john mulhall miicm; lib international credit & process management professional

TRANSCRIPT

Training Day Document

Process Workflow Management International

Accounts PayableJohn Mulhall MIICM; LIB

International Credit & Process Management Professional

AgendaBusiness Process Management & AP Positioning

Characteristics of policy and good process management workflows

Regulation – “SOX” V “Best Business Practice”

Internal Controls & Compensating Controls

VAT Processing

Operational AP Workflows

Processing Efficiency Manual V System based

Applied Workflow – AP Best Practice

Summary

Business Process Management

Business Process Management aka “BPM” is the process of aligning the business processes of a company with its wants and needs.

Functional BPM e.g. Creditor Payment Process & Cross (AP) Functional BPM e.g. Contra Payments Process (AR/AP).

Integration is key to connect processes as a “structure”. They must be functional, compatible and effective as a single process and as a group of processes

Process management with SOX’s “COSO” process model ensuring every process has controls embedded in the workflow managing financial risk in an effective and auditable manner at a process, functional and strategic level.

COSO Framework [SOX]

LAYERED CONTROL

BPM INTEGRITY

BPM EFFECTIVENESS

CONTROLS INTEGRITY

CONTROLS EFFECTIVENESS

RISKS COVERED

OPS/FINANCE/COMPLIANCE

FINANCIAL/NON FINANCIAL

KEY/ NON KEY

COVERS ALL AREAS

For Discussion: Are all business processes “good” for the company?

“The Titanic” knew on its maiden voyage that there was iceberg’s on the route in the northern passage which was nicknamed “iceberg alley”. Of the 3 processes deployed to counter icebergs;

The process that should have worked? The rope needed to duck a bucket into the sea to test the seawater temperature was too short, so with no controls inserted into the process, the hourly test results were falsified using onboard tap water which failed one of the processes to counter icebergs and the ship sailed full steam into “iceberg alley” without slowing down like it should have if the water temperature tests had returned an ”iceberg likely” result.

The process that kind of worked? The crows nest housed able seamen to physically spot and call “iceberg” but the able seamen were never given binoculars they needed to effectively execute the watch process from the crows nest. The unrelenting social class structure kicked in and the process of Officers never giving “their” privileges away meant they didn’t give the able Seamen their binoculars to use in the Watch process. The process of class enforcement worked preventing the transfer of tools to the watch process partially failing the effectiveness of the process on watch by reducing the spotting ranges by miles.

The process that did work? There was a process for launching lifeboats in the event of a sinking. The number of boats needed was 16 by law and the Titanic reduced the 40+ boats in the original design to 20 boats with not enough time to train the crew properly in their deployment process. The Process worked from a compliance perspective but failed to achieve the goal of launching enough boats to save all hands.

The Result “ ICEBERG!!!.. DEAD AHEAD!!!.... 1 partially working process hindered by a dysfunctional interactive process gave notice too little too late to avoid the collusion that sunk the Titanic.

Organisational Positioning

Chief Executive Officer (CEO)

Chief Finance Officer (CFO)

Accounting

General Ledger

Internal

Audit

FP&A

Commercial Finance

Accounts Receivabl

e Accounts Payable

Chief Operating Officer (COO)

Operations

Quality Assurance

Manufacturing

R&D

Sales & Marketing

Customer Service

Supply

Chain

Procurement

Logistics

HR

Board Directors

Audit Committee

Good AP Policy / Workflow Characteristics

Policy must be “Efficient, Accurate, Controllable, Audit/SOX Compliant, Integrated & Cost Effective”

Process Workflows are designed toProcess Invoices accurately and efficiently in a policy compliant manner

Process Payments accurately and efficiently in a policy compliant manner

Accurately and efficiently execute controls at a transactional, account and ledger level in a meaningful, auditable and value creating manner throughout the monthly and quarterly cycle

Ensure operator accuracy levels are at their best through use of controls both manual and systems based on a transactional level

Ensure operator efficiency/productivity levels are at their best through use of technology as a productivity aid

Guard against the risk of financial loss through defined workflow controls and segregation of duties in the procure 2 pay workflow chain

AP Workflow Characteristics

Always have a start, middle and end

Can be verified as accurate in a controllable and auditable manner

Are transactional (day to day processing) and functional based (weekly, monthly, quarterly control and reports)

Are synergy friendly allowing for internal synergies (standardization of invoice processing process allowing cross coverage and workload reallocation when necessary)

And external synergies… (good supplier service, integrated correctly into the procure 2 pay chain so purchasing activities can result in a payment in a timely manner)

They must effectively cover the services an AP department provides which are usually in the areas of Trade Creditors, Travel & Expense, Intercompany and Capital Projects

AP Workflow Policy

Requirements Compliance is required especially in the areas of control that workflows provide (approval limits/signatory compliance/query management/disbursement authorizations/filing and document storage/controls like creditors reconciliations)

Efficiency is required to meet or exceed Service Level Agreement aka SLA’s requirements which are often embedded in policy. These lead to metrics such as invoices loaded per day, week and month by Specialist, accuracy rate, payments returned number by Specialist, late payments rate per week and month, query to resolution ratio per month.

Workflows should also be detailed and liner in design leading to easier reporting and analysis which creates value for the function and business.

“SOX” V “Best Business Practice”

The Sarbanes Oxley Act 2002 a.k.a. “SOX” or Public Company Accounting Reform and Investor Protection Act is an act designed to ensure good governance along with accurate and transparent financial reporting of Public Limited companies in the United States and any associated foreign subsidiaries or “virtual interests”. (Investopedia)

We “have” to…

“Best Business Practice” is a method or technique that has consistently shown results superior to those achieved with other means, and that is used as a benchmark. (Wikipedia)

We “need’ to…

Internal Controls V Compensating Controls

“Its all connected”Internal Controls - Methods put in place by a company to ensure the integrity of financial and accounting information, meet operational and profitability targets and transmit management policies throughout the organization. (Investopedia)

Compensating Controls - The management, operational, and technical controls (i.e., safeguards or countermeasures) employed by an organization in lieu of the recommended controls in the low, moderate, or high security control baselines, that provide equivalent or comparable protection for an information system. (Expertglossary.com)

VAT ProcessingInter Community VAT Processing rules are more aligned given recent changes to VAT at EU level

Goods & Services follow more “aligned” rules allowing for VAT Rate on country of origin of goods and/or services to be charged.

There are scheduled exceptions which have to be explained on the invoice if zero rated. Note reverse charge VAT requires vendor VAT number on invoice.

VAT splits should be processed by VAT breakout split or by line and not by invoice (e.g. German companies require all invoices to be loaded by VAT rate/split, then by line, then by invoice)

Non EU invoices directly to us are exempt (separate customs duties/taxes)

EU invoices exempt for VAT must be explained

If you are not sure about an invoices VAT processing rules, ask!!. Bias errors in processing VAT lead to large fines by the Revenue Commissioners and further costs in remediation of the errors in processing

Irish VAT Summary 2013 – A Good Read!!... http://www.taxworld.ie/taxes/vat/current/summary

Workflow – Purchase Order Invoice 2 Payment

Cycle

Workflow – AP Payables Process

P1 - Invoice(s) confirmed via ERP/Manually that they are cleared for payment via 2 way receipting/3 way receipting/4 way receipting/signature approval & cost code. Cleared Invoices must also be due for payment at the time of the payment run to be included in the run.

P2 - Invoice register is ran and prepared with invoice proofs attached (Quality Control for Audit).

P 3 - Invoice register with invoice/claim proofs brought to signature authority/management figure whom audits the register and invoices for company policy compliance (AP Team Leader/Manager/Controller) and signs it off.

P4 - Payment batch is ran and exported to bank

P 5 - Approved Batch is brought to the management figure for review of approval proof and releases the payment. Payment release confirmation is stored as proof of payment with the payment register.

P 6 - All documents are stored safely in a retrievable manner in line with company policy and all regulatory requirements on document storage (Safe Harbor, Data Protection Act, etc.)

Workflow – AP Payables “Charted”

P1 – Invoices/Claims Vetted

P2 – Payment

Register Ran

P3 - Invoice Register &

Proofs Audited/Appr

oved for Payment

P4 – Payment

exported to the bank

P5 – Approved Payment register

released at bank

P6 – All documents stored in a safe and

compliant manner

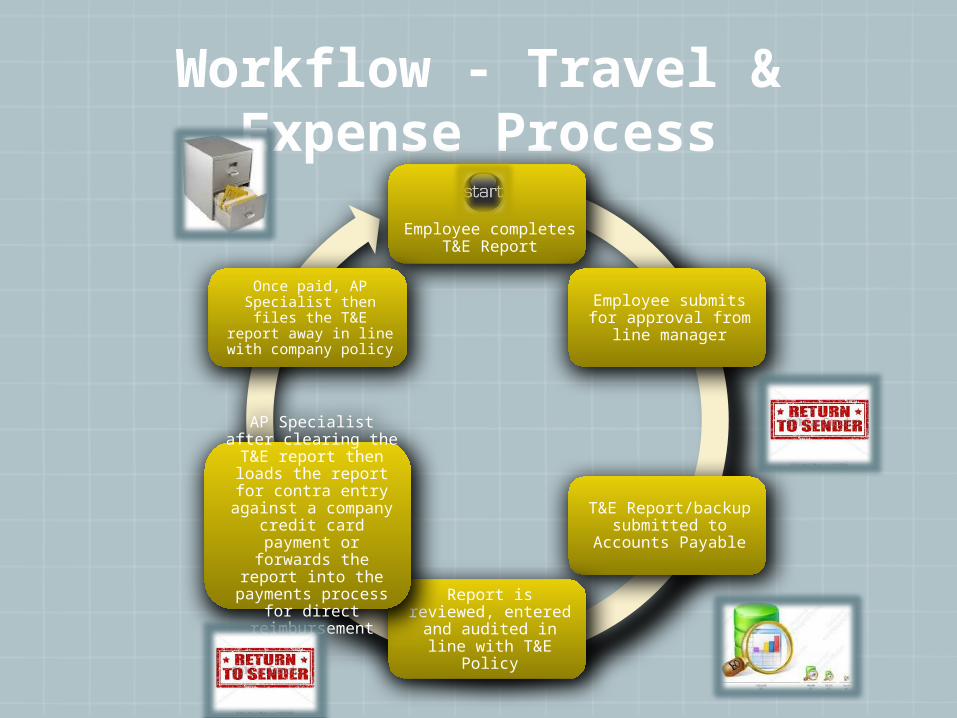

Workflow - Travel & Expense Process

Employee completes T&E Report

Employee submits for approval from line

manager

T&E Report/backup submitted to

Accounts Payable

Report is reviewed, entered and audited

in line with T&E Policy

AP Specialist after clearing the T&E

report then loads the report for contra entry

against a company credit card payment

or forwards the report into the payments process for direct reimbursement

Once paid, AP Specialist then files the T&E

report away in line with company policy

Workflow - Vendor Account Set Up

New Vendor Account Set up Form

[Procurement] Regulatory, Risk & Financial Appraisal/

Product Lines & Discount tree approved

Form completed by procurement and

approved

Form sent to Accounts Payable to be approved

Form sent to Budget Manager to be

approved

Account Set up, details stored in line with company policy

Workflow - Month End Pyramid AP

Creditors Ledger Report & Analysis

Accruals/Prepayments Calculation &

Analysis

Creditors, Cash/Bank &

Inventory (PO)Reconciliation

Management Analysis & KPI

Reporting

Process Efficiency Manual V System Based

Manual Based – Labour Intensive, easier to adjust, better responsiveness to flaws in process, higher error rate, lower process efficiency in based AP processes

Systems Based – Capital intensive, harder to adjust, poor responsiveness to flaws in process (change controls, etc.), lower error rate, higher process efficiency

What’s good for business???...

New Business Opportunities??

With Systems based invoice and payments processing you have options;

More expert AP Staff in a centralised AP team with higher AP processing efficiency and accuracy rates along with more “bandwidth” for new tasks

Take on more entities/processing work especially in a centralised AP model

Identify purchasing & payment trending along with supplier analysis such as identifying opportunities for cost synergies and savings on purchasing (especially in centralised AP environment).

AP staff could also carry out compensating controls over procurement on purchase 2 pay overruns/PO policy violations (repeats/extensions/etc) and dual PO invoice clearance reporting

Feed into business intelligence activities based around supplier risk

Better subject matter expertise to develop better and more effective system solutions for procure 2 pay with a centralised AP team

Better efficiency in AP ERP deployments with a centralised AP Team

Applied Workflow – AP Query Process

Invoice Query Detected/Receiv

ed

Log Completed and assigned

party contacted for resolution

Assigned party followed up

weekly

Query deadline expiring which

triggers escalation to AP

Leader & Resolver

Leader/Manager

Monthly Control report produced for Management on open queries

and their resolution to

overall aged AP Creditors

The Query Control Log “Good Data Capture leads to good actions and ends in good

results”Query Ref Vendor Number Vendor Name AP Ledger

Query Reporter Name – Customer

Query Reporter Contact Number

Query Classification

Query Type PO Ref Inv Ref Receipting Ref Invoice Due Date

Details

Assigned To

Assignee Department Assigned Date Due Date

Can you think of any more fields a good query control log should have?

Applied Workflow – AP Non PO Invoice

Purchase Invoice

Receive/ Recorded

by AP

Sent to Approver

for Approval

Approver approves or queries

invoice

Invoice on query log

or returned

for payment

Invoice forwarded

to Payments Process

Applied Workflow - Interest Based

Negotiation in disputes

Assertive mirroring tone

Calm and articulate in

expressing AP issues on the

dispute

Understanding the interests of the

counterparty and finding a win win

solution

Agreeing ways forward that engage the

counterparty interests and

acting on them

SummaryA Good AP Specialist is an expert in attention to detail, the procure to pay chain and a subject matter expert in AP Business Process Management

Good AP is truly understanding the part AP plays in the company’s organisation and it crucial role in company supply chain and liquidity

AP’s workflow discipline and effectiveness are the primary factor for existing given its organisational role and positioning

AP’s future development will only add value to the company if workflow discipline and accuracy is unrelentingly high over time. These are the foundation stones for AP, and critical to the core operational integrity of Finance, Supply Chain and Operations. Without AP, a company’s effective structures would crack and crumble over time

Be professional, be accurate, be understanding and be consistent time and time again!!

Thank you for your time…

JOHN MULHALL MIICM; LIB

ie.linkedin.com/pub/john-mulhall-miicm-lib/5a/98a/516/