investment risk and return under renewable decarbonization of a power market

TRANSCRIPT

This article was downloaded by: [University of West Florida]On: 11 October 2014, At: 07:08Publisher: Taylor & FrancisInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office:Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

Climate PolicyPublication details, including instructions for authors and subscriptioninformation:http://www.tandfonline.com/loi/tcpo20

Investment risk and return under renewabledecarbonization of a power marketJosé I. Muñoz a & Derek W. Bunn ba Universidad de Castilla – La Mancha , E.T.S. de Ingenieros Industriales,13071 , Ciudad Real , Spainb London Business School , Sussex Place, Regent's Park, London , NW1 5SA ,UKPublished online: 31 Jan 2013.

To cite this article: José I. Muñoz & Derek W. Bunn (2013) Investment risk and return under renewabledecarbonization of a power market, Climate Policy, 13:sup01, 87-105, DOI: 10.1080/14693062.2012.750473

To link to this article: http://dx.doi.org/10.1080/14693062.2012.750473

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”)contained in the publications on our platform. However, Taylor & Francis, our agents, and ourlicensors make no representations or warranties whatsoever as to the accuracy, completeness, orsuitability for any purpose of the Content. Any opinions and views expressed in this publicationare the opinions and views of the authors, and are not the views of or endorsed by Taylor &Francis. The accuracy of the Content should not be relied upon and should be independentlyverified with primary sources of information. Taylor and Francis shall not be liable for anylosses, actions, claims, proceedings, demands, costs, expenses, damages, and other liabilitieswhatsoever or howsoever caused arising directly or indirectly in connection with, in relation to orarising out of the use of the Content.

This article may be used for research, teaching, and private study purposes. Any substantialor systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, ordistribution in any form to anyone is expressly forbidden. Terms & Conditions of access and usecan be found at http://www.tandfonline.com/page/terms-and-conditions

Investment risk and return under renewabledecarbonization of a power marketJOSE I. MUNOZ1, DEREK W. BUNN2*

1 Universidad de Castilla – La Mancha, E.T.S. de Ingenieros Industriales, 13071 Ciudad Real, Spain2 London Business School, Sussex Place, Regent’s Park, London NW1 5SA, UK

How does financial performance risk affect investments in low-carbon electricity-generating technologies to achieve climatepolicy targets? A detailed risk simulation of price formation in the Great Britain wholesale power market is used to show that theincreasing replacement of fossil facilities with wind, ceteris paribus, may cause a deterioration of the financial risk–return per-formance metrics for incremental investments. Low-carbon investments appear to be high risk, low return, and as such mayrequire a progressively higher level of support over time than envisaged by the conventional degression trajectories. Theincreasing riskiness of the wholesale market will to some extent offset the benefits of lower capital costs and operational effi-ciencies if investors need to satisfy cautious debt coverage ratios alongside positive expected returns. This increased risk isadditional to the well-known ‘merit order effect’ of low-carbon investments progressively depressing wholesale prices and hencetheir expected investment returns.

Policy relevancePolicy support for renewable technologies such as wind is usually based upon levelized costs and is expected to reduce overtime as capital costs and operational efficiencies improve. However, levelized costs do not take full account of the risk aversionthat investors may have in practice. Expected policy support reductions may be moderated to some extent by the increasedfinancial performance risk that intermittent technologies bring to the power market. The annual risk-return profiles for incrementalinvestments deteriorate for all technologies as wind replaces fossil fuels. This extra risk premium will need to be incorporated intoevaluating policy incentives for new investments in a decarbonizing power market.

Keywords: coal; financing; incentives; investment; risk; wind power

1. Introduction

Governments have introduced a variety of policy interventions and selective support schemes to

reduce carbon emissions from the power sector, and at the same time have maintained policy commit-

ments to liberalized, competitive markets. The interaction of market and policy risks has thus emerged

as an important consideration for investors in the sector. The effects of rapid structural changes, market

reforms, and innovations on the risks and financial performances of both existing and prospective

assets are crucial to market participants and policy makers. Thus, it is now widely recognized that

increased penetration of wind and solar generation has led, and will continue to lead, to substantial

B *Corresponding author. Email: [email protected]

At the time of publication Jose I. Munoz is also member of Instituto de Investigaciones Energeticas UCLM

Vol. 13, No. S01, S87–S105, http://dx.doi.org/10.1080/14693062.2012.750473

B research article

# 2013 Taylor & Francis

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

changes in the wholesale market dynamics with greater price volatility and different operational

regimes for existing power plants (e.g. Green & Vasilakos, 2010; Hirth, 2012; Poyry, 2009; Saenz de

Miera, del Rio Gonzalez, & Vizcaıno, 2008; Sensfuß, Ragwitz, & Genoese, 2008). More fundamentally,

with a greater penetration of renewables (and perhaps nuclear), questions are increasingly being asked

regarding the ability of the typical wholesale energy market to deliver attractive returns for investors as

the sector moves to high-capital/low-operating-cost (and also intermittent) technologies. In Britain,

this has motivated substantial proposals for market reform (DECC, 2011a).

A substantial amount of research has examined the various aspects of renewable investment and its

effects on the wholesale power markets, including a declining incremental wind value as decarboniza-

tion progresses (this is due to the ‘merit order’ effect as higher-price-setting plants are pushed out of

normal price-setting; e.g. Gowrisankaran, Reynolds, & Samano, 2011; Hirth, 2012; Obersteiner and

Saguan, 2010; Sensfuß et al., 2008). A key observation has been the increasing divergence between

the expected price that an intermittent producer can achieve and that of a firm producer as a result

of periods when high renewable output depresses prices. This feature is explored in the present

article, but with a specific focus on the risk–return profile for new and existing assets in the power

sector as it undergoes radical decarbonization. Many studies have reported on the relative levelized

costs of various new technologies in the context of incremental investment in existing systems and

within future scenarios. However, as Joskow (2012) argues, levelized costs are not appropriate for

renewable technologies; in particular, these costs generally use average values that do not explicitly

reflect financial performance risks and how those risks may evolve.

Risk (and its impact on investment decisions) has been extensively analysed from a portfolio perspec-

tive (e.g. Awerbuch, 2006) and with respect to the timing, synergy, and operational flexibility of invest-

ments from real options (Fleten & Ringen, 2009; Keppo & Lu, 2003; Reuter, Fuss, Szolgayova, &

Obersteiner, 2012). However, it remains an open question how investment risks and returns may

change over the lifetimes of investments as the wholesale price formation adapts to the low-carbon

structural changes. This is clearly crucial in understanding whether policies aimed at stimulating low-

carbon investment will be as successful as economic analysis might suggest. Thus, it is now becoming

widely recognized – especially following analyses from the real options perspectives (Kettunen, Bunn,

& Blyth, 2011; Yang et al., 2008) – that policy and market risks will tend to induce an extra premium

requirement for investment and also that the risk of financial underperformance (in terms of those oper-

ational cash flows that do not cover financing costs) needs to be considered explicitly as a key risk metric.

Policy models for investment in the power sector rarely provide an explicit treatment of risk. Often it

is assumed that, given a hurdle discount rate for the cost of capital, Net Present Value positive invest-

ments will happen; sometimes the hurdle rates are increased for project risk, but these tend to be ad hoc

suggestions (Redpoint, 2007). With this in mind, while there is clearly an absence of substantial long-

term empirical evidence regarding asset-specific risk for new low-carbon technologies, estimating an

appropriate discount rate is nevertheless commonly attempted. Accordingly, the performances of

renewable technology sector stocks as a whole have been extensively tracked and analysed for excess

returns. However, the indices (e.g. NEX; www.nexindex.com) include a greater number of project

developers and new technology start-ups than long-term operators. This indicates, unsurprisingly,

that renewable energy has high-risk characteristics that are similar to those of technology stocks in

general (Henriques & Sadorsky, 2008). However, it is not likely that this analogy will be applicable to

the operational phase of renewable projects when the utilities generally take ownership.

S88 Munoz and Bunn

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

The analysis presented here seeks to take into account the way in which renewable energy investors

will carefully examine both financial performance and risk in terms of debt coverage and conventional

returns on investment. Investors will typically submit to potential lenders a detailed financial planning

analysis of the performance of the project over its lifetime, and provide extensive commentary on the

market risks and the possibilities of failing to cover debt repayments from earnings (CPI, 2011). Simi-

larly, ratings agencies look at such ‘coverage’ ratios, which will influence the cost of borrowing

(Moody’s, 2009). Thus, if critical debt coverage ratios are not perceived to be achievable with an accep-

table level of probability, even Net Present Value positive investments will be considered too risky to

advance. This conclusion is consistent with the observations made in CPI (2011) that

investors are particularly concerned with the default risk of their investments. . . Providers of debt

conduct rigorous assessments of project risks. . . and the likelihood of those scenarios. The assessment

of default risk determines whether project debt is investment grade. (CPI, 2011, p. 3)

Furthermore, following practice, this ‘value-at-risk’ screening of investment opportunities is becom-

ing increasingly apparent in models of power investment (Fortin et al., 2008; Kettunen et al., 2011).

The analysis here examines how the annual financial performance of generating assets may change,

as the technology mix is progressively decarbonized. Specifically, a detailed analysis is provided of

the risk–return properties of various new wind investments that they would have had in Great

Britain (GB, i.e. the UK, excluding Northern Ireland1) in 2011 had wind replaced coal.

In Section 2 the fundamental risk simulation model used in the analysis is described and is then

applied to asset returns in the GB wholesale power market as it was in 2011. In Section 3, various evol-

utionary simulations for the risk–return profiles of specific assets are examined as the 2011 target year

wholesale market becomes more deeply decarbonized, with wind gradually replacing coal. In Section 4,

the financial performances of various wind and coal mixes are described and analysed. It is concluded

in Section 5 that the increasing risk of debt coverage falling below a critical level, in conjunction with

the average decline in expected returns on investment, may counteract the expectation that there will

be decreasing policy support for the extensive penetration of key low-carbon technologies. This mod-

erates the generally accepted views that (1) public support for low-carbon investments (which is

initially necessary to stimulate innovation) will decline over time as technology learning brings

down capital costs to ‘grid parity’ and (2) even if capital costs suffer from supply chain escalations in

their early years (as with offshore wind in the UK), the long-term market expectation will be one of

declining costs and associated government support (Greenacre, Gross, & Heptonstall, 2010).

2. Stochastic price risk model

In order to focus upon the annual financial performance risks of assets, particularly with respect to cov-

erage ratios under progressive decarbonization, the analysis developed here uses a target year model.

This allows for a probabilistic simulation of operational and price risks within a year, based upon

empirical data, so that annual operational profit probability distributions can be compared with annui-

tized financing costs. The technology mix in this target year is then varied in order to investigate, ceteris

Investment risk and return S89

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

paribus, how the risk–return balance is affected as wind gradually replaces coal. The model creates a

range of demand, supply, and commodity risks using Monte Carlo simulations.

The model used is not a forecasting model and it addresses neither long-term uncertainties2 (e.g.

fossil-fuel prices, endogenous learning and investment, changing demand profiles) nor policy risks.

Hence, no position is taken regarding how the relative economics of the various technologies might

evolve in the future, how government interventions might move risks to or from market participants,

nor how companies might adjust their portfolios and market structure to manage risks better.

The benefit of taking a target year approach and looking at intra-year performance risk is that it

avoids speculation about how future prices, investments, and policies may behave. The limitation of

this approach, of course, is that such longer-term risks are additional and require substantial consider-

ation when investment forecasts are undertaken.

Yearly price distributions were computed from the intersection of supply and demand, based upon a

full representation of the 2011 GB wholesale market. All 320 generating plants offering energy into the

market were included, from the very small biomass, onshore and offshore wind facilities to large

nuclear stations. Installed capacities were taken from DECC (2011b). Availabilities and heat rates

were consistent with various sources (Mott MacDonald, 2010; RedPoint, 2007). Hourly demand for

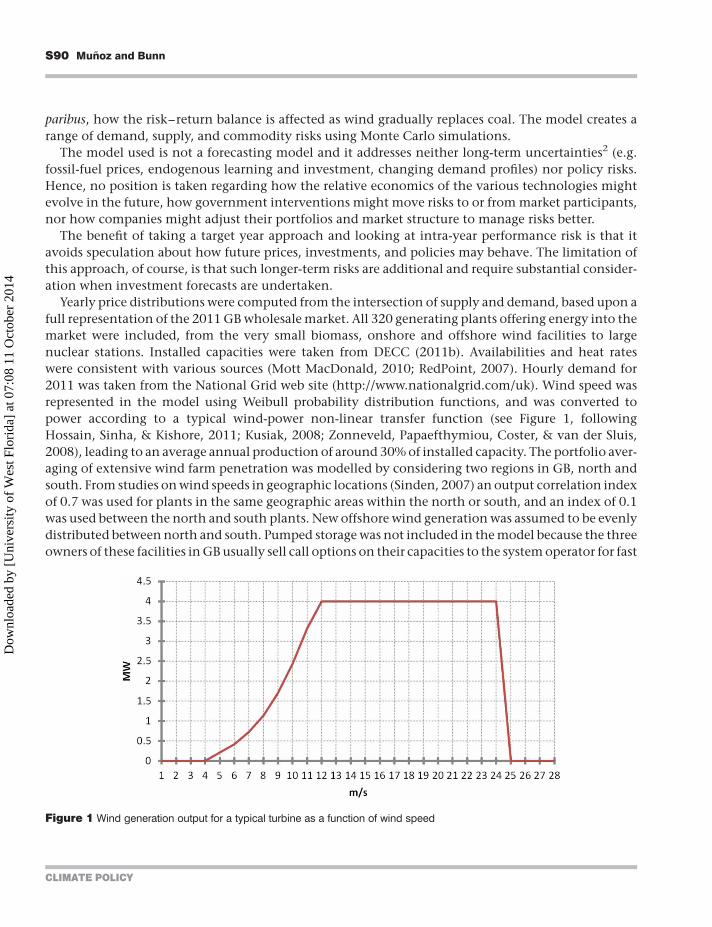

2011 was taken from the National Grid web site (http://www.nationalgrid.com/uk). Wind speed was

represented in the model using Weibull probability distribution functions, and was converted to

power according to a typical wind-power non-linear transfer function (see Figure 1, following

Hossain, Sinha, & Kishore, 2011; Kusiak, 2008; Zonneveld, Papaefthymiou, Coster, & van der Sluis,

2008), leading to an average annual production of around 30% of installed capacity. The portfolio aver-

aging of extensive wind farm penetration was modelled by considering two regions in GB, north and

south. From studies on wind speeds in geographic locations (Sinden, 2007) an output correlation index

of 0.7 was used for plants in the same geographic areas within the north or south, and an index of 0.1

was used between the north and south plants. New offshore wind generation was assumed to be evenly

distributed between north and south. Pumped storage was not included in the model because the three

owners of these facilities in GB usually sell call options on their capacities to the system operator for fast

Figure 1 Wind generation output for a typical turbine as a function of wind speed

S90 Munoz and Bunn

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

reserve and system balancing services, and so do not engage substantially in the day-ahead wholesale-

market price-setting.

With the economic recession following 2008, average demand and supply for the 2011 were 37.5 and

62 GW, respectively, which implies a relatively over-supplied market compared to previous years. In one

variation, demand was increased by 10% in order to match the supply–demand conditions more closely

to the ‘normal’ conditions envisaged before the recession (when installed capacity decisions were pre-

viously made by the generators). Initially, a competitive fundamental model was analysedon the assump-

tion that generators offer plants at short-run marginal costs (SRMC), which were taken as the heat rate

conversion of coal, gas, and oil for the fossil-fuel technologies. No allowances were made for start-up

costs, but the market price uncertainties in EU carbon allowances and GB Renewable Obligation Certifi-

cates (ROCs3) were included, as they have been empirically estimated around yearly means in recent

years. Transmission constraints do not factor into wholesale market prices, as they are part of the real-

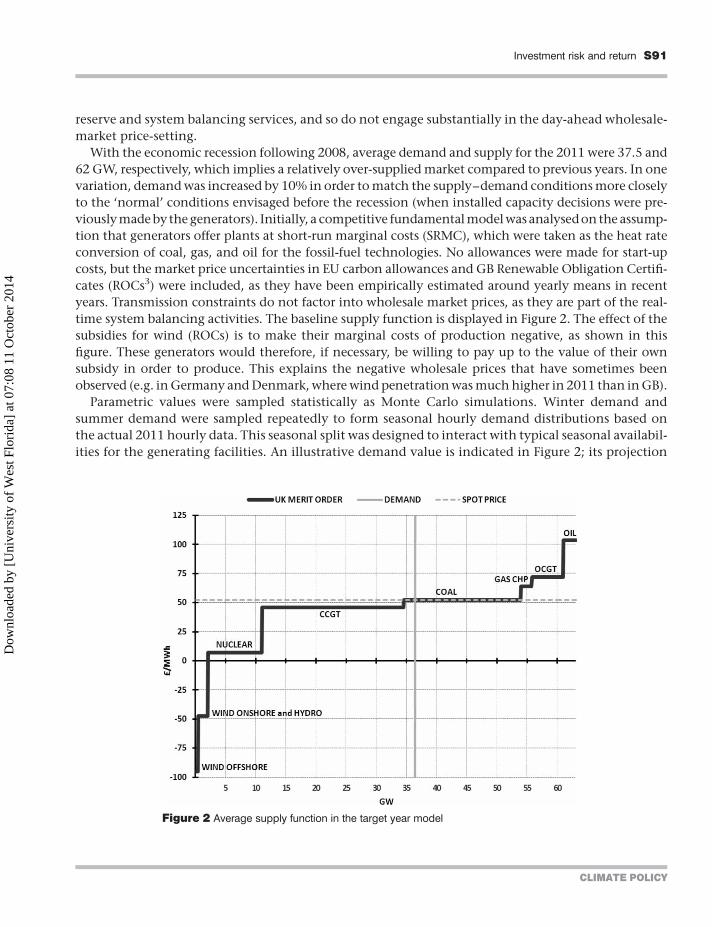

time system balancing activities. The baseline supply function is displayed in Figure 2. The effect of the

subsidies for wind (ROCs) is to make their marginal costs of production negative, as shown in this

figure. These generators would therefore, if necessary, be willing to pay up to the value of their own

subsidy in order to produce. This explains the negative wholesale prices that have sometimes been

observed (e.g. in Germany and Denmark, where wind penetration was much higher in 2011 than in GB).

Parametric values were sampled statistically as Monte Carlo simulations. Winter demand and

summer demand were sampled repeatedly to form seasonal hourly demand distributions based on

the actual 2011 hourly data. This seasonal split was designed to interact with typical seasonal availabil-

ities for the generating facilities. An illustrative demand value is indicated in Figure 2; its projection

Figure 2 Average supply function in the target year model

Investment risk and return S91

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

through the supply function into an SRMC market clearing price demonstrates the standard price for-

mation process. No demand elasticity was assumed. It is well known that offer prices into competitive

pools or power exchanges are, in practice, often above SRMC, particularly for lower load factor plants.

However, it is appropriate to start with SRMC as a competitive baseline. In fact, mark-ups of about 20%

in the price-setting range of technologies (non-renewables) gave a good calibration of average annual

price from this model to the actual average 2011 power exchange reference price. Figure 3 shows the

actual price distribution for 2011 (and the good fit of a log-logistic distribution), with a mean of

£49.9/MW and standard deviation of £4.9/MW. This is comparable with the 5000 iterations of the

simulation model used, as shown in Figure 4, which has a similar shape and range, a mean of £49.5/

MW and standard deviation of £5.0/MW.

Unplanned outages were simulated according to binomial distributions based upon average avail-

abilities. Fossil-fuel prices were sampled from log-normal distributions with intra-yearly standard devi-

ations and correlations estimated empirically over recent years. As this model is a target year risk

simulation, there was no speculation on diffusion processes for the commodities over the longer

term (which can be set by exogenous experimental variations with different annual mean values).

The base-case assumptions and parameters are shown in Tables 1 and 2.

The model simulates hourly market prices and utilizations for each plant, and returns statistical distri-

butions for the annual profit contributions for each plant in the system. These can also be aggregated by

company ownership. New investment performance was monitored in terms of annual profit contri-

butions, debt coverage ratios, and the probability that the debt coverage ratio falls below 1.2. The debt

coverage ratio is an annual value representing the ratio of annual operational profit contribution to

annuitized capital costs, where the annuitization depends on cost of capital and asset lifetime. A ratio

above 1 indicates that the asset has a positive return, which would be comparable to a Net Present

Value criterion. Following the risk simulation analysis, a probability distribution for this ratio was

Figure 3 Actual hourly price distribution for GB in 2011 (with log-logistic fit)

S92 Munoz and Bunn

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

obtained. Exceeding a ratio of 1.2 with 95% confidence was taken as an indicative criterion that may be

considered by analysts and ratings agencies to retain an investment grade (CPI, 2011). As a baseline,

100% debt financing of new assets and debt at 8% (pre-tax) were assumed over the life of the project.

Typically, onshore wind assets have been 80% debt-financed in GB, offshore rather less, while com-

bined cycle gas turbine (CCGT)/coal/nuclear have generally been on balance sheet. However, in order

Figure 4 Simulated price distribution with 20% non-renewable mark-ups

Table 1 Fossil fuels, carbon rights, and green credits distributions

Commodity Mean Standard deviation

Oil £70/bl 14

Gas £0.60/thm 12

Coal US$120/tonne 24

Carbon rights (EUAs) £14/tonne 3

Green certificates (ROCs) £50/tonne 3

Notes: EUAs, EU Allowance Unit; ROCs, Renewable Obligation Certificates.

Table 2 Estimated intra-year price correlations of fossil fuels

Correlations Oil Gas Coal

Oil 1 – –

Gas 0.631 1 –

Coal 0.861 0.628 1

Investment risk and return S93

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

to gain some rather fundamental comparative insights, these baseline assumptions were taken to provide

a reasonable and conservative proxy for the range of financial performance metrics that may be used in

practice (as, for leverage below 100%, higher equity returns than debt will generally be required). In any

particular case, a company’s idiosyncratic tax, leverage, amortization, and corporate circumstances will,

of course, be quite distinctive. The main investment parameters are shown in Table 3 and are consistent

with the various assumptions made in Redpoint (2007) and Mott MacDonald (2010).

3. Decarbonization effects on spot prices

Within a target year and its parameters, a decarbonization progression of replacing coal by offshore

wind, ceteris paribus, was investigated. Assuming an average availability of wind of 30%, firm gener-

ation was replaced according to this ratio in order not to change the average reserve margin in the

market. Figure 5 shows the evolution of the distribution of prices and the average annual base-load

price, based on 500 simulations. Initially, with very little replacement of the fossil fuels by wind, the

distributions around the average show some positive skew. However, because these simulations

assumed competitive behaviour, they exhibit none of the extreme spikes associated with market-

power effects and mark-ups seen in practice at times of scarcity. The model reflects what a very competi-

tive or tightly regulated market would deliver in terms of price risk. Evidently, as seen in Figure 5,

negative prices will become progressively more common if wind production becomes substantial

and continues to be given a subsidy through either green certificates (e.g. ROCs) or a feed-in tariff.

An interesting feature is the changing shape of the base-load price distribution. As observed in Figure

4, with relatively little wind in the base case (about 10% of energy delivered), the price distribution is

initially slightly positively skewed. Figure 5 indicates that this will become more negatively skewed as

the penetration increases, so – unlike conventional experience with power price risk and positive

spikes – base-load price risk and ‘spikiness’ emerges on the downside.

Figure 6 shows the baseline distribution of an individual peak hour (winter, 19.00 h) rather than the

daily average price (base-load). Typically, this would be skewed more to the right in practice, but is con-

strained by the assumption of SRMC. By contrast, Figure 7 – with all of the coal replaced by an equiv-

alent average amount of wind – has a more complex, multimodal shape. It is clear that the

combination of high wind output volatility and high demand causes regime switches in the price

setting, which in practice will create a need for discontinuous price forecasting and risk management

models around the evening peak.

Table 3 Main capital investment parameters

Investment parameter

Wind

Nuclear CCGTOffshore Onshore

Capital cost (£/kW) 2250 1200 3000 600

Life (years) 20 20 40 30

Annuitized (£/kW) 230 122 252 53

Note: CCGT, combined cycle gas turbine.

S94 Munoz and Bunn

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

Figure 8 shows the outage rates in TWh per year. Starting from a highly over-supplied initial con-

dition, significant outage rates do not materialize until about 50% (13 GW) of the coal has been

replaced, at which point it increases steeply. It is important to remember that the analysis here used

Figure 5 Competitive prices with wind gradually replacing coalNote: In the simulations, the inner dark bands are 5% and 95% limits and the outerlighter bands are max and min values.

Figure 6 Baseline distribution for winter evening peak (19.00 h)

Investment risk and return S95

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

Figure 8 Outage rates (TWh unserved) with progressive decarbonizationNote: In the simulations, the inner dark bands are 5% and 95% limits and the outerlighter bands are max and min values.

Figure 7 Distribution of winter evening peak (19.00 h) with 26 GW decarbonization

S96 Munoz and Bunn

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

a target year simulation based upon 2011, in which there was a historically large capacity margin. The

result is not meant to have forecasting implications other than indicating how the progressive replace-

ment of firm coal by intermittent wind preserves the same derated capacity margin, by eroding

reliability itself. However, the result is consistent with the short-term resource adequacy assessments

by the National Grid (NG, 2011). In the longer term, the National Grid forecasts higher expected

unserved energy levels due to anticipated lower derated capacity margins by 2015.

4. Simulated financial performances

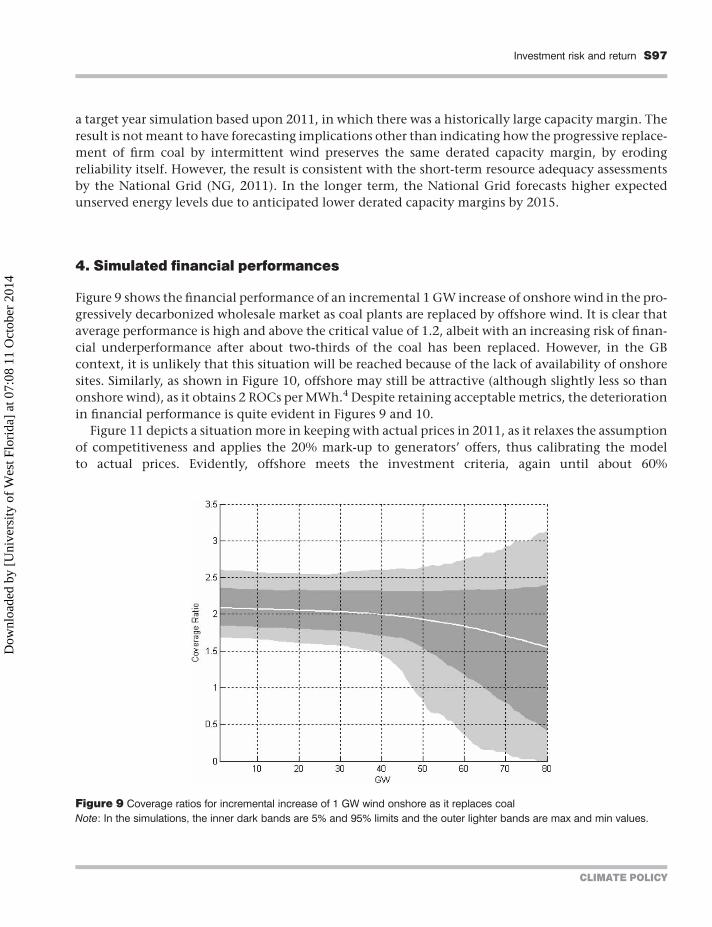

Figure 9 shows the financial performance of an incremental 1 GW increase of onshore wind in the pro-

gressively decarbonized wholesale market as coal plants are replaced by offshore wind. It is clear that

average performance is high and above the critical value of 1.2, albeit with an increasing risk of finan-

cial underperformance after about two-thirds of the coal has been replaced. However, in the GB

context, it is unlikely that this situation will be reached because of the lack of availability of onshore

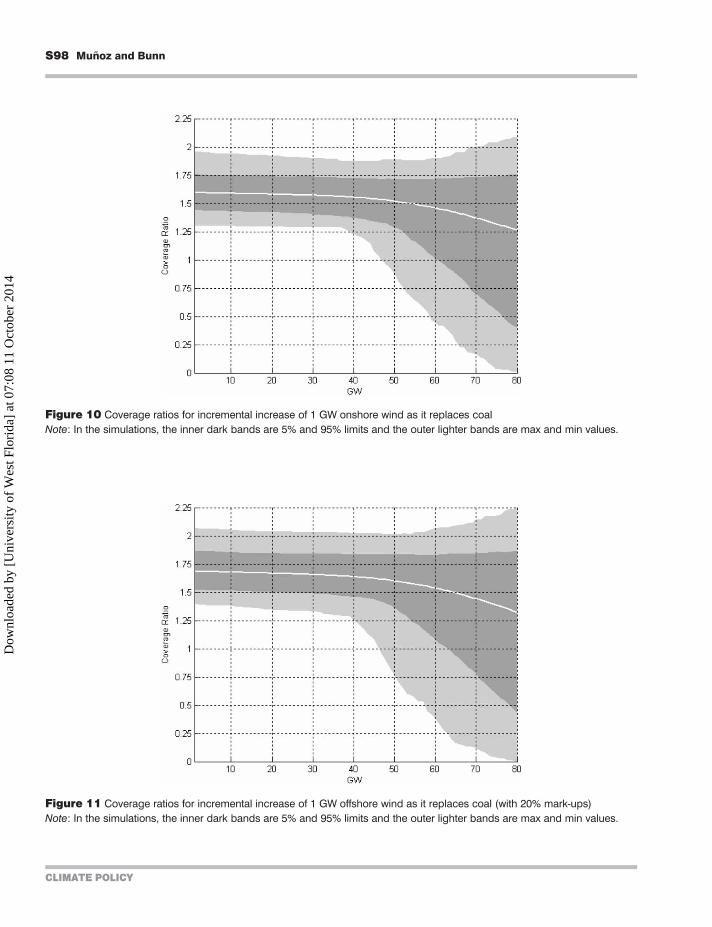

sites. Similarly, as shown in Figure 10, offshore may still be attractive (although slightly less so than

onshore wind), as it obtains 2 ROCs per MWh.4 Despite retaining acceptable metrics, the deterioration

in financial performance is quite evident in Figures 9 and 10.

Figure 11 depicts a situation more in keeping with actual prices in 2011, as it relaxes the assumption

of competitiveness and applies the 20% mark-up to generators’ offers, thus calibrating the model

to actual prices. Evidently, offshore meets the investment criteria, again until about 60%

Figure 9 Coverage ratios for incremental increase of 1 GW wind onshore as it replaces coalNote: In the simulations, the inner dark bands are 5% and 95% limits and the outer lighter bands are max and min values.

Investment risk and return S97

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

Figure 10 Coverage ratios for incremental increase of 1 GW onshore wind as it replaces coalNote: In the simulations, the inner dark bands are 5% and 95% limits and the outer lighter bands are max and min values.

Figure 11 Coverage ratios for incremental increase of 1 GW offshore wind as it replaces coal (with 20% mark-ups)Note: In the simulations, the inner dark bands are 5% and 95% limits and the outer lighter bands are max and min values.

S98 Munoz and Bunn

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

decarbonization, and this is consistent with the observed progress of actual active GB offshore invest-

ments in 2011–2012.

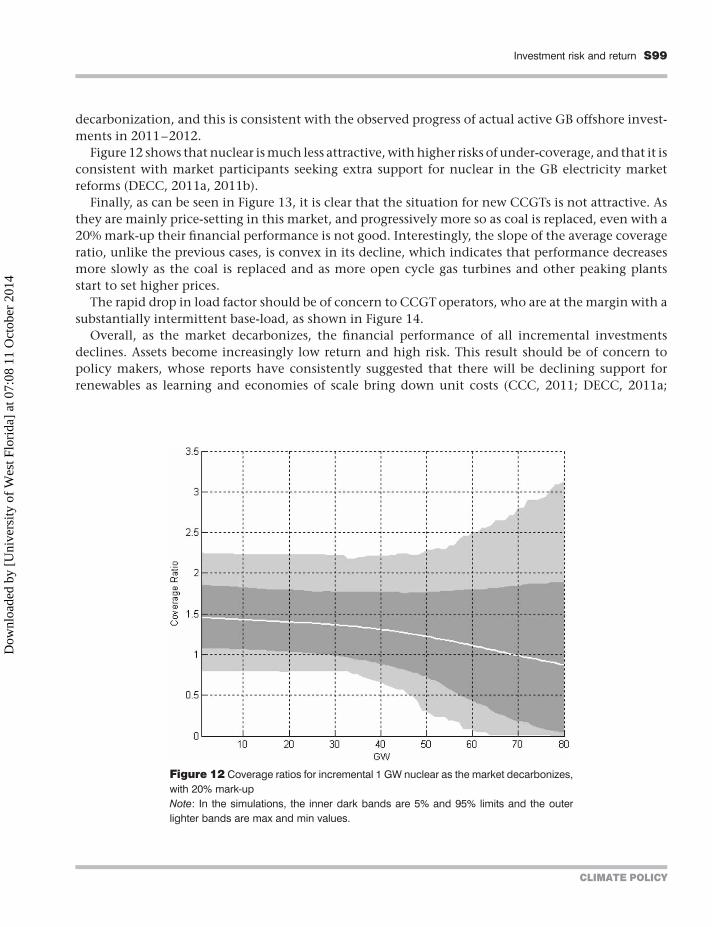

Figure 12 shows that nuclear is much less attractive, with higher risks of under-coverage, and that it is

consistent with market participants seeking extra support for nuclear in the GB electricity market

reforms (DECC, 2011a, 2011b).

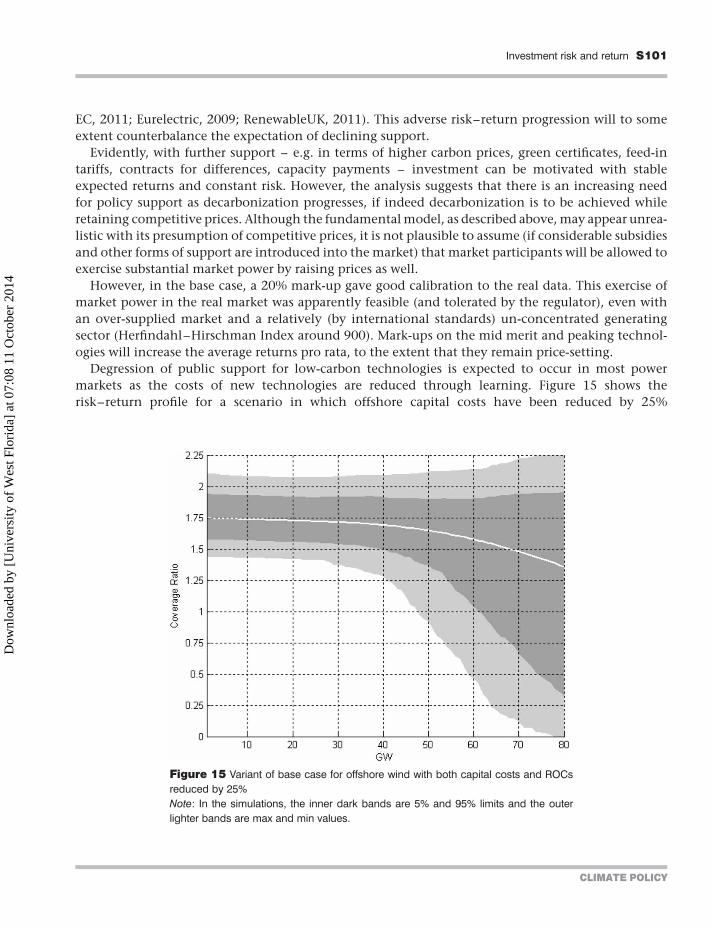

Finally, as can be seen in Figure 13, it is clear that the situation for new CCGTs is not attractive. As

they are mainly price-setting in this market, and progressively more so as coal is replaced, even with a

20% mark-up their financial performance is not good. Interestingly, the slope of the average coverage

ratio, unlike the previous cases, is convex in its decline, which indicates that performance decreases

more slowly as the coal is replaced and as more open cycle gas turbines and other peaking plants

start to set higher prices.

The rapid drop in load factor should be of concern to CCGT operators, who are at the margin with a

substantially intermittent base-load, as shown in Figure 14.

Overall, as the market decarbonizes, the financial performance of all incremental investments

declines. Assets become increasingly low return and high risk. This result should be of concern to

policy makers, whose reports have consistently suggested that there will be declining support for

renewables as learning and economies of scale bring down unit costs (CCC, 2011; DECC, 2011a;

Figure 12 Coverage ratios for incremental 1 GW nuclear as the market decarbonizes,with 20% mark-upNote: In the simulations, the inner dark bands are 5% and 95% limits and the outerlighter bands are max and min values.

Investment risk and return S99

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

Figure 13 Coverage ratios for incremental 1 GW CCGT as the market decarbonizes, with 20% mark-upNote: In the simulations, the inner dark bands are 5% and 95% limits and the outer lighter bands are max and min values.

Figure 14 Working hours for an average CCGT as the target year decarbonizesNote: In the simulations, the inner dark bands are 5% and 95% limits and the outer lighter bands are max and min values.

S100 Munoz and Bunn

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

EC, 2011; Eurelectric, 2009; RenewableUK, 2011). This adverse risk–return progression will to some

extent counterbalance the expectation of declining support.

Evidently, with further support – e.g. in terms of higher carbon prices, green certificates, feed-in

tariffs, contracts for differences, capacity payments – investment can be motivated with stable

expected returns and constant risk. However, the analysis suggests that there is an increasing need

for policy support as decarbonization progresses, if indeed decarbonization is to be achieved while

retaining competitive prices. Although the fundamental model, as described above, may appear unrea-

listic with its presumption of competitive prices, it is not plausible to assume (if considerable subsidies

and other forms of support are introduced into the market) that market participants will be allowed to

exercise substantial market power by raising prices as well.

However, in the base case, a 20% mark-up gave good calibration to the real data. This exercise of

market power in the real market was apparently feasible (and tolerated by the regulator), even with

an over-supplied market and a relatively (by international standards) un-concentrated generating

sector (Herfindahl–Hirschman Index around 900). Mark-ups on the mid merit and peaking technol-

ogies will increase the average returns pro rata, to the extent that they remain price-setting.

Degression of public support for low-carbon technologies is expected to occur in most power

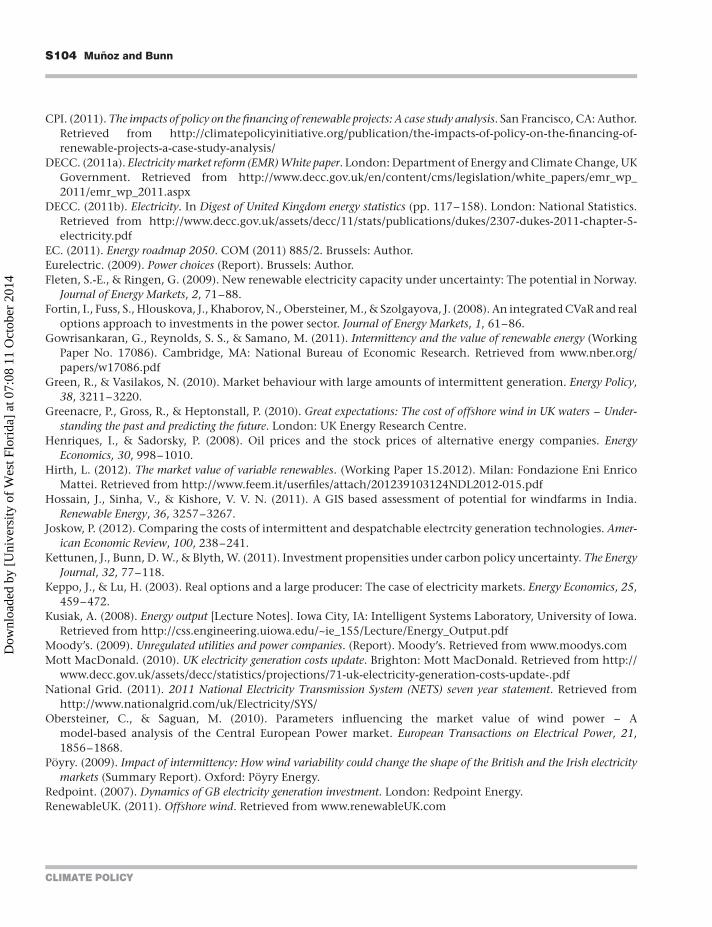

markets as the costs of new technologies are reduced through learning. Figure 15 shows the

risk–return profile for a scenario in which offshore capital costs have been reduced by 25%

Figure 15 Variant of base case for offshore wind with both capital costs and ROCsreduced by 25%Note: In the simulations, the inner dark bands are 5% and 95% limits and the outerlighter bands are max and min values.

Investment risk and return S101

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

(to £1687/kW) and ROCs have been reduced accordingly (to 1.5). A similar pattern emerges in Figure 15

as in Figure 10. Of course, to reach 25% reductions in both capital costs and subsidies, a substantial

number of installations would be needed. If this were to amount to a replacement of about 20 GW

of the 26 GW of coal with an equivalent derated amount of wind (i.e. 60 GW), before such learning

economics materialized the risk–return profile for the incremental wind investment would be as unat-

tractive at 60 GW in Figure 14 as in Figure 10. Thus, if degression of policy support simply follows

capital costs as the market decarbonizes, the attractiveness of financial performance in terms of

risk–return of marginal investments at a constant level will not be maintained.

5. Conclusion

Decarbonization of a wholesale power market, such as that in Great Britain, appears to be associated,

ceteris paribus, with a greater progressive deterioration in the financial risk–return profile of new and

existing assets than has been envisaged in the various pathways studies. Policy analysis is generally

based upon a careful evaluation of levelized costs for different technologies, which leads to an analysis

of the support that might be needed to incentivize the adoption of these technologies by investors.

However, the market and other risks that affect the financial performance of new assets have rarely

been explicitly taken into account in such a way that lenders and ratings agencies may evaluate

their prospects.

Using a detailed price formation model of the GB market, which was based upon fundamentals and

calibrated to 2011 data, risk and return was estimated through Monte Carlo simulations of all key par-

ameters, and it was shown that investors have a reduced propensity to engage in incremental invest-

ments. Although the specific parametric assumptions of market simulations such as those used in

this study are always subject to cautious interpretation, the underlying fundamentals identified here

clearly indicate that particular investments in the near and longer terms face a deteriorating risk–

return profile over their asset lives if decarbonization progresses as deeply as policy targets have so

far envisaged. The results reported here suggest that it is inevitable that this trend will lead to require-

ments for higher centrally administered support if capital costs and other parameters remain constant.

It is an open question whether this deteriorating trend with increased renewable penetration can be

mitigated or even reversed through the expected capital expenditure reductions of new technology

learning. The specification of the risk simulation, target year model used here is, on balance, a cautious

one. Essentially, it focuses upon the intra-year risk in operational profit contribution, relative to annui-

tized financing cost. On the one hand, the model does not allow speculation regarding how the average

parameter values used for the intra-year simulations will evolve over time. For gas and carbon, in par-

ticular, the stochastic evolution of these mean values will in practice add a lot more risk to the financial

evaluation over the lifetimes of the new assets. On the other hand, an interpretation based upon the

coverage ratio risk for an individual year may be too restrictive. Although companies may be averse

to the risk of presenting inferior annual performance, even ratings agencies tend to take a three- to

five-year view of corporate performance. Finally, although the financial performance analyses were

based upon full debt financing for analytical convenience, with lower levels of gearing, considerations

of return on equity will be just as crucial to investors in the long run, and usually at higher levels of

return than the cost of debt. Evidently, the high level of project risk indicated in this analysis has

S102 Munoz and Bunn

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

implications for the type of investor who may be attracted to such projects. From a market structure

perspective, large incumbent portfolio generators with strong retail markets will be better placed

than small new-entrant independent power producers. Market concentration appears both necessary

(to achieve long-run marginal costs) and inevitable (given the increasing risks). If the markets become

more concentrated as a result of these increased risk management needs, then climate and regulatory

policy makers will face increasingly inter-related and serious challenges to incentivize sufficient low-

carbon investment, preserve energy security, and mitigate the abuse of market power.

An extra ingredient that affects the pathway to decarbonization, and which has not so far received

significant attention, has been identified. In practice, endogenous interventions will emerge if energy

policies and market performances do not remain attractive to both governments and market partici-

pants. The target year analysis, which holds all parameters constant except for the replacement of

coal by wind, has been useful in isolating the debt coverage risk effect, but has not provided insights

into the rational consequences of the identified risks. Governments may take on more of the funda-

mental risks, so as to make renewable investments more attractive. Markets may become less volatile

through increased interconnections with neighbouring markets, more storage, and greater demand-

side engagement. Evidently, policy will evolve, infrastructures may change radically, and corporate

strategies will adapt. There are numerous pathways studies that have explored such scenarios. In

this article, we have suggested that financial investment risk should become a more important ingre-

dient in their evaluations. According to scenarios, the markets could become more or less risky.

Acknowledgement

The authors would like to acknowledge the support of UKERC (UK Energy Research Centre, London)

and EPRI (Electric Power Research Institute, California) in this research.

Notes

1. Northern Ireland is a separate market and is fully integrated with that of the Republic of Ireland.

2. Such longer-term uncertainties substantially affect investment analyses, but are invariably evaluated using scen-

arios and sensitivity analysis rather than probabilistic simulations. Essentially, these uncertainties set the mean

values for each year. The target year risk simulations analysed here are calibrated to intra-year variations around

such mean values.

3. Onshore earned 1 ROC per MWh, and offshore earned 2 ROC per MWh.

4. By contrast, one variation with 1.5 ROCS/MWh, as in 2010, showed unattractive financial performance on these

metrics after approximately 10% decarbonization. This is consistent with the reasons why the offshore ROCs

were increased from 1.5 to 2 in 2011.

References

Awerbuch, S. (2006). Portfolio-based electricity generation planning: Policy implications for renewables and energy

security. Mitigation and Adaptation Strategies for Global Change, 11, 693–710.

CCC. (2011). Renewable energy review. London: Author. Retrieved from http://www.theccc.org.uk/reports/

renewable-energy-review

Investment risk and return S103

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

CPI. (2011). The impacts of policy on the financing of renewable projects: A case study analysis. San Francisco, CA: Author.

Retrieved from http://climatepolicyinitiative.org/publication/the-impacts-of-policy-on-the-financing-of-

renewable-projects-a-case-study-analysis/

DECC. (2011a). Electricity market reform (EMR) White paper. London: Department of Energy and Climate Change, UK

Government. Retrieved from http://www.decc.gov.uk/en/content/cms/legislation/white_papers/emr_wp_

2011/emr_wp_2011.aspx

DECC. (2011b). Electricity. In Digest of United Kingdom energy statistics (pp. 117–158). London: National Statistics.

Retrieved from http://www.decc.gov.uk/assets/decc/11/stats/publications/dukes/2307-dukes-2011-chapter-5-

electricity.pdf

EC. (2011). Energy roadmap 2050. COM (2011) 885/2. Brussels: Author.

Eurelectric. (2009). Power choices (Report). Brussels: Author.

Fleten, S.-E., & Ringen, G. (2009). New renewable electricity capacity under uncertainty: The potential in Norway.

Journal of Energy Markets, 2, 71–88.

Fortin, I., Fuss, S., Hlouskova, J., Khaborov, N., Obersteiner, M., & Szolgayova, J. (2008). An integrated CVaR and real

options approach to investments in the power sector. Journal of Energy Markets, 1, 61–86.

Gowrisankaran, G., Reynolds, S. S., & Samano, M. (2011). Intermittency and the value of renewable energy (Working

Paper No. 17086). Cambridge, MA: National Bureau of Economic Research. Retrieved from www.nber.org/

papers/w17086.pdf

Green, R., & Vasilakos, N. (2010). Market behaviour with large amounts of intermittent generation. Energy Policy,

38, 3211–3220.

Greenacre, P., Gross, R., & Heptonstall, P. (2010). Great expectations: The cost of offshore wind in UK waters – Under-

standing the past and predicting the future. London: UK Energy Research Centre.

Henriques, I., & Sadorsky, P. (2008). Oil prices and the stock prices of alternative energy companies. Energy

Economics, 30, 998–1010.

Hirth, L. (2012). The market value of variable renewables. (Working Paper 15.2012). Milan: Fondazione Eni Enrico

Mattei. Retrieved from http://www.feem.it/userfiles/attach/201239103124NDL2012-015.pdf

Hossain, J., Sinha, V., & Kishore, V. V. N. (2011). A GIS based assessment of potential for windfarms in India.

Renewable Energy, 36, 3257–3267.

Joskow, P. (2012). Comparing the costs of intermittent and despatchable electrcity generation technologies. Amer-

ican Economic Review, 100, 238–241.

Kettunen, J., Bunn, D. W., & Blyth, W. (2011). Investment propensities under carbon policy uncertainty. The Energy

Journal, 32, 77–118.

Keppo, J., & Lu, H. (2003). Real options and a large producer: The case of electricity markets. Energy Economics, 25,

459–472.

Kusiak, A. (2008). Energy output [Lecture Notes]. Iowa City, IA: Intelligent Systems Laboratory, University of Iowa.

Retrieved from http://css.engineering.uiowa.edu/~ie_155/Lecture/Energy_Output.pdf

Moody’s. (2009). Unregulated utilities and power companies. (Report). Moody’s. Retrieved from www.moodys.com

Mott MacDonald. (2010). UK electricity generation costs update. Brighton: Mott MacDonald. Retrieved from http://

www.decc.gov.uk/assets/decc/statistics/projections/71-uk-electricity-generation-costs-update-.pdf

National Grid. (2011). 2011 National Electricity Transmission System (NETS) seven year statement. Retrieved from

http://www.nationalgrid.com/uk/Electricity/SYS/

Obersteiner, C., & Saguan, M. (2010). Parameters influencing the market value of wind power – A

model-based analysis of the Central European Power market. European Transactions on Electrical Power, 21,

1856–1868.

Poyry. (2009). Impact of intermittency: How wind variability could change the shape of the British and the Irish electricity

markets (Summary Report). Oxford: Poyry Energy.

Redpoint. (2007). Dynamics of GB electricity generation investment. London: Redpoint Energy.

RenewableUK. (2011). Offshore wind. Retrieved from www.renewableUK.com

S104 Munoz and Bunn

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4

Reuter, W. H., Fuss, S., Szolgayova, J., & Obersteiner, M. (2012). Investment in wind power and pumped storage in a

real options model. Renewable and Sustainable Energy Reviews, 16, 2242–2248.

Saenz de Miera, G., del Rıo Gonzalez, P., & Vizcaıno, I. (2008). Analysing the impact of renewable electricity support

schemes on power prices: The case of wind electricity in Spain. Energy Policy, 36, 3345–3359.

Sensfuß, F., Ragwitz, M., & Genoese, M. (2008). The merit-order effect: A detailed analysis of the price effect of

renewable electricity generation on spot market prices in Germany. Energy Policy, 36, 3076–3084.

Sinden, G. (2007). Characteristics of the UK wind resource: Long term patterns and relationship to electricity

demand. Energy Policy, 35, 112–127.

Yang, M., Blyth, W., Bunn, D. W., Bradley, R., Clarke, C., & Wilson, T. (2008). Evaluating power investment options

with uncertainty in climate policy. Energy Economics, 30, 1933–1950.

Zonneveld, P., Papaefthymiou, G., Coster, E., & van der Sluis, L. (2008). Calculation of grid losses with the aid of

stochastic modeling of wind turbines and loads. In 16th Power Systems Computation Conference 2008 (Vol. 2,

pp. 1295–1302). Glasgow: Curran Associates.

Investment risk and return S105

CLIMATE POLICY

Dow

nloa

ded

by [

Uni

vers

ity o

f W

est F

lori

da]

at 0

7:08

11

Oct

ober

201

4