io 2010 may aiece world trade.ppt

TRANSCRIPT

World Trade in 2010 and 2011AIECE General Meeting AIECE General Meeting

May 6, 2010Milan

Bart De Ketelbutter

plan.beplan.be

World trade in 2010-2011

plan.beplan.be

World economyy

Remarkably quick & Remarkably quick & vigorous recoveryOwing to extra-

d f l &3

4

5

ordinary fiscal & monetary stimulus... and the wearing 1

2

3

a d t e ea goff of the initial shock effectChina Asia and EM 2

-1

0

China, Asia and EM are leading the way

Size stimulus-3

-2

2006

Q1

2006

Q2

2006

Q3

2006

Q4

2007

Q1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

Largely insulated from fin.crisis

qoq grow th rates yoy grow th rates

plan.beplan.be

Commodities and financial markets

Oil & commodity Oil & commodity prices risen unabatedly since t t f 2009start of 2009

Financial markets rebounded (equity rebounded (equity, corporate debt, interbank market), b but not a normalisation yet as authorities have been authorities have been major player + fueled by liquidity

plan.beplan.besurge

World industrial productionp

115

120

10%

15%

IP bounced back strongly

10

110

0%

5%

back strongly Currently at 10% yoy

100

105

-10%

-5% But still not back to pre-crisis level

95

janv

/07

mar

s/07

mai

/07

juil/0

7

sept

/07

nov/

07

janv

/08

mar

s/08

mai

/08

juil/0

8

sept

/08

nov/

08

janv

/09

mar

s/09

mai

/09

juil/0

9

sept

/09

nov/

09

janv

/10

-15%

crisis level (blue line, LHS)

Index, 2005=100 yoy grow th rates (RHS)

plan.beplan.be

Industrial production, region by regionp , g y g

130

110

120

90

100

70

80

90

60

70

08M

1

08M

3

08M

5

08M

7

08M

9

8M11

09M

1

09M

3

09M

5

09M

7

09M

9

9M11

10M

1

Asian and EM lead and already above pre crisis level (not

200

200

200

200

200

2008 20

0

200

200

200

200

2009 20

1

US Japan Euro Area Emerging Countries Asia

plan.beplan.be

Asian and EM lead and already above pre-crisis level (not only because of faster recovery, higher trend growth)

World trade, growth rate, g

-16% in Oct08-16% in Oct08Jan09, -20% in 6M to Jan09

2 0%

4,0%

6,0%

10 0%

15,0%

20,0%

Reasons:US downturn, commodity prices-2,0%

0,0%

2,0%

0,0%

5,0%

10,0%

Consumer durables & investment gdsSynchronized -6,0%

-4,0%

2,0%

-15,0%

-10,0%

-5,0%

Synchronized downturnCredit conditions

Stabilisation in H1 09-10,0%

-8,0%

1 4 7 0 1 4 7 0 1 4 7 0 1-25,0%

-20,0%

,

Stabilisation in H1 09Strong recovery in H2 09 and start of 2010

2007

M20

07M

2007

M20

07M

120

08M

2008

M20

08M

2008

M1

2009

M20

09M

2009

M20

09M

120

10M

mom yoy (RHS)

plan.beplan.be

y y ( )

World trade, level,

But world trade not But world trade not back to pre-crisis level yet

160 0

170,0

Emerging countries are leading Asia China150,0

160,0

Among developed economies EA lags (US & Japan benefit

140,0

(US & Japan benefit from proximity China, size of stimulus)A i

130,0

Among emerging countries CEE lag (proximity lagging

120,0

2005

M1

2005

M9

2006

M5

2007

M1

2007

M9

2008

M5

2009

M1

2009

M9

plan.beplan.beEA)

2 2 2 2 2 2 2 2

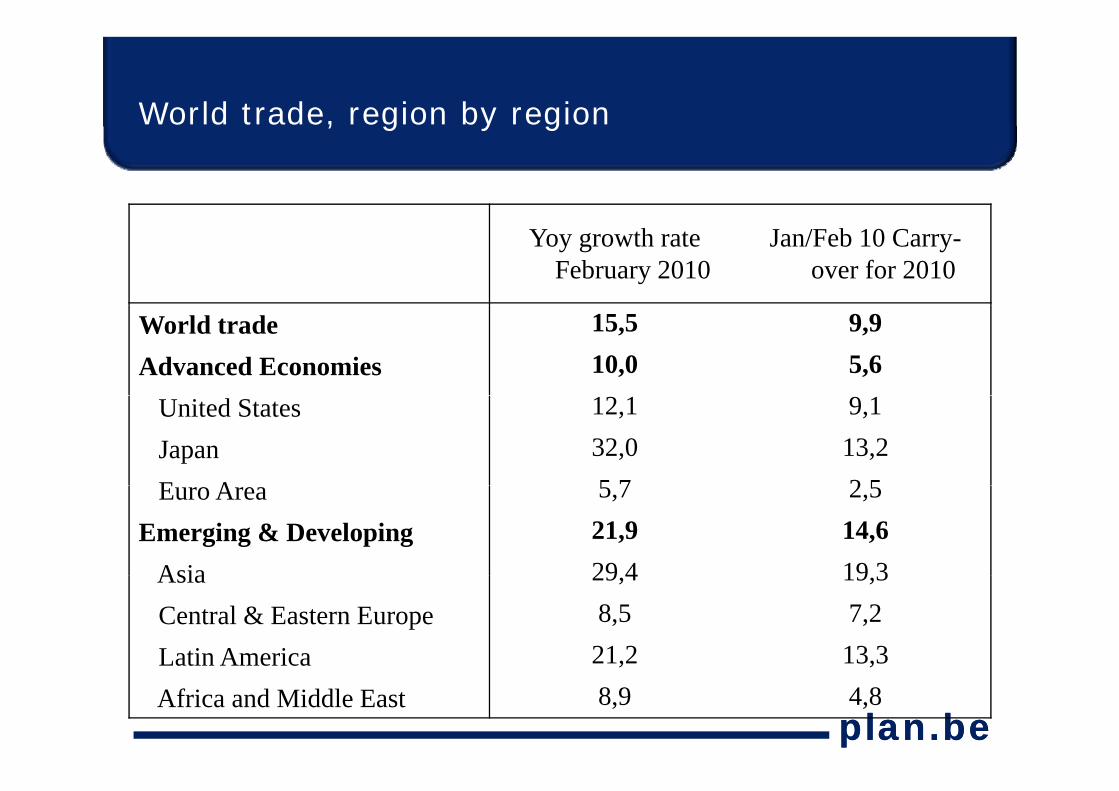

World trade, region by region, g y g

Yoy growth rate February 2010

Jan/Feb 10 Carry-over for 2010

World trade 15,5 9,9

Advanced Economies 10,0 5,6

United States 12,1 9,1

Japan 32,0 13,2

E A 5 7 2 5Euro Area 5,7 2,5

Emerging & Developing 21,9 14,6

Asia 29 4 19 3Asia 29,4 19,3

Central & Eastern Europe 8,5 7,2

Latin America 21,2 13,3

plan.beplan.be

Latin America , ,

Africa and Middle East 8,9 4,8

The outlook and the risks

plan.beplan.be

Outlook 1

M i t t d i Many economists expect some decrease in economic growth after a remarkably quick recovery (esp in Asia & US) from the depths recovery (esp. in Asia & US) from the depths of the recession Reasons for this relative pessimism are Reasons for this relative pessimism are numerous

plan.beplan.be

Outlook 2

Ending of large fiscal stimulusEnding of extra-ordinary monetary stimulus

Depart from near 0% interest ratesStop in provisioning of almost limitless liquidityQuantitative easingQuantitative easing

Ending of decreased destocking/restockingReduced level of credit supply by banks esp in Reduced level of credit supply by banks, esp. in EuropeRising commodity prices (oil!)Rising commodity prices (oil!)Sovereign debt crisis

plan.beplan.be

Outlook 3

But other economists (a growing number) are more optimistic about ) pthe futureReasons:

World trade and industrial production is surgingIndicators are often at levels that signal strong growth ahead

plan.beplan.be

Key Assumptions & World trade forecasty p

Autumn 2009 Spring 20102009 2010 2009 2010 2011

GDP volume (yoy)United States 2 7 2 0 2 4 3 0 2 5United States ‐2,7 2,0 ‐2,4 3,0 2,5Japan ‐5,4 2,0 ‐5,2 1,8 1,4Euro Area ‐3,7 1,5 ‐4,0 1,2 1,5China 8,2 8,5 8,6 10,0 8,7

Exchange Rates (levels)USD/EUR 1 38 1 45 1 39 1 38 1 38USD/EUR 1,38 1,45 1,39 1,38 1,38JPY/USD 95 90 93,6 92,0 92,0

World trade prices (USD)pCrude oil (Brent, level, $/b) 60,1 75,2 61,5 80 80Non‐energy prim. Commodities, yoy ‐23 12 ‐22,4 20 2

M f d d 6 3 0 4 0 4 1 3

plan.beplan.beManufactured goods, yoy ‐6,3 0,4 ‐7,5 ‐0,4 1,3World trade volume (goods, yoy) ‐13,5 7,4 ‐12,1 10,7 7,6

World trade forecast, quarterly profile, q y p

Level, 2000=100 qoq yoy

2009Q1 131,7 -9,9% -18,6%2009Q2 131,8 0,1% -18,2%2009Q3 137,0 3,9% -13,7%2009Q4 144,1 5,1% -1,4%2010Q1 147,7 2,5% 12,2%2010Q2 149 5 1 2% 13 4%2010Q2 149,5 1,2% 13,4%2010Q3 151,4 1,3% 10,5%2010Q4 154,0 1,7% 6,9%2011Q1 157,0 2,0% 6,3%2011Q2 160,3 2,1% 7,3%

plan.beplan.be2011Q3 163,7 2,1% 8,1%2011Q4 167,2 2,1% 8,6%

China

Ever more a driver for the world economy and financial Ever more a driver for the world economy and financial markets (cf. Market reaction when authorities signalled monetary tightening)Ever more important in our forecasts, but statistics not abundant & of doubtful qualityC b t Chi dit i t i Concerns about Chinese credit expansion, asset prices and rising inflationBank reserve requirements raised and lending Bank reserve requirements raised and lending restrictions imposedChina needs a new growth model relying more on g y ginternal consumer demand rather than on external demandY /USD R l ti US t ti i t

plan.beplan.beYuan/USD: Revaluation soon or US protectionist measures will be taken

China GDP growthg

Fiscal stimulus planIncredible surge in Incredible surge in bank lendingPushed yoy GDP y ygrowth from 6% to 12% in the course of just one yearjust one year

plan.beplan.be

The rising importance of emerging markets in world trademarkets in world trade

Source: DOTS IMF (values)

plan.beplan.be

World import market shares EM, BRICs, Chinap , ,

EM M growth 40%

surgingHigh domestic demand growth

30%

35%

40%

demand growthOpening up economies 15%

20%

25%

Shift toward intra-EM & intra-BRICs trade

5%

10%

15%

BRICs trade 0%19

90

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

EM China BRICsAv M gr 00-08DM 9,8EM 19,1

plan.beplan.beBRICs 21,7China 25,1

EM & DM export share going to EMp g g

40%

30%

35%

25%

15%

20%

1990 1992 1994 1996 1998 2000 2002 2004 2006 20081990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Emerging markets Developed markets

plan.beplan.be

World trade becoming more diversified-Top 10 Mg p

1990 2000 2008

1 US 14,6% US 18,8% US 13,1%

2 Germany 9 8% Germany 7 6% Germany 7 2%2 Germany 9,8% Germany 7,6% Germany 7,2%

3 Japan 6,7% Japan 5,8% China 6,8%

4 France 6,6% UK 5,1% Japan 4,6%, , p ,

5 UK 6,3% France 5,0% France 4,3%

6 Asia 5,7% Canada 4,0% UK 3,8%

7 Italy 5,2% Italy 3,6% Netherlands 3,5%

8 Canada 3,7% China 3,4% Italy 3,4%

9 N h l d 3 5 N h l d 3 3 B l i 2 89 Netherlands 3,5% Netherlands 3,3% Belgium 2,8%

10 Spain 2,5% Hong Kong 3,2% Canada 2,7%

Top 10 Total 64 6% Top 10 Total 59 7% Top 10 Total 52 2%

plan.beplan.be

Top 10 Total 64,6% Top 10 Total 59,7% Top 10 Total 52,2%

World trade becoming more diversified-Next 10 Mg

1990 2000 2008

11 Hong Kong 2,3% Mexico 3,0% South Korea 2,6%

12 South Korea 2,0% Belgium 2,7% Spain 2,6%, g , p ,

13 Switzerland 2,0% South Korea 2,4% Hong Kong 2,3%

14 Singapore 1,7% Spain 2,2% Mexico 2,1%

15 Sweden 1,5% Singapore 2,0% Singapore 1,9%

16 China 1,5% Switzerland 1,3% India 1,7%

17 Austria 1,4% Malaysia 1,2% Russia 1,6%17 Austria 1,4% Malaysia 1,2% Russia 1,6%

18 Australia 1,2% Australia 1,1% Brazil 1,4%

19 Thailand 0,9% Sweden 1,1% Australia 1,3%

20 Mexico 0,9% Austria 1,1% Poland 1,3%

Next 10 Total 15,5% Next 10 Total 18,1% Next 10 Total 18,8%

Top 20 Total 80 2% Top 20 Total 77 8% Top 20 Total 71 0%

plan.beplan.be

Top 20 Total 80,2% Top 20 Total 77,8% Top 20 Total 71,0%

European sovereign debt crisis

plan.beplan.be

Next big phase in the financial crisisg p

Let us not be overly optimistic C l bi 1998Let us not be overly optimistic because of buoyant world trade, IP & GDP growth Chile, 1980

Finland, 1991

Colombia, 1998

Financial crisis still among us (all our risks relate to it)Next big phase in the financial Historical Average

Spain, 1977

Indonesia, 1997

Next big phase in the financial crisis (after subprime, banking & economic crisis) Korea, 1997

Sweden, 1991

Historical Average

Reinhart & Rogoff: Public debt soars in wake of fin.crises & defaults often follow Japan 1992

Norway, 1987

Philippines, 1997

defaults often follow

Malaysia, 1997

Mexico, 1994

Japan, 1992

Cumulative rise in real debt in the 3Y following the banking/financial crisis

plan.beplan.be0 50 100 150 200 250 300

following the banking/financial crisis

Index= 100 in year of crisis

Bond yield spreads against German Bundsy p g

• It started with Greece s d G(statistics falsified) & 2009 deficit estimate suddenly doubled suddenly doubled

• Credit downgrades• Spreads of ES, PT, IR

also on the rise• Last week even small

rises in other countriesrises in other countries• Reasons behind crisis?

GR 714 IT 110

PT 286 BE 62

IR 225 FR 33

plan.beplan.be

IR 225 FR 33

ES 115 NL 29Spreads on 28/04:

1.State of public financesp

Deficit DebtGreece 12 7 112 6 D t i t d t l d Greece ‐12,7 112,6Spain ‐11,2 54,3Portugal ‐8,0 77,4

Deteriorated strongly due to recession, stimulus & capital injections in banksg , ,

Ireland ‐12,5 65,8Italy ‐5,3 114,6

p jIn some countries : Over-reliance on above-trend

i t f b bbl France ‐8,3 76,1Belgium ‐5,9 97,2Germany 3 4 73 1

receipts from bubbly sectors (e.g. construction in ES, financ.sector in UK)Germany ‐3,4 73,1

NL ‐4,7 59,8Austria ‐4,3 69,1

in ES, financ.sector in UK)LT cost of ageing

, ,Finland ‐2,8 41,3EA12 ‐6,4 78,7

plan.beplan.beUK ‐12,1 68,6US ‐11,3 65,2 Ameco Autumn 09 fc for 2009

2. Phasing out of exceptional monetary stimulusg p y

D t f 0% IRDeparture from near 0% IRsFade out almost limitless provisioning of liquidityprovisioning of liquidityEnd QEHas powered financial assetspCarry-trade on gov.bnds, popular strategyRemoval of subsidy to public debtM i l h t t i d bt d Mainly hurts most indebted countries (higher ylds ,made them main beneficiaries

plan.beplan.becarry-trade)

3.Competitiveness, CA deficits and foreign debtp , g

ULC Ch CA/GDP • Entrance in euro area Country

ULC Ch 08‐99

CA/GDP change 08‐99

Greece 40.4 ‐8.6Ireland 37 5 5 3

lowered interest rates & unleashed credit boomIreland 37.5 ‐5.3

Portugal 35.5 ‐3.2Spain 33.3 ‐6.8

boom• Higher wage growth

and inflationItaly 16.7 ‐4.0Belgium 17.8 ‐4.7Austria 8.6 5.1

• Deterioration of competitivenessSt t i l t France 19.7 ‐5.8

NL 24.9 0.0Finland 19 8 5 4

• Strongest rise over last 10Y seen in the four problem countriesFinland 19.8 ‐5.4

Germany 3.4 7.8EA12 17.9 ‐1.2U

problem countries• Related: The level of

foreign debt and the

plan.beplan.beUK 24.3 0.7US 17.2 ‐1.8

dependence on foreign capital (PT)

4. The functioning of the euro area: more integration?integration?

Lack of means to address these imbalancesLack to reach consensus rapidly in times of crisisInitial plan for Greece was vague and incredible & markets did not buy ith lThe EA is no optimal currency area

US neither, but regional imbalances are tt t d b th f d l b d t (b lk f t i attenuated by the federal budget (bulk of taxing

& spending) and stronger labour mobility Euro area needs to integrate more and go Euro area needs to integrate more and go towards a fiscal & political union or else ...

plan.beplan.be

What next? – The new plan for Greecep

M i fl ti t d d bt h d f lt More inflation to erode debt overhang, defaults, general loss of confidence in sovereign debt?The new plan for Greece:The new plan for Greece:

110bn EUR loan package from EA & IMFCondition of spending cuts & tax hikesEffort needed not entirely unprecedented, but ... (cf. Belgian case)10 bn EUR to stabilise banking systemg yECB suspends colleteral rule for Greek bondsPlus: No need to turn to bond market next 3YEnough to restore confidence?Enough to restore confidence?Insolvency remains a problem, some kind of debt restructuring still likely

plan.beplan.be

Questions remainQ

Amounts lent to Greece still need to be approved in Amounts lent to Greece still need to be approved in national parliamentsWill Greece really be able to achieve these draconian measuresContagion risk not addressed (ES, PT): Will they be saved too?saved too?Markets risk testing this & see if countries are really prepared to restore health in public financesp epa ed to esto e ea t pub c a cesNot only in Europe (US, UK, Japan)Policymakers need to find way to convince markets y ythey’ll do whatever necessary to get ahead of the crisis

plan.beplan.be

Effects of full-blown sovereign debt crisisg

Loss of confidence could still spreadEffects of a full-blown sovereign debt crisis:

Higher interest ratesPremature and severe tightening of fiscal policyHit to bank assets (writedowns on sovereign debt) and Hit to bank assets (writedowns on sovereign debt) and financial panic: The sovereign version of Lehman?Would imperil the still fragile economic recovery

plan.beplan.be

Foreign banks’ exposure to problem countriesg p p

Bulk with European banks in bn EURIncludes debt of public and private sector

in bn EUR

Greece 163,9

Portugal 198,3

Ireland 601,8e a d 60 ,8

Spain 795,4

Italy 984,2

Source: BIS

plan.beplan.be

Source: BIS

Thank you for your attention.

plan.beplan.be