5297

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

SECRETARIAL PRACTICE

(1999 onwards)

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions in about 200 words.

All questions carry equal marks.

1. Name some of the principal types of secretaries and briefly explain their functions.

2. What are all the legal provision and procedures to be followed for the appointment of company secretary? Draft the resolution for the purpose.

3. Explain the legal position of a company secretary.

4. What are the conditions under which a company is empowered to issue shares?

5. Explain requisites of a valid company meeting.

6. What are the legal provisions relating to Board of Directors Meeting? Explain the role of Secretary in holding the same.

7. What do you mean by notice of meeting? Explain.

8. Explain voluntary winding up of a company.

PART B — (4 × 15 = 60 marks)

15

21

Answer any FOUR questions in about 400 words each.

All questions carry equal marks.

9. What is an agenda? Why it is necessary? What are all the things that have to be considered while preparing agenda?

10. Discuss the voting right of members in a public company limited by shares with reference to both equity and preference shares capital.

11. What is meeting? Explain difference kinds of meetings of a company.

12. What is motion? Differentiate motion from resolution.

13. Draft a specimen of ordinary resolution and special resolution. Give an account of transactions requiring special resolution.

14. Explain the procedure relating to charges and consequences of non registration of charges.

15. Who is a Director? How he is appointed? What are his Qualifications? When he can be removed?

———————

16

DE–5298

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

COMMERCIAL LAW

(1999 onwards)

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions in about 200 words.

All questions carry equal marks.

1. What are the essentials of a valid contract?

2. "Stranger to a consideration cannot sue". Are there any exceptions to this rule?

3. Differentiate fraud from misrepresentation.

4. In what cases the consideration and object of an agreement are said to be unlawful?

5. State the persons by whom the contract should be performed.

6. Distinguish between a contract of guarantee and a contract of indemnity.

7. Define Pledge. State the essentials of a valid plede.

8. What are the rights of unpaid seller?

PART B — (4 × 15 = 60 marks)

17

22

Answer any FOUR questions in about 400 words each.

9. Define acceptance and state the legal rules governing valid acceptance.

10. Discuss the law regarding minor's agreements.

11. Explain when a consent is not said to be free. What is the effect of such consent on the formation of the contract?

12. Define contingent contract. Discuss the rules relating to contingent contracts.

13. Explain the circumstances under which a surety is discharged.

14. Explain the doctrine of Caveat Emptor with its exceptions.

15. Describe the various modes by which an agency may be terminated.

—————

18

DE–5299

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

BUSINESS STATISTICS

(1999 onwards)

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions.

1. Explain the different stages in a statistical investigation.

2. What are the important sources of ‘‘Collection of data’’?

3. Briefly explain the classification of data.

4. What are the properties of good average?

5. The following are the figures of profits earned by 1,400 companies during 1999-2000.

Profits (in lakhs)

No. of companies

200–400 500

400–600 300

600–800 280

800–1,000 120

1,000–1,200 100

1,200–1,400 80

1,400–1,600 20

19

23

Calculate the average profits by short-cut methods.

6. Find the median

Wages (Rs.) : 60–70

50–60

40–50

30–40

20–30

No. of labourers :

5 10 20 5 3

7. The following are the group index numbers and the group weights of an average working class family’s budget. Construct the cost of living index number :

Group Food Fuel & Lighting Clothing Rent Miscellaneous

Index number 352 220 230 160 190

Weight 48 10 8 12 15

8. Compute quartile deviation from the following data.

Height in inches :

58

59

60

61

62

63

64

65

66

No. of students :

15

20

32

35

33

22

20

10

8

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

All questions carry equal marks.

9. Explain briefly the types of non-random sampling methods.

10. Explain the methods of constructing index numbers.

11. Distinguish between primary data and secondary data. What are the precautions necessary before using secondary data?

20

12. From the following data compute standard deviation :Class Interval :

0–100 100–200

200–300

300–400

400–500

Above 500

Frequency : 17 13 29 11 50 120

13. Calculate mean, median and mode for the following data pertaining to marks in statistics out of 140 marks for 80 students in a class :

Marks more than :

0 20

40

60

80

100

120

No. of students : 80

76

50

28

18

9 3

14. The following data relate to the age of 10 employees and the number of days on which they reported sick in a month :

Age : 20

30

32

35

40

46

52

55

58

62

Sick days :

1 2 0 3 4 6 5 7 8 9

Calculate Karl Pearson’s coefficient of correlation and interpret its value.

15. In the following table are recorded data showing the test scores made by salesmen on an intelligence test and their weekly sales :Salesmen : 1 2 3 4 5 6 7 8 9 10

Test score : 40 70 50 60 80 50 90 40 60 60

Sales (’000 Rs.) :

2.5 6.0 4.0 5.0 4.0 2.5 5.5 3.0 4.5 3.0

Calculate the regression equation of sales on test scores and estimate the probable weekly sales volume if a salesman makes a score of 100.

21

––––––––––––––––

22

DE–5300

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

ADVANCED ACCOUNTANCY

(1999 onwards)

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions.

All questions carry equal marks.

1. State the salient points of Garner Vs Murray case in the case of Dissolution of Partnership.

2. What are the different methods of redeeming

Debentures?

3. What is profit prior to incorporation? How will you

calculate it?

4. Write short notes on :

(a) Average Clause

(b) Standard turnover

(c) Indemnity period.

5. P, Q and R are in partnership. P died on 31.3.1998. The partnership deed provide the following :

23

24

(a) The capital to his credit shall be calculated after adjusting drawing till the date of death.

(b) That his share of profit till the date of death calculated on the basis of the average of the three preceding years.

(c) That the goodwill of the firm shall be taken at one year’s purchase of the average profits of the preceeding 5 years.

(d) Interest on capital should be provided @ 5 percent.

The capital to his credit was Rs. 60,000 on 31.12.97 and there is no drawing afterwards.

Prepare P’s Executors Account.

6. (a) The Directors of a company forfeited 100 equity shares of Rs. 10 each on which Rs. 400 had been paid. The shares were reissued to one of the Directors up on the payment of Rs. 900. Give Journal entries.

(b) The Directors of a Company forfeited 100 equity shares of Rs. 10 each for non payment of the first call of Rs. 2 and final call of Rs. 2. The shares were reissued for Rs. 8 per share as fully paid shares. Give the necessary journal entries.

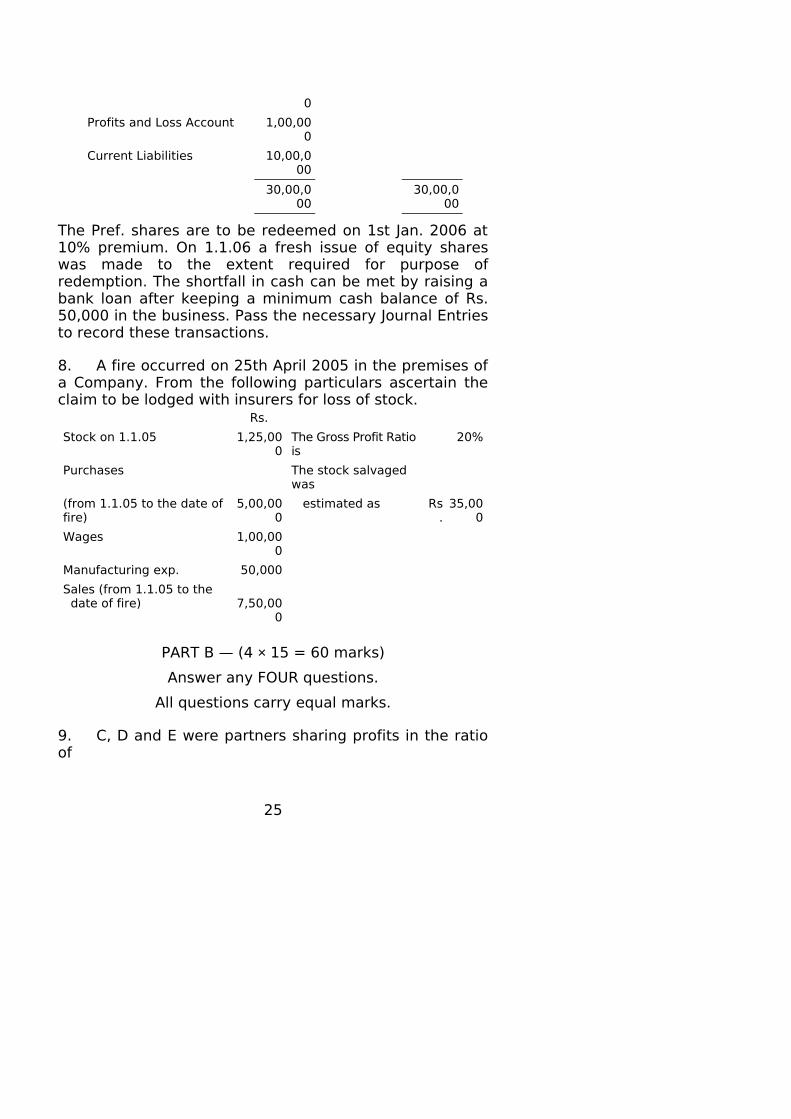

7. The following is the Balance sheet of A.P. Ltd. as on 31.12.05 :

Liabilities Rs. Assets Rs.

Share capital Fixed Assets

24,00,000

12% Redeemable Pref. shares

Stock 5,00,000

(5000 × 100) 5,00,000

Debtors 50,000

Equity shares (10000 × 100)

10,00,000

Cash 50,000

Share premium 2,00,000

General Reserve 2,00,00

24

0

Profits and Loss Account 1,00,000

Current Liabilities 10,00,000

30,00,000

30,00,000

The Pref. shares are to be redeemed on 1st Jan. 2006 at 10% premium. On 1.1.06 a fresh issue of equity shares was made to the extent required for purpose of redemption. The shortfall in cash can be met by raising a bank loan after keeping a minimum cash balance of Rs. 50,000 in the business. Pass the necessary Journal Entries to record these transactions.

8. A fire occurred on 25th April 2005 in the premises of a Company. From the following particulars ascertain the claim to be lodged with insurers for loss of stock.

Rs.

Stock on 1.1.05 1,25,000

The Gross Profit Ratio is

20%

Purchases The stock salvaged was

(from 1.1.05 to the date of fire)

5,00,000

estimated as Rs.

35,000

Wages 1,00,000

Manufacturing exp. 50,000

Sales (from 1.1.05 to the date of fire) 7,50,00

0

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

All questions carry equal marks.

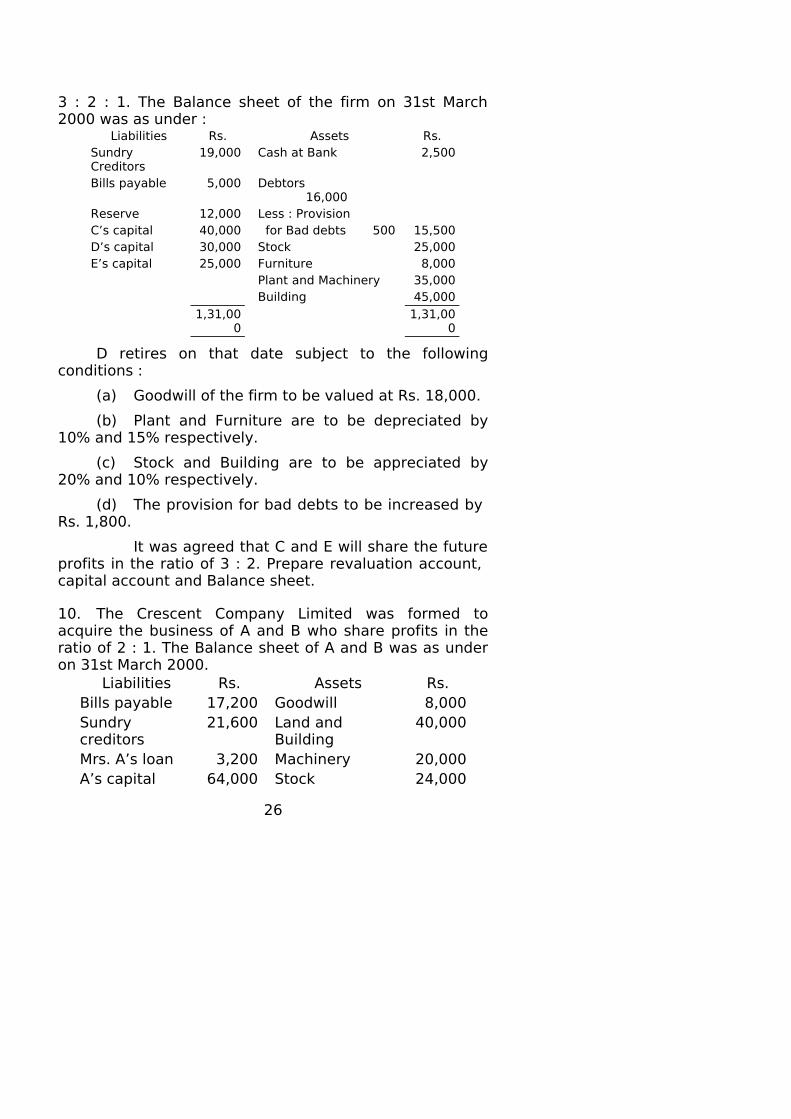

9. C, D and E were partners sharing profits in the ratio of

25

3 : 2 : 1. The Balance sheet of the firm on 31st March 2000 was as under :

Liabilities Rs. Assets Rs.Sundry Creditors

19,000 Cash at Bank 2,500

Bills payable 5,000 Debtors 16,000

Reserve 12,000 Less : Provision C’s capital 40,000 for Bad debts 500 15,500D’s capital 30,000 Stock 25,000E’s capital 25,000 Furniture 8,000

Plant and Machinery 35,000Building 45,000

1,31,000

1,31,000

D retires on that date subject to the following conditions :

(a) Goodwill of the firm to be valued at Rs. 18,000.

(b) Plant and Furniture are to be depreciated by 10% and 15% respectively.

(c) Stock and Building are to be appreciated by 20% and 10% respectively.

(d) The provision for bad debts to be increased by Rs. 1,800.

It was agreed that C and E will share the future profits in the ratio of 3 : 2. Prepare revaluation account, capital account and Balance sheet.

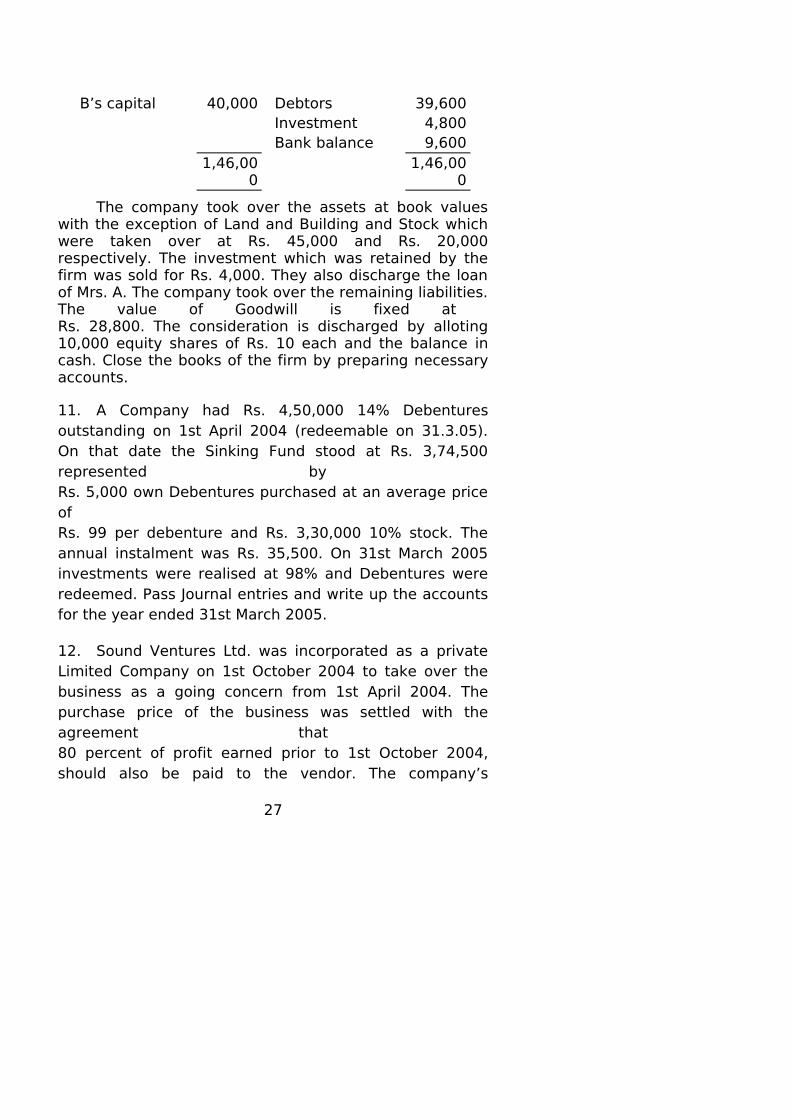

10. The Crescent Company Limited was formed to acquire the business of A and B who share profits in the ratio of 2 : 1. The Balance sheet of A and B was as under on 31st March 2000.

Liabilities Rs. Assets Rs.Bills payable 17,200 Goodwill 8,000Sundry creditors

21,600 Land and Building

40,000

Mrs. A’s loan 3,200 Machinery 20,000A’s capital 64,000 Stock 24,000

26

B’s capital 40,000 Debtors 39,600Investment 4,800Bank balance 9,600

1,46,000

1,46,000

The company took over the assets at book values with the exception of Land and Building and Stock which were taken over at Rs. 45,000 and Rs. 20,000 respectively. The investment which was retained by the firm was sold for Rs. 4,000. They also discharge the loan of Mrs. A. The company took over the remaining liabilities. The value of Goodwill is fixed at Rs. 28,800. The consideration is discharged by alloting 10,000 equity shares of Rs. 10 each and the balance in cash. Close the books of the firm by preparing necessary accounts.

11. A Company had Rs. 4,50,000 14% Debentures outstanding on 1st April 2004 (redeemable on 31.3.05). On that date the Sinking Fund stood at Rs. 3,74,500 represented by Rs. 5,000 own Debentures purchased at an average price of Rs. 99 per debenture and Rs. 3,30,000 10% stock. The annual instalment was Rs. 35,500. On 31st March 2005 investments were realised at 98% and Debentures were redeemed. Pass Journal entries and write up the accounts for the year ended 31st March 2005.

12. Sound Ventures Ltd. was incorporated as a private Limited Company on 1st October 2004 to take over the business as a going concern from 1st April 2004. The purchase price of the business was settled with the agreement that 80 percent of profit earned prior to 1st October 2004, should also be paid to the vendor. The company’s

27

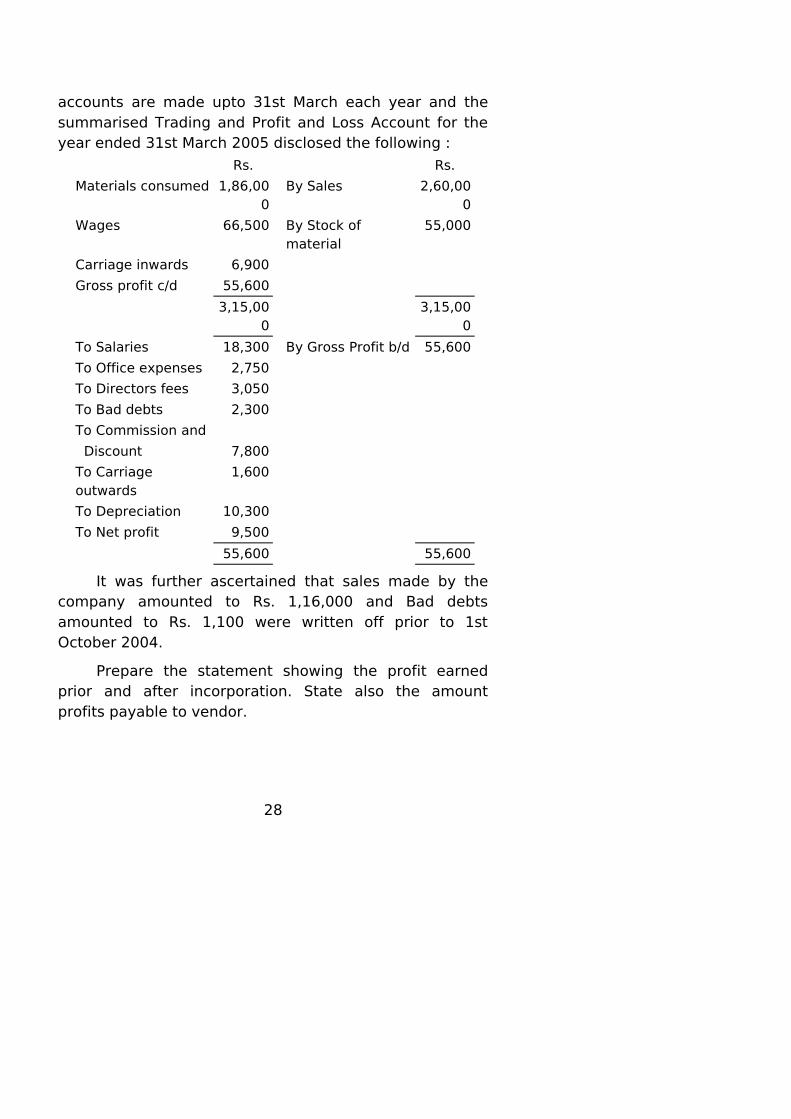

accounts are made upto 31st March each year and the summarised Trading and Profit and Loss Account for the year ended 31st March 2005 disclosed the following :

Rs. Rs.

Materials consumed 1,86,000

By Sales 2,60,000

Wages 66,500 By Stock of material

55,000

Carriage inwards 6,900

Gross profit c/d 55,600

3,15,000

3,15,000

To Salaries 18,300 By Gross Profit b/d 55,600

To Office expenses 2,750

To Directors fees 3,050

To Bad debts 2,300

To Commission and

Discount 7,800

To Carriage outwards

1,600

To Depreciation 10,300

To Net profit 9,500

55,600 55,600

It was further ascertained that sales made by the company amounted to Rs. 1,16,000 and Bad debts amounted to Rs. 1,100 were written off prior to 1st October 2004.

Prepare the statement showing the profit earned prior and after incorporation. State also the amount profits payable to vendor.

28

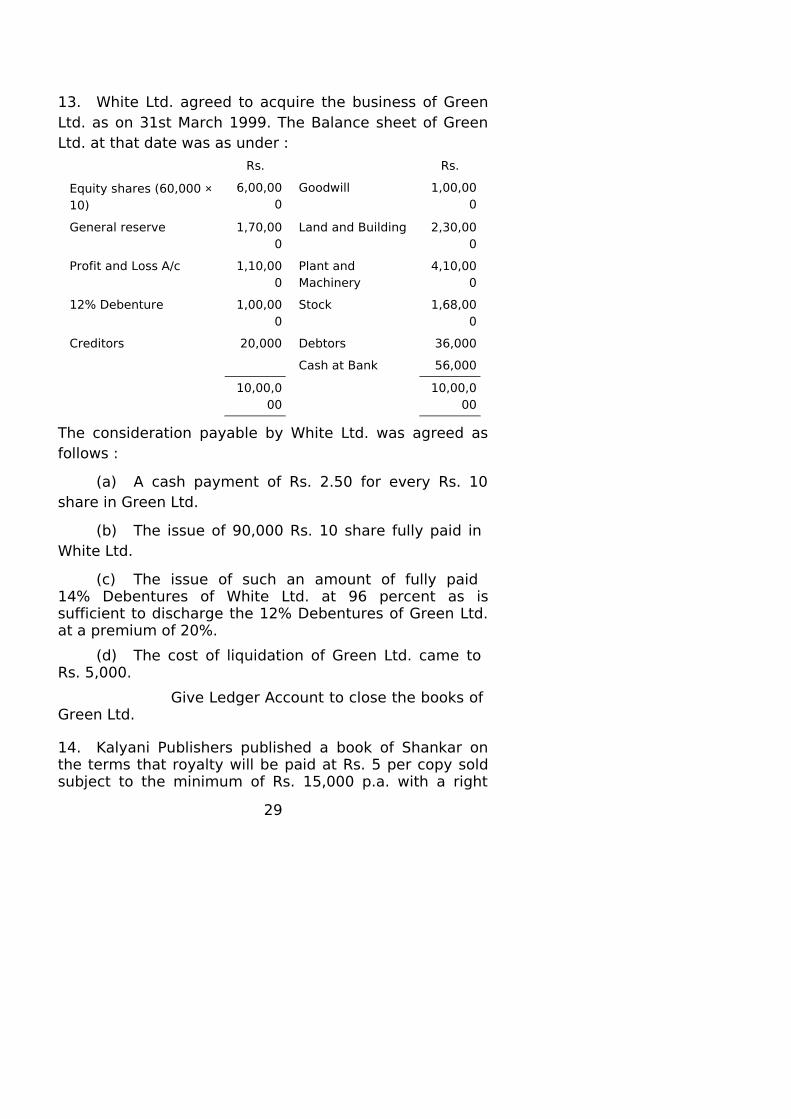

13. White Ltd. agreed to acquire the business of Green Ltd. as on 31st March 1999. The Balance sheet of Green Ltd. at that date was as under :

Rs. Rs.

Equity shares (60,000 × 10)

6,00,000

Goodwill 1,00,000

General reserve 1,70,000

Land and Building 2,30,000

Profit and Loss A/c 1,10,000

Plant and Machinery

4,10,000

12% Debenture 1,00,000

Stock 1,68,000

Creditors 20,000 Debtors 36,000

Cash at Bank 56,000

10,00,000

10,00,000

The consideration payable by White Ltd. was agreed as follows :

(a) A cash payment of Rs. 2.50 for every Rs. 10 share in Green Ltd.

(b) The issue of 90,000 Rs. 10 share fully paid in White Ltd.

(c) The issue of such an amount of fully paid 14% Debentures of White Ltd. at 96 percent as is sufficient to discharge the 12% Debentures of Green Ltd. at a premium of 20%.

(d) The cost of liquidation of Green Ltd. came to Rs. 5,000.

Give Ledger Account to close the books of Green Ltd.

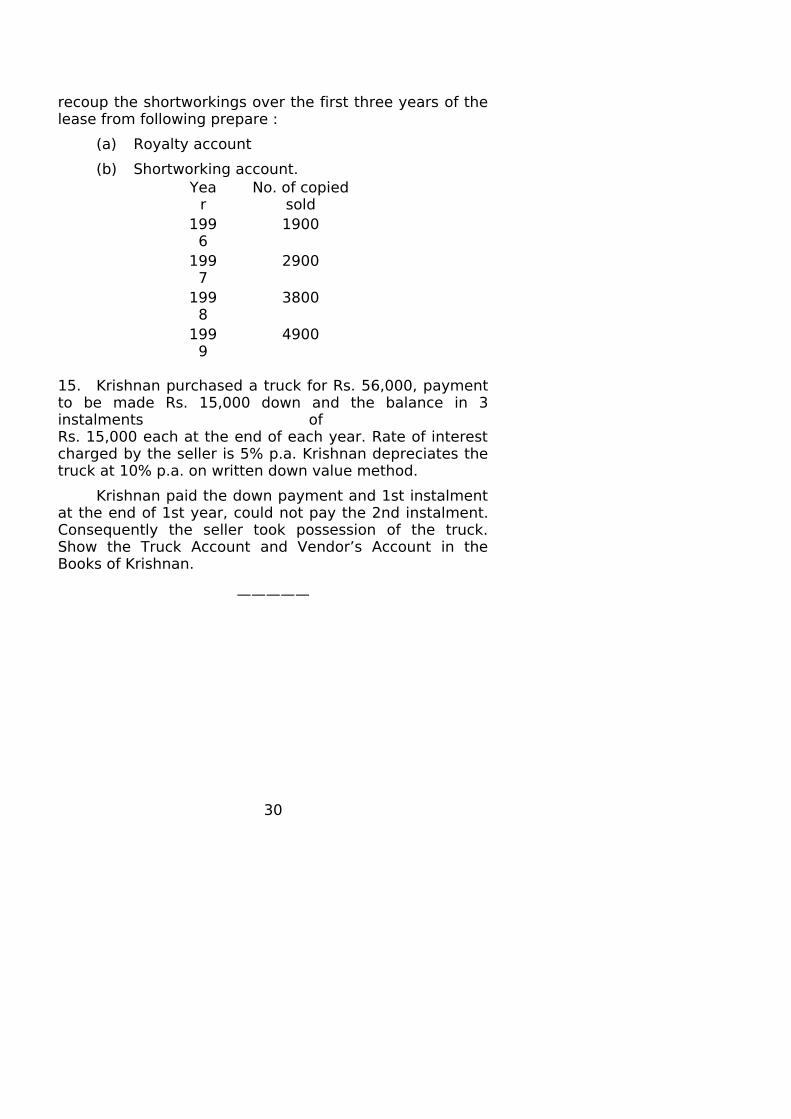

14. Kalyani Publishers published a book of Shankar on the terms that royalty will be paid at Rs. 5 per copy sold subject to the minimum of Rs. 15,000 p.a. with a right

29

recoup the shortworkings over the first three years of the lease from following prepare :

(a) Royalty account

(b) Shortworking account.Yea

rNo. of copied

sold199

61900

1997

2900

1998

3800

1999

4900

15. Krishnan purchased a truck for Rs. 56,000, payment to be made Rs. 15,000 down and the balance in 3 instalments of Rs. 15,000 each at the end of each year. Rate of interest charged by the seller is 5% p.a. Krishnan depreciates the truck at 10% p.a. on written down value method.

Krishnan paid the down payment and 1st instalment at the end of 1st year, could not pay the 2nd instalment. Consequently the seller took possession of the truck. Show the Truck Account and Vendor’s Account in the Books of Krishnan.

—————

30

DE–5301

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

CORPORATE FINANCE

(1999 onwards)

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions in 200 words.

1. How the finance department of a large company be organised?

2. Wealth maximisation is a superior objective of financial management. Do you agree? How?

3. What are the factors that affect financial plan?

4. Discuss the drawbacks of over capitalisation.

5. ‘‘Debt is the important source of financing’’. What merits it has from a company’s point of view?

6. What do you mean by ploughing back of profits? Discuss its merits.

7. Briefly explain the sources for term loans.

8. Inadequate working capital affects the smooth running of the Business. How?

31

25

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. Explain the determinants of working capital.

10. Discuss the functions of UTI.

11. Describe the merits and demerits of Equity Capital and Preference Capital.

12. What are the factors affecting capital structure of a firm?

13. Narrate the important considerations in planning finance.

14. ‘‘Modern days financial manager has tremendous responsibilities’’ — Argue.

15. Evaluate the Institutional finance as a source for permanent capital requirement.

———————

32

DE–5302

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

CAPITAL MARKET LAWS

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions.

1. Distinguish between capital market and money market.

2. Who are suppliers of funds to the capital market?

3. How does a stock exchange serve as an economic barometer?

4. Distinguish between broker and robber.

5. State the objectives of SEBI.

6. What are the advantages of Listing of Securities?

7. Distinguish between NSE and OTCEI.

8. What are the components of capital market?

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. Analyse the features of a developed capital market.

10. Explain the functions of a stock exchange.

33

31

11. Discuss the objectives of NSE. State the membership requirements of NSE.

12. Discuss the role of SEBI in regulating the working of stock exchanges.

13. Explain in detail the objectives and salient features of SEBI Act 1992.

14. Explain the objectives and benefits of OTCEI.

15. Discuss the advantages and evils of speculation in stock market.

————————

34

DE-5303

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

INCOME TAX LAW AND PRACTICE/TAX LAWS

(2002 onwards)

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions.

All questions carry equal marks.

1. State any four kinds of agricultural income.

2. State any four excluded assets from the definition of capital assets.

3. Ganesan furnishes the following particulars of his income for the previous year 2007–08. Compute the income from other sources for the assessment year 2008–09 :

Rs.

(a)

Dividend paid by Ashok Leyland Ltd. 35,000

(b)

Dividend from co-operative society 8,000

(c)

Interim dividend from Rane (Madras) Ltd.

4,000

35

32

(d)

Dividend from a foreign company 30,000

(e)

Dividend from U.T.I. 7,000

4. Give an account of (a) Causal income (b) TDS.

5. Explain Rebate under Section 88.

6. Murugan is engaged in the business of manufacturing Fibre Products. On 1.4.2007 the W.D.V. of his various assets was as given below :

Particulars P & M Building

Rs. Rs.

W.D.V. at the beginning of the year 8,00,000

30,00,000

Additions during the year 1.8.2007 4,00,000

Nil

Sale of a part of the asset during the year

20,00,000

6,00,000

Compute depreciation for PY 2007-08 and written down value on 31.3.2008. Rate of depreciation is as per the Income Tax Act.

7. Mr. Kumar owns a house at Delhi (Municipal value Rs. 20,000) of the fair rent of Rs. 24,000 p.a. during the previous year 2007–08 :

Expenses were :

Municipal taxes Rs. 6,000, Repairs Rs. 2,000, Fire insurance premium Rs. 3,500, Land revenue Rs. 4,000 and Ground rent Rs. 2,000. A loan of Rs. 30,00,000 was taken on 1st April 2000 @ 15% p.a. for construction of the house which was completed on 31st March, 2002. Nothing was repaid on loan account so far. Find out his taxable income from House Property for the assessment year

36

2008–09. The house was self occupied throughout the P.Y.

8. Explain the House Rent Allowance exemption under Sec. 10 (13 A).

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

All questions carry equal marks.

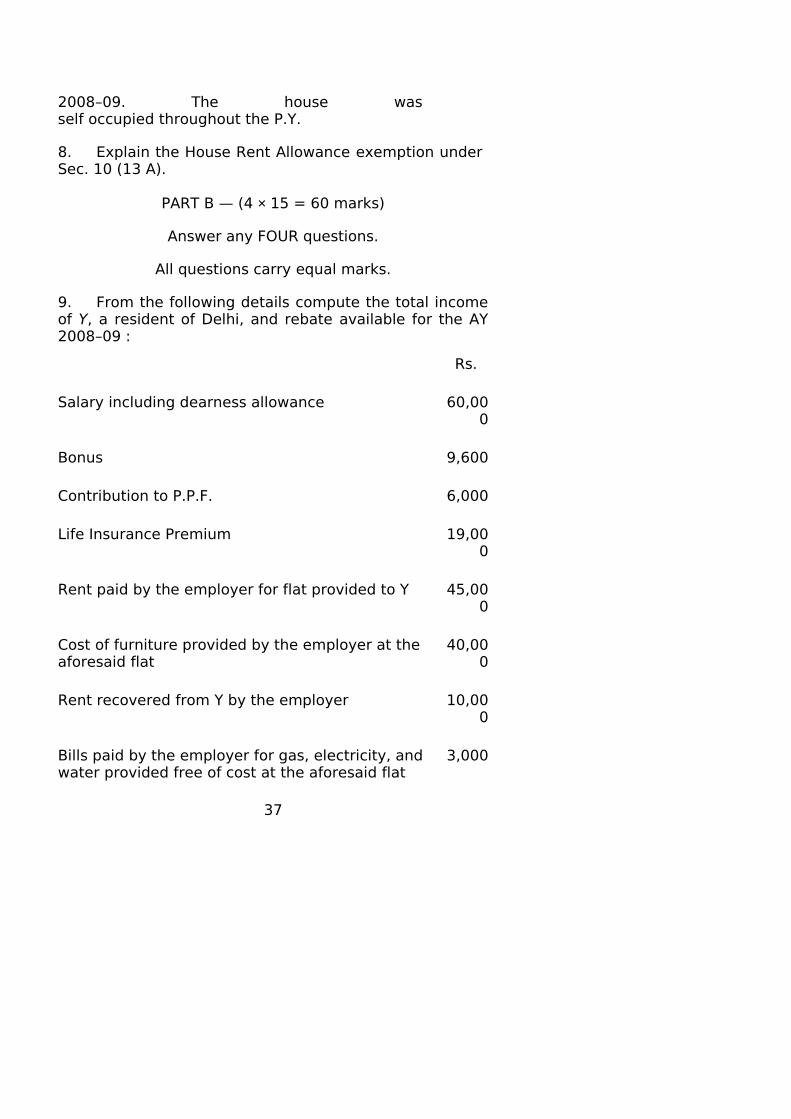

9. From the following details compute the total income of Y, a resident of Delhi, and rebate available for the AY 2008–09 :

Rs.

Salary including dearness allowance 60,000

Bonus 9,600

Contribution to P.P.F. 6,000

Life Insurance Premium 19,000

Rent paid by the employer for flat provided to Y 45,000

Cost of furniture provided by the employer at the aforesaid flat

40,000

Rent recovered from Y by the employer 10,000

Bills paid by the employer for gas, electricity, and water provided free of cost at the aforesaid flat

3,000

37

Rs.

Y owns a house at Delhi :

Rent received (12 months) 36,000

Municipal valuation 24,000

Municipal tax paid 6,000

Ground rent 1,000

Insurance charges 500

Collection charges 2,700

Interest on borrowings used for construction of house (The house was constructed in June 2000)

24,000

Interest received from Unit Trust of India 57,000

Deposit under National Saving Scheme 20,000

X was provided with company's car (self-driven) for personal use with effect from September 3, 2002. It is not possible to determine expenditure on personal use and all expenses were borne by the employer.

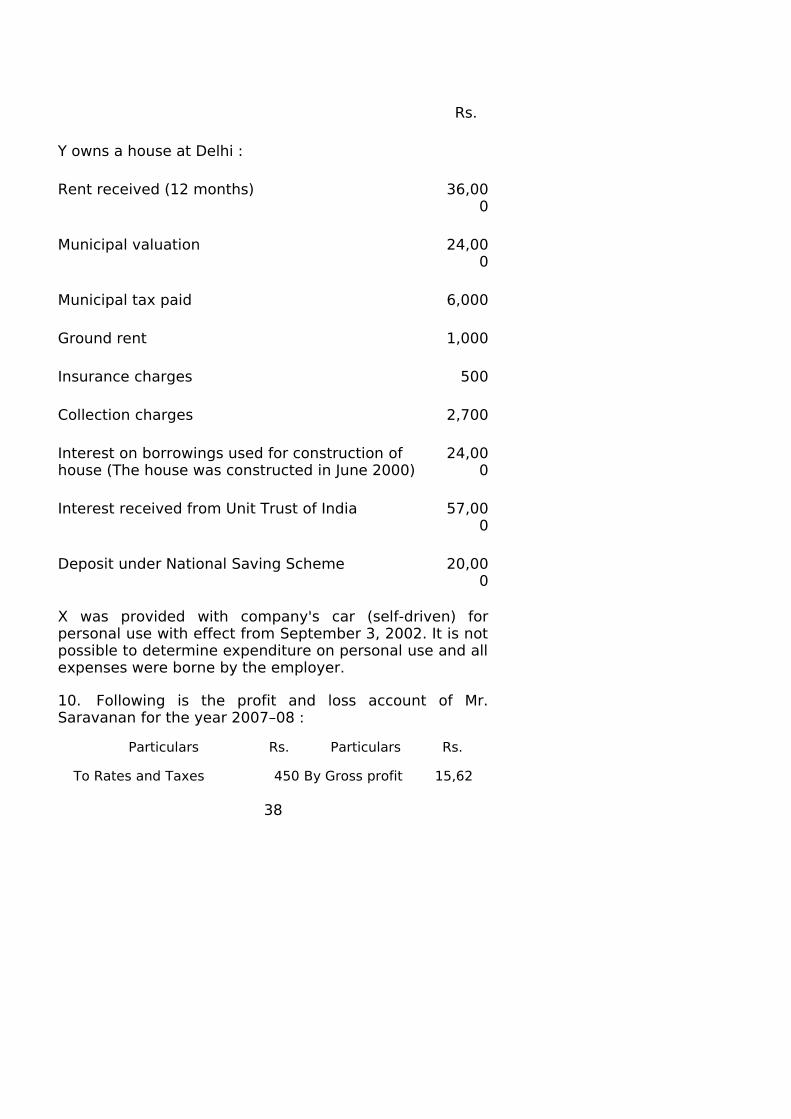

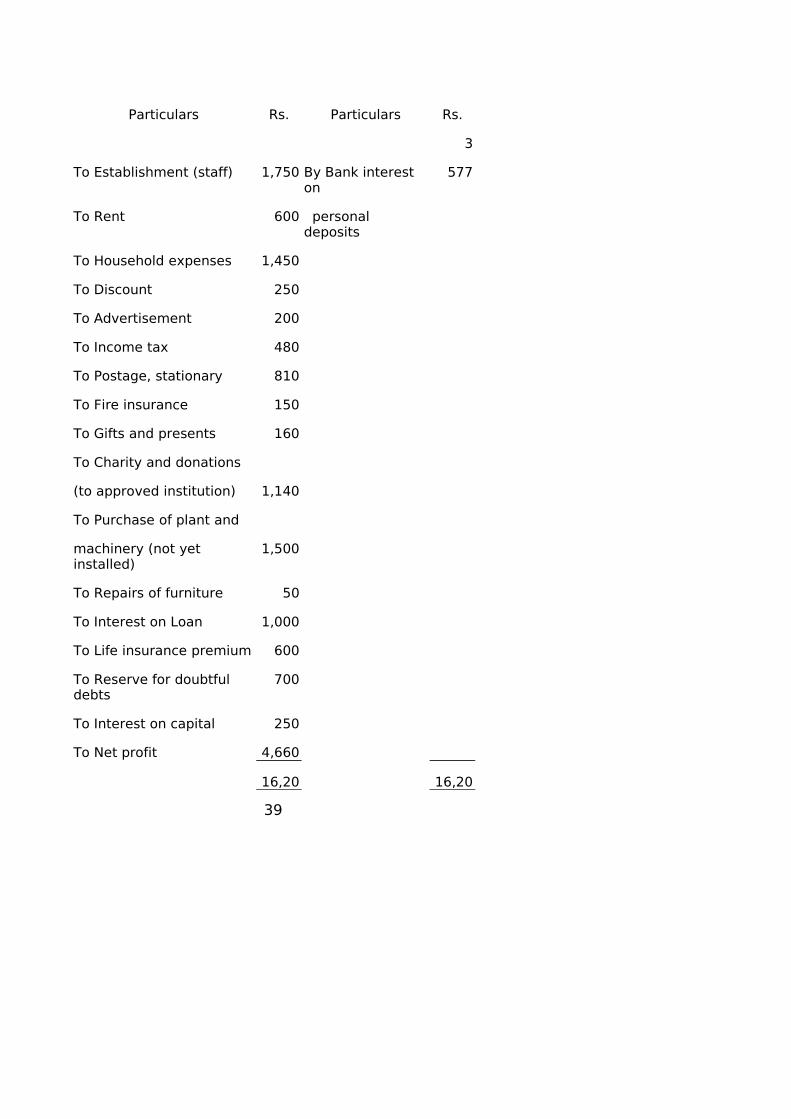

10. Following is the profit and loss account of Mr. Saravanan for the year 2007–08 :

Particulars Rs. Particulars Rs.

To Rates and Taxes 450 By Gross profit 15,62

38

Particulars Rs. Particulars Rs.

3

To Establishment (staff) 1,750 By Bank interest on

577

To Rent 600 personal deposits

To Household expenses 1,450

To Discount 250

To Advertisement 200

To Income tax 480

To Postage, stationary 810

To Fire insurance 150

To Gifts and presents 160

To Charity and donations

(to approved institution) 1,140

To Purchase of plant and

machinery (not yet installed)

1,500

To Repairs of furniture 50

To Interest on Loan 1,000

To Life insurance premium 600

To Reserve for doubtful debts

700

To Interest on capital 250

To Net profit 4,660

16,20 16,20

39

Particulars Rs. Particulars Rs.

0 0

You are required to ascertain the business income of Mr. Saravanan.

11. Mr. P. Saroja received the following emoluments during the financial year 2007–08. He is a central government employee. You are required to compute his income from salary for the relevant assessment year from the information given below :

Rs.

Basic pay per annum 36,000

Dearness allowance per annum (forming part

of salary)

18,000

Project allowance per annum 6,000

House rent allowance per annum 8,400

Advance salary for April 2008 3,000

Entertainment allowance (since 1975) per annum

6,000

Actual entertainment expenses per annum 4,800

Mr. P Sankar pays House Rent per month 800

12. Give an account of the following :

(a) Total income of a resident

(b) Incomes chargeable to tax under the head profits and gains of business or profession.

13. Mr. Kumar is a professor in Bombay University. Following are the particulars of his income for the assessment year 2008–09 :

(a)

Basic pay Rs. 16,000 p.m.

40

(b)

Dearness allowance @ 38% of salary

(c)

House rent allowance Rs. 3,000 p.m. he paid rent of Rs. 4,500 p.m.

(d)

Wardenship allowance Rs. 1,000 p.m.

(e)

Income received from house property (computed) Rs. 16,800

(f) Interest received from Govt. Securities (Gross) Rs. 8,200

(g)

Interest on Bank deposits Rs. 2,000

(h)

Contribution to provident fund 12% of basic salary.

(i) Premium paid by cheque on mediclaim insurance policy Rs. 5,000

(j) Donation to an approved charitable institution Rs. 30,000

Compute his total income for the Assessment year 2008–09.

14. Explain the provisions of Income Tax Act on :

(a) Section 54

(b) Section 54 B

(c) Section 80 G.

41

15. Mr. Daniel has the following incomes during the year ending 31.3.08 :

(a) Dividend declared by Y & Co. on 31.3.06 - Rs. 6,000

(b) Dividend declared by P & Co. on 31.3.07 - Rs. 9,000

(c) Interim dividend received on 1.5.07 - Rs. 3,000

(d) He won Gold worth Rs. 10,00,000 from Pondicherry Vaniga Thiruvizha

(e) During March 2008 he earned Rs. 1,00,000 as price money on horse races. These horses are owned by him and expenditure incurred on maintenance of these horses amounted to Rs. 1,60,000.

Compute the income from other sources.

——————

42

DE–5304

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

ECONOMIC LAWS

Time : Three hours Maximum : 100 marks

SECTION A — (5 × 8 = 40 marks)

Answer any FIVE questions.

1. Explain the need for development council.

2. What is meant by Notified Area?

3. How will the non resident Indians invest in shares of

Indian companies?

4. Define Foreign exchange.

5. Bring out the scope and powers of the MRTP

Commission.

6. What is meant by Monopoly and Restrictive Trade

Practice?

7. Explain the method of appeal against confiscation

order.

43

33

8. What are the objectives of Environmental Protection

Act of 1986?

SECTION B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. Describe the features of Industries (Development and Regulation) Act of 1951.

10. What are the transactions controlled by foreign Exchange Regulation Act?

11. Briefly explain the various types of restrictive trade practices.

12. Critically evaluate Role of Monopolies and Restrictive Trade Practices Act of 1969, in Indian Trade System.

13. Write an essay on control of production and distribution of essential commodities.

14. Explain briefly about seizure and confiscation of essential commodities.

15. Explain the features of Environment Protection Act of 1986.

———————

44

DE–5305

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

COST ACCOUNTING

(1999 onwards)

Time : Three hours Maximum: 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE out of Eight.

1. Define costing and bring out the objectives.

2. What is labour Turn Over and how it is calculated?

3. What is Economic Order Quantity and explain with

formula?

4. What are process losses?

5. What is cost plus contract?

6. Calculate the total earnings of a worker under

Halsey Plan.

Standard Time 15 hours, Time taken 12 hours

Hourly rate Rs. 2 plus D.A. @ 0.50 paise per hour.

7. From the following data calculate the value of Raw-Materials consumed.

45

34

Raw Materials purchased Rs. 88,000

Opening stock of materials Rs. 1,00,000

Closing stock of materials Rs. 1,23,000.

8. Ascertain :(a) Prime Cost

(b) Factory cost

(c) Cost of production

(d) Total Cost.

Factory Exp. Rs. 30,000

Admn. Exp. Rs. 20,000

Labour Rs. 25,000

Materials Rs. 35,000

Selling Exp. Rs. 10,000.

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. What are the various methods of pricing issue of

materials? Explain any four methods.

10. Calculate the normal and overtime wages payable to a worker.

Days Hours worked

Monday 8

Tuesday 10

Wednesday 9

Thursday 11

Friday 9

Saturday 4

46

Normal Working

hours 8 hours per day

Normal rate 0.50 paise per hour

Overtime rate Upto 9 hours in a day at single

rate

Over 9 hours in a day at double

rate.

11. The following particulars are taken from the costing

records of an Enterprise.

Rs.

Cost of Raw-Materials (Opening) 30,000

Cost of Raw-Materials (Closing) 25,000

Cost of Work in Progress

(Opening)

12,000

Cost of Work in Progress

(Closing)

15,000

Cost of finished goods (Opening) 60,000

Cost of finished goods (Closing) 55,000

Purchase of Raw-Materials 4,50,000

Wages paid 2,30,000

Factory overheads 92,000

Administration overheads 30,000

Selling and distribution

overheads

20,000

Sales 9,00,000

Prepare cost sheet showing Prime Cost, Factory Cost,

Cost of Production, Cost of sales and Profit.

12. From the following particulars, compute machine

hour rate.

47

Cost of machine 30,000

Estimated scrap value after the expiry of

its life of 5 years

3,000

Rent per month 500

General lighting per month 200

Supervision salary per month 1,500

Power consumption 5 units per hour @ 0.60 paise per

unit.

Estimated working hours 2000 per year.

The machine occupies 1/4 of the total area of the

shop.

The supervisor is expected to devote 1/5 of his time to

the machine.

13. Calculate the cost of each process and total cost of production from the following data :

Process I

Rs.

Process IIRs.

Process IIIRs.

Materials 2,250 750 300

Wages 1,200 3,000 900

Direct Exp.

Fuel 300 200 400

Carriage 200 300 100

Work Overheads

1,890 2,580 1,875

The indirect expenses Rs. 1,272 should be apportioned on the basis of wages.

48

14. The following are the expenses incurred in respect of two production depts. X and Y and are service dept. namely Z.

Power 8,400

Labour Welfare Exp. 4,500

Rent 7,200

Insurance 11,200

Dep.

Building 6,000

Machinery 16,000

Lighting 2,400

Additional Information :X Y Z

KWH Installed 12 10 2

Light Points 15 20 5

Area occupied Sq.ft. 1,000 800 600

No. of employees 20 8 2

Machine hours worked

2,000 1,500 500

Service Dept. Z has rendered service to the production departments equally. Ascertain the total cost of the departments and overhead rate per machine hour for production departments.

15. Write short notes on :

(a) Equivalent production.

(b) Batch Costing.

(c) Allocation and Apportionment of overheads.

–––––––––––––––

49

DE-5306

DISTANCE EDUCATION

B.C.S. DEGREE EXAMINATION, MAY 2009.

FINANCIAL SERVICES

Time : Three hours Maximum : 100 marks

SECTION A — (5 × 8 = 40 marks)

Answer any FIVE of the following.

1. What is a financial market? What are its components?

2. What is a finance company? What are its weaknesses?

3. What is fund based financial services of a commercial bank? Give any three examples.

4. What is an operating lease? Discuss its salient features.

5. What is a mutual fund? How it operates?

6. What are the types of mutual funds?

7. What is venture capital? What are its features?

8. Who is a merchant banker? What are his functions?

SECTION B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. Briefly trace out the development of financial markets in India.

50

35

10. What are the functions of finance companies?

11. What is a Hire purchase agreement? What are the usual clauses of a Hire purchase agreement?

12. What is credit rating? Why it is required? What are its merits from the point of view of the rated company?

13. ‘‘Credit card replaces currency, It is more a necessity rather than a luxury for the Middle class people in India’’-Discuss.

14. What are the types of mutual fund scheme? Discuss the salient features of any one scheme of U.T.I. Mutual Fund.

15. Who is an underwriter? What is his role in public issue? It is compulsory that every public issue should be underwritten?

———————

51