kefr16-2-내지-53p수정 - kif · 2017. 1. 31. · title: kefr16-2-내지-53p수정 created date:...

TRANSCRIPT

KoreanEconomic

FinancialReview

&

Vol.16 | No.2 | April 2011

President and Publisher

Tae-Joon Kim [email protected]

Contributors (in alphabetical order)

Junghan Koo

Jae-Youn Lee

Kyoobok Lee

Myungwhal Lee

Soonho Lee

Sukho Lee

Yoonsok Lee (Editor)

Hyungjoon (Ray) Lim

Hyoung-Seok Lim

Hyoungsik Noh

Sungwook Park

Jeong Ho Suh

Christopher Byungho Suh

Thomas Steinberger (English Editor)

The Korean Economic and Financial Review, April 2011, Vol.16, No.2. The

KEFR is published four times a year (January, April, July, October) by the

Korea Institute of Finance. Permission to reproduce any portion of this work for

non-commercial purposes or classroom use should be obtained from the Korea

Institute of Finance, (822) 3705-6108, KFB Building, 4-1 Myung-Dong 1-Ga,

Chung-Ku, Seoul, Korea 100-021

Copyright 2011 by the Korea Institute of FinanceSeoul, Korea. All Rights Reserved

Printed by KM

Printed on April 30, 2011

Registration No. Ma-02619

Registration on December 17, 1996

Contents

Overview (Yoonsok Lee)

ⅠⅠ. Macroeconomic DevelopmentsA. Demand and Supply 9

1. Aggregate Demand (Hyoung-Seok Lim, Sungwook Park) 9

2. Aggregate Supply (Hyoung-Seok Lim) 16

B. Inflation (Kyoobok Lee) 19

1. Oil and Import Prices 19

2. Domestic Inflation 21

C. Macroeconomic Outlook for 2011 23

1. Global Economy and Balance of Payments (Sungwook Park) 23

2. Economic Growth (Myungwhal Lee) 25

3. Inflation (Kyoobok Lee) 28

ⅡⅡ. Financial Markets and IndustryA. Asset Prices(Kyoobok Lee, Sungwook Park, Hyungjoon (Ray) Lim) 29

1. Recent Trends 29

2. Outlook for 2011 32

B. Money and Credit (Kyoobok Lee) 34

C. Financial Industries 37

1. Banking Industry (Hyoungsik Noh) 37

2. Non-Banking Financial Institutions (Soonho Lee) 40

3. Securities Industry (Junghan Koo) 45

4. Insurance Industry (Sukho Lee) 47

ⅢⅢ. Current IssuesA. Korea's Credit Card System & Potential Measures

(Jae-Youn Lee) 52

B. The Role of Private Finance in Helping Korean Firms Win

Overseas Projects (Jeong Ho Suh) 56

C. Policy Agenda for Domestic Banks' Foreign Expansion

(Christopher Byungho Suh) 60

Macroeconomic Developments

The domestic economy has maintained its underlying

upward trend on the strength of high growth shown by

exports, even though consumption and facilities invest-

ment have faltered. The Korean exports are likely to

remain strong, and the improvement in domestic

demand, such as facilities investment, will be further

enhanced. These economic forecasts, however, still

remain uncertain due to the risk factors in domestic and

overseas economies.

Outlook for 2011

The Korean economy in 2011 is anticipated to continue

remaining on a robust recovery path. We forecast a

GDP growth of 4.4% for 2011 resulting from an expan-

sion in both domestic demand and exports growth.

Growth is forecast to be 4.0% and 4.7% y.o.y. in the

first and second half, respectively. By the component of

expenditures, exports and private consumption are

expected to increase by 12.2% and 3.3% y.o.y. respec-

tively. We expect also facilities investment and con-

struction investment to be 6.9% and △0.4% y.o.y.

respectively in 2011.

The Korean economy continued to show strong growth in the first quarter of 2011 amid strongexports although consumption and facilities faltered. Despite worries of rapid increase in globalcommodity prices and possible negative effects of the Japan earthquake, we maintain our growthforecast of 4.4% in 2011. We lowered our expected current account surplus to 12.0 billion USD in2011 due to higher import expectations and also revised our won forecast to 1,075. While Koreanbanks deleveraged in the fourth quarter of 2010 we expect growth opportunities to rebound in thefirst half of 2011. During the fourth quarter of 2010, assets of credit card companies increased 7.1%to 54.5 trillion won partly due to recent rapid increase in credit card loans. Meanwhile profitability ofsecurities companies is expected to rise as brokerage commissions is expected to increase due tothe rising transaction volumes.

Overview

Korean Economic and Financial Review [April 2011]4

Export and imports are expected to increase 15.6% and

21.4%, respectively, in 2011. Therefore, the balance of

payments is expected to register a current account sur-

plus of 12.0 billion USD in 2011, smaller than the 28.2

billion USD figure from the previous year. The reduc-

tion should occur mainly from a faster recovery of

imports than exports and rising raw materials prices.

Financial Markets

In the first quarter of 2011, money market rates mostly

increased following a change in the monetary policy by

the Bank of Korea. Meanwhile, long-term market inter-

est rates decreased slightly as investors’ risk aversion

increased due to the Japanese earthquake and nuclear

accident and the unrest in North Africa and the Middle

East and so on. As the base rate of the Bank of Korea is

expected to increase additionally in the rest of 2011

with high inflationary pressure, Treasury bond (3yr)

yields in 2011 are expected to be 4.0%, or 0.3%p higher

than 2010.

In 2011, the won/dollar exchange rate is expected to

average 1,075, down from the 1,156 figure of 2010.

The rate is to be affected by the continuous current

account surplus in Korea, foreign portfolio investment

inflows and the extended easing policy by the Fed. The

downward trend in the won/dollar exchange rate will,

however, be slowed by high raw materials prices and

remaining uncertainties in the international financial

markets.

The Korea Composite Index (KOSPI) ended the first

quarter of 2011 at 2,107 points, up 37 points from the

beginning of the year. The index has been negatively

affected by the Middle Eastern liberalization and the

Japanese earthquake, but managed to recover owing to

the robust buying of institutional investors. In the sec-

ond quarter, Korea’s equity market is expected to have

balanced upside and downside risks.

Overview 5

Money and Credit

In January and February of 2011, the money supply

continued to increase, but at a slower pace. M2 and Lf

growth fell to 5.7% and 5.9% in those period versus

7.4% and 8.3% in the fourth quarter of 2010.

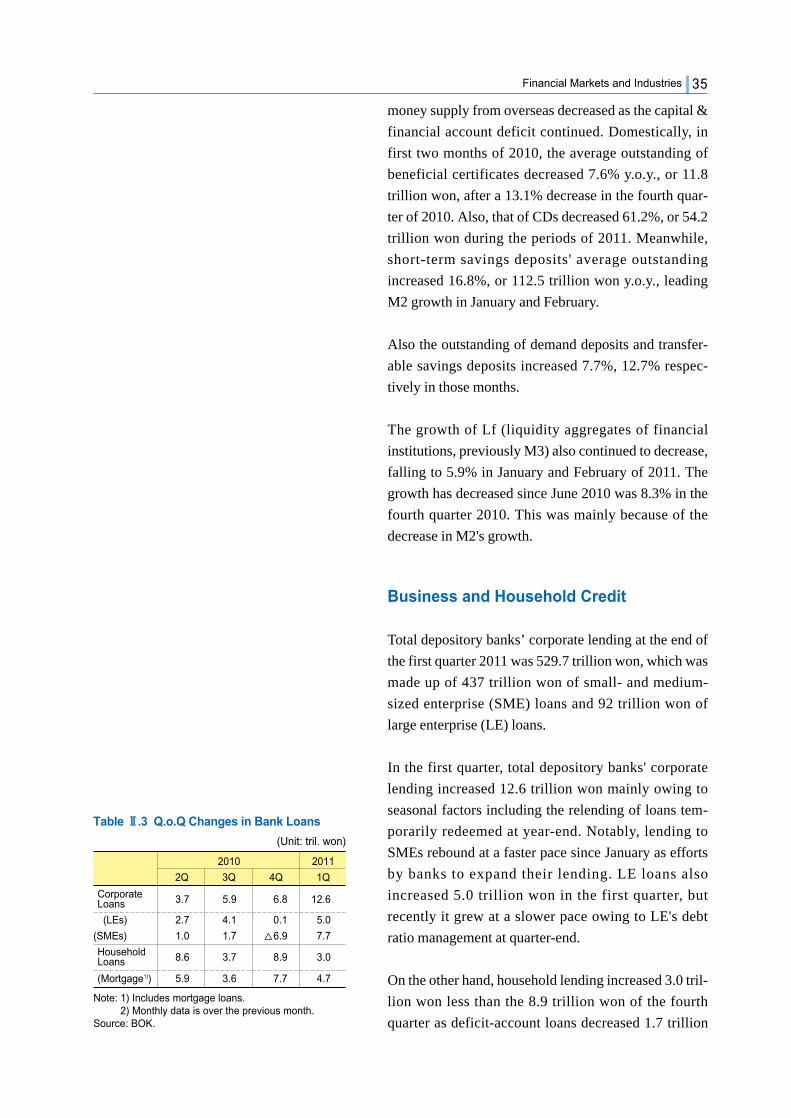

During the first quarter of 2011, total depository banks’

corporate and household lending increased 12.6 trillion

won and 3.0 trillion won each. In 2011, corporate and

individual bank lending is expected to continue to rise

as the solid growth of real economy and high loan

demand from high inflation. However, its growth will

be limited by a rise in the base rate.

Financial Industries

In the fourth quarter of 2010, Korean banks’ assets sig-

nificantly decreased with a meager increase in loans.

Net income decreased over the previous quarter thanks

to a decrease in non-interest income while interest

income increased with the help of an increase in net

interest margins. Both loan loss provisions and bad debt

expenses decreased. The asset soundness substantially

improved whereas the BIS capital adequacy ratio

slightly went down. Growth opportunities for Korean

banks are expected to rebound in the first half of 2011.

Net income is expected to continue to improve. The

asset soundness and the capital adequacy ratio are

expected to ameliorate slightly.

In the fourth quarter of 2010, most non-banking finan-

cial institutions experienced asset growth. The net

income of non-banking financial institutions was posi-

tive except for Mutual Savings Banks and Agricultural

Cooperatives. Excluding installment financing compa-

nies and MSBs, the loan soundness of non-banking

financial institutions improved. Except for Mutual

Credits, capital adequacy also improved. Since the

competition between credit card companies and credit

finance companies become increasingly heated, operat-

ing expenses are expected to increase. Owing to poten-

tial insolvent loans, MSBs and MCs will be required to

adequately manage credit risks.

Korean Economic and Financial Review [April 2011]6

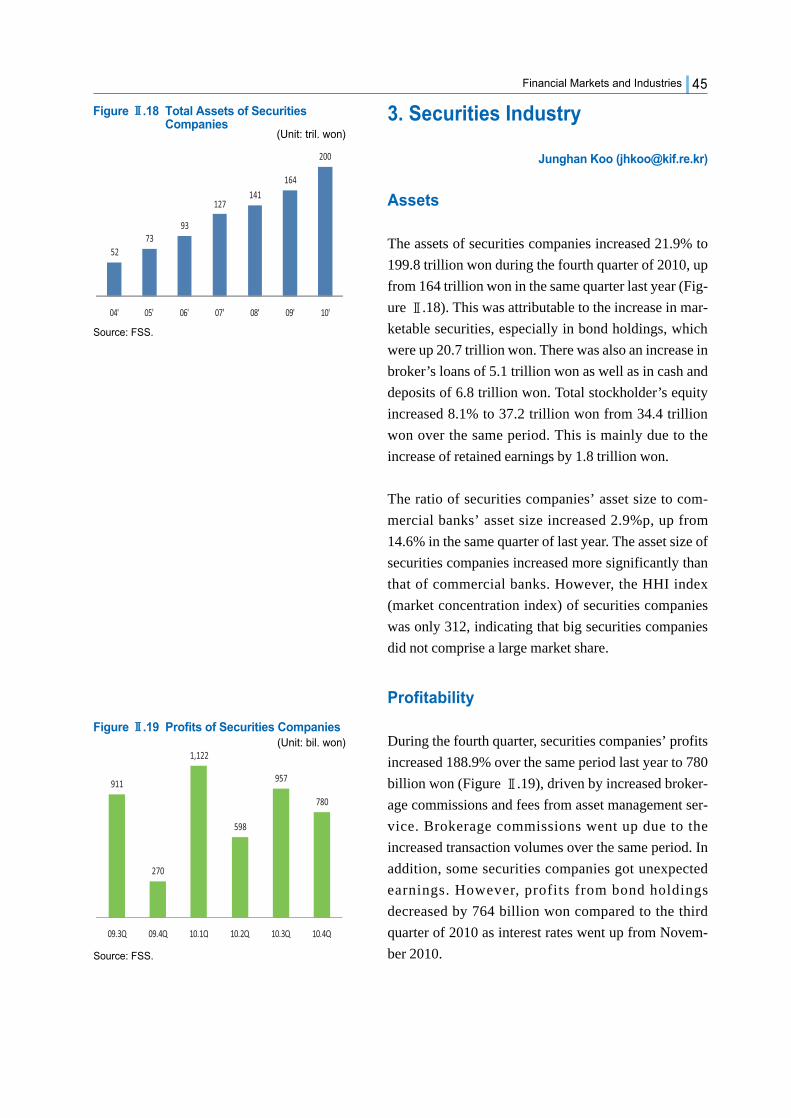

The assets of securities companies increased 21.9% to

199.8 trillion won during the fourth quarter of 2010, up

from 164 trillion won in the same quarter last year. This

was attributable to the increase in marketable securi-

ties, especially in bond holdings, which were up 20.7

trillion won. Securities companies’ profits increased

188.9% over the same period last year to 780 billion

won driven by increased brokerage commissions and

fees from asset management service. Capital adequacy

fell 37%p compared with the same quarter last year.

Despite higher net operating capital, total value at risk

rose due to the higher exposure to interest rate risk.

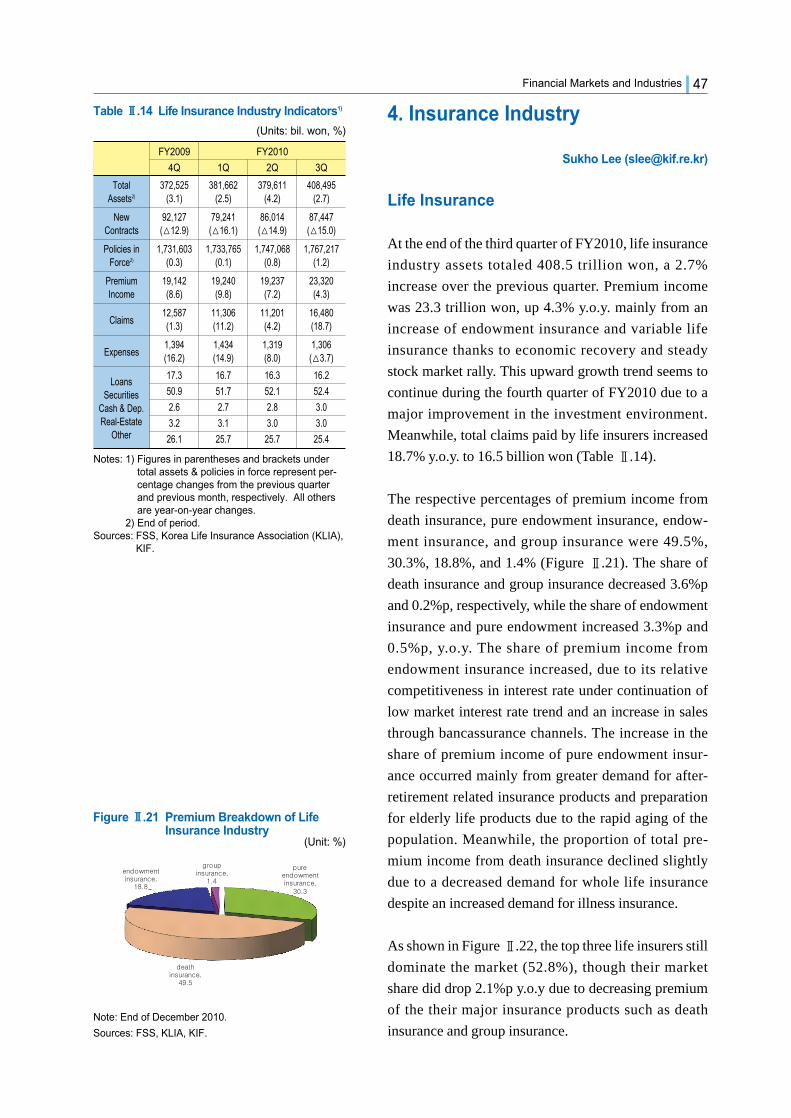

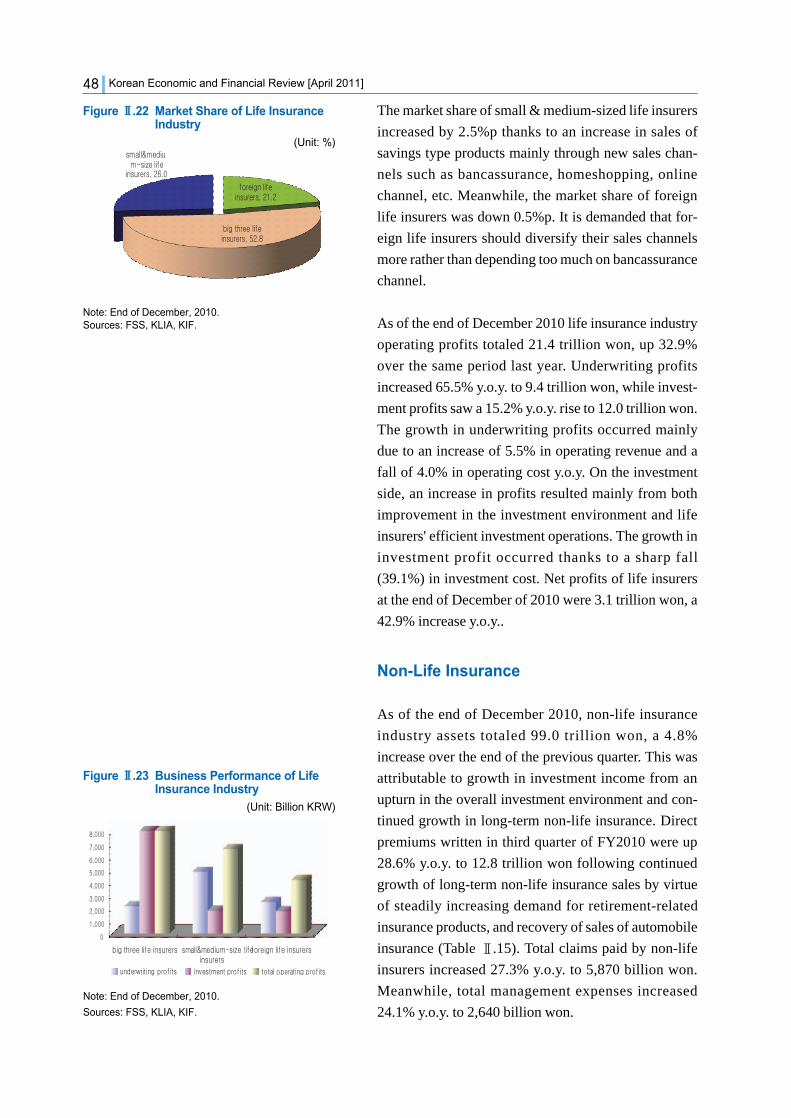

At the end of the third quarter of FY2010, premium

income of life insurers recorded 23.3 trillion won, up

4.3% y.o.y. Direct premiums written for non-life insur-

ers during the same period were up 28.6% y.o.y. to 12.8

trillion won. Total assets and premium income of the

life insurance industry during the first quarter of

FY2011 are expected to grow due to an upturn in the

sales of variable life insurance and continued inflow in

premium income from savings type insurance. Non-life

insurers are expected to maintain the growing trend,

driven by, in particular, long-term non-life insurance.

Current Issues

We have three papers that deals with current issues at

hand. The first paper covers the problems of the current

credit card system and potential measures to resolve

dissatisfaction among merchant members. Rapid

growth and competition in Korea’s credit card market

led to an expansion in benefits for card user members.

The costs of these benefits have been passed on not to

large merchant members but smaller ones because card

companies held the power to determine the merchant

fees of the latter exclusively in the 3-party scheme.

Mandating a merchant member pool system may allow

us to enjoy the benefits of the 4-party scheme while

maintaining the current 3-party scheme because it can

help improve bargaining power over large merchants

for the card companies. The second paper touches on

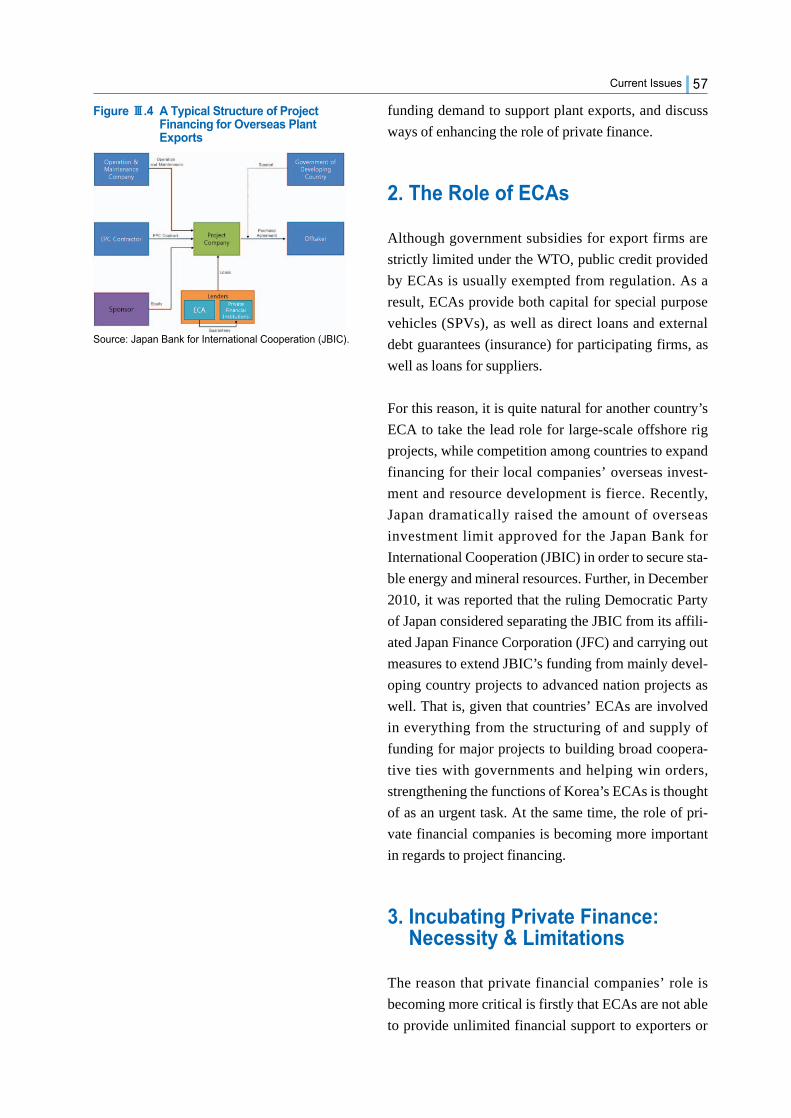

the role of private finance on supporting overseas pro-

jects of Korean firms. With the flurry of infrastructure

Overview 7

investment by resource-rich countries amid recent high

oil prices, competition has been heating up to win

orders for large-scale plants. In order to support mid-

/long-term demand for FX financing effectively, the

functions of Korea’s export credit agencies (ECAs)

should be strengthened first and foremost. However. as

there are limits to ECAs’ funding capacity, Korea also

need to enhance the competitiveness of private finan-

cial companies in the longer-term. ECAs, financial

companies, and supervisory authorities must design a

shared road-map for strengthening the private financial

sector, and push ahead with the globalization of

Korea’s financial industry. The last paper deals with the

policy agenda of domestic banks’ foreign business

expansion. It is imperative for the Korean government

to encourage domestic banks’ globalization through

foreign expansion. However, the institutional environ-

ment for domestic banks’ foreign expansion is not

friendly yet: Korean banks are required to keep their

loan exposure to each foreign country below 10%; it is

impossible for Korean banks to change the purchase

condition upon tender offer abroad; foreign sub-

sidiaries of domestic banks need to provide collateral

when they borrow money form their parent company;

and each foreign branch is subject to evaluation as an

independent entity. The government should abolish

rules that restrict domestic banks’ foreign expansion

and promote challenging so that domestic banks can

leap forward.

Korean Economic and Financial Review [April 2011]8

A. Demand and Supply

1. Aggregate Demand

Hyoung-Seok Lim ([email protected])

The domestic economy has maintained its underlying

upward trend on the strength of high growth shown by

exports, even though consumption and facilities invest-

ment have faltered. The domestic economy will keep

up its underlying trend, even in the presence of external

risks.

Real GDP (chained volume measure) increased 4.2% in

the first quarter of 2011. That primarily reflected posi-

tive contributions from expanded exports of goods &

services. On the production side, manufacturing

increased by 9.9% and services 2.8%. On the expendi-

ture side, facilities investment and exports went up by

12.0% and 16.8%, respectively, in the first quarter of

2011.

Domestic shipments and export shipments increased by

11.5% and 18.2%, y.o.y. in the last year and 6.3% and

15.7% y.o.y, respectively, in February 2011 (Figure

Ⅰ.1).

Macroeconomic Developments 9

The Korean economy continued to show signs of strong growth in the first quarter of 2011 althoughgrowth in consumption and facilities investment have been sluggish to that of last year. World tradevolumes climbed by 12.4% y.o.y. in 2010, following the uptrend in the global economy. It will contin-ue to have a positive effect on exports and improve domestic demand, such as that for facilitiesinvestment. However, there are also risk factors both at the domestic and international level.Domestically, the household debt, which has reached its historical levels, will be one of the seriousrisk. Internationally, sovereign debt problems in the Eurozone and inflationary pressure due to sharprise of oil and raw materials continue to be a challenge for the Korean economy.

Ⅰ.Macroeconomic Developments 1

FigureⅠⅠ.1 Monthly Shipments Indices

Source: National Statistical Office (NSO).

FigureⅠⅠ.2 Industrial Production Index

Source: NSO.

Industrial production and service industry production

have maintained their upward trend. Industrial produc-

tion index, following a 11.7% upswing in the fourth

quarter of 2010, increased by 13.4% and 9.1% y.o.y. in

January and February, respectively (Figure Ⅰ.2). Ser-

vice industry activity index registered 3.2% and 0.2%

increase y.o.y. in the fourth quarter of 2010 and Febru-

ary respectively in 2011 (Figure Ⅰ.2).

Economic Growth

The underlying upward trend of the Korean economy

continues to expand, even in the presence of external

risk. In particular, exports have continuously gone up.

Consumption and facilities investment slightly con-

tracted temporarily in the first quarter of 2011.

The economic growth rate, following a 4.7% y.o.y. in

the fourth quarter of 2010, increased by 4.2% y.o.y. in

the first quarter of 2011. Facilities investment

increased 12.0% y.o.y. in the first quarter of 2011,

including machinery and transport equipment invest-

ments. However, construction investment declined by

11.9%.

Exports in the national accounts grew 16.8% y.o.y. in

the first quarter of 2011, with an upswing in exports of

such items as semi-conductors, automobiles and

machinery. Imports also expanded 10.8% y.o.y. in the

same period.

In March, the trade surplus totaled $3.1 billion, up from

$2.46 billion in February. Exports rose 30.3% y.o.y.,

reaching an all-time high of $48.6 billion. Exports for

the first quarter of 2011 also set a new record with

$131.8 billion. Meanwhile, imports gained 27.9% to

record $45.5 billion. Higher energy prices drove up

inbound shipments of raw materials, which posted a

31.7% increase.

Korean Economic and Financial Review [April 2011]10

TableⅠⅠ.1 Economic Growth Trends

(Unit: %, y.o.y.)

Source: BOK.

2010 2011

1Q 2Q 3Q 4Q Year 1Q

G D P 8.5 7.5 4.4 4.76.2

4.2(q.o.q) (2.1) (1.4) (0.6) (0.5) (1.4)

Consumption 5.9 3.4 3.4 3.0 3.9 2.7

Private 6.6 3.5 3.6 2.9 4.1 3.0

Government 3.4 2.9 2.5 3.2 3.0 1.6

Investment 12.5 6.8 6.8 3.4 7.0 △2.2

Construction 4.3 △2.3 △3.1 △2.9 △1.4 △11.9

Facilities 29.1 30.5 26.6 15.9 25.0 12.0

Exports 16.7 14.5 11.6 15.7 14.5 16.8

Imports 21.5 18.0 14.7 14.2 16.9 10.8

GNI 9.6 5.6 4.5 3.0 5.5 -

FigureⅠⅠ.3 Service Industry Activity Index

Source: NSO.

FigureⅠⅠ.4 Export (f.o.b.) Growth

Source: Bank of Korea (BOK).

1.1 Domestic Demand

Aggregate consumption growth increased to 2.7%

y.o.y in the first quarter of 2011 from 3.0% y.o.y. in the

previous quarter. Private consumption showed sus-

tained growth, rising 3.0% y.o.y., while government

consumption modestly increased, growing to 1.6%,

after rising 3.2% in the previous quarter. The contribu-

tion of aggregate consumption to economic growth

reached 1.9%p, down slightly from 2.0%p in the previ-

ous quarter (Table Ⅰ.2).

Fixed investment declined 2.2% y.o.y. in the first quar-

ter of 2011. Facilities investment has kept on a marked

increase, rising 12.0% from the same period of the pre-

vious year, even though construction investment has

continued to be subdued. Fixed investment’s contribu-

tion to the real GDP growth was △0.5%p in the first

quarter of 2011 (Table Ⅰ.2).

Private Consumption

Private consumption in the national accounts rose 3.0%

y.o.y. in the first quarter, as expenditures on durables

exhibited high upward trends, and those on non-

durables and semi-durables also shifted to an increase.

This reflected increasing household buying power and

positive consumer confidence (Table Ⅰ.1). The con-

sumption-related economic indicators, however,

slightly contracted due to temporary factors such as

Lunar New Year holidays.

The consumer goods sales index declined 0.8% y.o.y.,

from 10.6% in January, due to temporary factors such

as the holiday season in February. By sector, the con-

sumption of durable and quasi-durable goods showed

an increase of 9.0% and 2.3%, respectively, compared

to 14.0% and 11.1% in January, while that of non-

durable goods declined 6.9%, compared to 9.3% of the

previous month. (Figure Ⅰ.6).

The service sector also has managed positive growth.

The service industry activity index increased 4.6% and

Macroeconomic Developments 11

TableⅠⅠ.2 Contributions to Real GDP Growth

(Unit: %p)

Source: BOK.

2010 2011

1Q 2Q 3Q 4Q Year 1Q

G D P 8.5 7.5 4.4 4.76.2

4.2(q.o.q) (2.1) (1.4) (0.6) (0.5) (1.4)

Consumption 4.3 2.4 2.3 2.0 2.7 1.9

Private 3.8 1.9 1.9 1.5 2.2 1.6

Government 0.6 0.5 0.4 0.5 0.5 0.3

Investment 3.2 2.1 2.0 1.1 2.0 △0.5

Construction 0.7 △0.5 △0.6 △0.6 △0.3 △1.8

Facilities 2.4 2.7 2.5 1.6 2.3 1.2

Inventories 2.7 4.0 1.2 0.3 2.0 △0.2

Net Exports △1.8 △1.0 △1.0 1.3 △0.6 3.1

FigureⅠⅠ.5 Contributions to Real GDP Growth

Source: BOK.

FigureⅠⅠ.6 Monthly Index of ConsumerGoods Sales

Source: NSO.

0.2% y.o.y. in January and February 2011, respectively

(Table Ⅰ.3).

At the sector level, finance & insurance, transportation,

business activities, and health & social work sectors

contributed in particular to output growth, while the

real estate & leasing was sluggish, recording △20.2%

y.o.y. in February, due to the real estate downturn

(Table Ⅰ.3).

The Consumer Expectations Index, a measure of

prospects for six months ahead in comparison with the

current situation, fell by 19.0 points to record 75 from

March’s 94, dropping below the benchmark of 100.

The Consumer Evaluation Index, a measure of current

situation in comparison with six months earlier,

recorded 64 in March, down 18.0 points from Febru-

ary’s 82 (Figure Ⅰ.7).

Real gross national income (GNI) increased 5.5% over

the previous year but this growth was smaller than that

of the real gross domestic product due to the deteriora-

tion of the terms of trade. (Figure Ⅰ.8). Per capita GNI

grew by US$ 3,566 to US$ 20,759 from US$ 17,193 in

2009.

Fixed Investment

Fixed investment growth in the national accounts

decreased 2.2% y.o.y. in the first quarter of 2011

reflecting construction investment which declined

11.9% y.o.y., owing to to an increase in civil engineer-

ing which offset the shrinkage of investment for build-

ing construction (Table Ⅰ.1), after diminishing △2.9%

in the fourth quarter of 2010. Facilities investment

including machinery and transport equipment invest-

ments, however, increased 12.0%.

Estimated equipment investment growth (current

value) was 26.6% and 0.7% in January and February,

respectively, buoyed by the decrease in machinery

investment (26.6% and 0.7% y.o.y., respectively).

Korean Economic and Financial Review [April 2011]12

FigureⅠⅠ.7 Consumer Sentiment Indices

Source: NSO.

FigureⅠⅠ.8 GDP, GDI, and Private Consumption

Source: BOK.

TableⅠⅠ.3 Service Industry Activity Indexby Type

(Unit: %, y.o.y.)

Source: NSO.

2010 2011

Year 4Q Sep. Jan. Feb.

Service Industry Activity 3.9 3.2 2.5 4.6 0.2

Wholesale & Retail 5.7 4.7 4.2 8.2 △1.0

Hotels & Restaurants 1.2 1.7 0.0 △0.4 △0.3

Transportation 12.0 10.0 12.0 8.4 4.4

Telecommunications 1.9 3.6 5.3 8.1 1.5

Finance & Insurance 4.6 8.2 7.9 8.0 7.2

Real Estate & Leasing △8.6△24.28△25.3△19.2△20.2

Business Activities 7.5 0.6 8.9 8.7 4.3

Education 2.0 3.1 4.4 4.3 -1.8

Health & Social Work 8.8 4.6 2.5 6.3 3.6

Culture & Sporting △0.4 2.7 △4.4 1.7 0.0

Domestic machinery orders (current value), a leading

indicator, accelerated modestly to 26.7% in January

from 19.7% in February due to the sustained upward

trend in the private sector and the rebound to increase in

the public sector.

The Business Survey Index (BSI) issued by the Bank of

Korea, which measures the level of confidence in the

Korean economy, dropped to 89 points in the first quar-

ter of 2011, from 92 points in the last quarter (Figure

Ⅰ.10). Similar indices produced by the Federation of

Korean Industries and the Korea Chamber of Com-

merce & Industry also showed comparable findings.

Construction Investment, a leading indicator, has been

tepid due to a xmodest decline in related indicators.

Construction Orders, a leading representative indicator,

were sluggish. Domestic construction orders registered

△16.7% growth in February 2011, due to the poor per-

formance shown by the public sector despite the rise in

the private sector (△35.7% y.o.y.). Construction com-

pleted (current value) also fell, slipping to △19.2% in

February, and thus continued the downward movement

from the previous month (△11.0%), due to increasing

sluggishness in construction and civil works.

From October 2008, the Bank of Korea shifted to an

expansionary monetary policy, with the base rate low-

ered from 5.25% to 2.00%, its historically lowest level.

The Bank of Korea, however, decided to raise the base

rate in January (from 2.5% to 2.75%) and March (from

2.75% to 3.0%) due to concerns about consumer price

inflation. Looking ahead, bank interest rates will be

readjusted as necessary to engender a continued upturn

in economic activity and inflation.

1.2 External Demand and theBalance of Payments

Sungwook Park ([email protected])

Even though the world economic recovery continues,

the pace of activity remains geographically uneven.

Macroeconomic Developments 13

FigureⅠⅠ.9 Monthly Equipment InvestmentIndices

Source: NSO.

FigureⅠⅠ.10 Business Survey Index

Source: BOK, Federation of Korean Industries (FKI),Korea Chamber of Commerce & Industry (KCCI).

FigureⅠⅠ.11 Monthly ConstructionInvestment Indices

Source: NSO.

FigureⅠⅠ.12 Real Interest Rateand BOK Base Rate

Source: BOK.

The US economy increased at an annual rate of 3.1%

q.o.q. in the fourth quarter of 2010, an increase from the

2.6% in the third quarter. Personal consumption expen-

ditures increased 4.0% q.o.q. in the fourth quarter of

2010, following an increase of 2.4% in the previous

quarter.

In contrast to private consumption, private fixed invest-

ment grew 6.8% q.o.q. in the fourth quarter, following

an increase of 1.5% q.o.q. in the previous quarter.

Exports of goods & services grew 8.6% q.o.q. from an

increase of 6.8% q.o.q. in the previous quarter. Imports

of goods & services decreased △12.6% q.o.q.. Mean-

while, the US unemployment rate recorded 8.8% in the

first quarter of 2011.

The Eurozone economy grew in the fourth quarter by

2.0% y.o.y. from 2.0% y.o.y. in the previous quarter,

boosted by strong performance in Germany and Swe-

den, which grew 4.0% and 7.2% y.o.y., respectively.

The main drag on the Eurozone was Greece, whose

GDP continued to contract by △6.6% y.o.y in the

fourth quarter of 2010. Eurozone private consumption

increased 1.1% y.o.y, and government spending rose by

0.6% y.o.y.. Exports and imports rose 11.6% y.o.y. and

10.7% y.o.y., respectively, in the fourth quarter. Mean-

while, eurozone unemployment has remained 10.0% in

the first quarter of 2011, slightly below the historical

high of 10.7% in January of 1997.

Japan’s GDP decreased at an annual pace of △1.3%

q.o.q., in the fourth quarter of 2010, driven by a

decrease in private consumption and exports. Private

consumption decreased △0.8% q.o.q. in the fourth

quarter from 0.9% q.o.q. in the third quarter. Private

residential investment rose 2.9% q.o.q., compared with

an increase of 1.8% q.o.q. in the previous quarter. Pub-

lic demand recorded △0.6% q.o.q. in fourth quarter

compared with △0.2% in the previous quarter. Exports

of goods & services decreased △0.8% q.o.q. in the

fourth quarter, down from the 1.5% in the previous

quarter. Meanwhile, Japan’s employment situation still

remains severe, although movements of an incipient

recovery could be seen shortly. The unemployment rate

Korean Economic and Financial Review [April 2011]14

TableⅠⅠ.4 Major Countries’ Economic Growth(Unit: %, q.o.q.)

Note: Annual rates from previous period.1) Bloomberg, y.o.y.2) ECB, Data refer to the Euro 17, y.o.y.

Source: Bureau of Economic Analysis, EurostatCabinet Office, Government of Japan

2009 20102010

1/4 2/4 3/4 4/4

US △2.6 2.8 3.7 1.7 2.6 3.1

Japan △6.3 3.9 6.1 2.1 3.3 △1.3

China1) 9.2 10.3 11.9 10.3 9.6 9.8

EU2) △4.1 1.8 0.8 2.0 2.0 2.0

Germany △4.9 3.6 2.1 3.9 3.9 4.0

France △2.5 1.6 1.2 1.6 1.7 1.5

Sweden △5.3 5.5 2.6 4.4 6.8 7.2

Greece △2.3 4.5 △0.7 △5.0 △5.1 △6.6

TableⅠⅠ.5 Major Countries’ UnemploymentRates (Unit: %)

Source: Bloomberg.

20092010 2011

1/4 2/4 3/4 4/4 1/4

US 9.3 9.7 9.6 9.6 9.6 1.4

Japan 5.1 4.9 5.2 5.1 5.0 4.8

Eurozone1) 9.5 10.0 10.0 10.0 10.0 10.0

TableⅠⅠ.6 Balance of Payments(Unit: 100 mil. USD)

Source: BOK.

2009 20102010 2011

2/4 3/4 4/4 1/4

Current Account 327.9 282.1 88.58 99.31 91.61 27.2

Goods 378.7 419.0 122.4 125.4 123.4 59.5Exports(f.o.b.) 3,581.9 4,642.9 1,175.9 1,182.6 1,270.9 1,277.0

Imports(f.o.b.) 3,203.2 4,223.8 1,053.5 1,057.2 1,147.5 1,217.5

Services △66.4 △112.3 △18.7 △29.6 △22.0 △25.4

Training 52.4 92.5 20.5 24.6 31.9 25.1

Travel △52.2 △79.0 △13.6 △27.0 △18.5 △22.4

Income 22.8 7.7 △10.1 13.0 △0.7 3.9

Current Transfers △7.1 △32.3 △5.0 △9.5 △9.1 △10.8

Exports (f.o.b.) 3,653.3 4,663.8 1,202.4 1,163.2 1,287.5 1,313.0

(%, y.o.y.) (△13.9) (28.3) (33.1) (22.7) (23.8) (29.9)

Imports (c.i.f.) 3,230.8 4,252.1 1,056.3 1,057.0 1,157.3 1,232.9

(%, y.o.y.) (△25.8) (△31.6) (42.8) (24.6) (24.6) (25.6)

recorded 4.8% in the first quarter of 2011, down from

5.0% in the fourth quarter of 2010.

The Chinese economy grew at 9.7% y.o.y. in the first

quarter of 2011, up from 9.8% y.o.y. in the fourth quar-

ter of 2010. Total retail sales of consumer goods

increased 16.3% y.o.y. in the first quarter of 2011.

Investment in fixed assets rose 25.0% y.o.y. in the same

period above. China’s investment in real estate devel-

opment recorded 34.1% y.o.y. in the first quarter of

2011.

Korea’s current account surplus recorded 9.2 billion

USD in the fourth quarter, down from 9.9 billion USD

in the third quarter of 2010, but remained positive

thanks to brisk exports backed by the global economic

recovery. The current account accumulated a surplus of

28.2 billion USD from the year of 2010.

The goods account surplus recorded 12.3 billion USD

in the fourth quarter to hit 12.5 billion USD in the third

quarter, with global economic conditions improving in

neighbor economies and trading partners. In particular,

daily exports averaged a high level of 1.9 billion USD

in September of 2011. The MENA region weathered

the global crisis relatively well, and while the recovery

is now in process, economic growth varies widely

across the region. In Japan, there are large uncertainties

associated with the Tohoku earthquake.

The services account deficit stood at 2.2 billion USD in

the fourth quarter, from 3.0 billion USD in the third

quarter, as travel expenses increased while transport

expenses decreased.

The income account shifted to a deficit of 67.6 million

USD in the fourth quarter from a surplus of 1.3 billion

USD due to the increase in dividend payments overseas.

Moreover, the current transfers account deficit recorded

0.9 billion USD during the fourth quarter from the 1.0

billion USD deficit in the third quarter of 2010.

Exports (customs-cleared basis) rose 28.9% y.o.y. to 48

billion USD from February to March 2011. Imports

Macroeconomic Developments 15

TableⅠⅠ.8 Exports and Export Growth By Sector(f.o.b., Units: 100 mil. USD, %, y.o.y.)

Note: ( ) denotes export growth.Source: Korea International Trade Association (KITA)

2009 2010 2011

4/4 1/4 2/4 3/4 4/4 1/4

Vessels115.3 98.9 146.7 114.1 131.4 165.6

(△11.8) (△8.4) (10.1) (20.4) (13.9) (67.4)

Petroleum & 69.4 62.9 80.0 80.5 92.4 106.9Derivatives (5.4) (44.0) (54.1) (24.0) (33.0) (70.0)

Machinery75.0 77.7 92.0 89.1 102.2 107.3

(△7.3) (33.2) (43.7) (25.2) (36.3) (38.1)Wireless 76.1 66.3 61.3 65.4 83.2 70.7Communication (△8.9) (△10.3) (-22.9) (-18.6) (9.3) (6.6)Equipment

Automobiles81.3 74.4 94.2 83.8 101.8 97.5

(△6.9) (51.2) (62.0) (28.0) (25.1) (31.1)Semi- 103.7 106.9 129.4 141.3 129.4 122.2

conductors (73.3) (120.7) (84.1) (60.8) (24.7) (14.3)Petro- 76.7 85.4 90.8 87.1 93.8 109.0

chemicals (35.0) (58.3) (33.3) (14.8) (22.3) (27.6)

Steel60.0 58.8 71.7 73.9 84.5 84.4

(△13.6) (14.8) (14.7) (30.3) (40.9) (43.6)

Liquid 69.8 67.2 75.8 82.5 73.6 66.6Devices (78.4) (64.1) (34.8) (22.3) (5.6) (△0.8)

Automobile 39.3 41.6 46.1 46.9 55.1 54.0Parts (37.9) (107.3) (74.7) (49.3) (40.2) (29.8)

Computers 23.7 22.4 22.7 20.2 25.9 21.2(25.4) (33.7) (19.1) (-1.9) (9.1) (△5.0)

TableⅠⅠ.7 Monthly Exports and Imports(Unit: 100 mil. USD, y.o.y %)

Source: Korea Customs Service

2010 2011

Sep. Nov. Dec. Jan. Feb. Mar.

Total 394.1 412.6 441.5 446.2 386.1 480.7

Growth 16.2 21.4 22.6 45.2 16.9 28.9Rate

Daily 18.8 17.2 18.0 19.4 20.3 20.0Exports

Total 350.0 386.7 400.6 418.0 362.0 452.9Growth 17.6 30.9 21.7 32.6 16.6 27.3Rate

Daily 16.7 16.1 16.3 18.2 19.1 18.9Imports

Trade 44.1 25.9 40.9 28.2 24.1 27.8Balance

Exports

Imports

increased 27.3% y.o.y. to 45.3 billion USD in the same

period.

Export volume in most key industries was up signifi-

cantly. In particular, automobiles, automobile parts,

steel, petrochemicals, vessels and semi-conductors has

continued to expand due to the pick up in overseas

demand. Stronger exports such as petroleum and deriv-

atives, machinery and wireless communication equip-

ment increased continuously. However, exports of liq-

uid devices and computers decreased 29.1% y.o.y. and

39.9% in the first quarter of 2011 from an increase of

9.3% and 9.1% y.o.y in the fourth quarter of 2010,

respectively.

Growth rates of Korea’s exports to countries increased

in the first quarter of 2011. Exports to China, Korea’s

top overseas market, grew 17.8% y.o.y. in the first quar-

ter of 2011. Exports to ASEAN countries and the US

rose 39.5% and 19.7% y.o.y., respectively, in the first

quarter of 2011, while shipping abroad to the EU

recorded 36.0% y.o.y in the same period. Exports to the

Middle East jumped 32.2% y.o.y., or 7.6 billion USD,

in the same period.

2. Aggregate Supply

Hyoung-Seok Lim ([email protected])

Potential Growth

Potential growth measured by smoothing real GDP

growth rates has been still hovering around 3% which

means real GDP growth can attain 3% without inflation

or other adverse effects by fully utilizing its resources.

However, recently, it has increased slightly. This was

mainly because real GDP growth has been high since

the fourth quarter of 2009 on the strength of the world

economic recovery, as well as the base effects.

Viewing potential growth from a long-term perspec-

tive, it peaked at 10.8% during 1986 and 1987. Since

then, the rate has been in a steady decline. The major

Korean Economic and Financial Review [April 2011]16

FigureⅠⅠ.13 Real and Potential GDP Growth

Note: Potential growth rate was estimated using by HP-

Filtering.

Source: BOK.

TableⅠⅠ.9 Exports by Region(Unit: $100 mill, %, y.o.y.)

Note: 1) ( ) denotes export growth.Source: KITA.

2009 2010 2011

4/4 1/4 2/4 3/4 4/4 1/4

China 254 266 291 292 320 313(45.6) (61.0) (38.9) (22.6) (25.8) (17.8)

Japan 62 60 68 73 81 89(△5.2) (28.6) (33.2) (24.6) (31.4) (49.9)

EU 136 115 147 129 144 157(6.3) (13.5) (22.1) (19.7) (5.5) (36.0)

ASEAN 121 116 138 130 148 162(18.3) (46.1) (39.2) (17.7) (22.4) (39.5)

US 100 105 130 127 136 126(△12.2) (26.8) (36.6) (29.8) (35.3) (19.7)

Latin 76 77 99 97 90 100America (△5.4) (39.5) (67.8) (24.9) (17.4) (30.2)Middle 63 57 76 67 84 76East (△10.1) (10.6) (14.7) (13.4) (31.7) (32.2)

FigureⅠⅠ.14 Total Fertility Rate

Source: NSO

factor behind the downward trend is population

changes like the low birthrate and rapid aging. Births

per female in 2000 and 2010 was 1.21 on average, com-

pared to 1.62 in 1987 and 1996. Meanwhile, the birth

rate increased in recent years after falling to 1.076 in

2005, but the number of newly-born babies remained

unchanged. These factors might lead to a long-run

slowdown in input growth. Further, the global financial

crisis also harmed potential growth.

Total Factor Productivity

Growth accounting analysis using the Cobb-Douglas

production function with human capital shows that

Total

Factor Productivity (TFP) has made up 1.01%p of the

4.58% real GDP growth for the period from 2000 to

2010. It accounts for effects in total output not

explained by the amount of inputs used in production.

During the period from 2000 to 2010, TFP’s portion of

real GDP growth was 22.2% (TFP/GDP growth), lower

than the 23.2% for the 10 years from 1987 to 1996

(Table Ⅰ.10).

Meanwhile, in 2010, TFP’s contribution turned to posi-

tive after two consecutive years of negative figures, as

real GDP increased 6.2% in 2010. During 2008 and

2009, the contribution of TFP growth was negative.

Especially, in 2009, it was △1.0%p of the 0.2% real

GDP growth (based on 2005 prices) after comprising

△0.3%p of the 2.3% real GDP growth in 2008. It was

because employment in 2009 decreased 0.3% and gross

capital formation decreased 15.0%, due to the global

financial crisis (Figure Ⅰ.15). Decreasing TFP during

the global financial crisis indicates that the economy

has been less efficient.

R&D intensity (R&D expenditures as a percentage of

GDP) which is considered to be one of the most impor-

tant determinants of TFP growth has been increasing

steadily (Figure Ⅰ.16). This shows that TFP growth

will remain robust as long as R&D is conducted effi-

Macroeconomic Developments 17

TableⅠⅠ.10 Contributions of TFP and FactorInputs to Average GDP Growth

(Unit: %, %p)

GDP Physical HumanGrowth TFP Capital Capital Labor

’87~’96 8.67 2.01 3.62 0.94 2.11(A)

’00~’10 4.58 1.01 1.98 0.55 1.04(B)

(B)-(A) △4.09 △1.00 △1.64 △0.39 △1.07

FigureⅠⅠ.16 R&D as of GDP

FigureⅠⅠ.15 Recent Trends in TFP and FactorInputs to Average GDP Growth

Source: National Science & Technology Commission

(NTIS)

Source: BOK, NSO, KIF.

Source: BOK, NSO, KIF.

ciently and effectively.

Labor Input and Human Capital

From 2000 to 2010, the annual contribution of labor to

economic growth averaged 1.04%p, down from

2.11%p between 1987 and 1996 (Table Ⅰ.10). This

slowdown can largely be attributed to the slower

growth of the labor force, or economically active popu-

lation, over the past decade (Figure Ⅰ.17). During this

period, the average population growth of those aged

15-64 dipped to 0.58% from 1.67% between 1987 and

1996 (Figure Ⅰ.17). Also, labor’s portion of real GDP

growth (labor/GDP growth) over the past decade fell to

22.6% from 24.3% for the prior 10 year period.

This indicates that the Korean economy has become

less labor-intensive. As the population growth rates

decreases, the slowdown in labor is expected to con-

tinue for many years to come (Figure Ⅰ.17).

The annual contribution of human capital or quality of

labor to economic growth averaged 0.55%p from 2000

to 2010, lower than 0.39%p for the 10 years from 1987

to 1996 (Table Ⅰ.10). However, the quality of labor,

measured in terms of average years of schooling, has

improved over time, albeit at a diminishing rate (Figure

Ⅰ.18).

The recent economic slowdown, which was brought on

by the global financial crisis, led to not only an increase

in the average years of schooling to 11.5 years from 9.7

years from 1987 to 1996 (Figure Ⅰ.18) but also a

decrease in youth employment (ages 15-29).

Youth employment growth continued to decrease,

while employment of those aged 30~59 has been on the

rise and employment of those aged 60 and over has

continued to increase.

These structural unemployment issues therefore remain

a lurking threat to the Korean economy’s potential

growth (Figure Ⅰ.19).

Korean Economic and Financial Review [April 2011]18

FigureⅠⅠ.19 Employment Changes by Age

Source: NSO.

FigureⅠⅠ.18 Labor Force Growth andAverage Years of Schooling

Source: NSO, KIF

FigureⅠⅠ.17 Population Growth Rates(Projections)

Source: NSO.

Physical Capital

Slow physical capital growth is the primary factor

behind the long-run slowdown in potential economic

growth. In recent years, its slowdown has been much

more pronounced than that of either labor inputs or

human capital (Figure Ⅰ.15).

The average annual contribution of physical capital to

economic growth from 2000 to 2010 was 1.98%p,

1.64%p off the 3.62%p attained in the 1987 to 1996

period (Table Ⅰ.10). Meanwhile, in 2010, equipment

investment growth was 25.0%, which may increase

future capital accumulation, with the economic recov-

ery and the base effects of 2009.

In fact, from a long-run perspective, a slowdown in the

rate of capital accumulation usually occurs in a devel-

oping country that is coming off several decades of

rapid growth. In Korea’s case, the capital-output ratio

has been rising steadily, implying that many previous

investment opportunities have been drying up (Figure

Ⅰ.20).

B. Inflation

Kyoobok Lee ([email protected])

1. Oil and Import Prices

Crude oil Prices

Crude oil prices (including WTI, Brent and Dubai)

increased steeply during the first quarter of 2011, as the

geopolitical problems in the Middle East and North

Africa, including the continued insurgency in Libya

triggered from Tunisia and Egypt, continued. Egypt

plays an important role in international energy markets

through the operation of the Suez Canal and the

SUMED pipeline which is a global thoroughfare for oil

traffic, linking Europe to the Middle East and Asia.

Macroeconomic Developments 19

FigureⅠⅠ.20 Capital-Output Ratio

Source: BOK.

FigureⅠⅠ.21 Oil Prices

Source: Bloomberg.

Furthermore, not only supply disruptions but also fears

about the possible spread of unrest to major exporters

have pushed prices higher. There are recent fears that

violence in Nigeria related to the country’s national

election could lead to supply interruptions. A massive

blackout appears to have affected some refineries in

Venezuela, making oil prices, especially Brent crude,

climb above $120 a barrel. Generally in Europe, Brent

crude sourced from the North sea and crude oil

imported from North Africa, a former European colony.

Therefore, the unrest in Africa greatly influenced the

Brent crude price. According to the IEA, OPEC’s

“effective” spare capacity, which excludes Iraq,

Venezuela and Libya, is estimated at 4.08 million barrel

a day, its lowest level since late-2008.

The weak dollar also encouraged the uptrend in prices.

The dollar has traditionally influenced the price of oil

and other commodities, including gold and base metals,

which are mostly priced in the currency and usually

move to compensate for changes in the its value. The

dollar/euro exchange rate increased to 1.44 in April

after lowered to 1.28 in January 2011.

On the other hand, global oil demand also has risen. It

was 89.0 million barrels a day in the first quarter 2011,

versus 86.5 million barrels a day during the same quar-

ter of 2010. Specifically, oil demand of China increased

to 9.9 million barrels a day in the first quarter 2011, up

from 8.9 million barrels a day of the first quarter 2010.

Not only emerging market counties’ demand is

increased, but also the speculation purpose demand

may also be increased. It is presumed that net purchases

of non-commercial oil was 2.64 million contracts in the

first quarter 2011, compared to 1.87 million contracts in

the last quarter of 2010 (Figure I.23). A contract means

a thousand barrel.

In addition, a non-opec’s oil supply in the first quarter

2011 also decreased 0.2 million barrels a day compared

to the fourth quarter 2010, as Alaskan output decreased

because of pipeline-related shut-ins in January. OPEC

crude oil output in February fell by 95 thousand barrels

a day to 30.05 million barrels a day.

Korean Economic and Financial Review [April 2011]20

FigureⅠⅠ.23 Import and Export Price Indices(Won-denominated)

Source: BOK.

FigureⅠⅠ.22 Non-commercial Crude Oil NetPurchase

Source: Bloomberg.

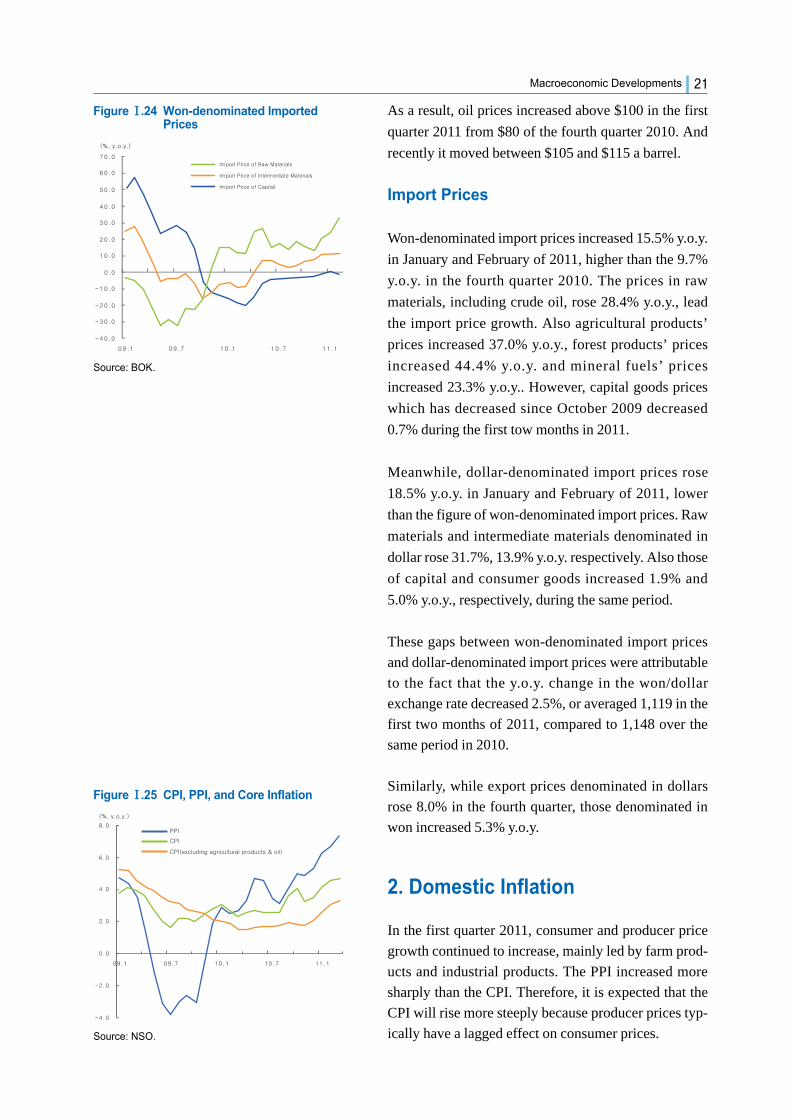

As a result, oil prices increased above $100 in the first

quarter 2011 from $80 of the fourth quarter 2010. And

recently it moved between $105 and $115 a barrel.

Import Prices

Won-denominated import prices increased 15.5% y.o.y.

in January and February of 2011, higher than the 9.7%

y.o.y. in the fourth quarter 2010. The prices in raw

materials, including crude oil, rose 28.4% y.o.y., lead

the import price growth. Also agricultural products’

prices increased 37.0% y.o.y., forest products’ prices

increased 44.4% y.o.y. and mineral fuels’ prices

increased 23.3% y.o.y.. However, capital goods prices

which has decreased since October 2009 decreased

0.7% during the first tow months in 2011.

Meanwhile, dollar-denominated import prices rose

18.5% y.o.y. in January and February of 2011, lower

than the figure of won-denominated import prices. Raw

materials and intermediate materials denominated in

dollar rose 31.7%, 13.9% y.o.y. respectively. Also those

of capital and consumer goods increased 1.9% and

5.0% y.o.y., respectively, during the same period.

These gaps between won-denominated import prices

and dollar-denominated import prices were attributable

to the fact that the y.o.y. change in the won/dollar

exchange rate decreased 2.5%, or averaged 1,119 in the

first two months of 2011, compared to 1,148 over the

same period in 2010.

Similarly, while export prices denominated in dollars

rose 8.0% in the fourth quarter, those denominated in

won increased 5.3% y.o.y.

2. Domestic Inflation

In the first quarter 2011, consumer and producer price

growth continued to increase, mainly led by farm prod-

ucts and industrial products. The PPI increased more

sharply than the CPI. Therefore, it is expected that the

CPI will rise more steeply because producer prices typ-

ically have a lagged effect on consumer prices.

Macroeconomic Developments 21

FigureⅠⅠ.25 CPI, PPI, and Core Inflation

Source: NSO.

FigureⅠⅠ.24 Won-denominated ImportedPrices

Source: BOK.

Producer Prices

In the first quarter 2011, producer prices climbed 6.7%

y.o.y., 1.7%p higher than the last quarter 2010. The

prices growth of agricultural, forest & marine products

fell to 21.0% y.o.y. in the first quarter from 23.7% of the

previous quarter, but still high. Also, the prices of indus-

trial products rose by 7.9% y.o.y. in the first quarter

2011, compared to 5.3% in the fourth quarter of 2010.

Service prices rose just 1.9% y.o.y.. Even though the

prices in professional, scientific & technical services

(which include architectural design, engineering, and

fees for CPAs and tax accountants) increased 3.6% and

the ones in financial services, including brokerage fees

and premiums, rose 5.3%, telecommunication service

prices decreased for five consecutive quarters and the

price of leasing & renting and advertising decreased

0.1%, 0.6% y.o.y., respectively, in the first quarter 2011.

Especially, in March, PPI growth was up 7.3%, which

is the fastest pace since November 2008.

This is because the costs for fresh vegetables and indus-

trial goods jumped. Prices for agricultural, forest and

marine products jumped 16.2% y.o.y. in March, with

live stock prices up 19.9% y.o.y. in the month. How-

ever, the price growth of vegetable was lowered to

5.3% in March as the cold weather has eased. Industrial

products’ prices, including products ranging from tex-

tiles to oil, plastics and computers, climbed 9.1% y.o.y.,

the highest since November 2008.

Consumer Prices

The Consumer Price Index (CPI) rose 4.5% y.o.y. in the

first quarter 2011, which exceed the BOK’s target range

(between 2.0% and 4.0%). The CPI for living necessi-

ties increased 4.9% in the first quarter, reflecting higher

prices for groceries.

Specifically, in the first quarter, consumer prices in the

agriculture, forestry and fishing sector increased 16.6%

and those in industrial products increased 5.0% higher

Korean Economic and Financial Review [April 2011]22

FigureⅠⅠ.26 Contributions to Consumer PriceInflation

Source: NSO, KIF

TableⅠⅠ.11 CPI and PPI

(Unit: %, y.o.y.)

Source: BOK.

2010 2011

3Q 4Q 1Q Jan. Feb. Mar.

CPI 2.9 3.6 4.5 4.1 4.5 4.7

Agriculture and 12.5 19.2 16.6 17.5 17.7 14.9Fishing

Industrial 2.5 2.8 5.0 4.3 5.0 5.9

Service 2.6 3.8 2.4 2.2 2.5 2.5

PPI 3.6 5.0 6.7 6.2 6.6 7.3

Agriculture, Forestry, 11.7 23.7 21.0 26.6 20.8 16.2and Fishing

Industrial 3.9 5.3 7.9 6.8 7.8 9.1

Services 1.3 1.8 1.9 1.8 1.9 2.1

than 2.8% of the fourth quarter 2010.

Especially, in March, consumer prices rose 4.7% the

highest level since October 2008. Notably, while con-

sumer prices growth in the agriculture, forestry and

fishing sector has decreased, industrial products prices

has increased since December 2010, mainly due to the

increase in oil prices.

Core CPI growth, which excludes oil and food costs,

also rose to 2.9% in the first quarter 2011, 1.0%p higher

than the previous quarter’s.

Real Wages

In the fourth quarter 2010, real wages for all industries

increased just 0.7% (y.o.y.) on average, lower than the

4.9% (y.o.y.) of the third quarter 2010. While real wages

in construction and financial intermediation increased

3.4%, 6.8% respectively, real wages for manufacturing

decreased 0.5% y.o.y. and the wholesale & retail sector

decreased 0.9% in the quarter. Furthermore, real wages

for the food & lodging sector continued to decrease by

1.6% for the fifth consecutive quarter.

C. Macroeconomic Outlook for2011

1. Global Economy and Balance ofPayments

Sungwook Park ([email protected])

The global economy should continue its moderate

recovery in 2011 according to the recent forecast by the

IMF. Fears that growth in advanced countries might lose

steam, after restocking process and fiscal stimulus come

to an end, and thus face a risk of a double-dip recession

have been fading. The world economy is expected to

grow at 4.4% in 2011 with advanced economies grow-

ing at 2.4% and emerging and developing economies

Macroeconomic Developments 23

FigureⅠⅠ.27 Real Wage Growth

Source: Ministry of Employment and Labor (MoEL),

BOK, KIF

growing at 6.5%, which implies that the recovery

remains uneven throughout the world. In the mean time,

prices for crude oil has been rising sharply mainly due to

the political unrest in the Middle East and North Africa

and high demand boosted by economic recovery. Soar-

ing oil prices and inflation in emerging economies pose

new risks to a stable recovery of the world economy.

The US economy is expected to recover at the growth

rate of 2.8% in 2011 with easing financial conditions

supporting private demand and external demand. The

US government helped boost the economic growth

with the Federal Reserves’s second round of quantita-

tive easing (QE2) and fiscal package approved in

December 2010. Healthy corporate balance sheet and

pent-up demand for durables may surprise on the

upside in the future. On the other hand, while labor

market seems to improve, unemployment rate of 8.8%

in March is still too high and the decline in the housing

market does not seem likely to stop soon.

The IMF forecasts 9.6% growth for the Chinese econ-

omy in 2011, following the 10.3% growth in the previ-

ous year. The drivers of growth seem to shift increas-

ingly from public to private demand. Inflation has

become one of the major policy concerns as CPI infla-

tion is about to move up above 5% y.o.y even after a

series of increases in the required reserve ratios and

hikes in the interest rates. Nevertheless, fears of a sharp

decline in the growth of the Chinese economy due to

overdone tightening seem to have subduing.

The Japanese economic growth is expected to slow to

1.4% in 2011 from 3.9% in 2010. As for the future fore-

cast, there are many uncertainties associated with the

recent Japanese earthquake which occurred in March. In

addition to the direct damage of capital stock after the

earthquake, possible power shortages and ongoing risks

associated with the crises at the nuclear power plant

pose further downside risks to the economic growth.

The Eurozone economy is forecast to grow modestly

and unevenly at a pace of 1.6% in 2011. The core

economies such as Germany, France and Italy should

Korean Economic and Financial Review [April 2011]24

TableⅠⅠ.13 Economic Outlook for EmergingCountries

Source: IMF WEO (April 2011).

(Unit: %)

Countries 2010Projections

2011 2012

Emerging and7.3 6.5 6.5Developing Economies

Commonwealth ofIndependent States 4.6 5.0 4.7

Developing Asia 9.5 8.4 8.4

Latin America and the 6.1 4.7 4.2Caribbean

Middle East and North Africa

3.8 4.1 4.2

Sub-Saharan Africa 5.0 5.5 5.9

Central and 4.2 3.7 4.0Eastern Europe

TableⅠⅠ.12 Economic Outlook for MajorTrade Partners

Source: International Monetary Fund World EconomicOutlook (IMF WEO) (April 2011).

(Unit: annualized GDP q.o.q.%)

2010Projections

2011 2012

World 5.0 4.4 4.5

Advanced 3.0 2.4 2.6countries

US 2.8 2.8 2.9

China 10.3 9.6 9.5

Japan 3.9 1.4 2.1

Euro Area 1.7 1.6 1.8

grow only gradually at the rate of 2.5%, 1.6%, and

1.1% respectively in 2011 due mainly to the fiscal con-

solidation and the slowdown in external demand

growth. The growth in the periphery of the euro area is

projected to be much lower because of a sharp contrac-

tion in public and private balance sheets and severe

structural unemployment problems.

In emerging markets, economic growth is expected to

remain high in 2011, boosted by accommodative

macroeconomic policies, rising global demand for

commodity prices and strong domestic demand. In the

meanwhile, inflation pressure should broaden. In par-

ticular, developing Asian economies are expected to

continue to expand rapidly and post 8.4% growth, fol-

lowed by economies in the Sub-Saharan Africa and the

Latin America which should grow 5.5% and 4.7%,

respectively, in 2011.

In Korea, the balance of payments is expected to regis-

ter a current account surplus of 12.0 billion USD in

2011, smaller than the 28.2 billion USD figure from the

previous year. The anticipated reduction stems from

expectations of a faster recovery of imports and travel

abroad than that of exports in 2011. Export and import

growth are expected to increase 15.6% and 21.4%,

respectively, for the year.

2. Economic Growth

Myong-Hwal Lee ([email protected])

The Korean economy has maintained its upward trend.

On the production side, manufacturing and services

increased by 9.9% and 2.8% y.o.y. respectively in the

first quarter of 2011. On the expenditure side, facilities

investment and exports have grown consistently, while

construction investment has decreased since the second

half of last year. The employment conditions continued

to improve, as the number of employed persons went

up by 442 thousand persons y.o.y. and the unemploy-

ment rate marked 4.2% in the first quarter of 2011.

Macroeconomic Developments 25

TableⅠⅠ.14 Balance of Payments Forecast

Notes: 1) Figures in parentheses represent percent changes from the previous year.

2) Period average.Source: BOK and KIF.

(Unit: 100 mil. USD)

20102011

1st half 2nd half Year

Current Account 282 49 71 120

Goods 419 144 139 285

Service·Income·△137 △97 △68 △165

Current Transfers

Exports (f.o.b.) 4,664 2,646 2,746 5,392(Growth, %)1) (28.3) (19.6) (12.0) (15.6)

Imports (c.i.f.) 4,252 2,527 2,636 5,163(Growth, %)1) (31.6) (24.0) (19.1) (21.4)

Won/Dollar 1,156 1,100 1,050 1,075Exchange Rate2)

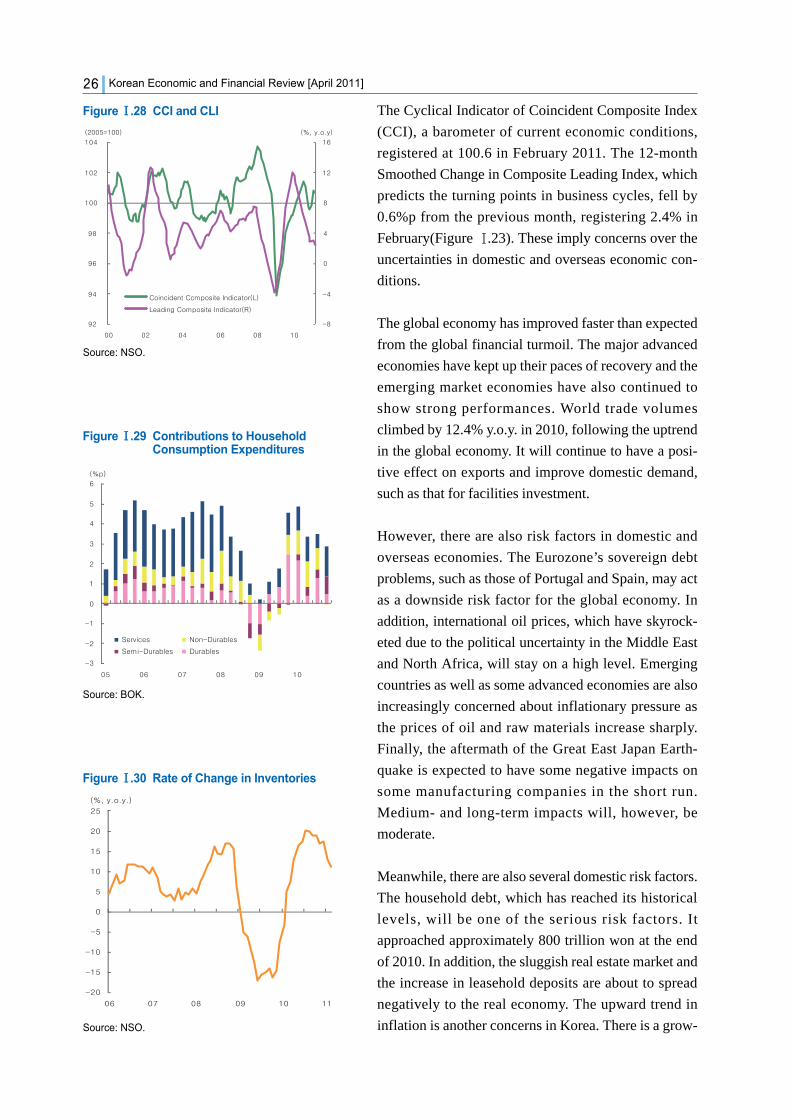

The Cyclical Indicator of Coincident Composite Index

(CCI), a barometer of current economic conditions,

registered at 100.6 in February 2011. The 12-month

Smoothed Change in Composite Leading Index, which

predicts the turning points in business cycles, fell by

0.6%p from the previous month, registering 2.4% in

February(Figure Ⅰ.23). These imply concerns over the

uncertainties in domestic and overseas economic con-

ditions.

The global economy has improved faster than expected

from the global financial turmoil. The major advanced

economies have kept up their paces of recovery and the

emerging market economies have also continued to

show strong performances. World trade volumes

climbed by 12.4% y.o.y. in 2010, following the uptrend

in the global economy. It will continue to have a posi-

tive effect on exports and improve domestic demand,

such as that for facilities investment.

However, there are also risk factors in domestic and

overseas economies. The Eurozone’s sovereign debt

problems, such as those of Portugal and Spain, may act

as a downside risk factor for the global economy. In

addition, international oil prices, which have skyrock-

eted due to the political uncertainty in the Middle East

and North Africa, will stay on a high level. Emerging

countries as well as some advanced economies are also

increasingly concerned about inflationary pressure as

the prices of oil and raw materials increase sharply.

Finally, the aftermath of the Great East Japan Earth-

quake is expected to have some negative impacts on

some manufacturing companies in the short run.

Medium- and long-term impacts will, however, be

moderate.

Meanwhile, there are also several domestic risk factors.

The household debt, which has reached its historical

levels, will be one of the serious risk factors. It

approached approximately 800 trillion won at the end

of 2010. In addition, the sluggish real estate market and

the increase in leasehold deposits are about to spread

negatively to the real economy. The upward trend in

inflation is another concerns in Korea. There is a grow-

Korean Economic and Financial Review [April 2011]26

FigureⅠⅠ.29 Contributions to HouseholdConsumption Expenditures

Source: BOK.

FigureⅠⅠ.30 Rate of Change in Inventories

Source: NSO.

FigureⅠⅠ.28 CCI and CLI

Source: NSO.

ing possibility that the high inflation rate will persist in

the coming months. The Bank of Korea’s monetary

policy is expected to be further tightened in order to

curb inflation.

Gross Domestic Product

The Korean economy in 2011 is anticipated to continue

remaining on a robust recovery path. We forecast a

GDP growth of 4.4% for 2011 resulting from an expan-

sion in both domestic demand and exports growth.

Growth is forecast to be 4.0% and 4.7% y.o.y. in the

first and second half, respectively (Table Ⅰ.15).

By the component of expenditures, all expenditure sec-

tors are expected to bolster except for construction

investment. In particular, exports, boosted by the con-

tinuing upward trends in the global economy, are antic-

ipated to show robust growth. Exports are forecast to

increase by 13.9% and 10.7% in the first and second

half, respectively. Overall, exports are expected to

increase by 12.2% in 2011.

Private consumption growth is also expected to stage a

sustained recovery in 2011 thanks to a rise in asset

prices, such as the increase in stock prices. However,

the increase in private consumption will be restricted

by the effects of the supply-side shock, such as higher

oil prices, and the interest burden on households due to

the interest rate hike of the Bank of Korea. Private con-

sumption is forecast to increase by 3.3% in 2011.

We expect facilities investment to be 6.9% in 2011,

with the rapid growth led by rising global demand and

improvements in corporate earnings. Internal and

external economic uncertainty and the price of interna-

tional oil and raw materials, however, may act as down-

side risk factors of facilities investment.

Construction investment has continued to be muted. It

is anticipated to show a slightly positive growth though

since the public sector will lead the increase in con-

struction investment, centering around SOC invest-

ment. Construction investment is forecast to increase at

Macroeconomic Developments 27

FigureⅠⅠ.32 Estimated Index of EquipmentInvestment

Source: NSO.

FigureⅠⅠ.31 Consumption Indices

Source: NSO.

TableⅠⅠ.15 2011 Macroeconomic Outlook(Unit: %, y.o.y.)

2010 2011

1st 2nd Year 1st 2nd Yearhalf half half half

G D P 8.0 4.5 6.2 4.0 4.7 4.4

Consumption 4.6 3.2 3.9 2.8 3.6 3.2

Private 5.1 3.3 4.1 3.0 3.5 3.3

Investment 9.3 5.0 7.0 △0.7 5.8 2.7

Construction 0.4 △3.0 △1.4 △7.3 5.8 △0.4

Equipment 29.8 21.0 25.0 9.1 5.0 6.9

Exports 15.5 13.7 14.5 13.9 10.7 12.2

Imports 19.7 14.5 16.9 10.4 11.6 11.0

an annualized rate of △0.4% in 2011, by △7.3% and

5.8% in the first and second half, respectively.

3. Inflation

Kyoobok Lee ([email protected])

Inflation (as measured by changes in the CPI) in 2011 is

forecast to be 4.2%, 1.3%p higher than 2010. In the

first half of 2011, inflation is expected to be in the mid-

4% range.

There are persistently high cost-push inflation pressure

in the economy like the increase of oil and raw material

prices and agriculture and forestry prices. In addition to

that, demand-pull inflation pressure with the solid

growth of the real economy. However, this high infla-

tion pressure may be alleviated a little bit by the

decreasing trend of the won/dollar exchange rate and

the government policy to decrease the consumer price.

Korean Economic and Financial Review [April 2011]28

TableⅠⅠ.16 Inflation Forecasts(Unit: %, y.o.y.)

20102011

1st half 2nd half Year

CPI 2.9 4.6 3.7 4.2

PPI 3.8 7.0 5.8 6.4

Notes: Figures are 2011 forecasts.

FigureⅠⅠ.33 Contributions to ConstructionInvestment Growth

Source: BOK.

29

A. Asset Prices

1. Recent Trends

Kyoobok Lee ([email protected])

Interest Rates

In the first quarter of 2011, money market rates mostly

increased following a change in the monetary policy by

the Bank of Korea. Meanwhile, long-term market inter-

est rates decreased slightly as investors’ risk aversion

increased due to the Japanese earthquake and nuclear

accident and the unrest in North Africa and the Middle

East.

The Monetary Policy Committee (MPC) of the Bank of

Korea decided to raise the base rate four times since

November 16, 2010, mainly due to the continued

upward inflationary pressure associated with the con-

tinued upswing in activity and the run-up in interna-

tional raw material prices.

Since the increase in the base rate, CD rates (91 days)

have gone up to 3.40% from 2.66%. CP rates (91 days)

also increased to 3.61% from 2.79%.

Meanwhile, treasury bond yields (3-yr) decreased as

global financial market’s uncertainty increased due to

We expect the Bank of Korea to tighten its monetary policy as the economy continues to strengthenand inflationary pressure still linger. We revised our Treasury bond (3yr) yields slightly higher to4.0%, 0.3%p higher than 2010. Continuous current account surplus, foreign portfolio investmentinflows and the ongoing monetary easing policy by the Fed will strengthen the won and we expectan average of 1,075, down from the 1,156 figure of 2010. Both upside and downside risks seem toco-exist in the equity market. Growth opportunities for Korean banks are expected to rebound in thefirst half of 2011. Assets of credit card companies increased 7.1% to 54.5 trillion won and profitabili-ty of securities companies is expected to improve due to expected increase in trading volumes.Premium income of the life insurance industry in FY2011 are forecasted to increase as sales in vari-able life insurance and savings type insurance show strong growth prospects.

Ⅱ. Financial Markets and Industries 2

Figure ⅡⅡ.1 Major Short-Term Interest Rates

Source: BOK.

Figure ⅡⅡ.2 Major Long-Term Interest Rates

Source: BOK.

the massive earthquake and the nuclear accident in

Japan and the geopolitical unrest in the Middle East and

North Africa region, including Libya and Egypt. Also,

in the bond market, foreign investors’ domestic bond

investment shifted to a slight net buying position since

January 2011. Foreigners’ net purchases was 3.0 tril-

lion won in March, 2.5 trillion won in February and 1.0

trillion won in January. As a result, while treasury bond

yields (3-yr) were above 3.9% before the Japanese

earthquake, it recently hovered the level of 3.7%.

This trend matched major countries' treasury bond

rates. While the bond yields of major countries includ-

ing the US, Germany, the UK and Japan decreased as

global financial uncertainty increased through Febru-

ary to mid-March, they have turned upward and been

steadily rising since late March.

This is because the expectations of economic recovery

increased and the uncertainty about Japan eased after

the G7 decided to intervene to control the yen rise on

March 18.

On the other hand, corporate bond yields moved in sync

with treasury bond yields. After corporate bond yields

(AA-, 3yr) increased to 4.51% in February, they

decreased to 3.89% on March 15, 2011. Recently, how-

ever, it rose to 4.56% in April. Consequently, the credit

spreads on corporate bonds sustained the level of 75bps

~ 80bps.

Exchange Rates

Sungwook Park ([email protected])

During the first quarter of 2011, the won appreciated

3.5% against the U.S. dollar. While the won/dollar had

fluctuated within a narrow band from January till the

middle of March, it fell down below 1,100 relatively

fast in the late March. The fall in the won/dollar rate

reflected not only Korea's strong fundamentals but also

the recent rise in inflation in Korea. It was widely

accepted in the market that the Korean government

Korean Economic and Financial Review [April 2011]30

Figure ⅡⅡ.3 Major Countries’ Treasury BondRates (5yr)

Source: Bloomberg.

Figure ⅡⅡ.4 Won/Dollar Exchange Rate andWon/Yen Exchange Rate

Source: BOK.

would have less incentive to intervene in the foreign

exchange market since the appreciation of the won

would help slow down inflation. Consequently, the

won/dollar rate stood at 1096.7 by the end of March.

The euro rose 5.8% to 1.4158 USD by the end of

March, up from 1.3387 USD at the end of 2010. This

was partly due to the expectation that the ECB would

start to raise its policy rate soon and normalize the mon-

etary policy earlier than other major central banks. In

fact, the ECB has decided to raise its policy rate by 25

basis points to 1.25% on April 7th.

The yen/dollar appreciated to 76.25 on March 17 from

81.52 on December 31, driven by the explosion in the

nuclear power plant. However, the G7 governments’

coordinated intervention since March 18 succeeded in

lifting up the yen/dollar rate above 80. Eventually, the

yen/dollar depreciated 1.5% to 82.8 between the end of

December and the end of March.

Stock Prices

Hyungjoon (Ray) Lim ([email protected])

The Korea Composite Index (KOSPI) ended the first

quarter of 2011 at 2,107 points, up 37 points from the

beginning of the year. In early January, KOSPI contin-

ued an upward trend from last year, breaking 2,100

points on January 14. Then the spread of the Egyptian

liberalization movement following Morgan Stanley's

bearish call on Korean equities on January 21 began

pushing KOSPI downward. From the yearly low 1,928

points on March 2, KOSPI had been gaining until the

Japanese earthquake again moved the index back to

1,924 on March 15. As oil producing countries vowed

to increase their oil production and as globally coordi-

nated effort calmed the Japanese FX market, KOSPI

recovered back to 2,107 points.

The increase in January is mainly due to global liquid-

ity condition backed by Quantitative Easing 2 (QE2) by

the Fed and to the robust outlook of emerging

Financial Markets and Industries 31

Figure ⅡⅡ.6 KOSPI and Total Trade Value

Source: Korea Stock Exchange (KSE).

Table ⅡⅡ.1 Stock Investment Flows(Unit: bil. won)

Note: 1) Including pension funds.Source: KSE.

2010 2011

1/4 2/4 3/4 4/4 1/4

Securities △325 43 434 877 605Cos.

Insurance 339 559 453 △860 △769Cos.

ITCs △2,551 △4,110 △5,607 △6,362 1,552

Banks △931 258 △165 △603 317

Other1) 710 418 1,681 △200 2,804

All △2,758 △2,832 △3,204 △7,147 1,406Institutions

Individuals 3,172 3,237 △3,425 △2,078 639

Foreign 5,930 △404 6,629 9,225 △2,045Investors

Figure ⅡⅡ.5 Dollar/Euro Exchange Rate andYen/Dollar Exchange Rate

Source: BOK.

economies. Risk appetite of foreign investors

decreased in late January, however, as evidenced by

their net selling of Korean equities, reversing the trend.

In this environment, the Japanese earthquake and the

nuclear crisis along with it appeared to further move the

index downward. But KOSPI proved more resilient

than that, though we still have to watch out for nuclear

breakout or abrupt rise in US yields after QE2.

Foreign investors purchased a net 9,225 billion won in

equities in the fourth quarter of 2010, continuing the

6,629 billion won in net buying in the previous quarter.

Foreign investors net purchased 10,579, 14,321, 5,531,

5,930, and -404 billion won in equities in the five preced-

ing quarters. On the other hand, as retail investors kept

redeeming their investments in mutual funds, ITCs trend

of net buying of 6,629 and 9,225 billion won in the two

preceding quarters. Their investment appetite shrank due

to the war in the Middle East and issue of high oil prices

in February. On the other hand, all institutions purchased

a net 1,406 billion won, as ITCs reduced their trend of

net selling of equities and other institutions net pur-

chased on a large scale. In four quarters of 2010, they net

sold 2,758, 2,382, 3,204, and 7,147 billion won. Retail

investors also net purchased equities amounting to 639

billion won in the first quarter of 2011.

KOSPI and KOSDAQ stock issuance in the first two

months of the first quarter amounted to 1,292 billion

won (monthly average), up 18% from the previous

quarter (Table II.2). Corporate financing also increased

in the quarter to 12,442 billion won, due to the increase

in both corporate securities offerings and corporate

bonds issuing.

2. Outlook for 2011

Interest Rates

Kyoobok Lee ([email protected])

Since inflationary pressures are expected to persist as

favorable economic conditions continued and interna-

Korean Economic and Financial Review [April 2011]32

Table ⅡⅡ.2 Corporate Financing(Unit: bil. won)

Note: 1) Total volume of direct financing(bonds and stocks).

2) Offerings on Korea Exchange (KRX) and KOSDAQ.

Source: Financial Supervisory Service (FSS).

2010 2011

1/4 2/4 3/4 4/4

Corporate 9,145 11,552 10,320 10,070 12,442Financing (A)1)

CorporateSecurities 922 725 708 1,092 1,292Offerings (B)2)

•Initial Public 687 213 317 218 314Offerings•Rights 235 512 391 874 978

Offerings

B/A 10.1 6.3 6.9 10.8 10.4

1/4(Jan.~Feb.)

tional commodity prices including crude oil rise, the

base rate of the Bank of Korea is expected to increase

additionally in the rest of 2011.

Therefore, market rates are expected to trend higher

during 2011. However, the increase in market rates

should be limited, since such rates factor in corporate

expectations of the BOK’s future strict monetary policy

and from high demand from financial institutions and

foreign investors.

Therefore, Treasury bond (3yr) yields and corporate bond

(AA- and 3yr) yields in 2011 are expected to be 4.0% and

4.8%. In the first half, they will be 3.8% and 4.6% and, in

the second half, they will be 4.1% and 4.9%.

Exchange Rate

Sungwook Park ([email protected])

In 2011, the won/dollar exchange rate is expected to

average 1,075, down from the 1,156 figure of 2010, dri-

ven by a sustained current account surplus in Korea,

foreign portfolio investment inflows and the ongoing

monetary easing policies of the Fed. However, this

downward trend of won/dollar exchange rate will be

gradual since the US dollar may strengthen after the ter-

mination of QE2 and a high oil price may reduce

Korea’s current account surplus and put a break on the

fast appreciation of won.

Stock Prices

Hyungjoon (Ray) Lim ([email protected]))

In the second quarter of 2011, Korea's equity market is

expected to have balanced upside and downside risks.

The upside risks mainly hinge on two things. First,

emerging economies would win the battle on inflation,

relieving the pressure of central banks to hike the rates

much further. Second, the commodity prices are

Financial Markets and Industries 33

expected to finally decrease, also downsizing the infla-

tion risks.

Downside risks also lurk, however. Should the loss in

project financing loan spread or should the household

debt crisis emerge, the KOSPI could face considerable

downward adjustments. Plus, the pullback of foreign

investors after the QE2 cannot be ruled out, albeit

unlikely.

B. Money and Credit

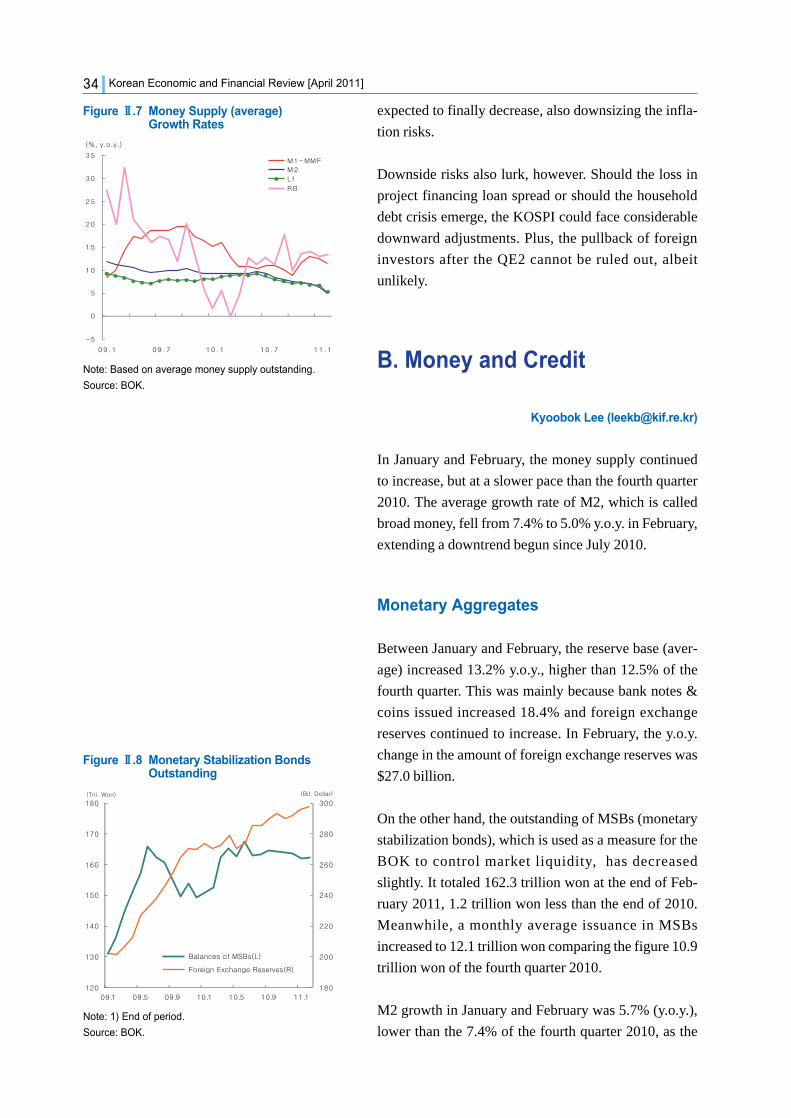

Kyoobok Lee ([email protected])

In January and February, the money supply continued

to increase, but at a slower pace than the fourth quarter

2010. The average growth rate of M2, which is called

broad money, fell from 7.4% to 5.0% y.o.y. in February,

extending a downtrend begun since July 2010.

Monetary Aggregates

Between January and February, the reserve base (aver-

age) increased 13.2% y.o.y., higher than 12.5% of the

fourth quarter. This was mainly because bank notes &

coins issued increased 18.4% and foreign exchange

reserves continued to increase. In February, the y.o.y.

change in the amount of foreign exchange reserves was

$27.0 billion.

On the other hand, the outstanding of MSBs (monetary

stabilization bonds), which is used as a measure for the

BOK to control market liquidity, has decreased

slightly. It totaled 162.3 trillion won at the end of Feb-

ruary 2011, 1.2 trillion won less than the end of 2010.

Meanwhile, a monthly average issuance in MSBs

increased to 12.1 trillion won comparing the figure 10.9

trillion won of the fourth quarter 2010.

M2 growth in January and February was 5.7% (y.o.y.),

lower than the 7.4% of the fourth quarter 2010, as the

Korean Economic and Financial Review [April 2011]34

Figure ⅡⅡ.8 Monetary Stabilization BondsOutstanding

Note: 1) End of period.

Source: BOK.

Figure ⅡⅡ.7 Money Supply (average)Growth Rates

Note: Based on average money supply outstanding.

Source: BOK.

money supply from overseas decreased as the capital &

financial account deficit continued. Domestically, in

first two months of 2010, the average outstanding of

beneficial certificates decreased 7.6% y.o.y., or 11.8

trillion won, after a 13.1% decrease in the fourth quar-

ter of 2010. Also, that of CDs decreased 61.2%, or 54.2

trillion won during the periods of 2011. Meanwhile,

short-term savings deposits' average outstanding