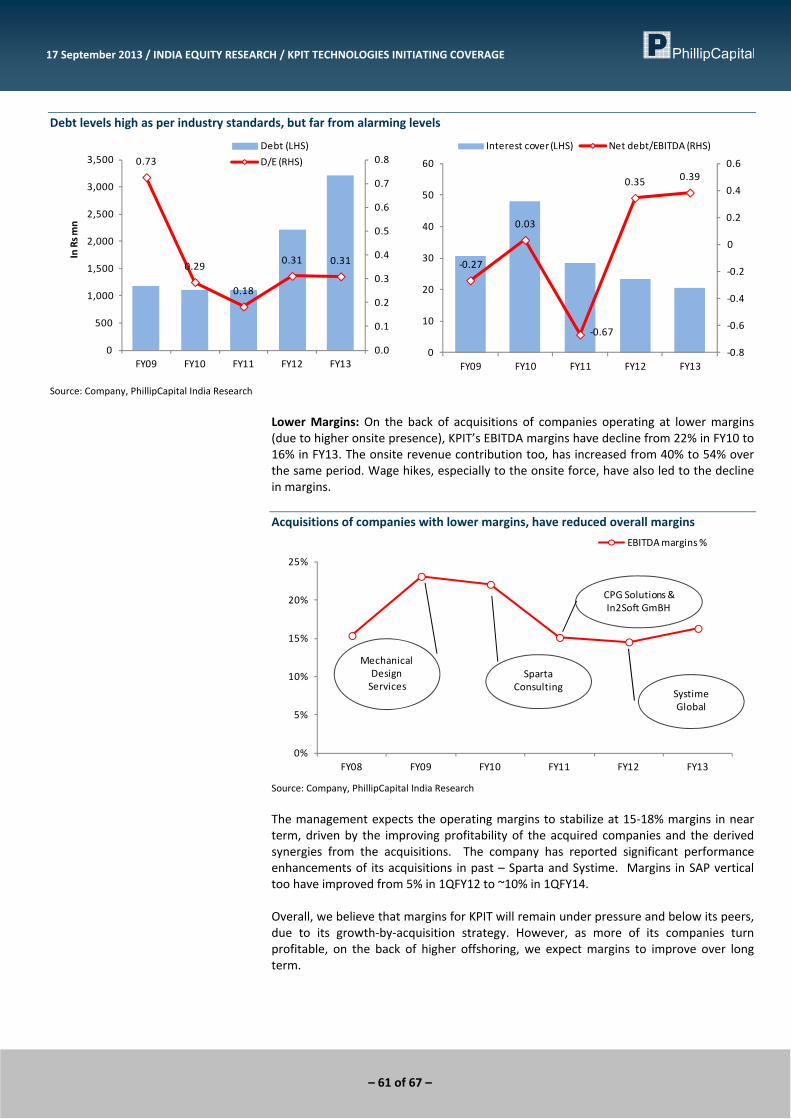

it services sector

TRANSCRIPT

Please refer to Disclosures and Disclaimers at the end of the Research Report

IT Services Sector Will The Party Continue ?

17 September 2013PhillipCapital (India) Pvt. Ltd.

Indian IT Services Sector – Tailwinds galore The Indian IT industry has had a dream‐run over the last six months. From the depreciating rupee adding to the margins to signs of revival in discretionary spending in US – the Indian IT companies never had it so good. Aiding these tailwinds has been the companies’ performance in terms of deal wins – the Indian IT companies have captured significant market share from the MNCs.

But not without its share of challenges However, we feel these tailwinds might be short‐lived or temporary in nature. The challenges that the industry faces – in form of tougher immigration laws being looked at by various countries or constantly evolving technology landscape in form of the new age technologies of CAMS (Cloud, Analytics, Mobile & Social) – are more fundamental in nature.

The Offshore Product Development (OPD) segment – an attractive domain India’s OPD exports grew to $1.4bn in FY13, growing faster than the industry average (CAGR of 15% over last five years), driven by Independent Software Vendors' (ISV) demand to improve time‐to‐market, enhance product features on‐the‐fly and adapt to new technologies. Effectively, the OPD companies have evolved from a project‐oriented low‐end support‐services provider into a strategic partnership role for their customers. As per NASSCOM, the OPD sector will grow by 18% over the next two years – outperforming the industry average.

Relatively better placed to exploit the changing environment As domestic unemployment rates rises in most developed countries, we expect more countries to implement stricter immigration laws. To counter its impact, IT companies will have to either start offshoring larger part of their development (does not augur well for the “Services” domain) or increase the proportion of local employees (significant erosion of margins). The OPD companies, on the other hand, offshore more than 80% of their effort and will be much better placed to mitigate the impact of these stricter immigration laws.

Also, the advent of disruptive technologies CAMS has redefined the entire IT landscape. The OPD firms have been ahead of their Services peers in harboring these technologies, and already have gained a clear headstart. In our opinion, the first mover advantage in these highly technical domains, will enable them to outperform the Services companies, over the next decade.

Key Recommendations We recommend BUY on TCS and HCL Tech – both the companies having a perfectly balanced portfolio and outperformed their peers in all respect. Wipro continues to battle with its management woes, but seems to be showing early signs of revival. And finally the risk‐reward profile for Infosys does not look attractive, with the recent exodus of key management personnel and the company lagging its peers in terms of adapting to new technologies. We recommend NEUTRAL on Infosys and Wipro.

In the OPD domain, we initiate coverage with BUY rating on Persistent Systems and KPIT Technologies – both the companies having carved out a niche for themselves and looking much better placed to exploit their early mover advantage in the CAMS domain and mitigate the impact of stricter immigration laws.

Companies Covered Tata Consultancy Services CMP Rs1902Reco BUYTarget Price Rs2223Upside 17% HCL Technologies CMP Rs997Reco BUYTarget Price Rs1256Upside 26% Infosys CMP Rs2992Reco NEUTRALTarget Price Rs2800Downside ‐6% Wipro CMP Rs451Reco NEUTRALTarget Price Rs486Upside 8% Persistent Systems CMP Rs574Reco BUYTarget Price Rs700Upside 22% KPIT Technologies CMP Rs135Reco BUYTarget Price Rs170Upside 27% Relative Positioning (FY14E)

Infosys

TCS

HCL

Wipro

PSYS

KPIT

0

5

10

15

20

0 10 20 30 40 50

P/E (X)

ROE (%)

Vibhor Singhal (+ 9122 6667 9949) [email protected] Varun Vijayan (+ 9122 6667 9992) [email protected]

2 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

Table of Contents Indian IT Services – Tailwinds galore ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 3

IT spends to report muted growth, competition to intensify ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 5

Indian IT Services – Challenges ahead ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 6

Global Products market and Offshoring ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 7

Evolution of the OPD Sector ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 9

Summary of recommendations ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 13

Companies Section Tata Consultancy Services ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 16

HCL Technologies ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 23

Infosys ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 31

Wipro ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 40

Persistent Systems ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 46

KPIT Technologies ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 55

3 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

Indian IT Services – Tailwinds galore The Indian IT industry has had a dream‐run over the last 6‐8 months. From the depreciating rupee adding to the margins to signs of revival in discretionary spending in US – the Indian IT companies never had it so good. Stalwarts like TCS and HCL Tech are beating their own targets, and reporting strong growth in all verticals, across geographies. On the other hand, Infosys and Wipro too seem to be finally getting their act together, and are likely to tread the recovery path. Mid‐cap companies too, are reporting strong revenue growth and margin expansion.

Consistent performance by the giants ….. ….. and aptly rewarded by the market too

25%

25%

26%

26%

27%

27%

0

5

10

15

20

25

30

35

FY10 FY11 FY12 FY13

US$bn

Top 4 ‐US$ revenuesTop 4 Avg EBITDA margins %

50

100

150

200

250

300

Apr‐10 Oct‐10 Apr‐11 Oct‐11 Apr‐12 Oct‐12 Apr‐13

HCL Tech Infosys

TCS Wipro

BSE Sensex

Source: Company, PhillipCapital India Research

Strong FX tailwinds to boost growth Driven by the deteriorating domestic economic condition and the widening Current‐account deficit, the Indian Rupee has fallen 15% since April‐2013, against USD. This augurs extremely for the IT companies, who directly benefit from Rupee depreciation – an expansion of 30‐50bps in margins for every 100bps depreciation in Rupee. Our economist expects the Rupee to stabilize at levels close to 64‐65 for the remaining part of FY14, taking the average USD‐INR rate to 63 for FY14. For FY15, we assume the Rupee to partially regain its lost ground, and average at Rs62/$.

Margin impact of 100bps depreciation in Rupee vs USD Rupee has lost significantly against major global currencies

22

37 36

30

52

42

10

15

20

25

30

35

40

45

50

55

Infosys TCS Wipro HCL tech KPIT Cummins

Persistent Systems

Chnage

in margins (bps)

For every 1% change in Re

90

100

110

120

130

Jan‐13 Mar‐13 May‐13 Jul‐13

INR/USD INR/GBP INR/EURO

Source: Bloomberg, PhillipCapital India Research

4 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

Grabbing market share from global peers While the developed world has been grappling with recession, leading to reduced discretionary spending by most corporate, we note that the Indian IT companies have performed much better than their global counterparts – in many cases, grabbing market share from the latter. The higher offshoring model provides them better margins than global peers, and hence headroom to win more deals. Also, the technical expertise developed through long standing relationships with clients in various domains has helped the Indian IT companies become the ‘partner by choice’ rather than ‘partner by default’. Indian companies have consistently outperformed the MNCs over last four quarters

‐2,000

‐1,000

0

1,000

2,000

3,000

4,0001Q

FY10

2QFY10

3QFY10

4QFY10

1QFY11

2QFY11

3QFY11

4QFY11

1QFY12

2QFY12

3QFY12

4QFY12

1QFY13

2QFY13

3QFY13

4QFY13

1QFY14

US$

M

Indian Vendors (IVs) MNC Vendors (MVs)

Consistent revenue addition from Indian IT vendors, while MNCs shakes up..

IVs outruns MNCs on revenue adds

IVs outruns MNCs on revenue adds

An upsurge in MNCs revenue

Source: PhillipCapital India Research

Indian IT companies enjoy a significant room in margins, as compared to global peers

7%

9%

11%

13%

15%

17%

19%

21%

23%

25%

FY8 FY9 FY10 FY11 FY12 FY13

Indian IT Avg margins %

MNC Avg margins %

Source: PhillipCapital India Research

However, we feel these tailwinds might be short‐lived or temporary. On the other hand, the challenges that the industry is staring at, are more prolonged, and fundamental in nature. Be it the western world recession and its after effects, or shoestring budgets limiting the discretionary spend of corporate, constantly evolving customer demands and technology landscape or volatile currency market clouding the growth and profitability potential.

5 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

IT spends to report muted growth, competition to intensify Gartner estimates CY2013 to have a better spends growth than that of CY12 in terms of overall technology spends as well as global IT Services spends. It suggests that spends on IT hardware would slowdown while mobile equipments and telecom hardware could see a surplus growth for the year. In IT space, it predicts growth from non‐traditional services which includes new age technology such as Cloud, Mobility, Social Media and Analytics. Though IT budget growth expectation remains muted in CY13, Indian vendors would be able to grow at a higher pace with penetration levels in emerging services and gains in marketshare from that of their MNC counterparts. Gartner estimates mellow spends growth for CY13 Particulars 2008 2009 2010 2011 2012 2013E 2014P

Global tech spending ($ Tn) 3.5 3.3 3.4 3.7 3.7 3.8 3.9growth % ‐6.5 3.5 7.4 1.1 2.2 4.0Global IT Services revenues ($bn) 806 769 793 846 890 926 968growth % ‐4.6 3.1 6.7 5.2 4.0 4.5

Source: Gartner estimates

While MNCs such as Accenture and IBM are facing slow down in its key service lines – Consulting and Enterprise services – TCS and HCL Tech have been gaining on them in regions such as Europe and emerging markets in the same horizontals. To meet regulatory norms, industries are outsourcing most of their IT functions to low cost vendors from India – of which TCS is a front runner. Deal flow data has been declining over the past few quarters

5.4

4.4

5.6

6.5

5.4

6

5.4 5.24.9

3.6

0.60.9

1.51.8

0.9

2.1

1.51.2 1.2

0.7

50

100

150

200

250

300

350

400

0

1

2

3

4

5

6

7

1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12 1Q'13 2Q'13

US$

bn

Global Market ‐ACV (LHS)Mega deals ‐ACV (LHS)No of deals ‐ (RHS)

Source: ISG data ‐ TPI index

Deal flow data from ISG shows a constant decline in the Total Contract Value (TCV) as well as Annual Contract Value (ACV) of the mega deals awarded in the past five quarters. While this points to a dismal future for the industry as a whole, we note that the ISG data does not include: 1) Deal with ACV < $5mn and TCV < $25mn 2) Renegotiation/Scope‐expansion of existing deals With the recovery in US and European corporate opening to outsourcing for the first time (driven by cost pressures), we expect the deal flow to improve over the next few quarters. We also note that over the next two years, a lot of the contracts with the Indian vendors are coming up for renewal, which will lead to further enhancement of the orderbooks.

6 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

Indian IT Services – Challenges ahead Inspite of performing better than their global counterparts, the Indian IT services industry is not without its own share of concerns, many of which bring the growth prospects of the entire industry into question. While few companies like TCS and HCL Technologies have been able to weather the storm and have constantly surprised the markets positively, the malaise has been much widespread. Few of the major issues that the Indian IT Services industry faces, and which have the potential to change the landscape of this industry, in our opinion, are: 1. Tougher immigration laws being (or will be) looked at, by various countries As domestic unemployment rates reach unprecedented highs in most developed countries, we expect more countries to join the US, in implementing stricter immigration laws. To counter their impact, most of IT companies will have to either start offshoring larger part of their development (which might not augur well for the “Services” domain) or increase the proportion of local employees in their workforce (which will lead to significant erosion of margins). 2. Advent of the new technologies CAMS (Cloud, Analytics, Mobility & Social) With the introduction of disruptive technologies like cloud and mobility, the traditional IT business model has gone for a toss. Solutions like SaaS, PaaS and IaaS have enabled the SMBs to scale‐up resources at minimal cost. Both Oracle and SAP have registered a sluggish demand for new license in the last two quarters and have guided for a muted growth in CY13 – primarily due to growth of cloud computing. License sales have historically acted as a leading indicator of growth momentum for the Services companies. Also most corporate now want to migrate their applications to a platform compatible with new age technologies – mobile and social network. These remain highly technical fields, and companies will have to develop strong expertise and domain knowledge, to be able to offer solutions in the same. Lastly, all this has led to a surge in the amount of data available, and hence, increased demand for predictive data analytics. 3. Difficult to move up the ladder to products / consulting functions Intellectual Property (IP) led revenues offer much higher margins than traditional application development jobs, apart from sustainable source of revenue, over a longer period of time. However, ADM or ERP applications for BFSI or Manufacturing, are hardly laden with any high technical requirement, so as to enable the companies develop their niche in any domain. This has been the primary reason behind the big IT Services companies failing to make it big in the IT Products domain. We believe these companies will find it very difficult to change their DNA, and move‐up the value chain to higher IP led revenues.

It is in the wake of the above concerns, that we feel that Indian OPD segment will outperform the traditional IT Services segment. The Indian OPD segment has grown at a robust CAGR of 15% over the last five years, and we expect it to grow by a CAGR of over 18% (NASSCOM estimates) over the next two years. At the same time, the Indian IT Services segment, facing multiple headwinds, is expected to grow by a CAGR of 14% only, over the next two years (NASSCOM estimates). We see the business model of the Indian OPD companies, much more geared to face these headwinds.

7 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

Global Products market and Offshoring The global software product market forms ~20% of the overall global IT industry. The total software product spend in CY11 was $335bn – 20% of the total $1.7trn IT spend. CY11 also saw the emergence of software products from the depths of recession – growing by 6% over CY10 as companies adopted the new technologies (read CAMS) to tread the waters. The year also saw renewed demand for global outsourcing – growing by 12% over CY10 – twice as much as the overall product market. Global Software Product Development market

313 309331

353374 391

‐2%

‐1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

50

100

150

200

250

300

350

400

450

2008 2009 2010 2011 2012 2013E

In US$

bn

Global software spendinggrowth %

Source: Bloomberg

India’s OPD exports crossed $1bn in FY11 and grew to $1.4bn in FY13 – growing faster than the industry growth of 17%. Over the last five years, it has grown at a CAGR of 15%, and as per NASSCOM estimates, it will grow by 18% over the next two years – again outperforming the IT Services (14%). Indian OPD exports growth has been a shade ahead of the average industry growth

16%

5%

19% 16%

10%15%

5%

19%

27%

10%

0%

5%

10%

15%

20%

25%

30%

FY9 FY10 FY11 FY12 FY13

Indian IT exports growth OSPD exports growth

Source: NASSCOM

Though most MNCs (like Microsoft, Facebook) have mainly offshored product development to their ‘own’ GICs (Global In‐house Centers), third party firms have also been making an increasingly significant contribution – enabling the Independent Software Vendors (ISV) to improve time‐to‐market, enhance product features on‐the‐fly, adapt existing products to new technologies etc. Also, long term exposure to clients’ products has enabled them to develop their own set of innovative product accelerators. Effectively, the third party OPD companies have matured into a strategic partnership role

8 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

for their customers – acting as an extended R&D and marketing team for them. We see the relationship only strengthening over the next decade. The Indian OPD market – geared up for the big leap The Indian OPD market has benefitted from both demand and supply side dynamics. There is an ever increasing demand from the ISVs for new product developments, maintenance of legacy products, reduce time‐to‐market for new launches, and re‐engineer product architecture to the new technologies. At the same time, the technological and domain expertise of the OPD firms have meant that these firms are now acting both as consultants and marketing partners – helping customers develop technology roadmap to remain in sync with the rapidly evolving market. And finally, at the center of it all, is the growing proliferation of technologies like cloud computing, data analytics, mobility and social media (CAMS) – especially for the SMBs (Small‐Medium Businesses), which are seeking to leverage these new age technologies to scale‐up resources at minimal cost.

Demand‐Supply side dynamics for the OPD market

• ISV’s: New product development, maintenance of legacy products

• Re‐engineering product architecture to emerging technologies

• SMBs and Industrial clients

• Cloud computing, Mobility, Analytics –expand customer reach, better user insights

• Shorter product lifecycles, faster, on‐the‐fly product upgrades, faster time‐to‐market pressures

• Large number of product releases in the near future

• Consumer‐centric verticals, enterprise application driving growth

• Cloud, Mobility, Big Data/Analytics, Social Media driving new product development

• Legacy systems: Upgradation and migration to new platforms – cloud, mobility

• Verticalised solutions

Service ProvidersCustomers

Market Dirvers

• ISV’s: New product development, maintenance of legacy products

• Re‐engineering product architecture to emerging technologies

• SMBs and Industrial clients

• Cloud computing, Mobility, Analytics –expand customer reach, better user insights

• Shorter product lifecycles, faster, on‐the‐fly product upgrades, faster time‐to‐market pressures

• Large number of product releases in the near future

• Consumer‐centric verticals, enterprise application driving growth

• Cloud, Mobility, Big Data/Analytics, Social Media driving new product development

• Legacy systems: Upgradation and migration to new platforms – cloud, mobility

• Verticalised solutions

Service ProvidersCustomers

Market Dirvers

Source: NASSCOM

Client profile of the Indian OPD vendors

Industrial, 20% ISV, 80%

US, 75% Europe, 15%

RoW, 10%

Customer mkt

Geographic mkt

Source: NASSCOM

9 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

Evolution of the Indian OPD sector Over the last decade, the Indian OPD firms have evolved from project‐oriented low‐end support‐services provider to an end‐to‐end strategic partner for its clients. The OPD firms started with their USP as providing cost‐arbitrage through product support, helpdesk and testing services. Today, the companies have developed technological and domain expertise to move‐up the value chain, and provide support as well as innovative solutions across the entire product lifecycle. The recent global recession has forced the ISVs to increase their focus on core competencies and end user markets. At the same time, disruptive technologies like cloud, mobility and social media are changing the way business is done. Each of these requires specific technical expertise – which is both time and effort consuming as well as expensive. To mitigate the same, the companies have realized importance and necessity of offshoring more and more activities of their product development process. As a result, the scope of services has evolved dramatically for the OPD firms, over the last five years. The OPD firms now form an integral part of the product development team, with their involvement including product designing, prototyping, product development and also, in few recent cases, marketing the product to the end customer.

Evolution of the OPD market

Product support• Helpdesk, technical• Training• Environment support

Testing• Product & Interoperability• Performance & Load• CertificationProfessional Services• Product Implementation• Product Support• Product Customization+ Product Support

Product management• Requirements gathering• Requirement specification• Proof of concept & prototyping• Product roadmapProduct development• Co‐development• Product globalizationUsability engineeringProduct documentationProduct Advancement &Sustenance• Product enhancements• Sustenance services• App maintenanceProduct re‐engineering• Legacy migration• Porting services• Technology refresh+ Testing + Professional Services + Product Support

New product development• Build & release management• Architecture, Design,• Development & testingIntegration• Architecture & planning• Adaptor development• Enterprise app integrationEmerging market focus• Emerging market initiatives• Business P&L for emg marketsProgram management• Vendor management• Business model consultingInnovation: IP generation+ Product management+ Product development+ Usability engineering+ Product documentation+ Product Advancement + Sustenance+ Product re‐engineering+ Testing + Professional Services + Product Support

2008 onwards

2004‐08

2000‐04

2000

Customer Benefits

• Reduced cost, better ROI

• Faster time to market• Continued focus on core competence development

Source: NASSCOM

10 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

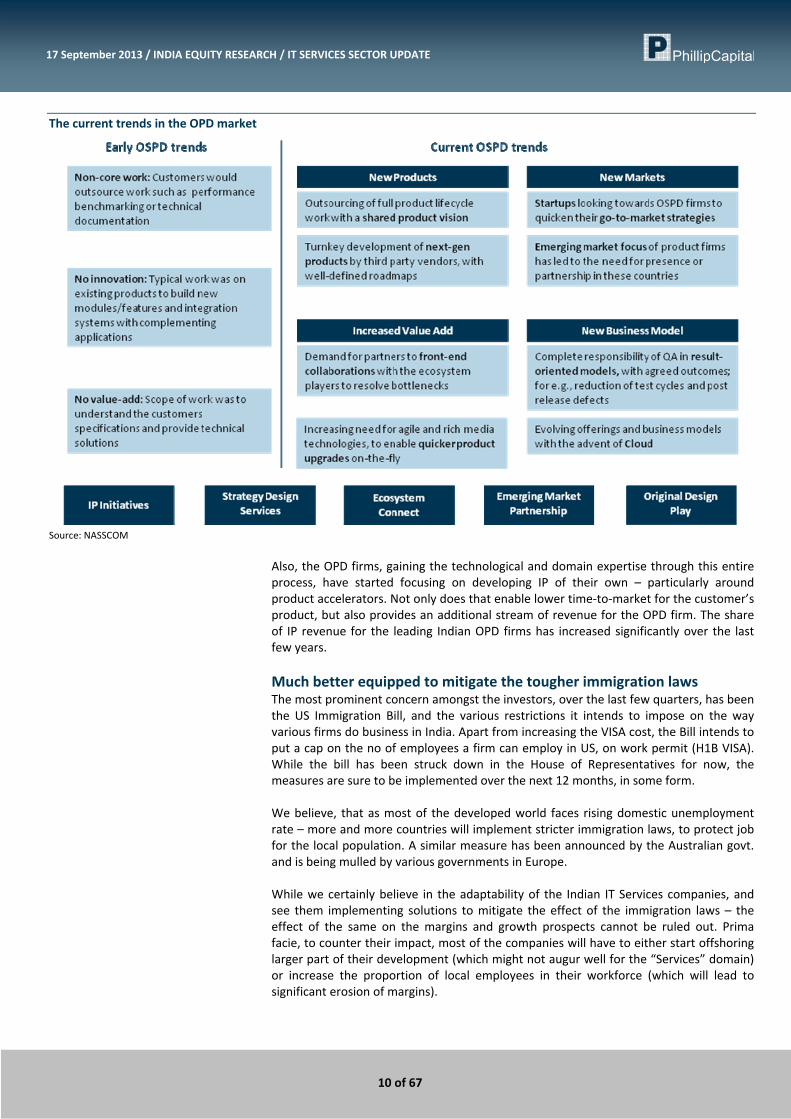

The current trends in the OPD market

Source: NASSCOM

Also, the OPD firms, gaining the technological and domain expertise through this entire process, have started focusing on developing IP of their own – particularly around product accelerators. Not only does that enable lower time‐to‐market for the customer’s product, but also provides an additional stream of revenue for the OPD firm. The share of IP revenue for the leading Indian OPD firms has increased significantly over the last few years. Much better equipped to mitigate the tougher immigration laws The most prominent concern amongst the investors, over the last few quarters, has been the US Immigration Bill, and the various restrictions it intends to impose on the way various firms do business in India. Apart from increasing the VISA cost, the Bill intends to put a cap on the no of employees a firm can employ in US, on work permit (H1B VISA). While the bill has been struck down in the House of Representatives for now, the measures are sure to be implemented over the next 12 months, in some form. We believe, that as most of the developed world faces rising domestic unemployment rate – more and more countries will implement stricter immigration laws, to protect job for the local population. A similar measure has been announced by the Australian govt. and is being mulled by various governments in Europe. While we certainly believe in the adaptability of the Indian IT Services companies, and see them implementing solutions to mitigate the effect of the immigration laws – the effect of the same on the margins and growth prospects cannot be ruled out. Prima facie, to counter their impact, most of the companies will have to either start offshoring larger part of their development (which might not augur well for the “Services” domain) or increase the proportion of local employees in their workforce (which will lead to significant erosion of margins).

11 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

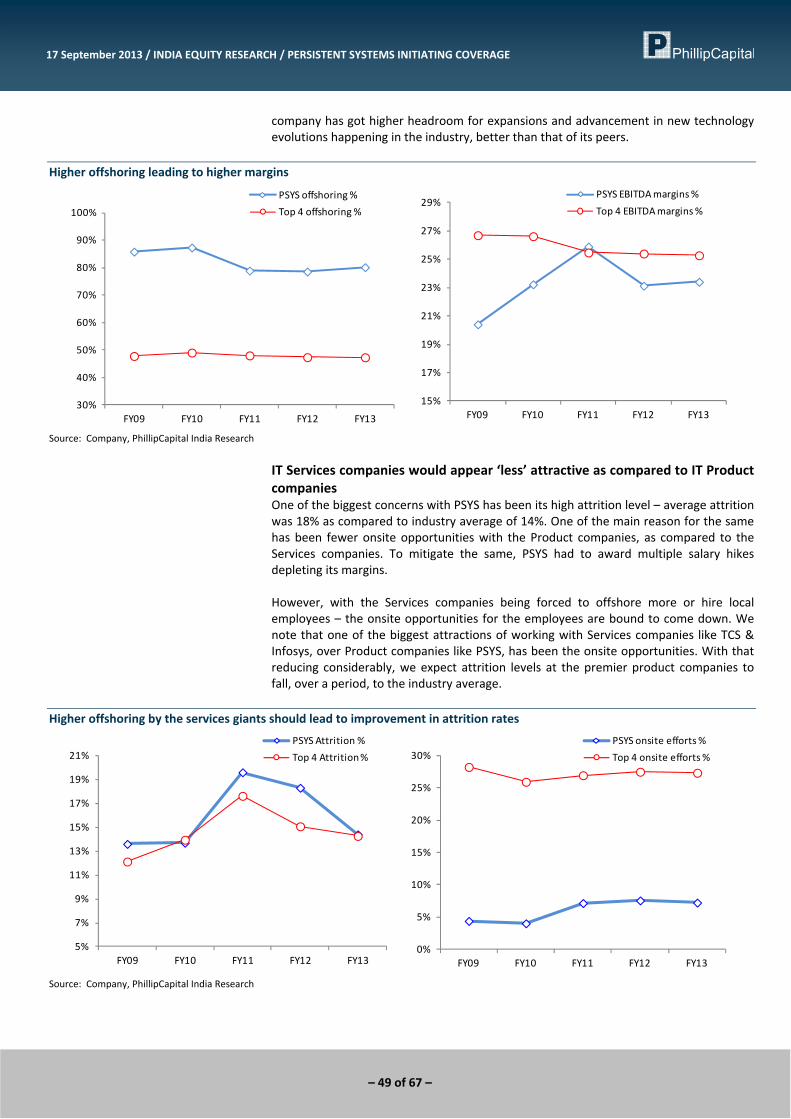

On the other hand, the OPD companies do not require significant onsite presence and can work with larger share of their effort being offshored. Even now, over 92% of workforce for PSYS and 85% for KPIT are based at offshore locations. OPD companies are able to offshore much more than the Services companies

25.9%26.9% 27.5% 27.3%

10.2%11.5% 12.4%

13.3%

8%

13%

18%

23%

28%

33%

FY10 FY11 FY12 FY13

Top 4 onsite efforts OSPD onsite efforts

Source: Company, PhillipCapital India Research

In near or distant future, the stricter immigration laws across the globe, is a reality that the IT industry will have to embrace, and implementing a mitigation strategy for the same could prove to be much more expensive for the IT Services firms, than the OPD firms. This, in our opinion, will lead to a significant outperformance of the OPD companies, over the Services companies over the next three – five years, and hence drive their rerating. The game changer – CAMS The last decade has brought forth disruptive technologies like cloud and mobility, which have the potential to redefine the entire IT landscape. The OPD firms have been ahead of their Services peers in harboring these technologies, and already have gained a clear headstart. In our opinion, the first mover advantage in these highly technical domains, will enable them to outperform the Services companies, which are still coming to terms with the new domains. Cloud Computing: Cloud computing has hit the enterprise solution firms like Oracle and SAP the hardest – with both the companies downgrading their guidance for CY13. Taking that as the lead indicator, we expect Enterprise Application Development domain to be badly hit over the next few years and hence the companies which derive a large part of their revenue from the same (Infosys, Wipro). The very nature of the Cloud‐computing model – its OPEX based, multi‐tenancy, ubiquitous, scalable and elastic delivery mechanism – has attracted the SMB segment, who wants to scale‐up resources at minimal cost, and pay only for what they use. OPD firms have been way ahead of their Services peers in building cloud competencies and setting up CoEs (Centre of Excellence) for R&D. They are increasingly partnering with ISVs to build cloud infrastructure software and various tolls and solutions to help migrate the existing products to cloud environment. Mobility: The convergence of mobility and Web has been facilitated by the rapid penetration of mobile connectivity and advent of smartphones. This has opened up new avenues for ISVs to develop mobile solutions, as extensions to their various enterprise applications. As more and more corporate feel the ‘need’ to stay connected while they are ‘mobile’, the potential for mobility solutions cannot be ignored.

27% of the workforce of the top four companies is currently employed onsite, as compared to 13% for the OPD companies

PSYS launched its first cloud based application in 2007. On the other hand, stalwarts like Infosys, have been slow to develop expertise in these domains.

12 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

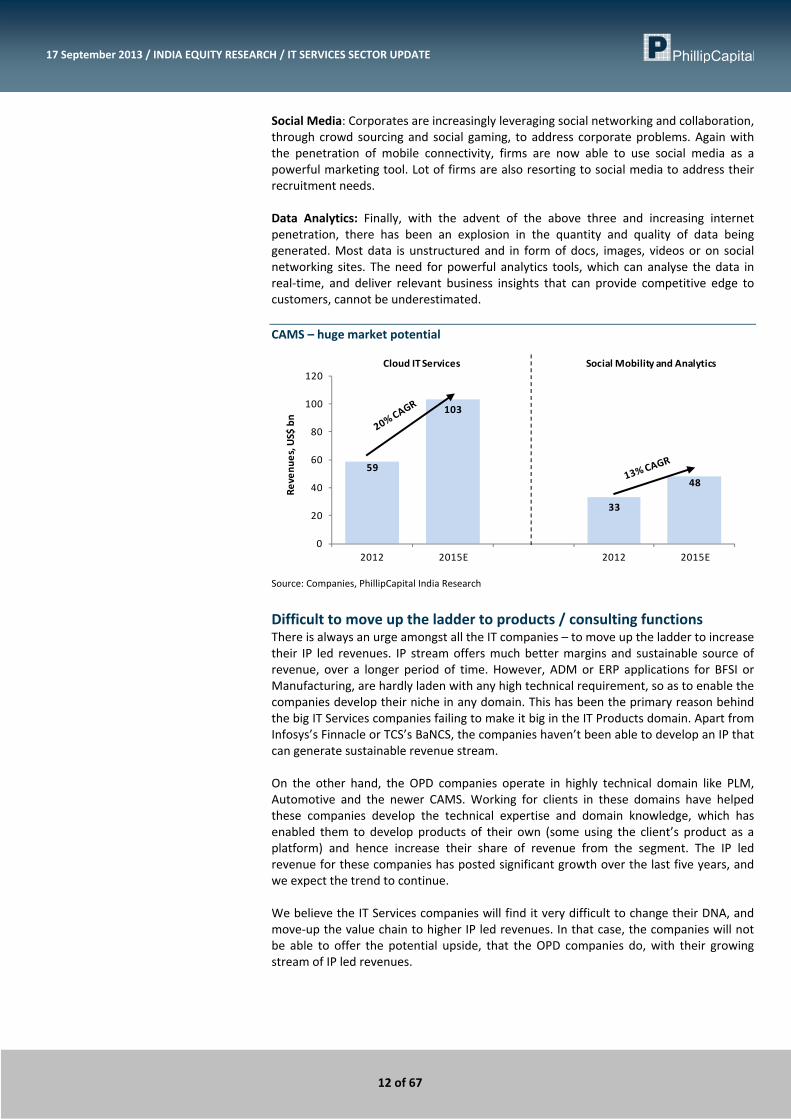

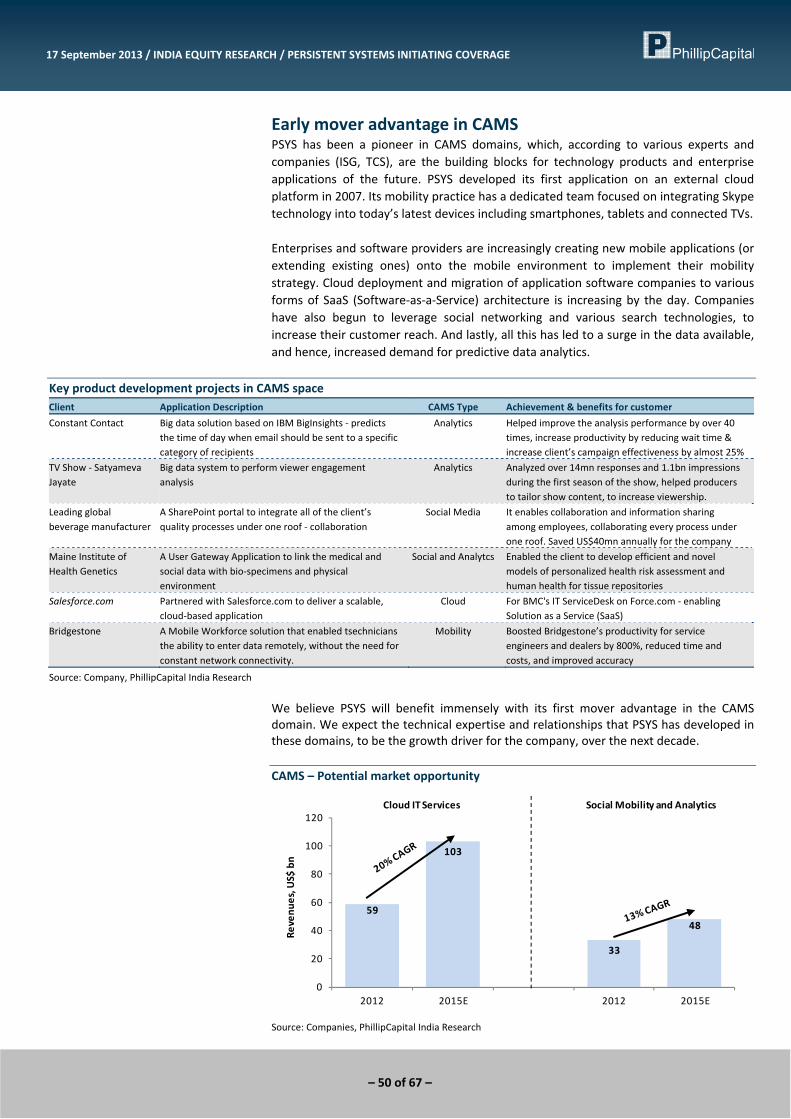

Social Media: Corporates are increasingly leveraging social networking and collaboration, through crowd sourcing and social gaming, to address corporate problems. Again with the penetration of mobile connectivity, firms are now able to use social media as a powerful marketing tool. Lot of firms are also resorting to social media to address their recruitment needs. Data Analytics: Finally, with the advent of the above three and increasing internet penetration, there has been an explosion in the quantity and quality of data being generated. Most data is unstructured and in form of docs, images, videos or on social networking sites. The need for powerful analytics tools, which can analyse the data in real‐time, and deliver relevant business insights that can provide competitive edge to customers, cannot be underestimated. CAMS – huge market potential

59

103

33

48

0

20

40

60

80

100

120

2012 2015E 2012 2015E

Revenu

es, U

S$ bn

Cloud IT Services Social Mobility and Analytics

Source: Companies, PhillipCapital India Research

Difficult to move up the ladder to products / consulting functions There is always an urge amongst all the IT companies – to move up the ladder to increase their IP led revenues. IP stream offers much better margins and sustainable source of revenue, over a longer period of time. However, ADM or ERP applications for BFSI or Manufacturing, are hardly laden with any high technical requirement, so as to enable the companies develop their niche in any domain. This has been the primary reason behind the big IT Services companies failing to make it big in the IT Products domain. Apart from Infosys’s Finnacle or TCS’s BaNCS, the companies haven’t been able to develop an IP that can generate sustainable revenue stream. On the other hand, the OPD companies operate in highly technical domain like PLM, Automotive and the newer CAMS. Working for clients in these domains have helped these companies develop the technical expertise and domain knowledge, which has enabled them to develop products of their own (some using the client’s product as a platform) and hence increase their share of revenue from the segment. The IP led revenue for these companies has posted significant growth over the last five years, and we expect the trend to continue. We believe the IT Services companies will find it very difficult to change their DNA, and move‐up the value chain to higher IP led revenues. In that case, the companies will not be able to offer the potential upside, that the OPD companies do, with their growing stream of IP led revenues.

13 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

Summary of recommendations TCS – BUY – On a different planet altogether TCS has consistently outperformed all its peers, across almost all parameters – posting $ revenue growth of 17.8% (CAGR) over 5 years, with margin expansion of 300bps. In the medium term, we expect the Rupee depreciation and robust deal wins to help it beat street expectations. Over longer term, its higher investment in S&M and early mover advantage in the CAMS domain, should boost it far ahead of peers. TCS stock has run‐up significantly run in the last few months (6m, +28%), driven by its robust operating performance, deal wins and rupee depreciation. We remain positive on the stock, and view it as an attractive investment, inspite of the recent run‐up and perceived rich valuations. Infosys – NEUTRAL – Miles to go before … Post its 1QFY14 results, which were at best, in‐line with expectations, Infosys stock has surged 22% ‐ partly aided by the depreciating Rupee. It currently trades at 16x FY14 and 14x FY15 earnings – still too high a multiple, in our opinion, considering the risk to future earnings and the inadequate gap in valuation with TCS (19x FY14 and 16x FY15). We have a negative stand on the stock, and view the exodus of key employees, lower revenue share of emerging technologies and margin contraction expected on the back of higher S&M spend pose significant risk to the earnings. HCL Technologies – BUY – Perfecting the balancing act HCL has a very balanced portfolio, with ES and IMS forming 47% and 32% of topline respectively. ES (highly related to discretionary spending) has grown by 21% CAGR over the last five years while IMS (not dependent of discretionary spending) by 40% over the same period. The latter has also led to signifcant expansion in margins. HCL also started focusing on non‐linear delivery model much ahead of peers, which contribute 52% of its topline today – highest in the industry. HCL currently trades at 12x FY14 and 11x FY15 earnings ‐ significant discount to the top three. We believe its discount to Infosys and Wipro is unwarranted, as it has delivered significantly better results, both on growth and margins front. Wipro – NEUTRAL – Out of the woods ? Constant management reshuffle ever since Mr Kurien took over as CEO in Feb‐2011 have taken a huge hit on Wipro's operations, and led to sub 8% growth (in $ terms) and non‐expansive margins over the last four years. The company has historically been a low spender on S&M activity (13% of sales), leading to loss of wallet share in key accounts, and the revenue per client growing by only 28% in last five years. However, clear management focus on driving non‐linear revenues has led to an increase in its share in revenues from 35% in FY09 to 45% in FY13. Its strong guidance of 2‐4% QoQ growth in 2QFY14E points to signs of revival in the US and increasing acceptance of outsourcing in Europe.

FY15 EPS: Rs117 Target Multiple: 19x Price Target: Rs2223

FY15 EPS: Rs215 Target Multiple: 13x Price Target: Rs2800

FY15 EPS: Rs90 Target Multiple: 14x Price Target: Rs1256

FY15 EPS: Rs35 Target Multiple: 14x Price Target: Rs486

14 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

Persistent Systems – BUY – Early bird catches more prey Persistent Systems is a leadng Offshore Product Development company, developed more than 3,000 products and applications for nearly 300 customers in the last five years. It has been a pioneer in CAMS domains, having developed its first application on an external cloud platform in 2007. It is also constantly looking to increase its revenue contribution from IP‐led business (8% in FY12 to 13% in FY13) and has dedicated 5% of its employee base to research and IP development. As more countries implement stricter immigration laws to fight rising domestic unemployment rates, we see the company, with higher offshoring effort (93%), to be able to mitigate the effect better than peers. Also, as onsite opportunities reduce with the services companies (due to higher offshoring or local hiring), they are bound to become less attractive from the employees’ perspective – inturn helping the attrition levels at product companies like PSYS. We expect the company to grow by a CAGR of ~26% over FY12‐15, maintaining average EBITDA margins of ~24% over the period. The company operates at much higher margins than peers in the product engineering space, owing to its higher offshoring profile. The PAT growth is expected to be 30% over this period, enabling the company to deliver robust ROE of 22%. KPIT Cummins – BUY – Unique Business Model KPIT Cummins is a niche IT company, concentrating in the Automotive, Manufacturing and Energy & Utilities domains. The three domains constitute over 90% of its topline, and the management envisions each vertical as $1bn+ potential opportunity. It is the largest third party vendor in the Automotive domain (excluding Auto OEMs and captives), and works with 9 out of 12 top Auto OEMs of the world. In the manufacturing domain, Cummins remains their anchor client, though its contribution from other accounts has been steadily increasing. KPIT has been THE most aggressive IT company, in terms of inorganic growth. It has acquired eight companies, since its merger with Cummins Infotech in 2002. The acquisitions have helped the company grow at a CAGR of 24% over last five years ‐ much higher than peers and industry average. However, the same has led to higher debt levels in the comapny (0.3x debt:equity), negative FCF for the last four years, and declining EBITDA margins (22% in FY10 to 16% in FY13). However, Interest coverage of 20.4x and Net debt/EBITDA of 0.4x suggest leverage is still at innocuous levels. Also, post integration of the acquired companies, we expect higher offshoring to improve the EBITDA margins. We expect KPIT to grow by a CAGR of 30% over FY12‐15, maintaining average EBITDA margins of 16% over the period. The PAT growth is expected to be 35% over FY12‐15, enabling the company to deliver robust ROE of 25%.

Valuation Table CMP M‐Cap ______ROE, %______ _______P/E, x_______ ______P/BV, x______ ____EV/EBITDA, x____

Companies (Rs) (Rs bn) FY14E FY15E FY14E FY15E FY14E FY15E FY14E FY15E

TCS 1,902 3,723 41.5 38.7 19.3 16.3 7.2 5.6 14.1 12.1Infosys 2,992 1,717 25.7 24.4 15.5 13.9 3.7 3.1 9.9 8.3Wipro 451 1108 26.1 23.4 13.7 13.0 3.3 2.8 9.8 9.1HCL Tech 997 688 35.5 30.8 12.1 11.1 3.8 3.0 7.7 7.8Persistent 574 23 25.8 22.8 7.9 7.4 1.9 1.6 4.2 3.7KPIT 135 26 27.2 23.9 8.1 7.3 2.0 1.6 5.1 4.4

Source: PhillipCapital India Research Estimates

FY15 EPS: Rs78 Target Multiple: 9x Price Target: Rs700

FY15 EPS: Rs19 Target Multiple: 9x Price Target: Rs170

15 of 67

17 September 2013 / INDIA EQUITY RESEARCH / IT SERVICES SECTOR UPDATE

Compa

nies Section

– 16 of 67 –

TCS On a different planet altogether…

IT SERVICES: Company Update 17 September 2013

PhillipCapital (India) Pvt. Ltd.

Superior performance all across TCS has consistently outperformed all its peers, across almost all parameters – posting $ revenue growth of 17.8% (CAGR) over 5 years, with margin expansion of 300bps. Delivering robust ROE of ~40%, the company is expected to report robust growth in all its verticals, and should benefit immensely from revival in discretionary spending in US and Europe. Robust client mining in all accounts, driven by strong S&M spend Over the last five years, TCS has almost doubled its revenue contribution from the top‐10 as well as non‐top‐10 clients. It currently spends ~18% of revenues for its SG&A base – significantly higher than peers. The strong S&M spend has helped it win mega new deals and rebids worth of US$8.1b over last two years – imparting high revenue visibility for next two years. Much ahead of peers in adopting new technology and delivery models TCS was one of the first few companies to realize the potential of the CAMS domain, and has already invested heavily in the segment. Its Emerging Services segment forms 35% of the total revenues (behind only HCL). Also, TCS has been the most active IT services company to migrate from linear T&M to non‐linear delivery models. Non‐linear revenues contribute ~50% of the total revenues – much ahead of peers again. Strong bench utilisations owing to top‐in‐class service execution It is almost a too good to be true story! Along with higher than industry growth rates and share of new technology & delivery models, TCS also boasts of the highest utilization rate in the industry (83%), and is targeting to further increase it to 85%. The attrition level too, is one of the lowest in the industry (~11%). Boosting up utilisations would squeeze out more realizations per employee, inturn opening profits for higher investments. Valuations appear expensive, but are justified TCS stock has run‐up significantly in the last few months (6m, +26%), driven by its robust operating performance, deal wins and rupee depreciation. On our estimates, TCS is currently trading at 19x FY14 and 16x FY15 earnings. While this is much higher than peers, we think it is justified. The company has consistently outperformed all its peers, on most parameters, and we expect the trend to continue over next two years. TCS has multiple tailwinds, helping it outperform its rivals. In the medium term, we expect the Rupee depreciation and robust deal wins to help it beat street expectations. Over longer term, its higher investment in S&M and early mover advantage in the CAMS domain should boost it far ahead of peers. We remain positive on the stock, and view it as an attractive investment, inspite of the recent run‐up. We value the stock at 19x FY15 earnings, giving us a price target of Rs2223, representing 17% upside from current levels. We recommend BUY.

BUY TCS IN | CMP RS 1902

TARGET RS 2223 (+17%) Company Data

O/S SHARES (MN) : 1957MARKET CAP (RSBN) : 3730MARKET CAP (USDBN) : 59.552 ‐ WK HI/LO (RS) : 2076 / 1198LIQUIDITY 3M (USDMN) : 42.4FACE VALUE (RS) : 1

Share Holding Pattern, %

PROMOTERS : 74.0FII / NRI : 15.7FI / MF : 5.9NON PROMOTER CORP. HOLDINGS : 0.3PUBLIC & OTHERS : 4.2

Price Performance, % 1mth 3mth 1yrABS 7.0 31.4 35.0REL TO BSE 0.8 28.3 27.9

Price Vs. Sensex (Rebased values)

70

120

170

220

270

320

Apr‐10 Mar‐11 Feb‐12 Jan‐13TCS BSE Sensex

Source: Bloomberg, Phillip Capital Research

Key Ratios

Rs bn FY13 FY14E FY15E

Net Sales 629.9 846.1 966.9EBIDTA 180.9 262.3 301.1Net Profit 139.4 192.4 229.0EPS, Rs 71.2 98.3 117.0PER, x 26.7 19.3 16.3EV/EBIDTA, x 20.5 14.1 12.1P/BV, x 9.1 7.2 5.6ROE, % 34.0 37.3 34.4Source: Phillip Capital India Research Vibhor Singhal (+ 9122 6667 9949) [email protected] Varun Vijayan (+ 9122 6667 9992) [email protected]

– 17 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / TATA CONSULTANCY COMPANY UPDATE

Consistent outperformance all across TCS has consistently outperformed all its peers, across almost all parameters – posting $ revenue growth of 17.8% (CAGR) over 5 years, with margin expansion of 300bps. Offering a bouquet of services to its clients with incremental revenue run rate of $1.4bn annually, TCS provides a balanced portfolio of traditional and emerging service lines. Keeping major growth focus on enterprise solutions and asset leveraged solutions (products), the company has grown at a CAGR of 17.8% in $ terms and 22.7% in INR terms for the past 5 years. Even when discretionary spends have declined for two years, TCS has been able to grow the traditional services (about 60‐70% – discretionary projects) at 17.2% along with emerging services (IMS, BI, and Analytics) at 18.8% for the last five years – both above industry average.

Above average (top 4) revenue growth in both traditional and emerging services

19.0

11.4

17.2

8.6

13.7

HCLT Infosys TCS Wipro

Traditional Services 5yr CAGR Average

24.8

15.0

18.8

11.0

17.0

HCLT Infosys TCS Wipro

Emerging lines 5 yr CAGR Average

Source: Company, PhillipCapital India Research

#Traditional services: ADMS, PI, consulting, Engg Services, BPO and Business App Services

Keen focus on key growth areas such as enterprise solutions, engineering solutions and infrastructure services has helped TCS run ahead of Infosys and Wipro in the peer group. With a run rate of 7.6% CQGR in IMS, 4.8% in Enterprise solutions and 4.7% in engineering solutions over last 12 quarters, TCS has managed its business well to compensate for the mellow growth in ASM and ADM services. Key support for the company came from its competitiveness in deal wins and marketshare gains. Overall CAGR for 5 years stands above average

21.5

12.2

17.8

9.5

14.8

HCLT Infosys TCS Wipro

Overall revenue CAGR ‐5 years Average

Source: Company, PhillipCapital India Research

– 18 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / TATA CONSULTANCY COMPANY UPDATE

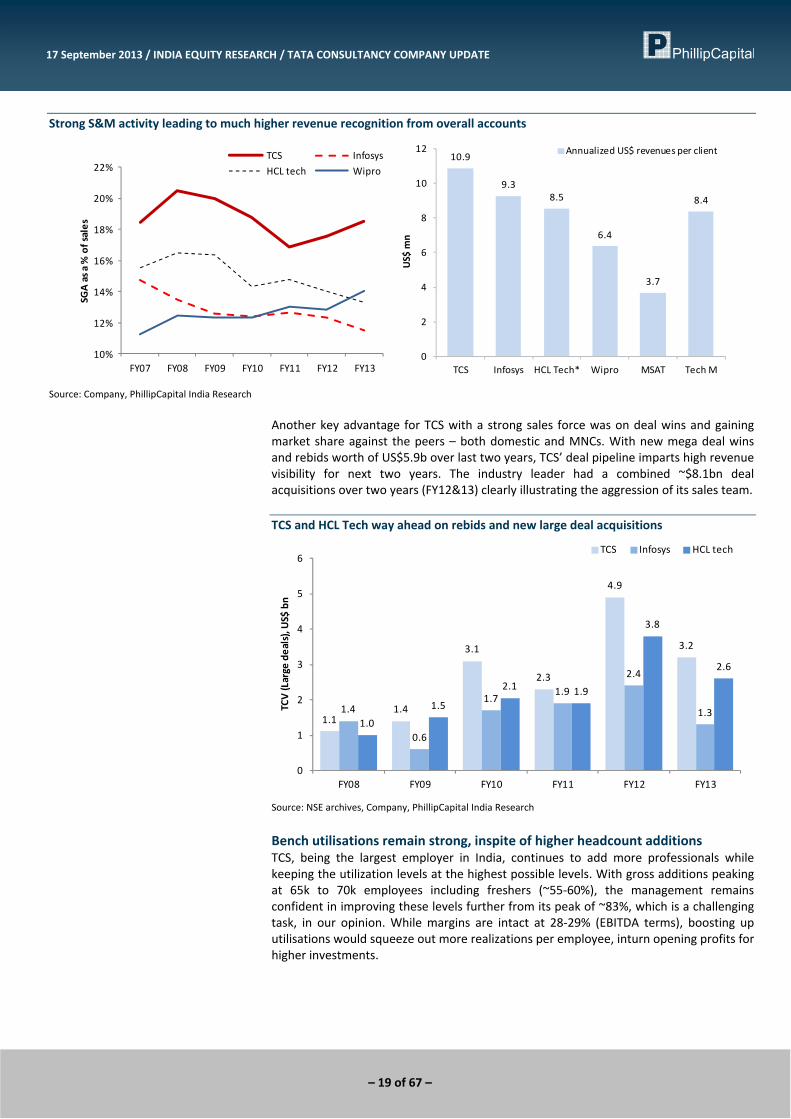

Consulting firms such as Gartner and KPMG estimates high double‐digit growth for IT services offered in cloud (ITaaS, IaaS, BPaaS) and analytics. Recent innovative strategy of TCS to partner with SAP for cloud‐based enterprise platform is a clear example for the IT leader foraying into this largely under penetrated space. We expect that TCS along with peers like HCL and Cognizant to be a front runner in the cloud‐based outsourcing space, which gives further value to the company’s services.

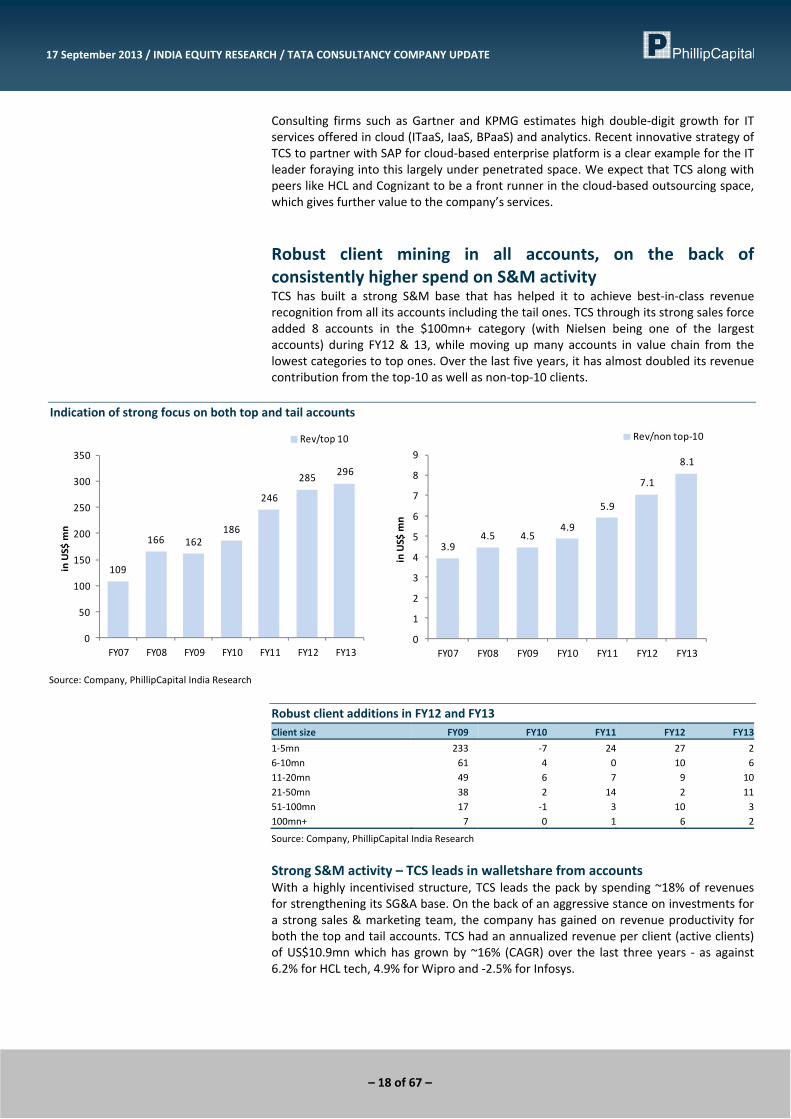

Robust client mining in all accounts, on the back of consistently higher spend on S&M activity TCS has built a strong S&M base that has helped it to achieve best‐in‐class revenue recognition from all its accounts including the tail ones. TCS through its strong sales force added 8 accounts in the $100mn+ category (with Nielsen being one of the largest accounts) during FY12 & 13, while moving up many accounts in value chain from the lowest categories to top ones. Over the last five years, it has almost doubled its revenue contribution from the top‐10 as well as non‐top‐10 clients.

Indication of strong focus on both top and tail accounts

109

166 162186

246

285 296

0

50

100

150

200

250

300

350

FY07 FY08 FY09 FY10 FY11 FY12 FY13

in US$

mn

Rev/top 10

3.94.5 4.5

4.9

5.9

7.1

8.1

0

1

2

3

4

5

6

7

8

9

FY07 FY08 FY09 FY10 FY11 FY12 FY13

in US$

mn

Rev/non top‐10

Source: Company, PhillipCapital India Research

Robust client additions in FY12 and FY13 Client size FY09 FY10 FY11 FY12 FY13

1‐5mn 233 ‐7 24 27 26‐10mn 61 4 0 10 611‐20mn 49 6 7 9 1021‐50mn 38 2 14 2 1151‐100mn 17 ‐1 3 10 3100mn+ 7 0 1 6 2

Source: Company, PhillipCapital India Research

Strong S&M activity – TCS leads in walletshare from accounts With a highly incentivised structure, TCS leads the pack by spending ~18% of revenues for strengthening its SG&A base. On the back of an aggressive stance on investments for a strong sales & marketing team, the company has gained on revenue productivity for both the top and tail accounts. TCS had an annualized revenue per client (active clients) of US$10.9mn which has grown by ~16% (CAGR) over the last three years ‐ as against 6.2% for HCL tech, 4.9% for Wipro and ‐2.5% for Infosys.

– 19 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / TATA CONSULTANCY COMPANY UPDATE

Strong S&M activity leading to much higher revenue recognition from overall accounts

10%

12%

14%

16%

18%

20%

22%

FY07 FY08 FY09 FY10 FY11 FY12 FY13

SGA as a

% of sales

TCS Infosys

HCL tech Wipro10.9

9.38.5

6.4

3.7

8.4

0

2

4

6

8

10

12

TCS Infosys HCL Tech* Wipro MSAT Tech M

US$

mn

Annualized US$ revenues per client

Source: Company, PhillipCapital India Research

Another key advantage for TCS with a strong sales force was on deal wins and gaining market share against the peers – both domestic and MNCs. With new mega deal wins and rebids worth of US$5.9b over last two years, TCS’ deal pipeline imparts high revenue visibility for next two years. The industry leader had a combined ~$8.1bn deal acquisitions over two years (FY12&13) clearly illustrating the aggression of its sales team. TCS and HCL Tech way ahead on rebids and new large deal acquisitions

1.11.4

3.1

2.3

4.9

3.2

1.4

0.6

1.71.9

2.4

1.31.0

1.5

2.1 1.9

3.8

2.6

0

1

2

3

4

5

6

FY08 FY09 FY10 FY11 FY12 FY13

TCV (Large

deals), US$

bn

TCS Infosys HCL tech

Source: NSE archives, Company, PhillipCapital India Research

Bench utilisations remain strong, inspite of higher headcount additions TCS, being the largest employer in India, continues to add more professionals while keeping the utilization levels at the highest possible levels. With gross additions peaking at 65k to 70k employees including freshers (~55‐60%), the management remains confident in improving these levels further from its peak of ~83%, which is a challenging task, in our opinion. While margins are intact at 28‐29% (EBITDA terms), boosting up utilisations would squeeze out more realizations per employee, inturn opening profits for higher investments.

– 20 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / TATA CONSULTANCY COMPANY UPDATE

Utilizations at all‐time high …. ….. attrition at all‐time low

26%

27%

28%

29%

30%

31%

32%

79%

80%

81%

82%

83%

84%

1Q'12 2Q'12 3Q'12 4Q'12 1Q'13 2Q'13 3Q'13 4Q'13 1Q'14

Utilizations (LHS)EBITDA margins (RHS)

5%

7%

9%

11%

13%

15%

17%

19%

21%

23%

25%

FY09 FY10 FY11 FY12 FY13

Attrition

%

InfosysTCSWiproHCL Tech

Source: Company, PhillipCapital India Research

Global network delivery model – key differentiator Global network delivery model (GNDM) is a trademark concept introduced by TCS to ease operations abroad. The structure manages onsite work overload from near shore delivery centers situated close to the client’s location. This model reduces the time to market delays and provides flexibility for TCS to allocate its resources in a structured and cost effective manner inturn supporting the overall margins. GNDM also allows TCS to partner with first party enterprise solution ‐ platform vendors to foray into innovative concepts which increases the company’s competitiveness. The model differentiates TCS from other peers including MNCs. Key advantages: Introduction of cost efficient models, Focus on key customisations and R&D, Better realisations than offshoring and high margins. The Global Network Delivery Model

TCS offshore

GDC

Client

GDC1

GDC2

GDC3

Client

SAP oriented

Oracle Oriented

Service oriented approach on a near

shore development

centre

Other key focus

TCS onsite

Partnering with clients providing key platforms for

undeterred services and support

Source: PhillipCapital India Research

Currently TCS has 32 delivery centers across the globe which manages significant portion of the onsite delivery

– 21 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / TATA CONSULTANCY COMPANY UPDATE

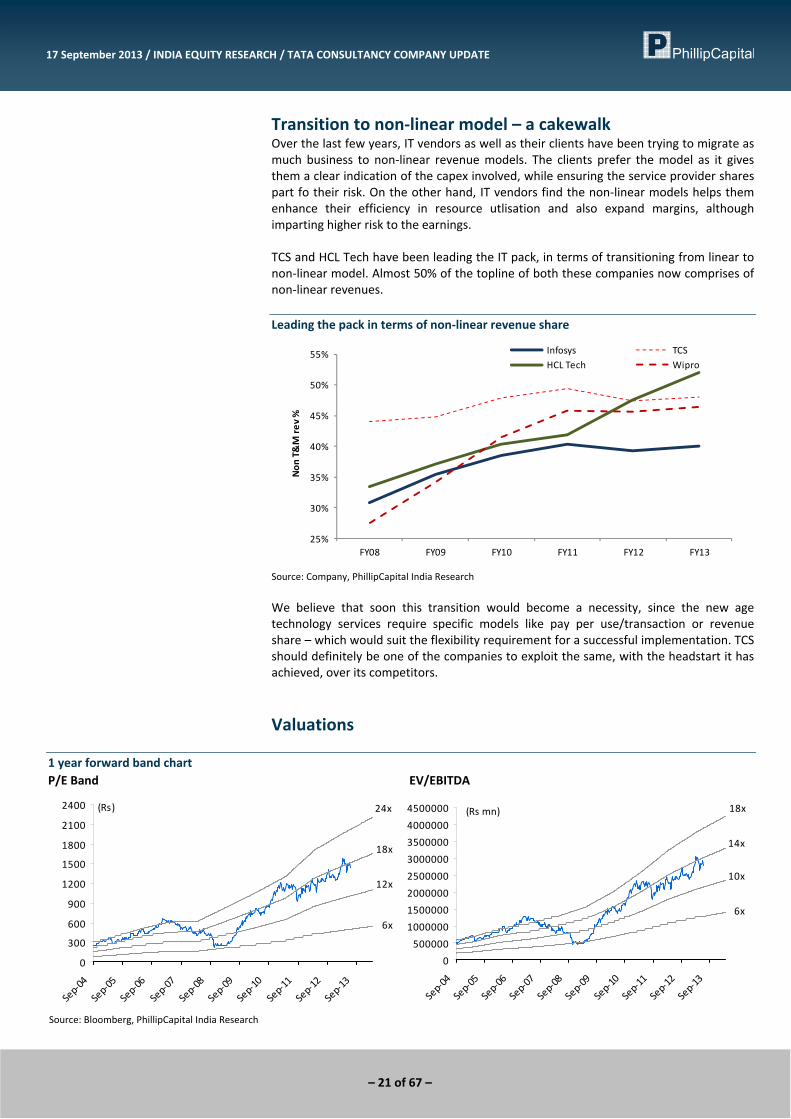

Transition to non‐linear model – a cakewalk Over the last few years, IT vendors as well as their clients have been trying to migrate as much business to non‐linear revenue models. The clients prefer the model as it gives them a clear indication of the capex involved, while ensuring the service provider shares part fo their risk. On the other hand, IT vendors find the non‐linear models helps them enhance their efficiency in resource utlisation and also expand margins, although imparting higher risk to the earnings. TCS and HCL Tech have been leading the IT pack, in terms of transitioning from linear to non‐linear model. Almost 50% of the topline of both these companies now comprises of non‐linear revenues. Leading the pack in terms of non‐linear revenue share

25%

30%

35%

40%

45%

50%

55%

FY08 FY09 FY10 FY11 FY12 FY13

Non

T&M re

v %

Infosys TCSHCL Tech Wipro

Source: Company, PhillipCapital India Research

We believe that soon this transition would become a necessity, since the new age technology services require specific models like pay per use/transaction or revenue share – which would suit the flexibility requirement for a successful implementation. TCS should definitely be one of the companies to exploit the same, with the headstart it has achieved, over its competitors.

Valuations

1 year forward band chart P/E Band EV/EBITDA

6x

12x

18x

24x

0

300

600

900

1200

1500

1800

2100

2400

Sep‐04

Sep‐05

Sep‐06

Sep‐07

Sep‐08

Sep‐09

Sep‐10

Sep‐11

Sep‐12

Sep‐13

(Rs)

6x

10x

14x

18x

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

Sep‐04

Sep‐05

Sep‐06

Sep‐07

Sep‐08

Sep‐09

Sep‐10

Sep‐11

Sep‐12

Sep‐13

(Rs mn)

Source: Bloomberg, PhillipCapital India Research

– 22 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / TATA CONSULTANCY COMPANY UPDATE

Financials

Income Statement Y/E Mar, Rs mn FY12 FY13 FY14E FY15E

Net sales 488,935 629,895 846,081 966,894Growth, % 31 29 34 14Employee expenses ‐258,773 ‐332,545 ‐437,320 ‐496,560Other Operating expenses ‐85,988 ‐116,480 ‐146,501 ‐169,194EBITDA (Core) 144,174 180,870 262,260 301,141Growth, % 28.9 25.5 45.0 14.8Margin, % 29.5 28.7 31.0 31.1Depreciation ‐9,036 ‐10,791 ‐13,528 ‐15,847EBIT 135,138 170,079 248,732 285,294Growth, % 30.1 25.9 46.2 14.7Margin, % 27.6 27.0 29.4 29.5Interest paid 0 0 0 0Other Non‐Operating Income 4,950 11,175 6,392 16,680Pre‐tax profit 139,178 181,254 255,124 301,974Tax provided ‐31,688 ‐40,344 ‐59,227 ‐69,454Profit after tax 107,490 140,910 195,897 232,520Others (Minorities, Associates) ‐1,110 ‐1,494 ‐3,480 ‐3,480Net Profit 106,380 139,416 192,417 229,040Growth, % 22.5 31.1 38.0 19.0Net Profit (adjusted) 106,380 139,416 192,417 229,040Wtd avg shares (m) 1,957 1,957 1,957 1,957

FY12 FY13 FY14E FY15E

US$ Revenue ($ mn) 10,171 11,569 13,414 15,595Growth, % 24 14 16 16Re / US$ (rate) 48.1 54.4 63.1 62.0

Balance Sheet Y/E Mar, Rs mn FY12 FY13 FY14E FY15E

Cash & bank 19,936 18,432 24,786 70,281Marketable securities at cost 0 0 0 0Debtors 115,023 140,766 187,533 216,675Inventory 0 0 0 0Other current assets 87,758 146,169 195,034 227,786Total current assets 222,717 305,367 407,353 514,742Investments 14,783 20,403 27,443 36,443Net fixed assets 174,549 194,965 224,739 270,015Non‐current assets 0 0 0 0Total assets 412,049 520,735 659,535 821,200 Total current liabilities 68,068 88,526 112,814 120,830Non‐current liabilities 13,259 16,088 20,540 22,059Total liabilities 81,327 104,614 133,354 142,889Paid‐up capital 1,957 1,957 1,957 1,957Reserves & surplus 323,490 407,603 514,438 663,088Minorities 5,275 6,561 9,786 13,266Shareholders’ equity 330,722 416,121 526,181 678,311Total equity & liabilities 412,049 520,735 659,535 821,200

Source: Company, PhillipCapital India Research Estimates

Cash Flow Y/E Mar, Rs mn FY12 FY13 FY14E FY15E

Pre‐tax profit 139,178 181,254 255,124 301,974Depreciation 9,036 10,791 13,528 15,847Chg in working capital ‐36,589 ‐61,023 ‐66,869 ‐52,360Total tax paid ‐31,688 ‐40,344 ‐59,227 ‐69,454Other operating activities 0 0 0 0Cash flow from operating activities 79,936 90,678 142,556 196,007Capital expenditure ‐41,316 ‐31,207 ‐43,303 ‐61,122Chg in investments 3,607 ‐5,620 ‐7,040 ‐9,000Chg in marketable securities 0 0 0 0Other investing activities 0 0 0 0Cash flow from investing activities ‐37,708 ‐36,827 ‐50,343 ‐70,122Free cash flow 38,621 59,471 99,254 134,885Equity raised/(repaid) 0 0 0 0Debt raised/(repaid) 1,114 156 ‐23 0Dividend (incl. tax) ‐57,249 ‐50,379 ‐67,536 ‐80,390Other financing activities 19,263 ‐4,924 ‐18,046 0Cash flow from financing activities ‐37,370 ‐55,355 ‐85,860 ‐80,390Net chg in cash 4,858 ‐1,504 6,354 45,495

Valuation Ratios & Per Share Data FY12 FY13 FY14E FY15E

Per Share data EPS (INR) 54.4 71.2 98.3 117.0Growth, % 22.5 31.1 38.0 19.0Book NAV/share (INR) 166.3 209.3 263.8 339.8CFPS (INR) 38.3 40.6 69.6 91.6DPS (INR) 25.0 22.0 29.5 35.1Return ratios Return on assets (%) 28.9 30.2 33.2 31.4Return on equity (%) 32.7 34.0 37.3 34.4Return on capital employed (%) 35.1 36.3 40.0 37.3Turnover ratios Asset turnover (x) 1.9 1.9 2.0 1.8Sales/Total assets (x) 1.3 1.4 1.4 1.3Sales/Net FA (x) 3.1 3.4 4.0 3.9Working capital/Sales (x) 0.3 0.3 0.3 0.3Receivable days 85.9 81.6 80.9 81.8Payable days 71.9 71.1 69.3 65.2Working capital days 100.6 115.0 116.4 122.2Liquidity ratios Current ratio (x) 3.3 3.4 3.6 4.3Quick ratio (x) 3.3 3.4 3.6 4.3Dividend cover (x) 2.2 3.2 3.3 3.3Total debt/Equity (%) 0.7 0.6 0.4 0.3Net debt/Equity (%) (5.5) (3.9) (4.4) (10.2)Valuation PER (x) 35.0 26.7 19.3 16.3PEG (x) ‐ y‐o‐y growth 1.6 0.9 0.5 0.9Price/Book (x) 11.4 9.1 7.2 5.6Yield (%) 1.3 1.2 1.6 1.8EV/Net sales (x) 7.6 5.9 4.4 3.8EV/EBITDA (x) 25.7 20.5 14.1 12.1EV/EBIT (x) 27.4 21.8 14.9 12.8

– 23 of 67 –

HCL Tech Perfecting the balancing act

IT SERVICES: Company Update 17 September 2013

PhillipCapital (India) Pvt. Ltd.

IMS leads through tough times While global economic slowdown impacted most Indian IT Services companies, HCL gained traction by winning large deals in the IMS space ‐ fundamentally decoupled from discretionary spending. The company has posted robust growth in the segment over the last four years (~40%) ‐ much ahead of peers. All along, it has expanded operating margins in the segment by 390bps since FY08, boosting overall margins by 150bps. Balanced portfolio with ES and IMS Services, to capture market share HCL has a very balanced portfolio, with ES and IMS forming 47% and 32% of topline respectively. ES, with its higher correlation to discretionary spending, has grown by 22% CAGR over the last four years for the company – far ahead of peers. IMS, on the other hand, not dependent on discretionary spending, has provided it with both growth and margin expansion. Strong S&M spend leads to higher deal wins HCL has historically been one of the highest spenders (~15% of sales) on S&M activity. The same has resulted in large deal wins for the company over the last few years. We also note a significant improvement in the revenue productivity (Annualized $revenue per employee) for the company in the recent 6 quarters. Alternative approach to IT ‐ geared up for the revolution HCL has been one of the first companies, to adapt to the changing needs of the business. It started focusing on non‐linear delivery model much ahead of peers, which contribute 52% of its topline today – highest in the industry. It has now increased its focus on partnering with businesses and bringing in new services through CAMS, as a part of its 'alternative approach to IT'. BPO Services – a turnaround story HCL management’s strong focus on cost management through automation and rationalisations, while reducing its dependency on resources have led to a strong revival of HCL’s BPO business, which reported continuous erosion of margins through FY11‐12. Margins have significantly improved during the past 4 quarters, indicating a significant change in its structural functions. The management also expects pent up demand from European companies, to drive future growth. Valuation gap not justified in our opinion, recommend BUY HCL currently trades at 12x FY14 and 11x FY15 earnings. While this is slightly higher than its historical average, it is at a significant discount to the top three IT Services giants. While its discount to TCS is justified, we believe it has delivered significantly better results than Infosys and Wipro, both on growth and margins front, to warrant a higher multiple. With a revenue CAGR of 21% over FY13‐15 and average ROE of 33%, we expect a significant re‐rating of the stock. We value the stock at 14x FY15 earnings (8% higher than Infosys), giving us a price target of Rs1256, representing 26% upside from current levels. We recommend BUY.

BUY HCLT IN | CMP RS 997

TARGET RS 1256 (+26%) Company Data

O/S SHARES (MN) : 697MARKET CAP (RSBN) : 695MARKET CAP (USDBN) : 11.152 ‐ WK HI/LO (RS) : 1081 / 548LIQUIDITY 3M (USDMN) : 19.5FACE VALUE (RS) : 2

Share Holding Pattern, %

PROMOTERS : 61.9FII / NRI : 26.0FI / MF : 6.5NON PROMOTER CORP. HOLDINGS : 2.7PUBLIC & OTHERS : 2.9

Price Performance, % 1mth 3mth 1yrABS 8.4 30.9 71.2REL TO BSE 2.1 27.9 64.1

Price Vs. Sensex (Rebased values)

0

50

100

150

200

250

300

350

Apr‐10 Mar‐11 Feb‐12 Jan‐13

HCL Tech BSE Sensex

Source: Bloomberg, Phillip Capital Research

Key Ratios

Rs bn FY13 FY14E FY15E

Net Sales 257.3 340.2 375.1EBIDTA 57.5 82.3 89.4Net Profit 40.2 58.0 63.6EPS, Rs 57.0 82.1 89.7PER, x 17.5 12.1 11.1EV/EBIDTA, x 11.7 8.0 7.1P/BV, x 4.9 3.8 3.1ROE, % 28.1 31.5 27.8Source: Phillip Capital India Research Vibhor Singhal (+ 9122 6667 9949) [email protected] Varun Vijayan (+ 9122 6667 9992) [email protected]

– 24 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / HCL TECH COMPANY UPDATE

IMS leads through tough times Global economic slowdown in FY09 forced many industries towards higher cost rationalisations and regulation cum compliance requirements, leading them to shift to primarily non‐core outsourcing. This, in‐turn, led most majority of the vendors to shift their focus from discretionary to non discretionary projects. This transformation in strategy was the sole play during the period of 2010‐13 to recover the lost revenues. HCL started with balancing its portfolio and forayed into newer technologies, while moving up its value chain in services. With its strong S&M base, the company gained traction by winning large deals from infrastructure management side of the business. IMS led the company through tough global demand challenges, with a CAGR of ~40% post recession period. Also by providing bundled services, HCL enabled its customers to rethink on their spends, where it engaged in multiple partnerships to provide end‐to‐end solutions.

Revenue growth in IMS for the top 4 Revenue growth in key verticals for the top 4

0%

10%

20%

30%

40%

50%

60%

70%

FY09 FY10 FY11 FY12 FY13

YoY IM

S rev grow

th %

HCL Tech* Infosys

TCS Wipro

0%

10%

20%

30%

40%

50%

60%

70%

FY09 FY10 FY11 FY12 FY13

HCL Tech ‐ IMS Infosys ‐ADMTCS ‐ IMS + AS Wipro ‐TIS

Source: Company, PhillipCapital India Research

IMS leading to strong revenue growth as well as margin expansion

0%

10%

20%

30%

40%

50%

60%

70%

80%

FY07 FY08 FY09 FY10 FY11 FY12 FY13

IMS YoY growth %Overall rev YoY growth

15%

16%

17%

18%

19%

20%

21%

22%

23%

24%

FY07 FY08 FY09 FY10 FY11 FY12 FY13

IMS margins Software services marginsOverall margins

Source: Company, PhillipCapital India Research

– 25 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / HCL TECH COMPANY UPDATE

Balanced to perfection – ES and IMS provide growth avenues on the discretionary and non‐discretionary domains HCL has a very balanced portfolio, with ES and IMS forming 47% and 32% of topline respectively. ES, with its higher correlation to discretionary spending, has grown by 22% CAGR over the last four years for the company – far ahead of peers. IMS, on the other hand, not dependent on discretionary spending, has provided it with both growth and margin expansion, over the same period.

Above peer average growth in both Enterprise services and IMS

21.9%

13.7%

HCL Tech Infosys TCS Wipro

4yr ES CAGR Average

40.0%

24.7%

HCL Tech* Infosys TCS Wipro

4Yr IMS rev CAGR Average

Source: Company, PhillipCapital India Research

Software services and enterprise solutions ‐ growth aided by bundled services Traditional software services enclosing Enterprise Application (EAS), Enterprise Transformation (ETS) and BPO had been impacted significantly by the global economic slowdown and the adverse economic events occuring in Europe. HCL Tech’s core software services revenue contribution has declined from 71% levels to ~64%, on reduced IT budgets for discretionary projects during FY11‐13. However, owing to strong deal wins in IMS and high quality executions, the company was able to increase the marketshare and witnessed a CAGR of 21% for the period of FY09‐13 (post recession). Recent transitions encouraged by HCL’s team in bundling up of multiple service lines (such as EAS, ETS, BPO and platform & products) has led to evolve its portfolio to low cost ‐ high value services for its clients. HCL saw its deal win ratio moving up from 40% to 60% over the recent quarters. Owing to the recent deal wins and the positive management commentary, we expect a strong growth in revenues from these services in near term.

Robust client addition, on the back of strong S&M activity HCL’s focus on gaining marketshare from its peers in IMS and Enterprise services has ended up in continued additions on new contracts in the deal pipeline. In FY12, HCL Tech added 4 clients among largest accounts – US$100mn+ category which moved up in value from the $50‐100mn category.

– 26 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / HCL TECH COMPANY UPDATE

Strong client addition during FY12 Client size FY09 FY10 FY11 FY12 FY13E

1‐5mn 168 8 30 27 25‐10mn 42 7 4 15 2110‐20mn 23 11 4 13 (4)20‐30mn 12 0 1 7 230‐40mn 1 4 7 (1) 340‐50mn 3 (1) (1) 3 150‐100mn 2 2 4 (3) 0100mn+ 2 (1) 0 4 0

Source: PhillipCapital India Research Estimates

While the revenue share from the top accounts declined, the company had been able to compensate from its tail accounts. We expect that owing to a strong S&M team and a robust incentive structure, HCL Tech would be able to bring up tail accounts to a profitable state, while keeping the LEAN program active ‐ to cut off the non performing accounts. Consistent margin expansion on increased wedge of profitability Keeping in mind that a strongly incentivized sales and marketing team would be a major factor in bringing up the revenue productivity, HCL has been building a very successful structure of sales and marketing professionals over the past decade. While HCL has been expanding its margins during FY11‐13, it has reduced the SGA investments which has led to contraction of cost margins. We note a significant improvement in the revenue productivity (Annualized $revenue per employee) for the company in the recent 6 quarters.

Strong S&M activity ….. ….. leading to higher revenue productivity (per employee)

10%

12%

14%

16%

18%

20%

22%

FY07 FY08 FY09 FY10 FY11 FY12 FY13

SGA as a

% of sales

TCS Infosys

HCL tech Wipro

40

42

44

46

48

50

52

54

56

58

60

1Q '12 2Q '12 3Q '12 4Q '12 1Q '13 2Q '13 3Q '13 4Q '13

Rev prod

uctivity, In US$

'000s

HCLT InfosysTCS Wipro

Source: Company, PhillipCapital India Research

– 27 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / HCL TECH COMPANY UPDATE

HCL's alternative approach to IT The changing demand environment over all the verticals and regions in the past two years has resulted a major migration from the traditional pricing model – T&M – to more outcome‐based model. HCL found their provision of more flexible pricing models – such as pay per solution or pay per use or fixed price models – to be more attractive to their clients. In return, the flexibility in resource allocation provides HCL more profitability while providing client stickiness which was the motivation to migrate from T&M. Along with this migratory pattern, they also focused on alternative methods to improve value of their services.

Alternative approach to IT

Gen1: First time outsource

Gen2 Gen+

Revenue Impact

Cost Impact Business Cost

Front, Middle and Back office innovation

Impact

Tactical

T&M

Resource Cost

Staff Augmentation

Program Based

Managed Services

Services Cost

Managed ServicesAPOConsolidation / VirtualizationEOOTBPlatform BPO

Business Driven & Strategic

Outcome Based

Business Cost

Alternative ITEg. ALT ASM, From No To How BPaaS, TechCMO

Outsourcing

Model

Cost

Key Proposition

Time

• Traditional model adopted by mostof the Indian IT vendors duringFY01‐09.

• During this phase, Indian IT vendorsplayed out on labor arbitrage

• Revenues were linear to resourceaddition.

• Managed services model where thedelivery model was highlydiscretionary.

• HCL and most of its peers are in thisphase currently.

• Transition to Alternative phasesfrom linear business structure.

• More critical and rewarding; clientstend to be more sticky.

• Partnering with businesses andbringing in new services throughnon traditional methods (CAMS)

Source: Company, PhillipCapital India Research

– 28 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / HCL TECH COMPANY UPDATE

Scope for alternative methods

Proactive Obsolescence

Agility & Flexibility Helicopter Landing

3yr CAGR

3yr CAGR

4.9%

4%

Traditional IT Services

“EXPLOIT”

Total market US $678bn

Penetrated Services*(EAS, ASM and ADM)

Total market US $289bn

Underpenetrated Services

IMS BPO ERS$231bn $112bn $6bn

Alternative Outsourcing

Alternative IT

Industry Utility Through Benefit Realization

Customer Experience

3yr CAGR

*IOP4 share <5% taken as under‐penetrated** Include BPaaS, SaaS, IaaS and PaaS*** Services market estimated based on software and solution market

20.4%

13.1%

New age ‐ IT Services

“EXPLORE”

Total market US $92bn

Xaas (Transformation led BPO, EAS & ETS)

Total market US $59bn**

Social, Mobility & Analytics

Total Market US $33bn***

Alternative Markets

Proactive Obsolescence

Agility & Flexibility Helicopter Landing

3yr CAGR

3yr CAGR

4.9%

4%

Traditional IT Services

“EXPLOIT”

Total market US $678bn

Penetrated Services*(EAS, ASM and ADM)

Total market US $289bn

Underpenetrated Services

IMS BPO ERS$231bn $112bn $6bn

Alternative Outsourcing

Alternative IT

Industry Utility Through Benefit Realization

Customer Experience

3yr CAGR

*IOP4 share <5% taken as under‐penetrated** Include BPaaS, SaaS, IaaS and PaaS*** Services market estimated based on software and solution market

20.4%

13.1%

New age ‐ IT Services

“EXPLORE”

Total market US $92bn

Xaas (Transformation led BPO, EAS & ETS)

Total market US $59bn**

Social, Mobility & Analytics

Total Market US $33bn***

Alternative Markets

Source: Company, PhillipCapital India Research

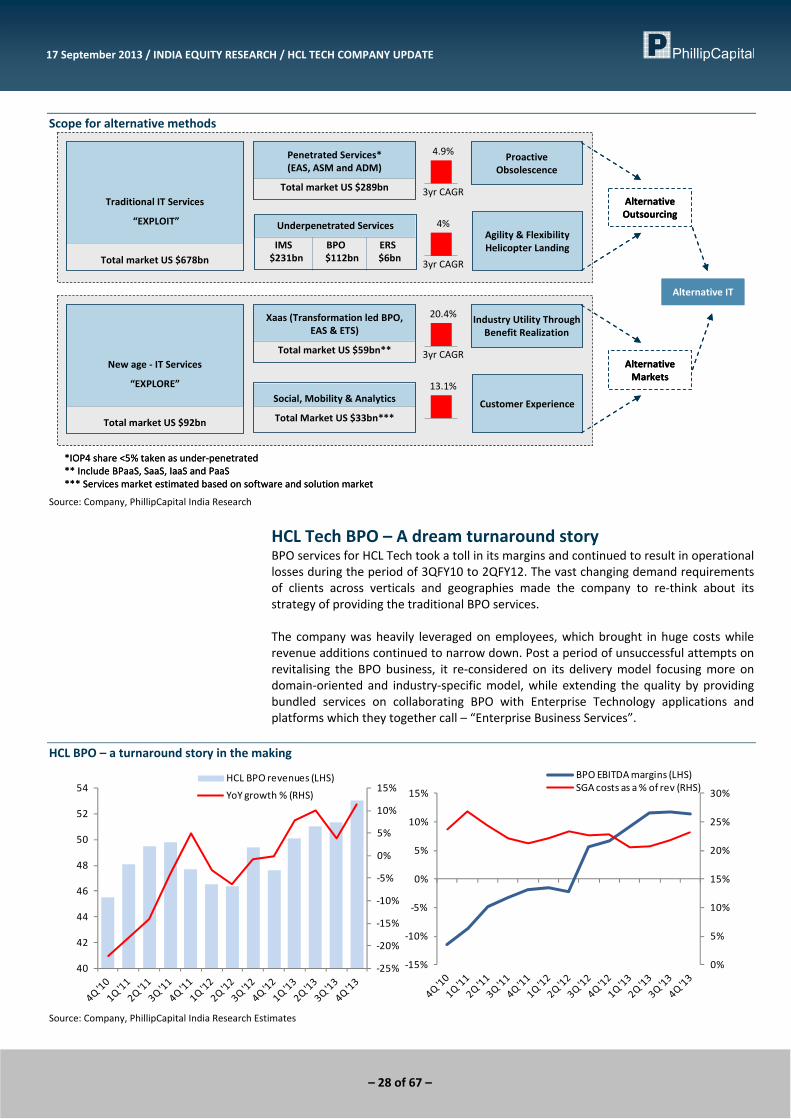

HCL Tech BPO – A dream turnaround story BPO services for HCL Tech took a toll in its margins and continued to result in operational losses during the period of 3QFY10 to 2QFY12. The vast changing demand requirements of clients across verticals and geographies made the company to re‐think about its strategy of providing the traditional BPO services. The company was heavily leveraged on employees, which brought in huge costs while revenue additions continued to narrow down. Post a period of unsuccessful attempts on revitalising the BPO business, it re‐considered on its delivery model focusing more on domain‐oriented and industry‐specific model, while extending the quality by providing bundled services on collaborating BPO with Enterprise Technology applications and platforms which they together call – “Enterprise Business Services”.

HCL BPO – a turnaround story in the making

‐25%

‐20%

‐15%

‐10%

‐5%

0%

5%

10%

15%

40

42

44

46

48

50

52

54HCL BPO revenues (LHS)

YoY growth % (RHS)

0%

5%

10%

15%

20%

25%

30%

‐15%

‐10%

‐5%

0%

5%

10%

15%

BPO EBITDA margins (LHS)SGA costs as a % of rev (RHS)

Source: Company, PhillipCapital India Research Estimates

– 29 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / HCL TECH COMPANY UPDATE

While below EBIT level losses still continue, the operating margins have improved for BPO business during the past 4 quarters, indicating a significant change in its structural functions. We note a change in BPO’s operating model from a traditional service vendor to a combined business services model which the management calls ‘Next Generation BPO’. Outlook on HCL BPO Strong focus on cost management through automation and rationalisations, while reducing its dependancy on resources have taken effect and is turning out to be a grand strategy for revival of HCL’s BPO business. The management expects a pent up demand from European companies who are forced to outsource most of its non‐core IT projects, where HCL’s Enterprise Business Services will come into play. We expect this segment to have higher penetration levels in EU regions where its unique structure would provide an upper hand in winning profitable deals. We also expect margin expansion to lead to the segment margins reaching close to the 15‐16% levels in the near term.

Valuations

1 year forward band chart P/E Band EV/EBITDA

5x

10x

15x

20x

0

200

400

600

800

1000

1200

1400

Apr‐06

Apr‐07

Apr‐08

Apr‐09

Apr‐10

Apr‐11

Apr‐12

Apr‐13

(Rs)

4x

6x

8x

10x

0

100000

200000

300000

400000

500000

600000

700000

800000

Apr‐06

Apr‐07

Apr‐08

Apr‐09

Apr‐10

Apr‐11

Apr‐12

Apr‐13

(Rs mn)

Source: Bloomberg, PhillipCapital India Research

– 30 of 67 –

17 September 2013 / INDIA EQUITY RESEARCH / HCL TECH COMPANY UPDATE

Financials

Income Statement Y/E Jun, Rs mn FY12 FY13 FY14E FY15E

Net sales 210,312 257,336 340,224 375,081Growth, % 33 22 32 10Employee expenses ‐141,413 ‐165,599 ‐214,432 ‐237,980Other Operating expenses ‐29,503 ‐34,201 ‐43,477 ‐47,694EBITDA (Core) 39,396 57,536 82,315 89,407Growth, % 50.2 46.0 43.1 8.6Margin, % 18.7 22.4 24.2 23.8Depreciation ‐5,641 ‐6,726 ‐7,405 ‐8,847EBIT 33,755 50,810 74,910 80,560Growth, % 58.5 50.5 47.4 7.5Margin, % 16.0 19.7 22.0 21.5Interest paid 0 0 0 0Other Non‐Operating Income 706 1,769 1,417 2,027Pre‐tax profit 32,585 52,381 75,379 82,587Tax provided ‐8,180 ‐12,217 ‐17,337 ‐18,995Profit after tax 24,405 40,164 58,041 63,592Others (Minorities, Associates) 0 0 0 0Net Profit 24,405 40,164 58,041 63,592Growth, % 53.0 64.6 44.5 9.6Net Profit (adjusted) 24,405 40,164 58,041 63,592Wtd avg shares (m) 700 705 707 709

FY12 FY13 FY14E FY15E

US$ Revenue ($ mn) 4,152 4,687 5,298 6,050Growth, % 17 13 13 14Re / US$ (rate) 50.7 54.9 64.2 62.0

Balance Sheet Y/E Jun, Rs mn FY12 FY13 FY14E FY15E

Cash & bank 6,673 7,321 13,968 25,046Marketable securities at cost 18,777 42,491 57,491 69,491Debtors 53,440 61,767 82,027 91,458Inventory 0 0 0 0Other current assets 15,212 19,071 23,580 27,719Total current assets 94,102 130,650 177,065 213,714Investments 2,943 577 1,077 1,577Net fixed assets 92,231 99,254 113,603 123,320Non‐current assets 0 0 0 0Total assets 189,276 230,481 291,745 338,611 Total current liabilities 49,394 65,423 85,185 91,280Non‐current liabilities 32,568 22,111 22,548 18,325Total liabilities 81,962 87,534 107,733 109,605Paid‐up capital 1,341 1,341 1,341 1,341Reserves & surplus 105,974 141,607 182,671 227,665Minorities 0 0 0 0Shareholders’ equity 107,314 142,947 184,012 229,005Total equity & liabilities 189,276 230,481 291,745 338,611

Source: Company, PhillipCapital India Research Estimates

Cash Flow Y/E Jun, Rs mn FY12 FY13 FY14E FY15E

Pre‐tax profit 32,585 52,381 75,379 82,587Depreciation 5,641 6,726 7,405 8,847Chg in working capital ‐6,410 3,843 ‐5,006 ‐7,476Total tax paid ‐8,180 ‐12,217 ‐17,337 ‐18,995Other operating activities 0 0 0 0Cash flow from operating activities 23,636 50,733 60,441 64,964Capital expenditure ‐23,437 ‐13,749 ‐21,754 ‐18,564Chg in investments ‐163 2,366 ‐500 ‐500Chg in marketable securities ‐1,566 ‐23,714 ‐15,000 ‐12,000Other investing activities 0 0 0 0Cash flow from investing activities ‐25,166 ‐35,097 ‐37,254 ‐31,064Free cash flow 199 36,984 38,687 46,399Equity raised/(repaid) 0 0 0 0Debt raised/(repaid) 4,441 ‐10,457 437 ‐4,223Dividend (incl. tax) ‐9,702 ‐9,749 ‐16,977 ‐18,598Other financing activities 8,266 5,218 0 0Cash flow from financing activities 3,005 ‐14,988 ‐16,540 ‐22,821Net chg in cash 1,475 648 6,647 11,078

Valuation Ratios & Per Share Data FY12 FY13 FY14E FY15E