it market outlook a new reality after september 11 january 16, 2002 sung-lae park [email protected]...

TRANSCRIPT

IT Market Outlook A New Reality

After September 11

IT Market Outlook A New Reality

After September 11January 16, 2002

Sung-Lae Park

Research Director / IDC Korea

January 16, 2002

Sung-Lae Park

Research Director / IDC Korea

IDC= Internet Data

Center

IDC is the foremost global market intelligence and advisory firm since 1964

IDC= International Data Corporation

Components and Peripherals

Channels

Communications

Personal SystemsEnterprise Systems

Software

IT Overview

Verticals

Internet and eBusiness

Services

Global Depth and Breadth400+ Subscription Services

Technology Areas

IDC’s International Research Centers44 Countries, 53 Offices

United StatesArgentinaBrazilCanadaChileColombiaMexicoVenezuela

AustriaBelgiumCzech RepublicDenmarkFinlandFranceGermanyHungaryItaly

AustraliaChinaEgyptHong Kong IndiaIsraelJapanKoreaMalaysia

Netherlands PolandPortugalRussiaSpainSwedenSwitzerlandTurkeyU.K.

New ZealandNigeriaPhilippinesSingaporeSouth AfricaTaiwanThailandU.A.E.Vietnam

••••

••••

••••••

••

•• ••

••••

••

••

••

••••

••

••

••••••••

••

•• ••••••••

•• •• ••••

••

•••• ••••

••••••••

••

••

••

Agenda

The Scene before September 11 Worldwide IT Spending, 2001 Sep. 11 and Operation Beacon Assumptions for New Scenarios

IT Market Outlook for 2002 and beyond Outlook by Product Outlook by Industry Outlook by Region Worst Case Scenario

Conclusions & Recommendations

IT Spending, 2001

US$B998 US$B432

Source: IDC, 2002

Worldwide

US43%

ROW57%

U S

Hardware31.5%

Software22.4%

Services46.1%

Before: A “Perfect Storm”

Internet Stock Crash

March 2000

US Economy

Slide

Q4 2000

Telecom Capacity

Glut

2001

But Things Weren’t That Bad

GDP was expected to bottom Q3 (Consensus)

Tax rebates almost .5% GDP, energy prices falling, leading indicators up, interest rate cuts

IDC surveys Q1, Q2, Q3 showed 2002 IT budget growth

CIO Tech Poll of CIOs in August showed spending trough in May

11.1

6.6

7.8

10.7

10.9

5.0

0

2

4

6

8

10

12

2000 2001 2002 2003 2004 2005

The Rebound Was Coming

US IT Spending“Worst Case”

Scenario

Source: IDC Global IT Economic Outlook Program

• GDP Up Q4, Business Investment Positive• Businesses able to anticipate profits start to spend again

• Recovery by segment

% Growth

IDC September 11 Response

Sept. 11 – press calls Sept. 14 – IDC company meeting Sept. 17 – European IT Forum Sept. 18 – 1st Web Site Posting (First top line)

Sept. 20 – launch Operation Beacon Oct. 11 – Client Telebriefing Nov. 11 – Full 55 Beacon Black Book Dec. 11 – Alternative Scenario

Operation Beacon

Elements of Operation Beacon Discuss and agree on a common scenario Agree on a schedule, common format, analysis

framework Use common analytical inputs – historical

context, GDP histories, etc. Perform small group Delphi process to adjust

growth rates; adjust first for worsening economy prior to September 11, then for the attack

Constantly update

Components and Peripherals

Channels

Communications

Personal SystemsEnterprise Systems

Software

IT Overview

Verticals

Internet and eBusiness

Services

Recasting 1000 Forecasts

The Beacon Scenario*

Beacon

Terrorism No major

Reaction Back to normal

Economy Rebound Q2

US GDP Just positive 2001

WE GDP 1%-2% 2002

Housing Starts stay up

Unempl. Nothing said

* Established on 9/20/2001

Inputs for a New Scenario

Y2K economic impact model

Other wild card events

100 analysts

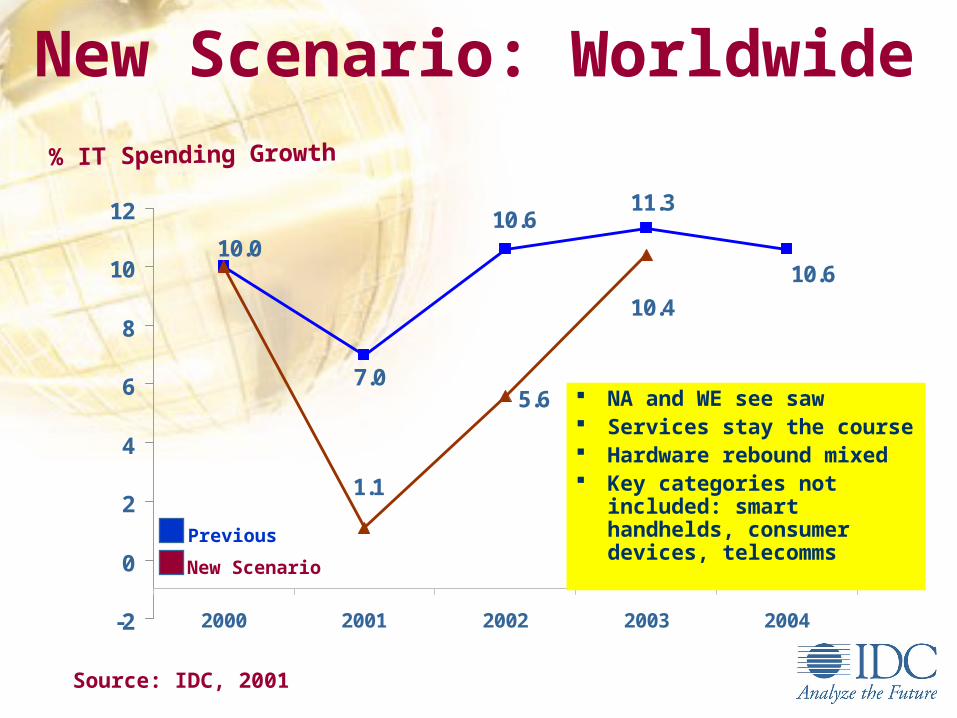

New Scenario: Worldwide

5.6

10.010.6

11.3

10.6

7.0

1.1

10.4

-2

0

2

4

6

8

10

12

2000 2001 2002 2003 2004

% IT Spending Growth

Source: IDC, 2001

Previous

New Scenario

NA and WE see saw Services stay the course Hardware rebound mixed Key categories not

included: smart handhelds, consumer devices, telecomms

PC Spending WW

Source: IDC, 2001

Economy, weak consumer sales in Europe, market saturation in the US, and slowdown in developing regions had already taken a toll

Portable replacements of desktops a long term driver

Windows XP not a major upgrade impetus

Commercial replacement cycles elongatingPrevious Forecast New Scenario

Growth

PCs: Already Down

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2000 2001 2002 2003

Server Spending WW

Source: IDC, 2001

The economy had already turned the market negative

Price declines take their toll

Entry server market flattens out

“Mainframes” hold their own

New technology at risk McKinley will help out in

2002Previous Forecast New Scenario

Growth

Servers: Transition Ahead

-10%

-5%

0%

5%

10%

2000 2001 2002 2003

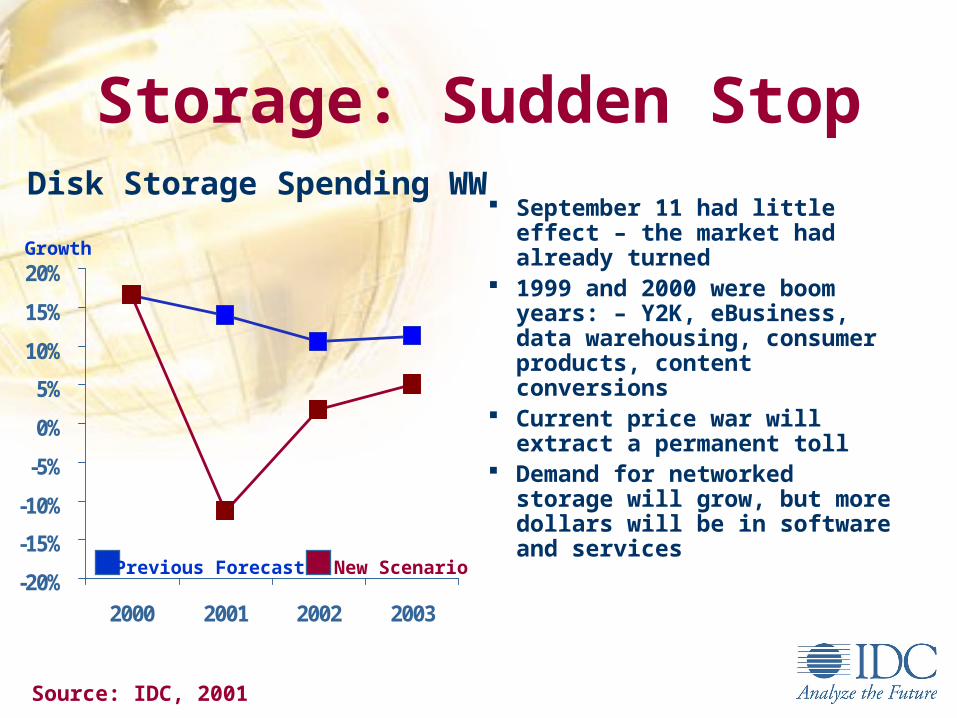

Disk Storage Spending WW

Source: IDC, 2001

September 11 had little effect – the market had already turned

1999 and 2000 were boom years: – Y2K, eBusiness, data warehousing, consumer products, content conversions

Current price war will extract a permanent toll

Demand for networked storage will grow, but more dollars will be in software and services

Previous Forecast New Scenario

Growth

Storage: Sudden Stop

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2000 2001 2002 2003

Printer Spending WW

Source: IDC, 2001

PC still drive printer shipments

Worst downturn as a result of the economy, not Sept. 11

Inkjet tied to consumer confidence; laser to commerce spending

High growth areas – wireless, photo, color laser – still to small to impact totals

Printer base aging – may drive an up tick

Previous Forecast New Scenario

Growth

Printers: Tied To PCs

-15%

-10%

-5%

0%

5%

10%

2000 2001 2002 2003

Network Equip. Spending WW

Source: IDC, 2001

Dot-com and CLEC implosion caused more problems than Sept. 11

New spending will focus on upgrades/add-ons

Wireless should get a boost Government Intervention to

solve congestion could help Spike in videoconferencing

equipment too small to make a difference

Previous Forecast New Scenario

Growth

Networking: Quick Spike

0%

5%

10%

15%

20%

2000 2001 2002 2003

Semiconductor Spending WW

Source: IDC, 2001

The worst year for semiconductors was already underway

A slowed economy will simply depress sales more

Inventories still haven’t cleared out of the channel

Wireless will lead the rebound Price cuts are not generating

demand Networking market holding up

– but opaqueNew Scenario

Growth

Semis: Paying The Price

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

96 97 98 99 00 01 02

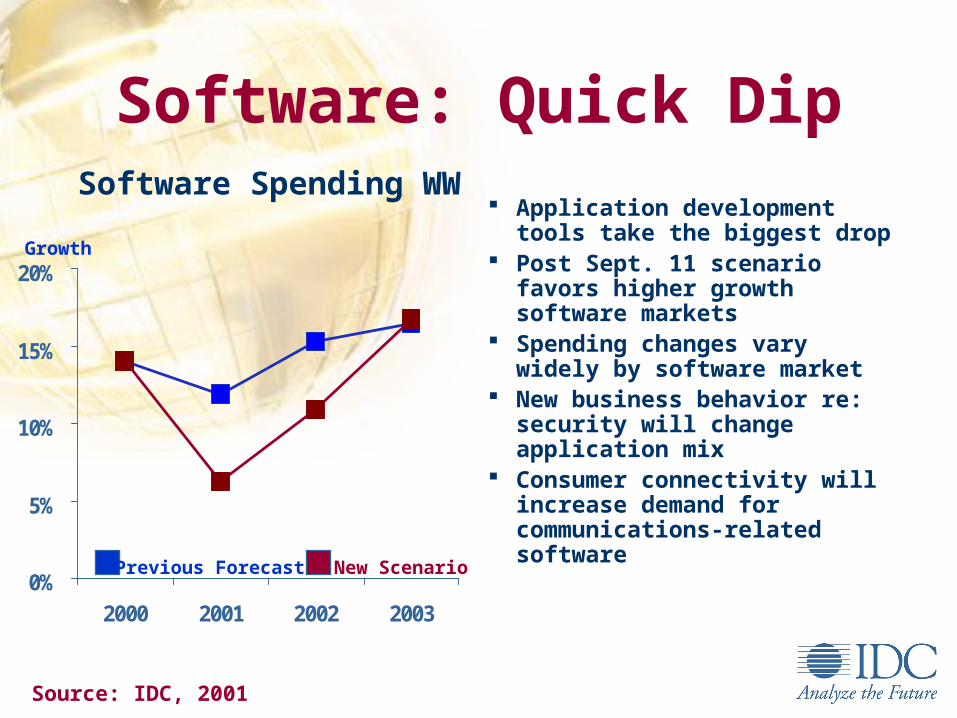

Software Spending WW

Source: IDC, 2001

Application development tools take the biggest drop

Post Sept. 11 scenario favors higher growth software markets

Spending changes vary widely by software market

New business behavior re: security will change application mix

Consumer connectivity will increase demand for communications-related softwarePrevious Forecast New Scenario

Growth

Software: Quick Dip

0%

5%

10%

15%

20%

2000 2001 2002 2003

Services Spending WW

Source: IDC, 2001

Device-related services down, but outsourcing, network consulting, and contract-based services less affected

Europe remains strong; US stays above 7.5% growth

Projects coming in smaller chunks, but pent-up demand to start hitting in 2003 in systems integration, CRM, supply chain servicesPrevious Forecast New Scenario

Growth

Services: Industry Fly Wheel

5%

10%

15%

2000 2001 2002 2003

Telecomms Spending WW

Source: IDC, 2001

The market is as big as IT, dominated by voice

No discernible effect from Sept. 11

Most growth outside US, which has been hit by economy, price wars, excess capacity, and CLEC implosion

Wireless is high growth but less than 15% of the market

Previous Forecast New Scenario

Growth

Telecomms: Status Quo

4%

8%

12%

2000 2001 2002 2003

Relative Size of IT Spending

Ave

rage

Bu

sin

ess

Gro

wth

, 200

2/20

01

Construction

Education

Transport

Health

Utilities

Insurance

Govmt

Comms/Media

Services

Banking/Finance

Average Share of US Business Market

Lower Growth

No Change

Higher Growth

Source : IDC’s Enterprise Technology Trends 2001

Verticals Post Sept. 11 Growth

Process Mfg/Resource

Retail Whol

Discrete Mfg

New Scenario: Worldwide

% IT Spending Growth

Source: IDC, 2001

Previous

New Scenario

NA and WE see saw Services stay the course Hardware rebound mixed Key categories not

included: smart handhelds, consumer devices, telecomms

5.6

10.010.6

11.3

10.6

7.0

1.1

10.4

-2

0

2

4

6

8

10

12

2000 2001 2002 2003 2004

New Scenario: North America

% IT Spending Growth

Source: IDC, 2001, Nov 11 Update

Previous

New Scenario

Price wars haven’t helped Canada doesn’t fall as far

as US Services and software

rebound helps most

4.1

12.0

9.5

11.3

10.5

5.7

-1.8

10.8

-2

0

2

4

6

8

10

12

2000 2001 2002 2003 2004

New Scenario: Western Europe

% IT Spending Growth

Source: IDC, 2001

Previous

New Scenario

Europe already deals with terrorism

Causes of downturn are mingled

Hardware most affected Mixed sector results –

Govt. up, transport down

12.0

10.2 10.5

10.2

8.4

6.1

4.9

8.7

0

2

4

6

8

10

12

2000 2001 2002 2003 2004

New Scenario: Asia Pacific

% IT Spending Growth

Source: IDC, 2001

Previous

New Scenario

Japan used to a down economy

AP spring back in 2003, China, India hold up region

Consumer exports hit mildly form Sept. 11

Domestic IT unaffected

8.0

12.0

13.1

11.810.8

8.2

2.7

11.9

2

4

6

8

10

12

14

2000 2001 2002 2003 2004

Market Opportunities by CountryTotal IT Spending, US$ MillionsTotal IT Spending, US$ Millions

Source: IDC Asia/Pacific, October 2001

0 5,000 10,000 15,000 20,000 25,000 30,000

Others

Vietnam

Indonesia

Philippines

Thailand

New Zealand

Malaysia

Hong Kong

Singapore

India

Taiwan

Korea

Australia

PRC

200220012000

The Case For A Downside View

Risk of further terrorist attacks

Self-reinforcing global downturn

Rising unemployment

Deflation

US$/stock market crash

A minority but not miniscule opinion

The Shipwreck Scenario

Beacon Shipwreck

Terrorism No major Possibly more

Reaction Back to normal Permanent change

Economy Rebound Q2 No rebound till 2003

US GDP Just positive 2001 Negative all 2002

WE GDP 1%-2% 2002 Below 1% 2002

Housing Starts stay up Market falls

Unempl. Nothing said Over 7% US

Two Scenarios: Worldwide

% IT Spending Growth

Source: IDC, 2001

Software has bad 2002 Services impact in 2002

& 2003 $275 billion

permanently lost between 2002-2004

Beacon

Shipwreck

1.1

10.411.5 11.2

5.6 7.6

10.2

-0.6

10.5

-2

0

2

4

6

8

10

12

2001 2002 2003 2004 2005

Two Scenarios: US

% IT Spending Growth

Source: IDC, 2001

Same trajectory as worldwide but steeper dip

Beacon

Shipwreck

-2.1

10.411.5 11.2

5.6

2.5

10.5

-3.7

10.3

-4

0

4

8

12

2001 2002 2003 2004 2005

PC Spending WW

PCs: Shipwreck Scenario

Source: IDC, 2001

2003 market 70% of 2000 market under “shipwreck,” US almost half

Weak consumer sales in Europe, market saturation in the US

Windows XP not a major upgrade impetus

Commercial replacement cycles elongate

Growth

Beacon

Shipwreck

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2001 2002 2003 2004

Spending WW

Servers & Storage: Shipwreck Scenario

Source: IDC, 2001

Pent-up demand drives rebound when economy improves

Some regions defy lower economic growth assumptions

Market not back to 2000 levels until 2004

Growth

Beacon

Shipwreck

-15%

-10%

-5%

0%

5%

10%

15%

2001 2002 2003 2004

Software Spending WW

Software: Shipwreck Scenario

Source: IDC, 2001

Big difference if recovery delayed Cancellations, not delays Some pent-up demand

dissipates

Long term new world order for software

New Scenario

Growth

Beacon

Shipwreck

0%

5%

10%

15%

20%

2001 2002 2003 2004

Services Spending WW

Services: Shipwreck Scenario

Source: IDC, 2001

Even outsourcing falls off

Other regions are impacted more by the economy

Support revenues flatten and stay there

Project cutbacks in 2002 affect 2003 revenue

Growth

Beacon

Shipwreck

0%

5%

10%

15%

2001 2002 2003 2004

Other

Same trajectory in other regions – delay of upturn, no “make-up”

Hardware “drag” matters less in the shipwreck scenario

Exchange rates not factored in – but would make a difference

Insights

Sept. 11 had little impact on many markets – the economy had already done its job

Price wars weren’t creating demandServices is the great flywheelCurrency exchange adds an impossible

dimension

E.g., Mobile Internet

Drivers of Pent-Up Demand

Source: IDC, 2001

Postponed Enterprise Applications

eBusiness Integration 71% say important 21% have it

New software architectures Collaboration Distribution

Background processing Mobile eBusiness (see

chart at left)

% of Total in 2003

Should Be Much Higher

0%

10%

20%

30%

40%

Mobile Users Mobile Sites

Caveats

These are scenarios, not final forecastsNumbers may change over timeAssumptions may change over timeExchange rates were held constantBeware of “irrational gloom” as counter to

“irrational exuberance”

* For more details by sector or region, contact the specific programs

Recommendations

Plan for a rebound in mid 2002 – with the possibility it could come sooner!

Stay close to your customers, counter FUD with RAS

Use the IDC Beacon forecasts; keep the “Shipwreck” scenario only for contingency planning

Upcoming IDC Events