kevin slevin tep cta(fellow) att slevin associates carter 19 slevin associates 20 6/(9,1...

TRANSCRIPT

A Presentation to the Society of Trust and Estate Practitioners by

Kevin Slevin TEP CTA(Fellow) ATT

Slevin Associates

1

You know what’s at stake:

Relief due: tax rate 10%

No Relief due: tax rate 28% Only applies to first £10m (lifetime

gains post 6.04.2008)

Maximum negligence claim £1.8 million (Per claimant)

2

A ‘trading company’ is a company carrying on trading activities whose activities do not include to a ‘substantial extent’ activities other than trading activities.

A ‘trading group’ means a group of companies:

(a) one or more of whose members carry on trading activities, and (b) the activities of whose members, taken together, do not include to a substantial extent activities other than trading activities.

3

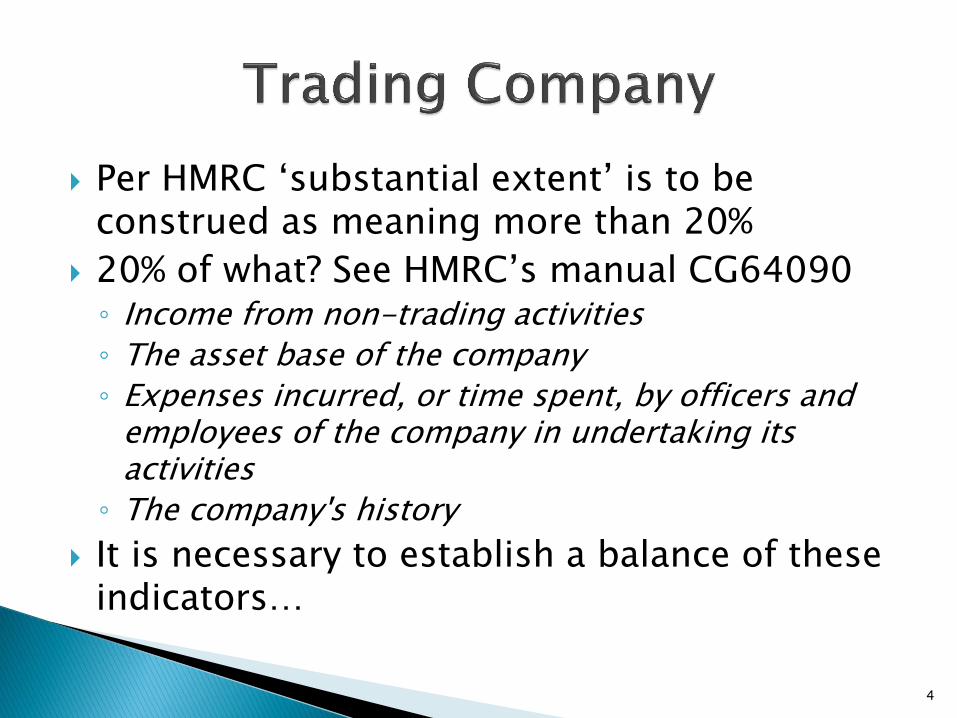

Per HMRC ‘substantial extent’ is to be construed as meaning more than 20%

20% of what? See HMRC’s manual CG64090 ◦ Income from non-trading activities

◦ The asset base of the company

◦ Expenses incurred, or time spent, by officers and employees of the company in undertaking its activities

◦ The company's history

It is necessary to establish a balance of these indicators…

4

The foregoing are “factors, or indicators, that may be useful in establishing whether there is substantial overall non-trading activity.

It may be that some indicators point in one direction and others the opposite way.

[Officers] should weigh up the relevance of each in the context of the individual case and judge the matter "in the round"

HMRC officers are referred to the IHT case of Farmer and another (exors of Farmer dec'd) v IRC SpC 216 for guidance.

5

Does your trading client have large cash accumulations at bank etc?

Each case to be judged on its own merits but Accumulations of funds by a company is

unlikely by itself be a major hurdle where funds derived from past trading activities are held at bank or place on the money market, etc

where there is clearly not an investment business carried on as such.

Consider HMRC’s Non-statutory Business Clearance Procedure – stating area of doubt.

6

See in particular CG64100 & NBCG8800 re Non-statutory Business Clearance Procedure

If the level of cash held is the cause for concern, this should be specifically referred to in the application if the clearance obtained is to be relied upon.

The full facts should be stated having regard to CG64090 re the Trading Company issue.

7

See ‘The Duck Test’ article in lecture notes.

8

The position post 17 March 2015

Asset owned by taxpayer but used by partnership.

9

The position post 17 March 2015

Asset owned by officer or employee but used by his personal company which is a trading company.

10

Biggest entrepreneurs’ relief “grey area” Just what does (c) below mean? 8) For the purposes of this section— (c)

at any time when a business is carried on by a partnership, the business is to be treated as owned by each individual who is at that time a member of the partnership.

Ergo, each partner is to be viewed as a soletrader

for all purposes of ER??? Not so per HMRC? But look at post-cessation

disposals of personal assets – especially where rent paid!

11

12

See CTM 36850

13

14

15

Goodwill can lo longer attract relief

16

17

Jim owns one property and sells it after many years of qualifying lettings. Jim claims ER.

Jim has five properties and sells all five after many years of qualifying lettings. Jim claims ER.

Jim has five properties and sells just one after many years of qualifying lettings of each property. Jim cannot claim ER?

18

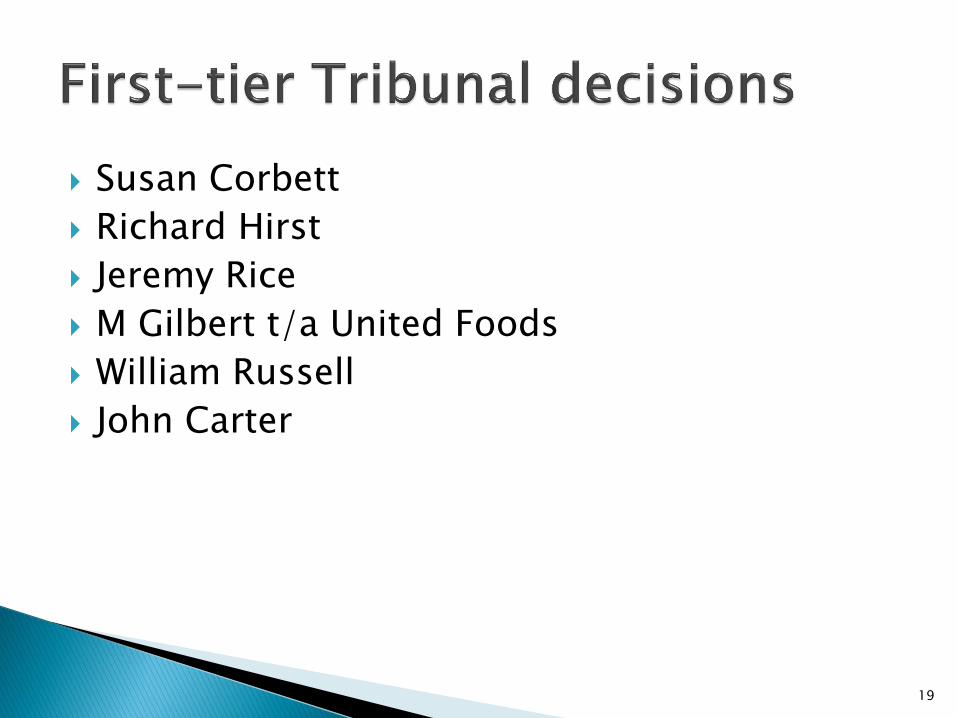

Susan Corbett

Richard Hirst

Jeremy Rice

M Gilbert t/a United Foods

William Russell

John Carter

19

Slevin Associates 20

SLEVIN’S WEALTH WARNING

The tax issues we have discussed today

are very complex and time prevents a detailed examination of

all the technical points.

Specific advice should be sought

before proceeding with, or refraining from, any particular

course of action.

The presenter cannot accept responsibility for any loss arising

from actions taken or refrained from as a result of comments

made during the presentation or shown in these slides or in any

accompanying notes.

© Kevin S Slevin 2015, Kevin Slevin Associates Limited 23 Ticknell Piece Road, Charlbury Oxon OX7 3TN

01608 811411 [email protected]