iri pulse report personal care · · 2015-11-10iri pulse report personal care ... iri retail...

TRANSCRIPT

PULSE REPORT

IRI Pulse Report Personal Care

Welcome to the Pulse H1 2015 edition for personal care. We hope you

find it useful. Please do not hesitate to contact us if you have any

questions or comments at [email protected].

H1 2015

IRIworldwide.com

PULSE REPORT

About the Report

2

• This personal care report is one of 10 super category reports designed to provide a high-

level comparison and analysis of retail markets across major countries in Europe.

• This report contains data gathered from countries throughout Europe. The market was split

into the following categories: deodorants, hair care, hair dye, body care, insect repellent,

oral care, body cleansing, facial care, sun care, sanitary products, feminine hygiene,

cosmetics, fragrances and shaving/hair removal.

• The report highlights key metrics such as total sales, market trends, category shares, and

winners and losers for Europe as a whole and for individual countries.

• The data has been sourced from IRI retail databases and Eurostat, the statistical branch of

administration for the European Commission.

• The countries included in the report are: France, Germany, Italy, the Netherlands, Spain

and the United Kingdom (UK).

• The market channels used for each country in this report are as follows:

Country Channels used

UK Hypermarkets, supermarkets, drugstores and impulse outlets

ES Hypermarkets, supermarkets, hard discounters, drugstores, including the Canary Islands

DE Hypermarkets, supermarkets, hard discounters and drugstores

NL Hypermarkets, supermarkets, hard discounters and drugstores

IT Hypermarkets, supermarkets, small self-service, hard discounters and drugstores

FR Hypermarkets and supermarkets

• For analytical purposes, the data sourced from available retail databases has been

consolidated to provide consistent results. However, for some countries it has not been

possible to source data pertaining to certain categories. When this has occurred, it has been

documented in the “Notes” section found at the end of the report.

PULSE REPORT

On the Radar

3

ECONOMIC FIGURES INFLUENCING CONSUMER BEHAVIOUR

Source: Eurostat, June 2015

The good news is that the first half of 2015 saw positive growth within the personal care category across Europe: +0.6% in value sales. While Germany and Spain have seen a positive trend, it is not the case for the Netherlands and France, where revenue sales have decreased. Some trends are transversal, strong growth in oral care and feminine hygiene, but each country exhibits its own specificities in terms of price evolution, channel dynamics and promotional activation.

POPULATIO

N IN

MILLIONS

UNEMPLOYMENT

(%)

AVERAGE 12

MONTHS

INFLATION

RATES

GDP IN MILLIONS

(€)

Jan.

2014

Jan.

2015

Avg.

2014

Jun.

2015

Avg.

2014

Jun.

2015 2013 2014

France 65.8 66.3 10.3 10.2 +0.7 +0.2 2 116 565 2 132 449

Germany 80.7 81.1 5.0 4.7 +0.9 +0.4 2 820 820 2 915 650

Italy 60.7 60.7 12.7 12.7 +0.3 +0.0 1 609 462 1 616 253

Netherlands 16.8 16.9 7.4 7.0 +0.5 +0.1 650 857 662 770

Spain 46.5 46.4 24.5 26.6 +0.0 -0.6 1 049 181 1 058 469

United

Kingdom 64.3 64.7 6.1 5.6 +1.7 +0.6 2 017 193 2 222 912

PULSE REPORT

701 787 855 718 719 808

500 570 530 507 487 550

1 083 1 189 1 255

1 099 1 098 1 215

3 012 3 181 3 171 3 438

3 093 3 265

1 516

1 606 1 561 1 442 1 479

1 639

1 637

1 811 1 856 1 724

1 645

1 816

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

30-mar-14 29-jun-14 28-sep-14 28-dic-14 29-mar-15 28-jun-15

Eu

ro

s, in

millio

ns

Period Ending

UK

France

Germany

Italy

Netherlands

Spain

GLOBAL TRENDS

4

TOTAL EUROPE +0.6%

-0.4%

2.2%

-0.1%

VALUE SALES IN MILLIONS (€)

Total EU 35 972

DE 12 967

FR 6 121

UK 7 041*

ES 3 099

IT 4 667

NL 2 075

TOTAL PERSONAL CARE VALUE SALES AND % CHANGE VERSUS PRIOR YEAR

*based on an exchange rate of €1.27 to the pound

+2.4%

-0.8%

-3.0%

TOTAL PERSONAL CARE VALUE SALES FOR THE LAST SIX QUARTERS

Source: IRI retail databases; period ending 28 June 2015

PULSE REPORT

Europe

5

5 279

4 538 4 206

3 599

2 824 2 787 2 550 2 481

2 237 2 038

Euro Sales

Oral Care Haircare Facial Care Body Cleansing

Shaving / Hair Removal Cosmetics Deodorants Body Care

Fragrances Sanitary Products

Eu

ros,

in m

illi

on

s

CATEGORY SHARE OF VALUE SALES IN THE LAST YEAR

Europe includes: France, Germany, Italy, the Netherlands, Spain and the United Kingdom

Source: IRI retail databases; period ending 28 June 2015

KEY TRENDS

• With a growth of 0.6% in value sales, the

personal care trend is positive in Europe. But,

this category is still underperforming

compared to fast moving consumer goods

(FMCG) which showed slight upward growth.

• However, the 0.6% increase makes it difficult

to identify different situations between

countries.

• In 2015, Germany and Spain saw positive

sales, while Italy and the UK stayed stable.

The Netherlands and France suffered a decline

in sales.

• The following pages will analyze different

trends in each country.

SHARE OF VALUE IN THE YEAR

Oral Care 14.7%

Hair Care 12.6%

Facial Care 11.7%

Body Cleansing 10.0%

Shaving / Hair Removal 7.8%

Cosmetics 7.7%

Deodorants 7.1%

Body Care 6.9%

Fragrances 6.2%

Sanitary Products 5.7%

Hair Dye 3.7%

Feminine Hygiene 3.0%

Sun care 2.5%

Insect Repellent 0.4%

PULSE REPORT

Euros, in millions

Europe

6

Europe includes: France, Germany, Italy, the Netherlands, Spain and the United Kingdom

Source: IRI retail databases; period ending 28 June 2015

TOP LOSERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

TOP WINNERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

103.3

87.5

77.4

69.4

55.1

0 50 100 150

Oral Care

Cosmetics

Feminine Hygeine

Body Care

Facial Care

Millions

5 279

4 538 4 206

3 599

2 824

2.0 -0.9

1.3 0.8 -2.2

Ora

l Care

Hair C

are

Facia

l Care

Body C

leansin

g

Shavin

g /

Hair

Rem

oval

Euro

s,

in m

illions

Euro Sales % € vs. YA

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

CATEGORY INSIGHTS

• The slight growth in personal care makes it

difficult to uncover trends among specific

categories.

• Oral care is still the most dynamic

category thanks to multiple marketing

activations (promotion, media and

innovation) and because of its potential for

consumer recruitment across Europe.

• Facial care also managed to increase sales,

specifically in France, Spain and Germany.

• The situation is difficult for one of the

largest categories, hair care, more

specifically in France, Italy and the

Netherlands.

• Shaving and hair removal are declining

with the beard trend being the driving

factor. Without innovation in this market,

sales will continue to decline.

- 34.0

- 39.6

- 40.7

- 49.2

- 62.8

-70 -50 -30 -10

Deodorants

Haircare

Hair Dye

Sun care

Shaving / Hair Removal

Euros, in millions

PULSE REPORT

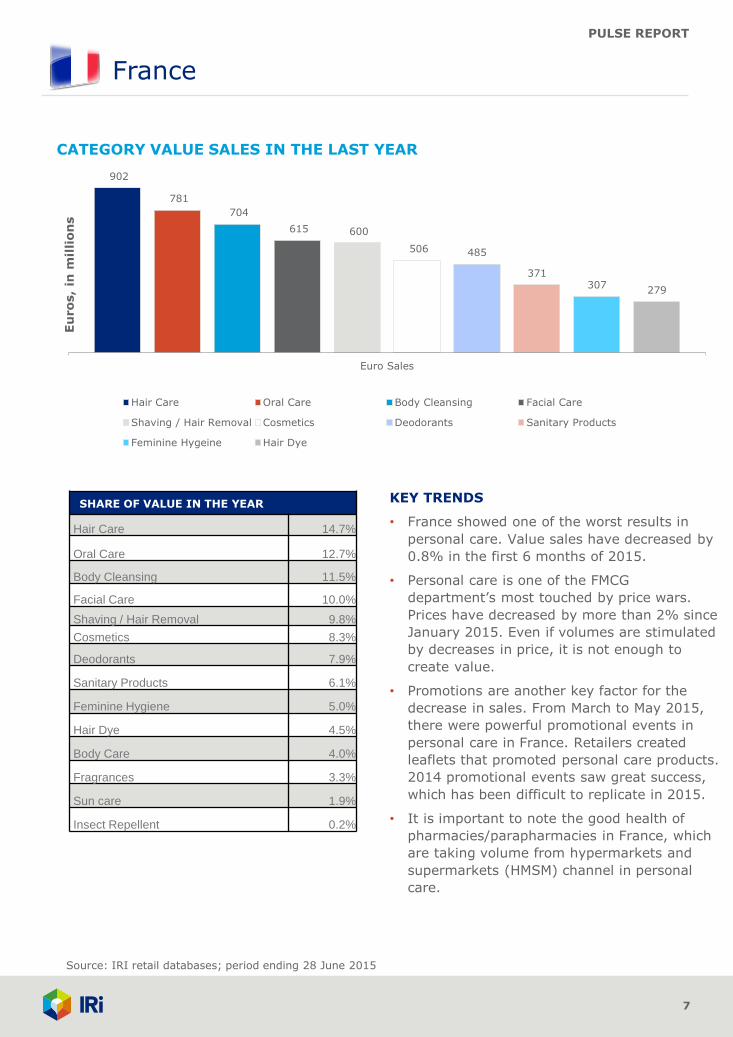

902

781

704

615 600

506 485

371 307

279

Euro Sales

Hair Care Oral Care Body Cleansing Facial Care

Shaving / Hair Removal Cosmetics Deodorants Sanitary Products

Feminine Hygeine Hair Dye

France

7

KEY TRENDS

• France showed one of the worst results in

personal care. Value sales have decreased by

0.8% in the first 6 months of 2015.

• Personal care is one of the FMCG

department’s most touched by price wars.

Prices have decreased by more than 2% since

January 2015. Even if volumes are stimulated

by decreases in price, it is not enough to

create value.

• Promotions are another key factor for the

decrease in sales. From March to May 2015,

there were powerful promotional events in

personal care in France. Retailers created

leaflets that promoted personal care products.

2014 promotional events saw great success,

which has been difficult to replicate in 2015.

• It is important to note the good health of

pharmacies/parapharmacies in France, which

are taking volume from hypermarkets and

supermarkets (HMSM) channel in personal

care.

Source: IRI retail databases; period ending 28 June 2015

Eu

ros,

in m

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

SHARE OF VALUE IN THE YEAR

Hair Care 14.7%

Oral Care 12.7%

Body Cleansing 11.5%

Facial Care 10.0%

Shaving / Hair Removal 9.8%

Cosmetics 8.3%

Deodorants 7.9%

Sanitary Products 6.1%

Feminine Hygiene 5.0%

Hair Dye 4.5%

Body Care 4.0%

Fragrances 3.3%

Sun care 1.9%

Insect Repellent 0.2%

PULSE REPORT

France

8

TOP LOSERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

TOP WINNERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

22.4

5.4

2.9

0 10 20

Feminine Hygeine

Facial Care

Deodorants

Millions

Source: IRI retail databases; period ending 28 June 2015

Euros, in millions

902

781

704

615 600

-2.4 -0.3 -0.2 0.9

-3.4

Hair C

are

Ora

l Care

Body C

leansin

g

Facia

l Care

Shavin

g /

Hair

Rem

oval

Euro

s,

in m

illions

Euro Sales % € vs. YA

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

CATEGORY INSIGHTS

• Declining sales for personal care in France

is transversal across categories which has

created a negative trend in sales.

• For example, hair care, which is

particularly impacted by price decreases

(-3.7% on H1 in HMSM). During 2015

there were fewer impactful innovations

versus 2014.

• Value sales in oral care which was one of

the most dynamic categories is now

slightly decreasing, mainly because of

toothpaste.

• The shaving category decline is not new,

but losses are still important in France;

French men are using less shaving

products because of the beard effect.

- 4.3

- 7.8

- 10.8

- 21.3

- 22.2

-25 -15 -5

Sanitary Products

Body Care

Sun Care

Shaving / Hair Removal

Hair Care

Euros, in millions

PULSE REPORT

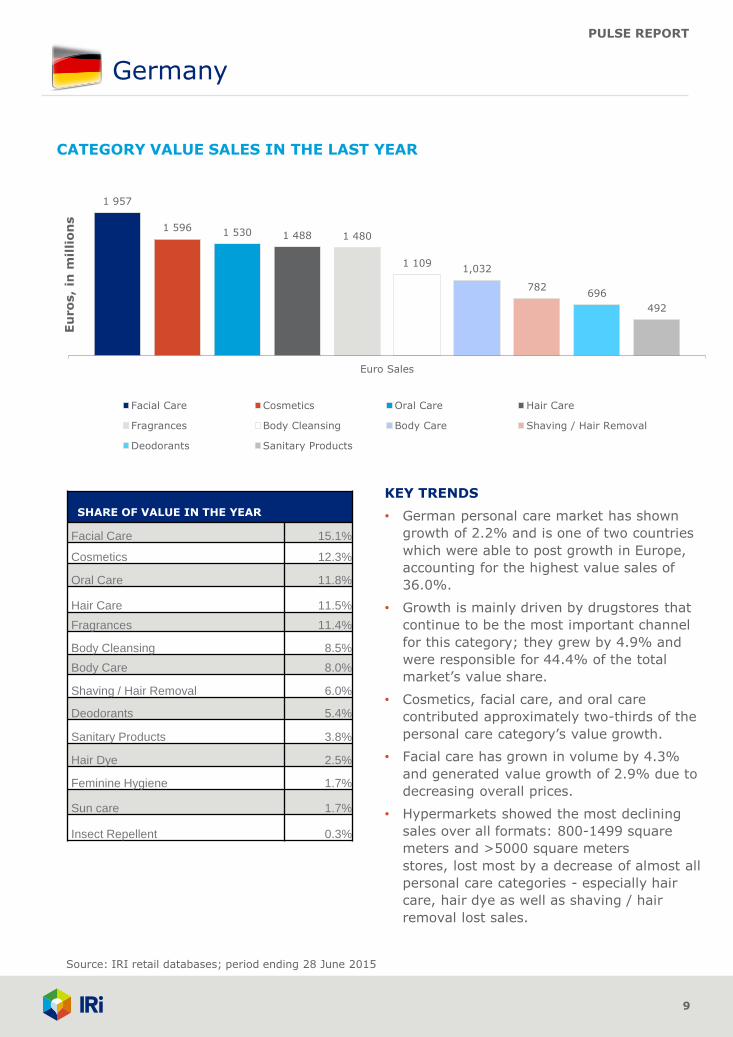

1 957

1 596 1 530 1 488 1 480

1 109 1,032

782 696

492

Euro Sales

Facial Care Cosmetics Oral Care Hair Care

Fragrances Body Cleansing Body Care Shaving / Hair Removal

Deodorants Sanitary Products

Germany

9

Source: IRI retail databases; period ending 28 June 2015

CATEGORY VALUE SALES IN THE LAST YEAR

Eu

ros,

in m

illi

on

s

SHARE OF VALUE IN THE YEAR

Facial Care 15.1%

Cosmetics 12.3%

Oral Care 11.8%

Hair Care 11.5%

Fragrances 11.4%

Body Cleansing 8.5%

Body Care 8.0%

Shaving / Hair Removal 6.0%

Deodorants 5.4%

Sanitary Products 3.8%

Hair Dye 2.5%

Feminine Hygiene 1.7%

Sun care 1.7%

Insect Repellent 0.3%

KEY TRENDS

• German personal care market has shown

growth of 2.2% and is one of two countries

which were able to post growth in Europe,

accounting for the highest value sales of

36.0%.

• Growth is mainly driven by drugstores that

continue to be the most important channel

for this category; they grew by 4.9% and

were responsible for 44.4% of the total

market’s value share.

• Cosmetics, facial care, and oral care

contributed approximately two-thirds of the

personal care category’s value growth.

• Facial care has grown in volume by 4.3%

and generated value growth of 2.9% due to

decreasing overall prices.

• Hypermarkets showed the most declining

sales over all formats: 800-1499 square

meters and >5000 square meters

stores, lost most by a decrease of almost all

personal care categories - especially hair

care, hair dye as well as shaving / hair

removal lost sales.

PULSE REPORT

Germany

10

TOP LOSERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

TOP WINNERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

Source: IRI retail databases; period ending 28 June 2015

- 1.7

- 3.0

- 8.6

- 10.5

- 15.3

-20 -10 0

Deodorants

Shaving / Hair Removal

Hair Dye

Insect Repellent

Sun Care

63.4

59.4

54.2

37.8

32.6

0 40 80

Cosmetics

Oral Care

Facial Care

Body Care

Body Cleansing

Euros, in millions

1 957

1 596 1 530 1 488 1 480

2.8 4.1

4.0

0.7 1.8

Facia

l C

are

Cosm

etics

Ora

l C

are

Hair C

are

Fra

gra

nce

s

Eu

ros,

in m

illio

ns

Euro Sales % € vs. YA

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

CATEGORY INSIGHTS

• All top five personal care categories (with a

value share of about 62%) were able to

increase sales and drove personal care’s

market growth.

• Cosmetics’ growth was primarily driven by

drugstores which generated a value growth

of 6.4% (53.4 million €), mainly due to an

increase in non promotional sales.

• Facial, eye and lip drove value growth within

cosmetics while nail cosmetic declined.

• Oral care’s value growth of 4.1% was mainly

driven by dental care products. Growth was

due to increased promotional (+10.2%) and

non promotional (+2.1%) sales – also

toothbrushes' non promotional sales showed

growth by 8.5%.

• Facial care was primarily driven by face

cream which has approximately 70% value

share within facial care, but face cleansing

showed the highest value growth in this

category followed by lip care which showed

the highest change over last year, with

growth of 18.1%.

Euros, in millions

PULSE REPORT

679

617

513

447 437 413

309 309 259 240

Euro Sales

Oral Care Hair Care Body Cleansing Sanitary Products

Facial Care Shaving / Hair Removal Feminine Hygeine Deodorants

Cosmetics Body Care

Italy

11

KEY TRENDS

• In the first half of 2015, food and drinks

departments drove growth. Personal care

showed a positive trend for six consecutive

months, both in terms of value and volume.

• In these first six months of 2015, the

promotional pressure for FMCG remained at

the same level as in 2014; the depth of

discount remained high but did not grow

further.

• In personal care prices decreased even

while FMCG prices increased during the

past six months.

• Although prices for FMCG are still declining

due to strong competition between retail

channels, revenue remains positive.

• Private labels market share for FMCG

remains the same versus 2014 (value share

9.9%).

Source: IRI retail databases; period ending 28 June 2015

CATEGORY VALUE SALES IN THE LAST YEAR

Eu

ros,

in m

illi

on

s

SHARE OF VALUE IN THE YEAR

Oral Care 14.5%

Hair Care 13.2%

Body Cleansing 11.0%

Sanitary Products 9.6%

Facial Care 9.4%

Shaving / Hair Removal 8.9%

Feminine Hygiene 6.6%

Deodorants 6.6%

Cosmetics 5.5%

Body Care 5.1%

Hair Dye 3.6%

Fragrances 3.0%

Sun care 2.0%

Insect Repellent 0.9%

PULSE REPORT

Italy

12

TOP LOSERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

TOP WINNERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

Source: IRI retail databases; period ending 28 June 2015

- 5.2

- 10.0

- 14.4

- 17.7

- 18.7

-20 -10 0

Deodorants

Sanitary Products

Body Cleansing

Hair Care

Shaving / Hair Removal

18.1

14.4

12.8

10.4

2.3

0 10 20

Cosmetics

Fragrances

Body Care

Feminine Hygeine

Oral Care

Millions Euros, in millions

679

617

513

447 437

0.3 -2.8 -2.7 -2.2 0.3

Ora

l C

are

Hair

Ca

re

Bo

dy C

lea

nsin

g

Sa

nitary

Pro

du

cts

Fa

cia

l C

are

Eu

ros,

in m

illio

ns

Euro Sales % € vs. YA

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

CATEGORY INSIGHTS

• Categories that are viewed as more of a

commodity such as body care (bath, shower,

soaps, deodorants), hair care (shampoo and

hair conditioner) and oral care (toothpastes

and mouthwashes) are increasing their market

share in the drugstore at the expense of

categories more specialized like make-up and

perfumes.

• Hair care (shampoo, hair conditioner and

styling products) show negative performances

even though promotional activity and price

cuts were higher in 2015 than 2014. In the

hair conditioner sub-category only rinse on

and off are increasing. On the contrary,

traditional conditioners are decreasing.

• Within the body cleansing category, shower is

the only sub-category with a positive trend.

Sales are negative for bath and soaps (bar

and liquid).

• Body care: in body cream not all segments

show negative trends like multipurpose or

fluid cream, but exfoliating and firming are

showing positive performance but their market

share in the total body cream is still low.

Euros, in millions

PULSE REPORT

303

266 264

218

181 160

148 147

123 109

Euro Sales

Hair Care Cosmetics Oral Care Facial Care

Body Cleansing Fragrances Body Care Deodorants

Shaving / Hair Removal Sanitary Products

The Netherlands

13

KEY TRENDS

• The personal care situation is still

negative in the Netherlands. The

economic context there remains tough

despite first encouraging economical

indicators.

• Luxury brands and segments in

personal care show a positive index.

This can be explained by the fact that

consumers are tired of the economic

situation and want to indulge

themselves.

• Sun care is one of the few segments in

personal care that show positive

results, due to the abundant sunny

days the Netherlands had during that

period.

Source: IRI retail databases; period ending 28 June 2015

CATEGORY VALUE SALES IN THE LAST YEAR

Eu

ros,

in m

illi

on

s

SHARE OF VALUE IN THE YEAR

Hair Care 14.6%

Cosmetics 12.8%

Oral Care 12.7%

Facial Care 10.5%

Body Cleansing 8.7%

Fragrances 7.7%

Body Care 7.1%

Deodorants 7.1%

Shaving / Hair Removal 5.9%

Sanitary Products 5.2%

Sun Care 3.1%

Hair Dye 2.9%

Feminine Hygiene 0.9%

Insect Repellent 0.6%

PULSE REPORT

The Netherlands

14

TOP LOSERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

TOP WINNERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

Source: IRI retail databases; period ending 28 June 2015

2.8

2.7

0.4

0 1 2 3

Body Care

Feminine Hygeine

Insect Repellent

Millions Euros, in millions

303

266 264

218

181

-3.4 -0.9

-1.4 -4.8

-6.7

Hair C

are

Cosm

etics

Ora

l C

are

Facia

l C

are

Bo

dy C

lea

nsin

g

Eu

ros,

in m

illio

ns

Euro Sales % € vs. YA

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

CATEGORY INSIGHTS

• During the past period, personal care was

losing sales in the Netherlands.

• An explanatory factor for this is the still

growing market of high, and low-end retail

(e.g. budget stores). The developing

market has impacted the performance of

traditional channels.

• Low end retail is growing rapidly in the

Netherlands, because of the low prices

compared to drugstores and

supermarkets.

• In addition, the promotional pressure

within drugstores is still rising, it is around

65% for total personal care. For some

segments there are little base sales to

track, since almost everything is sold on

promotion (e.g. hair coloring).

- 8.1

- 9.1

- 10.7

- 10.9

- 13.1

-15 -10 -5 0

Deodorants

Hair Dye

Hair Care

Facial Care

Body Cleansing

Euros, in millions

PULSE REPORT

Spain

15

KEY TRENDS

• Spain has the best year-over-year

performance in the personal care category

in Europe. It has increased its value sales

versus the previous year by 2.4%.

• Consumption in Spain has been growing

since the beginning of this year, and it has

been a driver for the personal care

category.

• Hair care, the most important category in

personal care in H1 2015, had weak year-

over-year performance. It has decreased in

value sales by 2.8%.

• The three categories with the greatest gain

in value sales were oral care, body

cleansing and fragrances.

Source: IRI retail databases; period ending 28 June 2015

493

370

300 275

259 256 255 216

184 161

Euro Sales

Hair Care Oral Care Body Cleansing Sanitary Products

Facial Care Shaving / Hair Removal Fragrances Deodorants

Body Care Cosmetics

Eu

ros,

in m

illi

on

s

SHARE OF VALUE IN THE YEAR

Hair Care 15.9%

Oral Care 11.9%

Body Cleansing 9.7%

Sanitary Products 8.9%

Facial Care 8.3%

Shaving / Hair Removal 8.3%

Fragrances 8.2%

Deodorants 7.0%

Body Care 5.9%

Cosmetics 5.2%

Hair Dye 4.2%

Sun care 3.9%

Feminine Hygiene 2.4%

Insect Repellent 0.1%

CATEGORY VALUE SALES IN THE LAST YEAR

PULSE REPORT

Spain

16

TOP LOSERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

TOP WINNERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

Source: IRI retail databases; period ending 28 June 2015

- 1.2

- 2.8

- 6.9

-8 -4 0

Hair Dye

Hair Care

Shaving / Hair Removal

21.7

10.7

10.1

9.6

8.0

0 10 20

Oral Care

Body Cleansing

Fragrances

Cosmetics

Facial Care

Millions Euros, in millions

493

370

300 275

259

-0.6 6.2 3.7 0.8 3.2

Hair C

are

Ora

l C

are

Bo

dy C

lea

nsin

g

Sanitary

Pro

ducts

Fa

cia

l C

are

Eu

ros,

in m

illio

ns

Euro Sales % € vs. YA

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

CATEGORY INSIGHTS

• There is a positive change in year-over-

year performance the Top 5 categories in

personal care. Only the biggest category,

hair care, is losing value sales.

• Potential growth is still important in Spain

in oral care, the second largest category in

value sales. This category is growing by

6.2% and has the greatest year-over-year

growth versus the other personal care

categories.

• The fragrances category is one of the most

important categories in personal care due

to ‘me too’ brands. This sub-category is

growing, because some manufacturers

have lowered prices and private labels

which have significant position (about the

12% of value market share) are growing.

Euros, in millions

PULSE REPORT

The United Kingdom

17

KEY TRENDS

• Total FMCG (excluding alcohol) fell by

1.3% in value sales during H1 2015 versus

H1 2014. Compared to this, personal care

sales were down 1.2%.

• FMCG through the traditional supermarket,

pharmacist and convenience trade is being

affected by a growing discount sector both

in the shape of Aldi and Lidl as well as the

bargain stores.

• The personal care sector was not helped by

the weather in 2015. Apart from a short

warm spell at the end of June,

temperatures were lower than in 2014.

• Volume on deal for the personal care

sector has not changed substantially. This

is slightly against the overall trend where

we have seen promotion levels falling

slightly for food.

• Volume sales are down in H1 for personal

care, falling faster than other categories,

but value sales have been supported to

some extent by higher prices. The price

war is not as fierce here as it is in food.

Source: IRI retail databases; period ending 28 June 2015

1 656

792 735 721 696 649 635

359 344 268

Euro Sales

Oral Care Body Cleansing Hair Care Facial Care

Deodorants Shaving / Hair Removal Body Care Hair Dye

Sanitary Products Sun care

Eu

ros,

in m

illi

on

s

SHARE OF VALUE IN THE YEAR

Oral Care 23.5%

Body Cleansing 11.2%

Hair Care 10.4%

Facial Care 10.2%

Deodorants 9.9%

Shaving / Hair Removal 9.2%

Body Care 9.0%

Hair Dye 5.1%

Sanitary Products 4.9%

Sun care 3.8%

Feminine Hygiene 2.1%

Insect Repellent 0.5%

CATEGORY VALUE SALES IN THE LAST YEAR

PULSE REPORT

The United Kingdom

18

Source: IRI retail databases; period ending 28 June 2015

TOP LOSERS: VALUE SALES CHANGE VERSUS A YEAR AGO (€)

TOP WINNERS: VALUE SALES CHANGE VERSU A YEAR AGO (€)

- 6.3

- 13.8

- 13.9

- 20.3

- 22.9

-25 -15 -5

Shaving / Hair Removal

Hair Dye

Sanitary Products

Sun care

Deodorants

26.0

16.2

15.8

13.3

2.9

0 10 20 30

Oral Care

Body Care

Feminine Hygeine

Body Cleansing

Haircare

Millions Euros, in millions

1 656

792 735 721 696

1.6 1.7 0.4

-0.4 -3.2

Ora

l C

are

Bo

dy C

lea

nsin

g

Hair

Ca

re

Facia

l C

are

Deo

do

ran

ts

Eu

ros,

in m

illio

ns

Euro Sales % € vs. YA

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

CATEGORY INSIGHTS

• The category gaining the most in value sales

in H1 2015 was toothbrushes. It was £8

million ahead of H1 2014 as premium

innovations continued to appear strong and

overall market prices have increased.

• The next highest increase came from

incontinence pads, continuing its spectacular

growth, with volume sales up by 10% and a

gain in H1 of £6.5 million.

• Deodorant and body spray were down versus

H1 2014 by 5% in both value and volume.

Percentage volume on deal remains

extraordinarily high at close to 80% and deal

depth has increased to more than 40%, but

the category has still fallen. The weather has

not helped, as value was down by £12.8

versus H1 2014.

• Similarly, sun care has had a bad start to the

year, with value down by 7.1% and volume

by 8.2%, sales were £7.6 million lower.

• Haircare value sales were down by 1.3% with

volume falling faster. Shampoo, styling and

male hair treatments showed small value

gains but volume was down throughout.

Euros, in millions

PULSE REPORT

Final Notes

19

Notes on category definitions for countries

Due to the diverse products found in individual countries across this market, it was necessary

to consolidate the available data into the categories in this report. In some cases, it wasn’t

always possible to align products across all six countries, hence the need to highlight any

anomalies in the report. Those exceptions are listed below.

Facial care

• The France data in this report includes wet wipes for this category, while the other countries

do not.

• The France data in this report does not include lip balm whereas the other countries do.

Feminine hygiene

• The Netherlands data in this report does not include intimate hygiene products, which are

included in body care.

Cosmetics

• The UK data in this report does not include this category.

Fragrance

• The UK data in this report does not include this category.

PULSE REPORT

Resources

20

About IRI. IRI is a leader in delivering powerful market and shopper information, predictive analysis and the foresight

that leads to action. We go beyond the data to ignite extraordinary growth for our clients in the CPG, retail and over-

the-counter healthcare industries by pinpointing what matters and illuminating how it can impact their businesses

across sales and marketing. Move your business forward at IRIworldwide.eu

Arlington Square, Downshire Way, Bracknell, Berkshire RG12 1WA, Tel +44 (0) 1344 746000

Copyright © 2015 Information Resources, Inc. (IRI). All rights reserved. IRI, the IRI logo and the names of IRI products and services

referenced herein are either trademarks or registered trademarks of IRI. All other trademarks are the property of their respective owners.

FOR MORE INFORMATION

Please contact Emily Mayer, Business Unit Director, France,

IRI at [email protected] or

+33 (0)130 06 26 56 with questions or comments about this report.

To gain insight into opportunities across specific categories, segments, channels or retailers,

contact your IRI client service representative regarding custom analyses leveraging the

following resources:

• IRI InfoScan Census® is a syndicated retail tracking service that enables manufacturers

and retailers to acquire industry insights used to make better business decisions. IRI

InfoScan Census utilizes the data that IRI collects from grocery, drug, and mass

merchandise retailers to provide the most comprehensive and accurate syndicated data

offering in the FMCG sector. With access to accurate, granular detail by category, geography,

measure, and time period, clients have the tools needed to develop marketing and sales

strategies based on product performance, distribution, and promotion responsiveness. All

data about personal care comes from IRI InfoScan Census.

• IRI Consulting provides strategic insights and advice leveraging a variety of data sources,

predictive analytics, enabling technologies, and business analyses to help FMCG

manufacturers and retailers address significant sales and marketing issues effectively.