law society of kenya savings & credit co-operative society...

TRANSCRIPT

FINANCIAL REPORTS

LAW SOCIETY OF KENYA SAVINGS & CREDIT CO-OPERATIVE SOCIETY LIMITED

www.lsksacco.co.ke CS/4676

ANNUAL REPORT and FINANCIAL STATEMENTS 2016

LSK SACCO LTD

VisionTo be an exemplary Sacco for members of the legal profession and affiliated persons

working in the administration of justice

MissionTo mobilize funds, lend to the members and avail other financial services at

affordable and competitive rates in accordance with the co-operative principles

Slogan“Your partner, your treasure, always there for you”

Core ValuesThese are the principles that guide LSK Sacco internal conduct as well as its

relationship with the external world. The following core values are championed by the board and are adhered to by the Sacco’s staff and the members.

Self help Commitment Honesty Selflessness

Self responsibility Respect Integrity Discipline

Openness Honour Social Solidarity

Innovation Dedication Responsibility Timeliness

Trust Equality Excellence Accountability

SOCIETY INFORMATION 5

NOTICE FOR THE AGM 2017 6

MINUTES OF LSK SACCO ANNUAL GENERAL MEETING 2016 7

CHAIRMAN’S REPORT 14

SUPERVISORY COMMITTEE REPORT 17

FINANCIAL REPORTS FOR THE YEAR ENDED 31ST DECEMBER 2016 20

STATEMENT OF THE BOARD OF DIRECTORS RESPONSIBILITIES 20

REPORT OF THE INDEPENDENT AUDITORS 21

STATISTICAL INFORMATION 22

STATEMENT OF COMPREHENSIVE INCOME 23

STATEMENT OF FINANCIAL POSITION 24

STATEMENT OF CHANGES IN EQUITY 25

STATEMENT OF CASH FLOW 26

NOTES TO THE FINANCIAL REPORTS 27

BUDGET 2016 ANALYSIS AND 2017 - 2018 PROPOSALS 33

NOTES TO THE BUDGET 35

BYLAWS AMENDMENTS SCHEDULE 2017 36

Table of Contents

Interest rates: 1% per month on a reducing balance.

Deposit Multiplier: 3 times of members total deposits

Loan Securities

• Owndeposits •ChattelsmortgageonMotorVehicles

• Guarantors’deposits •Titledeed

EDUCATION LOANS

Maximum amount of Ksh. 20,000,000Repayment period of up to 84 months

Maximum amount of Ksh. 500,000Repayment period of up to 24 months

OUR CREDIT PRODUCTSDEVELOPMENT LOANS

Joseph MakumiSecretary

Nancy KangetheMember

Boniface mutwiriMember

LSK Sacco Annual Report and Financial Statements 2016 | 5

SOCIETY INFORMATION AS AT 31ST DECEMBER 2016

THE MANAGEMENT AND SUPERVISORY COMMITTEE MEMBERS

Supervisory Committee

Ag. General Manager Michael N. WangangaP. O. Box 6740-00100 Nairobi

Registered office LSK Sacco LimitedCrawford Business Park 3rd FloorState House RoadP. O. Box 6740-00100Nairobi

Auditors

Victor Mutisya & Company Certified Public Accountants (K)P. O. Box 28421-00200Nairobi

Principal Bankers Co-operative Bank of Kenya Kimathi Street Branch P. O. Box 7512-00200Nairobi

Justus M. Munyithya Chairman

Salome MuhiaMember

Kellen G. Njue Secretary

George AkotoMember

Collins WanderiChairman

Lawrence MugambiTreasurer

Gladys WamaithaMember

Caleb NadebuVice Chairman

Dominic MbigiMember

Management Committee

LSK Sacco Annual Report and Financial Statements 20166 |

NOTICE FOR THE AGM 2017

TO ALL MEMBERS

RE: ANNUAL GENERAL MEETING

Notice is hereby given that an Annual General Meeting (AGM) of LSK Sacco Ltd is convened and will be held on Saturday 18th March 2017 at The 680 Hotel, along Kenyatta Avenue starting at 9.00 a.m.

AGENDA:

1. To note attendance and apologies.

2. To note and adopt the minutes of the last Annual General Meeting held on Saturday, 12th March 2016.

3. To consider the Chairman’s report for the year 2016.

4. To consider the Supervisory Board report for the year 2016.

5. To receive and note a list of loan defaulters.

6. To receive, consider and adopt the Financial Reports for the period ended 31st December 2016.

7. To approve payment of interest on deposit at 9% per annum (on weighted average) and the same are credited in each member’s deposit account.

8. To authorise Management Board to appoint Auditors for the year 2017 – 2018 and fix their remuneration.

9. To consider and approve the estimates of income and expenditure for the year 2017-2018.

10. To increase the borrowing ceiling to a maximum of Kshs. 20,000,000

11. To authorize/grant the Sacco borrowing powers to a Maximum Kshs. 1,000,000,000

12. To approve payment of honorarium of 2% on profit before tax to the members of the Management and Supervisory Board as a token of appreciation.

13. To amend LSK Sacco by-laws as per the attached proposal.

14. To elect pursuant to rule 28(1) of the Co-operatives Societies Rules three (3) members of the Management Committee following to the retirement of Dominic Mbigi who is NOT offering himself for re-election and Kellen Njue who IS OFFERING herself for re-election; and the resignation of Nancy Kangethe. A member desiring to offer himself/herself for election (except one seeking re-election) should pick and return a dully filled up Nomination Form to the Sacco office at least seven (7) days before the AGM.

15. To elect one member of Supervisory Board following the retirement on rotational basis of Collins Wanderi who IS OFFERING himself for re-election. A member desiring to offer himself/ herself for election (except one seeking re-election) should pick and return a dully filled up Nomination Form to the Sacco office at least seven (7) days before the date of the AGM.

16. To transact any other business whose notice will have been given to the Secretary fourteen (14) days prior to the date of the Annual General Meeting.

By the order of Management Board

KELLEN G. NJUEHON. SECRETARY

CC: County Co-operatives Officer Nairobi Province P.O. Box 30202 Nairobi

LSK Sacco Annual Report and Financial Statements 2016 | 7LSK Sacco Annual Report and Financial Statements 2016 | 7

Agenda 1: To Note Attendance and Apologies

Attendance

Member No.

Name

47 Dorcas Nanjero

155 Nancy Kangethe

161 Nancy Shikuku

210 Maurice . O Omuga

212 Dominic. N Mbigi

240 Alice Kimani

246 Gladys Karanja

346 James Okao

411 Mr. Joseph Kithinji

446 Erick Omariba

453 Monica M. Nzive

470 Lawrence Mugambi

471 Maryanne Mung’ara

476 George Mutua

478 Leonard Kimathi

529 Collins Wanderi

539 Ashitiva B. Mandale

547 Wilberforce L. Khalwale

557 Munyithya Justus

560 Francis Moriasi

576 Cecilia Mwangangi

611 Callen Masaka

628 Muma Andrew

632 Samuel Mundia

646 William Githara

693 Derek Ndonye

707 Maurice Lugadiru

716 E. Njaramba Gichuki

721 Pamela Opiyo

Member No.

Name

723 Benjamin Musyoki

724 Mbuthia Njiru

736 Stephen Saenyi

3376 Lilian Avisa

775 Japheth Mwalimu

801 Noah Kiptoo

860 Solomon Mugo

897 Ndegwa Wahome

925 Gladys Gichuki

933 Pwoka Godfrey

971 John Kimathi

979 James J. Joroge

980 Isaiah Mandala

995 Kellen Njue

1003 Andrew Ombwayo

1015 Chege Njoroge

1021 Nyawara Joshua

1031 John Karigi

1036 Luciah W. Maina

1050 Godfrey Mutubia

1066 Gibson Maina

1080 Ibrahim Lubia

1083 Anne M. Ashitiva

1091 Gilbert Kariri

1095 Carol Wacheke

1109 Beatrice Odhiambo

1117 Rehema Mbula

1130 Joseph H. Otieno

1167 Joyce Mukururi

1177 Simon Mbinda

1211 Proscovia Kapiriri

1262 Johnstone M. Kieti

MINUTES OF LSK SACCO ANNUAL GENERAL MEETING HELD ON SATURDAY 12TH MARCH 2016 9.00AM AT SIX EIGHTY HOTEL NAIROBI.

The Chairman called the meeting to order at 9.30am. After confirmation of quorum the meeting started with a word of prayer from Cecilia Mwangangi Member Number 576.

Member No.

Name

1271 Rindley Nyambura

1284 John Akado

1336 Nadebu Caleb

1338 Huldah Ogeto

1359 Makumi Joseph

1513 Hasnah Mbone Mudeizi

1516 Salome Muhia

1560 Stephen Okello

1561 Jane Akeyo Miregi

1590 Daniel M. Maithya

1608 Anne W. Kamau

1624 Maurice Ogongo

1637 Tom Nkonge

1669 Roselmelda Opanga

1678 James Yuka

1707 Godfrey Wafula

1712 Emmanuel .M. Mutuku

1713 Job O. Ochieng

1717 Walter Omoke

1739 Vincent .W. Milimu

1740 Kizito Mukabwa

1755 Sylus Minda

1770 Njeru Ithiga

1772 Samuel Kinyua Ndege

1778 Johnstone Nzivu

1786 Boniface .K. Mutwiri

1814 James Igati Mwai

1828 Kenneth Maingi

1834 Gabriel Peter Omondi

1842 Florence Waithaka

1843 Muema Kilonzo

1982 Chris Kinoti

LSK Sacco Annual Report and Financial Statements 20168 | LSK Sacco Annual Report and Financial Statements 20168 |

Member No.

Name

1870 Mugambi Laichena

1896 Maureen Atieno

1899 Geoffrey Eric Wesonga

1916 Rosalia Nzuki

2264 Samuel Mwangi

1930 Sammy Mutwanyaa

1938 Elizabeth Kiarie

1970 Emma Wanza

1973 Daniel Muriungi

1982 Chris Kinoti

1993 Rashid M. Makoti

1997 Nelly Mutungi

2004 Carolyne Njeri Waweru

2010 Calleb J. Onguto

2021 Ruth Kamau

2033 Justus Mutia

2046 Jackson Omwenga

2057 Joseph K. Ng’ang’a

2064 Peter Okelo

2067 Samson Kaloki

2101 Harrison Machio

2115 Samuel M. Kamau

2116 Alex Ngungi

2128 Michael Muchemi

2140 Gladys Muhuri

2158 Gitonga Kamiti

2159 Brown M. Kairaria

2198 Grace Musa

2236 Serah Akinyi

2236 Geoffrey Togo

2255 Wycliffe Onsongo

2279 Joseph Okumu Jagero

2307 Rodney Oluoch

2317 Wycliffe Kitigln

2318 Ruth Wanyonyi

2348 Paul B. Motanya

2364 Musyoki Masai

2376 Linda Awiti Osingo

2377 Benjamin Mailu

2472 Daniel Nkere

2514 Elizabeth H. Ogola

2516 Njeri Onyango

2526 Damaris N. Munyua

Member No.

Name

2626 Mary Njagi

2639 Dennis Murithi

2656 Hellen Memba

2671 Brenda N.Kamau

2680 Achieng Valentine

2694 David N. Njoroge

2719 Beatrice N. Mwaura

2726 Cosmas Mbuvi

2751 Anthony Lusenaka

2806 Lennah Nzioki

2829 Nicholus Kivinda

2835 Onyata Abrahim

2865 Alexander Musungu

2876 James Obam Osamo

2896 Egline Cheruto

2910 Marie Kapiyo

2918 Arthur Muiru

2929 Sophia Kimani

2934 Jeremiah Samba

2956 Ngari Nthumbi

2974 John Omudanga

2993 Otieno Evans

2994 Kusimba Joel Ashiachi

3005 Agnes Atieno

3006 Rahab Wambui

3010 Stella Amisi

3018 Beatrice Kariuki

3044 Ndeti Peninah

3045 Peninah Mutungi

3046 Kavune Nicholas

3048 Adhiambo Joyce

3061 Gad Gathu

3077 Duncan Musya

3109 Oscar Avedi

5000 Cyrus Nyamwamu

3141 Joash Ratemo

3142 Shijenje Johnson

3181 Robert Sewe

3216 Agnes Njeri Ndungu

3228 Esther Mathenge

3309 Kevin Kinyanjui

3317 Vincent K.B. Akarah

3352 Omwenga Perister

Member No.

Name

3442 Caroline Muchiri

3451 Nyambura Chege

3459 Gilbert .S. Wamalwa

3509 Mark Ndung’u

3515 Jane Jambukira

3522 Evans Ketoo

3526 Eunice Mola

3532 Florence Owoko

3544 Simon Kathumbi

3567 Masaviru Nelson

3611 Njoroge Paul

3623 Getrude Mwongera

3640 Lucy Ngari

3650 Martin Wambu

3651 Mathias Mboya

3664 Joyce Rupia

3781 Scola Nduku

3793 Rose Mercy

3843 Muhoro Ceciliah

3930 Lydia Chebiwot

3937 Jared Juma

4038 Emily Matano

4054 Morris Kaburu

4056 Hudson Chanzu

4092 Helen Ngessa

4117 Lyna Moraa

4120 Maureen Wambui

4141 Jackson Awele

4158 Alex Mbue

4175 Gideon Kimotho

4186 Shem A. Waguda

4189 Mumo Kimeu

4230 Peter Mwendwa

4237 Sharon E Mwakugu

4238 Moses Munoko

4246 Mose Isaac Onyore

4250 Hillary Isiaho

4253 Linet Maina

4257 Judy Ratanya

4260 Nornael Okelo

4286 Malowa Barbara

4287 James Oyuke

4289 Felix Odhiambo

LSK Sacco Annual Report and Financial Statements 2016 | 9LSK Sacco Annual Report and Financial Statements 2016 | 9

Member No.

Name

4312 Charity G. Kathurima

4337 Mokaya Orina

4364 Zena A. Rashid

4387 Muli Debora Ndunge

4398 Emmanuel Nzuku

4399 Peter Muthoni

4415 Muendo M. Uvyu

4427 Rosemary Kamathu

4444 Kenyanchui Moses

4465 Faith W. Muthee

4483 Vera N . Omondi

4491 George Wandati

4506 Rahab Wambui

4512 Kiarie Peter Mungai

4522 Amos Okungu

4536 Queenton Ochieng

4553 Okimaru Sarah Amoit

4563 Bradrick L. Mwangu

4564 Norbert Jude

4583 Margret Kariuki

4607 Mary Maina

4675 Joseph Nyagira

4693 Brenda Nandwa

4730 Sawe Luka Kipkemoi

4734 Oyuko Amos Ogutu

4754 Jaffer Markus

2480 Michael Wanganga

4800 Mary Njagi

3979 Isaac Kazungu

4895 Benson Kipchichir

4896 Davis Nyagaka

4917 Daniel Gichuki

4954 Dulo Enricah

4981 Kennedy Amunga

5014 Ann Mbugua

5025 Edna Nkirote

5040 Lenah Mwangi

5071 Denis Mutembei

5072 Oruo Chrispine Noel

5132 Peter Siva

5133 Adelaide Masitsa

5163 Gordon Abuya

5182 Solomon Moimbo

Member No.

Name

5244 Wilfred Naumbizi

5255 Edith Onyango

5256 Philip Kiptoo

5282 Emily Tenge

5293 Jacquiline Akello

5310 Emma Nudi

5320 Daniel Ouma

5391 Walter Anderi

5404 Ndanu Edwin Isaack

5405 Geofrey Anami

5410 Mwalimu Charles

5431 James G. Munyaka

5454 Jacinta Mukono

5497 Grace M. Mutemi

5504 Erick Mwoki

5509 Allo Rodgers Omondi

5519 Andrew Mshindi

5540 Njako Priscilla Mumbua

5551 Paul Kiarie

5557 Samwuel Gichuki

5599 Gerard Brian Otieno

5601 Silas Mbogo Gitari

5602 Kumali Jack Shikuku

5603 Vincent Onyancha

5605 Jean Ongallo

5615 Ngire Aduol Terry

5616 Martha Kiilu

3000 Helen Githinji

5620 Ibrahim Kiage

5620 Ibrahim Oenga

5641 Ben Indimuli

5664 Jackline Moraa

5686 Feisal O. Mulama

5689 Ojiambo Osunga

5802 Fridah Muthiani

5846 Kennedy Mwinamo

5856 Nahashon C Njoki

5883 Evans Oninyo

5888 Samuel Ogosi Ogosi

5889 Robert Muga

5894 Daniel Ndung’u

5903 Nzuki Musyoki

Absent with apology.Name Member No.

1. Michael Oloo 3356

2. Margret Ndwiga 391

3. Emma Ogola 3403

4. Jemimah Keli 4064

5. Alice Kasiki 4756

6. Lily Musinga 1573

7. Henry Kurauka 600

8. Cletus Kitambaa 4755

In attendance1. Luc y K imani – M in i s t r y o f

Industrialization & Enterprise Development

2. Catherine Wambua – Ministry of Industrialization & Enterprise Development

3. Victor Mutisya – External Auditor.

Agenda 2: To note and adopt the minutes of Last AGM held on 12th March, 2015.

The minutes were proposed to be adopted by Alexander Musungu Member Number 2265 and seconded by Njeri Onyango member number 2516.

Agenda 3: To consider Chairman Report for the year 2015.

The Chairman presented his report which highlighted the following achievements and challenges in the year 2015.

A. Management of the Sacco

The Management and Supervisory c o m m i t t e e s h a d w o r k e d harmoniously within the year to ensure the Sacco’s objectives were achieved.

B. Performance.

i. 572 members were recruited in 2015 bringing the total membership to 5798 as at 31st December, 2015.

ii. Deposit levels increased by 31.5% from 565 million in 2014 to 743 million in 2015.

LSK Sacco Annual Report and Financial Statements 201610 | LSK Sacco Annual Report and Financial Statements 201610 |

iii. Total Loans disbursed during the year ended 2015 was 759 million. This represented an increase of 28% compared to loans disbursed in 2014.

iv. Society income increased by 25,463,330 from 66,494,313 in 2014 to 91,129,085 in 2015.

v. During the year the Sacco procured a modern Integrated Management Information System (Navision 2015).We are in the process of implementing the process which will improve on our efficiency in our service delivery and put the Sacco in the same platform with other financial institutions.

vi. The Sacco was able to hold successful education days in Nairobi and Kisumu.

The following challenges were highlighted:

New Members-The chair noted that only 572 members joined the Sacco in 2015 which was below the Strategic plan target of 1,500 per year. Members were requested to do referrals to prospective members.

Non-performing Loans-The chair acknowledged that non performing loans have become a challenge to the Sacco and indicated that credit appraisal rules have been tightened. Members were requested to ensure loans that they have guaranteed were paid.

The Chairman report was adopted after being proposed by Stephen Kibunja member number 77 and Seconded by Maureen Odhiambo member number 1896.

Agenda 4: To receive and consider Supervisory Board report for 2015

The Chair of the Supervisory Committee Nancy Shikuku member number 161 presented the report which highlighted the following;

i. The Management Committee had conducted Sacco affairs well.

ii. The recruitment of new members in to the Sacco was 572 below the target of 1,500 as per the Strategic plan. Members were urged to assist in recruitment by referring eligible members.

iii. The Sacco need to acquire its own Pay Bill number.

iv. The Committee recommended a check off system for interested salaried member; this would boost the Sacco’s deposits.

v. The emergency loans were not processed within the recommended time line of 48 hours

and committee recommended that necessary measures to be put in place.

vi. The Customer Relationship Officers were commended for being instrumental in debt recovery. The committee indicated that appropriate action had been taken on Committee members who had defaulted on their loans.

vii. The procurement of Management Information System process was within the law and the Sacco got the best bargain. The implementation process should be fast tracked.

viii. Lost files and benevolent funds matters are still pending from previous AGM.

Jackson Awele member number 4141 raised concerns on missed recruitment targets and wanted to know the underlying reasons and the strategies to win new members. The Education Committee informed the members that the CROs program will be revamped to ensure that the targets were met. Customer Relationship Officers had attended all LSK organized forums, and have been dispatched to all regions of the country to ensure members are recruited. The Sacco had also organized successful Education days in Kisumu and Nairobi.

Joseph Otieno member number 1130 wanted to know the progress on lost files. He was informed that the case had been reported to the Anti Banking Fraud unit and the statements had been recorded with police. The matter was still under police investigation.

Andrew Muma member number 628 requested for clarification on the Mpesa Pay Bill used by Sacco visa vis Mpesa pay bill suggested by Supervisory Committee. The Supervisory Committee chair informed the members that the one in place is provided by Co-operative bank and attracts a surcharge. The Treasurer highlighted the risks associated with the pay bill number as currently the risk is handled by the bank. The implementation of the new system will minimize the risk.

The Supervisory Committee report was adopted after being proposed by Rindley Nyambane Member number 1271 and seconded by Queenton Ochieng member Number 4536.

Agenda 5: To receive and note the list of defaulters.

The list of defaulters was presented to members. Members were requested to note the members in the list and assist in collection of defaulted amount.

LSK Sacco Annual Report and Financial Statements 2016 | 11

A concern was raised on a Committee Member who appeared on the defaulters list. The Chairman explained that the appropriate action had been taken and that the said member had resigned from the Management Committee.

Agenda 6: To receive, consider and adopt the financial report for the period ended 31st December 2015.

The Auditor Mr. Victor Mutisya confirmed that the financial account gave the true state of the society financial status as at 31st December, 2015.

The Highlights included:-

i. The revenues for year 2015 grew by Ksh.25,463,330 from Ksh.66,494,313 in 2014 to Ksh.91,957,643 in 2015

ii. The year total expenses grew to Ksh.81, 849,486 compared to 61,172,713 in 2014.

iii. Total assets grew by Ksh.221, 841,805 from Ksh.648, 718,306 in 2014 to Ksh.870, 560,111 in 2015 which represents 34.2% growth.

iv. The loan book grew from Ksh.604238, 044 in 2014 to Ksh.759, 860,586 in 2015 which represent a 25.7% growth.

v. Member’s deposits grew from Ksh.32, 956 in 2014 to Ksh.47, 845,245 in 2015 representing a 3.7% growth.

Members raised concerns on increase on administrative expenses and they were informed that this was attributed to the growth of the Sacco.

Members also inquired on why the software was written off. They were informed that the previous system was inadequate to meet the Sacco needs and was not customizable.

Members also raised concerns over why the investments in Equity market had remained constant. They were informed that the management had made a strategic decision not to invest in the Equity market due to the huge investments such as purchase of an ERP system within the year.

The financial statements were adopted after being proposed by James Joroge member number 979, and seconded by Gilbert Maina Kariri Member Number 1091.

Agenda 7: To Approve payment of interest on deposit as at 9% per annum (on pro rata basis) and the same be indicated on member’s deposit account.

The proposal was approved after being proposed by Johnstone Kioko Nzivu member number 1778 and seconded by Maurice Lugadiru member number 707.

Maurice Lugadiru proposed that members be allowed to choose if they want to recapitalize their interest on deposits or receive cash. It was suggested to be a motion for 2016 Annual General Meeting.

Agenda 8: To authorize Members of the Management Board to appoint auditors for the year 2015-2016 ad fix their remuneration.

The proposal was approved after being proposed by Maurice Omuga member number 210 and seconded by Joyce Mukururi member number 1167.

Agenda 9: To consider and Approve the estimates of Income and Expenditure for year 2016-2017.

The proposal was approved after being proposed by Wilberforce Kamala member number 547 and seconded by Joseph Kithinji member number 411.

Agenda 10: To increase the borrowing ceiling to a Maximum of Kshs. 15,000,000

The proposal was approved after being proposed by Maurice Omuga member number 210 and seconded by Brown .M. Kairaria member number 2159.

Agenda 11: To Authorize /Grant Sacco borrowing powers to a maximum of Kshs.1, 000,000,000

The proposal was approved after being proposed by Ndegwa Wahome member number 897 and seconded by Alice Kimani member number 240.

Agenda 12: To approve payment of honorarium of 2% on profit before tax on members of the Management and Supervisory Committees as a token of appreciation.

The proposal was approved after being proposed by Maurice Omuga member number 210 and seconded by Njeri Onyango member number 2516.

A member raised a concern on fact that the Committee members were receiving Sitting allowance and hence no need for the honorarium and suggested it to be struck out.

LSK Sacco Annual Report and Financial Statements 201612 |

The Chair explained that honorarium was a token of appreciation to the Management and Supervisory Committee and it ’s pegged on the actual performance of the Sacco.

Members also enquired whether a member of the Management Committee who was in default would be paid the honorarium allowance. It was confirmed that he would not be paid since he had been suspended from the Management Committee .

Agenda 13: To approve payment of sitting allowance of ksh.5, 000 for Board meetings and Ksh.3, 000 for committee meetings allowance paid net of all taxes with effect from May 2015.

The proposal was approved after being proposed by Maurice Omuga member number 210 and seconded by Njeri Onyango member number 2516.

Agenda 14: To elect three retiring members of the Management Board pursuant to Rule 23 of Co-operative Societies Act to the effect that three members retire each year by rotation. Mr. Caleb Nadebu and Mr. George Akoto are retiring and offering themselves for re-election. Mr. Henry Kurauka is retiring and not offering himself for election.

The Elections were presided over by the Cooperative officers Lucy Kimani and Catherine Wambua.

There were two categories of candidates; Primary (Advocates) and secondary (None advocates). The primary were vying to fill two positions while the secondary members had one position.

Caleb Nadebu vying in the secondary position was re-elected unopposed as his only opposer Japheth Gavala Member number 1724 did not turn up. He was proposed by Ibrahim Wafula member number 1080 and seconded by Caroline Njeri Waweru member number 2004.

There were 7 candidates for the remaining two positions:

i. George Akoto Proposed by Terry Aduol member number 5615 and seconded by Benjamin Musyoki member number 723.

ii. Boniface Mutwiri proposed by Roselmelda Opanga member number 1669 and seconded by Felix Odhiambo member number 4289.

iii. Jackson Awele proposed by Njeri Onyango member number 2516 and seconded by Isaiah Orina member number 4347.

iv. Nancy Shikuku proposed by Alice Kimani member number 240 and seconded by Callen Masaka member number 611

v. Andrew Muma proposed by Johnstone Kioko member number 1778 and seconded by Barbara Achieng member number 4286.

vi. Caleb Onguto proposed by Ndegwa Wahome member number 897 and seconded by Sarah Amoit member number 4553

vii. Dorcas Nanjero proposed by Maurice Omuga member number 210 and seconded by Zena Rashid member number 4364.

The election started by members being asked to raise their hands for their most preferred candidates. However during the exercise, some members raised concerns over the credibility of the results and some members suggested secret ballot.

The Co-operative Officer Lucy Kimani proposed a vote between voting by show of hands and by secret ballot.

Voting by secret ballot was proposed by Maurice Omuga member number 210 and seconded by Njeri Onyango Member number 2516.

Voting by show of hands was proposed by Caroline Waweru member number 2004 and seconded by Rosemeilda Opanga member number 1669.

A vote was taken on secret ballot versus the show of hands systems. A majority of the members preferred the secret ballot.

Members were given each 2 ballots to elect two members to the Management committee. The results were as follows;

i. George Akoto – 170

ii. Boniface Mutwiri – 132

iii. Andrew Muma – 75

iv. Jackson Awele – 59

v. Nancy Shikuku – 46

vi. Dorcas Nanjero – 31

vii. Caleb Onguti – 17

viii. Spoilt votes – 38

George Akoto and Boniface Mutwiri were elected to the Management Board after garnering the highest and second highest number of votes.

LSK Sacco Annual Report and Financial Statements 2016 | 13

Agenda15: To elect pursuant to rule 28(1) of the Co-operatives Societies Rules one member of Supervisory Board following the retirement on rotation basis of Mrs Nancy Shikuku who is offering herself for re-election. There were two candidates for the vacant position. These were:

i. Salome Muhia was proposed by Alice Kimani member number 240 and seconded by Ndegwa Wahome member number 897.

ii. Callen Masaka was proposed by Peter Mwangi Muthoni member number 4399 and seconded by Francis Moriasi member number 560.

Members were given each 1 ballot to elect 1 member to the Supervisory Committee. The results were as follows:

i. Salome Muhia – 141

ii. Callen Masaka – 130

iii. Spoilt votes – 12

Salome Muhia was declared elected to the Supervisory Committee after garnering the highest number of votes.

Agenda16: To transact any other business whose notice will have been given to the Secretary fourteen (14) days prior to the date of the Annual General Meeting.

The Secretary confirmed that no notice had been received.

The Chairman recognised the presence of Chancery Wright Insurance Brokers.

There being no other business the meeting ended at 3.00 p.m.

Confirmed By

Justus M. MunyithyaChairman

Kellen G. NjueHon. Secretary

LSK Sacco Annual Report and Financial Statements 201614 |

On behalf of the LSK Sacco Management Committee, it is my great pleasure to welcome you all to our Annual General Meeting 2017. We have converged here on this day in order to review our past year’s performance and to project our future. I wish to thank everyone for their support in making LSK Sacco what it is today. Let me take this opportunity to make some remarks and observations regarding our society’s performance in the year 2016.

SACCO PERFORMANCE AND REVIEW OF OPERATIONS

Dear members, the Society continued to post good results, despite many challenges in the operating environment. Below are some of the highlights of the key areas.

1. Sacco RevenueThe total income in 2016 increased to Kshs.116, 346,612 from Kshs. 91,957,643 realized in 2015 an increase of 27%. Our main income which is interest on loans income grew by 24% to Kshs. 95,601,999 from Kshs. 77,339,162 in the year 2015. Other incomes include interest income on call deposits and fixed deposits with KUSCCO and CIC totaling Kshs. 4,373,096.

2. MembershipOur membership grew to 6,434 members as at 31st December 2016; up from 5,809 members in 2015 a total of 636 new members. The Management Committee is continuing to invest resources in recruitment of new members to meet our annual target of 1,500 members. I appeal to everyone to assist us in recruiting our spouses and employees in order to grow our Sacco.

Figure 1 – Membership growth

Members

2010 2012 20142011 2013 2015 2016

7000

6000

5000

4000

3000

2000

1000

0

3. Member deposits and assets Our deposits grew by 26% from Kshs 743,600,350 million in 2015 to Kshs 934,119,547 million in 2016. The Total Assets also increased to Kshs. 1,077,553,964 as at 31st December 2016 from Kshs. 870, 560,111 as at 31st December 2015 representing a growth of 24%. Institutional capital increased to Kshs. 60,009,284 from Kshs. 47,845,245 in 2015. As the society grows, we will strive to increase our institutional capital from the current 3.7 % to about 9% of the total assets. This is to ensure that the Sacco is built on a solid base that can withstand shocks and can undertake capital projects.

Share Capital

Share Capital represents your ownership of the Sacco. It is not withdrawable if you in case of leaving the Sacco but can be transferred to another member. This is the capital of the Sacco and enables the Sacco to undertake capital investments.

CHAIRMAN’S REPORT FOR THE YEAR ENDED 31ST DECEMBER 2016

Justus M. Munyithya Chairman, Management Committee

LSK Sacco Ltd

LSK Sacco Annual Report and Financial Statements 2016 | 15

The current minimum share capital is Kshs 4,000 per member divided into 200 shares worth Kshs 20 each. As the Sacco grows it is important to increase its capital base to match this growth and to ensure that the Sacco is built on a strong foundation. We are also targeting to grow our institutional capital which is composed of your share capital and our reserves from the current 3.7% of the total assets to the industry recommended rate of at least 9%. In this regard the Sacco will be seeking a resolution to increase share capital from a minimum of 200 shares per member to a minimum of 500 at shares per member.

This payment will be deducted gradually over a period of time from the member deposits until it is paid in full.

Figure 2 – Members Deposits

Total Deposits (in ‘000,000)

2010 2012 20142011 2013 2015 2016

1000

800

600

400

200

0

4. LoansThe total loan portfolio increased by 33% to Kshs. 986, 462,349 from Kshs. 743,600,350 in 2015. We have continued to finance member loans from internal sources mainly member deposits. However, as a precautionary measure we have been setting aside savings with KUSCCO as a backup borrowing plan incase our loan demand outstrips our own internal sources. The demand for loan continues to grow and we shall be seeking a resolution to increase the borrowing ceiling to Ksh. 20, 000,000 in order to meet our members’ needs.

Figure 3 – Non – performing loans

Total Deposits (in ‘000,000)

2010 2012 20142011 2013 2015 2016

1000

800

600

400

200

0

The pride of LSK Sacco shall be to have all loans repaid promptly and I wish to remind everyone that

loan repayment is an obligation for all members with loan and not an option. Over time, we managed to reduce our non-performing loans from highs of 10% to 4% which is below the industry recommendation of 5%.

We are working towards further reduction of the default rate by revamping our Customer Relationship program to improve on collection and partnering with the Credit Reference Bureaus to share and list non-performing accounts. We are also exploring other means of sharing our loan defaulters with other professional bodies like the Law Society of Kenya. We shall also be sharing a list of account in default with this meeting for discussion and noting..

5. Distribution of interest on deposits

This year we propose to pay Kshs 76,791,065 as interest on members deposits compared to Kshs 60,033,666 paid in 2015. This is at the rate of 9 % on a pro rata basis. The interest on deposit will be credited to member deposit accounts.

6. Review of Sacco bylawsDear members, the Sacco operates in a dynamic environment and our members need continue to change. There is aggressive completion from other financial institutions and more innovative products are coming up. There is also to strengthen our governance structure to ensure that we maintain the progress we have over the years. It is also important that we be ready for changes in regulatory environment. We believe these will both streamline the Sacco Sector and enhance public/member confidence in the movement. In light of this, the management committee will seek to amend our bylaws with a purpose to provide an enabling environment and conform to statutory requirements.

These amendments are geared towards enhancing our core and institutional capital, liquidity and investment ratios and the risk management.

7. Election to Management Committee

This year the Sacco is proposing to amend its bylaws to entrench our practice of nomination and vetting of members wishing to serve in the Management Committee well before the AGM. Those who would like, in the coming future to vie for positions in the Board will thus be required to apply to the

LSK Sacco Annual Report and Financial Statements 201616 |

Nomination Committee for Vetting. The Committee will then advise those who will have been cleared and those not cleared in writing. Only cleared candidates will be allowed to contest for positions falling vacant at the Annual General Meeting.

8. Information and Communication Technology (ICT)

Dear members, we have made great strides in leveraging on ICT to enhance efficiency and convenience in service delivery to our members. We have invested huge resources towards this and as a consequence we will be launching a member’s portal where members will be able to view their statements online. We have also introduced the use of bulk messaging as a means to enhance communication with our members and update them on developments within their Sacco. Through this means we intend to actively engage with our members at a personal level and sensitize them on new products and services.

We wish that all members update the office on any changes in their contact addresses so we are able to keep communication active.

We will also be reaching out to our members through other methods like push notification messages and Whatsapp. We wish to embrace ICT fully to improve operational and administrative efficiency thus saving costs to the Society while ensuring convenience and timeliness of service delivery to our members.

9. LSK Sacco 30th Anniversary The Sacco celebrated its 30th anniversary in November 2016 in Nairobi club with the Permanent Secretary Ministry of Industrialization and Enterprise as the Chief Guest. Other Guests who attended the event the President of the Law Society of Kenya, Chair of Mombasa, Nairobi, North Rift and . We wish to thank members for their participation and making this day a success.

10. Member Education.The Sacco also held two member education events outside Nairobi in Mombasa and in Mt Kenya region. In Mombasa 120 members attended and about 60 members attended in Mt. Kenya and were educated on the operations of the Sacco.

11. Strategic Plan 2017-2022The Sacco is in the process of developing a 3rd strategic plan 2017-2022 after expiry of the existing plan at the end of 2016.

12. AppreciationI want to thank all the members for their continued loyalty, support and choosing LSK SACCO as your investment vehicle. Special thanks to members of staff for working tirelessly during the year to realize impressive results. I want to thank the Management Committee for the support they have given me as the Chairperson of the Society.

I also want to acknowledge, recognize and appreciate the Ministry of Industrialization & Enterprise Development, KUSCCO, CIC, Co-operative Bank for the institutional support that they have given us. Special recognition to the Law Society of Kenya and to all branches of the Law Society for their tremendous support. We also wish to appreciate our legal Advisors, our Auditors victor Mutisya and Associates, members of the Supervisory Committee and everyone else who have contributed to our success.

As your Chairman, I feel honored to serve you and look forward to continuing meeting your needs today and in the future.

Long live LSK SACCO Ltd, Long live the cooperative movement

Justus M. Munyithya Chairman, Management Committee LSK Sacco Ltd

LSK Sacco Annual Report and Financial Statements 2016 | 17

The Chairman of LSK SACCO, fellow board members, District Co-operative Officer, invited guests, fellow LSK Sacco members, Ladies and Gentlemen; the Supervisory Committee has the pleasure of tabling its Annual report for the year 2016 to you.

In the year under review, the committee comprised of:-

1. Collins Wanderi - Chairperson

2. Joseph Makumi- Secretary

3. Salome Muhia Beacco- Member

The committee was given i ts mandate by the AGM of March 2016. In its mandate, the committee was charged with ensuring that the cooperative runs according to our bylaws, relevant legal requirements and in the interests of members. It was also given the authority to provide insights and recommendations on areas of improvements that can be implemented in the society.

Having reviewed the processes, transactions and overall performance of the society, we are pleased to report that there was fiduciary duty, skills and care observed by the board in exercising its duties for the benefit of the members.

The committee however observed the following and wishes to make recommendat ion on areas of improvement:-

a. Membership. The society recruited 636 members in 2016 against an exit of 81 members and a target of 1,500 members per year which is exactly 42% of the target.

We notice that the management has for the last 2 years not been able to hit more than 50% of the target. Although we have in the past recommended that the M.C. revamps its marketing strategy we notice that had the M.C. accepted the S.C. proposal for a paybill joining the SACCO would have been made easier to potential members.

b. Acquisition of paybill number

The committee notes that despite changes in technology and the previous recommendations by the SC in their reports of 2014, 2015 and 2016 the Society has not acquired its own pay bill number which would only take a day in acquisition.

The acquisition of a paybill would benefit the Sacco in real t ime crediting of members accounts hence assisting members earn dividends and encourage saving, remove the uncertainties of having to call the secretariat to find out if their payment through co-op bank paybill were manually entered to their accounts. The committee notes that it’s cheaper for members, in expensive to install and can be integrated with our I.T. system to give members instant feedback once their accounts are credited. In addition it is easier to reconcile member’s accounts with the deposits made via paybill thus reduce the overall costs of accounting for the society. Currently the Sacco has 2 members of staff engaged in day to day manual reconciliations of account and they can be better utilized elsewhere.

The SC is of the strong view that, it will be easier to market our own paybill to our members and this will in turn increase our deposits collections and improve loan repayments.

The explanation given that the same could be insecure and/or can lead to loss of funds is wanting as Paybill is a mode of inward payment (receipt of cash) and not outwards payments (payment of liabilities).

This explanation could only mean that the MC or their nominee can misappropriate member’s money as they are the only ones expected to handle and manage the Paybill.

The committee notes that there is no plausible explanations for the delay or non procurement of the

SUPERVISORY COMMITTEE (SC)

SUPERVISORY REPORT FOR THE YEAR 2016Society’s own pay bill number and the M.C.’s solution for the same was the removal of the transaction fees of Kshs 40/= previously charged by the bank. However this is not a permanent solution as the removal can not be reversed by the bank at its own discretion nor does it solve all the other concerns as related to reconciliation and timely crediting of members accounts.

Our further recommendation is the same is acquired without further delay as the same will make it convenient for members to save and lead to an increase members’ deposit.

c. Check off systemThe committee notes that the Sacco is still to enter into formal check-off agreements with institutions that have employed persons in the administration of justice such as the judiciary despite this recommendation having been made more than 2 years ago.

We reiterate that having this check off systems agreements will encourage members to save and in turn grow our deposits as well as assist members pay-up their loans.

d. Emergency and Normal loans issuance

The committee has noted that members are still not being issued with emergency loans within the recommended time of 48 hours. The issue has been raised with the M.C. over and over again to no avail.

We reiterate that the management puts up structures that will divert from the average of 6 days taken to issue an emergency loan which should be issued in less than 2days. The same applied to normal loans which are dispersed on average of 35 days for a normal loan which should be issued within 21 days.

LSK Sacco Annual Report and Financial Statements 201618 |

e. Default Management and Loan Issuance.

The S.C. notes that the Sacco is registering logbooks jointly with members applying for a loan as we had recommended. This has considerably reduced the Sacco’s exposure to bad; non performing and unsecured loans against assets.

The S.C. further note that since the customer relationship officer program was introduced default rate decreased from the then rate of 8% to 4% and this has been maintained for the last 2 years and the programme has been very successful on the issue of debt recovery. We commend the management for the efforts put in place in dealing with the issue of default and securing of loans.

We note that since our intervention on the previous year’s default by then board members, there has been no subsequent default by other board members due to the continued oversight and vigilance by the S.C.

f. Procurement of Management information system

The committee noted that with the investments in the IT systems that had put in place, the risk of the Sacco’s financial data being accessed and manipulated by unauthorized persons is higher.

The committee recommended the deployment of enhanced security protocols as well as a Business Continuity Plan (BCP) and a Disaster Recovery plan (DRP).

The committee has noted with appreciation the efforts by the M.C. to put in place the relevant polices for a security firewall, a Business Continuity Plan and Disaster Recovery plan.

g. Savings made to KUSSCO

The committee notes that the m o n t h l y s a v i n g s t o K U S S CO amounting to Ksh 100,000 per month is uneconomical since the interest earned from the savings is minimal. We recommend that the management reduce the savings to

the minimal amount of contribution required and reinvest the other amount to higher interest earning accounts.

The current savings with KUSCCO can enable the SACCO borrow Kshs 50,000,000/=. (Though at a loss). Going by the SACCO’ s history it is unlikely to borrow from KUSCCO as the only time it had liquidity challenges was when it was acquiring its premises and has always been liquid enough advance loans.

It was not shown nor noted by the SC that the SACCO has had to delay issuance of loans due to liquidity challenges.

h. Board Activities; consultancy and training.

The committee notes that in the year 2016 as opposed to the previous years the M.C. and the S.C. have been engaged in joint activities in fur therance of the society ’s objectives and promotion of prudent management of the resources of the SACCO.

We recommend that the M.C. organizes more activities on training and consultancy to build capacity for all members of the board.

i. Board Travel Expenses.

The Committee noted a sharp increase in committee travel and accommodation expenses. The total travel and accommodation expenses are Kshs 623,100 as compared to the previous year’s 458,220.00

This cost is largely attributed to one board member who travels from outside Nairobi to attend meetings. This increase eats to the profitability of the Sacco and is not sustainable in the long run.

The Committee has advised the MC to reorganise itself or use technology sucs as teleconferencing with a view of bringing down costs, a position which was supported by the District Co-operative officer. Although board accommodation and travel expenses are justifiable governance expenses,

options should be explored to keep them minimal in line with the expected growth in membership and geographical distribution which may necessitate regional representation in management of committees.

The SC is of the strong view that these costs are very high vis-a vis the productivity of such meetings and are otherwise eating considerably into the profitability of the Sacco.

A comparison of this expense vis-avis that of the previous year only shows that despite the Sacco having spent more this year it is less profitable than last year.

j. Outstanding issues from previous reports.

The committee notes the following issues are yet to be addressed conclusively:-

a. Benevolent fund

b. Lost files.

Despite the SC having recommended and the then chair adopted the SC proposal for a benevolent fund the SC sadly notes that no steps have been made towards realizing the same.

The MC is challenged to follow up with the police on the status of the lost files as the last follow up seems to have been made more than 3 years ago. The MC notes that the police are unlikely to act without constant follow up by the secretariat. The SC recommends that the MC deputize one of the CRO to do a monthly follow up and documents the progress.

Chairman

Secretary

Member

Interest rates: 1% per month on a reducing balance.

Deposit Multiplier: 3 times of members total deposits

Loan Securities

• Owndeposits •ChattelsmortgageonMotorVehicles

• Guarantors’deposits •Titledeed

OUR CREDIT PRODUCTS

EMERGENCY LOANS

MOTOR VEHICLE INS. LOANS

Repayment period of up to 36 months

Maximum amount of Ksh. 200,000Repayment period of up to 12 months

LSK Sacco Annual Report and Financial Statements 201620 |

The SACCOs Act, No 14 of 2008 requires the Board of Directors to prepare financial statements for each year which give a true and fair view of the state of affairs of the society as at the end of the financial year and of its operating results for that year in accordance with IFRS It also requires the Board of Directors to ensure that the society keeps proper accounting records which disclose with reasonable accuracy at any time the financial position of the society. They are also responsible for safeguarding the assets of the society and ensuring that the business of the society has been conducted in accordance with its objectives, by-laws and any other resolutions made at the society’s general meeting.

The Board of Directors accepts responsibility for the annual financial statements, which have been prepared using appropriate accounting policies supported by reasonable and prudent judgments and estimates, in conformity with International Financial Reporting Standards and in the manner required by the SACCO Societies Act No. 14 of 2008. The Board of Directors is of the opinion that the financial statements give a true and fair view of the state of the financial affairs of the society and of its operating results in accordance with the IFRS. The Board of Directors further accepts responsibility for the maintenance of accounting records which may be relied upon in the preparation of financial statements, as well as adequate systems of internal financial control.

Nothing has come to the attention of the Board of Directors to indicate that the society will not remain a going concern for at least twelve months from the date of this statement.

Approved by the Board of Directors on 22nd February 2017 and signed on its behalf by:

Chairman

Treasurer

Secretary

STATEMENT OF THE BOARD OF DIRECTORS RESPONSIBILITIES

FINANCIAL REPORTS

LSK Sacco Annual Report and Financial Statements 2016 | 21

FINANCIAL REPORTS

We have audited the accompanying financial statements of Law Society of Kenya Co-operative Society Limited set out on pages 6-19 which comprise the Statement of Financial Position as at 31st December 2015, and the Statement of Comprehensive Income, Statement of Changes in Equity, and Statement of Cash Flows for the year then ended, and a summary of significant accounting policies and other explanatory notes.

The Board of Directors’ Responsibility for the Financial Statements

The Board of Directors is responsible fo r the preparat ion and fa i r presentation of these financial statements in accordance with International Financial Reporting Standards and the requirements of the Kenyan Saccos Societies Act. This responsibility includes designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement

Auditors’ Responsibility Our responsibility is to express an independent opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Audit ing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from

REPORT OF THE INDEPENDENT AUDITORS TO THE MEMBERS OF LAW SOCIETY OF KENYA CO-OPERATIVE SAVINGS AND CREDIT SOCIETY LIMITED FOR THE YEAR ENDED 31ST DECEMBER 2016

material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers the internal control relevant to the society’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of society’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Board of Directors, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Limitation of Scope The Accounts reflect a Suspense Account i tem (credit) of Kshs 4,434,624 in respect of unanalyzed standing orders and direct bankings by members as at 31st December 2016 (2015 figure was Kshs 3,866,059). The standing orders and bankings could not be analyzed into their various components -share capital, and loan and interest repayment –

because of lack of vital information including names of the members who had placed such standing orders or had carried out the bankings and what the payments were in respect of.

OpinionExcept for the above observations, in our opinion, the financial statements give a true and fair view of the state of the Society’s financial affairs as at 31st December 2016 and of its operating results and cash flows for the year then ended in accordance with the International Financial Reporting Standards and the requirements of the Kenyan Sacco Societies Act.

Report on other Legal Requirements As required by the Kenya Sacco Societies Act, we report to you based on our audit that:

a. We h ave o b t a i n e d a l l t h e information and explanations w h i c h to t h e b e s t o f o u r knowledge and bel ief were necessary for the purposes of our audit.

b. In our opinion, proper books of account have been kept by the Society, so far as it appears from our examination of those books.

VICTOR MUTISYA & CO.

Certified Public Accountants (K)Date: 22nd February 2017

LSK Sacco Annual Report and Financial Statements 201622 |

FINANCIAL REPORTS

2016 2015

MEMBERSHIP

Active 4,230 4,285

Dormant 2,215 1,524

Total 6,445 5,809

Dormant Members are those members who have not made any payments to the Society over twelve (12) consecutive months.

FINANCIAL KSHS KSHS

Total Assets 1,077,553,964 870,560,111

Members Deposits 934,119,547 743,600,350

Loans to Members 986,462,349 759,860,586

Investment 2,124,693 2,124,693

Share Capital 16,265,640 15,654,540

Institutional Capital 39,476,978 32,190,705

Total Revenue 116,346,612 97,418,662

Total Loan Interest Income 95,601,999 77,339,162

Total Expenses 112,931,308 81,849,486

Employees of the Sacco 20 15

Key Ratios

Capital Adequacy Ratio

Institutional Capital/Total Assets 3.7% 3.7%

Liquidity Ratio

Liquid Assets/Total Deposits & Long Term Liabilities 5.10% 8.6%

Total Expenses/Total Revenue 97% 89%

Interest on Members Deposits/Total Revenue 66% 68%

Interest Rate on Members Deposits 9.0% 9.00%

STATISTICAL INFORMATION FOR THE YEAR ENDED 31ST DECEMBER 2016

LSK Sacco Annual Report and Financial Statements 2016 | 23

FINANCIAL REPORTS

2016 2015

NOTES KSHS KSHS

REVENUE

Interest on Loan to Members 95,601,999 77,339,162

Other Interest Income - -

Total Interest 95,601,999 77,339,162

Interest Expenses (3) (76,791,065) (60,033,666)

Net Interest Income 18,810,934 17,305,496

Other Operating Income (4) 15,555,667 12,294,912

Administration Expenses (5) (25,987,614) (15,388,494)

Other Operating Expenses (6) (10,152,629) (6,427,326)

Other Comprehensive Income

Other Comprehensive Income for the year, net of Tax (7) 5,188,946 2,323,569

Net Operating Surplus/(Deficit) Before Income Tax (8) 3,415,304 7,784,588

Income Tax Expense (9) - -

Net Surplus/(Deficit) for the Year 3,415,304 7,784,588

TOTAL COMPREHENSIVE INCOME 3,415,304 10,108,157

STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 31ST DECEMBER 2016

LSK Sacco Annual Report and Financial Statements 201624 |

FINANCIAL REPORTS

2016 2015

NOTES KSHS KSHS

ASSETS

Cash and Cash Equivalent (10) 50,163,508 67,961,925

Loans to Members (11) 986,462,349 759,860,586

LSK Housing Advances /Debts (12) 766,396 3,660,655

Sundry Debtors (13) 1,929,798 1,137,241

Fixed Assets (2) & (14) 36,107,220 -

Investment in Property (2) & (14) - 23,886,710

Intangible Assets (Software) (2) - 10,063,547

Office Partitions (2) - 942,848

Furniture and Fittings (2) - 647,982

Computers & Accessories (2) - 273,924

Other Non-Current Assets (15) 2,124,693 2,124,693

TOTAL ASSETS 1,077,553,964 870,560,111

LIABILITIES

Members Deposits (16) 934,119,547 743,600,350

Current Income Tax Payable (9) - -

Accrued Expenses (17) 76,953,675 60,188,544

Sundry Creditors (18) 6,303,500 15,059,913

Suspense Account: Unanalysed Bankings &Standing Orders (19) 4,434,624 3,866,059

Total Liabilities 1,021,811,346 822,714,866

EQUITY

Share Capital (20) 16,265,640 15,654,540

Reserves (21) 39,476,978 32,190,705

TOTAL EQUITY 55,742,618 47,845,245

TOTAL LIABILITIES AND EQUITY 1,077,553,964 870,560,111

The notes on pages 10 to 19 form an integral part of these accounts

The financial statements set out on pages 6 to 19 were approved by the Board of Directors on 22nd February 2017 and were signed on its behalf by:

Chairman Treasurer Board Member

STATEMENT OF FINANCIAL POSITION AS AT 31ST DECEMBER 2016

LSK Sacco Annual Report and Financial Statements 2016 | 25

FINANCIAL REPORTS

2016

Share Capital Statutory Reserve

Revenue Reserve

Total Members Capital

KSHS KSHS KSHS KSHS

As at 01.01.2016 15,654,540 8,116,660 24,074,045 47,845,245

Shares Paid 611,100 - - 611,100

Prior after Adjustment 5,672,212 5,672,212

Surplus/(Loss) for the Year - - 3,415,304 3,415,304

Provision for Tax - - - -

20% Transfer to Statutory Reserve - 683,061 (683,061) -

Provision for Honorarium - - (1,912,040) (1,912,040)

Sundry Creditor Written Back - - 110,697 110,697

As at 31.12.2016 16,265,640 8,799,721 30,677,258 55,742,618

i. During the year the Management Committee negotiated with a creditor to write off a long outstanding debt with the Society.

ii. Prior year Adjustment represents balances for unpaid interest on members deposits.

2015

Share Capital Statutory Reserve

Revenue Reserve

Total Members Capital

KSHS KSHS KSHS KSHS

As at 01.01.2015 9,569,831 6,095,029 17,291,355 32,956,215

Shares Paid 6,084,709 - - 6,084,709

Surplus/(Loss) for the Year - - 10,108,157 10,108,157

Provision for Tax - - - -

20% Transfer to Statutory Reserve - 2,021,631 (2,021,631) -

Provision for Dividends - - - -

Provision for Honorarium - - (1,402,836) (1,402,836)

Prior Year Adjustments - - 99,000 99,000

As at 31.12.2015 15,654,540 8,116,660 24,074,045 47,845,245

Prior Year Adjustment is in respect of accumulated unpaid interests on deposits for prior years. The Management is of the opinion that there is no possibility of payment of these.

STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31ST DECEMBER 2016

LSK Sacco Annual Report and Financial Statements 201626 |

FINANCIAL REPORTS

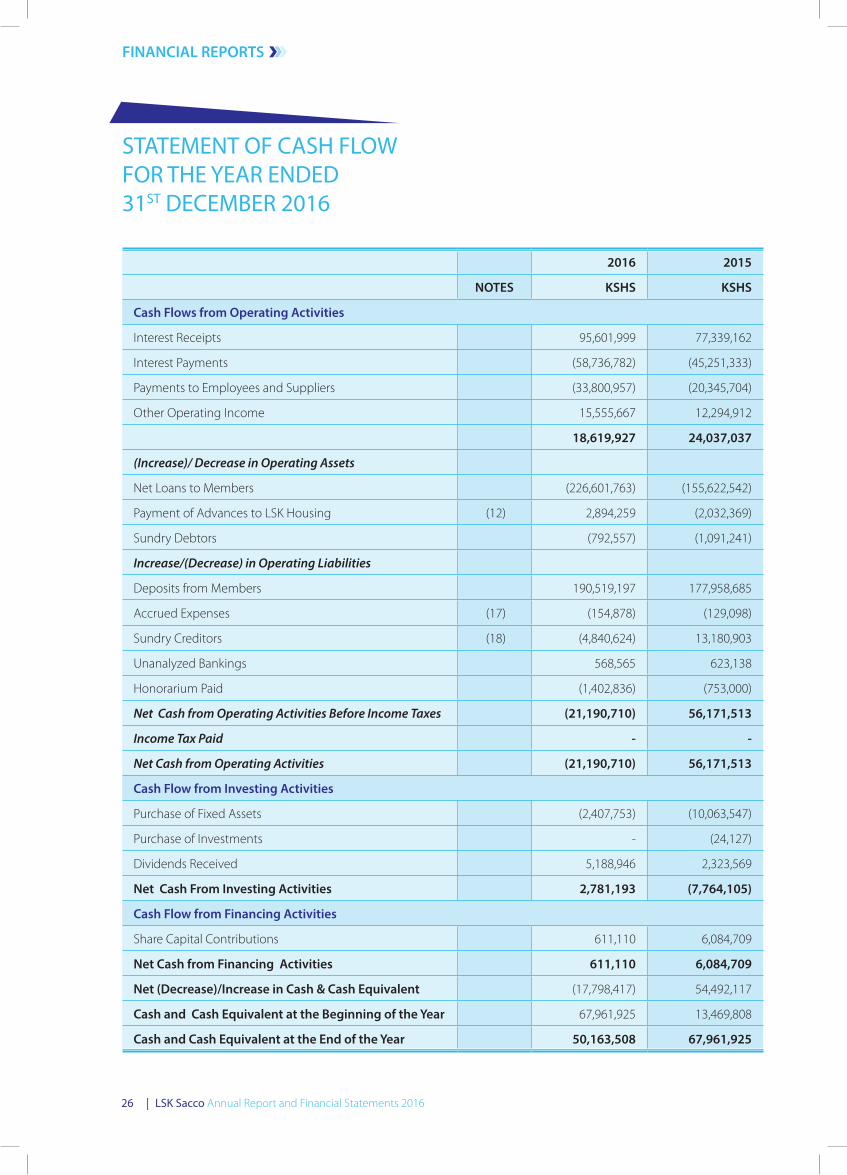

2016 2015

NOTES KSHS KSHS

Cash Flows from Operating Activities

Interest Receipts 95,601,999 77,339,162

Interest Payments (58,736,782) (45,251,333)

Payments to Employees and Suppliers (33,800,957) (20,345,704)

Other Operating Income 15,555,667 12,294,912

18,619,927 24,037,037

(Increase)/ Decrease in Operating Assets

Net Loans to Members (226,601,763) (155,622,542)

Payment of Advances to LSK Housing (12) 2,894,259 (2,032,369)

Sundry Debtors (792,557) (1,091,241)

Increase/(Decrease) in Operating Liabilities

Deposits from Members 190,519,197 177,958,685

Accrued Expenses (17) (154,878) (129,098)

Sundry Creditors (18) (4,840,624) 13,180,903

Unanalyzed Bankings 568,565 623,138

Honorarium Paid (1,402,836) (753,000)

Net Cash from Operating Activities Before Income Taxes (21,190,710) 56,171,513

Income Tax Paid - -

Net Cash from Operating Activities (21,190,710) 56,171,513

Cash Flow from Investing Activities

Purchase of Fixed Assets (2,407,753) (10,063,547)

Purchase of Investments - (24,127)

Dividends Received 5,188,946 2,323,569

Net Cash From Investing Activities 2,781,193 (7,764,105)

Cash Flow from Financing Activities

Share Capital Contributions 611,110 6,084,709

Net Cash from Financing Activities 611,110 6,084,709

Net (Decrease)/Increase in Cash & Cash Equivalent (17,798,417) 54,492,117

Cash and Cash Equivalent at the Beginning of the Year 67,961,925 13,469,808

Cash and Cash Equivalent at the End of the Year 50,163,508 67,961,925

STATEMENT OF CASH FLOW FOR THE YEAR ENDED 31ST DECEMBER 2016

LSK Sacco Annual Report and Financial Statements 2016

FINANCIAL REPORTS

| 27

NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES.

The principal accounting policies adopted in the preparation of these financial statements are set out below:

a. Statement of compliance & basis of preparation

The financial statements are prepared in accordance and comply with International Financial Reporting Standards (IFRSs). These financial statements are presented in the functional currency, Kenya shillings (Kshs) and prepared under the historical cost convention as modified by revaluation of certain assets a s prescribed by IFRSs.

b. Revenue recognition Revenue as reflected in the accounts is recognized on cash basis.

c. Fixed Assets i. All fixed assets are stated at historical cost less

accumulated depreciation and impairment losses.

ii. Depreciation is calculated using the Reducing Balance method to write down the cost of each asset to its residual value over its estimated useful life. The annual depreciation rates in use are:

Furniture & Fittings - 12.5% Computers and accessories - 30%Software - 30% Office Space - 2.5%Partitions - 12.5%

iii. The assets’ residual values and useful lives are reviewed, and adjusted if appropriate at each reporting date. Gains or losses on disposal of property, plant and equipment are determined by reference to their carrying amount and are taken into account in determining operating profit. On disposal of a revalued asset, amount in the revaluation reserve relating to that asset is transferred to retained earnings.

iv. Depreciation on SoftwareDuring the year the Management wrote off the Easy Sacco Software acquired in 2009 and for which no depreciation had been provided since the supplier had not completed customization of the software. During the same year, the Management acquired Navision 2015 ERP Software. No depreciation has been provided for this asset since the supplier was still installing it as at 31st December 2016.

d. Classification as debt or equity Debt and equity instruments are classified as either financial liabilities or as equity in accordance with the substance of the contractual arrangement.

e. Equity instruments An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. Equity instruments issued by the Sacco are recorded at the proceeds received, net of direct issue costs. The capital comprise primarily of minimum share capital prescribed under the By-laws of the Sacco.

f. Tax Current tax is provided on the basis of the results for the year, as shown in the financial statements, adjusted in accordance with tax legislation.

Deferred income tax is provided, using the liability method, on temporary differences arising between the tax bases of assets and liabilities and their carrying amounts in the financial statements. However, the deferred income tax is not accounted for if it arises from initial recognition of an asset or liability. Currently enacted tax rates are used to determine deferred income tax.

Deferred income tax assets are recognized only to the extent that it is probable that the future taxable profits will be available against which temporary differences can be utilized.

NOTES TO THE FINANCIAL REPORTS FOR THE YEAR ENDED 31ST DECEMBER 2016

LSK Sacco Annual Report and Financial Statements 2016

FINANCIAL REPORTS

28 |

g. Statutory reserves Co-op Act Transfers are made to the statutory reserve fund at a rate of 20% of net operating surplus after tax in compliance with the provision of section 47 (1& 2) of the Co-operative Societies Act ,Cap 490.

h. Trade and Other PayablesTrade and other payables are recognized initially at fair value and subsequently measured at amortized cost using the effective interest rate method.

i. ReceivablesReceivables are recognized initially at fair value and subsequently measured at amortized cost using the effective interest rate. A provision for impairment is recognized in the profit or loss account in the year when the recovery of the amount due as per the original terms is doubtful. The provision is based on the difference between the carrying amount and the present value of the expected cash flows, discounted at the effective interest rate. Receivables not collectible are written off against the related provision. Subsequent recoveries of amounts previously written off are credited to the profit or loss account in the year of recovery

j. Cash and cash equivalents Cash and cash equivalents comprise cash on hand and demand deposits and other short-term highly liquid investments that are readily convertible to a known amount of cash and are subject to an insignificant risk of changes in value net of bank overdrafts

k. Provisions for liabilities and other charges

Provisions are recognized when the Sacco has a present obligation (legal or constructive) as a result of a past event, it is probable that the Sacco will be required to settle the obligation, and a reliable estimate can be made of the amount of the obligation. The amount recognized as a provision is the best estimate of the consideration required to settle the present obligation at the reporting date, taking into account the risks and uncertainties surrounding the obligation.

l. InvestmentsInvestments are stated at cost less provision for any permanent diminution in value.

NOTE 2: FIXED ASSETS & DEPRECIATION SCHEDULE

2016Property

(Office Space)

Office Partitions

Computers &

Accessories

Furniture & Fittings

Software Total

KSHS KSHS KSHS KSHS KSHS KSHS

COST

As At 01.01.2016 25,933,752 1,452,800 1,238,578 1,118,538 10,063,547 39,807,215

Additions During the Year - - 1,006,302 262,739 1,138,712 2,407,753

(Disposals) During the Year

- - - - - -

Re-Classification of Assets - - 2,714,323 706,518 (3,420,841) -

As At 31.12.2016 25,933,752 1,452,800 4,959,203 2,087,795 7,781,418 42,214,968

DEPRECIATION

As at 01.01.2016 2,047,042 509,952 964,654 470,556 - 3,992,204

Charges for the Year 597,168 117,856 1,198,365.00 202,155 - 2,115,544

(Disposals) During the Year

- - - - - -

As at 31.12.2016 2,644,210 627,808 2,163,019 672,711 - 6,107,748

NET BOOK VALUE

As at 31/12/2016 23,289,542 824,992 2,796,184 1,415,084 7,781,418 36,107,220

As at 31/12/2015 23,886,710 942,848 273,924 647,982 10,063,547 35,815,011

LSK Sacco Annual Report and Financial Statements 2016

FINANCIAL REPORTS

| 29

2015Property

(Office Space)

Office Partitions

Computers &

Accessories

Furniture & Fittings

Software Total

KSHS KSHS KSHS KSHS KSHS KSHS

COST

As At 01.01.2015 25,933,752 1,452,800 1,238,578 1,118,538 527,000 30,270,668

Additions During the Year - - - - 10,063,547 10,063,547

(Disposals) During the Year

- - - - (527,000) (527,000)

As At 31.12.2015 25,933,752 1,452,800 1,238,578 1,118,538 10,063,547 39,807,215

DEPRECIATION

As at 01.01.2015 1,434,562 375,259 847,258 377,987 - 3,035,066

Charges for the Year 612,480 134,693 117,396 92,569 - 957,138

(Disposals) During the Year

- - - - - -

As at 31.12.2015 2,047,042 509,952 964,654 470,556 - 3,992,204

NET BOOK VALUE

As at 31/12/2015 23,886,710 942,848 273,924 647,982 10,063,547 35,815,011

As at 31/12/2014 24,499,190 1,077,541 391,320 740,551 527,000 27,235,602

i. In the 2016 Balance Sheet fixed assets have been shown under one heading unlike in the previous Balance Sheets where each item was being shown separately.

ii. During the year the Society was still installing the software acquired in 2015. No depreciation has been provided on the software since it was still being installed as at 31st December 2016.

iii. During the year there was re-classification of assets originally captured as software as follows:

KSHSComputers 2,714,323

Furniture & Fittings 706,518

3,420,841

NOTE 3: INTEREST EXPENSE

2016 2015

KSHS KSHS

Interest on Members Deposits

76,791,065 60,033,666

Interest on KUSCCO Loan - -

76,791,065 60,033,666

Interest on members deposits has been provided at 9% (2015 rate was 9.0%) per annum on members deposit balances each month .

NOTE 4: OTHER OPERATING INCOME

2016 2015

KSHS KSHS

Membership/Entrance Fees 636,000 572,000

Deposit Refund Processing Fees

97,500 123,000

Lumpsum Payment Charges 1,479,721 1,525,497

Loan Clearance Commission 2,401,310 1,927,177

Loan Offsetting Fees 4,022,358 4,508,610

Loan Application Processing Fees

3,616,302 2,409,391

Penalties on Dishonoured Cheques

27,000 19,500

Other Incomes 752,077 101,054

Loan Insurance Fees 1,655,913 1,108,683

LSK Housing Hosting Charges 867,486 -

15,555,667 12,294,912

NOTE 5: ADMINISTRATION EXPENSES

2016 2015

KSHS KSHS

Salaries and Wages 15,385,740 10,252,724

Other Staff Costs 2,080,029 1,116,985

Travelling & Subsistence 318,490 233,190

Electricity 239,419 93,332

LSK Sacco Annual Report and Financial Statements 2016

FINANCIAL REPORTS

30 |

Printing & Stationery 558,926 492,290

Consultancy Fees & Training 75,240 237,450

Office General Expenses 478,750 406,115

Telephone, postage and Email

428,972 347,568

Repairs and Maintenance 257,972 140,066

Rent & Rates/Service Charges 420,830 144,829

Subscriptions 36,500 -

Legal Fees 214,346 -

Anniversary Celebrations 3,859,262 -

Minor Office Eqipment 209,960 -

Staff Recruitment - 96,272

Tender Expenses - 281,613

Fixed Asset Written Off - 358,100

Insurances 1,260,568 1,033,082

Audit Fees & VAT 149,520 142,402

Audit Supervision Fees 13,090 12,476

25,987,614 15,388,494

NOTE 6: OTHER OPERATING EXPENSES

2016 2015

KSHS KSHS

Members & Committee Expenses

Committee Sitting Allowances

1,885,662 1,474,842

Committee Travel & Subsistence

645,907

Education and Seminars 595,960 436,275

A.G.M Expenses 883,420 449,100

Advertising, Marketing and Promotion

2,642,123 1,793,655

Team Building 104,300 98,730

6,757,372 4,252,602

Finance Expenses

Bank Charges and Commissions

1,279,713 1,217,586

Depreciation Expense

Charges for the Year 2,115,544 878,199

TOTAL OTHER OPERATING EXPENSES

10,152,629 6,348,387

NOTE 7: OTHER COMPREHENSIVE INCOME, NET OF TAX

2016 2015

KSHS KSHS

(i) Dividends Income

Ken-Gen Co. Ltd 3,087 -

Equity Bank Limited 19,000 17,100

East African Breweries Limited

13,063 -

Kenya Commercial Bank 31,563 21,025

Scan Group Limited 1,140 1,140

Housing Finance Company 3,242 6,982

Co-operative Bank of Kenya 658,981 -

Kenya Reinsurance 2,143 2,000

Co-operative Insurance Company

33,038 31,464

Nation Media Group 13,794 13,794

Stanbic Bank Uganda - -

Safaricom Limited 36,799 16,355

Access Kenya Limited - -

Total Dividends Income 815,850 109,860

(ii)Interest Income

Interest from Savings Account

3,075 23,102

Interest from Fixed Deposits 3,108,496 1,753,072

Interest from KUSCCO CFP 1,261,525 437,535

Total Interest Income 4,373,096 2,213,709

TOTAL OTHER COMPREHENSIVE INCOME NET OF TAX

5,188,946 2,323,569

NOTE 8: NET OPERATING SURPLUS BEFORE INCOME TAXThe following items have been charged in arriving at net operating surplus before income tax:

2016 2015

KSHS KSHS

Depreciation/Amortizaton 2,115,544 957,138

Salaries & Wages 15,385,739 10,252,724

Other Staff Costs 2,080,029 1,117,052

Operating Lease Rentals Expense

420,830 144,829

20,002,142 12,471,743

NOTE 9: INCOME TAX

2016 2015

KSHS KSHS

Current Tax - -

Deferred Tax - -

Tax Expense /(Credit) - -

No tax has been provided. Most of the Income for the Society was from dealings with members while income from taxable sources was taxed at source. Tax liability arising from this second category of income is as follows, and details of these are in Note 9.

LSK Sacco Annual Report and Financial Statements 2016

FINANCIAL REPORTS

| 31

2016 2015

KSHS KSHS

Gross Taxable Income 3,108,496 2,211,036

Tax @ 50% of Gross Taxable Income x 30%

466,274.40 331,655

Less: Tax at Source (466,274) (331,655)

Tax Due - -

NOTE 10: CASH AND CASH EQUIVALENTS

2016 2015

KSHS KSHS

Current Account 5,332,007 18,310,528

Savings Account 13,086,061 2,787,502

KUSCCO Central Finance (Savings)

21,314,005 19,086,397

Petty Cash 37,052 25,338

Housing Finance Co. 17,583 17,583

CIC Money Market Account 10,376,800 27,734,577

50,163,508 67,961,925

NOTE 11: LOANS TO MEMBERS

2016 2015

KSHS KSHS

Opening Balance 759,860,586 604,238,044

Issued During the Year 664,318,432 490,216,943

Repaid During the Year (437,716,669) (334,594,401)

Closing Balance 986,462,349

759,860,586

NOTE 12: LSK HOUSING ADVANCES/DEBTS

2016 2015

KSHS KSHS

Balance Brought Forward 3,660,655 1,628,286

Sacco Funds Deposited in LSK Housing A/c

267,910 915,475

LSK 2016 Hosting Sacco Charges

867,486 1,998,994

Less: Payments in 2016 (3,660,655) -

1,135,396 4,542,755

Less: Housing Funds Deposited in Sacco A/c

(369,000) (882,100)

Balance Carried Forward 766,396 3,660,655

Operating expenses are shared between LSK Sacco and LSK Housing Co-operative Society at the ratio of 95.05 respectively where applicable.

NOTE 13: SUNDRY DEBTORS2016 2015

KSHS KSHS

Co-operative Bank 19,000 19,000

Others (Parking Fees) - 18,000

Mackphilisa 50,000 -

Valere 20,000 -

CIC Insurance - 35,377.00

Pre-paid Staff Medical Insurance

1,427,992 885,975.00

Interest Receivable 412,806 178,889.00

1,929,798 1,137,241

NOTE 14: PROPERTY (OFFICE SPACE)The Society purchased office space at Crawford Business Park (3rd Floor, Offfice No. 23), L.R. No. 209/1519, State House Road, Nairobi in 2012. Total cost of the property was Kshs 25,933,752. Detailed analysis of this asset is in Note 2.

NOTE 15: OTHER NON-CURRENT ASSETSThis represents investments in the following companies:

2016 2015

KSHS KSHS

Quoted

900 Ordinary Shares Held in Access Kenya Limited

9,000 9,000

5119 Ordinary Shares Held in Kenya Commercial Bank

234,874 234,874

2,000 Ordinary Shares Held in Scan Group Limited

53,108 53,108

2,579 Ordinary Shares Held in Kenya Re-Insurance Co.

36,137 36,137

5000 Ordinary Shares Held in KENGEN

132,366 132,366

26900 Ordinary Shares Held in Safaricom

170,280 170,280

1,100 Ordinary Shares Held in EAB LTD

144,600 144,600

1,100 Ordinary Shares Held in Nation Media Group

147,843 147,843

10,000 Ordianry Shares Held in Equity Bank Ltd

142,548 142,548

32,000 Ordinary Shares Held inStanbic Uganda Ltd.

189,441 189,441

3500 Ordinary Shares Held in Housing Finance Co.(K)

87,569 87,569

Unquoted

420,000 Ordinary Shares Held in Co-op Bank (K) Ltd.

420,000 420,000

13,800 Ordinary Shares Held in CIC Insurance Co. Ltd

312,800 312,800

550 KUSCCO Shares 44,127 44,127

2,124,693 2,124,693

LSK Sacco Annual Report and Financial Statements 2016

FINANCIAL REPORTS

32 |

NOTE 16: MEMBERS DEPOSITS

2016 2015

KSHS KSHS

Savings Deposits at Start of Year

743,600,350 565,641,665

Deposits During the Year 194,665,919 187,793,864

Transfer from Interest on Deposits Payable

55,772,980 38,949,066

Withdrawals/Refunds/Offsets During the Year

(59,919,702) (48,784,245)