investor presentation v4

TRANSCRIPT

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 1/38

Petrojack ASAInitial public offering

A pure play jack-up rig investment with highleverage to expected increase in rig value

February 7, 2005

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 2/38

2

Important notice

This document has been prepared exclusively for the benefit and use of the reader in order to evaluate the feasibility of a possible transaction or transactions and does not carry any right of publication or disclosure to any other party. This document does not represent a formal offer to purchase shares in Petrojack ASA. This document is incomplete without reference to, and should be viewed solely inconjunction with, the oral briefing provided by First Securities ASA and/or ABG Sundal Collier Norge ASA. This presentation may not be used for any other purpose without the prior written consent of First Securities ASA and/or ABG Sundal Collier Norge ASA. In preparing this document we have relied upon and assumed, without independent verification, the accuracy and completeness of all informationavailable from public sources or which was provided to us or otherwise reviewed by us. The information contained in this document has been derived from sources deemed to be reliable. We do not represent that such information is accurate or complete and it should not be relied on as such. Any opinions expresses herein reflect our judgement at this date, all of which are accordingly subject tochange.

As per February 3., 2005 ABG Sundal Collier Norge ASA and F irst Securities ASA own 0 and 0shares in Petrojack ASA. Employees and partners of ABG Sundal Collier Norge ASA and First Securities ASA own 0 and 0 shares in Petrojack ASA as per the same date. ABG Sundal Collier Norge ASA and/or First Securities ASA and/or their employees and partners may, from time to time, hold shares,options or other securities of any issuer referred to in this document and may, as principal or agent, buy or sell such securities. First Securities ASA and/or ABG Sundal Collier may have other financial interests in transactions involving these securities.

The Shares have not been nor will be registered under the U.S. Securities Act of 1933, as amended, (the "Securities Act"), or any state securities laws, and are being offered within the United States only to qualified institutional buyers ("QIB") as defined in Rule 144A under the Securities Act ("Rule 144A"), in reliance upon the exemption from the registration requirements of the Securities Act provided by Rule 144 A. Prospective purchasers of the Shares are hereby notified that the Shares are subject to certain restrictions on transfer under the Securities Act.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 3/38

3

Agenda

I. Introduction

II. Transaction

III. Market

IV. Company

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 4/38

4

Strong outlook for the jack-up market

Strong oil and gas prices are finally resulting in significantly increasing E&Pexpenditure, which is the main driver for jack-up rig demand.

The jack-up rig fleet is close to fully utilized and day rates are increasingaccordingly. Historically, there has been a close relationship betweenutilization and day rates.

The jack-up rig fleet represents 2/3 of the total offshore drilling fleet. Theaverage age of the global fleet is 23 years, whereas the order bookconstitutes only 4% of the existing fleet.

An eventual new-building boom for jack-up rigs is expected to increasevalues (new-buildings and second hand) and increase delivery time for newrigs.

Strong E&P

spending

outlook.

High

utilization for

jack-up rigs.

The jack-up

rig fleet is

growing old.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 5/38

5

Petrojack has one jack-up rig under construction and two optional units

Petrojack ASA (³Petrojack´) has fully financed EPC contract for one modern jack-up rigwith Jurong Shipyard Pte Ltd. (³JSPL´ or ³Jurong´) with expected delivery in March2007.

Jurong is, together with its sister companies PPL and Sembawang, part of the SembCorpMarine Group (SCM), a leading offshore rig construction group.

Additionally, Petrojack has rig option agreement with PPL to construct two additionalunits with the same specifications as the first unit (higher price and some contractualdifferences).

The first option is to be exercised between June 16 and December 15, 2005, whereas thesecond option is to be exercised between December 16. 2005 and June 15, 2006. Thesecond option is not subject to the first option being exercised.

Fully financed jack-up project with high financial gearing:

Limited financial risk during construction phase and the period after delivery.

Attractive terms in the debt financing package (e.g. the last payment of 80% of the contractprice to Jurong is entirely covered by the debt financing package and the debt financingpackage can be moved to one of the optional units if the first unit is refinanced or sold).

F ully

financed jack-

up rig under

construction.

Option to

build two

additional

units.

Attractive

financing

package.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 6/38

6

Petrojack¶s flexible strategy is expected to create value for shareholders

Petrojack offers a highly leveraged exposure to the jack-up market. A 10%increase in newbuilding values will increase the NAV of Petrojack by 60% nottaking into account new shares issued in connection with the IPO.

Petrojack has a flexible business strategy going forward with the goal of maximizing shareholder value. Petrojack envisages three main strategicalternative paths depending on the situation in the ever changing oil and gas

market:

Operation of rig(s) with medium to long term contracts.

Merger with leading national or international rig company

Sale of rig(s) to other companies

Petrojack has an experienced management and board of directors with

background from the oil and gas industry as well as the financial industry.

High leverage

to increases

in rig values.

F lexible

strategy with

the goal of

maximizing

shareholder

value.

Experienced

management

and board of

directors.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 7/38

7

Agenda

I. Introduction

II. Transaction

III. Market

IV. Company

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 8/38

8

The offering

Minimum 3 700 000 and maximum 9 000 000 new shares.

Institutional offering:

Min subscription per investor: 70 000 shares.

Retail offering:

Min. subscription per investor: 1 000 shares.

Max. subscription per investor: 69 000 shares.

Max. number of shares in tranche: 3 000 000 shares.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 9/38

9

Final subscription price will be based on a book-building procedure

Indicative price range:

NOK 7.0 ± 9.0 per share.

Book-building/order period:

February 7, 2005 to February 18, 2005 at 16.00 hours Norwegian time (both datesinclusive).

Only orders in the Institutional offering will be considered in setting the final subscriptionprice. The indicative price range listed above is subject to change:

The final subscription price may be higher or lower than the indicative price range.

Discount for investors participating in the retail offering:

Automatically 10% discount relative to the final subscription price for subscriptions up to 1000 shares per investor.

The total number of discounted shares to be issued in the offering is limited to 2 000 000.

See prospectus for further details.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 10/38

10

The offering is carried out to expand Petrojack¶s shareholder base to facilitateregular trading of the Petrojack-shares.

The Offering proceeds will be used to strengthen the Company¶s workingcapital / general corporate purposes.

The gross proceeds from the Offering, if fully subscribed, will be minimum NOK 29 600 000 and maximum NOK 72 000 000, assuming a final subscription priceof NOK 8.00 per share, corresponding to the mid-point of the indicative pricerange.

The planned stock exchange listing will give Petrojack access to a regulatedmarketplace for trading of the Company¶s shares and is expected to provideaccess to capital for the financing of the First and Second rig Options, in casethese are exercised.

Purpose of the offering and use of proceeds

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 11/38

11

Agenda

I. Introduction

II. Transaction

III. Market

Oil and gas market

Drilling market

IV. Company

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 12/38

12

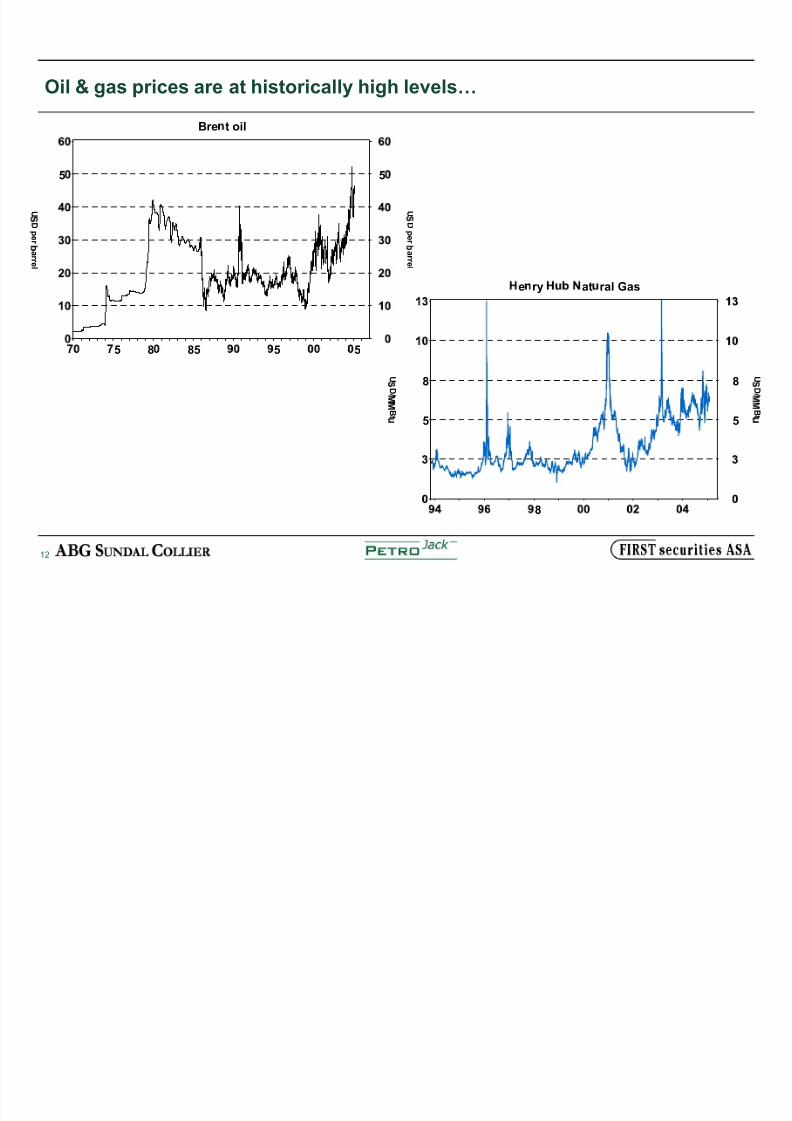

Oil & gas prices are at historically high levels«

Bre t oil

5 8 85 5 5

U

D p er

¡

ar r el

5

U

D p er

¡

ar r el

5

e ry at ral Gas

8

U

D /

¢

¢

B t

£

5

8 U

D /

¢

¢

B t £ 5

8

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 13/38

13

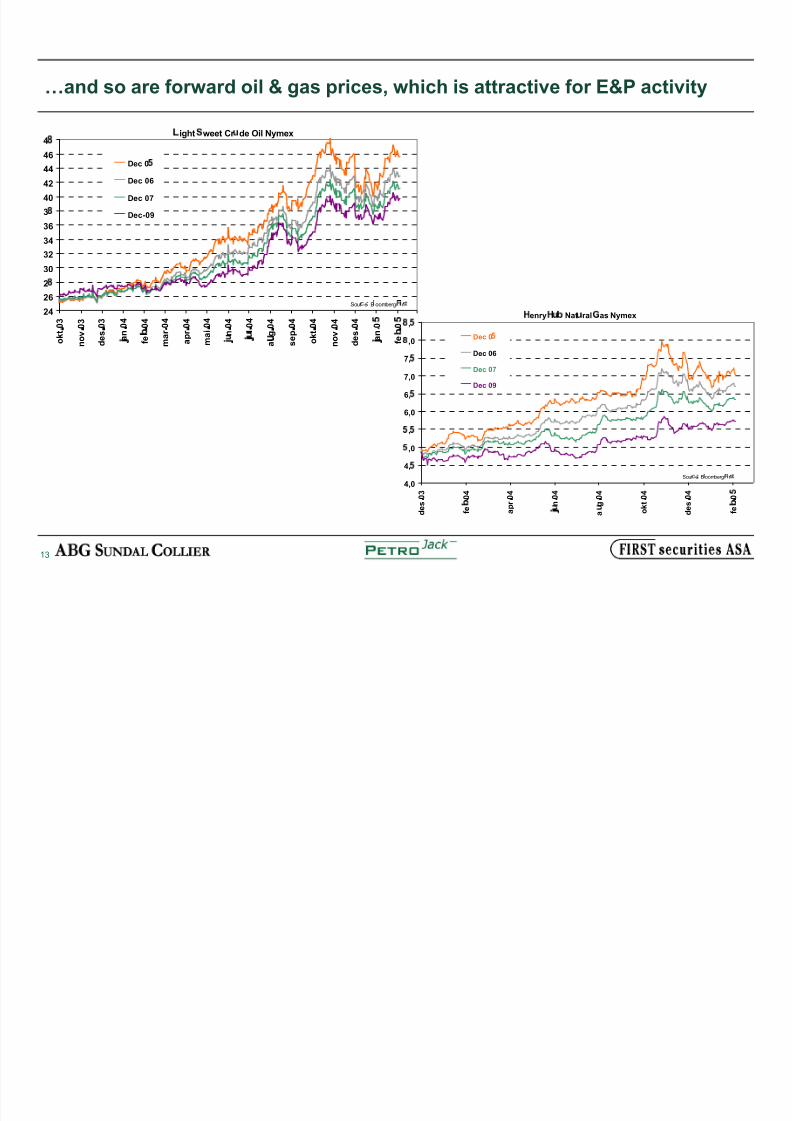

«and so are forward oil & gas prices, which is attractive for E&P activity

¤ ight¥

weet Cr ¦

de Oil Nymex

24

26

2§

30

32

34

36

3§

40

42

44

46

4§

o k t

¨

0 3

n o v

¨

0 3

d e s

¨

0 3

©

a n

¨

0 4

f e

¨

0 4

m a r

¨

0 4

a p r

¨

0 4

m a i

¨

0 4

©

n¨

0 4

©

l¨

0 4

a

g¨

0 4

s e p

¨

0 4

o k t

¨

0 4

n o v

¨

0 4

d e s

¨

0 4

©

a n

¨

0

f e

¨

0

Dec 0

Dec 06

Dec 07

Dec-09

Sour e B oomberg/

r

! enry! " #

Nat " ral$

as Nymex

4,0

4,

,0

,

6,0

6,

7,0

7,

%

,0

%

,

d e s

&

0 3

f e

'

&

0 4

a p r

&

0 4

(

)

n&

0 4

a

)

g&

0 4

o k t

&

0 4

d e s

&

0 4

f e

'

&

0

0

Dec 01

Dec 06

Dec 07

Dec 09

Sour 2

e 3 B4

oomberg/5 6

r 7

8

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 14/38

14

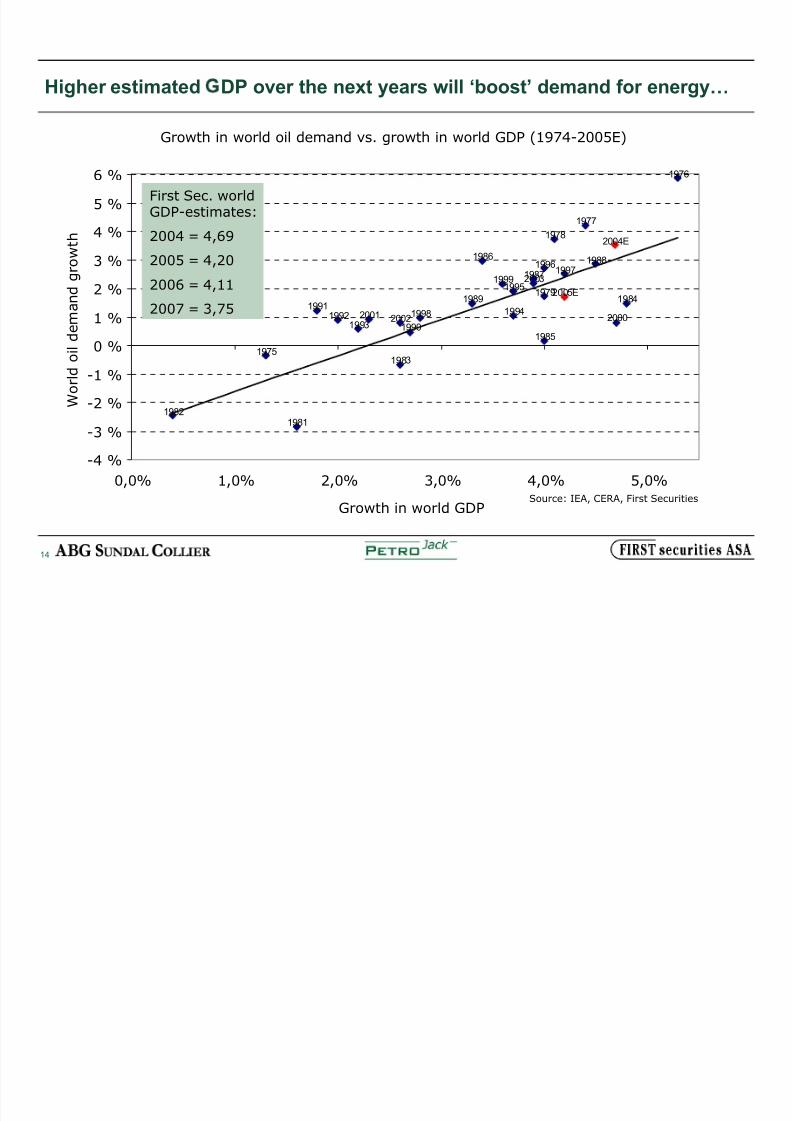

Higher estimated DP over the next years will µboost¶ demand for energy«

Growth in world oil demand vs. growth in world GDP (1974-2005E)

1975

1976

1977

1978

1979

19811982

1983

1984

1985

1986

1987

1988

1989

1990

19911992

1993

1994

1995

19961997

1998

1999

20002001 2002

2003

2004E

2005E

-4 %

-3 %

-2 %

-1 %

0 %

1 %

2 %

3 %

4 %

5 %

6 %

0,0% 1,0% 2,0% 3,0% 4,0% 5,0%

Growth in world GDP

W o r l d o i l d e m a n d g

r o w t h

First Sec. worldGDP-estimates:

2004 = 4,69

2005 = 4,20

2006 = 4,11

2007 = 3,75

Source: IEA, CERA, First Securities

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 15/38

15

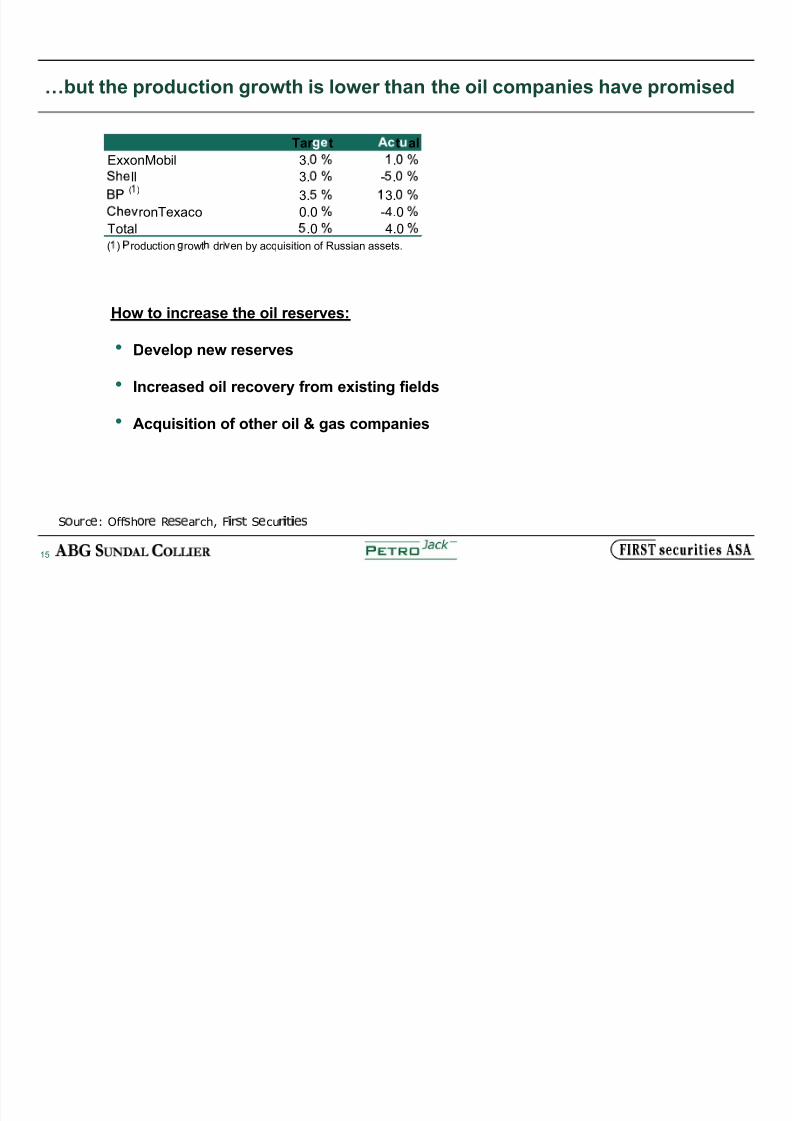

«but the production growth is lower than the oil companies have promised

How to increase the oil reserves:

Develop new reserves

Increased oil recovery from existing fields

Acquisition of other oil & gas companies

S9 u @ c A : Off B h9 @ A

RA B A

a @ ch, FC

@ B D S A cu @

C

D

C

A B

Tar t t alExxonMobil 3. .

ll 3. - .( E )

3. 3.

r onTexaco 0.0 -4.0

Total .0 4.0

( ) r oduction r owt dri en by acquisition of Russian assets.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 16/38

16

Positive Negative

Historically high oil & gas prices.

Actual production lower than planned.

Strong demand growth for energy.

Shell and others have downgradedproven reserves.

Investments lower than necessary for sustainable growth.

Several oil companies have increasedlong-term oil price assumption from 16 to20 SD /boe in new project calucations.

Summary oil & gas market: Despite some uncertainty concerning oil markets,strong demand for drilling services may be expected going forward

Volatile energy prices.

Preference for onshore investments inRussia and Iraq etc.

Lack of offshore prospects.

The major oil resources remain largelyimpossible to reach for western oil & gascompanies.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 17/38

17

Agenda

I. Introduction

II. Transaction

III. Market

Oil and gas market

Drilling market

IV. Company

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 18/38

18

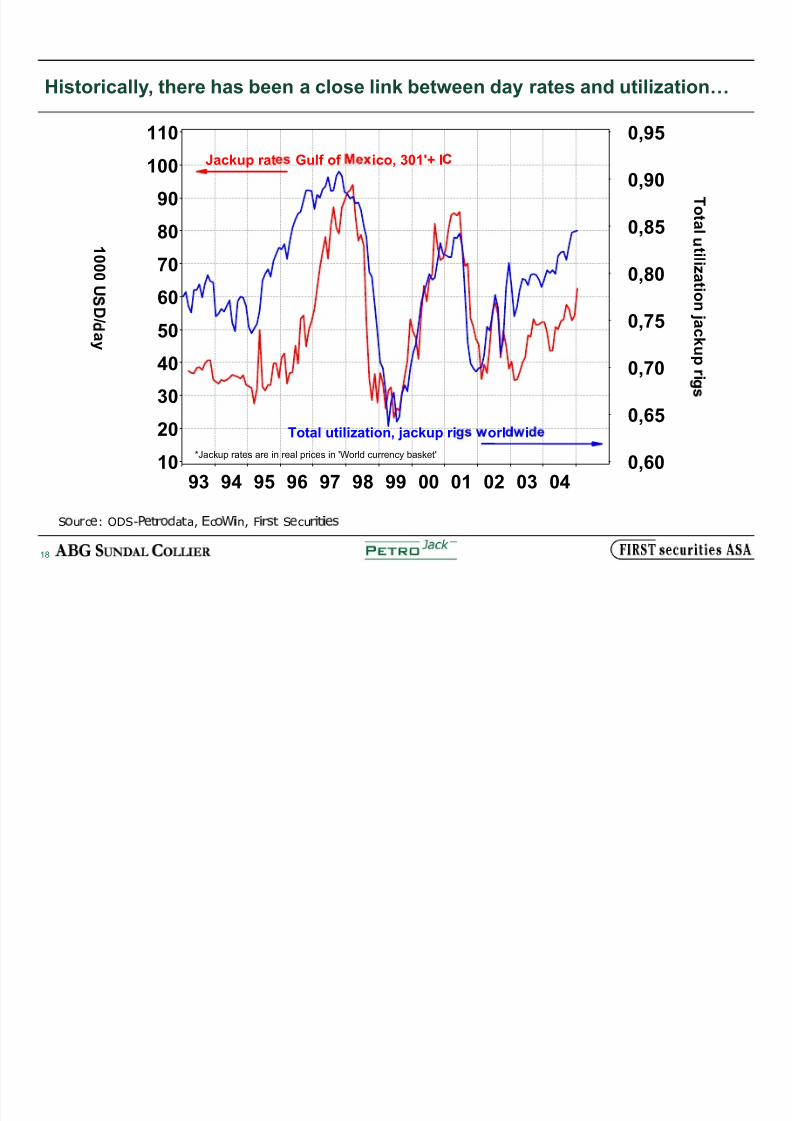

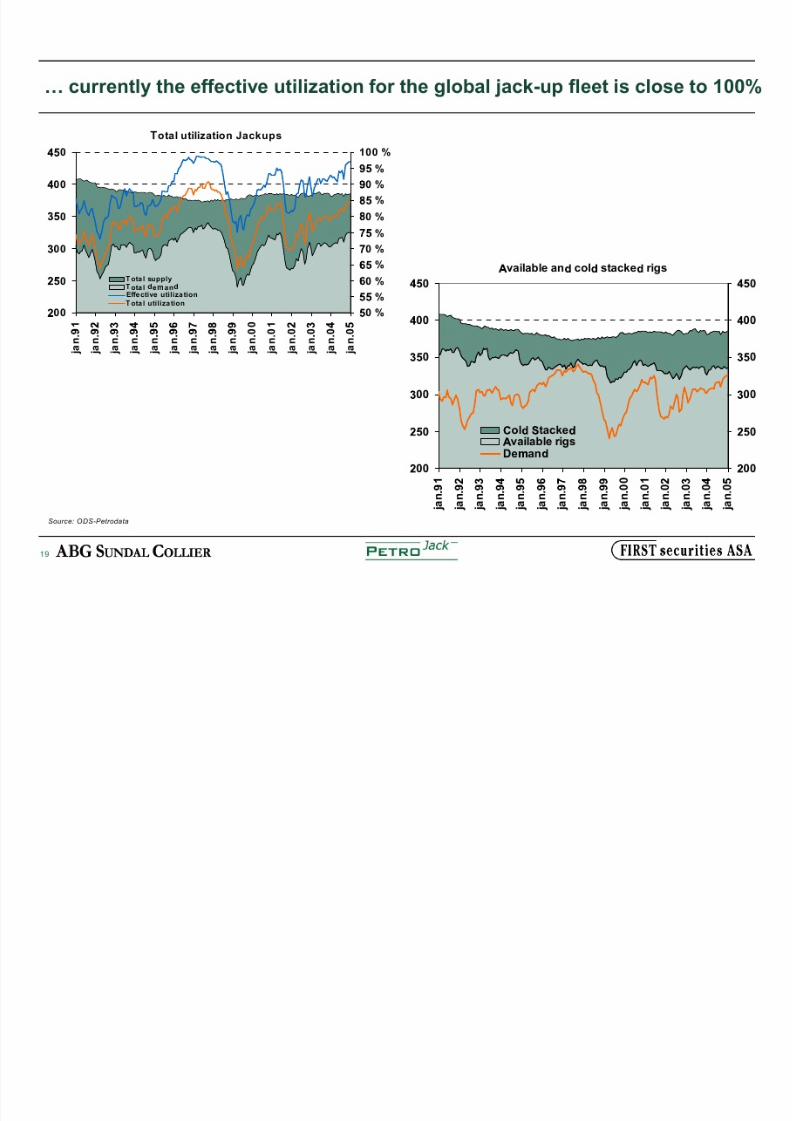

Historically, there has been a close link between day rates and utilization«

93 94 95 96 97 98 99 00 01 02 03 04

T o t al

t i l i z a t i on j a ck u pr i

0,60

0,65

0,70

0,75

0,80

0,85

0,90

0,95

1 0 0

0 U

D / a y

10

20

30

40

50

60

70

80

90

100

110

Jackup r at Gulf of ico, 301'+ I

Total utilization, jackup ri orl i

*Jackup r ates ar e in r eal prices in 'World curr ency basket'

SF u G c H : ODS-I H P G F Q

a P a, R cF S T

n, FT G U P

SH cuG T P T H U

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 19/38

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 20/38

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 21/38

21

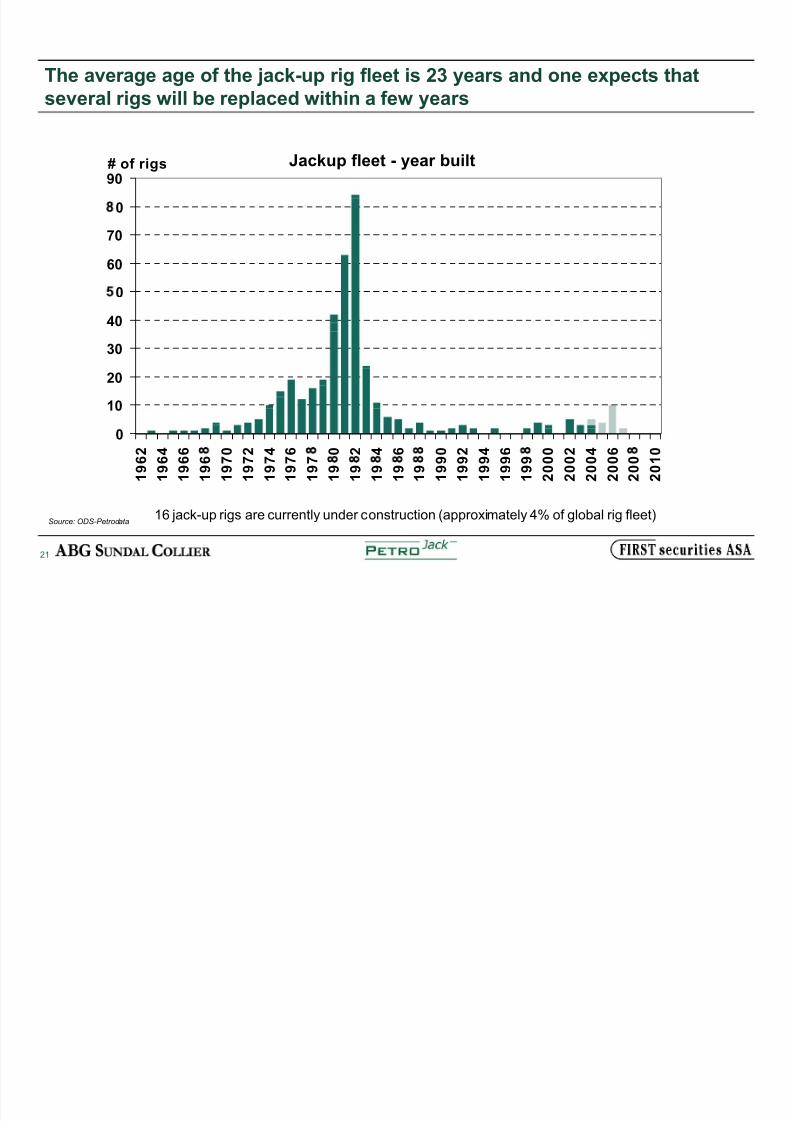

The average age of the jack-up rig fleet is 23 years and one expects thatseveral rigs will be replaced within a few years

Source: ODS-Petrodata16 jack-up rigs are currently under construction (approximately 4% of global rig fleet)

Jackup fleet - year built

0

10

20

30

40

0

60

70

0

90

1 9 6 2

1 9 6 4

1 9 6 6

1 9 6

1 9 7 0

1 9 7 2

1 9 7 4

1 9 7 6

1 9 7

1 9

0

1 9

2

1 9

4

1 9

6

1 9

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0

2 0 1 0

# of rigs

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 22/38

22

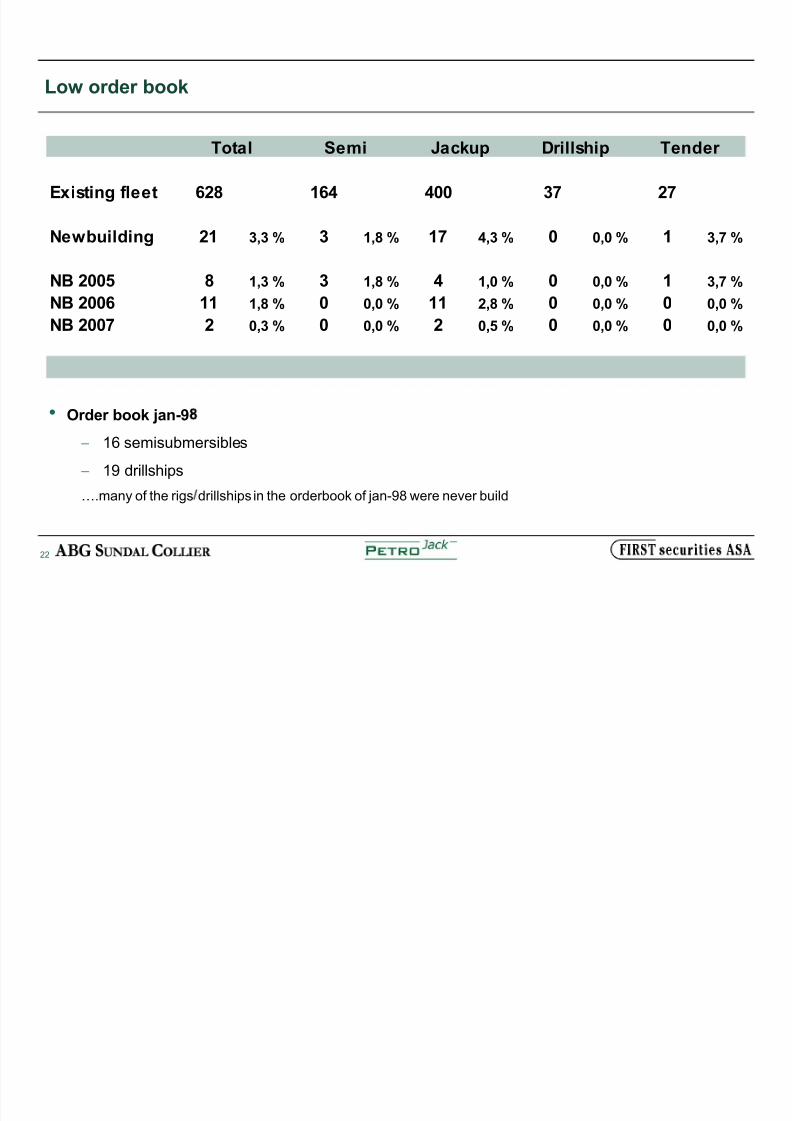

Low order book

Order book jan-9 16 semisubmersibles

19 drillships

«.many of the rigs drillships in the orderbook of jan-98 were never build

Existing fleet 628 164 400 37 27

Newbuilding 21 3,3 % 3 1,8 % 17 4,3 % 0 0,0 % 1 3,7 %

NB 2005 8 1,3 % 3 1,8 % 4 1,0 % 0 0,0 % 1 3,7 %

NB 2006 11 1,8 % 0 0,0 % 11 2,8 % 0 0,0 % 0 0,0 %

NB 2007 2 0,3 % 0 0,0 % 2 0,5 % 0 0,0 % 0 0,0 %

Tender Total Semi Jackup Drillship

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 23/38

23

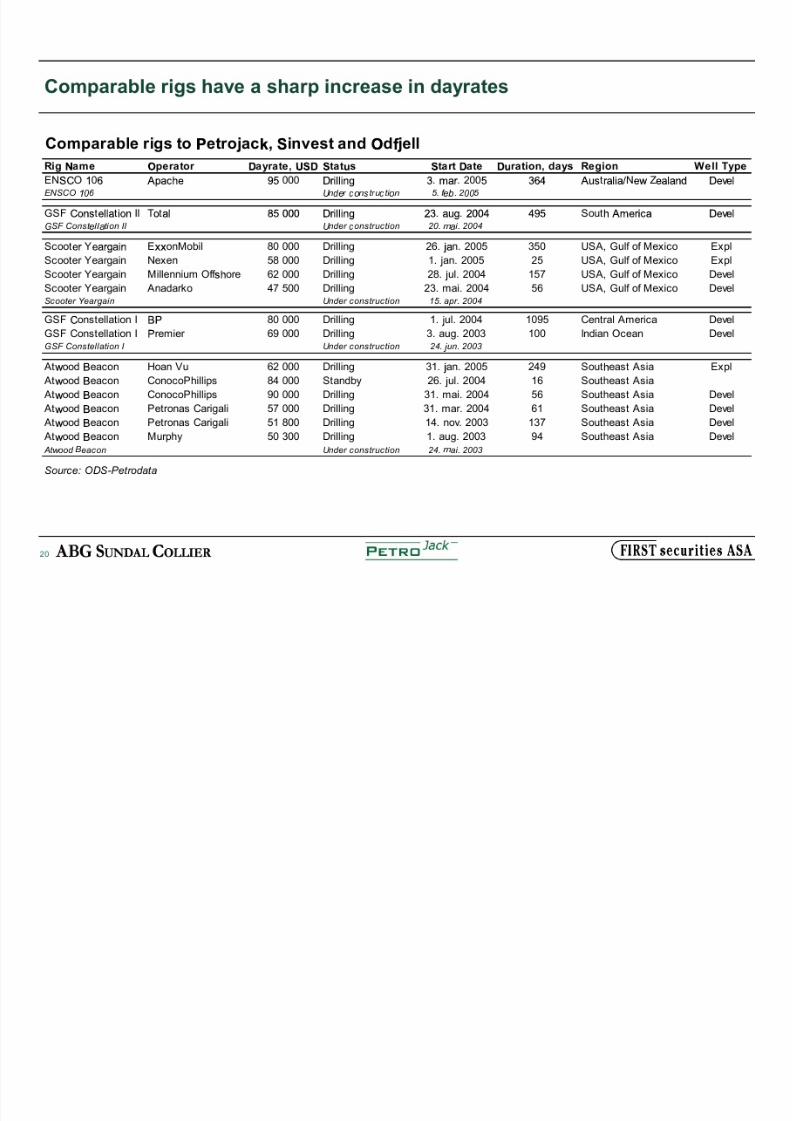

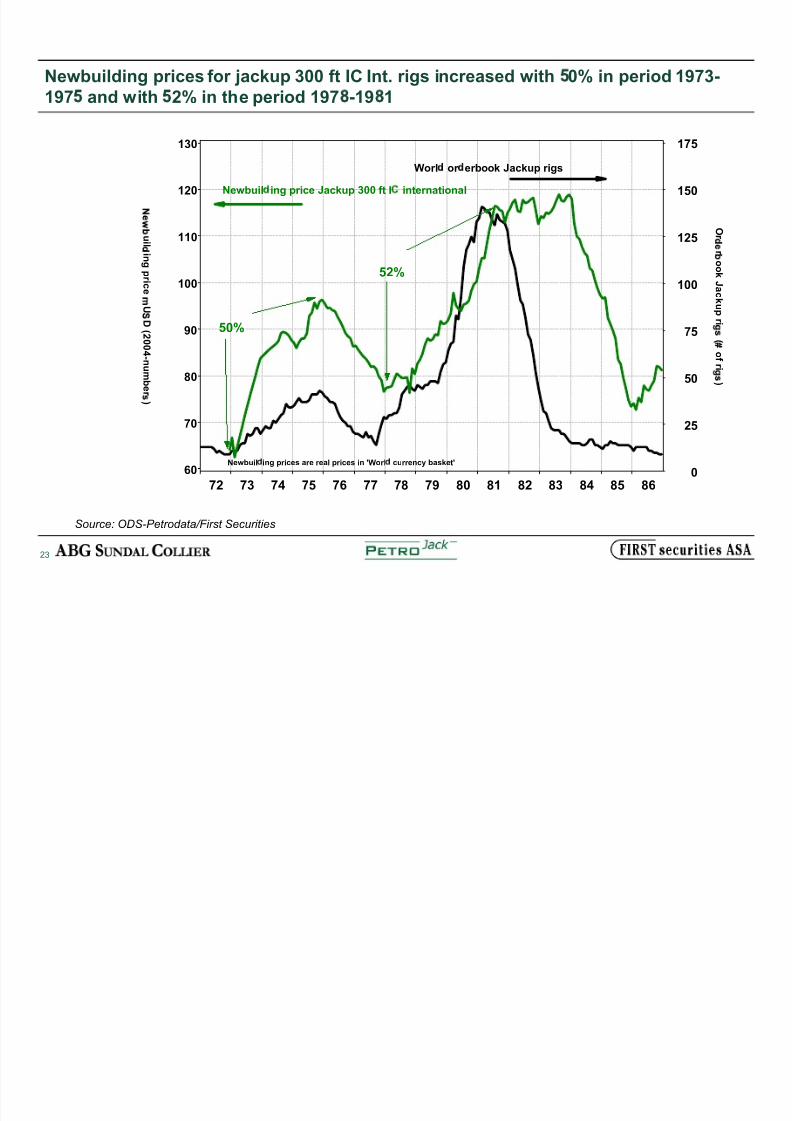

Newbuilding prices for jackup 300 ft IC Int. rigs increased with 0% in period 1973-197 and with 2% in the period 197 -19 1

Source: ODS-Petrodata/First Securities

72 73 74 75 76 77 78 79 80 81 82 83 84 85 86

Or

r

o o

k J a ck u pr i

(

of r i

)

0

25

50

75

100

125

150

175

ui l i n g pr i c e

U

D ( 2 0 0 4 -n um b er

)

60

70

80

90

100

110

120

130

Newbuil

ing prices ar e r eal prices in 'Worl

curr ency basket'

Worl or er book Jackup rigs

Newbuil ing price Jackup 300 ft I inter national

52%

50%

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 24/38

24

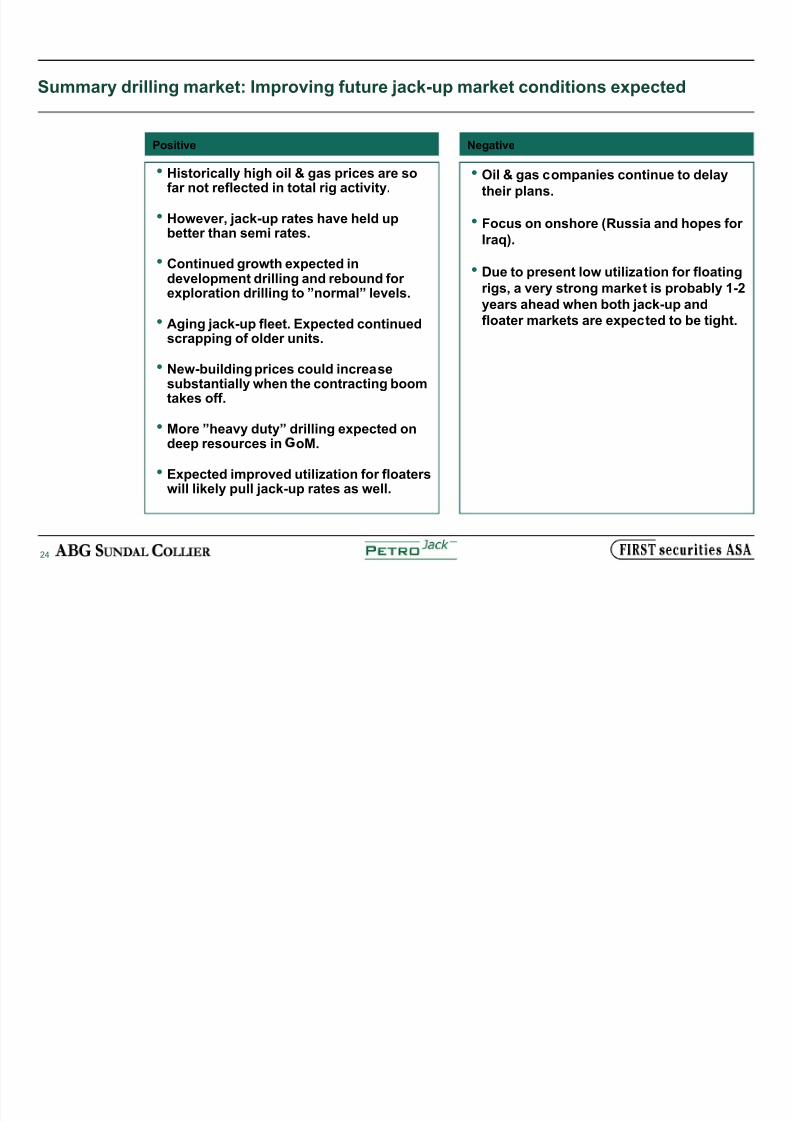

Positive Negative

Historically high oil & gas prices are sofar not reflected in total rig activity.

However, jack-up rates have held upbetter than semi rates.

Continued growth expected in

development drilling and rebound for exploration drilling to ́ normal´ levels.

Aging jack-up fleet. Expected continuedscrapping of older units.

New-building prices could increasesubstantially when the contracting boomtakes off.

More ́ heavy duty´ drilling expected ondeep resources in oM.

Expected improved utilization for floaterswill likely pull jack-up rates as well.

Summary drilling market: Improving future jack-up market conditions expected

Oil & gas companies continue to delaytheir plans.

Focus on onshore (Russia and hopes for Iraq).

Due to present low utilization for floatingrigs, a very strong market is probably 1-2years ahead when both jack-up andfloater markets are expected to be tight.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 25/38

25

Agenda

I. Introduction

II. Transaction

III. Market

IV. Company

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 26/38

26

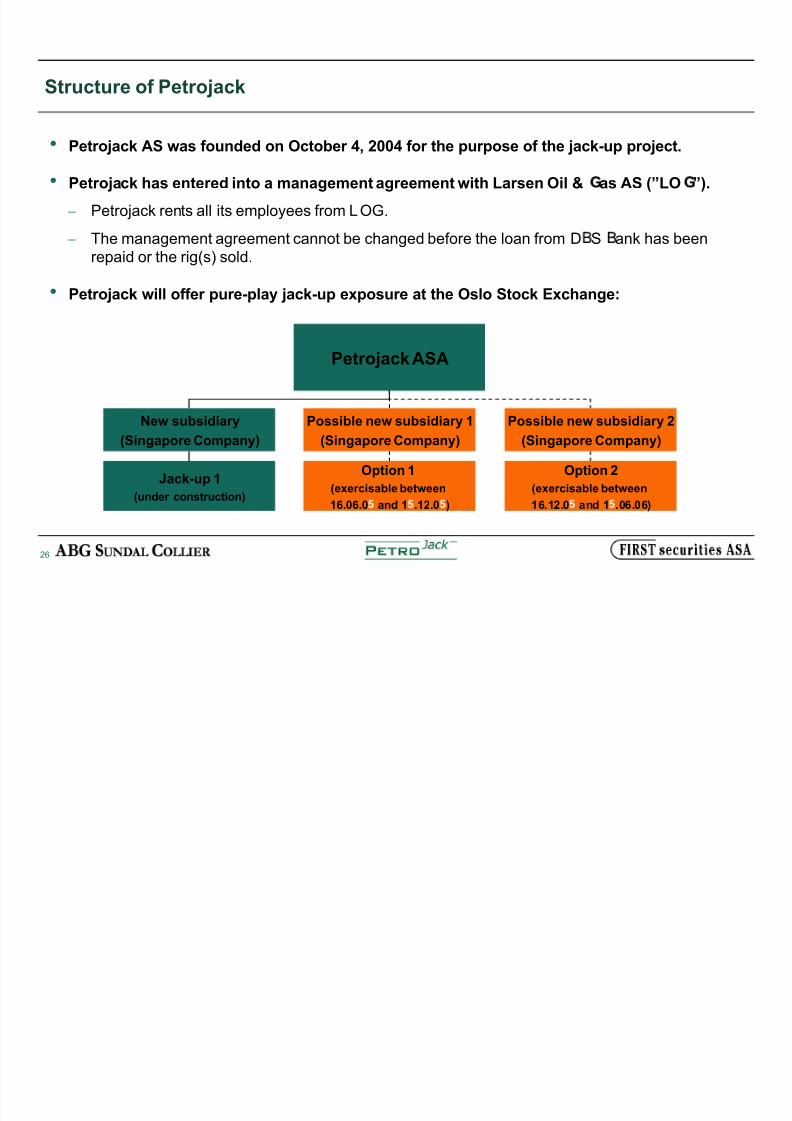

Structure of Petrojack

Petrojack AS was founded on October 4, 2004 for the purpose of the jack-up project.

Petrojack has entered into a management agreement with Larsen Oil & as AS (´LO ´).

Petrojack rents all its employees from LOG.

The management agreement cannot be changed before the loan from D S ank has beenrepaid or the rig(s) sold.

Petrojack will offer pure-play jack-up exposure at the Oslo Stock Exchange:

Petrojack ASA

Jack-up 1

(under construction)

Option 1

(exercisable between

16.06.0 and 1 .12.0 )

Option 2

(exercisable between

16.12.0 and 1 .06.06)

New subsidiary

(Singapore Company)

Possible new subsidiary 1

(Singapore Company)

Possible new subsidiary 2

(Singapore Company)

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 27/38

27

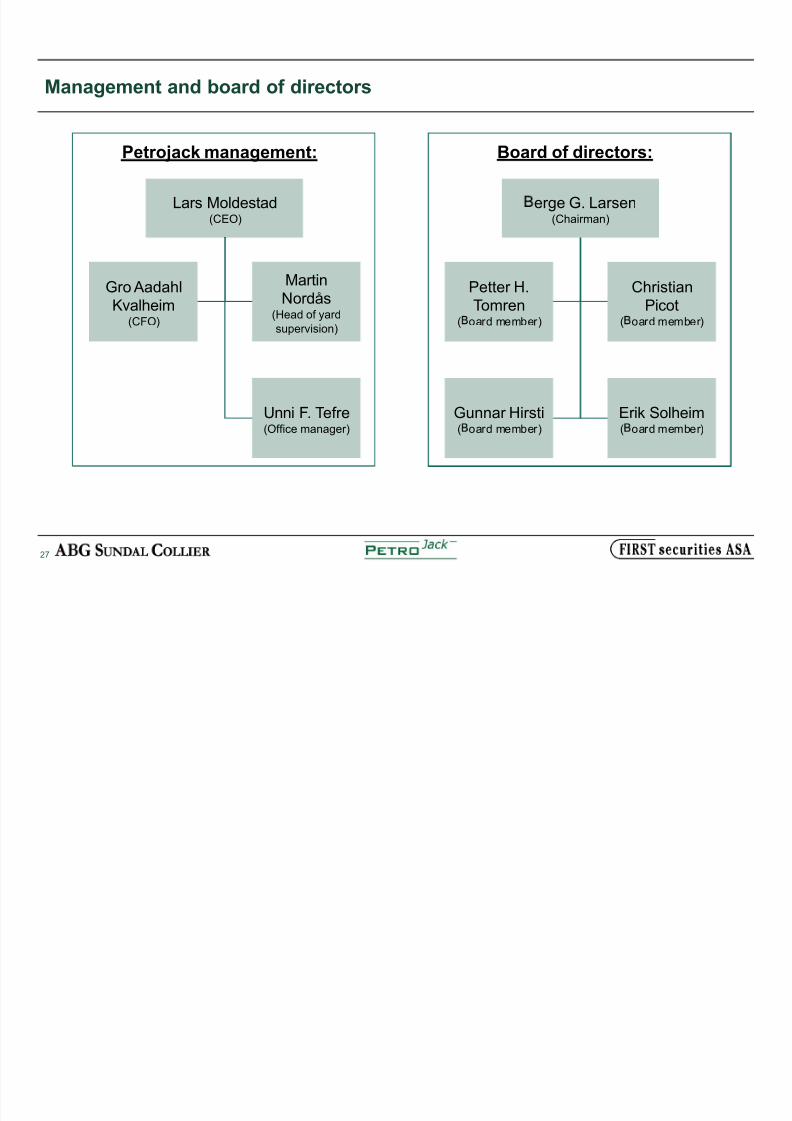

Management and board of directors

Lars Moldestad(CEO)

Petrojack management:

Gro AadahlKvalheim

(CFO)

MartinNordås

(Head of yard

supervision)

Unni F.Tefre(Office manager)

erge G. Larsen(Chairman)

Board of directors:

Petter H.Tomren

( oard member)

ChristianPicot

( oard member)

Gunnar Hirsti( oard member)

Erik Solheim( oard member)

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 28/38

28

Profiles of key personnel

ro Aadahl Kvalheim (born in 196 )

CFO of Petrojack (joining LO inthe second quarter of 200 ).

Previous employers include Ernst & Young (1993 ± present), Oslo andBergen offices.

Holds a master degree in financialauditing (Høyere revisorstudium,NHH).

Resides in Bergen, Norway.

Lars Moldestad (born in 1964)

CEO of Petrojack.

CEO of LO and acting asmanaging director of PetroliaDrilling ASA, which is under amanagement agreement with LO .

Previous employers include OdfjellDrilling and Finansbanken.

Holds a degree from the NorwegianSchool of Management (BI).

Resides in Bergen, Norway.

Martin Nordås (born in 19 9)

Head of Petrojack¶s yardsupervision team.

Independent consultant hired by

LO as head of the yard

supervision team during the

Construction Period.

Acted as Petrojack¶s representativein connection with the finalnegotiations of the Construction

Contract.

Has considerable international rigand offshore experience including

project management.

Holds an engineering degree from

Agder Regional College in Norway.

Resides in Bergen, Norway.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 29/38

29

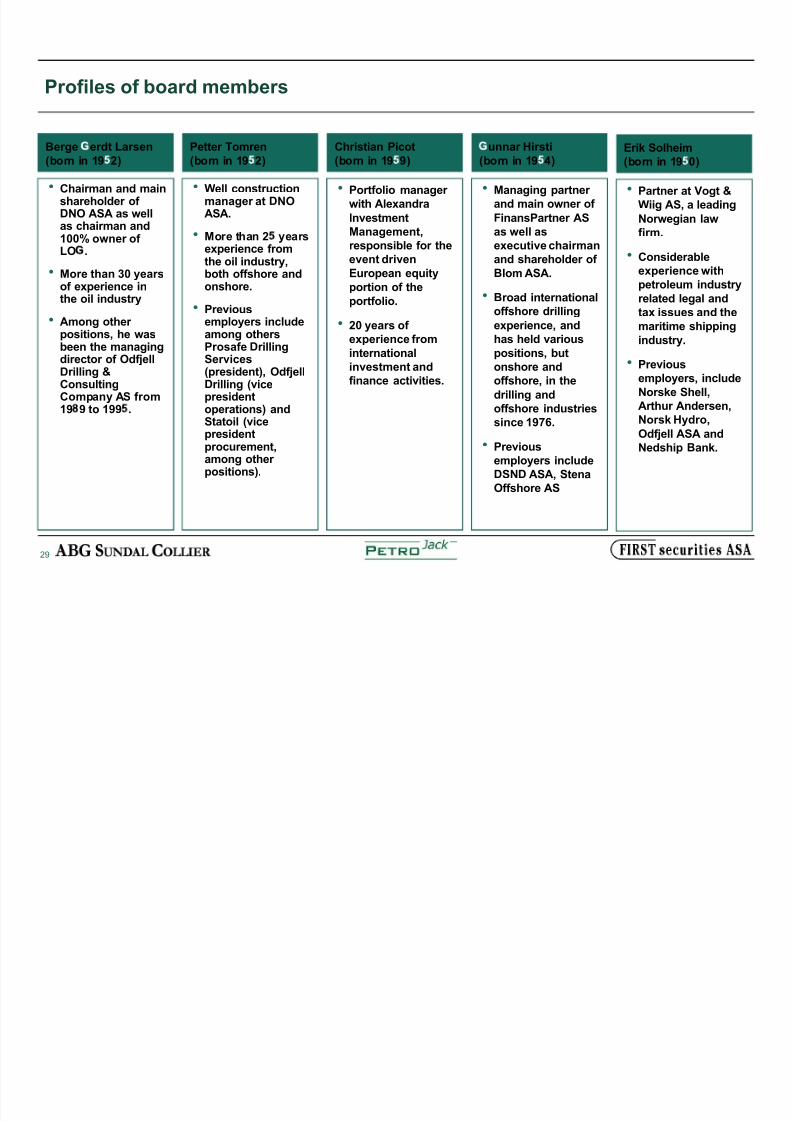

Profiles of board members

Petter Tomren(born in 19 2)

Well constructionmanager at DNOASA.

More than 2 yearsexperience fromthe oil industry,both offshore andonshore.

Previousemployers includeamong othersProsafe DrillingServices(president), OdfjellDrilling (vicepresidentoperations) and

Statoil (vicepresidentprocurement,among other positions).

Berge erdt Larsen(born in 19 2)

Chairman and mainshareholder of DNO ASA as wellas chairman and100% owner of LO .

More than 30 yearsof experience inthe oil industry

Among other positions, he wasbeen the managingdirector of OdfjellDrilling &ConsultingCompany AS from19 9 to 199 .

unnar Hirsti(born in 19 4)

Managing partner and main owner of

FinansPartner ASas well asexecutive chairmanand shareholder of Blom ASA.

Broad internationaloffshore drilling

experience, andhas held various

positions, butonshore andoffshore, in the

drilling andoffshore industries

since 1976.

Previousemployers includeDSND ASA, StenaOffshore AS

Erik Solheim(born in 19 0)

Partner at Vogt &Wiig AS, a leading

Norwegian lawfirm.

Considerableexperience with

petroleum industryrelated legal andtax issues and the

maritime shipping

industry.

Previousemployers, include

Norske Shell,Arthur Andersen,

Norsk Hydro,Odfjell ASA andNedship Bank.

Christian Picot(born in 19 9)

Portfolio manager with Alexandra

InvestmentManagement,responsible for theevent driven

European equity

portion of the

portfolio.

20 years of experience from

internationalinvestment andfinance activities.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 30/38

30

Brief description of Larsen Oil & as

LO is a Norwegian company 100% owned by Berge erdt Larsen with thefollowing operations:

Business development and investments within the oil and offshore industries.

ental services renting production e uipment to offshore companies.

Management and administrative services for third parties.

LO is also the provider of management services to Petrolia Drilling (PDR),an offshore company listed on the Oslo Stock Exchange.

The project is debt financed, although non-recourse, on the standing andtrack record of Berge erdt Larsen.

It is a condition of the loan facility from DBS Bank that LO maintains

management control over Petrojack ASA until the loan is repaid.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 31/38

31

Jurong is a solid shipyard

Jurong, Singapore, is a subsidiary of a major Asian engineering services groupcalled SembCorp Marine (SCM), one of the world¶s leading offshore rigconstruction groups.

Apart from Jurong, the SCM roup inlcudes other well known shipyards suchas PPL and Sembawang.

The SCM Group PPL is one of the most recognized rig-builders, having

consctructed a significant number of rigs of various types and sizes.

The SCM Group PPL will deliver similar jack-up rigs to Sinvest and Awilco before

delivery to Petrojack.

Jurong is currently building two Semis for GlobalSantaFe (among other projects).

PPL (the builder of Awilco and Sinvest rigs) is the issuer and contracting party for the Options Agreement. PPL will provide total engineering of all the igs and

support JSPL during construction of critical components.

J urong

Shipyard

(Singapore):

Source: Jurong, ODS-Petrodata

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 32/38

32

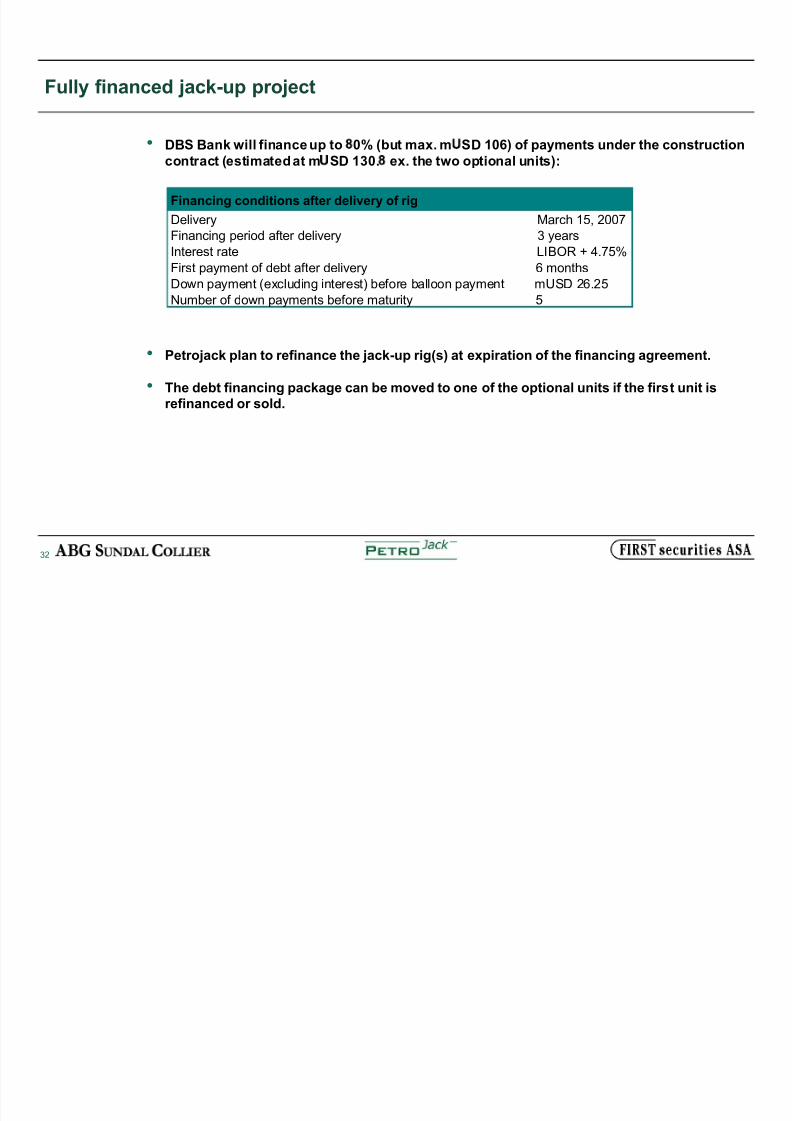

Fully financed jack-up project

DBS Bank will finance up to 0% (but max. m SD 106) of payments under the constructioncontract (estimated at m SD 130. ex. the two optional units):

Petrojack plan to refinance the jack-up rig(s) at expiration of the financing agreement.

The debt financing package can be moved to one of the optional units if the first unit isrefinanced or sold.

Financing conditions after delivery of rig

Delivery March 15, 2007

Financing period after delivery 3 years

Interest rate LIBOR + 4.75%

First payment of debt after delivery 6 months

Down payment (excluding interest) before balloon payment mUSD 26.25Number of down payments before maturity 5

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 33/38

33

Main rig specifications of jack-up to be built by Jurong

Design: Baker Pacific class mobile offshore self-elevating drilling unit.

Operating water depth: Shallow water / 37 ft.

Drilling depth: 30,000 ft.

Max. combined variable load: 3,401 MT.

Slush pumps: 3 pumps of 2,200 hp each.

AC power: diesel driven generators.

Cantilever extension: 21,33 meters.

Accomodation capacity: 120 persons.

Potential geographical foot-print of design: The ulf of Mexico, Indian Ocean,Southern North-Sea, Coast of the Middle-East, Mediterranean,West Africa(Nigeria-Angola range), Offshore India, Offshore Australia, Offshore NewZealand, South-East Asia.

Operational season: All year in most relevant areas of operation.

J urong jack-

up:

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 34/38

34

Price and conditions from Jurong/PPL

Total capital requirement

of approx.

USD 136 mill.

The option to

build a third

rig is not

subject to the

first option

being exercised.

Current capital

requirement

Financing requirement (m SD) Jack-up 1 Option 1 (*) Option 2

Rig price (incl. 0.8 spares) 123.3 125.4 129.2

Rig broker fees 2.0 2.0 2.0

Contract price (**) 125.3 127.4 131.2

Loose handling e uipment and other costs 3.0 3.0 3.0

Project management services 2.5 2.5 2.5

Financed costs 130.8 132.9 136.7

Available debt financing (up to 80%) (***) 104.6 79.7 82.0

Construction period (months from effective date) 27 27 27 Underwriting fee (1.5% flat) 1.6 1.2 1.2

Agency fee (mUSD 0.02 p.a.) 0.05 0.05 0.05

Commitment fee - (0.5% p.a.) 1.2 0.9 0.9

Building interests (****) N.a. 2.4 2.4

Total financing construction period 2.8 4.5 4.6

orking capital re uirement 1.0 1.0 1.0

Misc. financial services 1.3 1.0 1.0

Total project cost financing re uirement 135.9 139.4 143.4

Net equity requirement 31.3 9.7 61.3

(*) Assumed to be exercised after 12 months (end of option period) at contract price of mUSD 127.4. Contract price is mUSD 126.5 i

exercised in 7th, 8th or 9th month of option period.

(**) Concerning the options, there are risks of increased contract prices in case the price of the drilling package and, for option 2 only

also adjustment for steel prices if in excess of USD 620 per tonne.

Est. future capital requirement if

options are to be exercised

(****) Petrojack has one debt financing package which can be moved from the first rig to one of the optional units along with the

installment structure to the shipyard (20% of rig price before delivery and 80% at delivery). However, if the financing package is not

moved the optional units will have 5 installments à 20% and Petrojack will have to draw down debt before delivery and interests will

accrue. e used a LIBOR of approx. 3.3% + spread of 2% as a proxy for future interests.

(***) Max. debt financing available through the financing package from the shipyard is mUSD 106. Although the financing package

can be transferred from the first rig to one of the option rigs, we have chosen to present estimates getting debt financing directly fro

an external bank for the options. According to a leading international bank, we can get 60% debt financing for a rig under

construction without contract at a spread of 2%.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 35/38

35

Related party issues

Petrojack has entered into a management agreement with LO :

Berge Gerdt Larsen owns 100% of LOG and has significant direct and indirect

ownership stakes in PDR.

LOG, which is Lars Moldestad¶s employer, acts as manager for PDR in addition toPetrojack.

The Management Agreement has been entered into on market terms:

For pre-delivery yard supervision (project management), the manager is granted a fixedfee in the amount of mUSD 2.5. The owner shall further pay a management fee to themanager corresponding to a margin of 5% of the actual costs incurred (see the appendixfor further details and a definition of the management agreement).

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 36/38

36

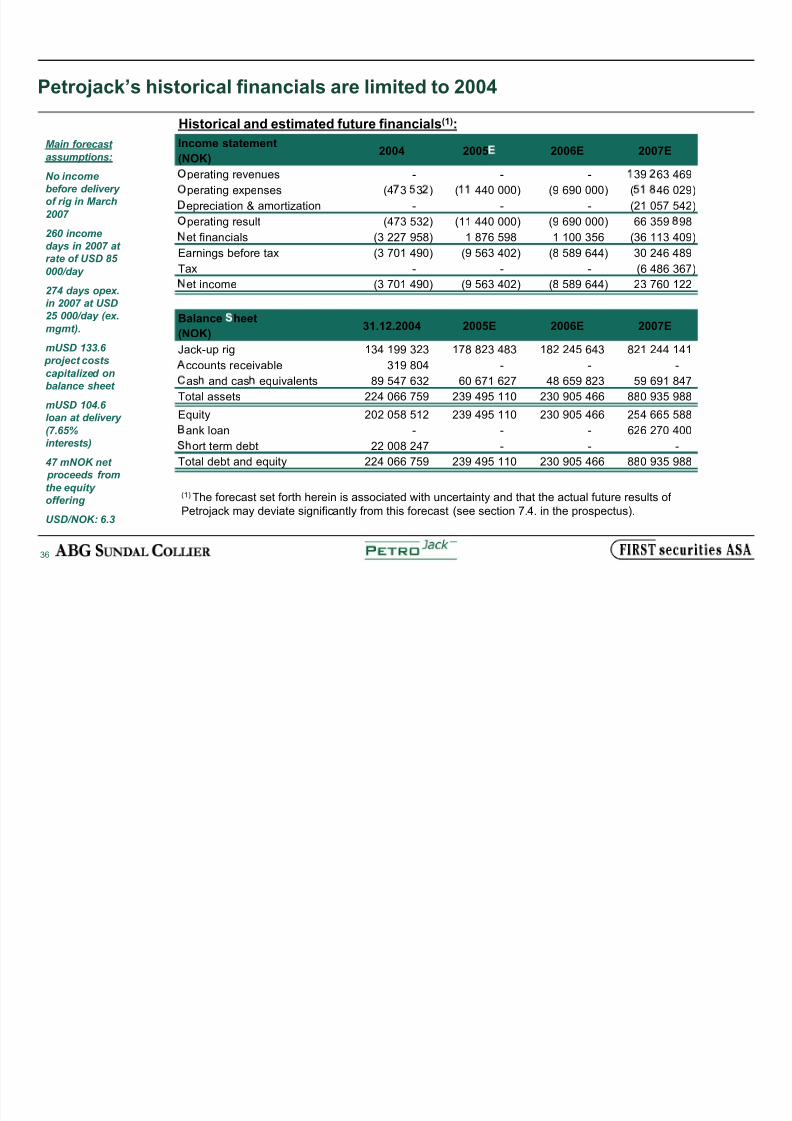

Petrojack¶s historical financials are limited to 2004

Income statement(NOK)

2004 2005 2006E 2007E

per ating r evenues - - - 39 63 469

per ating expenses (4 3 3 ) ( 440 000) (9 690 000) ( 46 029)

epr eciation & amortization - - - (21 057 542)

per ating r esult (473 532) (11 440 000) (9 690 000) 66 359 98

et financials (3 227 958) 1 876 598 1 100 356 (36 113 409)

Ear nings bef or e tax (3 701 490) (9 563 402) (8 589 644) 30 246 489

Tax - - - (6 486 367)

et income (3 701 490) (9 563 402) (8 589 644) 23 760 122

Balance heet

(NOK)31.12.2004 2005E 2006E 2007E

Jack-up rig 134 199 323 178 823 483 182 245 643 821 244 141

ccounts r eceivable 319 804 - - -

as and cas equivalents 89 547 632 60 671 627 48 659 823 59 691 847

Total assets 224 066 759 239 495 110 230 905 466 880 935 988

Equity 202 058

512 239

49

5 110 23

0 9

05 466 254 665 588

ank loan - - - 626 270 400

ort ter m debt 22 008 247 - - -

Total debt and equity 224 066 759 239 495 110 230 905 466 880 935 988

M ain forecast assumptions:

No income

before delivery

of rig in M arch

2007

260 income

days in 2007 at

rate of USD 85

000/day

274 days opex.

in 2007 at USD

25 000/day (ex.

mgmt).

mUSD 133.6

project costs

capitalized on

balance sheet

mUSD 104.6

loan at delivery (7.65%

interests)

47 mNOK net

proceeds from

the equity

offering

USD/NOK: 6.3

(1) The forecast set forth herein is associated with uncertainty and that the actual future results of

Petrojack may deviate significantly from this forecast (see section 7.4. in the prospectus).

Historical and estimated future financials(1):

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 37/38

37

A number of risk factors may adversely affect Petrojack (1/2)

Forward-looking statements ± forecasted financial statements: The forecast set forth herein is associated with uncertainty and that the actual future results of

Petrojack may deviate significantly from this forecast.

Lack of historical financial information:

Petrojack was founded on October 4, 2004 and has limited operating history. The historicalfinancial statements included herein may therefore not be useful in estimating the Company¶sfuture financial results.

Significant investments:

Petrojack has ordered a jack-up rig with a total project cost of mUSD 135.9. Petrojack has nooperating income or operating cash flow to finance the jack-up rig and is dependent on fundingfrom shareholders investors or banks.

Significant financial leverage:

Petrojack intends to borrow up to MUSD 106 to finance the jack-up rig. If Petrojack fails to

repay or refinance the loan facility, additional e uity financing may be re uired.

Risks related to loan agreement:

The loan agreement includes terms, conditions and covenants that may impose restrictions onthe operations of Petrojack.

I f any of these

risks and

uncertainties

actually

occurs, the

business,

operating

results and

financial

condition of

Petrojack

may be

materially and

adversely

affected.

8/8/2019 Investor Presentation v4

http://slidepdf.com/reader/full/investor-presentation-v4 38/38

38

A number of risk factors may adversely affect Petrojack (2/2)

Risks related to possible tax liabilities: Under the loan agreement, Petrojack is obliged to create a new Singapore subsidiary, and

transfer important contracts thereto by way of novation. To mitigate Norwegian tax risk, thetransfer should be executed without delay.

Dependence on external parties:

Petrojack has no staff or employees and is conse uently dependent on external parties toundertake the management of the Company. Such arrangement may reduce the controlfunctions of the Company.

Risks related to the management agreement:

The loan agreement includes covenants and provisions implying that LOG shall remainmanager of Petrojack for as long as the loan agreement remains in effect.

Risks related to the construction contract:

Any delays, cost overruns and technical problems related to the construction contract couldhave a material adverse effect on the Company and its financial position.

Risks related to the offer: The future share price development of Petrojack may be volatile due to various factors,

including fluctuations in Petrojack¶s results. There can be no guarantee that investorssubscribing for shares in the offering will be able to sell their shares in the future at a priceexceeding the final subscription price in the offering.