j.b. hunt transport services, inc. · what’s your next move?™ j.b. hunt transport services,...

TRANSCRIPT

®

What’s your next move?™

J.B. Hunt Transport Services, Inc.

2Q 2009 Results

®What’s your next move?™

Disclosure

Today’s presentation and discussion will contain forward-looking statements within the meaning of the

Private Securities Litigation Reform Act of 1995. Words such as “expects,” “anticipates,” “intends,”

“estimates,” or similar expressions are intended to identify these forward-looking statements. These

statements are based on J.B. Hunt’s current plans and expectations and involve risks and uncertainties

that could cause future activities and results of operations to be materially different from those set forth in

the forward-looking statements. For further information, please refer to J.B. Hunt’s reports and filings with

the Securities and Exchange Commission.

2

®What’s your next move?™

2Q 2009 Highlights

Seasonal improvement in volumes but broad-based cyclical weakness

JBI and JBT hurt by pricing pressures and network inefficiencies

Continued investments in JBI to solidify long-term positioning

Down-sizing of JBT to market conditions and customer needs likely nearing

completion

DCS sold more new business than any prior periods setting the stage for

attractive growth in Final-mile-delivery Channel

DCS bearing short-term costs to implement new or expanded Final-mile-

delivery contracts

ICS headcount growth to position for new opportunities

$10.3 million pretax charge to write down the value of certain tractors held

for sale; DCS mix change and JBI dray fleet upgrade

Well positioned for eventual recovery

3

®What’s your next move?™

Distinct Complementary Businesses

Intermodal (JBI) Largest, 100% 53’ high-cube container fleet

Largest drayage fleet in North America

Priority loading and unloading at major rail terminals

Dedicated (DCS) Fleet creation, conversion and augmentation

Design and implementation of value-driven supply

chain solutions

On-site management

Integrated Capacity Solutions (ICS) Non-asset based offering of dry van, flatbed,

refrigerated, expedited and LTL services

40- and 20-foot box domestic and international

containers and international intermodal services

Services to all 50 States, Canada and Mexico

Truckload (JBT) One of the largest capacity networks in North

America

Instant tracking via the Internet

GPS trailer tracking

4

®What’s your next move?™

2Q 2009 Results

• 2Q 2009 Revenue: $770 million; down 21%

• 2Q 2009 Revenue before FSC: $703 million; down 8%

• 2Q 2009 Operating Income: $47 million; down 50%*

• 2Q 2009 EPS: $0.19*, including $0.05/share charge

• Outstanding debt of $648 million vs. $825 million at 2Q08

• Segment Performance• Intermodal (JBI)

• Revenue: $425 million; down 14%

• Operating Income: $38.8 million; down 41%*

• Dedicated (DCS)

• Revenue: $174 million; down 28%

• Operating Income: $8.1 million; down 64%*

• Integrated Capacity Solutions (ICS)

• Revenue: $68 million; up 28%

• Operating Income: $4.2 million; up 85%

• Truck (JBT)

• Revenue: $108 million; down 44%

• Operating Income: ($4.0 million) vs. $3.4 million

• * 2Q 2009 includes $10.3 million pretax charge ($6.6 million for JBI and $3.7 million for DCS) to write down the value of certain tractors held for sale.

5

®What’s your next move?™

Results

6

®What’s your next move?™

Cash Generation and CAPEX

Reductions in JBT’s fleet reduces our

CAPEX needs, all else being equal

Upgrading JBI dray fleet and container and

chassis fleet for better long-term positioning

Equipment mix changes with DCS growth in

Delivery business, and run-off of Capacity

business

* 2006 CAPEX includes trailers previously under operating lease.

7

®What’s your next move?™

JBI and ICS: Load Growth Despite Weak Freight Market

8

®What’s your next move?™

Our Strategy; Before, During, After the Downturn

Use our unique network to bring our customers the low-cost, service-

sensitive advantages of intermodal (JBI)

Utilize our scale, experience, systems and network to drive growth in

services that have defensible characteristics (JBI, DCS Final Mile Delivery and

Replenishment, ICS)

Further leverage the JB Hunt brand, network and technology to penetrate

new markets (DCS, ICS)

Reduce asset-based exposure to areas with low entry barriers, high capital

requirements and undifferentiated service (JBT, DCS Capacity)

Deploy growing free cash flow to further strengthen balance sheet

9

®

What’s your next move?™

J.B. Hunt Transport Services, Inc.

Segment Discussion

®What’s your next move?™

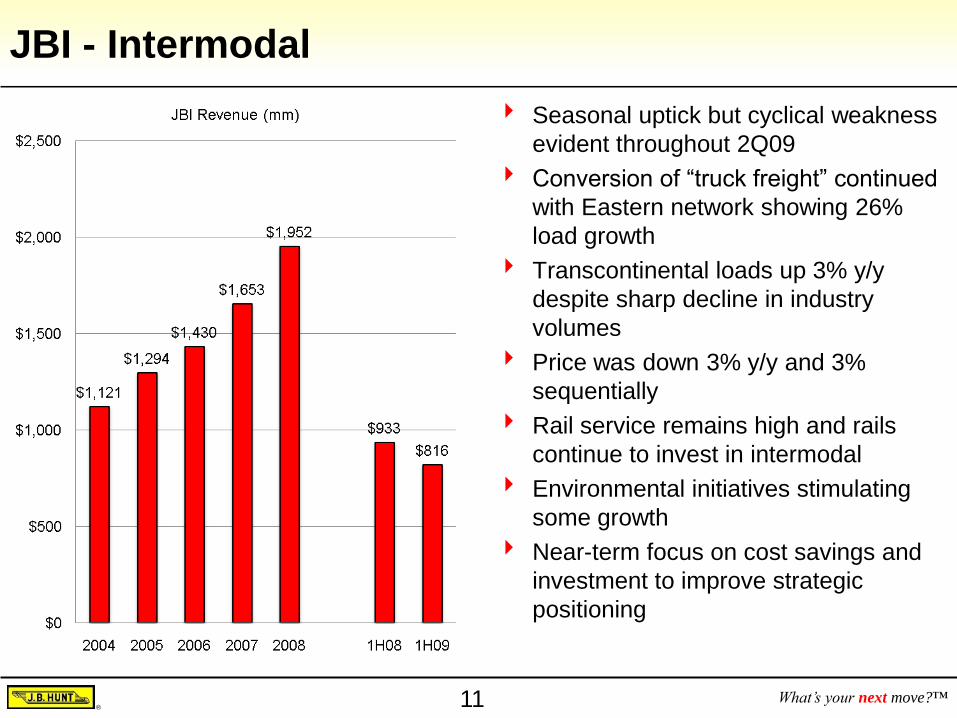

JBI - Intermodal

Seasonal uptick but cyclical weakness

evident throughout 2Q09

Conversion of “truck freight” continued

with Eastern network showing 26%

load growth

Transcontinental loads up 3% y/y

despite sharp decline in industry

volumes

Price was down 3% y/y and 3%

sequentially

Rail service remains high and rails

continue to invest in intermodal

Environmental initiatives stimulating

some growth

Near-term focus on cost savings and

investment to improve strategic

positioning

11

®What’s your next move?™

JBI Performance

12

®What’s your next move?™

Load Growth Despite Falling Diesel Prices

13

®What’s your next move?™

DCS - Dedicated

Sold more business in 2Q 09 than any

prior periods

Implementation costs on new or

expanded contracts hurting near-term

margins

Contracts typically ensure cost

recovery over life of contract

By final 1H 2010 implementation, 98%

of U.S. population will be within 150

miles of one of our delivery facilities

Worked closely with customers to

adjust service levels during period of

very weak demand

Continued run-off of Capacity channel

business that has traditionally been

more cyclical

14

®What’s your next move?™

DCS Performance

15

®What’s your next move?™

Final Mile Delivery

12 years experience in Final Mile

Channel revenue retention >95%

Targeting 100 Crossdock Service Centers

Currently operating 21

Capacity: > 2 million annual deliveries

Reach: 98% US population within 150 miles

Commercial and Residential

Restaurants, Agriculture, Home, Build-site,

Small business and retail

$110MM current annual revenue

Current customers: Best Buy, Cargill, The

Home Depot, Whirlpool, and Blue Seal

Over $100MM in signed agreements

Currently onboarding

Large & technologically advanced fleet and well-

trained employees

16

®What’s your next move?™

DCS: Traditionally Stable vs. Truckload

17

®What’s your next move?™

DCS Characteristics (Year-End 2008)

18

®What’s your next move?™

ICS – Non-asset Based

ICS stand-alone model showing

success in difficult market vs.

“overflow” model used by most

asset-based carriers

Diversification continued to support

growth and steady volume

increases throughout the quarter

Continued growth in workforce to

complete national coverage and

multi-modal offerings

9% growth in carrier base to

21,500 carriers

19

®What’s your next move?™

ICS Performance

20

®What’s your next move?™

ICS - Hitting Stride

Investment in

people and

systems

“Dividends” from

prior investments

21

®What’s your next move?™

ICS Characteristics

22

®What’s your next move?™

JBT – Truckload

Seasonal improvement in volumes

but cyclical weakness evident

throughout the quarter

Continued fleet rationalization with

20% y/y decrease in tractor count

Rates per loaded mile (excluding

FSC) decreased 8.7% y/y

Rates per loaded mile (excluding

FSC) from consistent shippers

declined 3.0% y/y

Maintenance expenses increased

due to the aging tractor fleet that is

not being replaced

23

®What’s your next move?™

JBT Performance

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

1Q08 1Q09 2Q08 2Q09

Revenue per Tractor per Week

24

®What’s your next move?™

Approaching Optimal Fleet Size

25

®What’s your next move?™

Summary

Competitively differentiated

Unique intermodal network

Distinct advantages in dedicated segments

Network economics and brand strength to

penetrate new markets

Prepared to weather downturn

Strong financial position

Less cyclical business model

Diversification

Complemented by industry dynamics

Shippers need to reduce costs

Shippers demand on-time service

Increasingly complex supply-chains

Positioned for recovery

Leading positions in large and

consolidating markets

Clear value proposition for our customers

Best-in-class systems and technology

Intermodal

Dedicated Contract Services

Truckload

Integrated Capacity Solutions

26

®What’s your next move?™

Balance Sheet

27