july / august 2011 - experian plc - home · overview the experian ... •integrated into colombian...

TRANSCRIPT

July / August 2011

2

Overview

The Experian investment case

Aim to sustain mid-high single digit organic growth

Market leading global information company

Unique proprietary data, coupled with value-added analytics

Scalable business model

Strong market positions

No. 1 or 2 position across our largest markets

High barriers to entry

Global growth potential

By expanding geographically, in new customer segments and through innovation

Strong financial track record

High quality, recurring revenues

Highly cash generative with low capital intensity

3

Overview

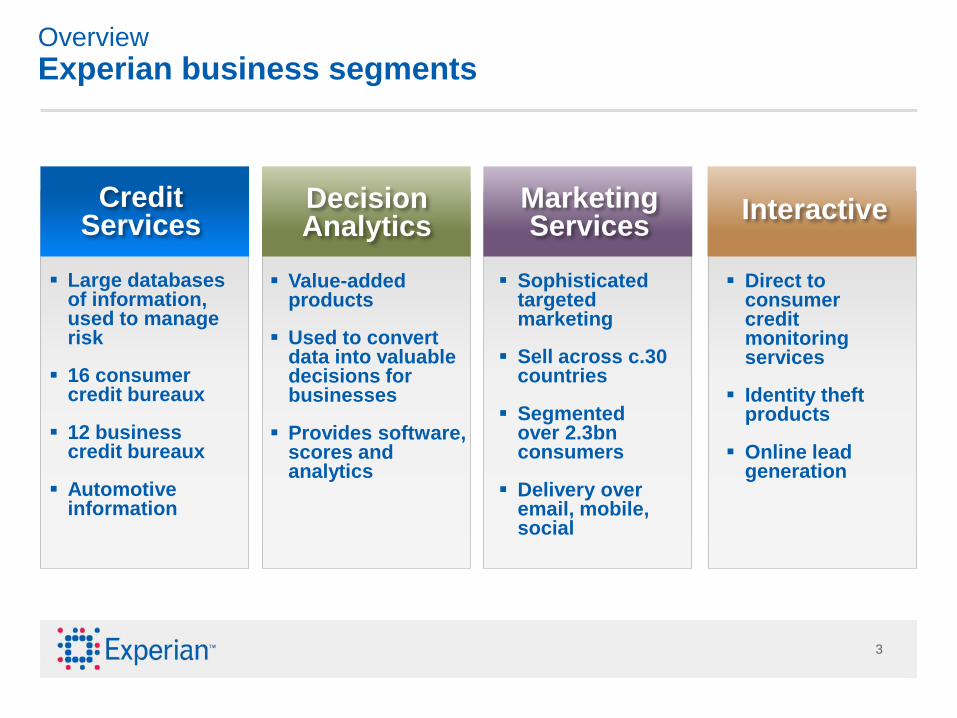

Experian business segments

Large databases of information, used to manage risk

16 consumer credit bureaux

12 business credit bureaux

Automotive information

Credit Services

Value-added products

Used to convert data into valuable decisions for businesses

Provides software, scores and analytics

Decision Analytics

Sophisticated targeted marketing

Sell across c.30 countries

Segmented over 2.3bn consumers

Delivery over email, mobile, social

Marketing Services

Direct to consumer credit monitoring services

Identity theft products

Online lead generation

Interactive

44Revenue for the year to 31 March 2011

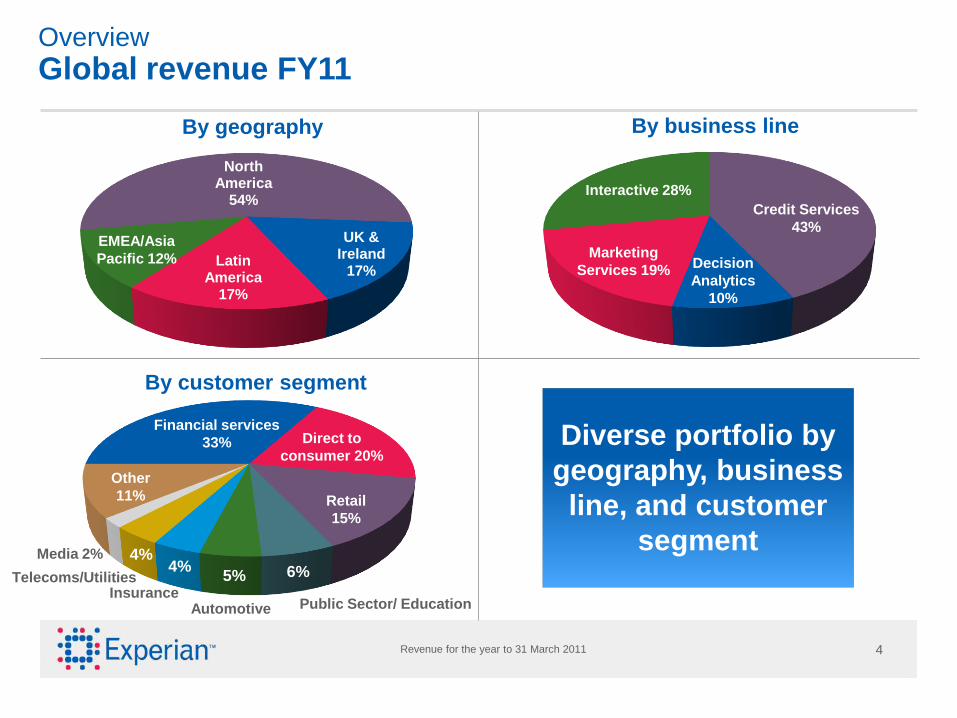

Overview

Global revenue FY11

Diverse portfolio by

geography, business

line, and customer

segment

By customer segment

Financial services

33% Direct to

consumer 20%

Retail

15%

Other

11%

Public Sector/ Education AutomotiveInsurance

Telecoms/Utilities

Media 2%

6%4%

4%5%

By business line

Credit Services

43%

Decision

Analytics

10%

Marketing

Services 19%

Interactive 28%

By geography

North America

54%

UK & Ireland

17%Latin

America 17%

EMEA/Asia

Pacific 12%

55*US onlySource: Latest full year revenue, company SEC filings

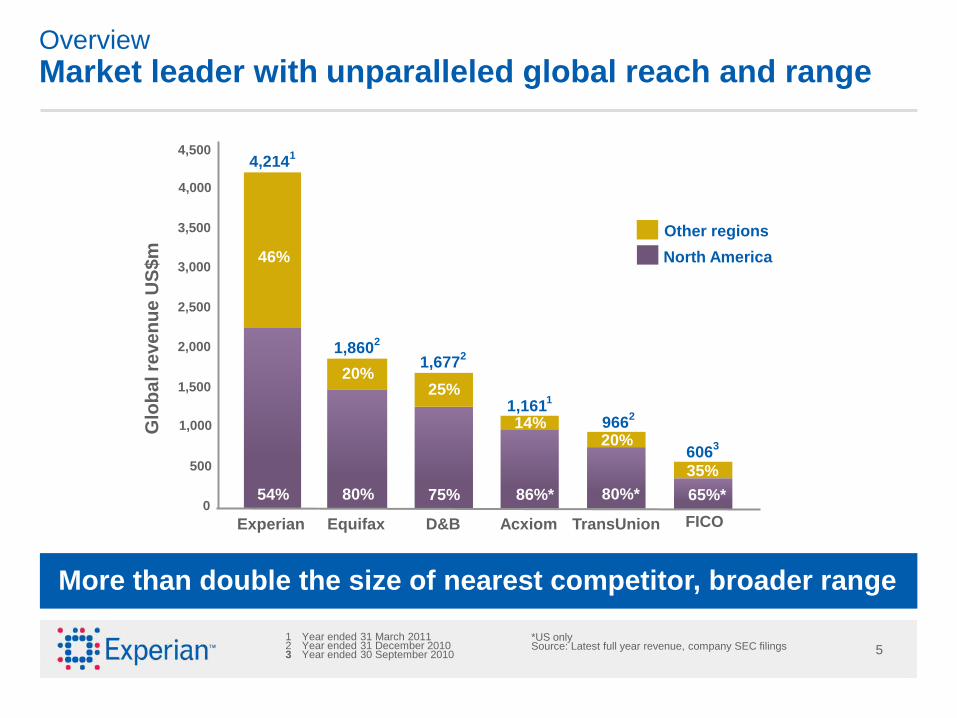

Overview

Market leader with unparalleled global reach and range

More than double the size of nearest competitor, broader range

1 Year ended 31 March 20112 Year ended 31 December 20103 Year ended 30 September 2010

55% 67%*

33%

77%*

23%

80% 86%*

14%

3,000

0

500

3,500

2,000

4,000

2,500

1,000

1,500

Glo

ba

l re

ve

nu

e U

S$

m

Other regions

North America

Experian Equifax

54%

46%

D&B Acxiom FICO

1,1611

6063

65%*

35%

75%

1,6772

25%

4,2141

80%

1,8602

20%

86%*

14% 9662

20%

80%*

TransUnion

4,500

66

Overview

Seven year revenue performance trend

Global continuing sales and EBIT only. EBIT margin excluding FARES. Operating cash conversion adjusted to exclude FARES. FY05 to FY10 EBIT adjusted to exclude FARES (discontinued operation). FY06 and FY07 sales and EBIT adjusted to exclude MetaReward. FY07 and FY08 sales and EBIT adjusted to exclude Loyalty Solutions. FY08 and FY09 sales and EBIT adjusted to exclude French Transaction Processing business and other smaller discontinuing activities. FY10 and FY11 sales and EBIT adjusted to exclude small discontinuing activities. Sales and EBIT growth shown at constant FX rates.

1,500

2,000

2,500

3,000

3,500

4,000

4,500

300

500

700

900

1,100

1,300

FY05 FY06 FY07 FY08 FY09 FY10 FY11

3,407

3,7123,790

3,803

4,214

747

15%

848

13%

896

8%

932

6%

1,046

11%Total

EBIT growth

Revenue US$m

EBIT

2,930

2,461

616

28%

490

17%

EBIT margin(direct business)

Operating cashconversion

Organic growth

21.9%

100%

8%14%

22.8%

99%

4%14%

23.6%

101%

3%8%

24.5%

100%

2%2%

24.8%

98%

8%10%Revenue growth

21.0%

102%

12%30%

20.0%

99%

9%18%

EBIT US$m

Financial

objectives:

Mid–high single

digit organic

revenue growth

Maintain or

improve margin

Convert at least

90% of EBIT into

operating cash

7

Overview

Major regional trends

North America• Gradual easing in credit

• More marketing of retail credit

• Some economic headwinds

• New regulations affecting some clients

• Shift to digital channels accelerates

Latin America

• Growth in credit demand

• Government action to contain inflation

• Strong structural underpinnings

UK & Ireland

• Banks still cautious; some signs of revival

• New banking entrants expand addressable market

• Some renewed investment in risk management platforms and value-added products

EMEA/Asia Pacific

• Rising credit penetration in emerging markets

• Growth in demand for targeted marketing

• Weak conditions in some established bureau markets

8

Overview

Organic revenue growth trends: Credit Services

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

FY10 H1 FY10 H2 FY11 H1 FY11 H2

North America

(8%)

(7%)

(6%)

(5%)

(4%)

(3%)

(2%)

(1%)

0%

FY10 H1 FY10 H2 FY11 H1 FY11 H2

UK & Ireland

(4%)

(3%)

(2%)

(1%)

0%

1%

2%

3%

4%

5%

6%

FY10 H1 FY10 H2 FY11 H1 FY11 H2

EMEA

0%

5%

10%

15%

20%

25%

FY10 H1 FY10 H2 FY11 H1 FY11 H2

Latin America

Credit Services Credit Services exc.

authentication

9

Strategic overview

Our global strategic objectives

Extend our global lead in credit information and analytics

Create successful businesses in new customer segments

Build large-scale operations in major emerging consumer economies

Become the global leader in digital marketing services

Become the most trusted consumer brand for credit information and identity protection services

10

Strategic overview

Delivering against our strategic metrics

2010 2011

27%

64%

>10% >10%

Year to 31 March

New customer segments

% of revenue from outside Financial Services

Innovation

New products as % of global revenue1

Expanding geographically

% of revenue from outside US & UK29%

67%

1 % of global revenue developed within past five years

30-40%

>65%

>10%

2014

1111

Strategic overview

Global growth programme: key initiatives

• North America business information products

• Next-generation bureau

• New Decision Analytics platform

• New Marketing Services platforms

• Consumer protection products

• Credit bureaux:

• Colombia

• India

• Australia

• Positive data

• Marketing Services product roll-out

• Consumer Direct roll-out

• SME

• Healthcare payments

• Insurance

• Public sector

• Telecommunications

• Utilities

Product innovation Expanding geographically New customer segments

1212

Strategic overview

Progress: global growth programme

Prioritising to deliver maximum returns

• Initiatives contributed 2% to organic revenue growth in FY11

• Largest contributors were:

• Fraud and identity management

• Consumer protection

• Telecoms and utilities segments

• Small and medium enterprise segment

Focus on data and analytics

Drive profitable growth

Optimise capital

efficiency

1313

Strategic overview

New bureau expansion: Colombia

• Definitive agreement to acquire majority stake in Computec

• Market leading bureau in Colombia, with smaller bureau operations in Peru and Venezuela

• Computec is a unique asset:

• c. 60% share in consumer credit bureau

• High brand recognition

• Most extensive consumer credit data in Colombia

• Integrated into Colombian banking sector

• Financially strong

• Aim to leverage Experian global expertise

1414

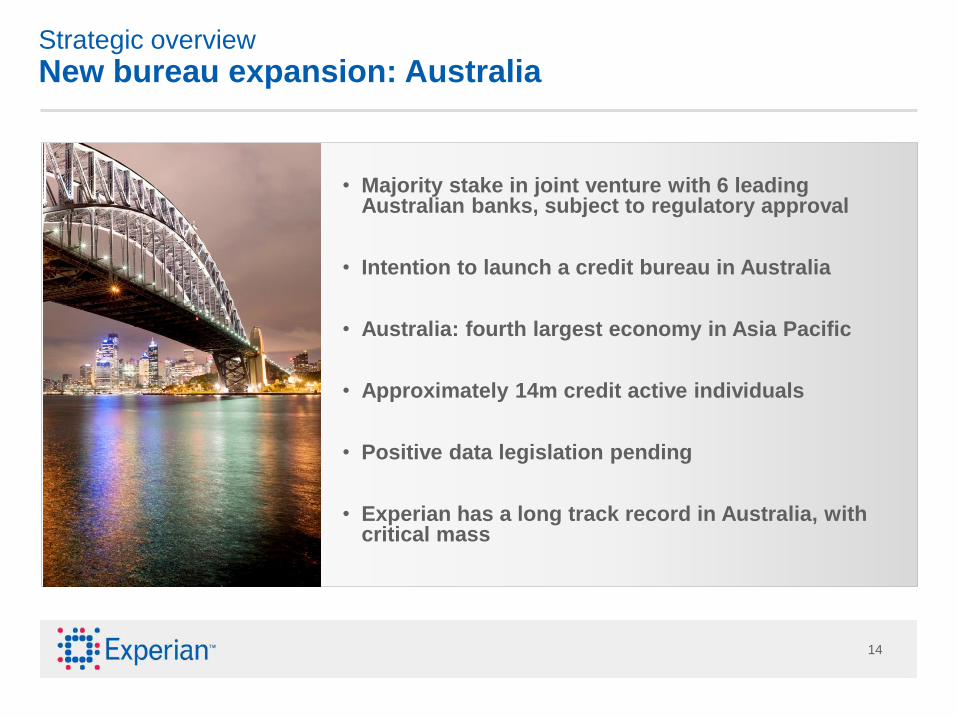

Strategic overview

New bureau expansion: Australia

• Majority stake in joint venture with 6 leading Australian banks, subject to regulatory approval

• Intention to launch a credit bureau in Australia

• Australia: fourth largest economy in Asia Pacific

• Approximately 14m credit active individuals

• Positive data legislation pending

• Experian has a long track record in Australia, with critical mass

1515

Strategic overview

North America business information

• North America market is over US$1bn

• Market dominated by one operator

• Large SME opportunity

• Global customers seeking access to US business information data

• Over 3,000 clients using BusinessIQ, with growing pipeline

• Corporate linkage launched, good client response

• Consumer data linkage in beta phase

• Positioned well for recovery in small business lending

Drivers and trends Experian progress

1616

Strategic overview

Global Marketing Services

• Global leadership in email delivery

• New social media capability through Techlightenment acquisition

• New mobile delivery capabilities

• Digital advertising services

• Traction with ISPs

• New client wins

Expanding delivery platforms

New digital segmentation

services

• Strengthened leadership

• Investment in innovation

• Uniting under a common brand

Operational focus to strengthen market

proposition

1717

Strategic overview

Global technology platforms

• Investing in best-in-class technology to support revenue growth

• Projects we’re implementing:

• Value-added products platform

• Next generation bureau platform

• New Decision Analytics architecture

• New Marketing Services platforms

Sophisticated technology + data quality + service excellence = client value

1818

Financial overview

Capital expenditure

Capex uplift reflects:

• Growing scale of the business

• Investment in technology and new products to drive growth

• Expect capex/revenue of c. 9%

• Convert at least 90% of EBIT to operating cash

DatabasesTechnologySoftware

0

50

100

150

200

250

300

350

400

450

500

FY10 FY11 FY12 forecast

US$m

1919

Financial overview

Net debt/EBITDA

1 Valuation at 31 March 2011

Net debt Serasa put option Net debt to EBITDA

US$bn Net debt to

EBITDA

Target net debt to EBITDA range

FY11 net debt/EBITDA towards lower end of range

Serasa put option value US$870m1

Pro forma FY11 net debt/EBITDA of c. 2x including Computec

Share purchases in FY12 for vesting employee plans only

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

FY08 FY09 FY10 FY11

2020

Financial overview

Financial summary and outlook

6% organic revenue growth in Q1

FY12 outlook:

Expect Q2 similar to Q1

Mid–high single digit organic revenue growth for FY12

Modest margin improvement

Strong cash conversion

2121

Summary

Strong progress all round

= Sustained growth

Global growth programme

Investment

Scale

+

+

2222

This slide has been left intentionally blank

Appendix

24

All figures above on continuing basis Growth at constant exchange rates2010 restated to exclude FARES (now classified as a discontinued operation) and small discontinuing activities in UK & Ireland and EMEA/AP

7%

8%

Year ended 31 MarchUS$million

Total growth

2011 2010Revenue

North America

UK and Ireland

EMEA/Asia Pacific

Total revenue

2,254

736

502

4,214

9%

3%

12%

10%

7%

2%

2,060

730

454

3,803

EBIT – continuing activities 1,046 11%932

EBIT margin 24.8% 24.5%

Latin America 722 19% 19%559

Central activities (66) (62)

EBIT before central activities 1,112 10%994

Appendix

Revenue and EBIT by geography

7%

6%

2%

4%

19%

Organic growth

FY11 Q1 FY12

25

Appendix

Group benchmark earnings

Growth at actual exchange rates. 2010 restated to exclude FARES which is now classified as a discontinued operation.1 Benchmark PBT is defined as profit before amortisation of acquisition intangibles, acquisition expenses, goodwill impairments, charges in respect of the demerger-related equity incentive plans, exceptional items, financing fair value remeasurements and tax. It includes the Group’s share of associates’ pre-tax profit.

2011 2010 Growth

(45)(52)Benchmark non-controlling interest

(162)(220)Benchmark taxation

692753Benchmark PAT

14%854973Benchmark PBT1

8%647701Benchmark earnings

12%9351,044Total EBIT

(81)(71)Net Interest

Dividend per share, US cents

Benchmark EPS, US cents

28.0

70.0 63.7

23.0

10%

22%

Year ended 31 MarchUS$million

1,002 1,015Weighted average number of shares

989 1,015Closing number of shares

19.0%22.6%Benchmark taxation rate

26

Appendix

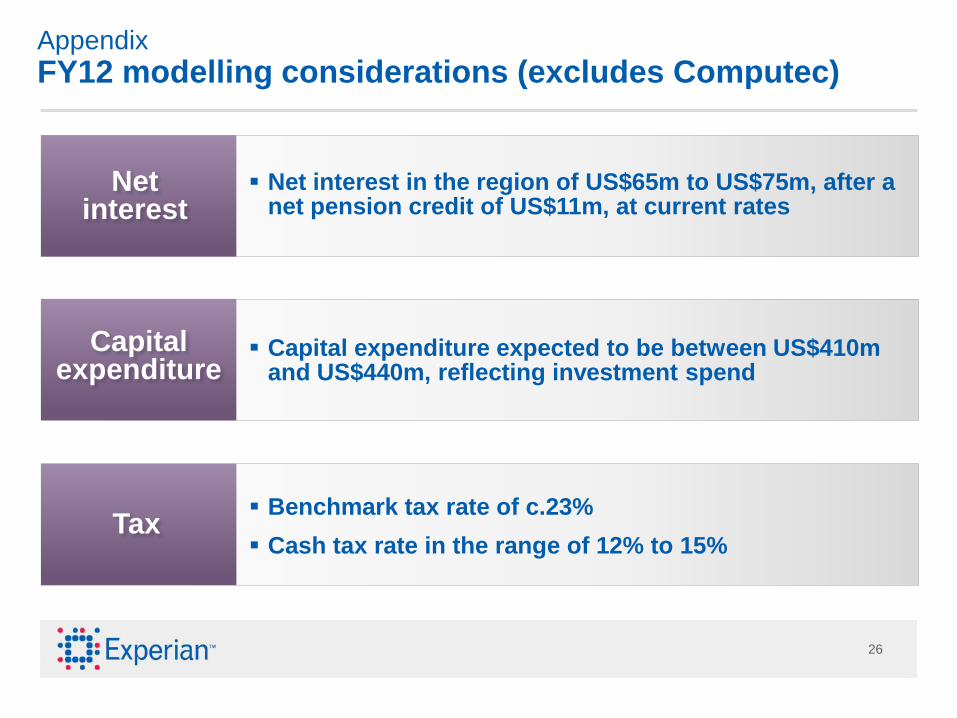

FY12 modelling considerations (excludes Computec)

Netinterest

Net interest in the region of US$65m to US$75m, after a net pension credit of US$11m, at current rates

Capital expenditure

Capital expenditure expected to be between US$410m and US$440m, reflecting investment spend

Tax Benchmark tax rate of c.23%

Cash tax rate in the range of 12% to 15%

27

Appendix

Cash flow performance

Depreciation and

amortisation

Free cash flow

Operating cash flow

EBIT

Capital expenditure

(374)

1,044

288

Working capital

3

Retained in associate

55

1,028

98% conversion of EBIT into

operating cash flow

Net interest

(92)

Tax

(88)

Dividends to minority interests

(56)

792

Sale of fixed

assets

113% conversion of benchmark

earnings into free cash flow

Year ended 31 March 2011

US$million

12

28

Appendix

Credit Services: our business and market influences

Market

influences

Our

business

• We build and manage large databases of credit

application and payment histories of consumers and

businesses

• We help clients manage the risks associated with

lending money so they can:

• decide who to lend to

• set appropriate lending limits

• take action on overdue accounts

• Competition between lenders for new customers

• Need to monitor risk in lending portfolios

• Growth in demand in new customer segments

• Growth in credit active population in emerging markets

29All figures above on continuing basisGrowth at constant exchange rates

716

225

184

1,812

3%

(2)%

(1)%

7%

609

33.6%

687

3%

(2)%

(1)%

7%

7%

18% 18%

693

234

190

1,655

555

33.5%

538

Year ended 31 MarchUS$million

Total growth

2011 2010Revenue

North America

UK and Ireland

EMEA/Asia Pacific

Total revenue

Latin America

EBIT

EBIT margin

Appendix

Credit Services: 43% of group revenue

3%

9%

4%

(2)%

18%

Q1 FY12

Organic growth

FY11

30

Appendix

Decision Analytics: our business and market influences

Market

influences

Our

business

• Need for sophisticated prospecting and risk

management tools

• Standardisation by lenders to create single customer

experience

• Growth in demand for fraud prevention and

authentication tools

• Client willingness to invest in large software platforms

• We provide software, scores and analytics to financial

services clients

• We help clients at all stages of the lending cycle to:

• identify new customers

• segment existing customers

• manage loan portfolios and optimise collections

• We provide detection and fraud prevention services

31

Year ended 31 MarchUS$million

Total growth

2011 2010Revenue

North America

UK and Ireland

EMEA/Asia Pacific

Total revenue

Latin America

All figures above on continuing basisGrowth at constant exchange rates2010 restated to exclude a small discontinuing activity in UK & Ireland

9%

2%

116

9%

4%

(3)%

175

125

423

2%

(3)%

7 60% 60%

8%111

26.2%

175

135

435

113

12

118

27.1%

EBIT

EBIT margin

Appendix

Decision Analytics: 10% of group revenue

(10)%

6%

13%

9%

119%

Q1 FY12

Organic growth

FY11

4%

32

Appendix

Marketing Services: our business and market influences

Market

influences

Our

business

• Spending by retailers on marketing in US & UK

• Strong growth in emerging markets

• Secular shift from traditional to digital advertising

• Growing demand for intelligent solutions

• Growth in demand for global services

• We own unique data on consumer attributes

• We use sophisticated marketing strategies to help

organisations identify, understand, target and engage

their best customers through:

• unrivalled data on consumers

• systems, analytics & platforms that puts data to work

• ability to help clients understand and measure

effectiveness of campaigns

33

EBIT

EBIT margin

Year ended 31 MarchUS$million

Total growth

2011 2010Revenue

North America

UK and Ireland

EMEA/Asia Pacific

Total revenue

Latin America

All figures above on continuing basis Growth at constant exchange rates2010 restated to exclude small discontinuing activities in UK & Ireland, EMEA and Asia Pacific

329367

218

183

791

11%

4%

31%

14%

11%

3%

17%

11%

212

139

694

126

15.9%

47%86

12.4%

23 58% 58%14

Appendix

Marketing Services: 19% of group revenue

24%

10%

10%

1%

1%

Q1 FY12

Organic growth

FY11

34

Appendix

Interactive: our business and market influences

Market

influences

Our

business

• Rising awareness of uses of credit information

and benefits of credit monitoring

• Growth in personal identity theft

• We provide online services directly to consumers via

subscription, including:

• access to their detailed credit history

• access to their credit scores

• credit monitoring for identity protection purposes

• Our online lead generation services help businesses

target offers to consumers e.g. loans or insurance

• We provide online comparison shopping services

35

EBIT

EBIT margin

Year ended 31 MarchUS$million

Total growth

2011 2010Revenue

North America

UK and Ireland

Total revenue

All figures above on continuing basis Growth at constant exchange rates

1,058

118

15%

10%

14%

8%

10%

922

109

1,031

259

22.0%

6%242

23.5%

1,176 9%

Appendix

Interactive: 28% of group revenue

Q1 FY12Organic growthFY11

(4)%

15%

(2)%

36

Appendix

Experian American Depositary Receipt (ADR) program

Experian ADR shares trade on the OTCQX under the

following information:

Symbol EXPGY

CUSIP 30215C101

Ratio 1 ADR : 1 ORD

Country United Kingdom

Effective Date October 11, 2006

Underlying SEDOL B19NLV4

Underlying ISIN GB00B19NLV48

U.S. ISIN US30215C1018

Depositary BNY Mellon

For ADR shareholder enquiries, please contact:

Shareholder Relations

Bank of New York Mellon

PO Box 358516

Pittsburgh

PA 15252 - 8516

United States

T: + 1 201 680 6825 (From the US: 1-888-BNY-ADRS, toll free)

W: www.adrbnymellon.com

37

Experian

Cardinal Place

80 Victoria Street

London

SW1E 5JL

Tel: +44 (0)203 042 4200

Website: www.experianplc.com

Paul Brooks Nadia Ridout-Jamieson

Chief Financial Officer Director of Investor Relations

Email: [email protected] Email: [email protected]

Peg Smith Sarah Schibli

Executive Vice-President Investor Relations Analyst

Email: [email protected] Email: [email protected]

Contacts

38

20 July 2011 Annual General Meeting

10 November 2011 Half-yearly results announcement

17 January 2012 Interim management statement, third quarter

10 May 2012 Prelims announcement, full year

Event calendar

39

This presentation is being made only to, and is only directed at, persons to whom this presentation may lawfully be communicated (“relevant persons”). Any person who is not a relevant person should not act or rely on this presentation or any of its contents.

Information in this presentation relating to the price at which relevant investments have been bought or sold in the past or the yield on such investments cannot be relied upon as a guide to the future performance of such investments.

This presentation does not constitute or form part of, and should not be construed as, an offering of securities or otherwise constitute an invitation, inducement or recommendation to any person to underwrite, subscribe for or otherwise acquire securities in any company within the Experian group (the “Group”).

Certain statements made in this presentation are forward looking statements. Such statements are based on current expectations and are subject to a number of risks and uncertainties that could cause actual events or results to differ materially from any expected future events or results expressed or implied in these forward-looking statements. Forward-looking statements speak only as of the date of this presentation.

This presentation contains certain non-GAAP financial information. The Group’s management believes that these measures provide valuable additional information in understanding the performance of the Group or the Group’s businesses because they provide measures used by the Group to assess performance. Although these measures are important in the management of the business, they should not be viewed as replacements for, but rather as complementary to, the GAAP measures.

Disclaimer