jefferson international academy financial statements together with independent ...€¦ · ·...

TRANSCRIPT

JEFFERSON INTERNATIONAL ACADEMY

FINANCIAL STATEMENTS

TOGETHER WITH INDEPENDENT AUDITORS’ REPORT

JUNE 30, 2014

JEFFERSON INTERNATIONAL ACADEMY FINANCIAL STATEMENTS

JUNE 30, 2014

TABLE OF CONTENTS

Page(s)

Independent Auditors’ Report on Financial Statements 1-2 Management’s Discussion and Analysis 3-9 Basic Financial Statements Academy-wide Financial Statements: Statement of Net Position 10 Statement of Activities 11 Fund Financial Statements Governmental Funds: Balance Sheet 12 Statement of Revenues, Expenditures and Changes in Fund Balances – Governmental Funds 13 Reconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balances of Governmental Funds to the Statement of Activities 14 Required Supplemental Information Budgetary Comparison Schedule – General Fund 15 Budgetary Comparison Schedule – School Service Fund 16 Notes to Financial Statements 17-22 Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters 23-24

INDEPENDENT AUDITORS’ REPORT ON FINANCIAL STATEMENTS To the Board of Directors Jefferson International Academy We have audited the accompanying financial statements of the governmental activities, each major fund, and the aggregate remaining fund information of Jefferson International Academy as of and for the year ended June 30, 2014, and the related notes to the financial statements, which collectively comprise the Academy’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial State ments

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, each major fund, and the aggregate remaining fund information of Jefferson International Academy as of June 30, 2014, and the respective changes in financial position for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis and budgetary comparison information on pages 3-9 and 15-16 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

GREGORY TERRELL & COMPANY Certified Public Accountants

September 22, 2014

2

JEFFERSON INTERNATIONAL ACADEMY MANAGEMENT’S DISCUSSION AND ANALYSIS

AS OF JUNE 30, 2014 Management Discussion and Analysis is intended to be the Jefferson International Academy (the “Academy”) Management’s discussion and analysis of the financial results for the year ended June 30, 2014. The intent of this discussion and analysis is to provide a look at the Academy’s performance and current position. Readers should also review the notes to the financial statements and financial statements to enhance their understanding of the Academy’s financial performance. Using the Annual Report This annual report consists of a series of financial statements and notes to those statements. The statements are organized so the reader can understand the Academy as a whole (academy-wide statements), and then proceed to provide an increasingly detailed look at specific financial statements (fund financial statements). Also included are various notes to the financial statements. The audit also contains supplemental information in addition to the basic financial statements. Reporting on the Academy as a Whole – Academy-Wide Financial Statements One of the most important questions asked about the Academy’s finances is, “Is the Academy better off or worse off as a result of the year’s activities?” The Statement of Net Position and the Statement of Activities report information about the Academy as a whole and about its activities in a manner to help address this question. These statements include all assets and liabilities of the Academy using the accrual basis of accounting similar to the accounting used by the private sector. All of the current year’s revenues and expenditures are taken into consideration regardless of when cash is received or paid. The two statements report the Academy’s net position and any changes in them. The change in net position provides the reader a tool to assist in determining whether the Academy’s financial health is improving or deteriorating. The reader will need to consider other non-financial factors such as state aid foundation grant, political conditions on a State level, student enrollment growth, quality of local service, and facility improvements prior to arriving at any conclusion regarding the overall health of the Academy. Reporting the Academy’s Most Significant Funds - Fu nd Financial Statements The fund financial statements provide detailed information about the most significant funds, not the Academy as a whole. Some funds are required to be established by state law and by debt covenants. However, the Academy establishes many other funds to help it control and manage money for a particular purpose (the Food Services and Athletic Funds are examples) or to show that it is meeting legal responsibilities for using grant and other money. The governmental funds of the Academy use the following accounting approach: Governmental Funds - Most of the Academy’s activities are reported in the governmental funds, which focus on how money flows into and out of those funds and the balances left at year end that are available for future periods. These funds are reported using an accounting method called modified accrual accounting, which measures cash and other financial assets that can be converted to cash. The governmental fund statements provide a detailed short term view of the Academy’s general operations and the basic services it provides. Governmental fund information helps you determine whether there are more or less financial resources available to spend in the near future to finance the Academy’s programs. The relationship (or differences) between governmental funds is reconciled in the basic financial statements.

3

JEFFERSON INTERNATIONAL ACADEMY MANAGEMENT’S DISCUSSION AND ANALYSIS

AS OF JUNE 30, 2014

The Academy as a Whole Table 1 provides a summary of the Academy’s net position as of June 30, 2014:

GovernmentalActivities

June 30, 2014

Assets

Current Assets 271,378$

Capital Assets 25,830

Total Assets 297,208$

Liabilities Current and Other Liabilities 268,988$

Net Position

Investment in Capital Assets 25,830$

Unrestricted 2,390

Total Net Position 28,220$

4

JEFFERSON INTERNATIONAL ACADEMY MANAGEMENT’S DISCUSSION AND ANALYSIS

AS OF JUNE 30, 2014

The results of this year’s operations for the Academy as a whole are represented in a Statement of Activities, Table 2, that shows the changes in net position for the fiscal year 2014.

GovernmentalActivities

June 30, 2014

Revenue Program Revenue:

Federal Grants and Entitlements 78,389$

General Revenue

State Foundation Allowance 756,923

Miscellaneous Revenue 51,906

Total Revenue 887,218$

Functions/Program Expenditures

Instruction 339,679$

Support Services 426,118

Food Services 54,360

Central Services 35,970

Unallocated Depreciation 2,871

Total Functions/Programs Expenditures 858,998$

Increase in Net Position 28,220$

Capital Assets At June 30, 2014 , the Academy had an investment in capital assets, net accumulated depreciation of $25,830. This includes furniture and equipment.

5

JEFFERSON INTERNATIONAL ACADEMY MANAGEMENT’S DISCUSSION AND ANALYSIS

AS OF JUNE 30, 2014 General Fund Budget Highlights During the first year of operation the Academy's student population grew from 66 students on the first day of school to 79 by the end of the school year. This growth in student body allowed the Academy to continue its mission to provide a challenging and differentiated learning experience to children in the Northern Oakland County area. This was partially accomplished through a technological based curriculum, with computers and smart board technology in every classroom.

To carry out our mission, our budget must remain lean placing all available funds into the class-rooms to benefit the learning experience for the children. We believe we met our goals for the 2013-2014 school-year by delivering a quality educational experience to the students and completed the year with an operating surplus $2,390. The Academy will continue to aim high to ensure a quality education for all students. Over the course of the year, the Academy revises its budget as it attempts to deal with unexpected changes in revenues, expenditures and shortfall in student count. State law requires that the budget is amended to ensure that expenditures do not exceed appropriations. A schedule showing the Academy’s original and final budget amounts compared with amounts actually paid and received is provided as part of the required supplemental information of these financial statements.

6

JEFFERSON INTERNATIONAL ACADEMY MANAGEMENT’S DISCUSSION AND ANALYSIS

AS OF JUNE 30, 2014 Student outcomes are based on actual student academic growth made during the 2013/2014 school

year as measured by NWEA Measures of Academic Progress Tests RIT* scores. The following data

shows yearly progress towards meeting our projected academic goals.

Student Outcomes

RIT* Mean

Fall 2013

RIT* Mean

Spring 2014 RIT* Growth Progress

Kindergarten

Reading 139.0 152.3 + 13.3

First Grade

Reading 154.0 172.1 + 18.1

Second Grade

Reading 158.7 177.3 + 18.6

Third Grade

Reading 165.2 181.3 + 16.1

Fourth Grade

Reading 191.3 199.6 + 8.3

Fifth Grade

Reading

188.8 186.8 - 2

* RIT stands for Rasch UnIT which is an equal interval measurement scale used by NWEA to measure student

achievement and growth. It was developed to simplify the interpretation of test scores and makes it possible to follow a

student’s educational growth from year to year.

7

JEFFERSON INTERNATIONAL ACADEMY MANAGEMENT’S DISCUSSION AND ANALYSIS

AS OF JUNE 30, 2014 Student outcomes are based on actual student academic growth made during the 2013/2014 school

year as measured by NWEA Measures of Academic Progress Tests RIT* scores. The following data

shows yearly progress towards meeting our projected academic goals.

Student Outcomes

RIT* Mean

Fall 2013

RIT* Mean

Spring 2014

RIT*

Growth Progress

Kindergarten

Math 133.7 151.3 + 17.6

First Grade

Math 151.5 172.4 + 20.9

Second Grade

Math 163.2 181.2 + 18.0

Third Grade

Math 173.8 186.9 + 13.1

Fourth Grade

Math 187.8 203.1 + 15.3

Fifth Grade

Math 191.2 201.8 + 10.6

* RIT stands for Rasch UnIT which is an equal interval measurement scale used by NWEA to measure student

achievement and growth. It was developed to simplify the interpretation of test scores and makes it possible to follow a

student’s educational growth from year to year.

8

JEFFERSON INTERNATIONAL ACADEMY MANAGEMENT’S DISCUSSION AND ANALYSIS

AS OF JUNE 30, 2014 Economic Factors and Next Year’s Budgets and Rates The Academy’s administration and Board of Directors (“the Board”) consider many factors in the budget process. One of the most important factors affecting the budget is student enrollment. The state foundation revenue is determined by multiplying the blended student count by the foundation allowance per pupil. Approximately 85 percent of total General Fund revenue is from the foundation allowance. As a result, the Academy funding is heavily dependent on the State’s ability to fund local school operations. Once the final student count and related per pupil funding is validated, state law requires the Academy to amend the budget if actual Academy resources are not sufficient to fund original appropriations. Under State Law, the Academy cannot assess property taxes to fund general operations. As a result, the Academy revenue heavily depended on State funding and the health of the State’s School Aid Fund, the actual revenue received depends on the State’s ability to collect revenues to fund its appropriation to school districts. The state periodically holds a revenue estimating conference to forecast revenues. This financial report is intended to provide our taxpayers, parents, and investors with a general overview of the Academy’s finances and their accountability for the money it receives. If you have questions about this report or need additional information, we welcome you to contact the business office (248) 682-5000 at 60 S. Lynn Ave., Waterford, MI 48328.

9

JEFFERSON INTERNATIONAL ACADEMY STATEMENT OF NET POSITION

JUNE 30, 2014

Governmental Activities

Assets

Cash and Cash Equivalents 57,101$

Due from Other Governmental Units 114,289

Accounts Receivable 94,511

Prepaid Expense 5,477

Capital Assets, Net of Depreciation 25,830

Total Assets 297,208$

Liabilities

Accounts Payable 157,896$

Accrued Expenditures 5,223

Unearned Revenue 105,869

Total Liabilities 268,988$

Net Position

Investment in Fixed Assets 25,830$

Unrestricted 2,390

Total Net Position 28,220$

The accompanying notes are an integral part of this financial statement.

10

JEFFERSON INTERNATIONAL ACADEMY STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2014

Functions/Programs Expenses Charges for

Services Operating

Grants

Governmental Net Revenues

(Expenses) and Change in

Net Position

Governmental Activities:

Instruction 339,679$ -$ -$ (339,679)$

Support Services 462,088 - 30,766 (431,322)

Food Services 54,360 - 47,623 (6,737)

Unallocated Depreciation 2,871 - - (2,871)

Total Governmental Activities: 858,998$ -$ 78,389$ (780,609)$

General Revenues:

State of Michigan School Aid Unrestricted 756,923$

Miscellaneous Revenue 51,906

Total General Revenues 808,829$

Change in Net Position 28,220$

Net Position, Beginning of Year -

Net Position, End of Year 28,220$

The accompanying notes are an integral part of this financial statement.

11

JEFFERSON INTERNATIONAL ACADEMY BALANCE SHEET

GOVERNMENTAL FUNDS JUNE 30, 2014

General Fund

OtherNonmajor

Governmental Funds

Total Governmental

FundsASSETS

Assets

Cash and Cash Equivalents 57,101$ -$ 57,101$

Due from Other Governmental Units 114,289 - 114,289

Accounts Receivable 94,511 - 94,511

Prepaid Expense 5,477 - 5,477

Due from Other Funds - 12,845 12,845

Total Assets 271,378$ 12,845$ 284,223$

LIABILITIES AND FUND BALANCES

Liabilities

Accounts Payable 145,051$ 12,845$ 157,896$ Accrued Expenditures 5,223 - 5,223 Due to Other Funds 12,845 - 12,845

Unearned Revenue 105,869 - 105,869

Total Liabilities 268,988$ 12,845$ 281,833$

Fund Balances

Non-spendable 5,477$ -$ 5,477$

Unassigned (3,087) - (3,087)

Total Fund Balances 2,390$ -$ 2,390$

Total Liabilities and Fund Balances 271,378$ 12,845$ 284,223$

Total Governmental Fund Balances 2,390$

Amounts reported for governmental activities in the Statement of Net Position

that are different because:

Capital assets used in governmental activities are not financial resources and

therefore are not reported in the funds.

The cost of the capital assets is 28,701$

Accumulated depreciation is (2,871) 25,830

Total Net Position of Governmental Activities 28,220$

The accompanying notes are an integral part of this financial statement.

12

JEFFERSON INTERNATIONAL ACADEMY STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN

FUND BALANCES GOVERNMENTAL FUNDS

FOR THE YEAR ENDED JUNE 30, 2014

GeneralFund

Other Nonmajor

Governmental Funds

Total Governmental

Funds

REVENUES:

Local Sources 51,906$ -$ 51,906$

State Sources 756,923 - 756,923

Federal Sources 30,766 47,623 78,389

Total Revenues 839,595$ 47,623$ 887,218$

EXPENDITURES:

Instruction:

Basic Programs 282,648$ -$ 282,648$

Added Needs 60,030 - 60,030

Total Instruction 342,678$ -$ 342,678$

Support Services:

Pupil Services 11,199$ -$ 11,199$

Instructional Staff 1,933 - 1,933

General Administration 52,046 - 52,046

School Administration 152,629 - 152,629

Business Service 1,617 - 1,617

Operations and Maintenance 175,143 - 175,143

Transportation 77,819 - 77,819

Central Support Services 15,204 - 15,204

Community Services 200 - 200

Total Support Services 487,790$ -$ 487,790$

Food Services -$ 54,360$ 54,360$

Total Expenditures 830,468$ 54,360$ 884,828$

Excess (Deficiency) of Revenues over Expenditures 9,127$ (6,737)$ 2,390$

OTHER FINANCING SOURCES (USES):

Operating Transfers In -$ 6,737$ 6,737$

Operating Transfers Out (6,737) - (6,737)

NET CHANGE IN FUND BALANCES 2,390$ -$ 2,390$

Beginning of Year - - -

End of Year 2,390$ -$ 2,390$

The accompanying notes are an integral part of this financial statement.

13

JEFFERSON INTERNATIONAL ACADEMY RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES AND

CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2014

Net Change in Fund Balances - Governmental Funds 2,390$

Amounts reported for governmental activities in the Statement of Activities that are different:

Governmental funds report capital outlays as expenditures in the statement of activities

These costs are allocated over their estimated useful lives as depreciation:

Capital Outlay 28,701

Depreciation Expense (2,871)

Change in Net Position - Governmental Activities 28,220$

The accompanying notes are an integral part of this financial statement. 14

JEFFERSON INTERNATIONAL ACADEMY

REQUIRED SUPPLEMENTAL INFORMATION BUDGETARY COMPARISON SCHEDULE

GENERAL FUND FOR THE YEAR ENDED JUNE 30, 2014

Original Final Actual

Amounts

VarianceUnder/ (Over)Final Budget

REVENUES:

Local Sources -$ 53,000$ 51,906$ 1,094$

State Sources 896,480 838,984 756,923 82,061

Federal Sources - 26,425 30,766 (4,341)

Total Revenues 896,480$ 918,409$ 839,595$ 78,814$

EXPENDITURES:

Instruction:

Basic Programs 240,269$ 278,081$ 282,648$ (4,567)$

Added Needs 50,594 53,610 60,030 (6,420)

Total Instruction 290,863$ 331,691$ 342,678$ (10,987)$

Support Services:

Pupil Services 58,275$ 11,235$ 11,199$ 36$

Instructional Staff 9,900 1,933 1,933 -

General Administration 123,982 51,612 52,046 (434)

School Administration 142,211 154,620 152,629 1,991

Business Service 940 1,608 1,617 (9)

Operations and Maintenance 219,728 173,317 175,143 (1,826)

Transportation - 74,558 77,819 (3,261)

Central Support Services 23,032 25,030 15,204 9,826

Community Services - 300 200 100

Total Support Services 578,068$ 494,213$ 487,790$ 6,423$

Total Expenditures 868,931$ 825,904$ 830,468$ (4,564)$

Excess (Deficiency) of Revenues over Expenditures 27,549$ 92,505$ 9,127$ 83,378$

OTHER FINANCING SOURCES (USES):

Operating Transfers In (Out) (20,000)$ (7,628)$ (6,737) (891)$

NET CHANGE IN FUND BALANCE 7,549$ 84,877$ 2,390$ (82,487)$

Beginning of Year - - - -

End of Year 7,549$ 84,877$ 2,390$ (82,487)$

Budgeted Amounts

The accompanying notes are an integral part of this financial schedule.

15

JEFFERSON INTERNATIONAL ACADEMY REQUIRED SUPPLEMENTAL INFORMATION

BUDGETARY COMPARISON SCHEDULE SCHOOL SERVICE FUND

FOR THE YEAR ENDED JUNE 30, 2014

Original Final Actual

Amounts

VarianceUnder/ (Over)Final Budget

REVENUES:

Local Sources -$ -$ -$ -$

Federal Sources 33,000 48,422 47,623 799

Total Revenues 33,000$ 48,422$ 47,623$ 799$

EXPENDITURES:Food Services 52,700$ 51,451$ 54,360$ (2,909)$

Total Expenditures 52,700$ 51,451$ 54,360$ (2,909)$

Excess (Deficiency) of Revenues over Expenditures (19,700)$ (3,029)$ (6,737)$ 3,708$

OTHER FINANCING SOURCES (USES):

Operating Transfers In (Out) 20,000$ 3,628$ 6,737$ (3,109)$

NET CHANGE IN FUND BALANCE 300$ 599$ -$ 599$

Beginning of Year - - - -

End of Year 300$ 599$ -$ 599 $

Budgeted Amounts

The accompanying notes are an integral part of this financial schedule.

16

JEFFERSON INTERNATIONAL ACADEMY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

(1) ORGANIZATION Jefferson International Academy (‘the Academy”) is a Public School Academy (K-5). The State of Michigan has delegated to Central Michigan University the responsibility of authorizing the establishment of public school academies. Central Michigan University approved the establishment of Jefferson International Academy pursuant to the Michigan School Code of 1976 (“Code”), as amended.

(2) ACADEMY-WIDE AND FUND FINANCIAL STATEMENTS The academy-wide financial statements (i.e., the statement of net position and the statement of activities) report information on all of the non-fiduciary activities of the Academy. For the most part, the effect of inter-fund activity has been removed from these statements. All of the Academy’s activities are classified as governmental activities. The statement of activities, demonstrates the degree to which the direct expenses of a given function or segment are offset by program revenues. Direct expenses are those that are clearly identifiable with a specific function or segment. Program revenues include: 1) charges to customers who purchase, use or directly benefit from goods or services by a given function or segment and 2) grants and contributions that are restricted to meeting the operational or capital requirements of a particular function or segment. State Foundation Aid and other unrestricted items are not included as program revenues but instead as general revenues. Measurement focus, basis of accounting, and financi al statement presentation The academy-wide financial statements are reported using the economic resources measurement focus and the accrual basis of accounting. Revenues are recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows. Grants and similar items are recognized as revenue as soon as all eligibility requirements imposed by the provider have been met. As a general rule, the effect of interfund activity has been eliminated from the Academy-wide financial statements. Amounts reported as program revenue include (1) charges to customers or applicants for goods, services, or privileges provided; (2) operating grants and contributions; and (3) capital grants and contributions. Internally dedicated resources are reported as general revenue rather than as program revenue. Likewise, general revenue includes all unrestricted state aid.

17

JEFFERSON INTERNATIONAL ACADEMY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 (Continued)

(2) ACADEMY-WIDE AND FUND FINANCIAL STATEMENTS (Cont’d) Governmental fund financial statements are reported using the current financial resources, measurement focus and the modified accrual basis of accounting. Revenues are considered to be available when they are collectible within the current period or soon enough thereafter to pay liabilities of the current period. For this purpose the Academy considers revenues to be available if they are collected within 60 days of the end of the current fiscal period. Expenditures generally are recorded when a liability is incurred, as under accrual accounting. However, debt service expenditures, as well as expenditures related to compensated absences and claims and judgments, are recorded only when payment is due.

State and federal aid and interest associated with the current fiscal period are all considered to be susceptible to accrual and so have been recognized as revenues of the current fiscal period. All other revenue items are considered to be measurable and available only when cash is received by the Academy. The Academy reports the following major governmental funds:

The general fund is the Academy’s primary operating fund. It accounts for all financial resources of the Academy, except those required to be accounted for in another fund.

The Academy reports the following non-major governmental funds: The school service fund is the Academy’s primary non-major fund. It is used to account for food services operations. It is a subsidiary operation and obligation of the general fund.

(3) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The financial statements have been prepared in accordance with the accounting principles outlined in the Michigan School Accounting Manual. The significant accounting policies followed by Jefferson International Academy (the “Academy”) are described below: Cash and Cash Equivalents Cash and cash equivalents include short-term, highly liquid investments that are readily convertible to cash. Revenue Recognition All grant and contract revenues are recognized only to the extent earned.

18

JEFFERSON INTERNATIONAL ACADEMY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 (Continued)

(3) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont’d) Use of Estimates The preparation of general purpose financial statement in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reported period. Actual results could differ from those estimates.

Budgets and Budgetary Accounts The General Fund budget was adopted on a basis consistent with accounting principles generally accepted in the United States of America and in compliance with the Uniform Budgeting and Accounting (P.A. 621 of 1978). A separate School Service Fund budget was adopted. For the year end June 30, 2014, all expenditures exceeded appropriations by less than 10%. Capital Assets Capital assets purchased or acquired are capitalized at historical cost or estimated historical cost. Donated fixed assets are valued at their estimated fair market value on the date received. The cost of normal maintenance and repairs that do not add to the value of the asset or materially extend asset lives are not capitalized. Improvements are capitalized and depreciated over the remaining useful lives of the related fixed assets. Depreciation on all assets is provided on the straight-line basis over the estimated useful lives as follows: Furniture and equipment 10 years

19

JEFFERSON INTERNATIONAL ACADEMY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 (Continued)

(3) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont’d) Deferred Outflows and Inflows of Resources Effective July 1, 2013, the Academy implemented the provisions of Governmental Accounting Standards Board Statements No. 63 and 65. Deferred Outflows of Resources are defined as the consumption or usage of net assets applicable to a future reporting period. These types of resources are similar to assets and have a positive effect on the Statement of Net Position. Deferred Inflows of Resources are defined as the acquisition of net assets applicable to a future reporting period. These types of resources are similar to liabilities and have a negative effect on the Statement of Net Position.

(4) CASH AND CASH EQUIVALENTS

The Academy’s deposits are included on the balance sheet under the following classifications: Cash and cash equivalents $57,101 State law authorizes the Academy to make deposits in the accounts of federally insured financial institutions. Cash held by fiscal agents or trustees is secured in accordance with the requirements of the agency or trust agreement. Custodial Credit Risk of Bank Deposits Custodial credit risk is the risk that in the event of bank failure, the Academy’s deposits may not be returned by the bank. The Academy believes that due to the dollar amounts of cash deposits and the limits of FDIC insurance, it is impractical to insure all bank deposits. As a result, the Academy evaluates each financial institution it deposits Academy funds with and assesses the level of risk of each financial institution; only those institutions with an acceptable estimated risk level are used as depositories. The above deposits were reflected in the accounts of the bank (without recognition of checks written but not yet cleared or of deposits in transit) at $88,220. This amount was covered by federal depository insurance.

20

JEFFERSON INTERNATIONAL ACADEMY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 (Continued)

(5) DUE FROM OTHER GOVERNMENTAL UNITS

Due from other governmental units as of June 30, 2014 for the Academy’s general fund and school service fund were as follows:

State of Michigan - State Aid 109,709$ State of Michigan - Federal Grants 4,580

Total due from other governmental units 114,289$

(6) CAPITAL ASSETS

A summary of capital assets is presented below:

July 1, 2013 Additions Retirements June 30, 2014

Furniture and equipment -$ 28,701 -$ 28,701$ Less: accumulated depreciation - (2,871) - (2,871)

Net capital assets -$ 25,830$ -$ 25,830$

Depreciation for fiscal year ended June 30, 2014 amounted to $630. The Academy determined that it was impractical to allocate depreciation to the various Academy activities as the assets serve multiple functions.

(7) MANAGEMENT AGREEMENT

For the year ended June 30, 2014, the Academy utilized a management company, The Hanley-Harper Group, Inc., a for profit corporation. The Hanley-Harper Group, Inc. provides all Academy personnel, as well as all Academy management and curriculum services. The Hanley-Harper Group, Inc. is reimbursed for its direct costs as approved in the Academy’s budget. Management fee is based on the Academy’s state aid and certain federal revenue sources and was set at 0% of the for the period July 1, 2013 through June 30, 2014; 10% for the period July 1, 2014 through June 30, 2015; and 13% for the period July 1, 2015 through June 30, 2018. The management agreement provides for a minimum management fee of $51,000 and a maximum management fee of $400,000. There was no management fee for the year ended June 30, 2014.

21

JEFFERSON INTERNATIONAL ACADEMY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 (Continued)

(8) OPERATING LEASE COMMITMENTS

The Academy leases classrooms and office space from the Archdiocese pf Detroit under an operating lease. The lease requires regular monthly payments of one-twelfth of 10% of State Aid plus $1,667 per month commencing July 2014 until June 30, 2017. Lease payments totaled $22,248 for the year ended June 30, 2014. The Academy is operating under a lease agreement for a copier. The lease expense was $3,072 for the year ended June 30, 2014. Payments of $256 are due monthly. Minimum future lease payments are as follows:

2015 3,072$ 2016 3,072

Total 6,144$

(9) UNEARNED REVENUE

At June 30, 2014, the Academy received governmental funds prior to meeting all eligibility requirements. Governmental funds are reported as unavailable revenue when receivables are considered to be unavailable to liquidate liabilities of the current period. Governmental funds are unearned when resources have been received but not yet earned. The components of deferred outflows and inflows of resources are as follows:

Unavailable Unearned

Grants and categorical aid payments received prior to meeting all egilibility requirements -$ 105,869$

Total Unearned Revenue -$ 105,869$

(11) SUBSEQUENT EVENTS

In August, 2014, the Academy entered into an Agreement with the Michigan Finance Authority for a State Aid Note in the amount of $170,000. The Note is guaranteed by the Academy’s State Aid payments. Subsequent events have been evaluated through September 22, 2014, which is the date the financial statements were available to be issued. Events occurring after that date have not been evaluated to determine whether a change in the financial statements would be required.

22

22

INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL OV ER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF

FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

To the Board of Directors Jefferson International Academy

We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of the governmental activities, each major fund, and the aggregate remaining fund information of Jefferson International Academy, as of and for the year ended June 30, 2014, and the related notes to the financial statements, which collectively comprise Jefferson International Academy’s basic financial statements, and have issued our report thereon dated September 22, 2014.

Internal Control Over Financial Reporting

In planning and performing our audit of the financial statements, we considered Jefferson International Academy’s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of Jefferson International Academy’s internal control. Accordingly, we do not express an opinion on the effectiveness of Jefferson International Academy’s internal control.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance.

Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or, significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

23

Compliance and Other Matters

As part of obtaining reasonable assurance about whether Jefferson International Academy’s financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the entity’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

GREGORY TERRELL & COMPANY Certified Public Accountants September 22, 2014

24

Report to the Board of Directors

September 22, 2014

JEFFERSON INTERNATIONAL ACADEMY

1

Audit Overview

• Responsibilities under U.S. Generally Accepted Auditing Standards

– We have audited the financial statements in accordance with auditing standardsgenerally accepted in the United States of America for the year ended June 30,2014.

– Our objective was to obtain reasonable, but not absolute, assurance about

whether these financial statements were free from material misstatement.

2

• Planned Scope and Timing of the Audit

– The scope of our audit was substantially described in our engagement letter datedMay 5, 2014, and was communicated in the planning meeting held on August 12,2014.

– We have issued an unmodified opinion on the June 30, 2014 financial statements.

– Audit results were reviewed with Jefferson International Academy Management.

Audit Overview(continued)

• Significant Audit Findings

– Qualitative Aspects of Accounting Practices

• We noted no transactions entered into by Jefferson International Academy

during the year for which there is a lack of authoritative guidance or

consensus.

– Difficulties Encountered in Performing the Audit

• We encountered no significant difficulties in dealing with management in

3

• We encountered no significant difficulties in dealing with management in

performing and completing our audit.

– Corrected and Uncorrected Misstatements

• Professional standards require us to accumulate all known and likely

misstatements identified during the audit, other than those that are clearly

trivial, and communicate them to the appropriate level of management.

Management has corrected all such misstatements. In addition, none of the

misstatements detected as a result of audit procedures and corrected by

management were material, either individually or in the aggregate, to the

financial statements taken as a whole.

Audit Overview(continued)

• Significant Audit Findings (continued)

– Disagreements with Management

• We are pleased to report there were no disagreements with managementregarding financial accounting, reporting or auditing matters that aroseduring the course of our audit.

– Management Representations

• Management has been requested to provide us with certain representations

4

• Management has been requested to provide us with certain representationsin a letter dated September XX, 2014.

– Management Consultations with Other Independent Accountants

• Management may decide to consult with other accountants about auditingand accounting matters, similar to obtaining a “second opinion” on certainsituations. To our knowledge, there were no such consultations with otheraccountants.

Audit Overview(continued)

• Significant Audit Findings (continued)

– Other Audit Findings or Issues

• We generally discuss a variety of matters, including the application ofaccounting principles and auditing standards, with management each yearprior to retention as the Academy’s auditors. However, these discussionsoccurred in the normal course of our professional relationship and ourresponses were not a condition to our retention.

5

• This information is intended solely for the use of the Board of Directors and management of Jefferson International Academy, and is notintended for and should not be used by anyone other than these specified parties.

Summary of Assets

General Fund

2014$57,101 , 21%

$94,511 , 35%

$5,477 , 2%

6

Total = $271,378

$114,289 , 42%

Cash and Cash Equivalents Due from Other Govermental Funds Accounts Receivable Prepaids

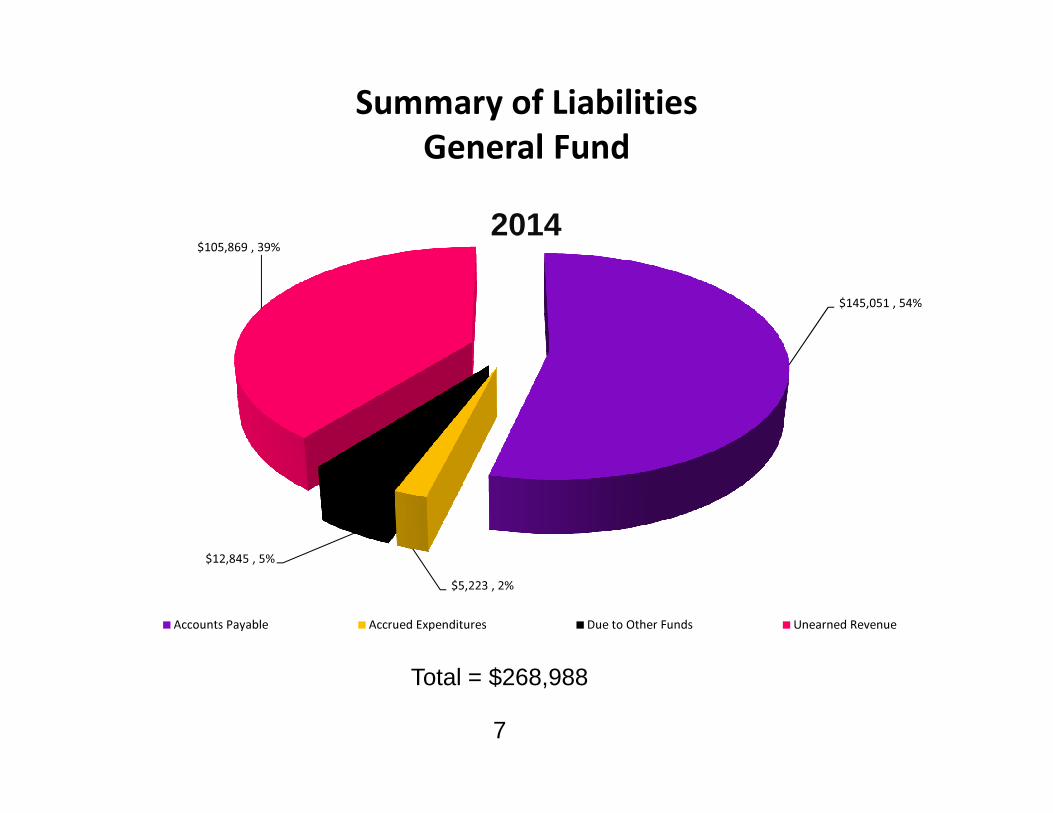

Summary of Liabilities

General Fund

2014

$145,051 , 54%

$105,869 , 39%

7

Total = $268,988

$5,223 , 2%

$12,845 , 5%

Accounts Payable Accrued Expenditures Due to Other Funds Unearned Revenue

Summary of Fund Balances

General Fund

2014

$2,000

$4,000

$6,000

$5,477

$2,390

8

Total = $2,390

$(4,000)

$(2,000)

$-

$2,000

$(3,087)

Non-Spendable Unassigned Total

Summary of Revenue

General Fund

2014

$51,906 , 6%

$30,766 , 4%

9

Total = $839,595

$756,923 , 90%

Local Sources State Sources Federal Sources

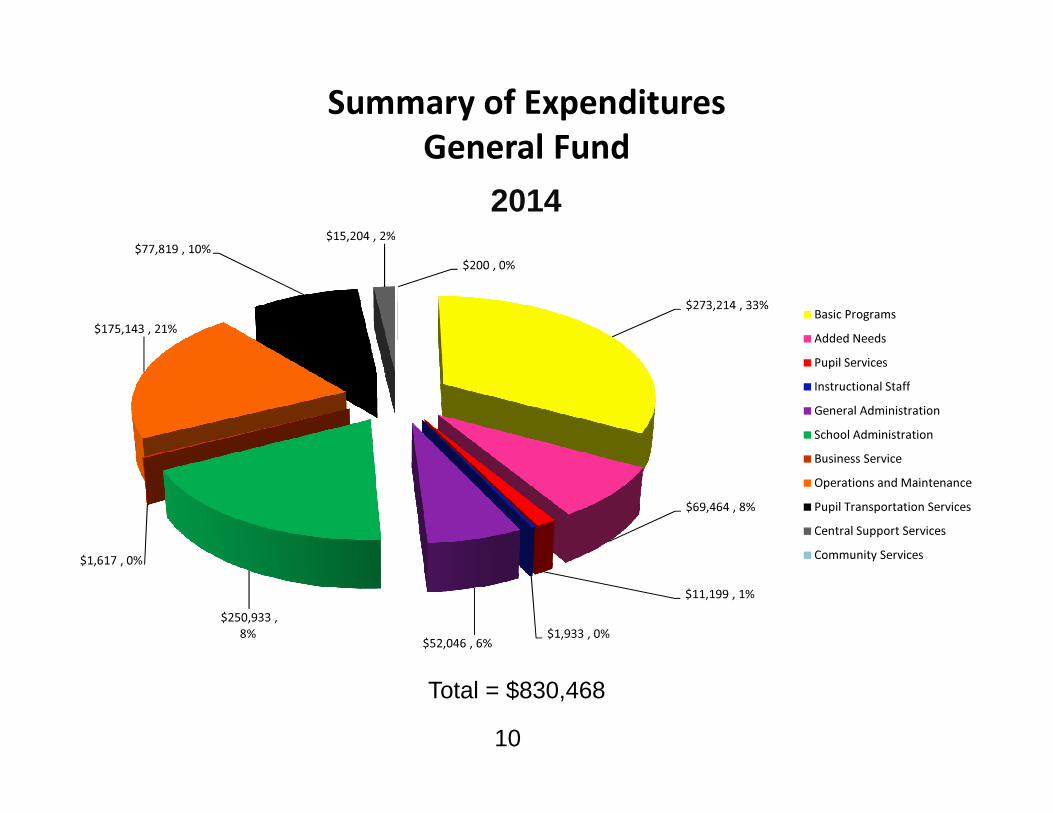

Summary of Expenditures

General Fund

2014

$273,214 , 33%

$175,143 , 21%

$77,819 , 10%$15,204 , 2%

$200 , 0%

Basic Programs

Added Needs

Pupil Services

Instructional Staff

General Administration

10

Total = $830,468

$69,464 , 8%

$11,199 , 1%

$1,933 , 0%$52,046 , 6%

$250,933 ,

8%

$1,617 , 0%

General Administration

School Administration

Business Service

Operations and Maintenance

Pupil Transportation Services

Central Support Services

Community Services

Summary of Net Change in Fund Balance

General Fund

2014

$2,390

11

Total = $2,390

2014

Summary of Assets

Nonmajor Funds

2014

12

Total = $12,845

$12,845 , 100%

Due from Other Funds

Summary of Liabilities

Nonmajor Funds

2014

13

Total = $12,845

$12,845 , 100%

Accounts Payable

Summary of Revenue

Nonmajor Fund

2014

14

Total = $47,623

$47,623 , 100%

Federal Sources

Summary of Expenditures

Nonmajor Fund

2014

15

Total = $54,360

$54,360

0

Food Services