layaway business model

TRANSCRIPT

Layaway as a mechanism for financial inclusion

15.S66 Business Model, Darin O. Bellisario, April 2015

Market context: the connection between financial inclusion, demand, and economic development............ 2

The layaway model of savings and consumption ......................................................................................... 4

Beachhead Market & Expansion Pathway .................................................................................................... 6

Market Size ................................................................................................................................................... 7

Local vendor distribution: fraud and incentives ............................................................................................. 7

Back-end inventory and delivery ................................................................................................................... 8

Product Mix & Sourcing ................................................................................................................................. 8

Basic Retail ................................................................................................................................................ 9

Exclusive Private Partnerships .................................................................................................................. 9

Government partnerships .......................................................................................................................... 9

Trust, branding, and partnerships ................................................................................................................. 9

Values ......................................................................................................................................................... 10

Revenues streams ...................................................................................................................................... 11

Sale of goods ........................................................................................................................................... 11

Negative working capital .......................................................................................................................... 11

Competition ................................................................................................................................................. 11

Retail substitutes ..................................................................................................................................... 11

Savings substitutes .................................................................................................................................. 12

Analogies..................................................................................................................................................... 12

myAgro .................................................................................................................................................... 12

KickStart .................................................................................................................................................. 13

Pilot Financials ............................................................................................................................................ 13

Steady State ............................................................................................................................................ 13

Go-to-market capital ................................................................................................................................ 14

Layaway in India Darin O. Bellisario

2

Market context: the connection between financial inclusion, demand, and economic development

Saving money is a double challenge for the poor in emerging economies. Structurally, there is a well-

documented absence of access to savings account and credit; over 70% of the population in low and low-

middle income countries is entirely unbanked, compared to 11% in high-income nations.1,2,3 Psychologically,

when your quality of life is low i.e., approximately, when your total consumption is low, the number and

appeal of short-term consumption options can overwhelm your capacity to abstain; if your child is ill, or

there is a hole in your roof, or your brother went bankrupt, it is hard not to tap into any money you have

tucked away even if you could likely ‘get by’ without.4,5,6 As a result, the global poor rarely save, even when

savings could increase not only their quality of life but also their incomes.7 The World Bank, the People’s

Bank of China, and the Gates foundation are

among countless other private, public, and

non-governmental organizations that have

cited financial inclusion, with an emphasis on

savings, as key market failures impeding

poverty alleviation and economic

development.

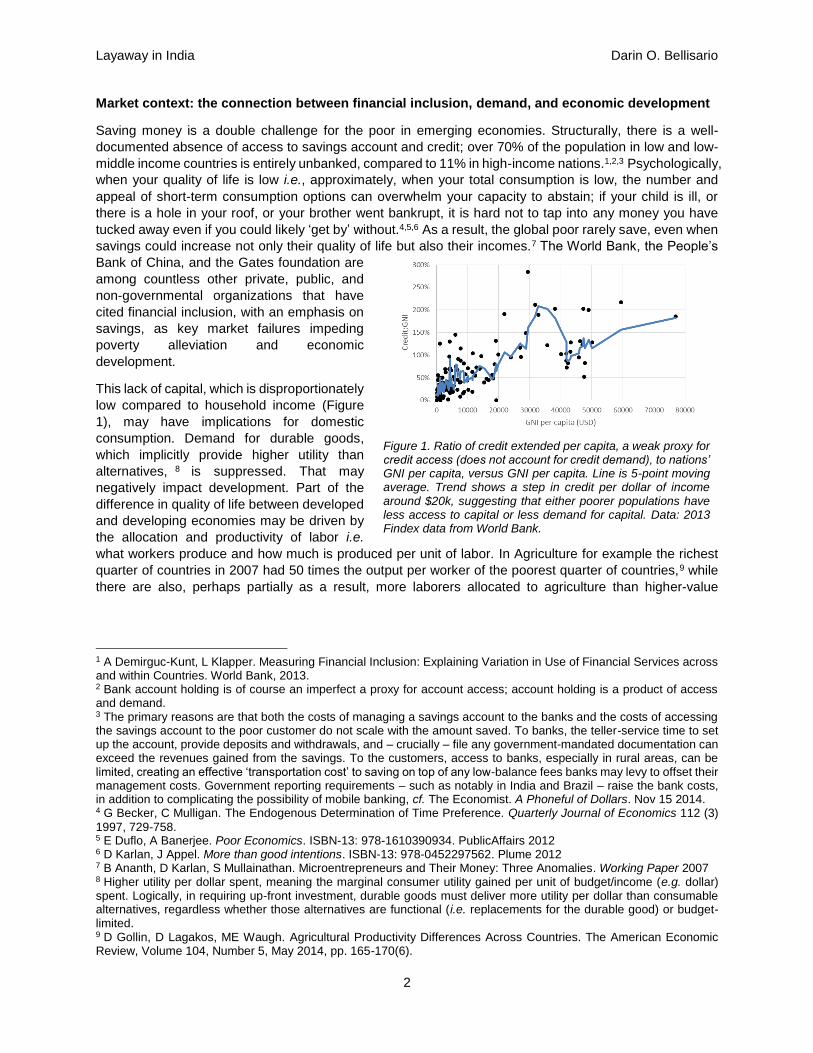

This lack of capital, which is disproportionately

low compared to household income (Figure

1), may have implications for domestic

consumption. Demand for durable goods,

which implicitly provide higher utility than

alternatives, 8 is suppressed. That may

negatively impact development. Part of the

difference in quality of life between developed

and developing economies may be driven by

the allocation and productivity of labor i.e.

what workers produce and how much is produced per unit of labor. In Agriculture for example the richest

quarter of countries in 2007 had 50 times the output per worker of the poorest quarter of countries,9 while

there are also, perhaps partially as a result, more laborers allocated to agriculture than higher-value

1 A Demirguc-Kunt, L Klapper. Measuring Financial Inclusion: Explaining Variation in Use of Financial Services across and within Countries. World Bank, 2013. 2 Bank account holding is of course an imperfect a proxy for account access; account holding is a product of access and demand. 3 The primary reasons are that both the costs of managing a savings account to the banks and the costs of accessing the savings account to the poor customer do not scale with the amount saved. To banks, the teller-service time to set up the account, provide deposits and withdrawals, and – crucially – file any government-mandated documentation can exceed the revenues gained from the savings. To the customers, access to banks, especially in rural areas, can be limited, creating an effective ‘transportation cost’ to saving on top of any low-balance fees banks may levy to offset their management costs. Government reporting requirements – such as notably in India and Brazil – raise the bank costs, in addition to complicating the possibility of mobile banking, cf. The Economist. A Phoneful of Dollars. Nov 15 2014. 4 G Becker, C Mulligan. The Endogenous Determination of Time Preference. Quarterly Journal of Economics 112 (3)

1997, 729-758. 5 E Duflo, A Banerjee. Poor Economics. ISBN-13: 978-1610390934. PublicAffairs 2012 6 D Karlan, J Appel. More than good intentions. ISBN-13: 978-0452297562. Plume 2012 7 B Ananth, D Karlan, S Mullainathan. Microentrepreneurs and Their Money: Three Anomalies. Working Paper 2007 8 Higher utility per dollar spent, meaning the marginal consumer utility gained per unit of budget/income (e.g. dollar) spent. Logically, in requiring up-front investment, durable goods must deliver more utility per dollar than consumable alternatives, regardless whether those alternatives are functional (i.e. replacements for the durable good) or budget-limited. 9 D Gollin, D Lagakos, ME Waugh. Agricultural Productivity Differences Across Countries. The American Economic Review, Volume 104, Number 5, May 2014, pp. 165-170(6).

Figure 1. Ratio of credit extended per capita, a weak proxy for credit access (does not account for credit demand), to nations’ GNI per capita, versus GNI per capita. Line is 5-point moving average. Trend shows a step in credit per dollar of income around $20k, suggesting that either poorer populations have less access to capital or less demand for capital. Data: 2013 Findex data from World Bank.

Layaway in India Darin O. Bellisario

3

goods.10 Domestic and international economic programs tend to focus on spurring the production side of

that dynamic, attempting to improve the productivity and industry-focus of domestic firms large or small.

Driving supply without domestic consumption however relies on exports, which means competing on a

global market against large multinational firms that don’t suffer the infrastructure or institutional

inefficiencies that tend to plague emerging economies. Less attention is paid to the demand side – giving

domestic consumers access to higher value-added products. If poor consumers could save money to spend

on durable goods, domestic firms could orient to produce those higher-value-added goods. That in turn

could create higher-value-added jobs, raising incomes, which raises demand for higher-value-added goods,

and so on in a virtuous cycle to incrementally shift the distribution of labor towards that of a wealthy economy.

In this proposed model, allowing the poor to buy higher-utility goods would lead to the production of higher-

utility goods, raising social welfare.

Despite this potential benefit of consumer savings, access to ‘microsavings’ remains limited for the

economic and psychological reasons discussed in the first paragraph. From a Bank P&L standpoint,

providing a customer with ready access to a savings account incurs front-end costs of account access (e.g.

branch employee hours, ATMs) and back-end costs of sign-up and maintenance (e.g. regulatory reporting,

labor costs for gathering, checking, and entering data) that don’t scale with savings amount and therefore

aren’t offset by the revenues from saving for the poor. A 2012 McKinsey report estimated that the cost

offering a traditional retail savings account in Mexico was $70 per year, and even for mobile banking was

$40 per year.11 For a commercial bank averaging a typical 1% annual return on assets, the minimum

account size to turn a profit is $7000, which is ten times the total income of someone living on $2 a day,

and essentially infinite compared to the amount they could conceivably save. In a 2011 randomized control

trial in Indonesia for example, Cole, Sampson, and Zia found that subsidizing bank account costs to provide

savings accounts to the poor led to account use that persisted through a two-year follow-up, suggesting

that demand for such accounts is not being met due to cost restrictions.12

Saving also entails the psychological issue of abstaining from consumption for the poor, explaining why the

poor have difficulty even stashing money under the mattress. The famous Cemex success story highlights

this experience. Cemex observed that poor customers were partially-building rooms and homes, gradually

adding cement and rebar over several years to complete construction. At first flush, that tactic seems absurd.

Surely the customer could simply hold on to the money and then purchase the construction materials

required all at once; building bit by bit prevents you from being able to pull from those savings in an

emergency, and exposes your investment to the elements or local economic risk. On average 30% of the

building materials were wasted due to this incremental construction practice. Talking to customers however,

the Cemex team realized that the poor were deliberately constraining their ability to draw from savings, as

otherwise the abundant temptations – impossible for us in wealthy nations to imagine – would constantly

drain their funds. Understanding this, cemex started selling smaller packets of cement, as well as providing

warehouses to gradually build portable structures more efficiently, growing the top line of a customer

segment representing 40% of their business.

What do the poor want to do with their savings? There are indications that demand exists to purchase

durable goods, for the purposes of pleasure, household enterprises, or home economics (i.e. avoiding the

‘poor tax’ of relying on low-efficiency consumables). In a randomized control trial, microcredit borrowers at

a 24% annual interest rate increased durable good spending without increasing household income.13 That

implies that those consumers are willing to incur essentially a 24% premium on the price for the sake of

10 D Gollin, D Lagakos, ME Waugh. The Agricultural Productivity Gap. The Quarterly Journal of Economics (2014) 129 (2): 939-993 11 D Hattingh, B Russo, A Sun-Basorun, A Van Wamelen. The Rise of the African Consumer. McKinsey Global Institute 2012. 12 S Cole, T Sampson, B Zia. Prices or Knowledge? What Drives Demand for Financial Services in Emerging Markets? The Journal of Finance. Volume 66, Number 6, December 2011, pp.1933. 13 E Duflo, A Banerjee, R Glennerster, CG Kinnan. The Miracle of Microfinance? Evidence from a Randomized Evaluation. NBER Working Paper, 2013.

Layaway in India Darin O. Bellisario

4

purchasing these goods. Unless we take them for fools, those micro-loans and resulting purchases must

be unquestionably improving their lives even if it does not raise their incomes. That premium also suggests

an enormous economic value proposition to firms: poor consumers are willing to pay an extra premium,

over their wealthier counterparts, for value-added goods.

To summarize, the poor seem to want to save, to invest in their future quality of life especially through the

purchase of durable goods. The traditional model of savings accounts however are incongruous with their

lifestyles. The maintenance of savings accounts is costly, even when implemented on a mobile platform,

even while consumers don’t necessarily want the financial flexibility they provide that creates that cost in

the first place. Indeed the Cemex, microcredit RCT, and numerous other examples14 suggest that a lack of

flexibility in how savings are spent may actually appeal to poor consumers by helping them avoid

detrimental behavioral patterns. Customers want to transport their income forward in time, but are willing,

or prefer, to decide what they want to invest in up-front as a means to lock-in their commitment.

The layaway model of savings and consumption

As described, there is an enormous demonstrated unmet demand for durable goods, but capital market

failures are inhibiting access. Our venture overcomes this challenge by connecting poor consumer cash

flow directly to their desired consumption pattern, circumventing more flexible and therefore far more costly

savings or credit channels. We use a layaway model, where consumers deposit savings with us,

irrecoverably, towards a particular good. When they have deposited enough to buy the good, we give them

the product.

Figure 2. The basic layaway model from the customers perspective. The customer gives a local vendor money towards the purchase of a good. They receive nothing in return (except a text receipt) until the good is fully paid, at which point the vendor provides them with the good. They cannot withdraw money, but they can move their credit between goods. Details such as transfer of cash to us, delivery of goods to vendor, and receipts confirming deposit of money are discussed below.

Compared to layaway, microcredit and microsavings give consumers greater flexibility in their expenditures,

such as allowing precautionary saving towards unexpected catastrophes. That flexibility however comes at

enormous costs of information and enforcement that get passed on to consumers, while also relying on the

existence of local markets for desired goods in the first place. The layaway model more directly meets poor

14 cf. Duflo and Banerjee Poor Economics; D Karlan and J Appel More than good intentions; cited above.

Layaway in India Darin O. Bellisario

5

consumers’ needs because the ‘savers’ primarily save in order to purchase certain higher-value products.

Table 1 summarizes this favorable trade-off.

Table 1. Comparison of banking versus layaway to the poor

Microcredit and/or Microsavings Layaway

Expenditure Flexibility

Can purchase durable goods; long-run quality of life and household savings15

Precautionary savings towards unexpected catastrophes (e.g. health)

Enterprise investment

Can purchase durable goods; long-run quality of life and household savings

Costs Screening information costs Consumer access costs16 Enforcement costs (microcredit)

Distribution costs

The full business model is as follows, as designed for India, our proposed first national market, where

mobile banking is not ubiquitous:

Step 1. We enlist local shopkeepers as our distributors. We provide them with a catalog

showcasing all of our goods, along with prices and item codes. They receive a

substantial commission upon the sale of any good.

Step 2. A customer goes to the shopkeeper, selects a good, and gives money to the

shopkeeper towards that good.

Step 3. The shopkeeper texts us a message with the amount the customer provided and the

good they would like to place it towards.

Step 4. We send a text message to the customer confirming receipt of the amount they

deposited, which they expect to receive because we printed that process on every

page of the catalog.

Step 5. The customer cannot ‘withdraw’ money – it is credited towards the purchase of a

good – but they can change what they put the money towards, such as shifting from

an expensive product to a more rapidly purchasable one.

Step 6. When the vendor reaches a certain amount of assets on hand, one of our money

collectors picks it up.

Step 7. The customer puts money towards the good whenever they want to. When a good is

paid off, our delivery company (internal or outsourced, depending on local market

conditions) takes the good from one of our warehouses where we stock it and drops

it off with the local vendor. The customer is texted that the good has been delivered.

Step 8. The customer picks up the good, and the vendor receives her commission.

This transaction model with the local shopkeeper is similar to how mobile minutes are recharged at vendors.

In markets where mobile banking is ubiquitous, the customer will transfer funds to us directly, rather than

via cash to the local vendor. In a section below we discuss how we address potential issues of fraud, as

15 Household savings are reductions in monthly expenditures realized with durable goods versus disposable ones. For example a more efficient refrigerator or generator reduces electricity cost, or a bicycle reducing transportation costs. 16 The cost associated with being available to the customer, such as allowing the customer to take out there money from a savings account or put money towards a good on layaway.

Layaway in India Darin O. Bellisario

6

well as the distribution and incentive principles we adopt. We also discuss how we source the goods, how

we build initial trust with the customer, and other issues crucial to adoption.

We can summarize the key benefits we are providing to each stakeholder.

Table 2. Stakeholder value propositions

Stakeholder Poor Consumer (‘poor’ def. income less than $3 per day)17

Value propositions The ability to save at no cost, albeit solely towards the purchase of any product we sell.

An enforced commitment to saving; you can’t get your money back. Access to a wide variety of goods that they may not, especially in rural

communities, have easy access to even with the requisite capital. Access to any ‘special’ goods that we exclusively provide through

partnerships with private firms e.g. Bollywood merchandise. Access to subsidized goods through government partnership e.g. water

purification systems, condoms, solar panels.

Present Alternatives Don’t save at all; little to no formal banking penetration. Informal personal network savings mechanism. If available, use microcredit to effectively save at a 25-100% premium

on the cost of the good.

Stakeholder Investors

Value propositions Revenue streams: Retail revenues from this new market for existing durable goods Negative working capital (consumer ‘savings’) available for investment.18 Retail revenues for exclusive goods enabled by our distribution network.

Stakeholder Wholesale suppliers

Value propositions New market for their goods

Stakeholder National and regional governments

Value propositions Higher standard of living, happier population. Increased domestic demand for durable goods; increased local

commerce. Through our distribution channel, access to population for subsidized-

good welfare programs.

Beachhead Market & Expansion Pathway

We have chosen urban centers in India as our beachhead market. Discussions with non-profit organizers

and academic researchers operating in that market suggest that most urban centers have the elements

critical to our success:

(1) Local vendors we can enlist as distribution channels

(2) High mobile phone penetration (over 70% in urban markets),19 albeit almost no penetration of

mobile money transfer.

(3) Access to savings accounts is low; only 7.5% of the poorest 40% of Indians saved money at a

financial institution in 2014.20

17 Correlates with poor access to formal savings, 2013 World Bank Findex Report. 18 This revenue stream, discussed below, is in some ways analogous to the insurance industry model. 19 146% penetration with an average 2.06 cell phones per user, according to the 2014 Dept. of Telecommunications pan-India tele-density report. 20 World Bank Findex data 2014.

Layaway in India Darin O. Bellisario

7

Because our distribution, Sales, and marketing are all localized, we can pilot this model in a single city to

start. When we have proven and refined the model in the first urban center, we can expand to other urban

centers one by one. The metrics we propose to prioritize city selection are:

(1) Mobile phone penetration among the poor

(2) Low savings account penetration among the poor

(3) Fraction of potential vendors with sufficient transportation access for deliveries and pickups

(4) Low petty crime rate

Where data does not exist, preliminary surveys can be conducted in candidate cities to estimate these

factors.

After establishing our presence in urban Indian markets, we can consider expanding to rural markets.

Compared to internationalization, this expansion presents the economies of scale of using our existing

supplier relationships, government relationships, brand investment, and potentially some overlap in

distribution. Negatively however, mobile phone penetration in rural India is sub-optimal, 42% in July 2013

based on the Dept. of Telecommunications figures. If the distribution of those users is disperse such enough

customers know someone who can receive text messages for them, the option remains available.

Otherwise, we can shift to internationalization.

Market Size

We estimate the global market for durable goods amongst the poor to be on the order of $353 billion.

We roughly estimate that total demand for durable goods amongst the unbanked by estimating a mean

willingness to pay and multiplying by the volume of consumers. For the latter figure, 2.5 billion adults in the

world are estimated to be unbanked, of which the majority are classified as poor (earning less than $1.25

ppp per day).21 For a willingness-to-pay figure, we approximate using the limited randomized control trial

data from microcredit investigations, such as footnote 13, where durable good consumption rose in

response to credit access at an APR of 24%. Although crude, we can use this ‘durable good penalty’ to

approximate that poor consumers are willing to spend of order 24% of their incomes towards durable goods

to which they do not have access. That figure could be low because it includes only the extra cost those

consumers were willing to take on, not the principle they are deriving it from, but could also be high because

not all of the consumers may have diverted their income in that manner. This penalty therefore simply

provides a baseline. For incomes, the global bottom two quintiles average $1.0 and 2.1 per day, respectively,

based on World Bank (2011), UNU-WIDER (2008) and Eurostat (2011) data.22

That provides an estimate of $141 per year average consumer spending on durable goods available, which

translates to our global market size of $352.5 billion. While that estimate is highly approximate, it provides

an order of magnitude that justifies the venture’s interest: if we can provide a market for durable goods

that financial exclusion is inhibiting, the market opportunity is large.

Local vendor distribution: fraud and incentives

Our distribution model relies on local vendors, which raises the specters of fraud and robbery. Our

implementation strategy focuses on minimizing these effects, while maintaining a strong relationship with

the vendor – who is, after all, our Sales representative.

21 Global Financial Development Report, World Bank, 2014 22 I Ortiz, M Cummins. Global Inequality: Beyond the bottom billion. Unicef 2011.

Layaway in India Darin O. Bellisario

8

(1) Vendors will be compensated with very competitive commissions, providing clear financial value

to their relationship with us over one-time fraudulent activities. As a ‘stick,’ black-lists of banned

vendors we find engaging in fraudulent activity can be circulated amongst other vendors, who can

use that to attract away customers (see below bullet on high density of vendors).

(2) Mobile phone receipts will be sent to the customer when they deposit their money. If the vendor

does not text us the deposit, pocketing the money, the customer will know when they don’t

receive a text message from us. This will be printed on every page of the catalog.

(3) A high density of vendors will be enlisted, such that every customer is no more than 15 minutes

from two vendors. That reduces fraud two ways:

a. To customers, the experience of our service can be compared across multiple vendors.

Many fraudulent activities would then be revealed by differences in vendor behaviors

observable to customers.

b. To us, outliers in any dimension, such as a high rate of robbery for a single vendor, would

indicate potential fraudulent activity to investigate.

(4) Cash pickups will be conducted when a certain amount of funds are with the vendor, rather than

at regular time intervals, to avoid predictability in pick-up patterns such that thieves won’t know

when vendors are holding the most cash. Pickups will also be as frequent as necessary to avoid

theft from vendors.

(5) Cash pickups will text the central office when they occur, and a receipt will be texted to the

vendor.

(6) Deliveries will be staggered, and texted to the customer. Also, delivery vehicles will be clearly

marked with our brand, making it publicly clear that a delivery has occurred.

(7) Customers need to be able to access our central office with complaints. One model of doing so is

sending representatives to hold regular e.g. monthly open hours where they will be present in a

given neighborhood at a time advertised in the catalog (all hours for all neighborhoods advertised

in a table in the back of the catalog). Alternatively, we can allow text requests for an on-site

customer service call where we reimburse the cost of the text message.

In markets where mobile payments are available, the text-message system of receipts is no longer

necessary as customers can transfer payments directly to us.

Back-end inventory and delivery

Our retail innovation is on the front-end, with the layaway, catalog, and local vendor elements. On the back-

end, we will operate like any other retailer. Goods will be purchased wholesale and stocked in central

warehouses, with locations and inventories optimized according to standard Operations practices. Cash

pickups will be conducted with dedicated in-house drivers as described above, and product deliveries to

the local vendor will be performed by either outsourcing to delivery companies or integrating our own

delivery service. These standard operational practices should be comparably straight-forward to implement

given the high density of customers in our urban markets. If we expand to rural markets, inventory and

distribution will have to be managed under a different model with likely trade-offs in some combination of

delivery time and cost (pricing).

Product Mix & Sourcing

Our product mixture on offer has three components: standard retail, exclusive retail partnerships, and

government partnerships. Catalogs will be replaced, with the old ones picked up, on a regular cycle such

as each month. The cycle date will be printed on each catalog, and old catalogs will be picked up upon

delivery of the new ones. When a product will no longer be offered, it is moved to a ‘deprecated’ section in

Layaway in India Darin O. Bellisario

9

the back of the catalog such that customers can still put money towards those products if they already have

done so.

We propose to initially allow customers to move their product credit between products at will; temptations

to expend savings prematurely, such as medicine and food, will likely not be present in our offerings.

Customer behavioral patterns after launch can be studied to alter this policy if necessary.

Basic Retail

Our core model is low-income durable good retail across diverse product segments. The specific selection

of goods will depend on local demand which we can initially evaluate with survey data and adjust with

expressed consumer demand. Goods can include for example:

Refrigerators

Generators

Solar panels

Air purification systems

Water purification systems

Television sets

Radios

Household tools

Common vehicle repair parts

Bicycles

Bulk-discounted detergents, building supplies, and other consumables.

Consumer electronics

Sourcing of goods e.g. what brands we carry will be optimized to consumer willingness to pay and wholesale

pricing. At least initially, we will not produce any goods internally.

Exclusive Private Partnerships

In addition to basic retail functionality, our unprecedented access to customers affords an opportunity for

us to add value to relationships with strong private brand partners, such as film production companies

looking for merchandise distribution opportunities. Exclusivity may not always be necessary, and will

generally be a negotiated trade-off with the margins we have to offer brand owners and suppliers, but has

a unique value to us beyond protecting marketshare; exclusive products build our brand as not merely the

only retailer our customers can afford (due to the layaway model), but rather a choice retailer with intrinsic

worth. In other words, it helps to prevent us from being over-identified with poverty. By analogy Macy’s

branded itself as a low-cost but premium-product provider in order to drive its layaway sales.

Government partnerships

Our distribution channels also allow us to help roll out government consumer subsidies. That provides not

only a potential source of revenue, but builds our relationship with both the government and the general

public. It contributes to our brand as a positive member of the local community, associating us with local

policies. This distribution could take the form of providing subsidized goods.

Trust, branding, and partnerships

Initial customer adoption relies exquisitely on their trust that we will deliver their goods, honestly represent

the goods, and stay in business. That relies on a brand of stability and honest business that we will

develop through a series of tactics:

Layaway in India Darin O. Bellisario

10

(1) A high density of vendors provides, in addition to the anti-fraud effects discussed above, multiple

sources of implicit validation of our presence.

(2) Partnership with a mobile phone carrier whereby we propagate their brand in our marketing

materials, including the catalog, in exchange for the positive association with a large, existent firm

we receive in our promotional campaigns (below). In other words, we place their logo in our

catalog and in our promotional materials to gain legitimacy while propagating their brand, aiding

their marketshare in a diffuse, competitive industry. We will have to select one mobile partner, but

that is not limiting to us in any way and indeed gives us leverage in that relationship.

(3) Very public promotional expenditures, e.g. billboards, bus-stop ads, ads in vendor stalls, and

physical temporary stalls we set up in customer neighborhoods to advocate for our product, all

serve to display that we are a legitimate company. In our early days, customers must be

inundated with our presence before our catalogs arrive in their stores. That up-front expenditure

is necessary to drive adoption.

(4) India-centric, or ideally locally-centric, branding through the marketing messages used and any

local public and celebrity figures that we are able to enlist to promote our business. We can

attract these endorsements with not only money but with our social impact message of poverty

alleviation and financial inclusion.

To summarize, we need aggressive public relations investment to establish the trustworthiness of our

brand. That is not the same as promotions aiming to convince consumers to use our product; the focus

should be on our brand, not directly on sales. The former more sustainably inspires the latter.

Values

We are stewards of people’s savings, which makes us stewards of their futures. As a result, every

stakeholder in our business – customers, investors, and politicians and regulators – demands that

we deliver social value; to build profits, our sales must correlate with social impact. For our customers,

they are placing their future in our hands, which means that to create sales we must first create trust. One

consequence of that is that long-term profitability, and hence investors’ interest, rests on customer

satisfaction. Investors with social impetus present an additional demand for social impact. Finally the

political apparatus can regulate us into oblivion at whim, so strong public support/relations is requisite to

mitigate political risk.

In each case, to maximize risk-adjusted cash flow we must have a positive social impact via our

sales; there must be a direct connection between the two. To achieve that, we have a series of policies

and principles governing our performance:

Our core policies & principles

1. We never misrepresent product benefits for the purposes of profit.

It can be tempting to take advantage of the limited education and access to information of

the poor to increase product sales or margins. For example, making a color TV look more

vivid in the catalog than it is in actuality. Resulting negative experiences undermine

customer trust, eroding long-term sales, and draw negative public relations which can

drive antagonistic policy-making.

2. Our job is to make our customers happier.

Service, time-translation of savings, and product accessibility drive customer utility, not

price control. As such, the better we understand our customers’ lives and aim to improve

them, the greater our revenues and the greater our profitability. This should manifest in

our service model, product selection, and promotional efforts.

3. Consumption that makes people happier makes an economy wealthier.

Layaway in India Darin O. Bellisario

11

Economic development is not just about entrepreneurship or increased production.

Helping people buy goods that give them more utility per dollar i.e. raise their quality of

life is an important part of economic growth. Poor customers deserve to pursue

happiness too, not merely base survival. Simultaneous to making consumers happier,

this consumption drives demand for higher value goods, creating a domestic market for

producers.

Revenues streams

We have two primary revenue streams: revenue from the sale of goods, and revenue from the ‘assets under

management’ or negative working capital.

Sale of goods

The back-end of our retail business model mirrors existing retailers; it is our front-end distribution and

financial service that provide a competitive advantage via access to customers that are currently excluded

from the market. As such, our cost objective is to maintain industry-average profit margins on goods,

focusing on revenue growth via customer access and service, not price competition.

As a result, if we are successful in reaching our customers, meeting their demand for savings towards

durable goods, we can deliver superior revenue growth compared to other retailers at similar profit margins.

Microcredit studies showing a shift in consumption towards durable goods also suggest that we may be

able to charge a price premium through our savings model. Taking a loan to buy a good implies a premium

on the price of that good.

Negative working capital

The time delay between the customers’ deposit of funds with us and the eventual delivery of the good can

be substantial – between a month and two years. As a result, our accounts receivable should exceed our

accounts payable substantially. That allows us to re-invest those funds in the intermediate period, just as a

traditional bank would with savings deposits. This steady-state asset pool we can, at the least, invest in

government debt at the risk-free rate of return for consistent income.

We could also exploit our distribution channels to invest in our vendors through credit-lines, providing

potentially a superior return. The ‘information costs’ of lending to our vendors are attenuated because we

are implicitly using our relationship with them, the commission they receive, as collateral against the loan.

Defaulting on a loan means losing our business, providing incentives to repay. Furthermore, our high

density of vendors may engender competition between them to attract customers, providing incentive to

tap into our credit program to expand their products, services, and facilities to draw more business.

Competition

Competition breaks down into two segments corresponding to the two areas of value we create: retail

substitutes and savings substitutes. In both areas we find competition limited, making the overlap of the

two needs even harder for our customers to fulfill with present alternatives, suggesting a strong value added

to our entry in these markets.

Retail substitutes

Urban transportation provides the urban poor with reasonable access to a relatively wide range of

socioeconomic environments and associated retail outlets. Without the savings constraints that are

resolved with our layaway model, our customers potentially have alternatives in retail stores, especially

Layaway in India Darin O. Bellisario

12

outlets (India has the highest number of outlets per capita in the world, 7 per thousand), that typically target

middle class consumers. Despite this theoretical possibility, in practice the Indian retail sector remains

nascent. Only 7% of India’s retail industry is ‘organized’ i.e. run by ‘modern’ enterprises, with the remaining

93% ‘unorganized’ such as the local vendors we are enlisting.23 That Indian organized retail sector grossly

lags other poor markets such as China (20%), Indonesia (30%), and Thailand (40%). Furthermore, the

existing organized retail is almost entirely limited to fashion, lifestyle, and food/grocery products. As a result,

penetration of retail into the durable goods products we propose appears, from macro data, to be limited.

Interviews with researchers familiar with the urban poor in Delhi and Mumbai corroborate limited access to

retail for durable goods.

Savings substitutes

Although financial inclusion has been a core objective of Indian policymakers and the central bank for a

decade now, it remains problematic. Mandates for banks to offer lower-regulatory-requirement (and hence

cheaper to service) accounts gained little traction, leaving India today with only 7.5% of the poorest 40% of

citizens saving money with a financial institution.24 As Rajesh Chakrabarti of ISB put it last year, “India’s

financial inclusion indicators, particularly in banking, put it below the median of countries, and bank

accounts are a first step to inclusion.” Mobile banking penetration has also remained low despite relatively

high mobile phone penetration in Urban environments, 25 with only 14% of Indians currently using any form

of mobile money (which could theoretically be used as a substitute for low-volume savings).26

Under these conditions our product provides one of the only opportunities for savings for the poor at all, let

alone ‘locked-in’ savings that can help drive commitment.

That situation may change however with Prime Minister Modi’s aggressive push for expansion of mobile

banking access. By August of 2015, his program is targeting the creation of 75 million new accounts.27

While a paltry amount in comparison to the total population of India’s poor, a successful program provides

a testing and proving ground for banks and telecom companies to refine their models for mobile banking.

Analogies

Our layaway model is adapted from the tactics used by department stores operating in poor urban, often

minority communities in the United States from the 1950s up through the 1980s. While there are no cases

of broad retail application of the model in emerging markets, a couple organizations have been attempting

similar models with a more narrow single-product scope.

myAgro

myAgro is a nonprofit currently operating in Mali using a layaway model through mobile phones and local

rural village vendors, similar to us, to sell agricultural inputs (fertilizer and seed) on layaway. Although a

nonprofit, removing the growth incentive that comes with private investment, and focused on agricultural

products, we may be able to learn from myAgro’s implementation. At present, they are at an early stage of

development, still establishing operations, so no outcomes are available for comparison.

23 Booz & Co. Successful Innovations in Indian Retail. 2013 24 2014 World Bank Findex data. 25 The lower penetration of mobile phones in rural environment, 42% in 2013, may explain in part the limited adoption; in previous cases, such as M-Pesa in Kenya, a core value proposition was application of mobile banking to money transfer between urban poor and their rural friends and family. 26 Ernest & Young. Mobile money — the next wave of growth. 2014 27 Wharton School of Business. Financial Inclusion in India: Moving Beyond Bank Accounts. Knowledge @ Wharton. Sept. 14 2014

Layaway in India Darin O. Bellisario

13

KickStart

KickStart is a nonprofit that takes advantage of the ubiquity of M-Pesa in Kenya to sell water pumps to

farmers on a layaway model. KickStart sends representatives to local agricultural suppliers who sell fertilizer,

seed, tools, etc. and sells them a couple pumps to theoretically sell out of the shop but in practice are there

to entice farmers. The representatives then provide periodic demonstrations of the product at the shops to

show farmers its utility. They then offer to sell the pumps via a layaway program, sending payments via M-

Pesa to KickStart until they provide enough to receive the pump.

KickStart piloted the program in 2010, two years later rolling it out more broadly. Unfortunately, only 350

farmers have used the program since then, in comparison to over 200k pumps KickStart sold by more

conventional means. From their 2014 report: “from farmer feedback, we learned that there is still a general

lack of trust in mobile savings in Kenya which offered some insight as to why the program has not spread

more quickly.” They are currently piloting a Rent-to-own model as an alternative.

The experience of KickStart highlights the importance of trust in the layaway model. Our targeting (selection

of customer segments to address), promotional tactics, and business model must focus on overcoming the

trust barrier that will make or break the business.

Pilot Financials

Steady State

To establish basic feasibility, we estimate the balance sheet of projected pilot operation. We estimate the

cost structure of the pilot program in a simplified manner as below. As a proxy for our unknown basket of

products, we chose a single product – a budget LG color TV retailing for 3575 Rupee or $57 at outlets – as

representative of our cost elements and margins.28 We estimate costs based on India urban national

averages or, where available, Mumbai data. We approximate sales volume at 1,000 units per month, with

customers providing layaway deposits uniformly over 12 months. Returns on accounts payable

reinvestment are approximated as 0.1% real risk-free rate based on US TIPS. Alternatively, adopting the

insurance industry norm of stock market investment at a 4-9% real risk premium in a well-diversified portfolio

is feasible. Any risk-return profile in between can be achieved by a mixture of stocks and bonds, so these

two extremes provide useful benchmarks.

Table 3. Annual Steady-State Pilot Program Balance Sheet (all values USD)

Monthly Per Unit Sales Annual - 1k

units/mo Annual - 5k

units/mo Annual - 10k

units/mo Notes

Revenues Gross Sales Revenue - 64.98 779,760 3,898,800 7,797,600 a Accounts payable - 28.50 342,000 1,710,000 3,420,000 b AP reinvestment revenue - Risk Free

- 0.03 342 1,710 3,420 c

AP reinvestment revenue - Market Risk

- 1.43 17,134 85,671 171,342 d

Back-end costs

Wholesale Purchase Price - 48.45 581,400 2,907,000 5,814,000 Carrying Cost - 0.03 348 1,740 3,480 e

Logistics and Operations - 1.95 23,393 116,964 233,928 f Delivery Costs

Delivery Service - 0.50 6,000 30,000 60,000 g Text Messaging - 0.06 768 3,840 7,680

Promotional Costs Static (e.g. billboards) 4,754.31 - 57,052 57,052 57,052

Dynamic (manned stalls) 9,600.00 - 115,200 115,200 115,200 Vendor Commission - 3.25 38,988 194,940 389,880 h

28 Estimates based on data from Kaunsa.com, infibeam.com, Flipkart, Hindustan Unilever, PNG, Whirlpool, and Business Standard.

Layaway in India Darin O. Bellisario

14

General Administration 25,000.00 - 300,000 300,000 300,000 Net Costs 39,354.31 54.24 1,123,149 3,726,736 6,981,220

Net Profit - risk-free investment

(343,047) 173,774 819,800

Net Margins - risk-free investment

-44% 4.41% 10.47%

Net Profit - risk premium (326,254) 257,735 987,722 Net Margins - risk premium -42% 6.61% 12.67%

Notes a Online retail price with a 14% premium for access and savings service benefits b Average deposit amount at a uniform rate over 12 months c 0.1% real rate, US TIPS d 5% risk premium for diversified stock portfolio e 18 rupee per year with industry average retail turnover of 10x f industry average 3% of top-line g Delivery wage $2/hr/person, 4 package deliveries per hour h 5% of sale price

We can see that to achieve a tidy profit margin we must, with this rough calculation, invest at the market

risk premium and sell ~5k units per month on average, a substantial feat. In Mumbai, that translates to

having to sell at least one product per year to one in every 1,000 poor citizens. In that context this volume

is theoretically achievable, but certainly not a guaranteed windfall.

The key challenge is that retail margins are so tight that the space for requisite promotional investments is

limited unless volumes are enormous. That said, promotional costs may diminish with time as our brand

becomes established, improving margins substantially. Even at 10k units/mo sales volume, promotional

costs account for 3% of our margins. The negative working capital provided by the layaway model does

improve margins substantially if we can achieve 5% return on that capital, providing 2.5% additional profit

margins.

One consequence of these observations is that this business may be best implemented as a new business

unit through an existing multinational retailer, bringing the requisite operational expertise to keep back-end

costs under control.

Go-to-market capital requirement

The above estimates are at steady state; at launch, revenues will gradually rise from zero but costs will

essentially be the same. We can estimate capital requirements for the pilot program therefore by

approximating a linear 24 month ramp-up of sales volume from $0 to steady state, with costs conservatively

estimated by fixing them at the steady state level. Finally we add on startup costs. Given how rough our

estimate is, we do not include the cost of capital discounting over the 24 month period.

Table 4. Ramp-up capital requirements (all values USD)

24 month costs 16,862,599

24 month revenues 8,481,600

capital requirement 8,380,999

We therefore require an initial capital injection of at least $8.4m for the pilot program.