latin america beer market - arena international · latin america beer market ... industry with more...

TRANSCRIPT

LATIN AMERICA BEER MARKET

Pinpointing major challenges and opportunities in

Latin America and identifying key areas of growth

May 2012

2

Out of 10 litres of beverages consumed in

LatAmhellip

5 lts are non-commercial

beverages

5 lts are commercial

beverages

3

Out of 10 lts of commercial beverages

consumed in LatAmhellip

Soft Drinks lead the

industry with more than 4 lts

Alcoholic Bevs represent 16

lts with Beer accounting for

14 lts

Dairy Hot Drinks etc 44 lts

Dairy Drinks Hot Drinks amp HODBulk water

4

Out of 10 beers consumed in LatAmhellip

4 are purchased away from

home and 8 are consumed in

refillable formats

4 are part of Ambevrsquos portfolio and

2 are sold by Heineken amp

SABMiller together

8 are Mainstream brands

5

Out of 10 beers consumed in LatAmhellip

315 million hectolitres

70 billion Euros

16 of global consumption

6

LatAm is diverse

7

Brazil and Mexico gather more than

50 of LatAm populationhellip

LatAm is diverse

Population 2011 by country

Mexico 21

Brazil 43

Others 36 hellip and almost 65 of

beer consumption

19 36 36 45 50 51 52 54 75 126

281 302 364 374

471

710

1657

2282

-600

-100

400

900

1400

1900

0

50

100

150

200

250

300

350

400

450

500

GDP 2011 (PPP) Beer per cap Total Alc per cap

8

LatAm is diverse

Beer vsTotal Alcohol

9

3072

4240

5426

6919

12615

5023

16019

12520

4875

8372

16078

9958

11390

13480

10038

17382

14514

11892

-6000

-1000

4000

9000

14000

19000

0

100

200

300

400

500

600 GDP per capita (PPP) Beer per cap Total Alc per cap

LatAm is diverse

Beer vsTotal Alcohol

LatAm GDP per capita

(PPP)

11770

10

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

11

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption above

average

12

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption below

average

lowest levels of

alcohol

consumption

LatAm is diverse

Beer vsTotal Alcohol

13

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

Consumption gap due

to local alc bevs

Informal alc bevs

VINO

(JESSICA)

FOTO FOTO

FOT

O

FOTO

Local alcoholic drinks and a

number of local factors boost

alcohol consumption

LatAm is diverse

Beer vsTotal Alcohol

14

1

2

3

4

5

Average price USD 31

25 Euros

Partially driven by the

appreciation of the

Braziliean Real

LatAm is diverse

Price per litre

23

38

15

Common factors among LatAm Countries

16

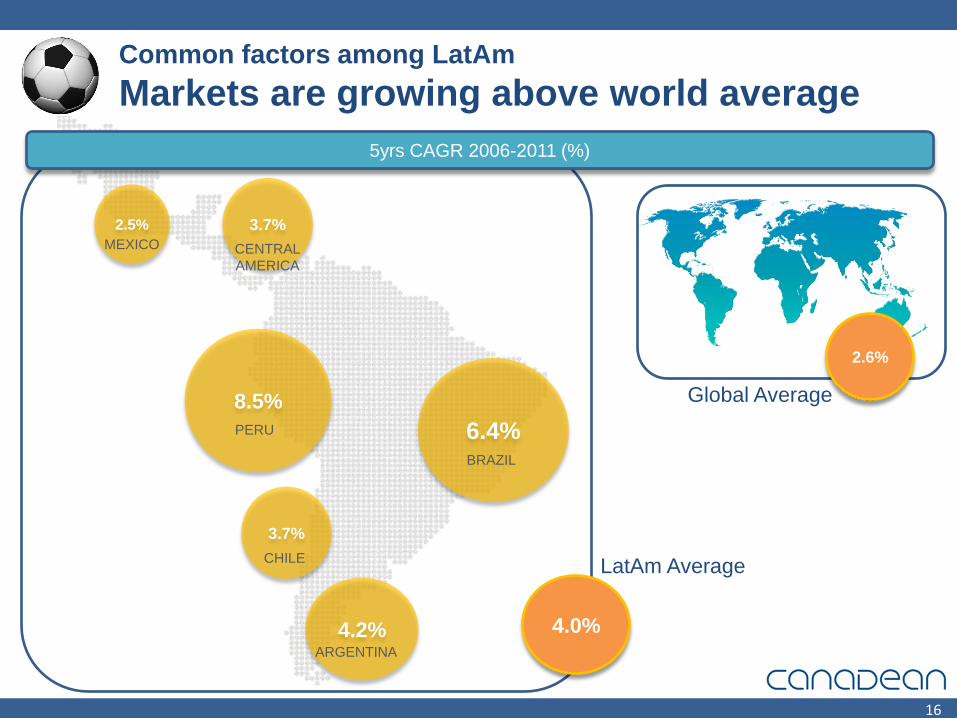

Common factors among LatAm

Markets are growing above world average

5yrs CAGR 2006-2011 ()

26

42

64

25 37

85

37

40

Global Average

LatAm Average

MEXICO CENTRAL

AMERICA

PERU

CHILE

BRAZIL

ARGENTINA

200

220

240

260

280

300

320

340

360

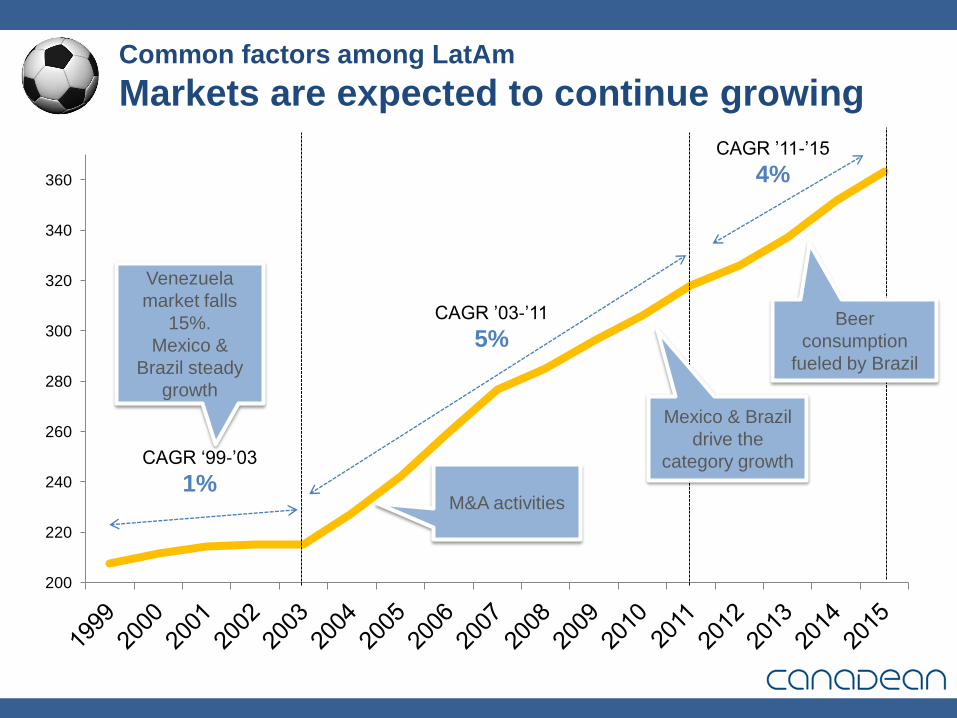

CAGR lsquo99-rsquo03

1

CAGR rsquo03-rsquo11

5

CAGR rsquo11-rsquo15

4

Venezuela

market falls

15

Mexico amp

Brazil steady

growth

MampA activities

Mexico amp Brazil

drive the

category growth

Beer

consumption

fueled by Brazil

Common factors among LatAm

Markets are expected to continue growing

18

Common factors among LatAm

Lager beer is the norm 99 of the market

Skol is the

leading beer

in Brazil and

worldrsquos fourth

best selling

beer brand

Brahma is

consumed in

more than 15

countries In

2011 many

product

innovations

were driven by

this brand

Corona is the

leading beer

in Mexico and

worldrsquos fifth best

selling beer

brand

90 sold in

Mexico and the

US

Antarctica

Pilsen beer is

the 3rd best

selling beer

in Brazil

Itrsquos the largest

best known

beer in

Venezuela

Polar produces

beers and raw

malt

19

Common factors among LatAm

Competing against Soft Drinks

40

24

5 yrs CAGR ()

Beer

CSDs

20

Ambev ndash 30

AB-InBev ndash 50 (Modelo+CND+Regional)

SAB Miller

12

22

2006 2011

54

SAB Miller

11

Common factors among LatAm

Growing Investments and Consolidation

Heineken (+CCU

+Florida)

16

21

2012 Consolidation

Polar Regional

Cerv Centroamericana

Cerv Dominicana

Warsteiner

Schincariol

Paraense

Petropolis

2010

Ajegroup

2010 beer

presentation hellip

22

2012 Consolidation

Polar Cerv Centroamericana

Paraense

Petropolis

2010

Ajegroup

Is there room for

more consolidation

23

2016 LatAm

Incremental Volume 2006 - 2011 - 2016

Beer Oth Alc CSDs

CAGR 06-16

4

CAGR 06-16

2

CAGR 06-16

3

+ 116 Million Hlts

+ 13 Million Hlts

+ 168 Million Hlts

24

2012 Consolidation

Danone Group

Dr Pepper

Snapple Group

Postobon

2010

Ajegroup

Soft drinks companies

Jumex Is there room for

more consolidation

25

USA China Brazil

Spain Germany Italy

Sources of future VOLUME growth

Population +18yrs By 2020 the LatAm young adults

population will reach 207 millions

Annual growth of legal drinking age

population in LatAm +17

26

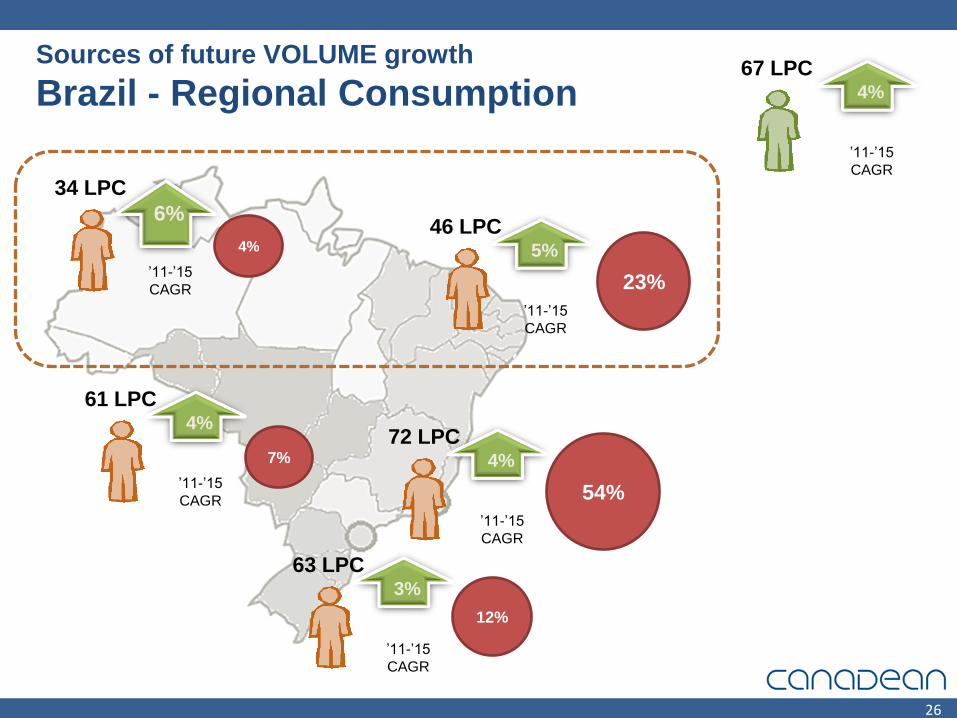

Sources of future VOLUME growth

Brazil - Regional Consumption 4

67 LPC

rsquo11-rsquo15

CAGR

5

46 LPC

rsquo11-rsquo15

CAGR

23

4

72 LPC

rsquo11-rsquo15

CAGR

54

3

63 LPC

rsquo11-rsquo15

CAGR

12

6

34 LPC

rsquo11-rsquo15

CAGR

4

4

61 LPC

rsquo11-rsquo15

CAGR

7

27

Sources of future VOLUME growth

Brazilrsquos Northeast Region

30 of the population

23 of beer consumption

Regional consumption 46 LPC

Brewery locations

Ambev Heineken Schincariol

+ 6 millions Hl by 2015F

Regional segmentation approach

28

$ 4405 millions

$ 6177 millions

$ 1005 millions

$ 1494 millions

$ 394 millions

$ 1347 million dollars

+10 production

capacity

in 2012

+18 investments in

2011 vs 2010

Sources of future VOLUME growth

Ambev continued to invest in capacity to fulfill

the marketrsquos expected growth

29

Latin America

China North America

West Europe

Superpremium

Premium

Mainstream

Discount

Sources of future VALUE growth

Premium amp Super Premium segments

Substantial interest in the high end

segment

Case Examples

Stella Artois shakes up the Argentinian market

15 USD

244 USD

145 USD

16 USD

244 USD

CCU

(Heineken)

SAB

CCU

(Heineken)

0

40

80

2004 2005 2006 2007 2008 2009 2010 2011

Heineken

Stella Artois

25

Case Examples

Mexico Heineken entrance to a brand-saturated market

12

2

12

13

12

Case Examples

Budweiser takes over Sao Paulohellip and Rio

085 USD

090 USD

102 USD

107 USD

115 USD

Premium 36

2005

Premium 58

2011

15

5

33

Industry challenges 2012

Brazil will drive LatAm beer

consumption the north east region is

still the major volume source in the

region

Volume and Value drivers

bull Population

bull Development of Premium

Segments

Room for more consolidationhellip

hardly any MampA in the Soft Drinks

industry

Positive outlook across most of the

markets CAGR 2011-16 +4

Annual growth of legal

drinking age pop in

LatAm +17

LATIN AMERICA BEER MARKET

May 2012

2

Out of 10 litres of beverages consumed in

LatAmhellip

5 lts are non-commercial

beverages

5 lts are commercial

beverages

3

Out of 10 lts of commercial beverages

consumed in LatAmhellip

Soft Drinks lead the

industry with more than 4 lts

Alcoholic Bevs represent 16

lts with Beer accounting for

14 lts

Dairy Hot Drinks etc 44 lts

Dairy Drinks Hot Drinks amp HODBulk water

4

Out of 10 beers consumed in LatAmhellip

4 are purchased away from

home and 8 are consumed in

refillable formats

4 are part of Ambevrsquos portfolio and

2 are sold by Heineken amp

SABMiller together

8 are Mainstream brands

5

Out of 10 beers consumed in LatAmhellip

315 million hectolitres

70 billion Euros

16 of global consumption

6

LatAm is diverse

7

Brazil and Mexico gather more than

50 of LatAm populationhellip

LatAm is diverse

Population 2011 by country

Mexico 21

Brazil 43

Others 36 hellip and almost 65 of

beer consumption

19 36 36 45 50 51 52 54 75 126

281 302 364 374

471

710

1657

2282

-600

-100

400

900

1400

1900

0

50

100

150

200

250

300

350

400

450

500

GDP 2011 (PPP) Beer per cap Total Alc per cap

8

LatAm is diverse

Beer vsTotal Alcohol

9

3072

4240

5426

6919

12615

5023

16019

12520

4875

8372

16078

9958

11390

13480

10038

17382

14514

11892

-6000

-1000

4000

9000

14000

19000

0

100

200

300

400

500

600 GDP per capita (PPP) Beer per cap Total Alc per cap

LatAm is diverse

Beer vsTotal Alcohol

LatAm GDP per capita

(PPP)

11770

10

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

11

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption above

average

12

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption below

average

lowest levels of

alcohol

consumption

LatAm is diverse

Beer vsTotal Alcohol

13

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

Consumption gap due

to local alc bevs

Informal alc bevs

VINO

(JESSICA)

FOTO FOTO

FOT

O

FOTO

Local alcoholic drinks and a

number of local factors boost

alcohol consumption

LatAm is diverse

Beer vsTotal Alcohol

14

1

2

3

4

5

Average price USD 31

25 Euros

Partially driven by the

appreciation of the

Braziliean Real

LatAm is diverse

Price per litre

23

38

15

Common factors among LatAm Countries

16

Common factors among LatAm

Markets are growing above world average

5yrs CAGR 2006-2011 ()

26

42

64

25 37

85

37

40

Global Average

LatAm Average

MEXICO CENTRAL

AMERICA

PERU

CHILE

BRAZIL

ARGENTINA

200

220

240

260

280

300

320

340

360

CAGR lsquo99-rsquo03

1

CAGR rsquo03-rsquo11

5

CAGR rsquo11-rsquo15

4

Venezuela

market falls

15

Mexico amp

Brazil steady

growth

MampA activities

Mexico amp Brazil

drive the

category growth

Beer

consumption

fueled by Brazil

Common factors among LatAm

Markets are expected to continue growing

18

Common factors among LatAm

Lager beer is the norm 99 of the market

Skol is the

leading beer

in Brazil and

worldrsquos fourth

best selling

beer brand

Brahma is

consumed in

more than 15

countries In

2011 many

product

innovations

were driven by

this brand

Corona is the

leading beer

in Mexico and

worldrsquos fifth best

selling beer

brand

90 sold in

Mexico and the

US

Antarctica

Pilsen beer is

the 3rd best

selling beer

in Brazil

Itrsquos the largest

best known

beer in

Venezuela

Polar produces

beers and raw

malt

19

Common factors among LatAm

Competing against Soft Drinks

40

24

5 yrs CAGR ()

Beer

CSDs

20

Ambev ndash 30

AB-InBev ndash 50 (Modelo+CND+Regional)

SAB Miller

12

22

2006 2011

54

SAB Miller

11

Common factors among LatAm

Growing Investments and Consolidation

Heineken (+CCU

+Florida)

16

21

2012 Consolidation

Polar Regional

Cerv Centroamericana

Cerv Dominicana

Warsteiner

Schincariol

Paraense

Petropolis

2010

Ajegroup

2010 beer

presentation hellip

22

2012 Consolidation

Polar Cerv Centroamericana

Paraense

Petropolis

2010

Ajegroup

Is there room for

more consolidation

23

2016 LatAm

Incremental Volume 2006 - 2011 - 2016

Beer Oth Alc CSDs

CAGR 06-16

4

CAGR 06-16

2

CAGR 06-16

3

+ 116 Million Hlts

+ 13 Million Hlts

+ 168 Million Hlts

24

2012 Consolidation

Danone Group

Dr Pepper

Snapple Group

Postobon

2010

Ajegroup

Soft drinks companies

Jumex Is there room for

more consolidation

25

USA China Brazil

Spain Germany Italy

Sources of future VOLUME growth

Population +18yrs By 2020 the LatAm young adults

population will reach 207 millions

Annual growth of legal drinking age

population in LatAm +17

26

Sources of future VOLUME growth

Brazil - Regional Consumption 4

67 LPC

rsquo11-rsquo15

CAGR

5

46 LPC

rsquo11-rsquo15

CAGR

23

4

72 LPC

rsquo11-rsquo15

CAGR

54

3

63 LPC

rsquo11-rsquo15

CAGR

12

6

34 LPC

rsquo11-rsquo15

CAGR

4

4

61 LPC

rsquo11-rsquo15

CAGR

7

27

Sources of future VOLUME growth

Brazilrsquos Northeast Region

30 of the population

23 of beer consumption

Regional consumption 46 LPC

Brewery locations

Ambev Heineken Schincariol

+ 6 millions Hl by 2015F

Regional segmentation approach

28

$ 4405 millions

$ 6177 millions

$ 1005 millions

$ 1494 millions

$ 394 millions

$ 1347 million dollars

+10 production

capacity

in 2012

+18 investments in

2011 vs 2010

Sources of future VOLUME growth

Ambev continued to invest in capacity to fulfill

the marketrsquos expected growth

29

Latin America

China North America

West Europe

Superpremium

Premium

Mainstream

Discount

Sources of future VALUE growth

Premium amp Super Premium segments

Substantial interest in the high end

segment

Case Examples

Stella Artois shakes up the Argentinian market

15 USD

244 USD

145 USD

16 USD

244 USD

CCU

(Heineken)

SAB

CCU

(Heineken)

0

40

80

2004 2005 2006 2007 2008 2009 2010 2011

Heineken

Stella Artois

25

Case Examples

Mexico Heineken entrance to a brand-saturated market

12

2

12

13

12

Case Examples

Budweiser takes over Sao Paulohellip and Rio

085 USD

090 USD

102 USD

107 USD

115 USD

Premium 36

2005

Premium 58

2011

15

5

33

Industry challenges 2012

Brazil will drive LatAm beer

consumption the north east region is

still the major volume source in the

region

Volume and Value drivers

bull Population

bull Development of Premium

Segments

Room for more consolidationhellip

hardly any MampA in the Soft Drinks

industry

Positive outlook across most of the

markets CAGR 2011-16 +4

Annual growth of legal

drinking age pop in

LatAm +17

LATIN AMERICA BEER MARKET

May 2012

3

Out of 10 lts of commercial beverages

consumed in LatAmhellip

Soft Drinks lead the

industry with more than 4 lts

Alcoholic Bevs represent 16

lts with Beer accounting for

14 lts

Dairy Hot Drinks etc 44 lts

Dairy Drinks Hot Drinks amp HODBulk water

4

Out of 10 beers consumed in LatAmhellip

4 are purchased away from

home and 8 are consumed in

refillable formats

4 are part of Ambevrsquos portfolio and

2 are sold by Heineken amp

SABMiller together

8 are Mainstream brands

5

Out of 10 beers consumed in LatAmhellip

315 million hectolitres

70 billion Euros

16 of global consumption

6

LatAm is diverse

7

Brazil and Mexico gather more than

50 of LatAm populationhellip

LatAm is diverse

Population 2011 by country

Mexico 21

Brazil 43

Others 36 hellip and almost 65 of

beer consumption

19 36 36 45 50 51 52 54 75 126

281 302 364 374

471

710

1657

2282

-600

-100

400

900

1400

1900

0

50

100

150

200

250

300

350

400

450

500

GDP 2011 (PPP) Beer per cap Total Alc per cap

8

LatAm is diverse

Beer vsTotal Alcohol

9

3072

4240

5426

6919

12615

5023

16019

12520

4875

8372

16078

9958

11390

13480

10038

17382

14514

11892

-6000

-1000

4000

9000

14000

19000

0

100

200

300

400

500

600 GDP per capita (PPP) Beer per cap Total Alc per cap

LatAm is diverse

Beer vsTotal Alcohol

LatAm GDP per capita

(PPP)

11770

10

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

11

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption above

average

12

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption below

average

lowest levels of

alcohol

consumption

LatAm is diverse

Beer vsTotal Alcohol

13

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

Consumption gap due

to local alc bevs

Informal alc bevs

VINO

(JESSICA)

FOTO FOTO

FOT

O

FOTO

Local alcoholic drinks and a

number of local factors boost

alcohol consumption

LatAm is diverse

Beer vsTotal Alcohol

14

1

2

3

4

5

Average price USD 31

25 Euros

Partially driven by the

appreciation of the

Braziliean Real

LatAm is diverse

Price per litre

23

38

15

Common factors among LatAm Countries

16

Common factors among LatAm

Markets are growing above world average

5yrs CAGR 2006-2011 ()

26

42

64

25 37

85

37

40

Global Average

LatAm Average

MEXICO CENTRAL

AMERICA

PERU

CHILE

BRAZIL

ARGENTINA

200

220

240

260

280

300

320

340

360

CAGR lsquo99-rsquo03

1

CAGR rsquo03-rsquo11

5

CAGR rsquo11-rsquo15

4

Venezuela

market falls

15

Mexico amp

Brazil steady

growth

MampA activities

Mexico amp Brazil

drive the

category growth

Beer

consumption

fueled by Brazil

Common factors among LatAm

Markets are expected to continue growing

18

Common factors among LatAm

Lager beer is the norm 99 of the market

Skol is the

leading beer

in Brazil and

worldrsquos fourth

best selling

beer brand

Brahma is

consumed in

more than 15

countries In

2011 many

product

innovations

were driven by

this brand

Corona is the

leading beer

in Mexico and

worldrsquos fifth best

selling beer

brand

90 sold in

Mexico and the

US

Antarctica

Pilsen beer is

the 3rd best

selling beer

in Brazil

Itrsquos the largest

best known

beer in

Venezuela

Polar produces

beers and raw

malt

19

Common factors among LatAm

Competing against Soft Drinks

40

24

5 yrs CAGR ()

Beer

CSDs

20

Ambev ndash 30

AB-InBev ndash 50 (Modelo+CND+Regional)

SAB Miller

12

22

2006 2011

54

SAB Miller

11

Common factors among LatAm

Growing Investments and Consolidation

Heineken (+CCU

+Florida)

16

21

2012 Consolidation

Polar Regional

Cerv Centroamericana

Cerv Dominicana

Warsteiner

Schincariol

Paraense

Petropolis

2010

Ajegroup

2010 beer

presentation hellip

22

2012 Consolidation

Polar Cerv Centroamericana

Paraense

Petropolis

2010

Ajegroup

Is there room for

more consolidation

23

2016 LatAm

Incremental Volume 2006 - 2011 - 2016

Beer Oth Alc CSDs

CAGR 06-16

4

CAGR 06-16

2

CAGR 06-16

3

+ 116 Million Hlts

+ 13 Million Hlts

+ 168 Million Hlts

24

2012 Consolidation

Danone Group

Dr Pepper

Snapple Group

Postobon

2010

Ajegroup

Soft drinks companies

Jumex Is there room for

more consolidation

25

USA China Brazil

Spain Germany Italy

Sources of future VOLUME growth

Population +18yrs By 2020 the LatAm young adults

population will reach 207 millions

Annual growth of legal drinking age

population in LatAm +17

26

Sources of future VOLUME growth

Brazil - Regional Consumption 4

67 LPC

rsquo11-rsquo15

CAGR

5

46 LPC

rsquo11-rsquo15

CAGR

23

4

72 LPC

rsquo11-rsquo15

CAGR

54

3

63 LPC

rsquo11-rsquo15

CAGR

12

6

34 LPC

rsquo11-rsquo15

CAGR

4

4

61 LPC

rsquo11-rsquo15

CAGR

7

27

Sources of future VOLUME growth

Brazilrsquos Northeast Region

30 of the population

23 of beer consumption

Regional consumption 46 LPC

Brewery locations

Ambev Heineken Schincariol

+ 6 millions Hl by 2015F

Regional segmentation approach

28

$ 4405 millions

$ 6177 millions

$ 1005 millions

$ 1494 millions

$ 394 millions

$ 1347 million dollars

+10 production

capacity

in 2012

+18 investments in

2011 vs 2010

Sources of future VOLUME growth

Ambev continued to invest in capacity to fulfill

the marketrsquos expected growth

29

Latin America

China North America

West Europe

Superpremium

Premium

Mainstream

Discount

Sources of future VALUE growth

Premium amp Super Premium segments

Substantial interest in the high end

segment

Case Examples

Stella Artois shakes up the Argentinian market

15 USD

244 USD

145 USD

16 USD

244 USD

CCU

(Heineken)

SAB

CCU

(Heineken)

0

40

80

2004 2005 2006 2007 2008 2009 2010 2011

Heineken

Stella Artois

25

Case Examples

Mexico Heineken entrance to a brand-saturated market

12

2

12

13

12

Case Examples

Budweiser takes over Sao Paulohellip and Rio

085 USD

090 USD

102 USD

107 USD

115 USD

Premium 36

2005

Premium 58

2011

15

5

33

Industry challenges 2012

Brazil will drive LatAm beer

consumption the north east region is

still the major volume source in the

region

Volume and Value drivers

bull Population

bull Development of Premium

Segments

Room for more consolidationhellip

hardly any MampA in the Soft Drinks

industry

Positive outlook across most of the

markets CAGR 2011-16 +4

Annual growth of legal

drinking age pop in

LatAm +17

LATIN AMERICA BEER MARKET

May 2012

4

Out of 10 beers consumed in LatAmhellip

4 are purchased away from

home and 8 are consumed in

refillable formats

4 are part of Ambevrsquos portfolio and

2 are sold by Heineken amp

SABMiller together

8 are Mainstream brands

5

Out of 10 beers consumed in LatAmhellip

315 million hectolitres

70 billion Euros

16 of global consumption

6

LatAm is diverse

7

Brazil and Mexico gather more than

50 of LatAm populationhellip

LatAm is diverse

Population 2011 by country

Mexico 21

Brazil 43

Others 36 hellip and almost 65 of

beer consumption

19 36 36 45 50 51 52 54 75 126

281 302 364 374

471

710

1657

2282

-600

-100

400

900

1400

1900

0

50

100

150

200

250

300

350

400

450

500

GDP 2011 (PPP) Beer per cap Total Alc per cap

8

LatAm is diverse

Beer vsTotal Alcohol

9

3072

4240

5426

6919

12615

5023

16019

12520

4875

8372

16078

9958

11390

13480

10038

17382

14514

11892

-6000

-1000

4000

9000

14000

19000

0

100

200

300

400

500

600 GDP per capita (PPP) Beer per cap Total Alc per cap

LatAm is diverse

Beer vsTotal Alcohol

LatAm GDP per capita

(PPP)

11770

10

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

11

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption above

average

12

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption below

average

lowest levels of

alcohol

consumption

LatAm is diverse

Beer vsTotal Alcohol

13

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

Consumption gap due

to local alc bevs

Informal alc bevs

VINO

(JESSICA)

FOTO FOTO

FOT

O

FOTO

Local alcoholic drinks and a

number of local factors boost

alcohol consumption

LatAm is diverse

Beer vsTotal Alcohol

14

1

2

3

4

5

Average price USD 31

25 Euros

Partially driven by the

appreciation of the

Braziliean Real

LatAm is diverse

Price per litre

23

38

15

Common factors among LatAm Countries

16

Common factors among LatAm

Markets are growing above world average

5yrs CAGR 2006-2011 ()

26

42

64

25 37

85

37

40

Global Average

LatAm Average

MEXICO CENTRAL

AMERICA

PERU

CHILE

BRAZIL

ARGENTINA

200

220

240

260

280

300

320

340

360

CAGR lsquo99-rsquo03

1

CAGR rsquo03-rsquo11

5

CAGR rsquo11-rsquo15

4

Venezuela

market falls

15

Mexico amp

Brazil steady

growth

MampA activities

Mexico amp Brazil

drive the

category growth

Beer

consumption

fueled by Brazil

Common factors among LatAm

Markets are expected to continue growing

18

Common factors among LatAm

Lager beer is the norm 99 of the market

Skol is the

leading beer

in Brazil and

worldrsquos fourth

best selling

beer brand

Brahma is

consumed in

more than 15

countries In

2011 many

product

innovations

were driven by

this brand

Corona is the

leading beer

in Mexico and

worldrsquos fifth best

selling beer

brand

90 sold in

Mexico and the

US

Antarctica

Pilsen beer is

the 3rd best

selling beer

in Brazil

Itrsquos the largest

best known

beer in

Venezuela

Polar produces

beers and raw

malt

19

Common factors among LatAm

Competing against Soft Drinks

40

24

5 yrs CAGR ()

Beer

CSDs

20

Ambev ndash 30

AB-InBev ndash 50 (Modelo+CND+Regional)

SAB Miller

12

22

2006 2011

54

SAB Miller

11

Common factors among LatAm

Growing Investments and Consolidation

Heineken (+CCU

+Florida)

16

21

2012 Consolidation

Polar Regional

Cerv Centroamericana

Cerv Dominicana

Warsteiner

Schincariol

Paraense

Petropolis

2010

Ajegroup

2010 beer

presentation hellip

22

2012 Consolidation

Polar Cerv Centroamericana

Paraense

Petropolis

2010

Ajegroup

Is there room for

more consolidation

23

2016 LatAm

Incremental Volume 2006 - 2011 - 2016

Beer Oth Alc CSDs

CAGR 06-16

4

CAGR 06-16

2

CAGR 06-16

3

+ 116 Million Hlts

+ 13 Million Hlts

+ 168 Million Hlts

24

2012 Consolidation

Danone Group

Dr Pepper

Snapple Group

Postobon

2010

Ajegroup

Soft drinks companies

Jumex Is there room for

more consolidation

25

USA China Brazil

Spain Germany Italy

Sources of future VOLUME growth

Population +18yrs By 2020 the LatAm young adults

population will reach 207 millions

Annual growth of legal drinking age

population in LatAm +17

26

Sources of future VOLUME growth

Brazil - Regional Consumption 4

67 LPC

rsquo11-rsquo15

CAGR

5

46 LPC

rsquo11-rsquo15

CAGR

23

4

72 LPC

rsquo11-rsquo15

CAGR

54

3

63 LPC

rsquo11-rsquo15

CAGR

12

6

34 LPC

rsquo11-rsquo15

CAGR

4

4

61 LPC

rsquo11-rsquo15

CAGR

7

27

Sources of future VOLUME growth

Brazilrsquos Northeast Region

30 of the population

23 of beer consumption

Regional consumption 46 LPC

Brewery locations

Ambev Heineken Schincariol

+ 6 millions Hl by 2015F

Regional segmentation approach

28

$ 4405 millions

$ 6177 millions

$ 1005 millions

$ 1494 millions

$ 394 millions

$ 1347 million dollars

+10 production

capacity

in 2012

+18 investments in

2011 vs 2010

Sources of future VOLUME growth

Ambev continued to invest in capacity to fulfill

the marketrsquos expected growth

29

Latin America

China North America

West Europe

Superpremium

Premium

Mainstream

Discount

Sources of future VALUE growth

Premium amp Super Premium segments

Substantial interest in the high end

segment

Case Examples

Stella Artois shakes up the Argentinian market

15 USD

244 USD

145 USD

16 USD

244 USD

CCU

(Heineken)

SAB

CCU

(Heineken)

0

40

80

2004 2005 2006 2007 2008 2009 2010 2011

Heineken

Stella Artois

25

Case Examples

Mexico Heineken entrance to a brand-saturated market

12

2

12

13

12

Case Examples

Budweiser takes over Sao Paulohellip and Rio

085 USD

090 USD

102 USD

107 USD

115 USD

Premium 36

2005

Premium 58

2011

15

5

33

Industry challenges 2012

Brazil will drive LatAm beer

consumption the north east region is

still the major volume source in the

region

Volume and Value drivers

bull Population

bull Development of Premium

Segments

Room for more consolidationhellip

hardly any MampA in the Soft Drinks

industry

Positive outlook across most of the

markets CAGR 2011-16 +4

Annual growth of legal

drinking age pop in

LatAm +17

LATIN AMERICA BEER MARKET

May 2012

5

Out of 10 beers consumed in LatAmhellip

315 million hectolitres

70 billion Euros

16 of global consumption

6

LatAm is diverse

7

Brazil and Mexico gather more than

50 of LatAm populationhellip

LatAm is diverse

Population 2011 by country

Mexico 21

Brazil 43

Others 36 hellip and almost 65 of

beer consumption

19 36 36 45 50 51 52 54 75 126

281 302 364 374

471

710

1657

2282

-600

-100

400

900

1400

1900

0

50

100

150

200

250

300

350

400

450

500

GDP 2011 (PPP) Beer per cap Total Alc per cap

8

LatAm is diverse

Beer vsTotal Alcohol

9

3072

4240

5426

6919

12615

5023

16019

12520

4875

8372

16078

9958

11390

13480

10038

17382

14514

11892

-6000

-1000

4000

9000

14000

19000

0

100

200

300

400

500

600 GDP per capita (PPP) Beer per cap Total Alc per cap

LatAm is diverse

Beer vsTotal Alcohol

LatAm GDP per capita

(PPP)

11770

10

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

11

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption above

average

12

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption below

average

lowest levels of

alcohol

consumption

LatAm is diverse

Beer vsTotal Alcohol

13

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

Consumption gap due

to local alc bevs

Informal alc bevs

VINO

(JESSICA)

FOTO FOTO

FOT

O

FOTO

Local alcoholic drinks and a

number of local factors boost

alcohol consumption

LatAm is diverse

Beer vsTotal Alcohol

14

1

2

3

4

5

Average price USD 31

25 Euros

Partially driven by the

appreciation of the

Braziliean Real

LatAm is diverse

Price per litre

23

38

15

Common factors among LatAm Countries

16

Common factors among LatAm

Markets are growing above world average

5yrs CAGR 2006-2011 ()

26

42

64

25 37

85

37

40

Global Average

LatAm Average

MEXICO CENTRAL

AMERICA

PERU

CHILE

BRAZIL

ARGENTINA

200

220

240

260

280

300

320

340

360

CAGR lsquo99-rsquo03

1

CAGR rsquo03-rsquo11

5

CAGR rsquo11-rsquo15

4

Venezuela

market falls

15

Mexico amp

Brazil steady

growth

MampA activities

Mexico amp Brazil

drive the

category growth

Beer

consumption

fueled by Brazil

Common factors among LatAm

Markets are expected to continue growing

18

Common factors among LatAm

Lager beer is the norm 99 of the market

Skol is the

leading beer

in Brazil and

worldrsquos fourth

best selling

beer brand

Brahma is

consumed in

more than 15

countries In

2011 many

product

innovations

were driven by

this brand

Corona is the

leading beer

in Mexico and

worldrsquos fifth best

selling beer

brand

90 sold in

Mexico and the

US

Antarctica

Pilsen beer is

the 3rd best

selling beer

in Brazil

Itrsquos the largest

best known

beer in

Venezuela

Polar produces

beers and raw

malt

19

Common factors among LatAm

Competing against Soft Drinks

40

24

5 yrs CAGR ()

Beer

CSDs

20

Ambev ndash 30

AB-InBev ndash 50 (Modelo+CND+Regional)

SAB Miller

12

22

2006 2011

54

SAB Miller

11

Common factors among LatAm

Growing Investments and Consolidation

Heineken (+CCU

+Florida)

16

21

2012 Consolidation

Polar Regional

Cerv Centroamericana

Cerv Dominicana

Warsteiner

Schincariol

Paraense

Petropolis

2010

Ajegroup

2010 beer

presentation hellip

22

2012 Consolidation

Polar Cerv Centroamericana

Paraense

Petropolis

2010

Ajegroup

Is there room for

more consolidation

23

2016 LatAm

Incremental Volume 2006 - 2011 - 2016

Beer Oth Alc CSDs

CAGR 06-16

4

CAGR 06-16

2

CAGR 06-16

3

+ 116 Million Hlts

+ 13 Million Hlts

+ 168 Million Hlts

24

2012 Consolidation

Danone Group

Dr Pepper

Snapple Group

Postobon

2010

Ajegroup

Soft drinks companies

Jumex Is there room for

more consolidation

25

USA China Brazil

Spain Germany Italy

Sources of future VOLUME growth

Population +18yrs By 2020 the LatAm young adults

population will reach 207 millions

Annual growth of legal drinking age

population in LatAm +17

26

Sources of future VOLUME growth

Brazil - Regional Consumption 4

67 LPC

rsquo11-rsquo15

CAGR

5

46 LPC

rsquo11-rsquo15

CAGR

23

4

72 LPC

rsquo11-rsquo15

CAGR

54

3

63 LPC

rsquo11-rsquo15

CAGR

12

6

34 LPC

rsquo11-rsquo15

CAGR

4

4

61 LPC

rsquo11-rsquo15

CAGR

7

27

Sources of future VOLUME growth

Brazilrsquos Northeast Region

30 of the population

23 of beer consumption

Regional consumption 46 LPC

Brewery locations

Ambev Heineken Schincariol

+ 6 millions Hl by 2015F

Regional segmentation approach

28

$ 4405 millions

$ 6177 millions

$ 1005 millions

$ 1494 millions

$ 394 millions

$ 1347 million dollars

+10 production

capacity

in 2012

+18 investments in

2011 vs 2010

Sources of future VOLUME growth

Ambev continued to invest in capacity to fulfill

the marketrsquos expected growth

29

Latin America

China North America

West Europe

Superpremium

Premium

Mainstream

Discount

Sources of future VALUE growth

Premium amp Super Premium segments

Substantial interest in the high end

segment

Case Examples

Stella Artois shakes up the Argentinian market

15 USD

244 USD

145 USD

16 USD

244 USD

CCU

(Heineken)

SAB

CCU

(Heineken)

0

40

80

2004 2005 2006 2007 2008 2009 2010 2011

Heineken

Stella Artois

25

Case Examples

Mexico Heineken entrance to a brand-saturated market

12

2

12

13

12

Case Examples

Budweiser takes over Sao Paulohellip and Rio

085 USD

090 USD

102 USD

107 USD

115 USD

Premium 36

2005

Premium 58

2011

15

5

33

Industry challenges 2012

Brazil will drive LatAm beer

consumption the north east region is

still the major volume source in the

region

Volume and Value drivers

bull Population

bull Development of Premium

Segments

Room for more consolidationhellip

hardly any MampA in the Soft Drinks

industry

Positive outlook across most of the

markets CAGR 2011-16 +4

Annual growth of legal

drinking age pop in

LatAm +17

LATIN AMERICA BEER MARKET

May 2012

6

LatAm is diverse

7

Brazil and Mexico gather more than

50 of LatAm populationhellip

LatAm is diverse

Population 2011 by country

Mexico 21

Brazil 43

Others 36 hellip and almost 65 of

beer consumption

19 36 36 45 50 51 52 54 75 126

281 302 364 374

471

710

1657

2282

-600

-100

400

900

1400

1900

0

50

100

150

200

250

300

350

400

450

500

GDP 2011 (PPP) Beer per cap Total Alc per cap

8

LatAm is diverse

Beer vsTotal Alcohol

9

3072

4240

5426

6919

12615

5023

16019

12520

4875

8372

16078

9958

11390

13480

10038

17382

14514

11892

-6000

-1000

4000

9000

14000

19000

0

100

200

300

400

500

600 GDP per capita (PPP) Beer per cap Total Alc per cap

LatAm is diverse

Beer vsTotal Alcohol

LatAm GDP per capita

(PPP)

11770

10

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

11

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption above

average

12

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption below

average

lowest levels of

alcohol

consumption

LatAm is diverse

Beer vsTotal Alcohol

13

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

Consumption gap due

to local alc bevs

Informal alc bevs

VINO

(JESSICA)

FOTO FOTO

FOT

O

FOTO

Local alcoholic drinks and a

number of local factors boost

alcohol consumption

LatAm is diverse

Beer vsTotal Alcohol

14

1

2

3

4

5

Average price USD 31

25 Euros

Partially driven by the

appreciation of the

Braziliean Real

LatAm is diverse

Price per litre

23

38

15

Common factors among LatAm Countries

16

Common factors among LatAm

Markets are growing above world average

5yrs CAGR 2006-2011 ()

26

42

64

25 37

85

37

40

Global Average

LatAm Average

MEXICO CENTRAL

AMERICA

PERU

CHILE

BRAZIL

ARGENTINA

200

220

240

260

280

300

320

340

360

CAGR lsquo99-rsquo03

1

CAGR rsquo03-rsquo11

5

CAGR rsquo11-rsquo15

4

Venezuela

market falls

15

Mexico amp

Brazil steady

growth

MampA activities

Mexico amp Brazil

drive the

category growth

Beer

consumption

fueled by Brazil

Common factors among LatAm

Markets are expected to continue growing

18

Common factors among LatAm

Lager beer is the norm 99 of the market

Skol is the

leading beer

in Brazil and

worldrsquos fourth

best selling

beer brand

Brahma is

consumed in

more than 15

countries In

2011 many

product

innovations

were driven by

this brand

Corona is the

leading beer

in Mexico and

worldrsquos fifth best

selling beer

brand

90 sold in

Mexico and the

US

Antarctica

Pilsen beer is

the 3rd best

selling beer

in Brazil

Itrsquos the largest

best known

beer in

Venezuela

Polar produces

beers and raw

malt

19

Common factors among LatAm

Competing against Soft Drinks

40

24

5 yrs CAGR ()

Beer

CSDs

20

Ambev ndash 30

AB-InBev ndash 50 (Modelo+CND+Regional)

SAB Miller

12

22

2006 2011

54

SAB Miller

11

Common factors among LatAm

Growing Investments and Consolidation

Heineken (+CCU

+Florida)

16

21

2012 Consolidation

Polar Regional

Cerv Centroamericana

Cerv Dominicana

Warsteiner

Schincariol

Paraense

Petropolis

2010

Ajegroup

2010 beer

presentation hellip

22

2012 Consolidation

Polar Cerv Centroamericana

Paraense

Petropolis

2010

Ajegroup

Is there room for

more consolidation

23

2016 LatAm

Incremental Volume 2006 - 2011 - 2016

Beer Oth Alc CSDs

CAGR 06-16

4

CAGR 06-16

2

CAGR 06-16

3

+ 116 Million Hlts

+ 13 Million Hlts

+ 168 Million Hlts

24

2012 Consolidation

Danone Group

Dr Pepper

Snapple Group

Postobon

2010

Ajegroup

Soft drinks companies

Jumex Is there room for

more consolidation

25

USA China Brazil

Spain Germany Italy

Sources of future VOLUME growth

Population +18yrs By 2020 the LatAm young adults

population will reach 207 millions

Annual growth of legal drinking age

population in LatAm +17

26

Sources of future VOLUME growth

Brazil - Regional Consumption 4

67 LPC

rsquo11-rsquo15

CAGR

5

46 LPC

rsquo11-rsquo15

CAGR

23

4

72 LPC

rsquo11-rsquo15

CAGR

54

3

63 LPC

rsquo11-rsquo15

CAGR

12

6

34 LPC

rsquo11-rsquo15

CAGR

4

4

61 LPC

rsquo11-rsquo15

CAGR

7

27

Sources of future VOLUME growth

Brazilrsquos Northeast Region

30 of the population

23 of beer consumption

Regional consumption 46 LPC

Brewery locations

Ambev Heineken Schincariol

+ 6 millions Hl by 2015F

Regional segmentation approach

28

$ 4405 millions

$ 6177 millions

$ 1005 millions

$ 1494 millions

$ 394 millions

$ 1347 million dollars

+10 production

capacity

in 2012

+18 investments in

2011 vs 2010

Sources of future VOLUME growth

Ambev continued to invest in capacity to fulfill

the marketrsquos expected growth

29

Latin America

China North America

West Europe

Superpremium

Premium

Mainstream

Discount

Sources of future VALUE growth

Premium amp Super Premium segments

Substantial interest in the high end

segment

Case Examples

Stella Artois shakes up the Argentinian market

15 USD

244 USD

145 USD

16 USD

244 USD

CCU

(Heineken)

SAB

CCU

(Heineken)

0

40

80

2004 2005 2006 2007 2008 2009 2010 2011

Heineken

Stella Artois

25

Case Examples

Mexico Heineken entrance to a brand-saturated market

12

2

12

13

12

Case Examples

Budweiser takes over Sao Paulohellip and Rio

085 USD

090 USD

102 USD

107 USD

115 USD

Premium 36

2005

Premium 58

2011

15

5

33

Industry challenges 2012

Brazil will drive LatAm beer

consumption the north east region is

still the major volume source in the

region

Volume and Value drivers

bull Population

bull Development of Premium

Segments

Room for more consolidationhellip

hardly any MampA in the Soft Drinks

industry

Positive outlook across most of the

markets CAGR 2011-16 +4

Annual growth of legal

drinking age pop in

LatAm +17

LATIN AMERICA BEER MARKET

May 2012

7

Brazil and Mexico gather more than

50 of LatAm populationhellip

LatAm is diverse

Population 2011 by country

Mexico 21

Brazil 43

Others 36 hellip and almost 65 of

beer consumption

19 36 36 45 50 51 52 54 75 126

281 302 364 374

471

710

1657

2282

-600

-100

400

900

1400

1900

0

50

100

150

200

250

300

350

400

450

500

GDP 2011 (PPP) Beer per cap Total Alc per cap

8

LatAm is diverse

Beer vsTotal Alcohol

9

3072

4240

5426

6919

12615

5023

16019

12520

4875

8372

16078

9958

11390

13480

10038

17382

14514

11892

-6000

-1000

4000

9000

14000

19000

0

100

200

300

400

500

600 GDP per capita (PPP) Beer per cap Total Alc per cap

LatAm is diverse

Beer vsTotal Alcohol

LatAm GDP per capita

(PPP)

11770

10

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

11

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption above

average

12

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption below

average

lowest levels of

alcohol

consumption

LatAm is diverse

Beer vsTotal Alcohol

13

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

Consumption gap due

to local alc bevs

Informal alc bevs

VINO

(JESSICA)

FOTO FOTO

FOT

O

FOTO

Local alcoholic drinks and a

number of local factors boost

alcohol consumption

LatAm is diverse

Beer vsTotal Alcohol

14

1

2

3

4

5

Average price USD 31

25 Euros

Partially driven by the

appreciation of the

Braziliean Real

LatAm is diverse

Price per litre

23

38

15

Common factors among LatAm Countries

16

Common factors among LatAm

Markets are growing above world average

5yrs CAGR 2006-2011 ()

26

42

64

25 37

85

37

40

Global Average

LatAm Average

MEXICO CENTRAL

AMERICA

PERU

CHILE

BRAZIL

ARGENTINA

200

220

240

260

280

300

320

340

360

CAGR lsquo99-rsquo03

1

CAGR rsquo03-rsquo11

5

CAGR rsquo11-rsquo15

4

Venezuela

market falls

15

Mexico amp

Brazil steady

growth

MampA activities

Mexico amp Brazil

drive the

category growth

Beer

consumption

fueled by Brazil

Common factors among LatAm

Markets are expected to continue growing

18

Common factors among LatAm

Lager beer is the norm 99 of the market

Skol is the

leading beer

in Brazil and

worldrsquos fourth

best selling

beer brand

Brahma is

consumed in

more than 15

countries In

2011 many

product

innovations

were driven by

this brand

Corona is the

leading beer

in Mexico and

worldrsquos fifth best

selling beer

brand

90 sold in

Mexico and the

US

Antarctica

Pilsen beer is

the 3rd best

selling beer

in Brazil

Itrsquos the largest

best known

beer in

Venezuela

Polar produces

beers and raw

malt

19

Common factors among LatAm

Competing against Soft Drinks

40

24

5 yrs CAGR ()

Beer

CSDs

20

Ambev ndash 30

AB-InBev ndash 50 (Modelo+CND+Regional)

SAB Miller

12

22

2006 2011

54

SAB Miller

11

Common factors among LatAm

Growing Investments and Consolidation

Heineken (+CCU

+Florida)

16

21

2012 Consolidation

Polar Regional

Cerv Centroamericana

Cerv Dominicana

Warsteiner

Schincariol

Paraense

Petropolis

2010

Ajegroup

2010 beer

presentation hellip

22

2012 Consolidation

Polar Cerv Centroamericana

Paraense

Petropolis

2010

Ajegroup

Is there room for

more consolidation

23

2016 LatAm

Incremental Volume 2006 - 2011 - 2016

Beer Oth Alc CSDs

CAGR 06-16

4

CAGR 06-16

2

CAGR 06-16

3

+ 116 Million Hlts

+ 13 Million Hlts

+ 168 Million Hlts

24

2012 Consolidation

Danone Group

Dr Pepper

Snapple Group

Postobon

2010

Ajegroup

Soft drinks companies

Jumex Is there room for

more consolidation

25

USA China Brazil

Spain Germany Italy

Sources of future VOLUME growth

Population +18yrs By 2020 the LatAm young adults

population will reach 207 millions

Annual growth of legal drinking age

population in LatAm +17

26

Sources of future VOLUME growth

Brazil - Regional Consumption 4

67 LPC

rsquo11-rsquo15

CAGR

5

46 LPC

rsquo11-rsquo15

CAGR

23

4

72 LPC

rsquo11-rsquo15

CAGR

54

3

63 LPC

rsquo11-rsquo15

CAGR

12

6

34 LPC

rsquo11-rsquo15

CAGR

4

4

61 LPC

rsquo11-rsquo15

CAGR

7

27

Sources of future VOLUME growth

Brazilrsquos Northeast Region

30 of the population

23 of beer consumption

Regional consumption 46 LPC

Brewery locations

Ambev Heineken Schincariol

+ 6 millions Hl by 2015F

Regional segmentation approach

28

$ 4405 millions

$ 6177 millions

$ 1005 millions

$ 1494 millions

$ 394 millions

$ 1347 million dollars

+10 production

capacity

in 2012

+18 investments in

2011 vs 2010

Sources of future VOLUME growth

Ambev continued to invest in capacity to fulfill

the marketrsquos expected growth

29

Latin America

China North America

West Europe

Superpremium

Premium

Mainstream

Discount

Sources of future VALUE growth

Premium amp Super Premium segments

Substantial interest in the high end

segment

Case Examples

Stella Artois shakes up the Argentinian market

15 USD

244 USD

145 USD

16 USD

244 USD

CCU

(Heineken)

SAB

CCU

(Heineken)

0

40

80

2004 2005 2006 2007 2008 2009 2010 2011

Heineken

Stella Artois

25

Case Examples

Mexico Heineken entrance to a brand-saturated market

12

2

12

13

12

Case Examples

Budweiser takes over Sao Paulohellip and Rio

085 USD

090 USD

102 USD

107 USD

115 USD

Premium 36

2005

Premium 58

2011

15

5

33

Industry challenges 2012

Brazil will drive LatAm beer

consumption the north east region is

still the major volume source in the

region

Volume and Value drivers

bull Population

bull Development of Premium

Segments

Room for more consolidationhellip

hardly any MampA in the Soft Drinks

industry

Positive outlook across most of the

markets CAGR 2011-16 +4

Annual growth of legal

drinking age pop in

LatAm +17

LATIN AMERICA BEER MARKET

May 2012

19 36 36 45 50 51 52 54 75 126

281 302 364 374

471

710

1657

2282

-600

-100

400

900

1400

1900

0

50

100

150

200

250

300

350

400

450

500

GDP 2011 (PPP) Beer per cap Total Alc per cap

8

LatAm is diverse

Beer vsTotal Alcohol

9

3072

4240

5426

6919

12615

5023

16019

12520

4875

8372

16078

9958

11390

13480

10038

17382

14514

11892

-6000

-1000

4000

9000

14000

19000

0

100

200

300

400

500

600 GDP per capita (PPP) Beer per cap Total Alc per cap

LatAm is diverse

Beer vsTotal Alcohol

LatAm GDP per capita

(PPP)

11770

10

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

11

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption above

average

12

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption below

average

lowest levels of

alcohol

consumption

LatAm is diverse

Beer vsTotal Alcohol

13

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

Consumption gap due

to local alc bevs

Informal alc bevs

VINO

(JESSICA)

FOTO FOTO

FOT

O

FOTO

Local alcoholic drinks and a

number of local factors boost

alcohol consumption

LatAm is diverse

Beer vsTotal Alcohol

14

1

2

3

4

5

Average price USD 31

25 Euros

Partially driven by the

appreciation of the

Braziliean Real

LatAm is diverse

Price per litre

23

38

15

Common factors among LatAm Countries

16

Common factors among LatAm

Markets are growing above world average

5yrs CAGR 2006-2011 ()

26

42

64

25 37

85

37

40

Global Average

LatAm Average

MEXICO CENTRAL

AMERICA

PERU

CHILE

BRAZIL

ARGENTINA

200

220

240

260

280

300

320

340

360

CAGR lsquo99-rsquo03

1

CAGR rsquo03-rsquo11

5

CAGR rsquo11-rsquo15

4

Venezuela

market falls

15

Mexico amp

Brazil steady

growth

MampA activities

Mexico amp Brazil

drive the

category growth

Beer

consumption

fueled by Brazil

Common factors among LatAm

Markets are expected to continue growing

18

Common factors among LatAm

Lager beer is the norm 99 of the market

Skol is the

leading beer

in Brazil and

worldrsquos fourth

best selling

beer brand

Brahma is

consumed in

more than 15

countries In

2011 many

product

innovations

were driven by

this brand

Corona is the

leading beer

in Mexico and

worldrsquos fifth best

selling beer

brand

90 sold in

Mexico and the

US

Antarctica

Pilsen beer is

the 3rd best

selling beer

in Brazil

Itrsquos the largest

best known

beer in

Venezuela

Polar produces

beers and raw

malt

19

Common factors among LatAm

Competing against Soft Drinks

40

24

5 yrs CAGR ()

Beer

CSDs

20

Ambev ndash 30

AB-InBev ndash 50 (Modelo+CND+Regional)

SAB Miller

12

22

2006 2011

54

SAB Miller

11

Common factors among LatAm

Growing Investments and Consolidation

Heineken (+CCU

+Florida)

16

21

2012 Consolidation

Polar Regional

Cerv Centroamericana

Cerv Dominicana

Warsteiner

Schincariol

Paraense

Petropolis

2010

Ajegroup

2010 beer

presentation hellip

22

2012 Consolidation

Polar Cerv Centroamericana

Paraense

Petropolis

2010

Ajegroup

Is there room for

more consolidation

23

2016 LatAm

Incremental Volume 2006 - 2011 - 2016

Beer Oth Alc CSDs

CAGR 06-16

4

CAGR 06-16

2

CAGR 06-16

3

+ 116 Million Hlts

+ 13 Million Hlts

+ 168 Million Hlts

24

2012 Consolidation

Danone Group

Dr Pepper

Snapple Group

Postobon

2010

Ajegroup

Soft drinks companies

Jumex Is there room for

more consolidation

25

USA China Brazil

Spain Germany Italy

Sources of future VOLUME growth

Population +18yrs By 2020 the LatAm young adults

population will reach 207 millions

Annual growth of legal drinking age

population in LatAm +17

26

Sources of future VOLUME growth

Brazil - Regional Consumption 4

67 LPC

rsquo11-rsquo15

CAGR

5

46 LPC

rsquo11-rsquo15

CAGR

23

4

72 LPC

rsquo11-rsquo15

CAGR

54

3

63 LPC

rsquo11-rsquo15

CAGR

12

6

34 LPC

rsquo11-rsquo15

CAGR

4

4

61 LPC

rsquo11-rsquo15

CAGR

7

27

Sources of future VOLUME growth

Brazilrsquos Northeast Region

30 of the population

23 of beer consumption

Regional consumption 46 LPC

Brewery locations

Ambev Heineken Schincariol

+ 6 millions Hl by 2015F

Regional segmentation approach

28

$ 4405 millions

$ 6177 millions

$ 1005 millions

$ 1494 millions

$ 394 millions

$ 1347 million dollars

+10 production

capacity

in 2012

+18 investments in

2011 vs 2010

Sources of future VOLUME growth

Ambev continued to invest in capacity to fulfill

the marketrsquos expected growth

29

Latin America

China North America

West Europe

Superpremium

Premium

Mainstream

Discount

Sources of future VALUE growth

Premium amp Super Premium segments

Substantial interest in the high end

segment

Case Examples

Stella Artois shakes up the Argentinian market

15 USD

244 USD

145 USD

16 USD

244 USD

CCU

(Heineken)

SAB

CCU

(Heineken)

0

40

80

2004 2005 2006 2007 2008 2009 2010 2011

Heineken

Stella Artois

25

Case Examples

Mexico Heineken entrance to a brand-saturated market

12

2

12

13

12

Case Examples

Budweiser takes over Sao Paulohellip and Rio

085 USD

090 USD

102 USD

107 USD

115 USD

Premium 36

2005

Premium 58

2011

15

5

33

Industry challenges 2012

Brazil will drive LatAm beer

consumption the north east region is

still the major volume source in the

region

Volume and Value drivers

bull Population

bull Development of Premium

Segments

Room for more consolidationhellip

hardly any MampA in the Soft Drinks

industry

Positive outlook across most of the

markets CAGR 2011-16 +4

Annual growth of legal

drinking age pop in

LatAm +17

LATIN AMERICA BEER MARKET

May 2012

9

3072

4240

5426

6919

12615

5023

16019

12520

4875

8372

16078

9958

11390

13480

10038

17382

14514

11892

-6000

-1000

4000

9000

14000

19000

0

100

200

300

400

500

600 GDP per capita (PPP) Beer per cap Total Alc per cap

LatAm is diverse

Beer vsTotal Alcohol

LatAm GDP per capita

(PPP)

11770

10

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

11

LatAm is diverse

Beer vsTotal Alcohol

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption above

average

12

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

51 LPC

41 LPC

Consumption below

average

lowest levels of

alcohol

consumption

LatAm is diverse

Beer vsTotal Alcohol

13

0

10

20

30

40

50

60

70

80

90

100

Beer per cap Total Alc per cap

Consumption gap due

to local alc bevs

Informal alc bevs

VINO

(JESSICA)

FOTO FOTO

FOT

O

FOTO

Local alcoholic drinks and a

number of local factors boost

alcohol consumption

LatAm is diverse

Beer vsTotal Alcohol

14

1

2

3

4

5

Average price USD 31

25 Euros

Partially driven by the

appreciation of the

Braziliean Real

LatAm is diverse

Price per litre

23

38

15

Common factors among LatAm Countries

16

Common factors among LatAm

Markets are growing above world average

5yrs CAGR 2006-2011 ()

26

42

64

25 37

85

37

40

Global Average

LatAm Average

MEXICO CENTRAL

AMERICA

PERU

CHILE

BRAZIL

ARGENTINA

200

220

240

260

280

300

320

340

360

CAGR lsquo99-rsquo03

1

CAGR rsquo03-rsquo11

5

CAGR rsquo11-rsquo15

4

Venezuela

market falls

15

Mexico amp

Brazil steady

growth

MampA activities

Mexico amp Brazil

drive the

category growth

Beer

consumption

fueled by Brazil

Common factors among LatAm

Markets are expected to continue growing

18

Common factors among LatAm

Lager beer is the norm 99 of the market

Skol is the

leading beer

in Brazil and

worldrsquos fourth

best selling

beer brand

Brahma is

consumed in

more than 15

countries In

2011 many

product

innovations

were driven by

this brand

Corona is the

leading beer

in Mexico and

worldrsquos fifth best

selling beer

brand

90 sold in

Mexico and the

US

Antarctica

Pilsen beer is

the 3rd best

selling beer

in Brazil

Itrsquos the largest

best known

beer in

Venezuela

Polar produces

beers and raw

malt

19

Common factors among LatAm

Competing against Soft Drinks

40

24

5 yrs CAGR ()

Beer

CSDs

20

Ambev ndash 30

AB-InBev ndash 50 (Modelo+CND+Regional)

SAB Miller

12

22

2006 2011

54

SAB Miller

11

Common factors among LatAm

Growing Investments and Consolidation

Heineken (+CCU

+Florida)

16

21

2012 Consolidation

Polar Regional

Cerv Centroamericana

Cerv Dominicana

Warsteiner

Schincariol

Paraense

Petropolis

2010

Ajegroup

2010 beer

presentation hellip

22

2012 Consolidation

Polar Cerv Centroamericana

Paraense

Petropolis

2010

Ajegroup

Is there room for

more consolidation

23

2016 LatAm

Incremental Volume 2006 - 2011 - 2016

Beer Oth Alc CSDs

CAGR 06-16

4

CAGR 06-16

2

CAGR 06-16

3

+ 116 Million Hlts

+ 13 Million Hlts

+ 168 Million Hlts

24

2012 Consolidation

Danone Group

Dr Pepper

Snapple Group

Postobon

2010

Ajegroup

Soft drinks companies

Jumex Is there room for

more consolidation

25

USA China Brazil

Spain Germany Italy

Sources of future VOLUME growth

Population +18yrs By 2020 the LatAm young adults

population will reach 207 millions

Annual growth of legal drinking age

population in LatAm +17

26

Sources of future VOLUME growth

Brazil - Regional Consumption 4

67 LPC

rsquo11-rsquo15

CAGR

5

46 LPC

rsquo11-rsquo15

CAGR

23

4

72 LPC

rsquo11-rsquo15

CAGR

54

3

63 LPC

rsquo11-rsquo15

CAGR

12

6

34 LPC

rsquo11-rsquo15

CAGR

4

4

61 LPC

rsquo11-rsquo15

CAGR

7

27

Sources of future VOLUME growth

Brazilrsquos Northeast Region

30 of the population

23 of beer consumption

Regional consumption 46 LPC

Brewery locations

Ambev Heineken Schincariol

+ 6 millions Hl by 2015F

Regional segmentation approach

28

$ 4405 millions

$ 6177 millions

$ 1005 millions

$ 1494 millions

$ 394 millions

$ 1347 million dollars

+10 production

capacity

in 2012

+18 investments in

2011 vs 2010

Sources of future VOLUME growth

Ambev continued to invest in capacity to fulfill

the marketrsquos expected growth

29

Latin America

China North America

West Europe

Superpremium

Premium

Mainstream

Discount

Sources of future VALUE growth

Premium amp Super Premium segments

Substantial interest in the high end

segment

Case Examples

Stella Artois shakes up the Argentinian market

15 USD

244 USD