june 3, 2011 the state of retailing online 2011: marketing...

TRANSCRIPT

Making Leaders Successful Every Day

June 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobileby Sucharita Mulpurufor eBusiness & Channel Strategy Professionals

© 2011 Forrester Research, Inc. All rights reserved. Forrester, Forrester Wave, RoleView, Technographics, TechRankings, and Total Economic Impact are trademarks of Forrester Research, Inc. All other trademarks are the property of their respective owners. Reproduction or sharing of this content in any form without prior written permission is strictly prohibited. To purchase reprints of this document, please email [email protected]. For additional reproduction and usage information, see Forrester’s Citation Policy located at www.forrester.com. Information is based on best available resources. Opinions reflect judgment at the time and are subject to change.

For eBusiness & Channel Strategy Professionals

ExECuTivE SuMMARyWhile eCommerce continues to grow and take market share from the physical retail channel, retailers also look to experiment with new approaches to their web businesses such as social commerce and mobile selling. Both of those tactics have generated only single digits in sales for most retailers but promise to capture more marketing dollars in the year to come as web retailers anticipate big gains from those channels in the coming months. Many retailers said they were planning to add custom stores on social networks and incorporate features like ratings and reviews onto their mobile sites.

TABlE OF COnTEnTSOnline Growth Accelerates For Multichannel Retailers

Social network Marketing Emerges As An Area Of investment in Spite Of little ROi

Mobile Strategies Expand To incorporate More Objectives

RECOMMEndATiOnS

Don’t Be Swept Up By The Hype Around Social And Even Mobile

Supplemental Material

nOTES & RESOuRCESThis report uses data from the “The State of Retailing Online,” an annual survey conducted by Forrester Research and executed in conjunction with Shop.org. Respondents include online retailers that transact with consumers by selling products via the internet.

Related Research Documents“Will Facebook Ever drive eCommerce?”April 7, 2011

“The State Of Retailing Online 2010: Key Metrics And Multichannel And Global Strategies”October 28, 2010

“The State Of Retailing Online 2010: Marketing, Social Commerce, And Mobile”July 29, 2010

June 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobileby Sucharita Mulpuruwith Ben Zeidler and doug Roberge

2

17

18

© 2011, Forrester Research, inc. Reproduction ProhibitedJune 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

2

OnlinE GROwTH AccElERATES FOR MUlTicHAnnEl RETAilERS

Forrester Research reported that annual web sales in 2010 totaled $176 billion, an 11% increase over the previous year. Our annual survey with web retailers conducted in partnership with Shop.org exhibited that multichannel retailers and manufacturers fared particularly well (see Figure 1). This growth points to the Web as an increasingly mainstream retail channel. As such, the Web is also a channel that demands retailers’ attention (and budget) as it expands sales in global markets and — via mobile devices — is increasingly integrated with the physical retail store.

Figure 1 year-Over-year Growth Of Web Retailers

Source: Forrester Research, Inc.58625

Percent increase in web sales in 2010 over 2009 by type of retailer

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research*Young: less than four years in operation; medium: four to 10 years in operation; mature: more than 10 years inoperation

†Small: less than $10 million revenue; medium: $10 million to $100 million revenue; large: more than $100million revenue

‡ Multichannel includes brick and mortar, catalogs, television, and other channels.

40%

91%

36%

21%

45% 49%

25% 22%

33%

79%

All companies

Young*

Medium*

Mature*

Small†

Medium†

Large†

Pure-p

lay‡

Multichannel‡

Manufacturer‡

Web tenure Web revenue Channels of operationBase: 68 online retailers

Social network Marketing Emerges As An Area Of investment in Spite Of little ROi

Traditional marketing tactics continue to capture the lion’s share of marketing budgets (see Figure 2). More than half of marketing spend by web retailers is in fact for search and email, the online marketing workhorses. Customer acquisition tactics also remain largely the same as in years past, with search engine marketing and affiliates driving the most value for web retailers. However, this year social networks surfaced higher in the data than ever before as an investment area. This year:

© 2011, Forrester Research, inc. Reproduction Prohibited June 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

3

· Social networks crept higher on the customer acquisition list. While the most successful customer acquisition tactics hands down are in search and affiliate marketing, retailers employ a “long tail” of tactics overall. Several retailers surveyed discovered some success with social networks in the past year, a level similar to those that are able to drive new customers through email prospecting (see Figure 3-1). Social networks ranked fourth on the list of successful customer acquisition tactics for manufacturers selling direct to consumer in particular, indicating that this sector is able to leverage social networks to drive engagement with their brands and promote peer-to-peer sharing (see Figure 3-2).

· Social network spending will grow significantly. For years, search was regarded as the stalwart of the web marketing world; however, the growth of sites like Facebook and Twitter has encouraged retailers to shift areas of focus. This year, more retailers say they will increase their spend levels in social networks than increase paid search spending (see Figure 4). This evolution marks a highly speculative shift in interest from retailers, as search continues to deliver strong figures for them: Fully 53% of retailers surveyed said that paid search in 2010 was more effective than in 2009.1

· Social network presence continues to underwhelm. Despite pinning their hopes for future growth on social networks, social activity continues to deliver little other than qualitative feedback for retailers. On average, retailers report that only a small single-digit percent of sales can be attributed to social media at this juncture. Close to two-thirds (62% and 61%, respectively) of retailers surveyed also note that the ROI associated with social is unclear and that the primary ROI is around listening (see Figure 5). When evaluating Facebook in particular, retailers overall rank the social network low relative to paid search, email, and affiliate marketing. Furthermore, the majority of these retailers feel that, while it delivers better on brand building and listening to customers, Facebook excels neither at acquiring new, nor retaining existing, customers (see Figure 6).

· Mobile marketing exhibits promise. While mobile is not prominent on the overall web marketing spend list, 16% of retailers do say that they plan to increase their mobile marketing spend in the coming year. Marketer focus on the channel, however, may be underrepresented as some mobile focus falls into search. In fact, 22% of retailers surveyed said that they had explicit mobile search efforts and that approximately 3% of their search budgets were dedicated to mobile search.2

© 2011, Forrester Research, inc. Reproduction ProhibitedJune 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

4

Figure 2 Marketing Budgets in 2010

Source: Forrester Research, Inc.58625

Total Pure-play Multichannel Manufacturer

Average budget $5.5 million $4.3 million $7.3 million $2.7 million

Paid search 37% 38% 41% 28%

Email (house and prospecting) 17% 12% 15% 26%

A�liate programs 13% 16% 12% 12%

SEO/natural search 9% 13% 8% 6%

Comparison shopping engines 5% 5% 5% 3%

Remarketing/behavioral targeting 5% 1% 6% 11%

Social network ads 3% 2% 4% 4%

Traditional portal deals 2% 3% 1% 1%

Other 9% 10% 8% 9%

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

Base: 68 online retailers

© 2011, Forrester Research, inc. Reproduction Prohibited June 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

5

Figure 3 Top Customer Acquisition Sources

Source: Forrester Research, Inc.58625

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

90%

49%

44%

18%

18%

10%

10%

7%

7%

4%

4%

3%

3%

3%

1%

1%

1%

Search engine marketing

A�liate marketing

Organic tra�c

Email prospecting

Social network presence

Direct mail

Sweepstakes

Remarketing

O�ine ads

Online marketplaces

Flash sales

Behavioral marketing

Text ads

Coregistrations

Blogs

Microblogs (e.g., Twitter)

Alternative payments

“Which of the following were your top three most effective sources used to acquire customersin 2010?“

3-1

3-2

Rank Pure-play Multichannel Manufacturer1 SEM SEM SEM2 Organic A�liate A�liate

3 A�liate Organic Organic

4 Email prospecting Comparison shopping engines Social network presence

Search engine marketing was the top acquisition tactic in 2010

Top acquisition sources by type of web retailer

Base: 68 online retailers

Base: 68 online retailers

© 2011, Forrester Research, inc. Reproduction ProhibitedJune 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

6

Figure 4 Areas Of increase in Marketing Spend

Source: Forrester Research, Inc.58625

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

75%

61%

72%

61%

61%

61%

36%

33%

22%

16%

13%

13%

12%

9%

“For which marketing tactics are you spending more in 2011 versus 2010?”

SEO/natural search

Social networks

Email to house �le

Paid search

Remarketing

A�liate networks

Behavioral targeting

Comparison shopping engines

Microblogs

Wireless/mobile

Text ads

Online marketplaces

Blogs and message boards

Traditional portal deals

Base: 67 online retailers

© 2011, Forrester Research, inc. Reproduction Prohibited June 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

7

Figure 5 Social Marketing Strategies

Source: Forrester Research, Inc.58625

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

19%

29%

34%

36%

37%

45%

52%

61%

62%

82%

We are pursuing a social marketing strategybecause our senior management

has pressured us to do so

Social marketing strategies have helpedto grow our business to date

We use a speci�c set of metrics by which tomeasure social marketing initiatives

We are pursuing social marketing strategiesbecause our competitors are

We are pursuing social marketing strategiesbecause it is inexpensive to do so

We are pursuing social marketing strategiesbecause there is tremendous buzz about them

We are pursuing social marketing strategiesbecause we do not want to be late movers

We see the primary ROI from socialmarketing as listening to and better

understanding our customers

The returns on social marketingstrategies are unclear

We are pursuing social marketing strategiesbecause this is a great time to experiment

and learn more about what they can do

“To what extent do you agree with the following statements?“(Respondents who selected [5] Strongly agree or [4] Agree on a �ve-point scale)

Attitudes toward social marketing5-1

Base: 68 online retailers

© 2011, Forrester Research, inc. Reproduction ProhibitedJune 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

8

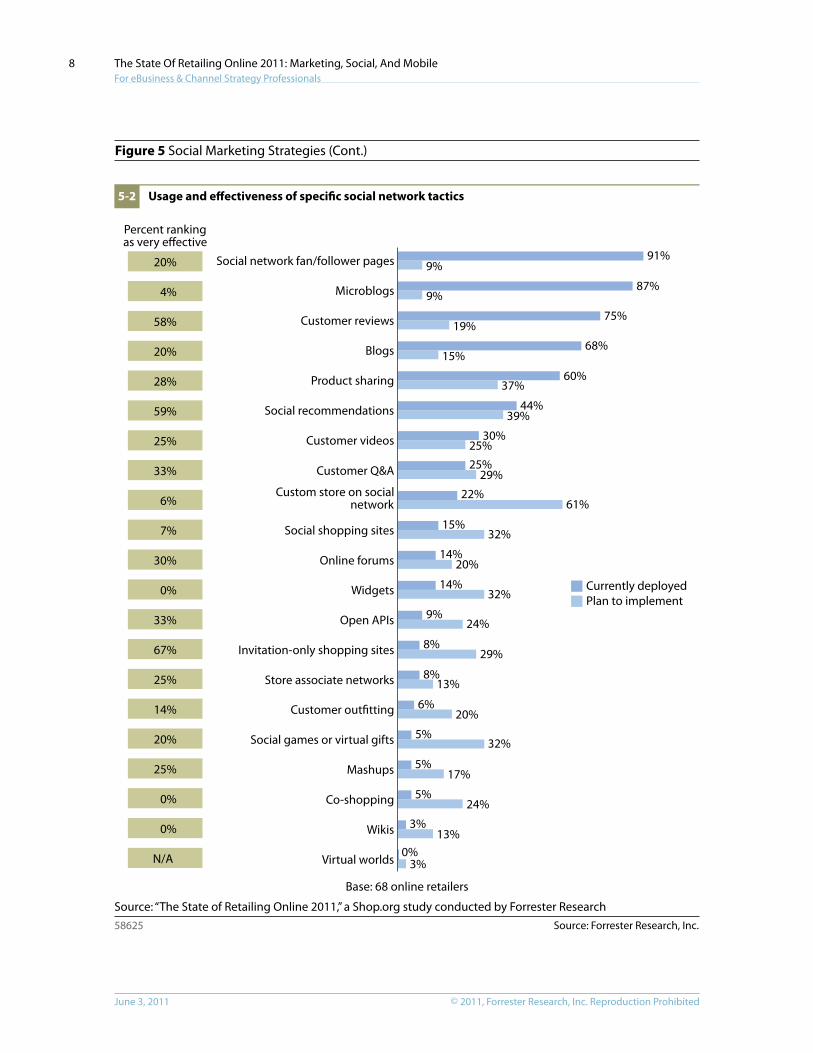

Figure 5 Social Marketing Strategies (Cont.)

Source: Forrester Research, Inc.58625

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

Percent rankingas very effective

20%

4%

58%

20%

28%

59%

25%

33%

6%

7%

30%

0%

33%

67%

25%

14%

20%

25%

0%

0%

N/A

91%Social network fan/follower pages

Microblogs

Customer reviews

Blogs

Product sharing

Social recommendations

Customer videos

Customer Q&A

Custom store on socialnetwork

Social shopping sites

Online forums

Widgets

Open APIs

Invitation-only shopping sites

Store associate networks

Customer outfitting

Social games or virtual gifts

Mashups

Co-shopping

Wikis

Virtual worlds

9%

9%87%

75%

68%

60%

44%

30%25%

22%

15%

14%

14%

9%

8%

8%

6%

5%

5%

5%

3%

0%

19%

15%

37%

39%

25%29%

61%

32%

20%

32%

24%

29%

13%

20%

32%

17%

24%

13%

3%

Currently deployedPlan to implement

Usage and effectiveness of specific social network tactics5-2

Base: 68 online retailers

© 2011, Forrester Research, inc. Reproduction Prohibited June 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

9

Figure 5 Social Marketing Strategies (Cont.)

Source: Forrester Research, Inc.58625

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

“How are you measuring the effectiveness of social media initiatives that youhave implemented to date?”

94%

72%

69%

69%

62%

59%

49%

38%

35%

34%

34%

29%

21%

21%

18%

18%

Growth rate of followers

Click-throughs to the retail site

Total subscribers

Sales attributable to links on socialnetworks

Total visits to social tool

Unique visitors

Requested action taken

More than one review

Return visits

Time spent

Improved SEO

Number of forwards

Market research

In�uencers reached

Media buzz

Sentiment analysis

Measurement of social network tactics5-3

Base: 68 online retailers

© 2011, Forrester Research, inc. Reproduction ProhibitedJune 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

10

Figure 6 Facebook is used For Brand Building not driving ROi

Source: Forrester Research, Inc.58625

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

40%

37%

16%

6%

1%

Brand building

Listening to customers

New fans or likes

Lifetime value of existing customers

Customer acquisition

68% of retailerssurveyed said that ifFacebook went awaytomorrow, it wouldnot adversely affectweb sales in 2011.

“Please rank the following four marketing tactics in terms of return on investment for your company.”

Key benefits of Facebook6-1

Rank order of ROI of key marketing tactics6-2

Facebook metrics for web retailers6-3

Facebook’s impact on email marketing6-4

Rank Total Pure plays Multichannel Manufacturers

1 Email Email Email Affiliate

2 Paid search Paid search Paid search Email

3 Affiliate Affiliate Affiliate Paid search

4 Facebook Facebook Facebook Facebook

Measure/KPI Average

Percent of sales attributable to “social” 2%

Percent of site customers who are also Facebook fans 11%

Percent of email subscribers who are also Facebook fans 11%

65%

63%

53%

32%

7%

1%

We plan to maintain both Facebook and email

Facebook is not a substitute for email

Facebook is a complement to email

Facebook will not be a substitute for email

Facebook will be a substitute for emailin the next 12 to 24 months

Facebook is a good substitute for email

The top metric formeasuring Facebookis the growth of fans/likes.

Base: 68 online retailers

Base: 67 online retailers

Base: 68 online retailers, 49 online retailers, 47 online retailers, respectively

Base: 68 online retailers

“In your experience to date, Facebook delivers better on:”(Please select one)

“Please indicate which statements below you agree with regarding Facebook as a substitute for email:” (Select all that apply)

© 2011, Forrester Research, inc. Reproduction Prohibited June 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

11

Mobile Strategies Expand To incorporate More Objectives

In “The State of Retailing Online 2011” study, we incorporate tablet investments and metrics in our discussion around mobile. As the number of households with smartphones and tablets has continued to grow in the past 12 months, retailers have also expanded their offerings to shoppers in these channels. Progress on numerous fronts is palpable: While a double-digit percent of retailers surveyed in last year’s survey said that they did not have a mobile strategy at all, progress can be measured by the fact that fewer than one in 10 responded the same this year (see Figure 7). Increasingly, web teams have come to own the mobile channel in many cases and are often turning to outside partners to develop products quickly across multiple devices and browsers. While mobile is well poised to be executed well, many challenges continue to exist.

· Many retailers still have not optimized their mobile presence. The availability of mobile-optimized web presences continues to wane in the retail world. While more retailers claim to have a mobile strategy in place, many simply have shrunk their existing sites on smartphones. Fully 44% of retailers surveyed said that they had nothing special about their mobile sites (see Figure 8).

· There is little differentiation in objectives for smartphones versus tablets. In spite of very different experiences that have the ability to serve shoppers in different states, retailers appear to want both devices to achieve all objectives to equal degree, versus defining distinct objectives that leverage the advantages of each. Whereas smartphones are best for real-time offers that supplement in-store experiences, tablets are able to enrich the brand experience in a consumer’s home, often substituting time away from a PC or laptop. In fact, the only difference in objectives is related to in-store usage of tablets for store associates, which is higher than for smartphones (see Figure 9-1).

· Retailers are saddling mobile platforms with traditional web-centric goals and features. Most retailers agreed on a key priority for their mobile efforts: revenue and sales (see Figure 9-2). Indeed, mobile functionality currently offered reflects largely “traditional” web-centric features such as product information, ratings and reviews, store locator info, and payment options, as well as sales alerts and coupons. With some exceptions, planned functionality enhancements center largely on much the same. However, in separate research with consumers, shoppers cite that usability and form factor issues are significant inhibitors to the mobile shopping experience. To date, in-store functionality such as in-store product availability, checkout, store maps/layouts, 2D bar codes, real-time coupons for shoppers who are already in the store, and in-store navigation have had little investment (see Figure 9-3). Even though some investment is planned for several of these features, it appears that the majority of retailers will not be investing here and thereby will miss the opportunity for palpable ROI for their mobile channels.

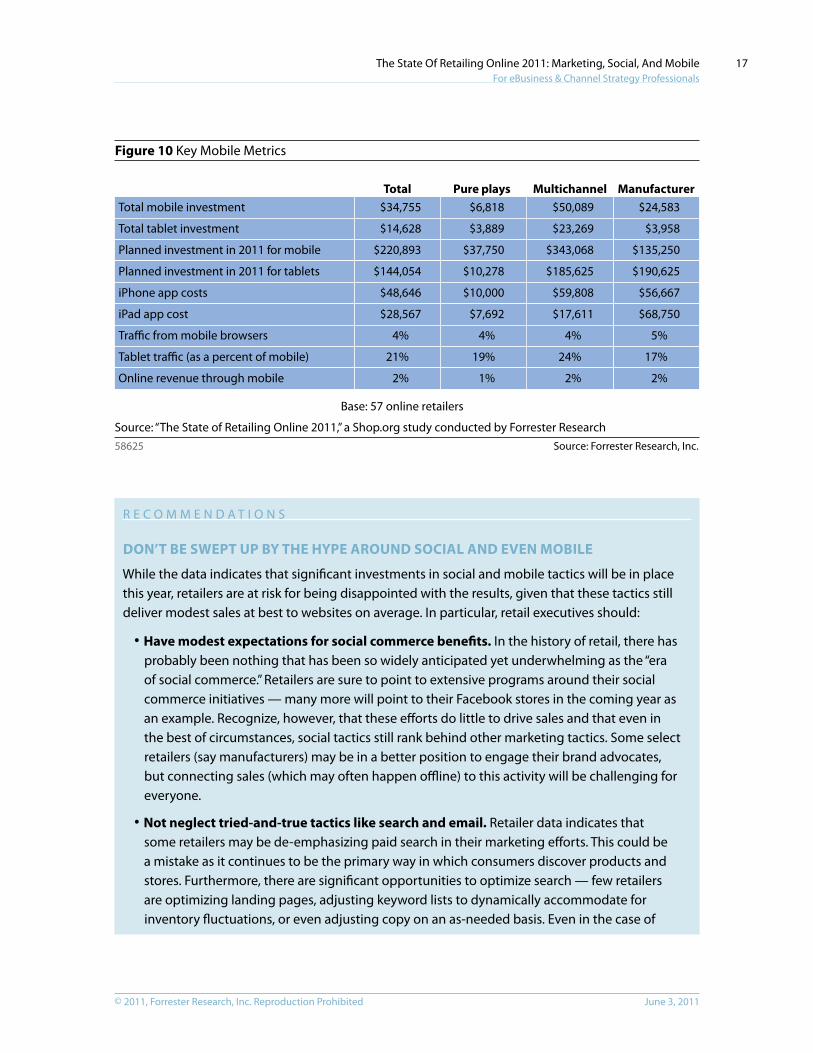

· Mobile retail metrics are mixed. One of the key arguments to invest in mobile programs in the past was that significant traffic was coming to retail websites even though sites were not optimized for the experience. In the past year, even with greater investment, the overall average

© 2011, Forrester Research, inc. Reproduction ProhibitedJune 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

12

metrics of traffic and revenue to sites from smartphones has not increased significantly (see Figure 10). Investment levels in fact may be altogether inadequate. Investments in mobile banking, for instance (where some banks now report 50% of their traffic even though mobile traffic to bank sites also experienced very slow adoption curves in the earlier part of the last decade), now measure millions of dollars annually for the most successful players. For the time being, select retailers like Amazon.com and eBay are likely to be the primary recipients of mobile shopping traffic because of the ease of use of their sites and simple purchasing capabilities.

Figure 7 development Process For Retailers’ Mobile Strategy

Source: Forrester Research, Inc.58625

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

“Which of the following best describes your mobile strategy today?”

“Who owns mobile strategy and management within your organization?”

Mobile strategy stage7-1

Owners of mobile strategy7-2

9%

34%

9%

19%

29%Have a strategy, implemented it,now re�ning it

Don’t have a strategy

Early stage; developing a strategy

Have a strategy

Have a strategy and starting work

More mature

Less mature

Web/eCommerceteam42%

Marketing/CMO24%

President or otherdivision head

18%

No one . . . yet9%

Other7%

44% of surveyrespondentshave one ormore employeesdedicated tomobile e�orts.

Base: 68 online retailers

Base: 67 online retailers

© 2011, Forrester Research, inc. Reproduction Prohibited June 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

13

Figure 7 development Process For Retailers’ Mobile Strategy (Cont.)

Source: Forrester Research, Inc.58625

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

“How did your company build its mobile site?”

Support for mobile development7-3

5%

5%

22%

25%

28%

Licensed a platform and built within-house resources

Outsourced to an interactive agency

Internally with our own developers

Outsourced to our eCommerce platform vendor

Opted for a mobile website service(e.g., UsableNet, Digby)

Base: 60 online retailers

Figure 8 Overall Mobile Presence

Source: Forrester Research, Inc.58625

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

“Which of the following best describe your mobile eCommerce?”

48%

44%

35%

15%

15%

13%

6%

5%

A special site optimized for mobile browsers

Nothing special; our site unoptimized

iPhone app

Android app

iPad

SMS

BlackBerry app

Third-party partnership (e.g., Cellfire)

Base: 62 online retailers

© 2011, Forrester Research, inc. Reproduction ProhibitedJune 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

14

Figure 9 Smartphones And Tablets Aim To drive Customers To Websites And Physical Stores

Source: Forrester Research, Inc.58625

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

“What are your company’s objectives for mobile?”

82%

63%

63%

62%

58%

54%

49%

49%

43%

37%

31%

28%

23%

14%

6%

87%

65%

65%

61%

57%

56%

46%

48%

41%

35%

22%

26%

19%

30%

6%

Drive revenue/sales to website

Improve customer satisfaction

Develop brand loyalty

Be a ready source of product andprice information for customers

Improve customer acquisition

Improve customer retention

Drive tra�c/sales in other channels(e.g., stores)

Keep up with competitors

Learn from and/or pilot mobile programs

Drive sign-ups/registrations

Location-based targeting

Real-time marketing

Drive 1:1 dialogue with customers

Provide store associates with toolsto improve selling

Reduce operations or marketing costs

SmartphonesTablets

Base: 65 online retailers

Objectives for smartphones and tablets9-1

© 2011, Forrester Research, inc. Reproduction Prohibited June 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

15

Figure 9 Smartphones And Tablets Aim To drive Customers To Websites And Physical Stores (Cont.)

Source: Forrester Research, Inc.58625

80%

75%

54%

32%

20%

20%

20%

14%

8%

Mobile site traffic

Revenue transacted directly via mobile devices

Average order value

Number of mobile app downloads

Product searches via mobile devices

Number of customers who have opted in for SMSalerts, coupons, daily deals, etc.

Repeat visits/logins

Mobile site/app satisfaction

Number of pickup alerts sent to mobile devices(e.g., for in-store pickup of orders placed online)

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester ResearchBase: 59 online retailers

Mobile key performance indicators9-2

“Which KPIs/metrics do you use to measure the success/progress of your mobile strategy and business?” (Select all that apply)

© 2011, Forrester Research, inc. Reproduction ProhibitedJune 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

16

Figure 9 Smartphones And Tablets Aim To drive Customers To Websites And Physical Stores (Cont.)

Source: Forrester Research, Inc.58625Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

Currently o�erPlan to o�er

“What kind of information and alerts does your company currently offer customers viaits mobile app/site?”

54%

42%

34%

27%

21%

21%

21%

18%

18%

16%

15%

14%

14%

10%

10%

8%

7%

7%

4%

4%

2%

2%

36%

26%

50%

38%

44%

43%

28%

18%

24%

44%

12%

36%

31%

25%

36%

24%

17%

9%

29%

24%

15%

2%

21%

Product information

Store information (e.g., hours, directions)

Customer ratings and reviews

Easy payment options

Alerts for online specials or sales

Coupons

Scanning a QR code

User manuals or other productinformation and instructions

Storing a shopping list

Shipping noti�cation

Price comparison information

In-store events

In-store product availability

Expert reviews

Checkout

The ability to access the loyalty programwhile shopping in a store

Alerts for in-store events, specials, or sales

Store maps/layouts

The ability to access gift registries forfriends and family members

2D bar code

Real-time coupons while customersare shopping in a store

In-store navigation (e.g., help�nding products in a store)

Sharing a shopping list

Base: 56 online retailers

Mobile features and functionality9-3

© 2011, Forrester Research, inc. Reproduction Prohibited June 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

17

Figure 10 Key Mobile Metrics

Source: Forrester Research, Inc.58625

Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research

Total Pure plays Multichannel ManufacturerTotal mobile investment $34,755 $6,818 $50,089 $24,583

Total tablet investment $14,628 $3,889 $23,269 $3,958

Planned investment in 2011 for mobile $220,893 $37,750 $343,068 $135,250

Planned investment in 2011 for tablets $144,054 $10,278 $185,625 $190,625

iPhone app costs $48,646 $10,000 $59,808 $56,667

iPad app cost $28,567 $7,692 $17,611 $68,750

Tra�c from mobile browsers 4% 4% 4% 5%

Tablet tra�c (as a percent of mobile) 21% 19% 24% 17%

Online revenue through mobile 2% 1% 2% 2%

Base: 57 online retailers

R E C O M M E n d A T i O n S

DOn’T BE SwEpT Up By THE HypE AROUnD SOciAl AnD EvEn MOBilE

While the data indicates that significant investments in social and mobile tactics will be in place this year, retailers are at risk for being disappointed with the results, given that these tactics still deliver modest sales at best to websites on average. in particular, retail executives should:

· Have modest expectations for social commerce benefits. in the history of retail, there has probably been nothing that has been so widely anticipated yet underwhelming as the “era of social commerce.” Retailers are sure to point to extensive programs around their social commerce initiatives — many more will point to their Facebook stores in the coming year as an example. Recognize, however, that these efforts do little to drive sales and that even in the best of circumstances, social tactics still rank behind other marketing tactics. Some select retailers (say manufacturers) may be in a better position to engage their brand advocates, but connecting sales (which may often happen offline) to this activity will be challenging for everyone.

· not neglect tried-and-true tactics like search and email. Retailer data indicates that some retailers may be de-emphasizing paid search in their marketing efforts. This could be a mistake as it continues to be the primary way in which consumers discover products and stores. Furthermore, there are significant opportunities to optimize search — few retailers are optimizing landing pages, adjusting keyword lists to dynamically accommodate for inventory fluctuations, or even adjusting copy on an as-needed basis. Even in the case of

© 2011, Forrester Research, inc. Reproduction ProhibitedJune 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

18

email, retailers still are continuing to batch and blast, particularly around the holidays when they need to customize their messages the most.

· Realize mobile matters more for some categories now than others. Mobile traffic has not taken significant share from overall PC/laptop-based web traffic to retail sites. However, retailers anecdotally report that some categories, particularly those with higher-ticket, higher-consideration goods are most vulnerable to the mobile influence, primarily because consumers price-compare in stores to ensure they are getting the best deal possible. While consumers may not be extensively exploring product information yet, basic store information, transparent pricing, and easy checkout capabilities are likely to be the most pressing opportunities for most sites in the near term. Multichannel retailers in particular should recognize that they need a twofold objective with their smartphone presences: enabling sales, but also serving store shoppers.

· Have different strategies for tablets and smartphones. While few retailers have expressed significant differences in their tablet and smartphone strategies, the two devices are extremely varied in their usage and benefits. To this end, retailers who view tablets as brand-building tools will be well served while retailers need to view their smartphone execution as one that needs to be extremely utilitarian. look to Forrester’s POST (people, objectives, strategy, technology) method as a framework to develop a defensible answer to whether a site requires a phone or tablet app or simply a mobile-optimized site experience. By distinguishing more clearly the specific business objectives for each device, retailers should be able to more clearly set development priorities, budgets, and metrics to evaluate the progress for each platform independently.

SUpplEMEnTAl MATERiAl

Methodology

The “State of Retailing Online” (SORO) annual survey is conducted by Forrester Research and executed in conjunction with Shop.org. Respondents include online retailers that transact with consumers by selling products via the Internet. The annual SORO survey is conducted in two waves. The first wave was fielded in March 2011 and included questions pertaining to online marketing and merchandising, social media budget and priorities, and mobile strategy and investment. The second wave will be conducted in June 2011.

For the first wave, we received 68 complete and partial responses across a variety of industries, including apparel, footwear, general merchandise, home furnishings, and personal care. In this report, web-based retailers generated the majority of their 2010 revenue through the online channel (including mobile), while store-based retailers generated the majority of their 2010 revenue through stores/wholesale. Fifty-three percent of participating companies were multichannel retailers, while 25% were web-based retailers and 22% manufacturers selling direct to consumer. Twenty-eight percent of the respondents generated more than $100 million in direct sales from their web channels in 2010, while 54% of respondents have been selling online for more than 10 years.

© 2011, Forrester Research, inc. Reproduction Prohibited June 3, 2011

The State Of Retailing Online 2011: Marketing, Social, And Mobile For eBusiness & Channel Strategy Professionals

19

EnDnOTES1 Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research.

2 Source: “The State of Retailing Online 2011,” a Shop.org study conducted by Forrester Research.

Forrester Research, Inc. (Nasdaq: FORR)

is an independent research company

that provides pragmatic and forward-

thinking advice to global leaders in

business and technology. Forrester

works with professionals in 19 key roles

at major companies providing

proprietary research, customer insight,

consulting, events, and peer-to-peer

executive programs. For more than 27

years, Forrester has been making IT,

marketing, and technology industry

leaders successful every day. For more

information, visit www.forrester.com.

Headquarters

Forrester Research, Inc.

400 Technology Square

Cambridge, MA 02139 USA

Tel: +1 617.613.6000

Fax: +1 617.613.5000

Email: [email protected]

Nasdaq symbol: FORR

www.forrester.com

M a k i n g l e a d e r s S u c c e s s f u l E v e r y d a y

58625

For information on hard-copy or electronic reprints, please contact Client Support

at +1 866.367.7378, +1 617.613.5730, or [email protected].

We offer quantity discounts and special pricing for academic and nonprofit institutions.

For a complete list of worldwide locationsvisit www.forrester.com/about.

Research and Sales Offices

Forrester has research centers and sales offices in more than 27 cities

internationally, including Amsterdam; Cambridge, Mass.; Dallas; Dubai;

Foster City, Calif.; Frankfurt; London; Madrid; Sydney; Tel Aviv; and Toronto.