irish investment market review - sherry fitzgerald blog

TRANSCRIPT

Irish Investment Market Review suMMeR 2013

2 Summer 2013 | Irish Investment market review

The following report provides an overview of the Irish investment market. The Irish investment market has witnessed remarkable performance despite the lingering challenges that remain as the economy transitions towards stabilisation. The opening section provides an overview of the economic background followed by a comprehensive review of the Irish investment market. The total volume of investment for the first half of 2013 stood at approximately €610m; this compares favourably to a total of €624m transacted for 2012 as a whole. Notably, activity remains concentrated on the capital and in particular Dublin city centre.

3 Summer 2013 | Irish Investment market review

The european union’s finance ministers have confirmed a deal which will give Ireland more time to repay european loans from its eu-ImF bailout fund. Subsequently, this will extend the term of the average european loan from 12.5 years to 19.5 years. This applies to loans from the european Financial Stabilisation mechanism (eFSm), from which Ireland has borrowed €21.7 billion. Consequently, Ireland will have a higher capacity to attain finance for repayments. That said, the overall cost of Ireland’s bailout will increase marginally; however the interest rates to be applied will be fixed so the increases will be minimal.

According to the latest exchequer figures published by the Department of Finance, tax revenues in the seven month period to the end of July totalled €21,032m; an increase of 3.5% on the same period in 2012 and marginally above target. Tax revenues remain ahead of target, driven by

corporation taxes, while other taxes such as income tax and VAT performed weaker than expected. The overall exchequer deficit stood at €5,167m at the end of July, compared with a deficit of €9,126m in the same period in 2012. exchequer returns for July show that the government is still on track to beat its 7.4% of GDP deficit target.

Despite the Irish economy’s relative resilience to external turbulence, the latest preliminary figures from the Central Statistics Office (CSO) reveal that the Irish economy declined by 0.6% in the opening quarter of 2013.

economic Background

Figure 1

Annual % change Gross Domestic Product (GDP)

Source: CSO

Tax revenues remain ahead of target

As a small open economy, the performance of the Irish economy is inherently impacted by the external environment. In recent years, exports have been the main driver of economic growth in Ireland. However, on-going weakness in external demand in many of Ireland’s main trading partners, particularly in the UK and the Eurozone, has resulted in a marked slowdown in exports of goods and services. Having said that, on a positive note, the Euro area returned to positive growth in the second quarter of 2013; having contracted during the previous six quarters. GDP rose by 0.3% over the three month period to June. Furthermore, moderate improvements in employment have been observed, while significant progress has been made in terms of the EU-IMF bailout.

The decline was the third consecutive quarter of contraction in GDP. Simultaneously, the volume of GNP rose by 2.9% in the three month period compared with the previous quarter. Furthermore, on a year-on-year basis, GNP saw a rise of 6.1%.

Growth figures for 2012 have also been revised back to 0.2% from the previous estimate of 0.9%.

exports of goods and services dropped by 3.2% in the quarter and 4.1% in the year. This represents the first annual decline since the final quarter of 2009 and reflects weak demand in export markets at present. In addition, imports recorded a decline of 1.0% on a quarterly basis.

Domestic demand continues to decline, with the majority of measures declining during the three month period. Personal consumption, accounting for approximately two thirds of domestic demand, fell 3.0% on a seasonally adjusted basis in the quarter and dropped 1.6% on a twelve month basis. In relation to the other components of domestic demand, capital investment fell by 7.4% in the quarter; moreover it was 19.8% lower in the year. Notably, investment figures are heavily influenced by the timing of purchases by aircraft leasing companies. On a more positive note, Government expenditure recorded a marginal increase, 0.3%, on a seasonally adjusted basis during quarter one.

4 Summer 2013 | Irish Investment market review

A comparison with the corresponding quarter in 2012 reveals a significant uplift in activity. Current investment volumes for the first half of 2013 almost exceed the total turnover for 2012 which stood at approximately €624m. With a number of significant transactions in the pipe line, investment asset volumes for 2013 are set to exceed €1bn for the first time since 2007. most notable, is the recent acquisition by Kennedy Wilson and partner of the Opera portfolio: a portfolio of 14 properties valued at €306m. The portfolio comprises a strong tenant list, including Bank of Ireland, KPmG, marks & Spencer and mason Hayes & Curran. Furthermore, the portfolio value is represented by 64%

office and 36% retail asset types. In addition, loan sales remain a key part of the market supply with key deals including the NAmA disposal of project Aspen.

The Irish investment market recovery is well underway, supported by improving sentiment and growing

demand from both international and domestic investors. The recovery, however, has not been uniform across the country or indeed sectors. There exists a two tier market; the Dublin market and the rest of Ireland. The Dublin market has out-performed the rest of the country, accounting for the majority of transactions during the first six months of the year. Furthermore, Dublin offices have performed demonstrably better and are driving the overall market at present. Investors are largely focusing their attention on central Dublin offices and residential buildings at the expense of the secondary market and other assets.

Irish Investment Volume: “strong momentum continues into second quarter”

Figure 2

Irish Investment market Turnover, €Bn

Source: DTZ Sherry FitzGerald research

Strong demand internationally and domestically

The opening quarter of 2013 saw the Irish investment market witness its strongest start to a year since 2007, with the total investment volume for quarter one reaching approximately €346m. This strong momentum continued into the second quarter with overall asset transactional turnover for the first half of 2013 standing at approximately €610m*.

With demand greater than supply for key sales, buyers must now compete on pricing and their ability to execute a transaction expediently. Furthermore, most positively, the supply of bank finance and the number of active lenders has now also increased.

The number of asset deals transacted during the first six months of the year (52) was significantly higher than the corresponding period in 2012 (13). Furthermore, the average transaction size stood at €11.7m up from €10.8m during the corresponding period in 2012.

The five largest deals transacted during the first half of 2013 accounted for €320m or 52% of the total value of transactions during the six month period. Included within this is the Gemini portfolio which has been signed and will close in the latter part of the year. The most notable investment deal during the second quarter was the sale of a prime residential scheme at Clancy Quay, Islandbridge, Dublin 8 to uS based investor Kennedy Wilson for approximately €82m. The property comprises a mix of residential and commercial income along with development and residential refurbishment angles.

* excludes loan sales and trading assets

* includes gemini portfolio deal

5 Summer 2013 | Irish Investment market review

Majority of investment focussed on Dublin city centre

Table 1

Table of Notable Transactions in H1 2013

Building Price (€) Quarter Sector Net Initial

Yield (%) Vendor Purchaser

Clancy Quay, Islandbridge, Dublin 8

€81m approx. Q2 mixed use _ Lloyds/

ulster BankKennedy Wilson

Bishops Sq., Dublin 2 €65m Q1 Office 9.87 IPuT/

ulster Bank

King Street Capital

The Gemini Portfolio €65m Q2 mixed use 8.19 ulster Bank Comer

Group

A&L Goodbody, Dublin 1

€58m Q1 Office 6.6 N/A IPuT

Airlines Portfolio €50m Q1 mixed use 7.16

Irish Airlines Pension

Fund

IPuT

Source: DTZ Sherry FitzGerald research

Figure 3

Investment Volume by Lot Size, H1 2013

Source: DTZ Sherry FitzGerald research

Irish Investment Volume

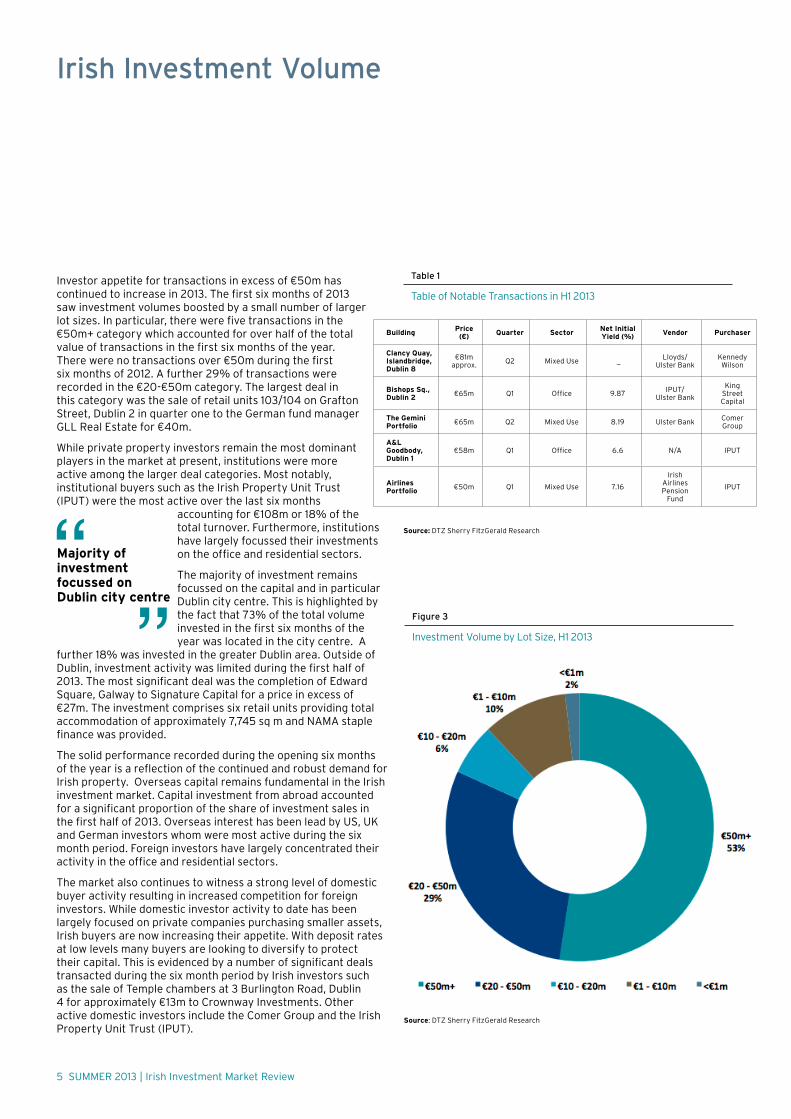

Investor appetite for transactions in excess of €50m has continued to increase in 2013. The first six months of 2013 saw investment volumes boosted by a small number of larger lot sizes. In particular, there were five transactions in the €50m+ category which accounted for over half of the total value of transactions in the first six months of the year. There were no transactions over €50m during the first six months of 2012. A further 29% of transactions were recorded in the €20-€50m category. The largest deal in this category was the sale of retail units 103/104 on Grafton Street, Dublin 2 in quarter one to the German fund manager GLL real estate for €40m.

While private property investors remain the most dominant players in the market at present, institutions were more active among the larger deal categories. most notably, institutional buyers such as the Irish Property unit Trust (IPuT) were the most active over the last six months

accounting for €108m or 18% of the total turnover. Furthermore, institutions have largely focussed their investments on the office and residential sectors.

The majority of investment remains focussed on the capital and in particular Dublin city centre. This is highlighted by the fact that 73% of the total volume invested in the first six months of the year was located in the city centre. A

further 18% was invested in the greater Dublin area. Outside of Dublin, investment activity was limited during the first half of 2013. The most significant deal was the completion of edward Square, Galway to Signature Capital for a price in excess of €27m. The investment comprises six retail units providing total accommodation of approximately 7,745 sq m and NAmA staple finance was provided.

The solid performance recorded during the opening six months of the year is a reflection of the continued and robust demand for Irish property. Overseas capital remains fundamental in the Irish investment market. Capital investment from abroad accounted for a significant proportion of the share of investment sales in the first half of 2013. Overseas interest has been lead by uS, uK and German investors whom were most active during the six month period. Foreign investors have largely concentrated their activity in the office and residential sectors.

The market also continues to witness a strong level of domestic buyer activity resulting in increased competition for foreign investors. While domestic investor activity to date has been largely focused on private companies purchasing smaller assets, Irish buyers are now increasing their appetite. With deposit rates at low levels many buyers are looking to diversify to protect their capital. This is evidenced by a number of significant deals transacted during the six month period by Irish investors such as the sale of Temple chambers at 3 Burlington road, Dublin 4 for approximately €13m to Crownway Investments. Other active domestic investors include the Comer Group and the Irish Property unit Trust (IPuT).

6 Summer 2013 | Irish Investment market review

Irish Investment Volume

Figure 4

Investment Volume by Location, H1 2013

Source: DTZ Sherry FitzGerald research

Investor appetite continues to grow with at least €6bn of capital looking to enter the

market. This, combined with rising stock levels expected in the latter half of 2013, should see investment asset sales top the €1bn mark for the first time since 2007.

michele Jackson, Director, DTZ Sherry FitzGerald

Furthermore, Irish Life, one of Ireland’s largest property investors, recently announced its intention to re-enter the investment market with a fund reported to be in the region of €200m. This is a positive development and a reflection of the opportunities and value present in the market.

On a further positive note, Green Property Holdings Ltd has established Ireland’s first real-estate investment trust (reIT). The newly listed fund known as Green reIT has raised over €300m in equity as part of its admission to the Irish market and aims to spend approximately half of the fund this year as it creates a property portfolio consisting of commercial property in Ireland. Furthermore, following the successful launch of the Green reIT; WK Nowlan, an Irish property management and advisory firm, and Willett Companies, an American investment company, have announced its plans to launch a €300m reIT in the autumn.

7 Summer 2013 | Irish Investment market review

Investment by sector

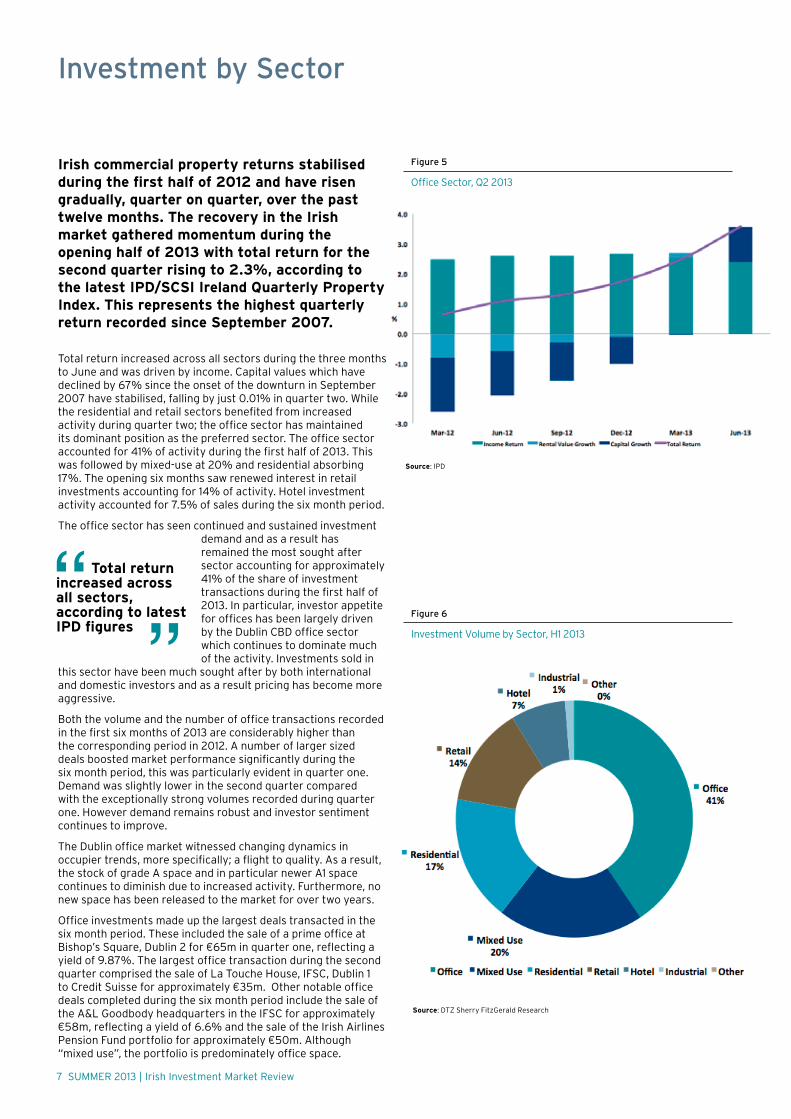

Irish commercial property returns stabilised during the first half of 2012 and have risen gradually, quarter on quarter, over the past twelve months. The recovery in the Irish market gathered momentum during the opening half of 2013 with total return for the second quarter rising to 2.3%, according to the latest IPD/SCSI Ireland Quarterly Property Index. This represents the highest quarterly return recorded since September 2007.

Total return increased across all sectors during the three months to June and was driven by income. Capital values which have declined by 67% since the onset of the downturn in September 2007 have stabilised, falling by just 0.01% in quarter two. While the residential and retail sectors benefited from increased activity during quarter two; the office sector has maintained its dominant position as the preferred sector. The office sector accounted for 41% of activity during the first half of 2013. This was followed by mixed-use at 20% and residential absorbing 17%. The opening six months saw renewed interest in retail investments accounting for 14% of activity. Hotel investment activity accounted for 7.5% of sales during the six month period.

The office sector has seen continued and sustained investment demand and as a result has remained the most sought after sector accounting for approximately 41% of the share of investment transactions during the first half of 2013. In particular, investor appetite for offices has been largely driven by the Dublin CBD office sector which continues to dominate much of the activity. Investments sold in

this sector have been much sought after by both international and domestic investors and as a result pricing has become more aggressive.

Both the volume and the number of office transactions recorded in the first six months of 2013 are considerably higher than the corresponding period in 2012. A number of larger sized deals boosted market performance significantly during the six month period, this was particularly evident in quarter one. Demand was slightly lower in the second quarter compared with the exceptionally strong volumes recorded during quarter one. However demand remains robust and investor sentiment continues to improve.

The Dublin office market witnessed changing dynamics in occupier trends, more specifically; a flight to quality. As a result, the stock of grade A space and in particular newer A1 space continues to diminish due to increased activity. Furthermore, no new space has been released to the market for over two years.

Office investments made up the largest deals transacted in the six month period. These included the sale of a prime office at Bishop’s Square, Dublin 2 for €65m in quarter one, reflecting a yield of 9.87%. The largest office transaction during the second quarter comprised the sale of La Touche House, IFSC, Dublin 1 to Credit Suisse for approximately €35m. Other notable office deals completed during the six month period include the sale of the A&L Goodbody headquarters in the IFSC for approximately €58m, reflecting a yield of 6.6% and the sale of the Irish Airlines Pension Fund portfolio for approximately €50m. Although “mixed use”, the portfolio is predominately office space.

Figure 5

Office Sector, Q2 2013

Figure 6

Investment Volume by Sector, H1 2013

Source: IPD

Source: DTZ Sherry FitzGerald research

Total return increased across all sectors, according to latest IPD figures

8 Summer 2013 | Irish Investment market review

Office capital values rose by 1.2%

The office sector delivered the strongest quarterly total return during quarter two of 2013; this marks the seventh consecutive quarter of positive total returns for Dublin offices. According to the latest IPD figures, total returns increased to 3.6% during quarter two; up from 2.5% recorded during the previous quarter. Income returns continue to drive returns. The office sector delivered the only positive capital growth across all sectors during the three month period. Overall office capital values rose sharply to 1.2% during the three months to June, this compares to a decline of 0.04% in quarter one and a fall of 1.5% during the corresponding quarter in 2012.

Furthermore, the second quarter of 2013 saw capital values for offices in Dublin’s Docklands grow by 5% and Central Dublin (excluding Docklands) values rise by 0.6%. Outside the Capital, capital values remain in negative territory, however, the rate of decline has slowed notably.

The sale of retail assets has rebounded strongly in 2013 as volumes totalled €83m at the end of June accounting for 14% of the total investment volume. A comparison with the corresponding period in 2012 reveals an 85% increase in activity levels and a significant increase in the number of deals transacted. Activity levels were boosted by the completion of edward Square in Galway to Signature Capital for a price in excess of €27m during the second quarter. The latest IPD figures reveal that while the retail sector remains the weakest performing sector, a 0.5% increase in total return was recorded during quarter two. Capital values on the other hand continue to decline, albeit at a much reduced rate. retail capital values declined by 1.5% during the three months to June.

The stabilisation of the Dublin residential market has attracted increased interest from investors, most notably overseas investors. residential investment activity improved during the second quarter of the year following a somewhat subdued start to the year.

Investment by sector

Figure 7

Irish Commercial market – Total return (Quarterly)

Source: IPD

At the mid point in the year, residential investment accounted for approximately 17% of the total investment activity during the six month period. Activity levels were boosted during the second quarter following the sale of the Clancy Quay residential development to uS investor Kennedy Wilson for in excess of €80m.

The second quarter of the year witnessed an improvement in supply levels with some larger residential investments including the iconic Alto Vetro residential tower in Grand Canal Dock coming to the market. The total figure for residential investment stock on the market, as at the end of quarter two, totalled approximately €97m, of which the majority of this is expected to transact by the end of the third quarter. A Canadian real estate firm CAPreIT, have acquired four apartment complexes in Dublin; rockbrook in Sandyford, Kings Court on North Kings Street, Dublin 1, Camac Crescent in Inchicore and Priorsgate in Tallaght; totalling over €40m.

There is good appetite from investors for well-located income producing residential blocks, encouraged by a doubling in the overall rental market from 2006 to 2011 as recorded in the census (145,317 persons renting from private landlords in 2006 versus 305,377 in 2012) and a general improvement in rental levels due to a more limited supply.

The appetite for industrial investment was subdued during the first six months of the year; this followed a similar trend in 2012. The industrial share of the total volume of investment transactions stood at just 1% at the end of quarter two. No industrial sales transacted during the second quarter. This followed a low level of activity in the opening quarter when just two small sized deals transacted in the greater Dublin area. According to the latest IPD results, total return was largely stable in the second quarter of 2013 rising by 1.9%. However, capital values remain weak declining by 1% during the three month period to June. This was offset by strong income growth of 2.9%, the strongest across all sectors in quarter two.

9 Summer 2013 | Irish Investment market review

Outlook for the Future

The past twelve months have witnessed a turnaround in the performance of the Irish investment market; supported by a number of successful key sales and an improvement in investor sentiment. In particular, the opening six months of 2013 has seen approximately €610m invested in Irish property across 52 transactions. This represents a notable uplift in the half-year performance compared with the corresponding period in 2012. The current investment volumes for the first half of 2013 almost exceed the turnover for 2012 as a whole which stood at approximately €624m. Looking to the remaining part of the year, the expectation is that the current momentum in the market will continue and that total transaction levels are expected to reach between €1.3bn and €1.5bn by year end 2013.

The latest IPD figures for the second quarter of 2013 show solid performance in the Irish investment market. Irish commercial property returns rose to 2.3% in the three months to June; the

highest return witnessed in almost six years.

Overall, the prime Dublin office sector remains the most popular asset type, accounting for the majority of transactions during the opening half of 2013. Within

the office market the ‘flight to quality’ has seen investors and lenders still focusing their attention on core assets at the expense of the secondary market. That said, we expect to see the continued improvement in the market to spill over into other sectors and indeed beyond Dublin. This is evidenced by increased levels of interest in retail property. Investors are no longer limiting themselves to Dublin and are considering other opportunities where the properties are in prime locations and have strong occupiers in place.

Availability of on-market opportunities are limited, particularly in the case of larger lot sizes. At the end of quarter two there was approximately €427.5m worth of commercial properties for sale; heavily weighted towards small to medium lot sizes. That said, the latter half of the year is expected to see supply levels increase notably with the disposal of Project ArC by Danske Bank and Project ulysses, which is a predominately office based portfolio, with values of €127m and €140m respectively.

Transaction levels expected to rise considerably by year end

In addition, loan sales remain a key part of the market supply and, in the latter part of 2013, are expected to see the volume of activity match asset sales.

The market continues to witness a strong level of both domestic and international buyer activity with many new partnerships marrying sector expertise with equity. many of these new entrants have put platforms in place and have a strategy to assemble a property portfolio that they can actively manage.

The capital gains tax window for investors to December 2013 should see a push from both buyers and sellers to transact before year end. The key for 2013 is to see an increase in supply in response to demand levels which would allow volume to increase further. This should facilitate the attraction of additional funders into the market and help the recovery to a more functioning market.

AuTHOrSmarian FinneganChief economist, Directorresearch+353 (0) 1 237 [email protected]

Siobhan moloneyresearch manager+353 (0) 1 237 [email protected]

michele JacksonDirector of Investments+353 (0) 1 639 [email protected]

Patricia WardDirector of Investments+353 (0) 1 639 [email protected]

rosemary CaseyDirector of Investments+353 (0) 1 639 [email protected]

About DTZ Sherry FitzGeraldDTZ Sherry FitzGerald is the sole Irish affiliate of DTZ, a uGL company, a global leader in property services. With Irish offices in Dublin, Cork, Galway, Limerick and an associated office in Belfast, we are the largest commercial property advisory network in Ireland and are part of Sherry FitzGerald Group, Ireland’s largest real estate adviser.We provide occupiers and investors around the world with best-in-class, end-to-end property solutions comprised of leasing agency and brokerage, integrated property management, capital markets, investment, asset management and valuation. DTZ has 47,000 employees including sub-contractors, operating across 217 offices in 53 countries. www.dtz.ie

© 2013

This report should not be relied upon as a basis for entering transactionswithout seeking specific, qualified, professional advice. It is intended as a general guide only. This report has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. While reasonable care has been taken in the preparation of the report, neither Sherry FitzGerald nor any of directors, employees or affiliates guarantees the accuracy or completeness of the information contained in the report. Any opinion expressed (including estimates and forecasts) may be subject to change without notice. No warranty or representation, express or implied, is or will be provided by Sherry FitzGerald, its directors, employees or affiliates, all of whom expressly disclaim any and all liability for the contents of, or omissions from, this document, the information or opinions on which it is based. Information contained in this report should not, in whole or part, be published, reproduced or referred to without prior approval. Any such reproduction should be credited to DTZ Sherry FitzGerald.