keynote: opportunities, trends & forecasts for o&g - midstream/downstream projects and...

TRANSCRIPT

OPPORTUNITIES, TRENDS & FORECASTS FOR O&G – MIDSTREAM/DOWNSTREAM PROJECTS AND WORKFORCE

Michael Bergen Executive VP, Industrial Info Resources

KEYNOTE

STRATEGIES & OPPORTUNITIES: MANAGING IN A TURBULENT OIL & GAS WORLD

Workforce Next Spring Summit – 2015

P r e s e n t e d b y

Industrial Info Resources, Inc.

Industrial Market Outlook

IIR provides market intelligence that can be leveraged across all departments

Website Resources

IIR’s Industrial Market Coverage

O & G PRODUCTION ONSHORE AND OFFSHORE OIL & GAS PROCESSING LNG EXPORT TERMINALS, GAS-TO-LIQUIDS

O &G PIPELINES ONSHORE AND OFFSHORE CRUDE OIL, CONDENSATE, GAS & REFINED PRODUCTS

O & G TERMINALS STORAGE FACILITIES, LNG RECEIVING & REGASIFICATION

PETROLEUM REFINING (HPI) REFINERIES, LUBE OIL PLANTS AND ASPHALT PLANTS

CHEMICAL PROCESSING (CPI) PETROCHEMICAL, AGRICULTURAL, INDUSTRIAL GASES, ORGANIC & INORGANIC CHEMICALS

PHARMACEUTICAL & BIOTECH MANUFACTURING FACILITIES AND RESEARCH LABORATORIES

ELECTRIC POWER GENERATION, TRANSMISSION & DISTRIBUTION

METALS & MINERALS MINES, MILLS AND PROCESSING PLANTS

INDUSTRIAL MANUFACTURING DURABLE AND NON-DURABLE GOODS MANUFACTURING

FOOD & BEVERAGE PROCESSING & DISTRIBUTION/STORAGE FACILITIES

PULP, PAPER & WOOD MILLS, FOREST PRODUCTS & CONVERTING PLANTS

ALTERNATIVE FUELS ETHANOL, BIODIESEL, COAL GASIFICATION, FUEL PELLETS

Latin America 8,906 Projects $1.23 Trillion 18% Growth

Africa 2,854 Projects $694 Billion 67% Growth

Oceania 2,414 Projects $710 Billion 33% Growth

Asia 37,744 Projects $6.66 Trillion 37% Growth

Europe 14,855 Projects $2.14 Trillion 34% Growth

North America 18,620 Projects $2.41 Trillion 15% Growth

Worldwide Coverage Represents a 30% increase (Feb 2014 to Feb 2015). Flags Represent IIR’s World Regional Research Offices

Our Global Reach 87,388 Projects in Progress worth $13.93 trillion

Based on active projects with future completion dates and QC’d in the last 12 months

Latin America 10,888 Projects $1.3 Trillion 17% Growth

4

42% 37%

41%

28% 19%

30%

18%

17%

20%

29%

30%

29%

5%

6%

6% 10%

14%

8%

7% 10%

7% 5% 7%

7%

6% 4%

4% 5% 7%

4%

13% 16% 12% 13% 15% 15%

8% 8% 7% 8% 8% 6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015

Pharmaceutical

Industrial Mfg

Food & Beverage

Pulp & Paper

Metals & Minerals

Chemical

Oil & Gas

Power

65% 60% 67% 67% 63%

United States

How Has Industry Spending Shifted?

Energy & Chemical Maintain 60+% of Industrial Construction Activity

Pre-fallout observation

$300 billion Proposed

Oil & Gas Production – Industrial Market Spending Driver 7 of the 12 Industries are benefitting from unconventional production

Bakken, Eagle Ford, Permian, Utica

Marcellus, Niobrara

INPUT BENEFICIARIES OUTPUT BENEFICIARIES

6

Drill Pipe Fabrication

Steel Pipe/ Tube Mills

Fracturing Equipment Producers

Proppant Producers

High-Velocity Fluids

Frac Sand Mines

Midstream Processing

Ethylene Capacity

Storage Terminals Fertilizer

Plants

LNG Export Market

Gas to Liquids

Petroleum Refineries

Manufacturing

Electronics

Ceramics

Textile

Micro-LNG Domestic Market

Pipelines

Automotive

Downstream Petrochem

Methanol

Power Generation

Production Field

Still Viable with Low Crude Prices

2,558 Projects @ $182 billion 2007 - 2014

Paints Coatings

Chemical Industry

Rubber & Plastic Good

?

?

?

-1.5

-1

-0.5

0

0.5

1

1.5

Q1 2012

Q2 2012

Q3 2012

Q4 2012

Q1 2013

Q2 2013

Q3 2013

Q4 2013

Q1 2014

Q2 2014

Q3 2014

Q4 2014

Global Supply / Demand Trends Versus WTI/Brent Spot Price

IEA February 2015

WTI Spot $/bbl Brent Spot $/bbl

Short Term Supply / Demand Outlook Marginal Price Increases

7

Dem

and

> S

up

ply

Short Term Supply Trends

• Crude prices stabilized following early Feb gains – Brent higher than WTI.

• Price rebound off falling US rig counts and “opportunistic buyers” – Contango traders

• US rig count declines not yet filtered into lower US production growth.

• Global supply rose by 1.3 m/bpd Yr-on-Yr to an estimated 94 m/bbl/d in Feb.

• Led by a 1.4 m/bpd gain in non-OPEC production.

• US supply revised upwards by 300 k/bpd for Q4 2014 and Q1 2015 also revised up.

• OPEC crude edged down by 90 k/bpd - loses in Libya and Iraq offset higher Saudi, Iranian and Angolan production.

Sup

ply

> D

eman

d

Axis shows difference (mn/bpd) between global crude production and global demand.

-ve indicates demand greater than daily +ve indicates supply volumes exceed demand.

Mn bpd

Sources: IEA, EIA

Short Term Demand Trends

• Global Demand bottomed out in Q2 2014 and since steadily risen. Yr-on-Yr gains of 0.9 m/bpd for Q4 2014 and 1m/bbl/d for Q1 2015.

• Global demand forecast raised 75 k/bpd to 1 m/bpd. 2015 average to be approx. 93.5 m/bpd.

• Global Refining throughputs raised for H1 2015 but annual gains are forecast to be down from 2.2 m/bpd in Q4 2014.

• Storage build up in US, China, India, Europe, S. Korea, Africa, Japan (70% capacity).

North America Petroleum Refining Industry U.S. Crude Imports

© 2015, Industrial Info Resources, Inc., 2277 Plaza Drive Suite 300, Sugar Land, Texas 77479

2,129

829

35 0

500

1,000

1,500

2,000

2,500

3,000

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Tho

usa

nd

s o

f B

arre

ls p

er D

ay

Crude Imports into the US Gulf Coast (PADD 3)

Heavy

Medium

Light

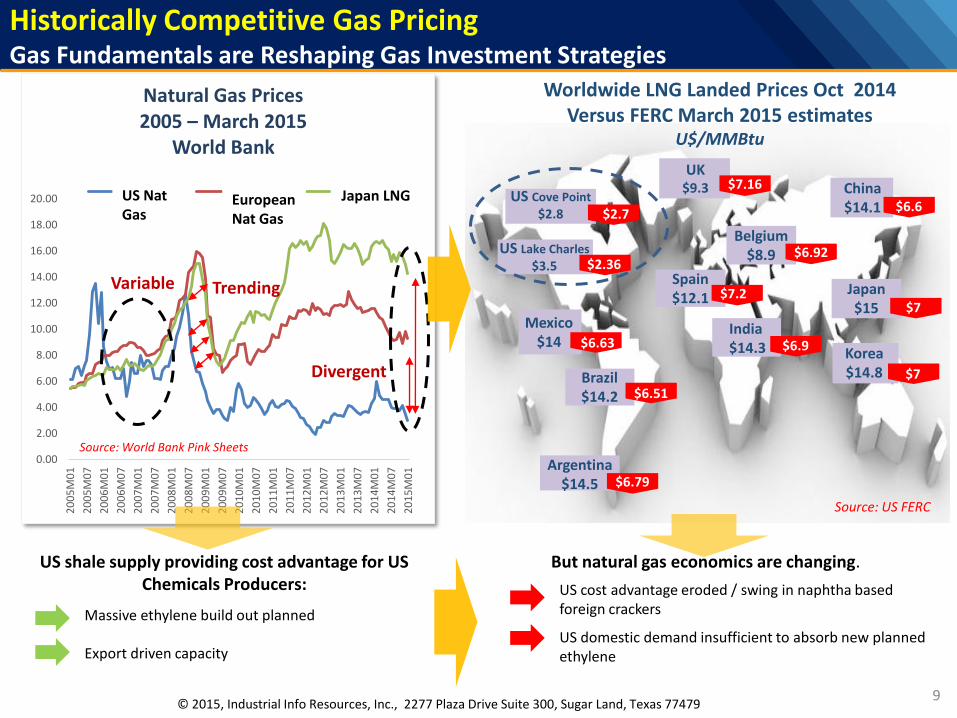

Historically Competitive Gas Pricing Gas Fundamentals are Reshaping Gas Investment Strategies

9

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

20

05

M0

1

20

05

M0

7

20

06

M0

1

20

06

M0

7

20

07

M0

1

20

07

M0

7

20

08

M0

1

20

08

M0

7

20

09

M0

1

20

09

M0

7

20

10

M0

1

20

10

M0

7

20

11

M0

1

20

11

M0

7

20

12

M0

1

20

12

M0

7

20

13

M0

1

20

13

M0

7

20

14

M0

1

20

14

M0

7

20

15

M0

1

Natural Gas Prices 2005 – March 2015

World Bank

Series1 Series2 Series3

Source: World Bank Pink Sheets

Japan LNG European Nat Gas

US Nat Gas

Variable Trending

Divergent

US shale supply providing cost advantage for US Chemicals Producers:

Massive ethylene build out planned

Export driven capacity

US Lake Charles

$3.5

UK $9.3

Belgium $8.9

India $14.3

Mexico $14

Brazil $14.2

Argentina $14.5

Japan $15

Korea $14.8

China $14.1

Spain $12.1

$7.16

Worldwide LNG Landed Prices Oct 2014 Versus FERC March 2015 estimates

U$/MMBtu

US Cove Point

$2.8

Source: US FERC

$2.7

$2.36

$6.63

$6.51

$6.92

$7.2

$6.9

$6.6

$7

$7

$6.79

But natural gas economics are changing.

US cost advantage eroded / swing in naphtha based foreign crackers

US domestic demand insufficient to absorb new planned ethylene

© 2015, Industrial Info Resources, Inc., 2277 Plaza Drive Suite 300, Sugar Land, Texas 77479

$76.6 Billion LNG Export Industry Build Out

Oil & Gas Industry Oil & Gas Production Industry Breakout

5.04

12.14 16.02

23.80 0.00

$0.63

$2.14

$13.56

$15.19 $7.74

$4.64

$0

$5

$10

$15

$20

$25

$30

$35

2014 2015 2016 2017

$ D

olla

rs in

Bill

ion

s

Oil & Gas Production

GTL

LNG

Company LNG Liquefaction Plant Location Cost

1 Cheniere Energy Incorporated Sabine Pass, Louisiana $9.0 bn 2 Sempra LNG Cameron, Louisiana $12.0 bn

3 Lake Charles LNG (Trunkline) Lake Charles, Louisiana $9.0 bn

4 Cheniere Energy Incorporated Corpus Christi, Texas $9.0 bn 5 Freeport LNG Development LP Freeport, Texas $8.0 bn

6 Golden Pass Products LLC Sabine Pass, Texas $3.3 bn 7 Annova LNG Brownsville, Texas $3.7 bn

8 NextDecade (Train 1 only) Brownsville, Texas $8.0 bn 9 Gulf LNG Energy LLC Pascagoula, Mississippi $8.0 bn

10 Dominion Transmission Inc Cove Point, Maryland $4.1 bn

11 Southern LNG Inc (Train 1 only) Elba Island, Georgia $2.5 bn

What’s included in our forecast for LNG?

GTL ? Sasol & G2X NGL Fractionation Bubble

© 2015, Industrial Info Resources, Inc., 2277 Plaza Drive Suite 300, Sugar Land, Texas 77479

155.0

160.0

165.0

170.0

175.0

180.0

185.0

190.0

195.0

200.0

205.0

64.0

65.0

66.0

67.0

68.0

69.0

70.0

71.0

72.0

73.0

74.0

Jan

-13

A

pr-

13

Ju

l-1

3

Oct

-13

Ja

n-1

4

Ap

r-1

4

Jul-

14

O

ct-1

4

Jan

-15

A

pr-

15

Ju

l-1

5

Oct

-15

Ja

n-1

6

Ap

r-1

6

Jul-

16

O

ct-1

6

Pro

cess

ing

Cap

acit

y (i

n B

cf)

Mo

nth

ly P

rod

uct

ion

(in

Bcf

/d)

Natural Gas Production vs. Processing Capacity

Monthly Production Processing Capacity

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Pro

cess

ing

Cap

acit

y (i

n B

cf)

Mo

nth

ly P

rod

uct

ion

(in

Bcf

/d)

Northeast Natural Gas Production vs. Processing Capacity

Monthly Production Processing Capacity

© 2015, Industrial Info Resources, Inc., 2277 Plaza Drive Suite 300, Sugar Land, Texas 77479

Oil & Gas Industry – Upstream/Midstream Natural Gas Processing Overcapacity?

Oil & Gas Industry – Upstream/Midstream Regional Need for Natural Gas Processing Capacity

© 2015, Industrial Info Resources, Inc., 2277 Plaza Drive Suite 300, Sugar Land, Texas 77479

Total US Gas Production

Pipelines – Oct. 2014

TIV

2012 $11.53 B

2013 $10.13 B

2014 $11.15 B

2015 $21.52 B

2016 $16.99 B

2017 $35.62 B

Total $106.96 B

Pipelines – Jan. 2015

TIV

2012 $11.53 B

2013 $10.13 B

2014 $9.27 B

2015 $7.29 B

2016 $27.39 B

2017 $27.81 B

Total $103.28 B

Production – Oct. 2014

TIV

2012 $15.26 B

2013 $8.45 B

2014 $13.82 B

2015 $13.86 B

2016 $8.38 B

2017 $6.03 B

Total $65.82 B

Production – Jan. 2015

TIV

2012 $15.23 B

2013 $8.45 B

2014 $14.23 B

2015 $7.69 B

2016 $4.79 B

2017 $11.29 B

Total $67.4 B

1993 2003 2013 2023

BCF/d 45.7 49.0 66.3 84.7

Oil & Gas Industry Oil & Gas Industry – Upstream/Midstream Crude Oil Transportation

Total Proposed Pipeline Capacity 18.9 Million Barrels

© 2015, Industrial Info Resources, Inc., 2277 Plaza Drive Suite 300, Sugar Land, Texas 77479

October 2014

Miles TIV

2012 1,175 $4,554

2013 1,515 $5,234

2014 4,802 $8,961

2015 3,952 $8,893

2016 4,094 $17,831

2017 790 $395

Total 16,328 $45,868

January 2015

Miles TIV

2012 1,175 $4,554

2013 1,515 $5,234

2014 3,645 $9,600

2015 5,119 $10,249

2016 1,680 $24,460

2017 1,826 $11,077

Total 14,960 $69,436

15 MM BBLs of crude storage capacity was added in 2014

Transportation Costs (per barrel):

Gathering

Canada to Houston

by Rail by Pipeline

by Pipeline by Truck

$0.50 $2.00

$5 - 6.00 $12.00

Thank You!

Upcoming IIR Industry Outlooks Chicago, IL – May 6th 2015

Jersey City, NJ – Sept 9th 2015