klöckner & co se press conference presentation q1 2016 results

TRANSCRIPT

Q1 2016 Results

Press Conference

May 4, 2016

Gisbert Rühl | CEO

No.2 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

Disclaimer

This presentation contains forward-looking statements which reflect the current views of the management of

Klöckner & Co SE with respect to future events. They generally are designated by the words “expect”, “assume”, “presume”, “intend”,

“estimate”, “strive for”, “aim for”, “plan”, “will”, “endeavor”, “outlook” and comparable expressions and generally contain information that relates

to expectations or goals for economic conditions, sales proceeds or other yardsticks for the success of the enterprise. Forward-looking

statements are based on currently valid plans, estimates and expectations. You therefore should view them with caution. Such statements are

subject to risks and factors of uncertainty, most of which are difficult to assess and which generally are outside of the control of Klöckner & Co

SE. The relevant factors include the effects of significant strategic and operational initiatives, including the acquisition or disposition of

companies. If these or other risks and factors of uncertainty occur or if the assumptions on which the statements are based turn out to be

incorrect, the actual results of Klöckner & Co SE can deviate significantly from those that are expressed or implied in these statements.

Klöckner & Co SE cannot give any guarantee that the expectations or goals will be attained. Klöckner & Co SE – notwithstanding existing

obligations under laws pertaining to capital markets – rejects any responsibility for updating the forward-looking statements through taking into

consideration new information or future events or other things.

In addition to the key data prepared in accordance with International Financial Reporting Standards, Klöckner & Co SE is presenting non-

GAAP key data such as EBITDA, EBIT, Net Working Capital and net financial liabilities that are not a component of the accounting

regulations. These key data are to be viewed as supplementary to, but not as a substitute for data prepared in accordance with International

Financial Reporting Standards. Non-GAAP key data are not subject to IFRS or any other generally applicable accounting regulations. Other

companies may base these concepts upon other definitions.

No.3

1. Highlights and update on strategy

2. Financials

3. Outlook

4. Appendix

Agenda

Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

No.4 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

Highlights01

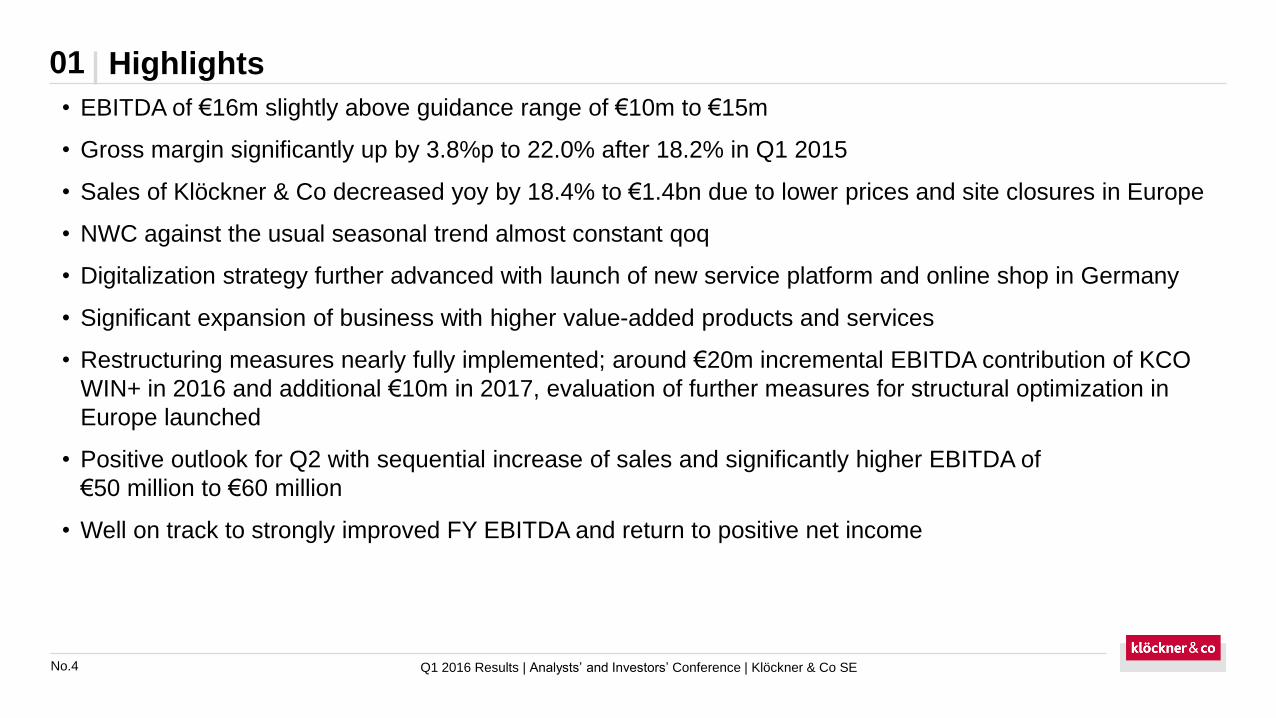

• EBITDA of €16m slightly above guidance range of €10m to €15m

• Gross margin significantly up by 3.8%p to 22.0% after 18.2% in Q1 2015

• Sales of Klöckner & Co decreased yoy by 18.4% to €1.4bn due to lower prices and site closures in Europe

• NWC against the usual seasonal trend almost constant qoq

• Digitalization strategy further advanced with launch of new service platform and online shop in Germany

• Significant expansion of business with higher value-added products and services

• Restructuring measures nearly fully implemented; around €20m incremental EBITDA contribution of KCO

WIN+ in 2016 and additional €10m in 2017, evaluation of further measures for structural optimization in

Europe launched

• Positive outlook for Q2 with sequential increase of sales and significantly higher EBITDA of

€50 million to €60 million

• Well on track to strongly improved FY EBITDA and return to positive net income

No.5 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

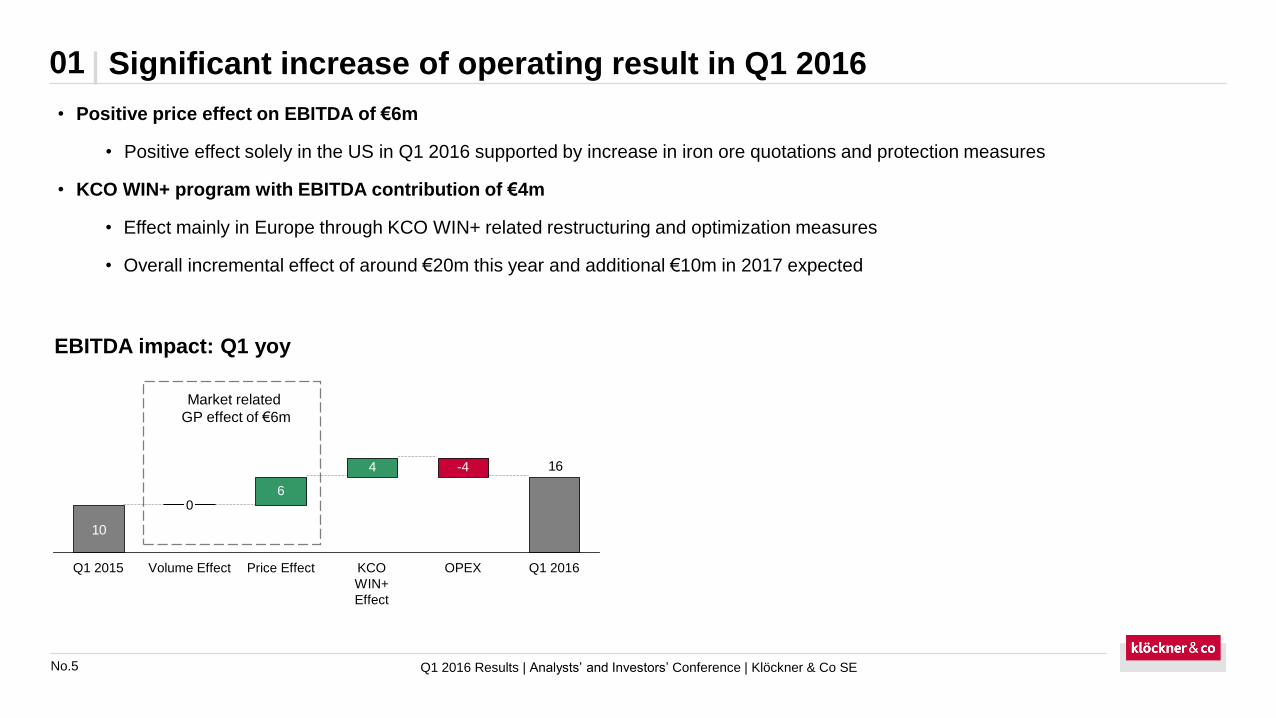

Significant increase of operating result in Q1 201601

EBITDA impact: Q1 yoy

Market related

GP effect of €6m

• Positive price effect on EBITDA of €6m

• Positive effect solely in the US in Q1 2016 supported by increase in iron ore quotations and protection measures

• KCO WIN+ program with EBITDA contribution of €4m

• Effect mainly in Europe through KCO WIN+ related restructuring and optimization measures

• Overall incremental effect of around €20m this year and additional €10m in 2017 expected

4

10

16

6

Price EffectVolume EffectQ1 2015

0

KCO

WIN+

Effect

-4

OPEX Q1 2016

No.6 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

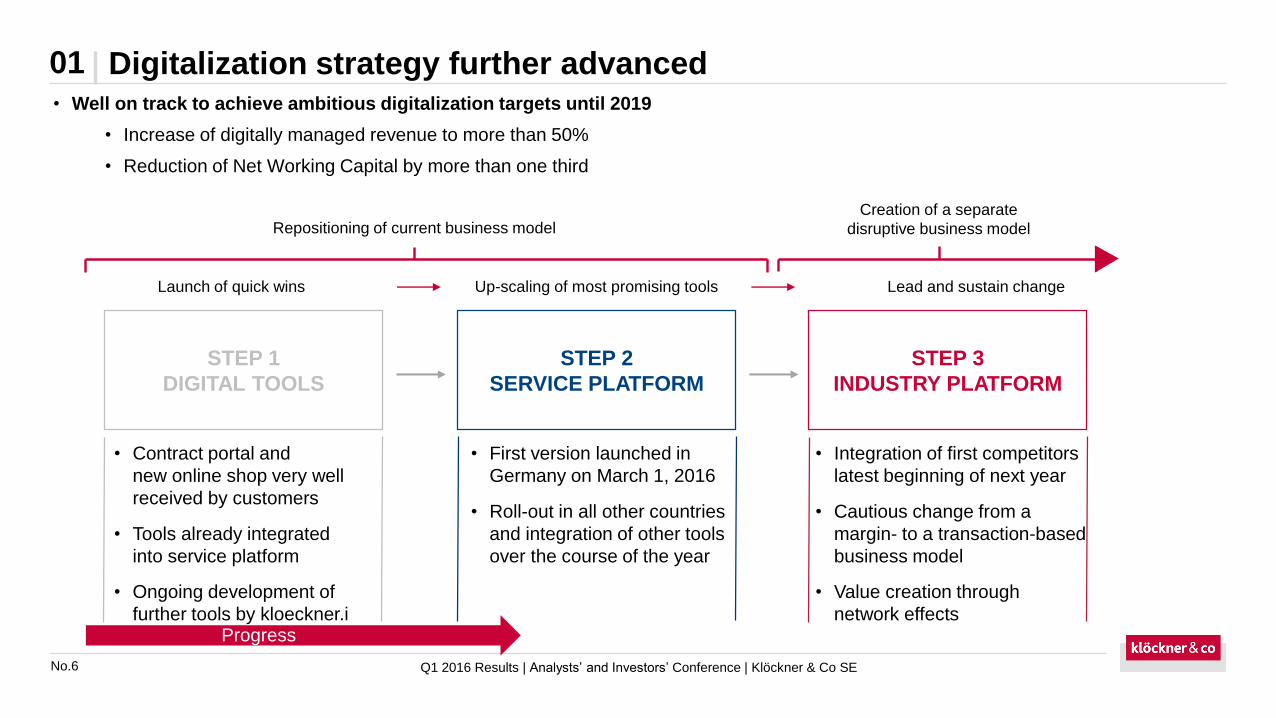

Digitalization strategy further advanced01• Well on track to achieve ambitious digitalization targets until 2019

• Increase of digitally managed revenue to more than 50%

• Reduction of Net Working Capital by more than one third

• Contract portal and

new online shop very well

received by customers

• Tools already integrated

into service platform

• Ongoing development of

further tools by kloeckner.i

• First version launched in

Germany on March 1, 2016

• Roll-out in all other countries

and integration of other tools

over the course of the year

• Integration of first competitors

latest beginning of next year

• Cautious change from a

margin- to a transaction-based

business model

• Value creation through

network effects

Repositioning of current business modelCreation of a separate

disruptive business model

Launch of quick wins Up-scaling of most promising tools Lead and sustain change

STEP 1

DIGITAL TOOLS

STEP 2

SERVICE PLATFORM

STEP 3

INDUSTRY PLATFORM

Progress

No.7

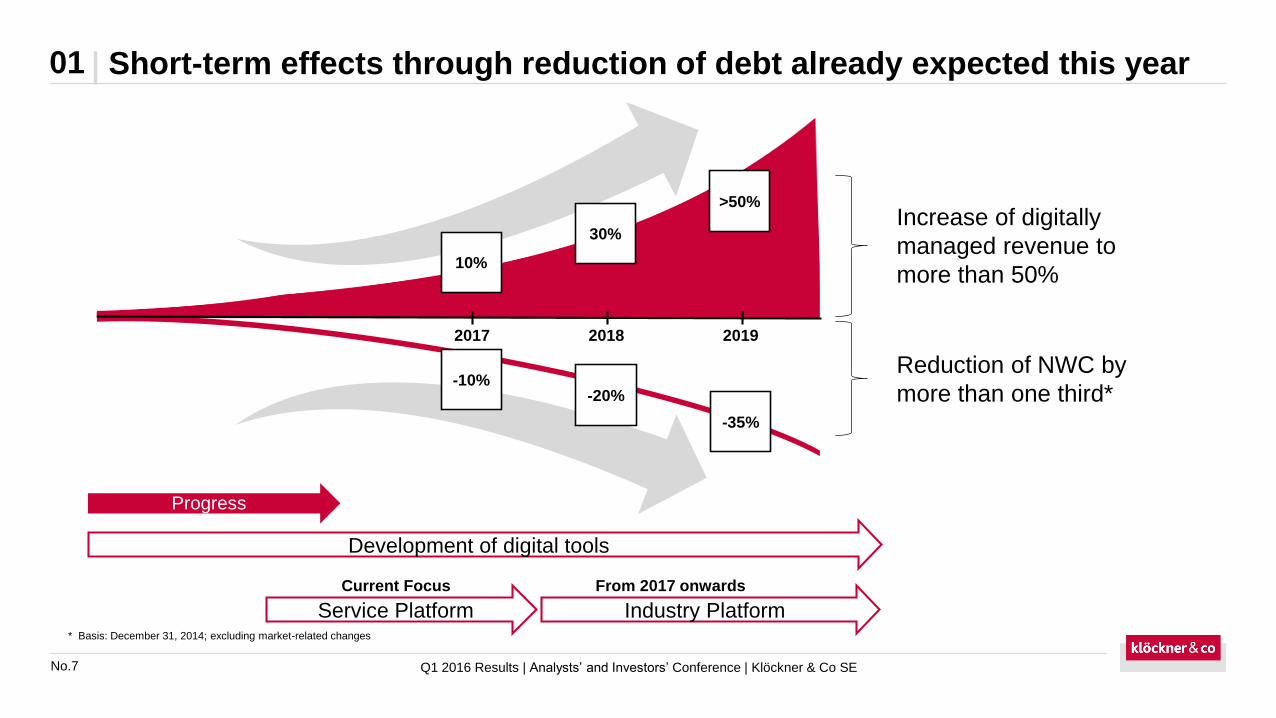

Short-term effects through reduction of debt already expected this year01

Reduction of NWC by

more than one third*

Increase of digitally

managed revenue to

more than 50%

Development of digital tools

Service Platform Industry Platform

Progress

Current Focus From 2017 onwards

* Basis: December 31, 2014; excluding market-related changes

-10%-20%

10%

30%

>50%

-35%

201920182017

Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

No.8

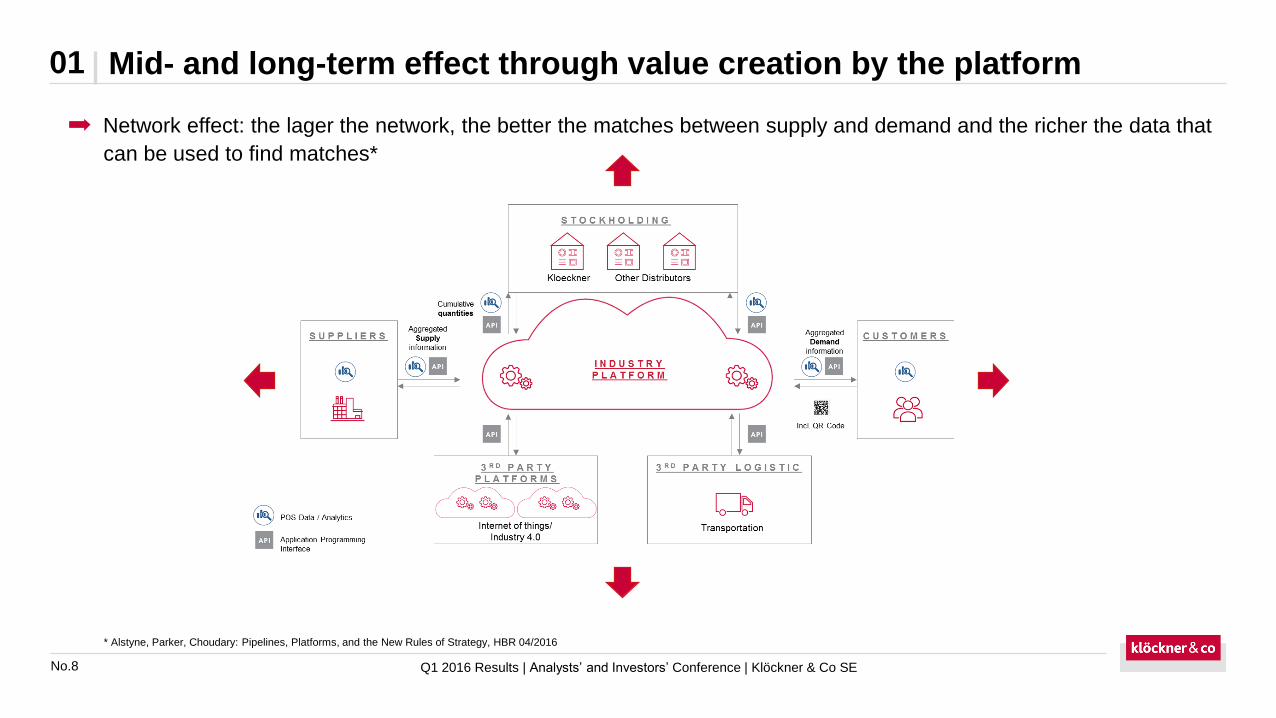

01

Network effect: the lager the network, the better the matches between supply and demand and the richer the data that

can be used to find matches*

* Alstyne, Parker, Choudary: Pipelines, Platforms, and the New Rules of Strategy, HBR 04/2016

Mid- and long-term effect through value creation by the platform

Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

No.9

20%

25%35%

20%

T A R G E T 2 0 1 7

Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

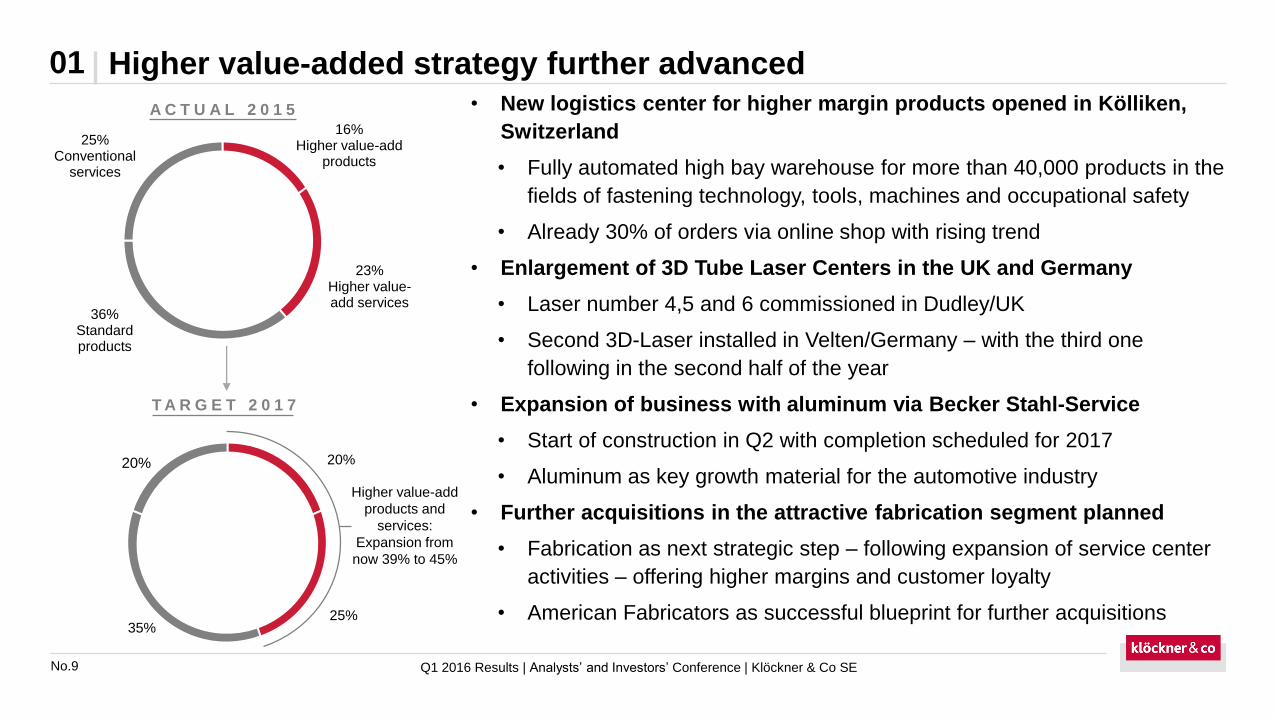

Higher value-added strategy further advanced01• New logistics center for higher margin products opened in Kölliken,

Switzerland

• Fully automated high bay warehouse for more than 40,000 products in the

fields of fastening technology, tools, machines and occupational safety

• Already 30% of orders via online shop with rising trend

• Enlargement of 3D Tube Laser Centers in the UK and Germany

• Laser number 4,5 and 6 commissioned in Dudley/UK

• Second 3D-Laser installed in Velten/Germany – with the third one

following in the second half of the year

• Expansion of business with aluminum via Becker Stahl-Service

• Start of construction in Q2 with completion scheduled for 2017

• Aluminum as key growth material for the automotive industry

• Further acquisitions in the attractive fabrication segment planned

• Fabrication as next strategic step – following expansion of service center

activities – offering higher margins and customer loyalty

• American Fabricators as successful blueprint for further acquisitions

16% Higher value-add

products

23%Higher value-add services

36% Standard products

25% Conventional

services

A C T U A L 2 0 1 5

Higher value-add

products and

services:

Expansion from

now 39% to 45%

No.10 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

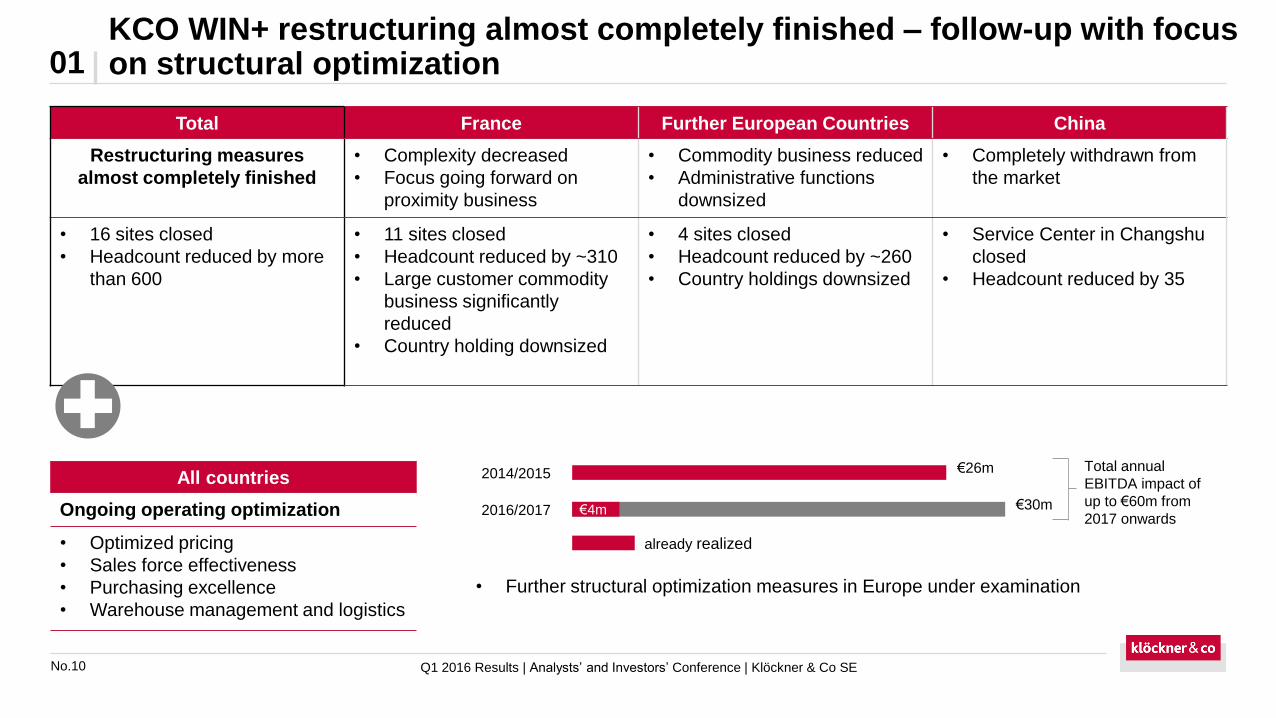

KCO WIN+ restructuring almost completely finished – follow-up with focus on structural optimization01

Total France Further European Countries China

Restructuring measures

almost completely finished

• Complexity decreased

• Focus going forward on

proximity business

• Commodity business reduced

• Administrative functions

downsized

• Completely withdrawn from

the market

• 16 sites closed

• Headcount reduced by more

than 600

• 11 sites closed

• Headcount reduced by ~310

• Large customer commodity

business significantly

reduced

• Country holding downsized

• 4 sites closed

• Headcount reduced by ~260

• Country holdings downsized

• Service Center in Changshu

closed

• Headcount reduced by 35

All countries

Ongoing operating optimization

• Optimized pricing

• Sales force effectiveness

• Purchasing excellence

• Warehouse management and logistics

2014/2015

2016/2017

already realized

€26m

€30m

Total annual

EBITDA impact of

up to €60m from

2017 onwards€4m

• Further structural optimization measures in Europe under examination

No.11

1. Highlights and update on strategy

2. Financials

3. Outlook

4. Appendix

Agenda

Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

No.12 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

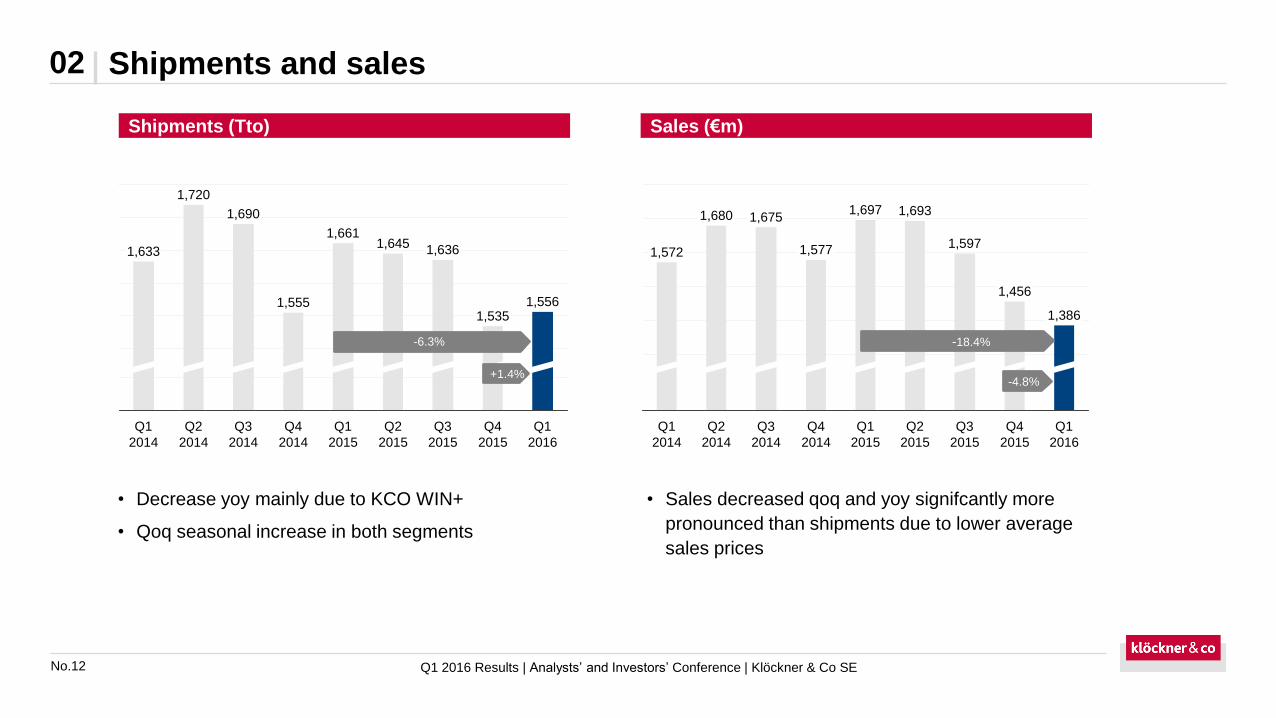

Shipments and sales02

• Decrease yoy mainly due to KCO WIN+

• Qoq seasonal increase in both segments

• Sales decreased qoq and yoy signifcantly more

pronounced than shipments due to lower average

sales prices

Q4

2015

1,535

Q3

2015

1,636

Q2

2015

Q1

2015

1,661

Q4

2014

1,556

Q1

2016

1,633

Q1

2014

1,720

Q2

2014

1,645

1,690

Q3

2014

1,555

Q2

2015

1,693

Q1

2015

1,697

Q4

2014

1,577

Q3

2014

Q1

2016

Q2

2014

1,680

Q1

2014

1,572

Q4

2015

1,456

1,386

Q3

2015

1,597

1,675

-6.3%

+1.4%

-18.4%

-4.8%

Shipments (Tto) Sales (€m)

No.13 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

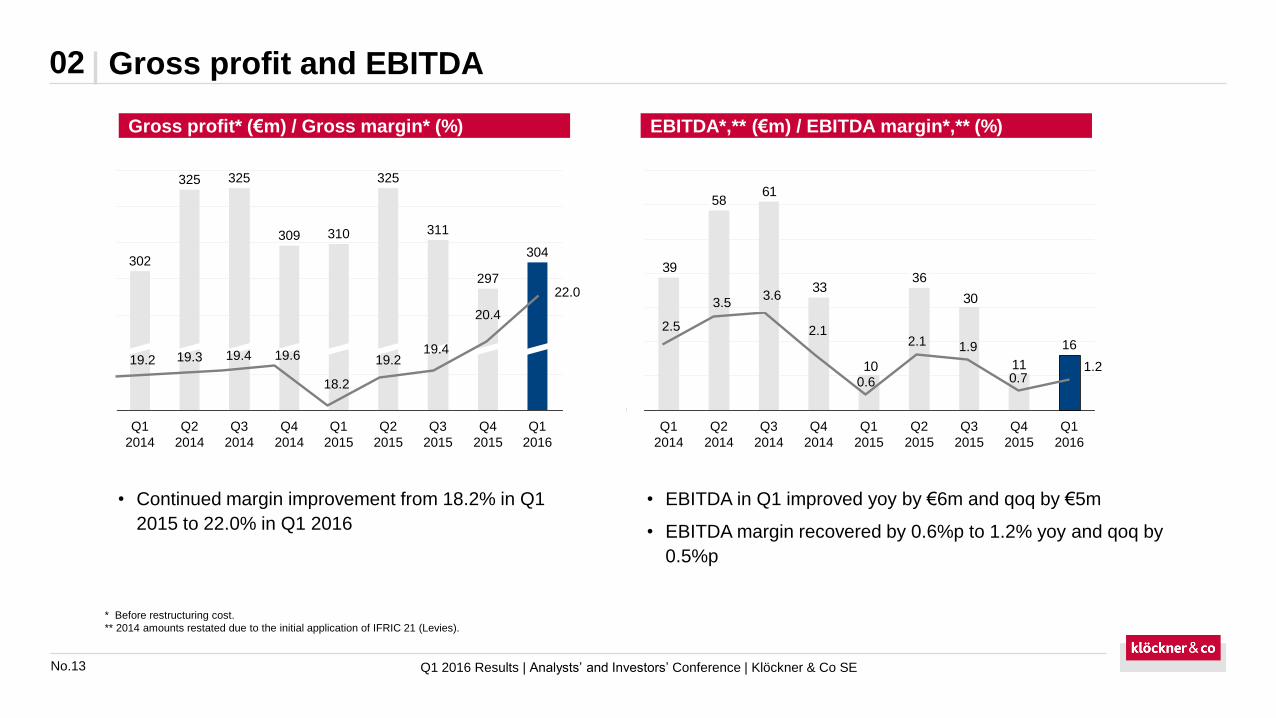

Gross profit and EBITDA02

* Before restructuring cost.

** 2014 amounts restated due to the initial application of IFRIC 21 (Levies).

11

30

10

33

61

39

Q1

2016

16

Q4

2015

Q3

2015

Q2

2015

36

Q1

2015

Q4

2014

Q3

2014

Q2

2014

58

Q1

2014

1.20.7

1.92.1

0.6

2.1

3.63.5

2.5

Q1

2014

302

310309

Q1

2016

Q2

2015

297

Q4

2015

311

Q3

2015

304

325325

Q1

2015

325

Q2

2014

Q3

2014

Q4

2014

19.4

22.0

20.4

19.219.2 19.419.3

18.2

19.6

• Continued margin improvement from 18.2% in Q1

2015 to 22.0% in Q1 2016

• EBITDA in Q1 improved yoy by €6m and qoq by €5m

• EBITDA margin recovered by 0.6%p to 1.2% yoy and qoq by

0.5%p

Gross profit* (€m) / Gross margin* (%) EBITDA*,** (€m) / EBITDA margin*,** (%)

No.14 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

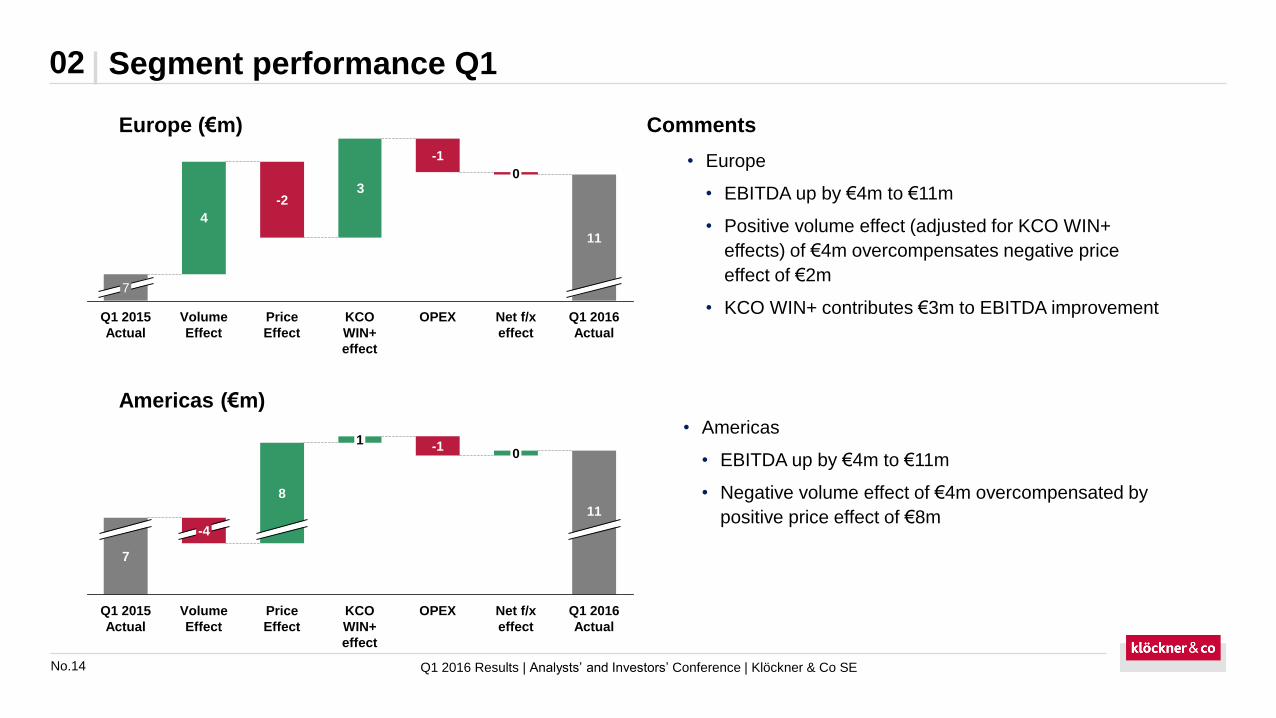

Segment performance Q102

• Europe

• EBITDA up by €4m to €11m

• Positive volume effect (adjusted for KCO WIN+

effects) of €4m overcompensates negative price

effect of €2m

• KCO WIN+ contributes €3m to EBITDA improvement

CommentsEurope (€m)

Americas (€m)

0

OPEX

-1

KCO

WIN+

effect

1

Price

Effect

Q1 2016

Actual

11

Net f/x

effect

8

Volume

Effect

-4

Q1 2015

Actual

7

3

4

KCO

WIN+

effect

Price

Effect

-2

Volume

Effect

Q1 2015

Actual

7

Q1 2016

Actual

11

Net f/x

effect

0

OPEX

-1

• Americas

• EBITDA up by €4m to €11m

• Negative volume effect of €4m overcompensated by

positive price effect of €8m

No.15 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

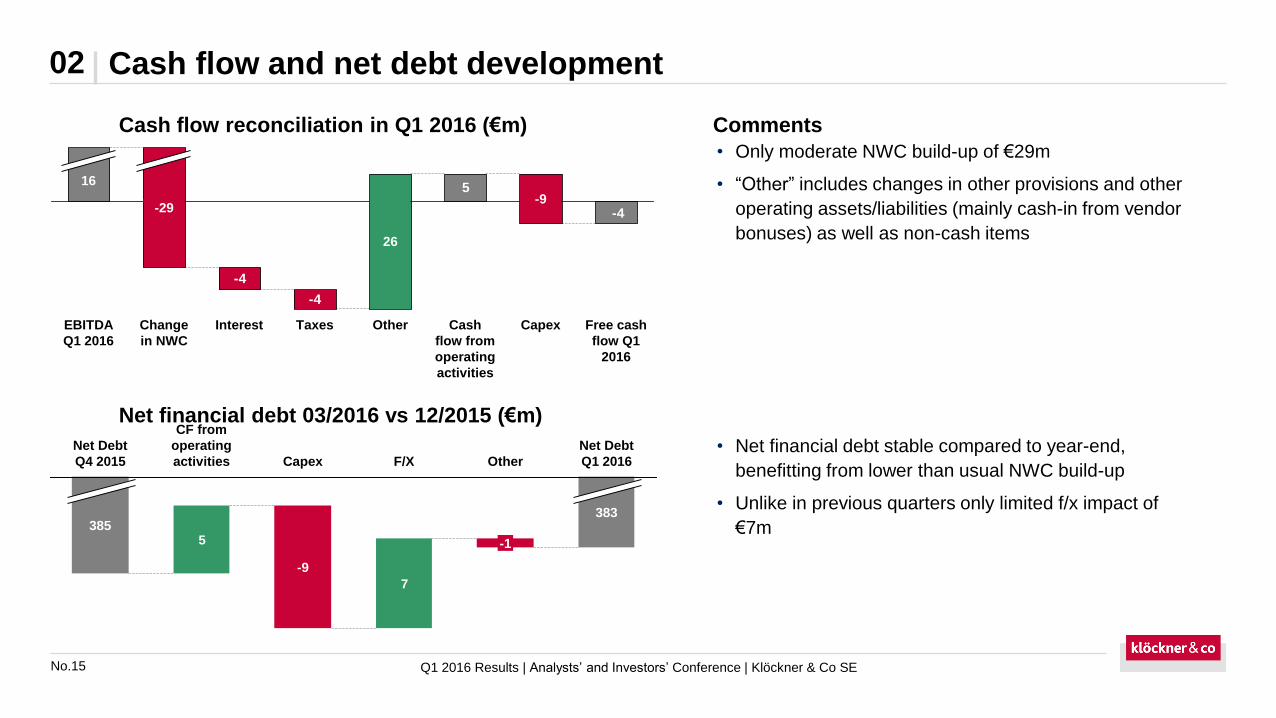

Cash flow and net debt development02

36

• Only moderate NWC build-up of €29m

• “Other” includes changes in other provisions and other

operating assets/liabilities (mainly cash-in from vendor

bonuses) as well as non-cash items

-4

-4

5

-4

Free cash

flow Q1

2016

Capex

-9

Cash

flow from

operating

activities

Other

26

TaxesInterestChange

in NWC

-29

EBITDA

Q1 2016

16

CommentsCash flow reconciliation in Q1 2016 (€m)

• Net financial debt stable compared to year-end,

benefitting from lower than usual NWC build-up

• Unlike in previous quarters only limited f/x impact of

€7m

Net financial debt 03/2016 vs 12/2015 (€m)

7

5

Net Debt

Q1 2016

383

Other

-1

F/XCapex

-9

CF from

operating

activities

Net Debt

Q4 2015

385

No.16 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

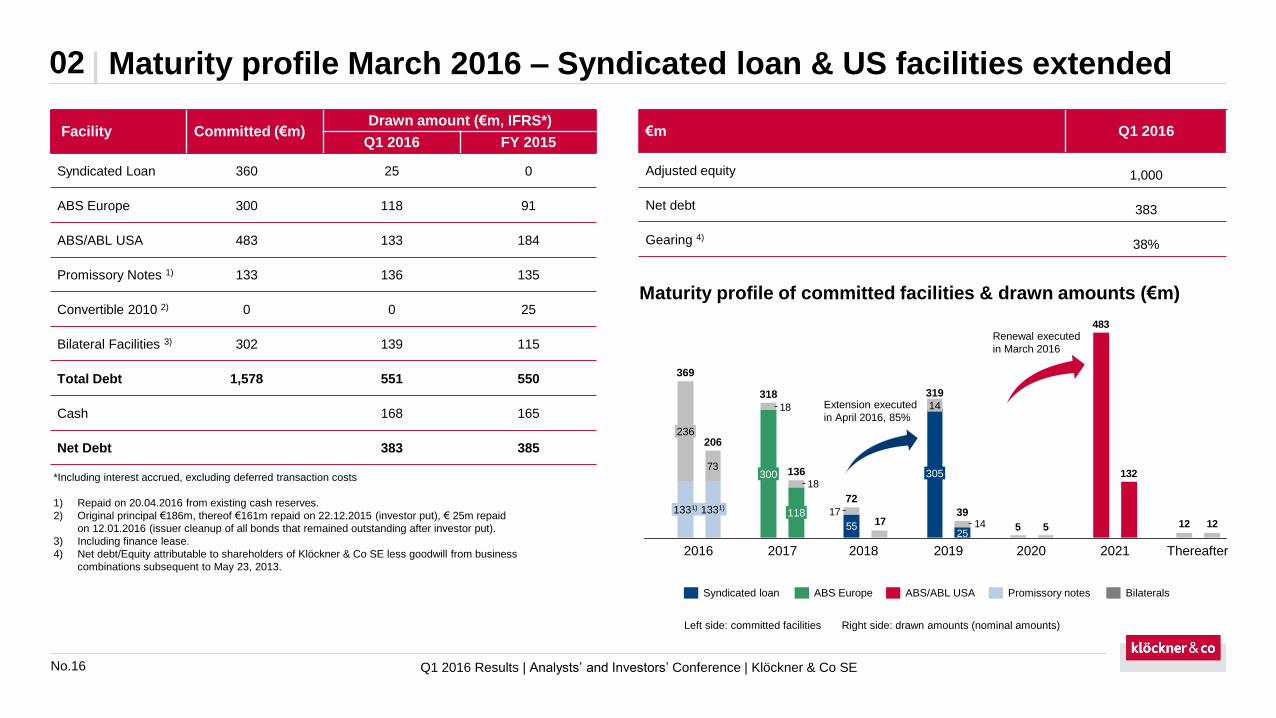

Maturity profile March 2016 – Syndicated loan & US facilities extended 02

Facility Committed (€m)Drawn amount (€m, IFRS*)

Q1 2016 FY 2015

Syndicated Loan 360 25 0

ABS Europe 300 118 91

ABS/ABL USA 483 133 184

Promissory Notes 1) 133 136 135

Convertible 2010 2) 0 0 25

Bilateral Facilities 3) 302 139 115

Total Debt 1,578 551 550

Cash 168 165

Net Debt 383 385

€m Q1 2016

Adjusted equity 1,000

Net debt 383

Gearing 4)38%

Maturity profile of committed facilities & drawn amounts (€m)

Left side: committed facilities Right side: drawn amounts (nominal amounts)

ABS/ABL USA BilateralsSyndicated loan ABS Europe Promissory notes

*Including interest accrued, excluding deferred transaction costs

1) Repaid on 20.04.2016 from existing cash reserves.

2) Original principal €186m, thereof €161m repaid on 22.12.2015 (investor put), € 25m repaid

on 12.01.2016 (issuer cleanup of all bonds that remained outstanding after investor put).

3) Including finance lease.

4) Net debt/Equity attributable to shareholders of Klöckner & Co SE less goodwill from business

combinations subsequent to May 23, 2013.

2555

132

483

121255141717

18

18

73

206

1331)

369

1331)

236

136

118

318

300

39

319

305

14

72

Extension executed

in April 2016, 85%

Renewal executed

in March 2016

2016 2017 2018 2019 2020 2021 Thereafter

No.17

1. Highlights and update on strategy

2. Financials

3. Outlook

4. Appendix

Agenda

Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

No.18 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

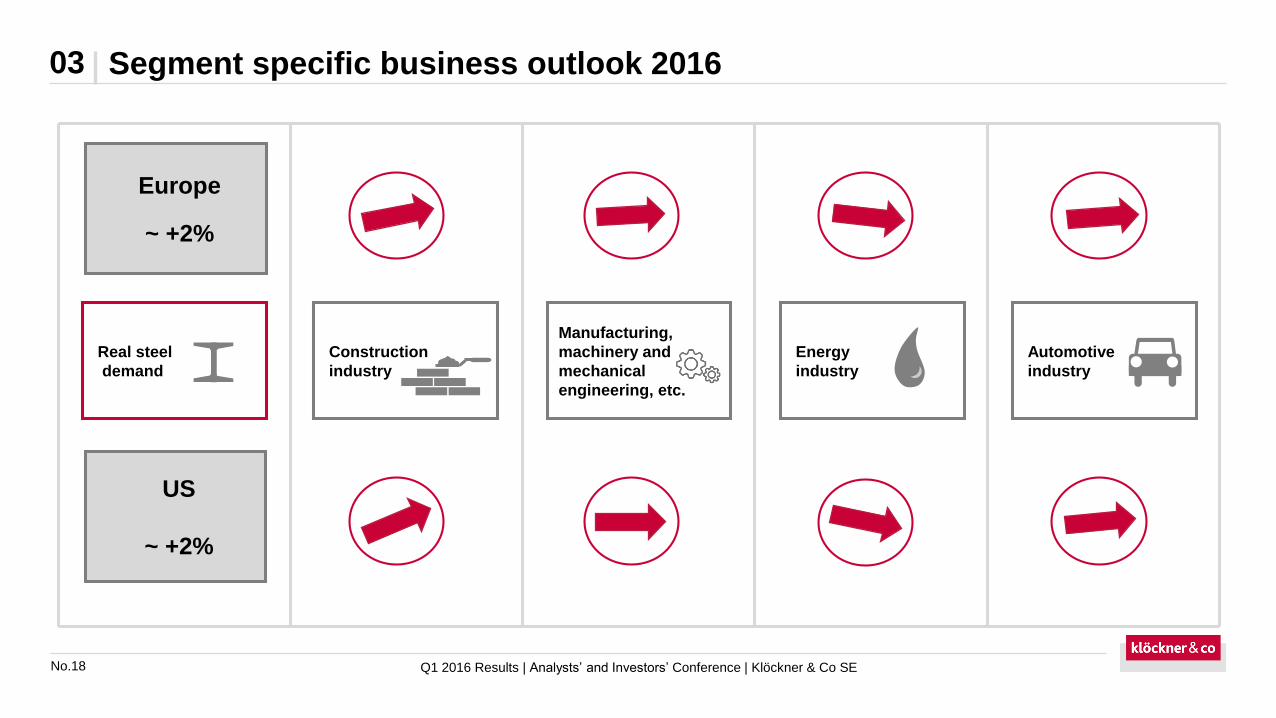

Segment specific business outlook 201603

Energy

industry

Real steel

demand

Europe

~ +2%

Construction

industry

Manufacturing,

machinery and

mechanical

engineering, etc.

Automotive

industry

US

~ +2%

No.19 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

Outlook 03

• Q2 2016

• Sales expected to be sequentially up

• Significantly higher operating EBITDA anticipated in a range between €50m and €60m

• FY 2016

• Lower sales anticipated despite market growth due to continued exit of low margin business and lower price level

• EBITDA expected to rise significantly compared to previous year`s figure adjusted for restructuring expenses of €86m

• Positive net income supported by lower financing expenses and the expected absence of further goodwill impairments

No.20

1. Highlights and update on strategy

2. Financials

3. Outlook

4. Appendix

Agenda

Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

No.21 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

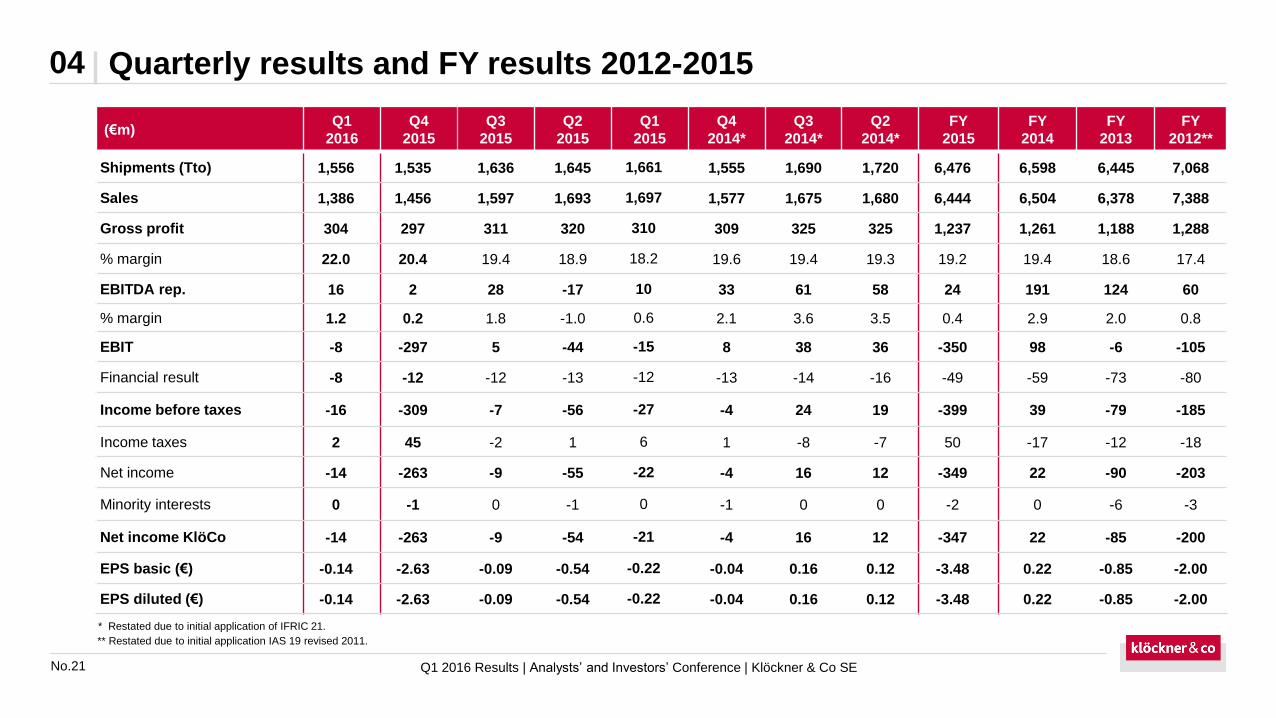

Quarterly results and FY results 2012-201504

(€m)Q1

2016

Q4

2015

Q3

2015

Q2

2015

Q1

2015

Q4

2014*

Q3

2014*

Q2

2014*

FY

2015

FY

2014

FY

2013

FY

2012**

Shipments (Tto) 1,556 1,535 1,636 1,645 1,661 1,555 1,690 1,720 6,476 6,598 6,445 7,068

Sales 1,386 1,456 1,597 1,693 1,697 1,577 1,675 1,680 6,444 6,504 6,378 7,388

Gross profit 304 297 311 320 310 309 325 325 1,237 1,261 1,188 1,288

% margin 22.0 20.4 19.4 18.9 18.2 19.6 19.4 19.3 19.2 19.4 18.6 17.4

EBITDA rep. 16 2 28 -17 10 33 61 58 24 191 124 60

% margin 1.2 0.2 1.8 -1.0 0.6 2.1 3.6 3.5 0.4 2.9 2.0 0.8

EBIT -8 -297 5 -44 -15 8 38 36 -350 98 -6 -105

Financial result -8 -12 -12 -13 -12 -13 -14 -16 -49 -59 -73 -80

Income before taxes -16 -309 -7 -56 -27 -4 24 19 -399 39 -79 -185

Income taxes 2 45 -2 1 6 1 -8 -7 50 -17 -12 -18

Net income -14 -263 -9 -55 -22 -4 16 12 -349 22 -90 -203

Minority interests 0 -1 0 -1 0 -1 0 0 -2 0 -6 -3

Net income KlöCo -14 -263 -9 -54 -21 -4 16 12 -347 22 -85 -200

EPS basic (€) -0.14 -2.63 -0.09 -0.54 -0.22 -0.04 0.16 0.12 -3.48 0.22 -0.85 -2.00

EPS diluted (€) -0.14 -2.63 -0.09 -0.54 -0.22 -0.04 0.16 0.12 -3.48 0.22 -0.85 -2.00

* Restated due to initial application of IFRIC 21.

** Restated due to initial application IAS 19 revised 2011.

No.22 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

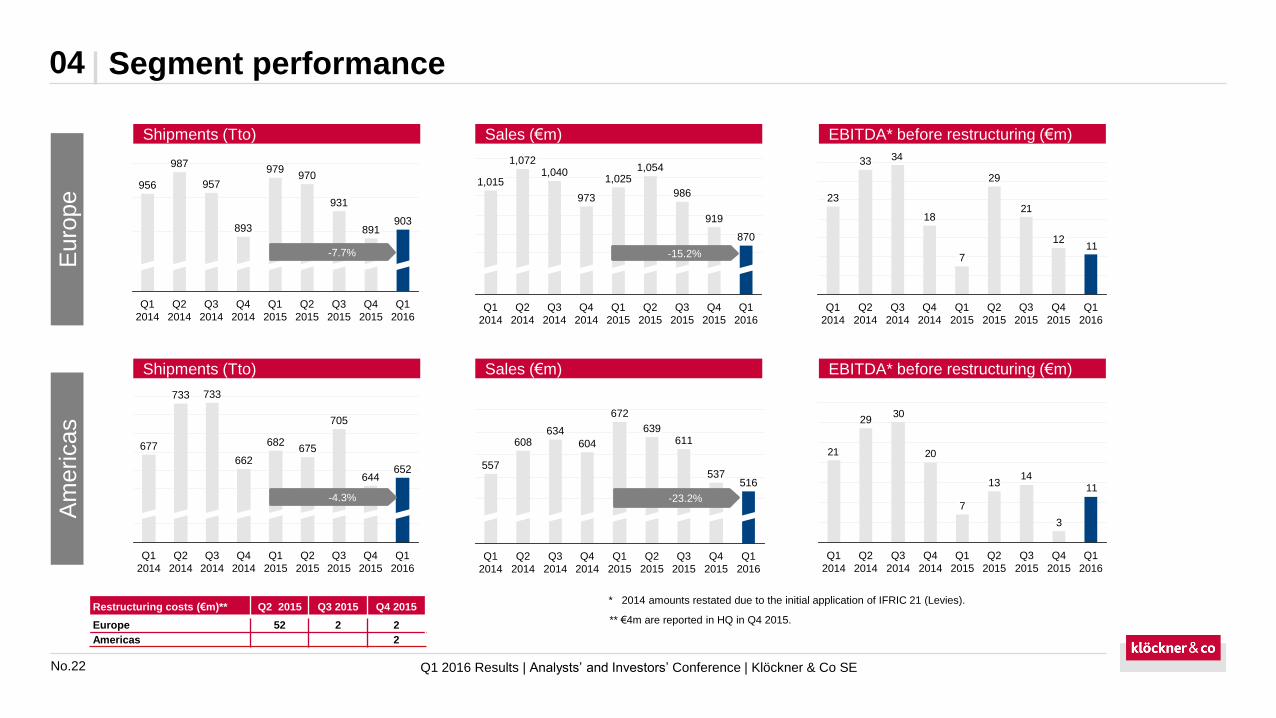

Segment performance04

* 2014 amounts restated due to the initial application of IFRIC 21 (Levies).

Q1

2016

903

Q4

2015

891

Q3

2015

931

Q2

2015

970

Q1

2015

979

Q4

2014

893

Q3

2014

957

Q2

2014

987

Q1

2014

956

919

Q3

2015

Q2

2015

1,054

Q1

2015

1,025

Q4

2014

973 986

Q1

2016

870

Q4

2015

Q3

2014

1,040

Q2

2014

1,072

Q1

2014

1,015

11

21

34

Q2

2015

29

Q1

2015

7

Q4

2014

18

Q3

2014

Q2

2014

33

Q1

2014

23

Q1

2016

Q4

2015

12

Q3

2015

Q4

2015

644

Q3

2015

705

Q2

2015

675

Q1

2015

682

Q4

2014

662

Q3

2014

733

Q2

2014

733

Q1

2014

677

Q1

2016

652

Q1

2014

557

Q3

2014

672

Q2

2015

537

608634

Q1

2015

611

Q2

2014

604

Q4

2014

639

Q3

2015

516

Q4

2015

Q1

2016

1114

20

30

21

Q3

2014

Q2

2014

29

Q1

2014

3

Q1

2016

Q4

2015

13

Q3

2015

7

Q2

2015

Q1

2015

Q4

2014

-7.7%

-4.3%

-15.2%

-23.2%

Euro

pe

Am

ericas

Restructuring costs (€m)** Q2 2015 Q3 2015 Q4 2015

Europe 52 2 2

Americas 2

Shipments (Tto) Sales (€m) EBITDA* before restructuring (€m)

Shipments (Tto) Sales (€m) EBITDA* before restructuring (€m)

** €4m are reported in HQ in Q4 2015.

No.23 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

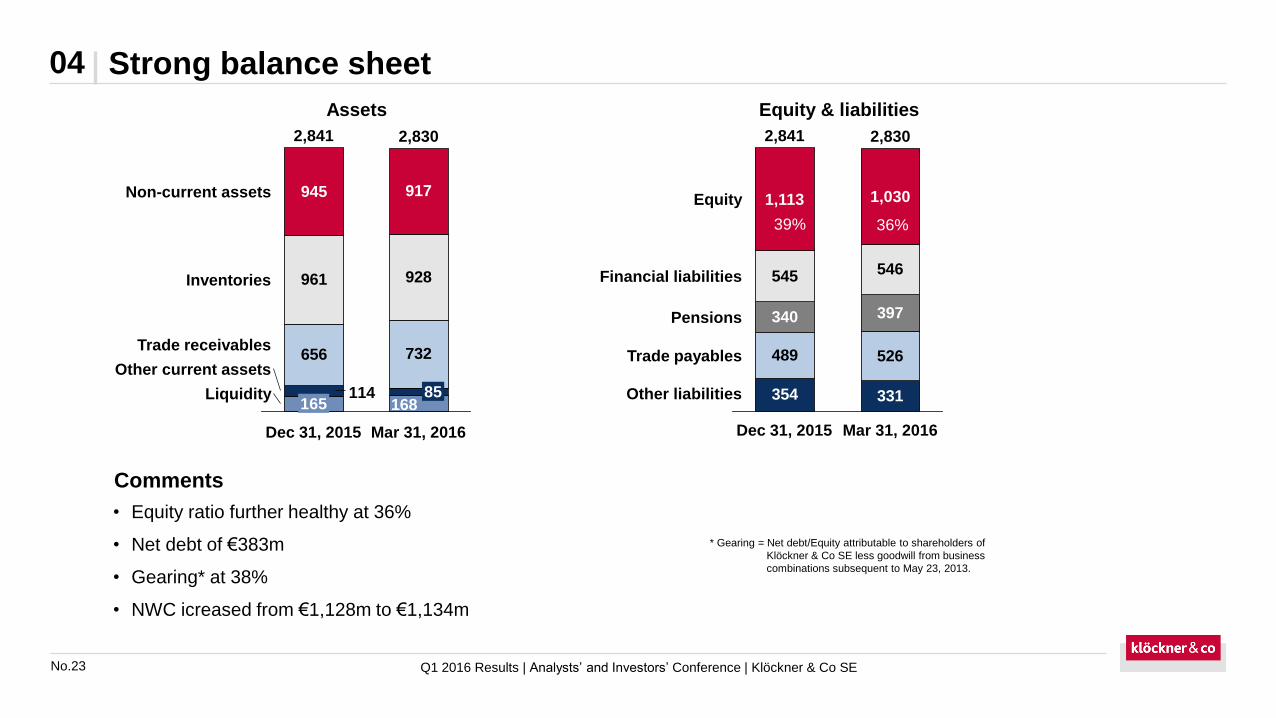

Strong balance sheet04

• Equity ratio further healthy at 36%

• Net debt of €383m

• Gearing* at 38%

• NWC icreased from €1,128m to €1,134m

* Gearing = Net debt/Equity attributable to shareholders of

Klöckner & Co SE less goodwill from business

combinations subsequent to May 23, 2013.

Comments

Assets Equity & liabilities

39% 39%

656 732

168114

928961

917945

Inventories

Non-current assets

Mar 31, 2016

2,830

85

Dec 31, 2015

2,841

165Liquidity

Other current assets

Trade receivables

354 331

489 526

340 397

545 546

Other liabilities

Trade payables

Pensions

Financial liabilities

Equity

Mar 31, 2016

2,830

1,030

Dec 31, 2015

2,841

1,113

39% 36%

No.24 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

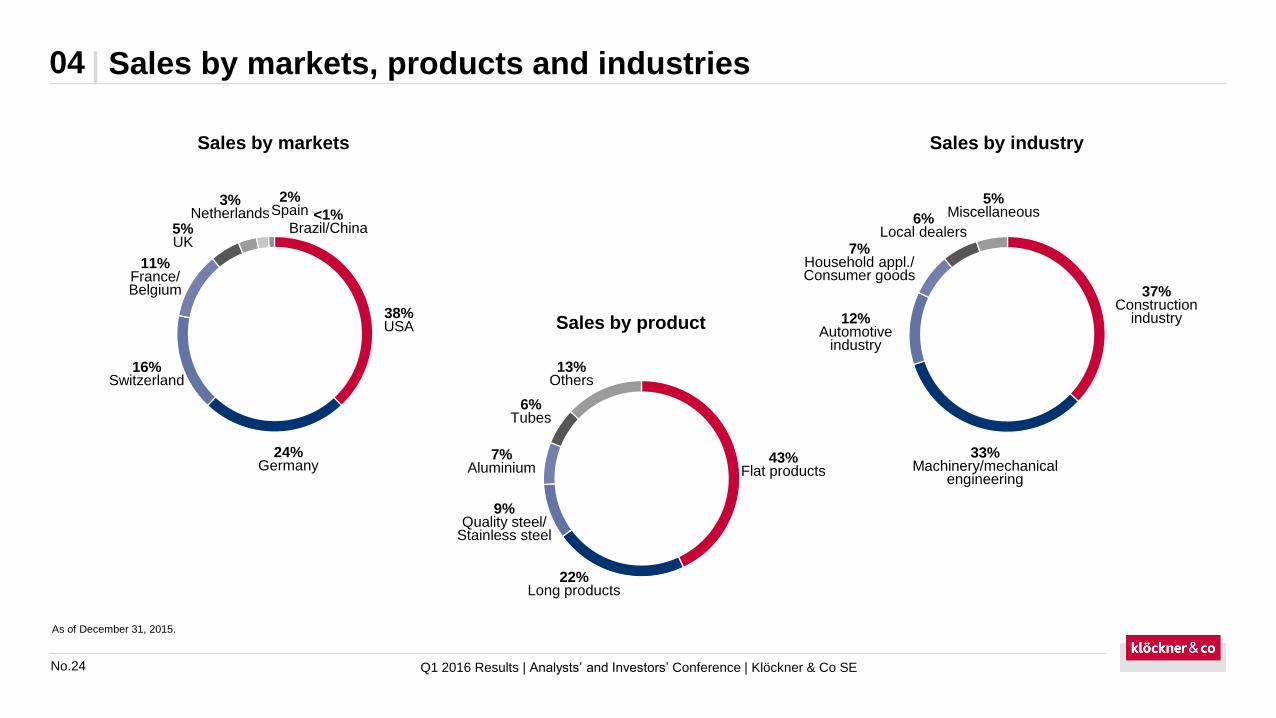

Sales by markets, products and industries04

As of December 31, 2015.

Sales by markets Sales by industry

Sales by product

5%UK

<1%Brazil/China

11%France/Belgium

16%Switzerland

24%Germany

38%USA

3%Netherlands

2%Spain

6%Tubes

7%Aluminium

9%Quality steel/

Stainless steel

22%Long products

43%Flat products

13%Others

12%Automotive

industry

5%Miscellaneous6%

Local dealers

33%Machinery/mechanical

engineering

37%Construction

industry

7%Household appl./Consumer goods

No.25 Q1 2016 Results | Analysts’ and Investors’ Conference | Klöckner & Co SE

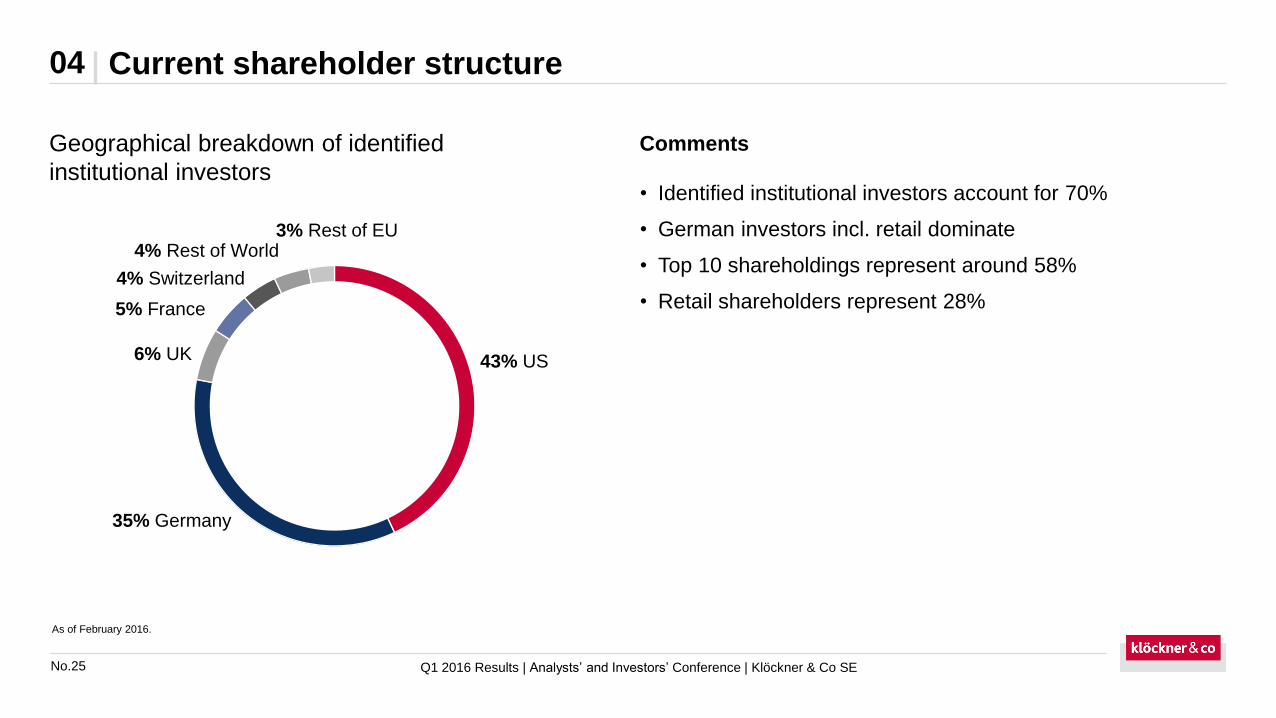

Current shareholder structure04

Geographical breakdown of identified

institutional investors• Identified institutional investors account for 70%

• German investors incl. retail dominate

• Top 10 shareholdings represent around 58%

• Retail shareholders represent 28%

Comments

3% Rest of EU

43% US

4% Rest of World

4% Switzerland

6% UK

5% France

35% Germany

As of February 2016.

Financial calendar 2016

Christian PokroppHead of Investor Relations & Corporate Communications

Phone: +49 203 307 2050

Fax: +49 203 307 5025

Email: [email protected]

Internet: www.kloeckner.com

May 13, 2016 Annual General Meeting 2016,Düsseldorf

August 4, 2016 Q2 interim report 2016

November 3, 2016 Q3 interim report 2016

Contact details