kyle model governance atoms bonds - oxford-man … · kyle model governance atoms bonds outline 1...

TRANSCRIPT

Kyle Model Governance Atoms Bonds

Outline

1 Continuous time Kyle (1985) model2 Kerry Back, Tao Li, and Alexander Ljungqvist, “Liquidity

and Governance.”3 Kerry Back, Tao Li, and Kevin Crotty, “Detecting the

Presence of an Informed Trader and Other Atoms in KyleModels.”

4 Kerry Back and Kevin Crotty, “The Informational Role ofStock and Bond Volume.”

Kyle Model Governance Atoms Bonds

Continuous Time Kyle Model

Risk-free rate = 0.Single risky asset. Value w is announced at date 1.Single risk-neutral informed trader. Observes unbiasedsignal v at date 0.Xt = # shares held by informed trader at date t .Noise (liquidity) trades a (0, σz) Brownian motion Z .Risk neutral competitive (Bertrand) market makers forceprice to expected value, given information Y def

= X + Z .

Kyle Model Governance Atoms Bonds

Equilibrium Conditions

Competitive pricing:

Pt = E[v | FY

t

].

Look for equilibrium with Pt = p(t ,Yt ).

Informed trader chooses θtdef= dXt/dt to maximize

E

[∫ 1

0[v − p(t ,Yt )]θt dt

∣∣∣∣∣ v

].

Kyle Model Governance Atoms Bonds

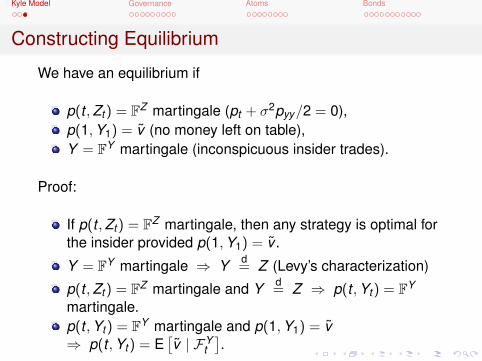

Constructing Equilibrium

We have an equilibrium if

p(t ,Zt ) = FZ martingale (pt + σ2pyy/2 = 0),p(1,Y1) = v (no money left on table),Y = FY martingale (inconspicuous insider trades).

Proof:

If p(t ,Zt ) = FZ martingale, then any strategy is optimal forthe insider provided p(1,Y1) = v .

Y = FY martingale ⇒ Y d= Z (Levy’s characterization)

p(t ,Zt ) = FZ martingale and Y d= Z ⇒ p(t ,Yt ) = FY

martingale.p(t ,Yt ) = FY martingale and p(1,Y1) = v⇒ p(t ,Yt ) = E

[v | FY

t].

Kyle Model Governance Atoms Bonds

Liquidity and Governance

The presence of large shareholders is generally believed tomitigate agency problems.

But will a large shareholder take the trouble to intervene incorporate governance or will she surreptitiously sell her shares(take the Wall Street Walk) instead?

Liquidity can be good for governance (makes it easier toaccumulate a large block) or bad for governance (makes iteasier to exit).

Closest reference: Maug (JF, 1998) solves a single period Kylemodel. Cannot analyze how blockholder responds to market.

Kyle Model Governance Atoms Bonds

Model

Blockholder owns X0 ≥ 0 shares at date 0. Governance eventafter the close of trading at date 1. Blockholder must own B toaffect governance. Costs c to intervene. Intervention changesvalue of firm from L to H.

Intervention is both possible and profitable if

X1 ≥ B,

X1 ≥ ξ def= c/(H − L).

Assume c is normally distributed and private information.Liquidity traders and market makers as before.

Kyle Model Governance Atoms Bonds

Equilibrium Conditions

The investor’s date–1 shares X1 are worth V (X1, ξ) to her,where

V (x , ξ) =

{Lx if x < max(B, ξ) ,

Lx + (H − L)(x − ξ) otherwise .

She trades to maximize

E

[V (X1, ξ)−

∫ 1

0Ptθt dt − P1∆X1

∣∣∣∣∣ ξ],

where ∆X1 is a possible discrete order at the close oftrading.Equilibrium prices must satisfy

p(t ,Yt ) = L + (H − L) prob(

X1 ≥ max(B, ξ) | FYt

).

Kyle Model Governance Atoms Bonds

Equilibrium Informed Trading

Define

δ =σz√

σ2ξ + σ2

z

, A =δ(X0 − µξ)

1 + δ.

The equilibrium trading strategy is

θt =δ(µξ − ξ − Zt )− Yt

(1− t)(1− δ),

∆X1 =

{(B − X1−)+ if Z1 ≤ µξ − ξ + A/δ ,0 otherwise .

In equilibrium, the large trader becomes active iff

Z1 ≤ µξ − ξ + A/δ ⇔ Y1− ≥ A⇔ Y1 ≥ A .

Kyle Model Governance Atoms Bonds

Equilibrium Prices

Equilibrium prices are

p(1, y) = L + (H − L)1{y≥A} ,

p(t , y) = E[p(1,Z1) | Zt = y ] .

Also,X1− = X0 − δ(ξ − µξ)− (1 + δ)Z1 .

Kyle Model Governance Atoms Bonds

Example

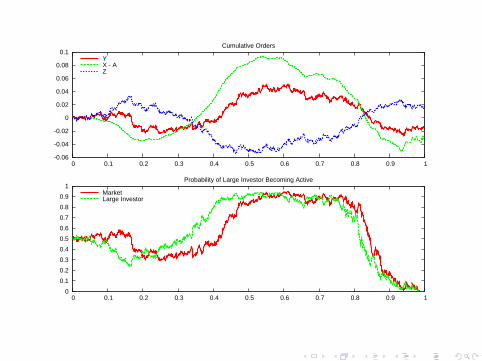

X0 = µξ (so the large trader would become active with 50%probability if there were no trade).This implies A = 0, so the large trader becomes active iffY1− ≥ 0.1 share outstanding, µξ = 0.1, σξ = 0.02, σz = 0.05.Consider ξ = µξ, so the informed trader becomes active iffZ1 ≤ 0.These imply δ = 0.93 and X1− = X0 − 1.93× Z1.

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

0.08

0.1

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

Cumulative Orders

YX - AZ

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

Probability of Large Investor Becoming Active

MarketLarge Investor

Kyle Model Governance Atoms Bonds

Probability of Intervention

The unconditional probability of the blockholder becomingactive is N(A/σz), where N is the standard normal cdf.

It is increasing in σz if

A < 0 ⇔ X0 < µξ

and decreasing in σz otherwise.

Thus, liquidity improves governance when X0 is small andharms governance when X0 is large. Same conclusion asMaug (JF, 1998).

Kyle Model Governance Atoms Bonds

IPO Mechanisms

Suppose X0 is acquired when the firm goes public. DifferentIPO mechanisms (Stoughton-Zechner, JFE, 1998):

1 Take-it-or-leave-it offers.2 Walrasian.3 Discriminatory pricing.4 Discriminatory pricing with a take-it-or-leave-it offer to the

large investor.5 Non-discriminatory pricing with a take-it-or-leave-it offer to

the large investor and rationing of small investors.

No equilibrium in (2). Mechanisms (1), (4) and (5) producehigher revenue than (3) and produce a large X0. We concludethat post-IPO liquidity is harmful for governance.

Kyle Model Governance Atoms Bonds

Kyle Model with Atoms

Examples with discontinuous distribution function for v :

w = true value. Large trader gets unbiased signal s withprobability φ, so

v =

{s with probability φ ,µ with probability 1− φ ,

where µ = E[s].Bankruptcy risk—positive probability that v = 0.Bernoulli distribution: v = L or v = H.

Kyle Model Governance Atoms Bonds

Notation

F = cdf of Z1.H = right-continuous cdf of v .R = right-continuous inverse of v .

R(a) = inf{v | H(v) > a} for 0 ≤ a ≤ 1.Smirnov transform: Take x ∼ uniform on [0,1].Then R(x)

d= v .

V = {R(a) ∈ R | 0 ≤ a ≤ 1}. Then, prob(v ∈ V ) = 1.

Kyle Model Governance Atoms Bonds

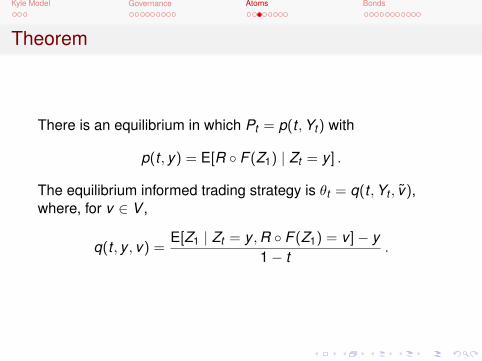

Theorem

There is an equilibrium in which Pt = p(t ,Yt ) with

p(t , y) = E[R ◦ F (Z1) | Zt = y ] .

The equilibrium informed trading strategy is θt = q(t ,Yt , v),where, for v ∈ V ,

q(t , y , v) =E[Z1 | Zt = y ,R ◦ F (Z1) = v ]− y

1− t.

Kyle Model Governance Atoms Bonds

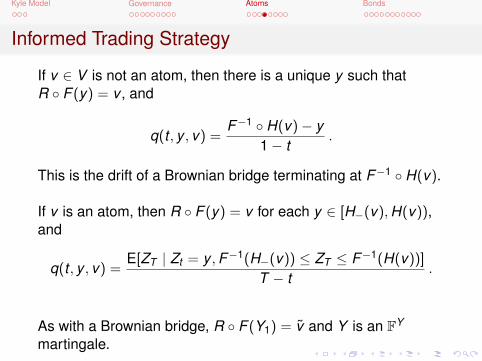

Informed Trading Strategy

If v ∈ V is not an atom, then there is a unique y such thatR ◦ F (y) = v , and

q(t , y , v) =F−1 ◦ H(v)− y

1− t.

This is the drift of a Brownian bridge terminating at F−1 ◦ H(v).

If v is an atom, then R ◦ F (y) = v for each y ∈ [H−(v),H(v)),and

q(t , y , v) =E[ZT | Zt = y ,F−1(H−(v)) ≤ ZT ≤ F−1(H(v))]

T − t.

As with a Brownian bridge, R ◦ F (Y1) = v and Y is an FY

martingale.

Kyle Model Governance Atoms Bonds

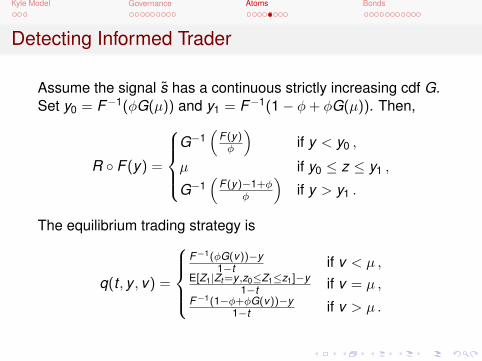

Detecting Informed Trader

Assume the signal s has a continuous strictly increasing cdf G.Set y0 = F−1(φG(µ)) and y1 = F−1(1− φ+ φG(µ)). Then,

R ◦ F (y) =

G−1

(F (y)φ

)if y < y0 ,

µ if y0 ≤ z ≤ y1 ,

G−1(

F (y)−1+φφ

)if y > y1 .

The equilibrium trading strategy is

q(t , y , v) =

F−1(φG(v))−y

1−t if v < µ ,E[Z1|Zt=y ,z0≤Z1≤z1]−y

1−t if v = µ ,F−1(1−φ+φG(v))−y

1−t if v > µ .

Kyle Model Governance Atoms Bonds

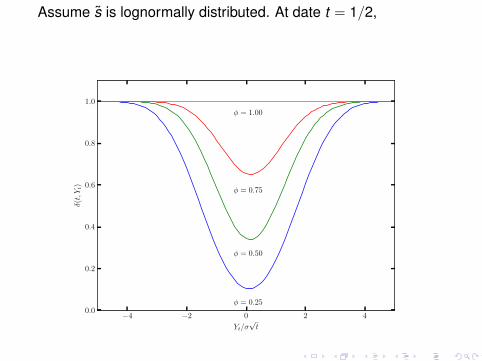

Probability of Information

The conditional probability that the strategic trader is informed,given market makers’ information at any date t < T , is δ(t ,Yt ),where

δ(t , y) = prob(ZT < z0 | Zt = y) + prob(ZT > z1 | Zt = y)

= N(

z0 − yσ√

T − t

)+ 1− N

(z1 − yσ√

T − t

).

Assume s is lognormally distributed. At date t = 1/2,

−4 −2 0 2 4

Yt/σ√t

0.0

0.2

0.4

0.6

0.8

1.0

δ(t,Yt)

φ = 0.25

φ = 0.50

φ = 0.75

φ = 1.00

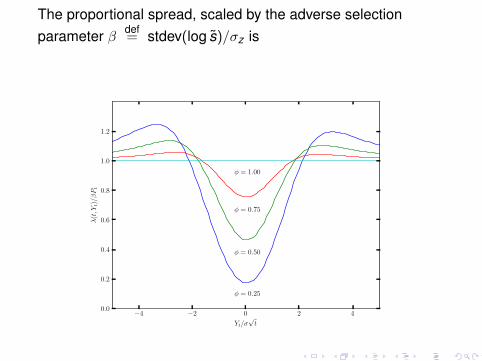

The proportional spread, scaled by the adverse selectionparameter β def

= stdev(log s)/σz is

−4 −2 0 2 4

Yt/σ√t

0.0

0.2

0.4

0.6

0.8

1.0

1.2

λ(t,Y

t)/βPt

φ = 0.25

φ = 0.50

φ = 0.75

φ = 1.00

Kyle Model Governance Atoms Bonds

Debt and Equity with Taxes and Bankruptcy

Zero-coupon bond with face value D maturing at date 1.Firm’s gross value v at date 1 shared among bondholders,shareholders, taxes, and the deadweight costs ofbankruptcy.Total payout to bondholders and shareholders is

x def=

(1− α)v if v < D ,

v if D ≤ v < D + E ,

τ(D + E) + (1− τ)v if v ≥ D + E .

Bondholders get min(x ,D), and shareholders get (x −D)+.

Kyle Model Governance Atoms Bonds

Trading Model

No private information when the time the bond is issued.Single risk-neutral trader observes v immediately after theissue.Vector of stock and bond liquidity trades a (0,Σ) Brownianmotion.

Kyle Model Governance Atoms Bonds

Default and Solvency Regions

Equilibrium is defined in terms of a strictly increasingfunction G of date–1 bond and stock orders (yb, ys).Define

D = {y | G(y) < 0} ,S = {y | G(y) ≥ 0} .

In equilibrium, YT ∈ D if and only if x < D.D is the default region, and S is the solvency region.

Kyle Model Governance Atoms Bonds

Equilibrium Prices

Define functions πb and πs by

prob(ZT ∈ D and Z bT ≤ a) = prob(x ≤ πb(a)) ,

prob(ZT ∈ S and Z sT ≤ a) = prob(D < x ≤ D + πs(a)) ,

Set

pb(1, y) =

{πb(yb) if y ∈ D ,D if y ∈ S ,

ps(1, y) =

{0 if y ∈ D ,πs(ys) if y ∈ S ,

Set p = (pb,ps) and, for t < 1,

p(t , y) = E[p(1,Z1) | Zt = y ] .

Kyle Model Governance Atoms Bonds

Equilibrium Informed Trades

For each x < D, set A(x) = {y ∈ D | πb(yb) = x}.For x > D, set A(x) = {y ∈ S | πs(ys) = x − D}.The equilibrium informed trading strategy is

q(t , y , x) =1

1− t

(E[Z1 | Zt = y ,Z1 ∈ A(x)

]− y

).

Kyle Model Governance Atoms Bonds

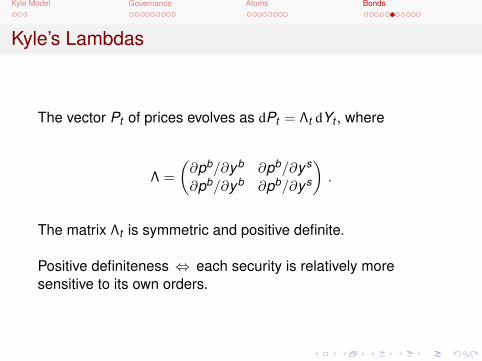

Kyle’s Lambdas

The vector Pt of prices evolves as dPt = Λt dYt , where

Λ =

(∂pb/∂yb ∂pb/∂ys

∂pb/∂yb ∂pb/∂ys

).

The matrix Λt is symmetric and positive definite.

Positive definiteness ⇔ each security is relatively moresensitive to its own orders.

Kyle Model Governance Atoms Bonds

Boundary between D and S

Impose the following condition on G:

G(yb, ys) = 0 ⇒ ∂G(yb, ys)/∂ys

∂G(yb, ys)/∂yb =πs(ys)

D − πb(yb).

In a single-security Kyle model, the informed trader neithermakes nor loses money by trading in one direction andthen immediately reversing the trades.With multiple securities, there are many possible paths onecan take to move from one inventory pair (yb, ys) toanother (wb,ws).Trading from one to the other and then back along anypaths generates neither gains nor losses when thecondition on G holds.

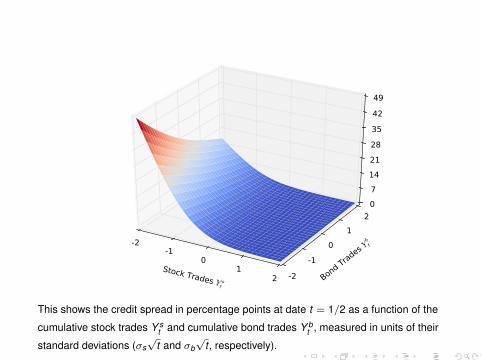

Stock Trades Y st

-2-1

01

2 Bond Trades Ybt

-2

-10

12

071421283542

49

This shows the credit spread in percentage points at date t = 1/2 as a function of the

cumulative stock trades Y st and cumulative bond trades Y b

t , measured in units of their

standard deviations (σs√

t and σb√

t , respectively).

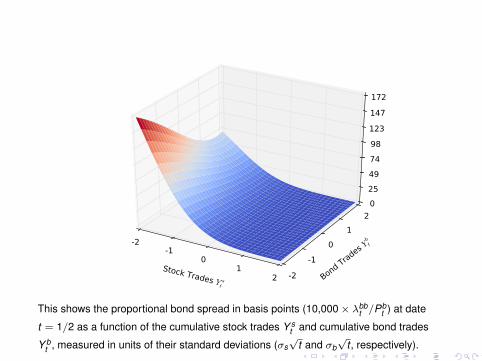

Stock Trades Y st

-2-1

01

2 Bond Trades Ybt

-2

-10

12

025497498123147172

This shows the proportional bond spread in basis points (10,000× λbbt /Pb

t ) at date

t = 1/2 as a function of the cumulative stock trades Y st and cumulative bond trades

Y bt , measured in units of their standard deviations (σs

√t and σb

√t , respectively).

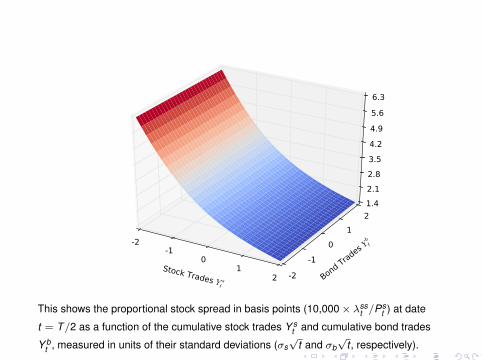

Stock Trades Y st

-2-1

01

2 Bond Trades Ybt

-2

-10

121.42.12.83.54.24.95.6

6.3

This shows the proportional stock spread in basis points (10,000× λsst /Ps

t ) at date

t = T/2 as a function of the cumulative stock trades Y st and cumulative bond trades

Y bt , measured in units of their standard deviations (σs

√t and σb

√t , respectively).

Kyle Model Governance Atoms Bonds

Empirics

3 years of daily stock and bond transactions data for 334 firms.

Elements of Λ are positive, and Λ is positive definite.

Λss/Ps (proportional stock spread) declines with stockpurchases and with bond purchases.