investment research fx top trades 2014

TRANSCRIPT

Important disclosures and certifications are contained from page 20 of this report. www.danskeresearch.com

Investment Research

One positive supply shock, four implications,10 FX trades

For the fifth time, we present our year-end FX Top Trades for the coming year. In the

years 2010-13, our FX top trades delivered an average return of 3.0% with an average hit

ratio of 75% each year.

This year’s trade ideas are based on the view that the global economy will face very low

inflation in 2014 primarily due to falling commodity prices and plenty of spare capacity

in most economies. The low inflation will work as a positive supply shock to the global

economy and should have a number of implications that, in our view, will drive the FX

market in 2014.

The positive supply shock will (i) support the global growth recovery, (ii) put focus on

relative monetary policy as global central banks will react differently to the low inflation,

(iii) put focus on alternative monetary policy tools as interest rates have already reached

zero in many countries, and finally (iv) underline that investors will have an EM and

commodity scare as developed markets will be favoured over emerging markets and not

least commodity-producing countries.

We would stress that there is no hedging or portfolio element built into the 10 trades and

the return potential is based on a risk/reward ratio of approximately 1:2. We present five

spot/forward trades and five option-based recommendations. The latter are primarily used

to take advantage of attractive option market pricing, express a view on volatility or lower

spot exposure or hedge tail-risks in the trade recommendations.

We run an active trade management and reserve the right to book profits or take losses at

any time should the underlying fundamentals change. We will, of course, follow up on

the trades with P/L updates from time to time. In the table below, we list the 10 trade

recommendations plotted against the different implications.

9 December 2013

FX Top Trades 2014How to position for the coming year

FX Top Trades 2014

#1: Bullish USD/CHF call spread

#2: Bullish USD/JPY straddle

#3: Short EUR/GBP

#4: Bearish EUR/SEK seagull

#5: Bearish EUR/NOK risk reversal

#6: Bullish EUR/CZK ratio forward

#7: Short AUD and CAD vs USD

#8: Long TRY/DKK

#9: Sell 12M USD/CNH

#10: Long RON/PLN

Table 1: FX Top Trades 2014* � the matrix

Source: Danske Bank Markets *) Prices are updated Friday December 6, 14.00 cet.

Chief Analyst Arne Lohmann Rasmussen +45 45 12 85 21 [email protected]

Global growth recovery

Relative monetary policy

Monetary policy tools

EM/commodity scare

#1: Short EUR/USD via long USD/CHF x x x

#2: Bullish USD/JPY straddle x x

#3: Short EUR/GBP x x x

#4: Bearish EUR/SEK seagull x

#5: Bearish EUR/NOK risk reversal x x

#6: Bullish EUR/CZK ratio forward x x

#7: Short AUD and CAD vs USD x x x

#8: Long TRY/DKK x x x

#9: Sell 12M USD/CNH

#10: Long RON/PLN x x

2 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

Looking back at our 2013 Top Trades

This year’s FX Top Trades yielded a positive return for the fourth consecutive year. The hit ratio was 60% and the average return was 1.9% for the 10 FX trades.

The average profit from our 10 FX Top Trades for 2013 was 1.9%. This is slightly lower

than the average return in 2010-12 of 3.0%, probably reflecting that we managed our P/L

in a more cautious way than previously and that we were wrong on carry currencies. We

took a relatively optimistic view on the market, arguing that in 2013 (i) we would see a

modest global recovery, (ii) monetary easing would continue, (iii) the low volatility

environment from a year ago would continue, (iv) we would see fewer tail-risks, (v) value

would be found in EMEA, and finally that (vi) macro-prudential policies would be a new

important theme to follow in the FX market.

Monetary easing did indeed continue in 2013. Ben Bernanke fulfilled his promise of

aggressive monetary easing despite the better US economic performance, Abenomics

became the new buzzword in Japan and the unorthodox Mark Carney managed to weaken

sterling even before he was officially named governor. Even the ECB eased monetary

policy in 2013.

Our view on relative monetary policy was successfully expressed in a bearish JPY/SEK

strategy (+6.44%), a short GBP/NOK position (+1.0%), a bullish USD/JPY risk reversal

(+11.45%) and a long RUB/CZK position (+3.33%). The latter trade was closed in April

as the rouble outlook started to become less positive and we did not benefit from the

expected FX intervention by the Czech central bank, which did not happen before last

month. We are happy to say that we managed to take profit on our long Scandi trades

ahead of the large-scale sell-off mid 2013. Tapering fears derailed risk sentiment during

the summer and 2013 did not become an EMEA and carry year as we had assumed and

we had to close our carry basket (long TRY, MXN and HUF against USD) in August

with a total loss of 2.90%. We were satisfied, however, to see that our view that

commodity currencies should be avoided in carry strategies limited the loss.

One of our main stories for 2013 was that the yen would be the big loser this year and our

short JPY/SEK and long USD/JPY strategies were the best two-performing strategies.

Four trades did not perform well. The carry basket, the short USD/CAD and the short

USD/SGD all suffered as the US dollar gained broadly. Finally, our six-month option

strategy for a higher EUR/USD expired just before the cross was pushed above the

breakeven level over the summer. However, our positive euro view benefited the long

EUR/CHF trade, which was closed with a 2.89% profit in January.

Danske Bank Markets� FX Top Trades 2013

Source: Danske Bank Markets

# Type Trade Level Closed Level P/L

1 Option Bearish 6M JPY/SEK risk reversal 8.02 11/01/13 7.320 6.44%

2 Spot Sell GBP/NOK 9.04 16/01/13 8.962 1.00%

3 Spot Buy EUR/CHF 1.2145 18/01/13 1.250 2.89%

4 Spot Sell USD/CAD 0.9914 19/01/13 1.015 -2.16%

5 Spot Sell USD/SGD 1.2183 11/03/13 1.250 -2.70%

6 Option USD/JPY option strategy 82.20 22/03/13 94.850 11.45%

7 Spot Buy RUB/CZK 0.6246 16/04/13 0.6305 3.33%

8 Option EUR/USD butterfly 1.3121 05/06/13 1.3079 -0.74%

9 Forward Sell USD/CNH 12 Forward 6.3550 17/07/13 6.2025 2.46%

10 Spot Long TRY, MXN, HUF vs. Short USD 100 27/08/13 97.1 -2.90%

Danske Bank Markets FX Top Trades

Source: Danske Bank Markets

Short JPY/SEK closed after one month of strong performance

Source: Macrobond, Danske Bank Markets

We closed long EUR/CHF in January

Source: Macrobond, Danske Bank Markets

Hit ratio Avg Return Acc. Return Best trade Worst trade

2010 80% 3,7% 37,0% 10,5% -4,6%

2011 80% 3,5% 35,0% 11,0% -1,8%

2012 80% 2,1% 21,0% 7,1% -2,2%

2013 60% 1,9% 19,0% 11,5% -2,9%

Average 75% 3% 28% 10% -3%

3 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

Dynamics of a positive supply shock

Recently, inflation has come down significantly – not least in Europe and the US –

on the back of weak capacity utilisation in general and softer commodity prices in

particular. In our view, the disinflation pressures are here to stay and we think these

represent a significant positive supply shock to the global economy. We believe the

market will increasingly have to price the widespread consequences of this during

the course of 2014.

The positive global supply shock that we see unfolding takes its most visible form in the

commodity markets. A supply revolution driven by, among other things, new and

improved drilling technology within the oil and gas industry is gradually starting to be

passed on to consumers. We think this process still has further to run in the years to come

– though we highlight that risks to food prices are still on the upside.

However, stagnating commodity prices are not the only positive supply-side factor

driving the economy at the moment. Economic growth will benefit from the pick-up in

productivity growth and the long list of supply-side reforms. Together with the fiscal

consolidation that has taken place in many developed countries over the past couple of

years, this should foster activity from a more structural point of view. At the same time,

the significant economic slack in many areas, notably in the labour market, implies that

economic growth should be able to recover without initiating a wage-price spiral.

These dynamics are illustrated in the simplified chart below: this shows how the positive

supply shock originates from movements in commodity prices, excess capacity and

productivity. This is in turn positive for global growth and bodes well for a benign

inflation outlook. Disinflation in turn leaves room for monetary policy to stay

accommodative for global growth and risk appetite. The latter could then be fuelled

further by the decent growth outlook; however, we emphasise that the FX market has now

moved beyond the environment where this would invite a simple bet on the traditional

‘risk-on carry currencies.

Dynamics of a positive supply shock

Source: Danske Bank Markets

Positive commodity supply shock

Source: Macrobond

Plenty of available resources

Source: Macrobond

Productivity has started growing again

Source: Macrobond

4 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

The drop in inflation on the back of the positive supply shock currently benefits growth

through a boost to consumer purchasing power and easy monetary policy (see implication

#1 below). However, in some places the recovery is gaining ground and central banks are

moving closer to scaling back, which affects relative monetary policy (see implication

#2). For central banks close to the zero lower bound on interest rates, further monetary

easing can, however, only take place via alternative tools (see implication #3). The global

growth recovery is beneficial for risk appetite, but the combination of a Chinese

slowdown and stagnating commodity prices will likely weigh on EM and commodity

currencies (see implication #4).

5 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

#1: Global growth recovery

While plenty of pessimism has been expressed about the global economy over recent

years, the truth is that we have witnessed several positive supply shocks over the

past 20-30 years: shocks of a structural nature that have given a temporary lift to

global growth several times. We are about to witness another one as a result of the

rise in oil and gas production from shale formations.

Remembering the global positive supply shocks

In the 1990s, global growth benefited from a rise in productivity growth from the IT

revolution. It led to the term ‘New economy’ but was really just a positive supply shock

which meant growth could be higher for a while before causing inflation – as long as the

transition of implementing the new technology took place. As a consequence, the then

Fed chairman, Alan Greenspan, kept rates lower than otherwise – and most likely helped

fuel the IT bubble.

The 2000s was the decade of emerging markets. A positive supply shock on a global scale

took place because millions of people in emerging markets became markedly more

productive as they went from farming (which added little value) into factories in the cities

producing goods for western consumers. The outsourcing boom from developed markets

to emerging markets led to a rise in global productivity growth, which meant the global

economy could grow faster without inflation and thus with lower central bank rates – all

else being equal. Actually, inflation was not that low in this period but was mostly

concentrated in commodity prices. It was therefore deemed ‘temporary’ by western

central banks and did not count as real inflation. Hence, rates were kept low for longer.

This helped fuel the Great Housing Bubble in the US and most of western Europe.

In the 2010s we are witnessing another positive supply shock. The shale oil and gas

adventure is unleashing new production potential which, all else being equal, is reducing

the costs on oil. This feeds through to other commodity prices as well. Since the positive

supply shock comes at a time when the western world is already experiencing a large

output gap (demand much lower than supply), the disinflationary forces are quite

significant. However, the fall in inflation stemming from the positive supply shock gives

a lift to growth. Lower inflation in energy and food frees up purchasing power to buy

refrigerators, DVDs, cars, etc. As consumption of these items at the starting point is

already very suppressed the case for recovery becomes stronger.

Fiscal austerity in Europe and US is over

The global recovery in 2014 will also be underpinned by easing headwinds as well as

pent-up demand. Fiscal austerity has taken place in both Europe and the US in 2013 and

this will be over in 2014. At the same time, the euro debt crisis has been tamed and the

‘bond yield shock’ to the US economy in 2013 is likely to fade in 2014. Pent-up demand

is biggest in Europe where the significant stress of the past few years has pushed

investments and durable goods consumption to extremely low levels.

Overall, we look for the global recovery to move up a gear next year, while inflation stays

low and probably moves even lower in the euro area over the coming quarters. This will

create an environment of (a) global recovery, (b) subdued inflation and (c) low rates for

longer and this time it will even be very low rates for a very long time. It is a great

environment for risk assets and we look for further gradual spread compression in

peripheral bond markets and credit. The risk of new bubbles is quite clear based on the

experience in the 1990s and 2000s.

It is also an environment in which central banks with the clearest focus on inflation (euro

area and Japan) and the largest output gap (euro area) will be relatively accommodative

versus central banks with a broader mandate (US).

Oil prices to keep inflation low�

Source: Macrobond Financial, Danske Bank

Markets

... while global growth picks up to 4% (above trend growth at 3.5%)

Source: Macrobond Financial, Danske Bank

Markets

Search for yield will underpin further spread compression

Source: Reuters EcoWin, Danske Bank Markets

6 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

#2: Relative monetary policy

With the world economy set for a continued recovery yet subdued inflationary

pressure, a range of central banks are likely to have their priorities twisted in 2014.

Some will be looking to scale back on easing, albeit still keeping monetary conditions

relatively loose. The Fed and Bank of England (BoE) are cases in point. Others will

face the deflation scare: the Bank of Japan (BoJ) will have to continue its long-

standing battle against the deflation spiral whereas the ECB will have to deal with

this less well-known threat to price stability.

Less easing, but only as growth recovers

With the US set to drive the recovery in the developed world, the Fed is also set to be a

first mover in scaling back on monetary easing. However, it will be a very gradual

process as we think the FOMC will be determined not to risk the rapid rate rises seen over

the summer. Notably, the discrepancy between where the market sees the Fed funds rate

and where the FOMC projects it will be by end-2016 differ markedly, i.e. at 1.50% and

2.00%, respectively. This also differs from where a Taylor rule based on Fed’s own

economic projections for inflation and unemployment suggest the policy rate ought to be

by end-2016, i.e. at 4.00%. This underlines that while the Fed is itself projecting a dovish

tapering move away from the zero lower bound, the market is even less aggressive. Our

rate strategists see the flat US money market curve as a key candidate for a significant re-

pricing (steepening) next year. This should fuel a broad-based move higher in the US

dollar.

A similar story goes for the BoE albeit with the roles switched: we think the BoE has

further to go in acknowledging the potential for the healing of the UK economy to

continue – something the market has in fact been projecting for a while. The pound

should stay supported as a result.

More easing to scare off the deflation ghost

However, it is not all ‘happy days’ in central banking: disinflation is a direct threat to

targets for a range for some central banks and these will have to act as a result.

Specifically, we expect the BoJ to counter next year’s fiscal contraction by means of a

continued expansion of the monetary base. Despite the marked downtrend in the yen this

year, we look for more yen weakness to be sustained in 2014.

The ECB will, in our view, do a lot to avoid a Japanese-like debt-deflation spiral. Indeed,

price stability is core business for the ECB and the swift reaction to the decline in

inflation with the refi rate cut delivered in November by Draghi underlined that the bank

has a symmetric view: both positive and negative deviations from the 2% inflation target

require policy action. While the ECB toolbox is constrained by its distaste of quantitative

easing, the bank still has a few options left such as a cut in the deposit rate to negative;

the technical as well as mental barriers to this now appear to have been overcome at the

Governing Council. We think the ECB will manage to keep EONIA rates down, which

should exert some (limited) downward pressure on the euro.

Monetary policy to stay benign for risk assets

As inflation worries move aside, it should be possible for central banks to act in a way

that does not scare risk markets: only to the extent that growth picks up, easing will be

removed – and less monetary stimuli should be manageable for risk appetite if it takes

place in an environment where growth gains pace.

USD-OIS pricing of Fed

Source: Danske Bank Markets

Market vs Taylor rule projection

Note: Taylor rule based on2+core PCE+0.5*(core PCE-2)+1.5*NAIRU gap

06 07 08 09 10 11 12 13 14 15 16-5

-3

-1

1

3

5

7

-5

-3

-1

1

3

5

7% %

Fed funds target rate

Market pricing

Range based on FOMC projections

Taylor rule on PCE core,

NAIRU at 5.5%

Source: FOMC, Reuters EcoWin, Danske Bank

Markets

Monetary policy response to demand shocks in 2014

Source: FOMC, EcoWin, Danske Bank Markets

Note: Demand shock includes effect from fiscal

policy, house prices and oil prices

-0.20%

0.30%

0.80%

1.30%

1.80%

2.30%

2.80%

Sep13 Mar14 Sep14 Mar15 Sep15 Mar16 Sep16 Mar17 Sep17

Pricing USD-OIS 1m swap

Current live 17-Sep-13 Current policy rate Next policy move

NOK

JPY

CADAUD

SEK

EUR

TRYRON

PLN

USDGBP

Demand shock change (Negative)

Demand shock change

(Positive)

Monetary policy vs market pricing (tightening)

Monetary policy vs market pricing (easing)

Neutral currency impact

Neutral currency impact

Negative currency impact

Positive currency impact

7 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

#3: Alternative monetary policy tools

As deflationary pressures have been building more and more, inflation-targeting

central banks have started to undershoot their inflation targets and some countries

are now even facing outright deflation. Most inflation-targeting central banks use

the interest rate as a policy instrument; however, as interest rates have dropped

close to zero in many countries, many central banks face the problem of how to react

to disinflation or even deflation. Central bankers therefore have to utilise other

policy instruments.

FX intervention as a monetary policy instrument

The most commonly used tool by the major central banks to stimulate the economy over

the past five years has been quantitative easing, where the central bank buys assets to

boost the money base. However, there are other options: with regard to the currency

markets, the possibility of intervening in the currency markets as an instrument of

monetary easing is particularly interesting.

In 2011, the Swiss central bank (SNB) moved to weaken the Swiss franc and then put a

floor under EUR/CHF to counteract deflationary pressures in the Swiss economy.

Recently the Czech central bank (CNB) followed suit and implemented a policy and

introduced a floor under EUR/CZK as initially devaluing the Czech koruna by around

4%. Both the SNB and CNB implemented these measures because interest rates had

effectively hit the zero lower bound. Also, we would not rule out that the Reserve Bank of

Australia (RBA) could resort to new rounds of intervention to bring AUD lower still.

We believe that both the SNB and the CNB will keep these policies in place during 2014.

We think that there is a good chance that the CNB will respond to continued deflationary

pressures and a weak economy and move the floor up for EUR/CZK during the year.

Overcoming the mental and technical barriers to negative rates

While the mental and technical barriers to negative interest rates have long prevailed

among Council members at the ECB, these now appear to be gradually removed. Indeed,

the Danish experience suggests that technicalities can be overcome. The ECB with its key

policy (refi) rate at 0.25% has very limited room to cut rates further and has been very

reluctant to talk about a negative deposit rates (currently at 0.00%) – until recently, that

is. We think it fairly likely that the ECB will have to resort to alternative policy tools to

ease monetary conditions in the coming years to fight disinflation with the most likely

options a deposit-rate cut to negative territory or an LTRO designed to improve the

monetary-transmission mechanism. Overall, such alternatives to ‘traditional’ rate cuts

could open the door for more monetary easing than is currently being priced by the

markets, which would be likely to put some pressure on the euro in 2014.

�Outsourcing� macro-prudential worries

Finally, other central banks have been constrained in cutting rates by the fact they have

had to consider financial stability explicitly in setting the policy rate. This is particularly

relevant for those central banks that have been concerned about household imbalances

fuelled by booming property markets, such as in Sweden, Norway, Australia, New

Zealand and Canada. These central banks have in general kept monetary conditions too

tight given their inflation targets. However, as more and more central banks see the

responsibility for such macro-prudential concerns becoming increasingly separated from

their rate-setting process, this should provide more room for manoeuvre in easing.

CNB introduces target for EUR/CZK

Source: Danske Bank Markets

Nordic house prices have become a macro-prudential issue

Source: Macrobond, Danske Bank Markets

8 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

#4: EM and commodity scare

Although we expect 2014 to mark a further lift in global growth, not everyone stands

to win. As a result, we are looking at a global economic recovery a bit out of the

ordinary in terms of the implications for the currency market. Historically, EM and

commodity currencies have performed well when the global economy was doing

well. However, the nature of the recovery this time round (largely supply-side

driven) means that we are not too optimistic on the EM region and commodity

prices.

Commodity-exporting currencies stand to lose

The positive supply shock discussed in Dynamics of a positive supply shock means that a

further acceleration in global growth will not be associated with higher commodity prices

for once. Certainly some commodity producers may be able to up volumes and thus

revenue but we think the negative price effect will dominate for the most part. While

commodity-importing countries stand to win in this scenario, a positive commodity

supply shock works as a negative demand shock for commodity-exporting countries. A

number of currencies have historically recorded a high correlation with commodity

prices. The terms of trade of these countries will suffer if our commodity strategists are

right in calling oil and commodities more broadly lower in 2014.

EM challenges remain

Growth in the Chinese economy is also set to remain in modest territory next year as

economic policies will likely be kept tight next year as well, underlining the Chinese

authorities’ tolerance for lower growth as longer-term structural reforms are being

implemented. The economic slowdown in China has significant repercussions for other

EM economies. Notably, we have recently witnessed a slowdown in the large EM

economies of Indonesia, India and Brazil. Furthermore, the lack of a recovery in China

will weigh on demand for commodities and weigh further on prices, adding to the

downward pressure on these from the positive supply shock.

Not your usual �risk-on� bet

The combination of commodity-price drops and a challenging environment for the EM

region suggests that even if global growth looks good (implication #1) and we think

monetary policy will stay accommodative for risk assets (implication #2), we are now

beyond the days where such positive risk sentiment should invite a simple bet on the

traditional ‘risk-on’ carry currencies. Rather, we stress that the euro could benefit to some

degree in this search for yield as capital may continue to flow to the euro-zone periphery.

And of course that commodity and EM currencies are at risk as well to th extent that the

supply shock hit domestic activity.

Currency-commodity correlations

Source: Macrobond, Danske Bank Markets

Chinese economic slowdown

Source: Macrobond

with the oil price with the CRB indexAUD 0.39 0.44

BRL 0.43 0.39

CAD 0.52 0.50

NOK 0.32 0.20

RUB 0.32 0.08

TRY 0.01 0.11

ZAR 0.26 0.38

monthly correlation since 2009

9 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

Trade #1: short EUR/USD in disguise - bullish USD/CHF call spread

We recommend positioning for some (limited) EUR/USD downside via a long

USD/CHF position: the latter is essentially a short EUR/USD bet in disguise and we

argue that this provides some insulation against the risk of continued euro peripherals’

sentiment improvement. Specifically, we suggest entering a bullish USD/CHF call

spread as we see potential as limited and risks on either side as evenly distributed.

We look for a move lower in EUR/USD...

As discussed under implication #2, we see good potential for relative monetary policy to

push EUR/USD gradually lower in 2014. This view is primarily based on the potential we

see for a steeper US money market curve which should materialise when the Fed starts to

scale back its QE programme in December. However, we also see EONIA rates capped

by markets having to price the likelihood of more fierce measures from the ECB to fight

disinflation (a new LTRO or a cut in the deposit rate into negative territory). This

underlines that relative movements in short-end rates should exert some downward

pressure on EUR/USD.

... but also see risks limiting the potential

At the same time, we also have to acknowledge that the euro-zone economy has potential

to surprise on the upside growth-wise, which should eventually make the ECB

comfortable with rates on hold. More importantly, sentiment towards the peripheral

economies could continue to improve as past austerity and reforms make the euro zone

firmly put debt issues aside. For the single currency, PIIGS rate spreads to Germany have

been instrumental over the past few years, making a continued bettering in sentiment a

key risk to our weaker EUR/USD outlook.

CHF provides some insulation against peripheral inflows

Notably, in a situation where capital inflows into the euro-zone pick up, the Swiss franc

would probably stand to suffer as this was where a good deal of inflows were seen during

the euro debt crisis. That is, should the search for yield and improved sentiment towards

peripheral countries fuel inflows into the euro-zone, CHF should be exposed.

This year EUR/CHF has been lifted a little above the 1.20 floor adopted by the SNB in

late 2011 to stem the consequences of a strong franc. However, with deflation still an

issue in Switzerland, we expect the SNB to keep the floor for EUR/CHF in place

throughout 2014. This suggests that EUR/CHF upside is rather limited.

As a result, we suggest positioning for a (yet limited) move higher in USD/CHF, which

should essentially prove a short EUR/USD bet in disguise providing some insulation from

the key risk of continued peripherals’ spread tightening. As we see upside as limited, we

prefer a call spread to a spot position; also, this position is set to benefit from a rise in

volatility which would likely result if USD/CHF moves higher.

Risks: SNB removes the floor

A key risk when positioning for a weaker EUR/USD via CHF is if inflation picks up in

Switzerland, leaving room for the SNB to remove the EUR/CHF floor. More broadly, the

failure of the ECB to keep the money-market curve in check also poses a key issue as

does a failure of our key view that the US short end should steepen to materialise.

Trading strategy

Enter a 6M bullish USD/CHF call

spread with a bought call @

0.9040 and a sold call @ 0.9700

(spot ref.: 0.8960): this costs an

indicative 125 CHF pips (i.e.

break-even at 0.9165).

Alternatively, enter a bearish

EUR/USD put spread.

USD/CHF call spread � pay-off profile

Source; Danske Bank Markets

EUR/USD or USD/CHF

Source: Macrobond, Danske Bank Markets

PIIGS sentiment and EUR/USD

Source: Macrobond, Danske Bank Markets

-200

-100

0

100

200

300

400

500

600

0.874 0.899 0.924 0.949 0.974 0.999

Bullish USD/CHF call spread, P/L (CHF pips)

Break-even @ 0.9165

Downside capped@ 0.9040

Upside capped@ 0.9700

10 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

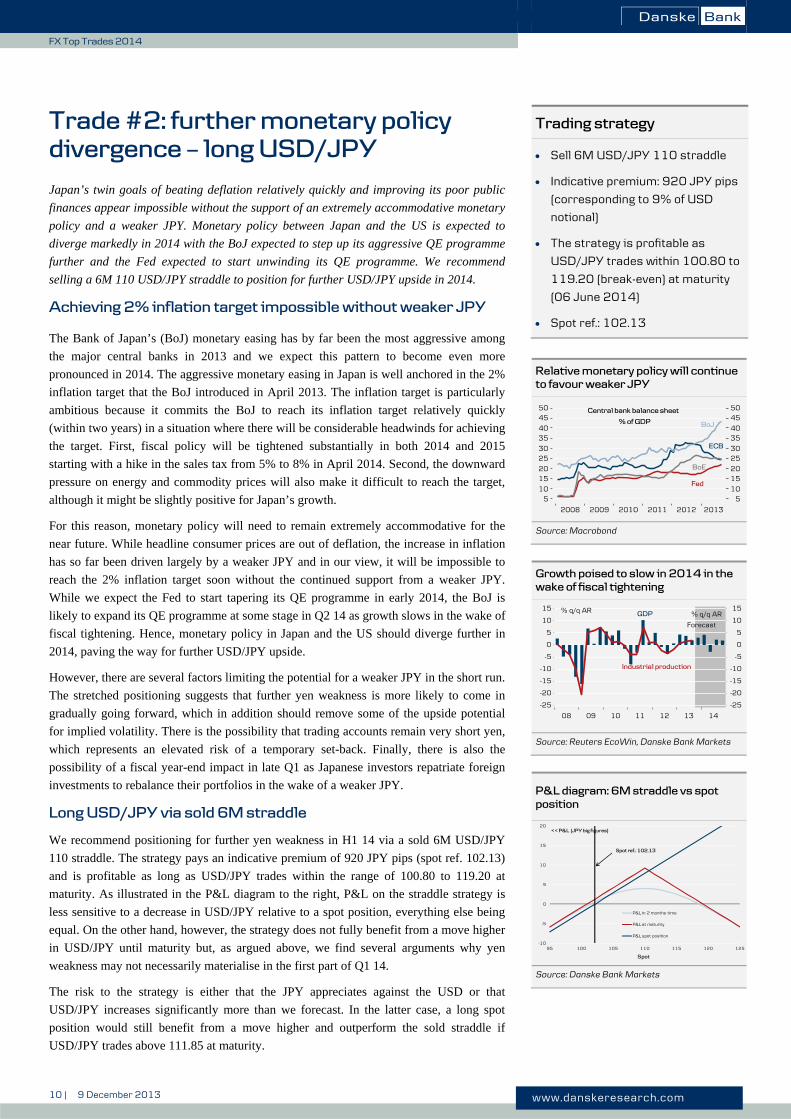

Trade #2: further monetary policy divergence � long USD/JPY

Japan’s twin goals of beating deflation relatively quickly and improving its poor public

finances appear impossible without the support of an extremely accommodative monetary

policy and a weaker JPY. Monetary policy between Japan and the US is expected to

diverge markedly in 2014 with the BoJ expected to step up its aggressive QE programme

further and the Fed expected to start unwinding its QE programme. We recommend

selling a 6M 110 USD/JPY straddle to position for further USD/JPY upside in 2014.

Achieving 2% inflation target impossible without weaker JPY

The Bank of Japan’s (BoJ) monetary easing has by far been the most aggressive among

the major central banks in 2013 and we expect this pattern to become even more

pronounced in 2014. The aggressive monetary easing in Japan is well anchored in the 2%

inflation target that the BoJ introduced in April 2013. The inflation target is particularly

ambitious because it commits the BoJ to reach its inflation target relatively quickly

(within two years) in a situation where there will be considerable headwinds for achieving

the target. First, fiscal policy will be tightened substantially in both 2014 and 2015

starting with a hike in the sales tax from 5% to 8% in April 2014. Second, the downward

pressure on energy and commodity prices will also make it difficult to reach the target,

although it might be slightly positive for Japan’s growth.

For this reason, monetary policy will need to remain extremely accommodative for the

near future. While headline consumer prices are out of deflation, the increase in inflation

has so far been driven largely by a weaker JPY and in our view, it will be impossible to

reach the 2% inflation target soon without the continued support from a weaker JPY.

While we expect the Fed to start tapering its QE programme in early 2014, the BoJ is

likely to expand its QE programme at some stage in Q2 14 as growth slows in the wake of

fiscal tightening. Hence, monetary policy in Japan and the US should diverge further in

2014, paving the way for further USD/JPY upside.

However, there are several factors limiting the potential for a weaker JPY in the short run.

The stretched positioning suggests that further yen weakness is more likely to come in

gradually going forward, which in addition should remove some of the upside potential

for implied volatility. There is the possibility that trading accounts remain very short yen,

which represents an elevated risk of a temporary set-back. Finally, there is also the

possibility of a fiscal year-end impact in late Q1 as Japanese investors repatriate foreign

investments to rebalance their portfolios in the wake of a weaker JPY.

Long USD/JPY via sold 6M straddle

We recommend positioning for further yen weakness in H1 14 via a sold 6M USD/JPY

110 straddle. The strategy pays an indicative premium of 920 JPY pips (spot ref. 102.13)

and is profitable as long as USD/JPY trades within the range of 100.80 to 119.20 at

maturity. As illustrated in the P&L diagram to the right, P&L on the straddle strategy is

less sensitive to a decrease in USD/JPY relative to a spot position, everything else being

equal. On the other hand, however, the strategy does not fully benefit from a move higher

in USD/JPY until maturity but, as argued above, we find several arguments why yen

weakness may not necessarily materialise in the first part of Q1 14.

The risk to the strategy is either that the JPY appreciates against the USD or that

USD/JPY increases significantly more than we forecast. In the latter case, a long spot

position would still benefit from a move higher and outperform the sold straddle if

USD/JPY trades above 111.85 at maturity.

Trading strategy

Sell 6M USD/JPY 110 straddle

Indicative premium: 920 JPY pips

(corresponding to 9% of USD

notional)

The strategy is profitable as

USD/JPY trades within 100.80 to

119.20 (break-even) at maturity

(06 June 2014)

Spot ref.: 102.13

Relative monetary policy will continue to favour weaker JPY

Source: Macrobond

Growth poised to slow in 2014 in the wake of fiscal tightening

Source: Reuters EcoWin, Danske Bank Markets

P&L diagram: 6M straddle vs spot position

Source: Danske Bank Markets

08 09 10 11 12 13 14

-25

-20

-15

-10

-5

0

5

10

15

-25

-20

-15

-10

-5

0

5

10

15 % q/q AR % q/q AR

Forecast

GDP

Industrial production

-10

-5

0

5

10

15

20

95 100 105 110 115 120 125

Spot

P&L in 2 months time

P&L at maturity

P&L spot position

Spot ref.: 102.13

<< P&L (JPY big figures)

11 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

Trade #3: BoE in reverse � sell EUR/GBP

We recommend selling EUR/GBP spot for a move lower to 0.78. The trade is based on

the view that divergent monetary policy and the repricing of hikes in the UK money

market curve will continue in the wake of strong growth, while low inflation in the euro

zone will keep the ECB on a dovish stance and weigh on the euro.

UK recovery to continue

When Mark Carney was appointed the next Governor of the BoE on 26 November 2012,

a new era started in UK monetary policy. It became clear that the new governor would do

‘whatever it takes’ to ‘escape velocity’ as he put it. The sterling suffered badly in H1 13

on this new ‘super dove’ that was about to head the Old Lady. However, when he

officially became governor on 1 July, his ‘dove wings’ were clipped a bit by the mere

introduction of the 7.0% unemployment threshold for rate hikes.

However, much more importantly, it turned out that Mark Carney had managed to kick-

start optimism and growth in the UK economy even before he was officially in office.

The UK economy has surprised strongly on the upside this autumn. GDP increased by

0.8% q/q in Q3 and UK PMI is now at the highest level since November 2010 and more

importantly, forward-looking indicators such as ‘PMI new orders’ point to even better

PMIs ahead and growth accelerating in Q1 next year. It is also our view that the

composition of UK growth will be broader based in 2014. The recovery will no longer be

driven only by the housing market and consumption. The strong turnaround in activity

bodes well for investment, and with a better global economy, even the Achilles heel of

the UK economy – exports – might soon start to pick up.

BoE and ECB on a divergent path in 2014

The MPC had previously said it would not consider tightening policy – neither raising the

Bank Rate nor unwinding the QE programme – at least until the unemployment rate has

fallen to 7%. However, in the November Inflation Report, the MPC moved its forecast for

this threshold to be met from Q3 16 to Q3 15. This is now much more aligned with

market expectations, as the market currently prices the first rate hike in summer 2015.

We expect more of the same in 2014 as the unemployment rate continues to edge lower

and probably hit the 7.0% earlier than currently expected by the BoE. We believe the

market will gradually move the timing of the first rate hike ahead in time and the BoE

will slowly follow suit. The recent, albeit small, change in the Funding for Lending

Scheme to exclude new housing loans is just an example of the direction in which we

believe the BoE will move in 2014.

On the other hand, we expect the ECB to remain on a dovish path in 2014 (implication

#2). The positive supply shock we expect in 2014 would push euro-zone inflation

dangerously close to zero. Also, just as the ECB could not tolerate too high inflation in

2008 and 2011 and hiked rates, in our view the reaction will be symmetrical when euro-

zone inflation continues to trend lower in Q1 14. To mitigate the low inflation our

macroeconomists expect the ECB will react in early 2014, likely by means of a deposit-

rate cut or alternative easing measures. This should help to exert downward pressure on

the euro. The UK will likely also face lower inflation in 2014 but contrasting with the

ECB we doubt the BoE will suddenly have to fight disinflation in 2014. We also do not

expect the BoE to be haunted by falling inflation expectations, which might very well be

the case for the ECB in 2014.

Trading strategy

Sell EUR/GBP spot @0.8360 for

a 0.7800 target with stop/loss at

0.8650

The genie is out of the bottle, UK PMI

Source: Macrobond

Relative rates important for EUR/GBP

Source: Macrobond

UK unemployment continues to drop

Source: Macrobond

12 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

Trade #4: short EUR/SEK through a bearish seagull

The short-term outlook for SEK is dominated by the Riksbank rate decision where we

have pencilled in a rate cut and thus see mainly upside risks. We consider any further

gains in EUR/SEK in the near term as offering attractive selling opportunities for

strategic players. We think that the medium-term outlook is constructive for the krona,

both in terms of data and in terms of relative monetary policy. In addition, at current

levels, the krona looks cheap versus the euro from a fundamental perspective.

Surprise in the data

There is a tight link between the past few months’ rise in EUR/SEK and soft hard data.

The thing is that survey data has consistently indicated that real growth momentum

should pick up but it has not yet done so. Instead, forecasters, us included, have been

forced to revise down their (our) 2013 GDP forecast(s). The stream of predominantly

negative data surprises has pushed EUR/SEK higher since the early autumn (see chart).

The macro surprise index, by construction, is mean reverting, which, given that the index

reached historical highs in November, suggests that the upside in EUR/SEK is limited and

that the next cyclical trend (cf implication #2) is for a lower EUR/SEK. Meanwhile, 2014

GDP forecasts have largely been left unchanged; a pick-up next year is still our base case

too, which, if correct, should provide the SEK with a tailwind over the medium term.

Relative yields

The short-term outlook is dominated by the upcoming Riksbank rate decision. We have

pencilled in a rate cut on 17 December and thus see mainly upside risks in EUR/SEK

through year-end. A test of 9.00 could be on the cards if the bank does cut and is also read

as really soft. However, we do not expect these levels to last. Our short-term rate model

indicates that EUR/SEK has overshot with fair value remaining around 8.60.

We must not forget that this is a relative play, where the Riksbank is obviously not the

only bank lowering rates and Sweden not the only country with low/falling inflation.

Thus, it is not evident that a currency with still positive rates such as SEK should

underperform vis-à-vis the EUR where the policy rate is nailed close to zero and where

the bank is even considering negative rates and/or another LTRO. We see relative

monetary policy over the medium term as a tailwind rather than the opposite for the krona

versus the euro. Indeed, we believe a positive rate gap will prevail and the Riksbank will

be priced for hikes earlier than the ECB.

Moreover, Swedish inflation continues to undershoot its Euroland counterpart meaning

the krona is becoming increasingly undervalued (EUR/SEK overvalued) in terms of

purchasing power parity. Indeed, most long-term fundamental measures suggest

EUR/SEK is dear at current levels.

Key risks

The key risk to this trade relates to the Riksbank. ‘Low for long’ is not necessarily a risk

as it is a policy shared by most major central banks. However, if, for example, the

Riksbank were to do a 50bp cut this month, the rebound in the krona would be delayed

further. We see verbal interventions on behalf of the Riksbank aimed at weakening the

krona as remote, unlikely and, not least, misleading. Another upside risk for EUR/SEK

would be if hard data, contrary to our expectations, failed to pick up.

Trading strategy

Enter a seagull (ratioed) for

EUR/SEK downside: buy 1*8.90

put; sell 2*8.60 put; sell 1*9.30

call; horizon: 6M (spot ref 8.92).

Zero cost.

This trade will profit if EUR/SEK

trades between 8.30 and 8.90 at

maturity, maximum profit at 8.60.

EUR/SEK vs surprise index

Source :Macrobond

EUR/SEK vs relative rates

Source: Macrobond

Bearish EUR/SEK seagull P/L

Source: Danske Bank Markets

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

8.2 8.3 8.4 8.5 8.6 8.7 8.8 8.9 9 9.1 9.2 9.3 9.4

P/L

EUR/SEK (at expiry)

Seagull

Spot ref.: 8.92

Rate: 8.60

Rate: 9.30Rate: 8.30

13 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

Trade #5: long NOK for a fifth time

We have successfully over the past four years promoted long NOK strategies in our

annual FX Top Trades. However, the ‘Northern star’ has been one of the worst

performing G10 currencies for the past six months. After the latest NOK sell-off and

given relative monetary policy and too negative growth expectations for Norway, we

now recommend positioning for a lower EUR/NOK through a risk reversal that

currently offers attractive pricing and some protection against still erratic moves in the

cross.

Norges Bank �low for longer�, but no rate cut

The December Monetary Policy Report from Norges Bank underlined that it is ‘low for

longer’. The Norwegian central bank clearly stated that no rate hike should be expected

before the summer of 2015. However, importantly, no rate cut was discussed and Norges

Bank did not revert to the dovish message in June when it said that a rate cut was more

likely than a rate hike. Norges Bank’s rate path is now slightly above market pricing,

where a small probability of a rate cut is expected. Given our view on Norwegian growth

and inflation, we see little risk of Norges Bank actually cutting rates in 2014. In our view,

Norges Bank is now firmly on hold and it will take yet another turn for the worse to

trigger a rate cut. Furthermore, if we take our view that the ECB will keep a dovish stance

in 2014 into account, we believe that relative rates will be supportive for the NOK in

2014 (cf implication #2). EUR/NOK still has a very high correlation with relative rates.

Oil investments and housing collapse fears overdone

Growth in the Norwegian economy has slowed throughout 2013 and the latest Regional

Network Report indicated that growth would be below trend in Q1 14. However, the

really big concern for the Norwegian economy is the risk of a collapse in oil investments

and the housing market.

The December oil investment survey from the Statistical Office showed that oil

investments are expected to rise 7% in 2014 after growing 17% in 2013. Hence, there are

still few signs that Norway is going to experience a direct drop in oil investments in 2014.

In that respect, Norway is still different to, for example, Australia where it seems that a

peak in mining investments is now much closer.

In respect of the housing market, income growth is still very healthy in the Norwegian

economy and demand for housing is expected to continue for demographic reasons.

Further, the recent reassurance from Norges Bank that it intends to keep rates low for a

prolonged period of time should underpin the housing market. Remember, Norwegian

households are primarily financed short and the interest burden is still at a modest level

relative to disposable income.

NOK liquidity premium to ease in Q1

One of the reasons why the NOK has suffered recently has been the poor liquidity, which

has added a ‘liquidity premium’ to the NOK. We estimate that this premium will slowly

disappear throughout the first quarter of 2014, adding support to the NOK. However, if

the poor liquidity continues in Q1 it would be a clear risk to this trade. The same foes for

the general weak demand for commodity currencies (cf implication #4) and a further

reversal of safe-haven flows from 2011 and 2013. The risk of erratic moves and an

attractive skew is also the reason why we recommend using a risk reversal to position for

a lower EUR/NOK.

Trading strategy

We recommend entering a risk

reversal to benefit from an

expected move lower in EUR/NOK

on a 6M horizon: buy a 6M

EUR/NOK put at 8.30 and sell a

6M EUR/NOK call at 8.70 (zero

cost, spot ref. 8.4390).

The skew is positive and offers

close to a 2:1 ratio between the

two strikes relative to the spot.

Alternatively sell EUR/NOK spot.

Norges Bank on hold

10 11 12 13 14 15 161.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

% %

<< 3M NOKFRA (market pricing)

MPR 4/13 (3M NIBOR forecast Norges Bank)

Source: Norges Bank, Danske Bank Markets

Attractive skew in EUR/NOK

Source: Macrobond, Danske Bank Markets

P&L diagram: EUR/NOK risk reversal

Danske Bank Markets

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

8 8.1 8.2 8.3 8.4 8.5 8.6 8.7 8.8 8.9Spot

P&L at maturity

Spotref.: 8.4390

<<P&L (% of notional)

14 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

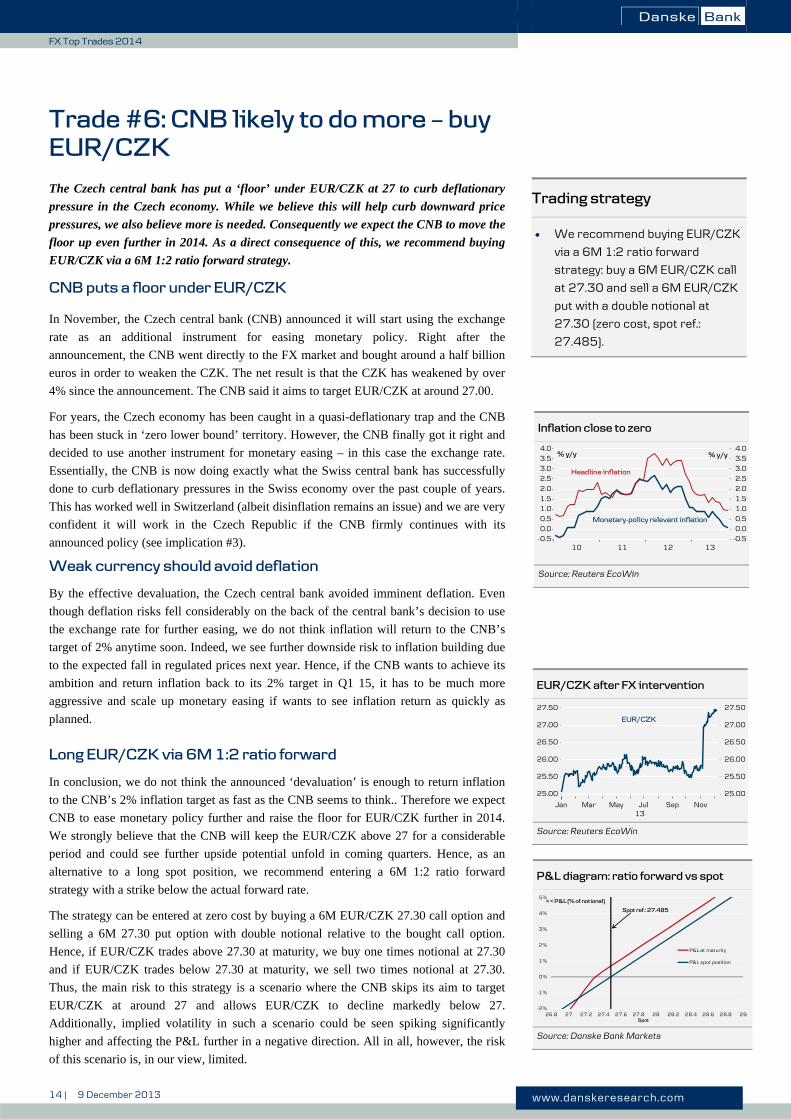

Trade #6: CNB likely to do more � buy EUR/CZK

The Czech central bank has put a ‘floor’ under EUR/CZK at 27 to curb deflationary

pressure in the Czech economy. While we believe this will help curb downward price

pressures, we also believe more is needed. Consequently we expect the CNB to move the

floor up even further in 2014. As a direct consequence of this, we recommend buying

EUR/CZK via a 6M 1:2 ratio forward strategy.

CNB puts a floor under EUR/CZK

In November, the Czech central bank (CNB) announced it will start using the exchange

rate as an additional instrument for easing monetary policy. Right after the

announcement, the CNB went directly to the FX market and bought around a half billion

euros in order to weaken the CZK. The net result is that the CZK has weakened by over

4% since the announcement. The CNB said it aims to target EUR/CZK at around 27.00.

For years, the Czech economy has been caught in a quasi-deflationary trap and the CNB

has been stuck in ‘zero lower bound’ territory. However, the CNB finally got it right and

decided to use another instrument for monetary easing – in this case the exchange rate.

Essentially, the CNB is now doing exactly what the Swiss central bank has successfully

done to curb deflationary pressures in the Swiss economy over the past couple of years.

This has worked well in Switzerland (albeit disinflation remains an issue) and we are very

confident it will work in the Czech Republic if the CNB firmly continues with its

announced policy (see implication #3).

Weak currency should avoid deflation

By the effective devaluation, the Czech central bank avoided imminent deflation. Even

though deflation risks fell considerably on the back of the central bank’s decision to use

the exchange rate for further easing, we do not think inflation will return to the CNB’s

target of 2% anytime soon. Indeed, we see further downside risk to inflation building due

to the expected fall in regulated prices next year. Hence, if the CNB wants to achieve its

ambition and return inflation back to its 2% target in Q1 15, it has to be much more

aggressive and scale up monetary easing if wants to see inflation return as quickly as

planned.

Long EUR/CZK via 6M 1:2 ratio forward

In conclusion, we do not think the announced ‘devaluation’ is enough to return inflation

to the CNB’s 2% inflation target as fast as the CNB seems to think.. Therefore we expect

CNB to ease monetary policy further and raise the floor for EUR/CZK further in 2014.

We strongly believe that the CNB will keep the EUR/CZK above 27 for a considerable

period and could see further upside potential unfold in coming quarters. Hence, as an

alternative to a long spot position, we recommend entering a 6M 1:2 ratio forward

strategy with a strike below the actual forward rate.

The strategy can be entered at zero cost by buying a 6M EUR/CZK 27.30 call option and

selling a 6M 27.30 put option with double notional relative to the bought call option.

Hence, if EUR/CZK trades above 27.30 at maturity, we buy one times notional at 27.30

and if EUR/CZK trades below 27.30 at maturity, we sell two times notional at 27.30.

Thus, the main risk to this strategy is a scenario where the CNB skips its aim to target

EUR/CZK at around 27 and allows EUR/CZK to decline markedly below 27.

Additionally, implied volatility in such a scenario could be seen spiking significantly

higher and affecting the P&L further in a negative direction. All in all, however, the risk

of this scenario is, in our view, limited.

Trading strategy

We recommend buying EUR/CZK

via a 6M 1:2 ratio forward

strategy: buy a 6M EUR/CZK call

at 27.30 and sell a 6M EUR/CZK

put with a double notional at

27.30 (zero cost, spot ref.:

27.485).

Inflation close to zero

10 11 12 13-0.50.0

0.5

1.01.5

2.0

2.5

3.03.5

4.0

-0.50.0

0.5

1.01.5

2.0

2.5

3.03.5

4.0% y/y % y/y

Monetary-policy relevant inflation

Headline inflation

Source: Reuters EcoWin

P&L diagram: ratio forward vs spot

Source: Danske Bank Markets

EUR/CZK after FX intervention

Jan13

Mar May Jul Sep Nov

25.00

25.50

26.00

26.50

27.00

27.50

25.00

25.50

26.00

26.50

27.00

27.50

EUR/CZK

Source: Reuters EcoWin

-2%

-1%

0%

1%

2%

3%

4%

5%

26.8 27 27.2 27.4 27.6 27.8 28 28.2 28.4 28.6 28.8 29Spot

P&L at maturity

P&L spot position

Spot ref.: 27.485

<< P&L (% of notional)

15 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

Trade #7: commodities - hands off! Sell AUD and CAD against USD

We suggest positioning for a move lower in selected commodity currencies against

USD. While both AUD and CAD have already suffered extensively this year, we think

central banks along with commodity markets will accommodate more of the same next

year. Specifically, we suggest selling an equally weighted basket of AUD and CAD

against USD; this costs an indicative 1.61% in negative carry (ann.); target at 106; stop

at 97.

Significant 2013 moves in AUD and CAD...

As we emphasise in implication #4, commodity currencies could in general continue to

weaken in 2014, as exporters need to rebalance growth towards the non-resource sector as

terms of trade turn less favourable. Australia has already suffered markedly on this

account. Moreover, as we discussed in implication #2, it is increasingly clear that a range

of central banks will lag the Fed in moving towards tighter policy: both the Reserve Bank

of Australia (RBA) and the Bank of Canada (BoC) have made important changes in their

policy stances in a more dovish direction this year. As a result, AUD and CAD have lost

13% and 7%, respectively, against USD in the year so far.

... to be continued in 2014 as RBA and BoC lag Fed

Will these downtrends be sustained heading into 2014? We think so – albeit we stress that

the large moves of 2013 are unlikely to materialise again – not least considering that we

are now closer to PPP levels on both AUD and CAD. First of all, we look for downward

pressure on oil and metal prices to continue as a result of the global supply shock

discussed above. Moreover, we expect China to get a soft start to 2014, not least as

monetary policy has tightened recently; this would add to the potential for looser market

balances within commodities.

Second, RBA remains rather explicit about its boldness to push AUD lower still, denoting

its level ‘uncomfortably high’ despite the violent sell-off this year. RBA has been

reluctant to cut more aggressively, as past easing is expected to come into effect gradually

and as still elevated commodity prices have kept the resource sector going strong in a

historical perspective and thus inflation close to target. There is a small chance the RBA

may cut rates next year (not priced), or more likely, we think that the central bank will

step up on intervention to curb AUD strength more directly without the unwarranted

effects of further rate cuts (implication 3).

Third, BoC has adopted a ‘neutral’ policy stance and now seems determined to shift the

composition of growth towards exports, which has been a drag for a while. While BoC

remains much more hands-off the currency than the RBA, we think governor Poloz and

co will now want to clearly lag the Fed in moving towards rate hikes. Notably, there is a

chance the market may actually start to price a cut from BoC (it may not necessarily

materialise though). One thing that keeps holding the BoC back in committing to “low

rates for longer” as the bank has done previously is the household imbalances that persist

despite various macro-prudential attempts to curb these.

Finally, the USD strength that we project from a steepening of the US money-market

curve should also play a role in pushing AUD and CAD further down against USD.

Risks: less dovish central banks

RBA and/or BoC turn less dovish than we look for as global growth picks up and the Fed

tapers. Also, we should not forget that speculators are already positioned for further AUD

downside; shorts are at less extreme levels for CAD.

Trading strategy

Sell AUD/USD (spot ref. 0.9067)

and buy USD/CAD (spot ref.

1.0659) in equal amounts @ 100

for a 106 target; stop at 97; this

has an indicative negative carry of

1.61% annually.

AUD, CAD vs USD and GSCI

Source: Macrobond, Danske Bank Markets

Pricing of central banks

Source: Danske Bank Markets

Positioning is a risk

Source: Macrobond, Danske Bank Markets

0

0.01

0.02

0.03

0.04

0.05

0.06 BoC Fed RBA

16 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

Trade #8: global growth but lower oil price � buy TRY/DKK

Following a sharp correction this year, the Turkish lira no longer looks overvalued. We

therefore like what 2014 has to offer for TRY. Overall, the global positive supply shock

creates a beneficial environment for the currency. Furthermore, we like what the

prospects of an Iran nuclear deal would mean for the lira. Finally, being long

TRY/DKK offers good carry.

2014 should favour the lira

One argument in favour of the lira in 2014 is the positive supply shock that is set to

continue to be a main driver in the global economy next year. The positive supply shock

implies higher global growth (implication #1), lower commodity prices (implication #4)

and central banks keeping monetary policy easy, which creates beneficial conditions for

the lira ((implication #2).

Turkish exports will gain on higher global growth, while lower commodity prices should

reduce Turkish import expenses on oil and other commodities. Both factors will

contribute to erasing part of the large Turkish current account deficit. A narrowing of the

deficit, which currently runs close to 7% of GDP, would better the long-term valuation of

the lira.

Furthermore, we like what the prospects of a more comprehensive deal on Iran’s nuclear

programme, which could be on the cards in 2014, offers for the lira. An Iran nuclear deal

would probably be beneficial for the Turkish current account balance, as it would weigh

further on oil prices and furthermore remove the strains Turkish exporters currently face

on the Iranian market due to the West’s sanctions.

Also, a deal would be likely to do much to ease geopolitical tensions in the Middle East.

That would mean a decline in the geopolitical premium, which would be a further

positive for the lira.

Lira no longer looks overvalued

This year has been hard on the lira. Amid the market pricing in Fed tapering, the lira

suffered a heavy beating along with other emerging market currencies over the course of

the summer. In nominal effective terms, the lira has lost almost 12% since April – the

biggest six-month slide since 2011.

However, following the correction, our fair-value model now indicates that the lira is no

longer overvalued. With the lira close to fair value, there is a good foundation for taking

on a long position in the lira in 2014.

TRY/DKK offers good carry

Furthermore, going long the Turkish lira against the Danish kroner would add good carry.

Following the November ECB refinancing rate cut we have become more sceptical on the

outlook for independent rate hikes from Danmarks Nationalbank next year. Furthermore,

ECB is set to remain on an easing bias next year which will keep a lid on Danish rates as

well.

On the other hand, we expect Turkish rates to remain relatively stable in 2014 as well. We

therefore recommend going long TRY/DKK spot at 2.6750 for a 2.85 target with a stop

loss at 2.5880. One might also consider locking in the current high carry using a forward

(see the graph to the right for annualised carry with different tenors).

Trading strategy

Buy TRY/DKK spot @ 2.6750;

target @ 2.85; stop @ 2.5885.

Alternatively, consider locking in

the current level carry via a

forward.

Summer EM sell-off hurt TRY badly

Source: Bloomberg

Turkish CA deficit to fall in 2014

Source: Macrobond

Long TRY/DKK (annualised carry, %)

Source: Danske Bank Markets (indicative prices)

6.8%6.9%7.0%7.1%7.2%7.3%7.4%7.5%7.6%7.7%7.8%

1M 2M 3M 4M 5M 6M 7M 8M 9M 10M 11M 1Y 2Y 3Y

Tenors

17 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

Trade #9: China continues to muddle through - sell 12M USD/CNH

Position for a continued modest appreciation of CNY in 2014 and take advantage of the

current depreciation expectations in the market by selling a 12M USD/CNH. The

offshore CNH currently discounts the largest depreciation in the forward curve and

hence we recommend using the offshore CNH market instead of the non-deliverable

USD/CNY forwards.

CNY still appears to be undervalued despite recent appreciation

CNY still appears to be slightly undervalued despite a real appreciation of close to 45%

against USD since 2005. China’s exports overall continue to gain market share on the

international market and we expect China’s current account to again start increasing

moderately to close to 3% of GDP in 2014 from about 2% of GDP in 2013, supported by

improving exports to the developed countries and lower energy and commodity prices.

The rise in China’s FX reserves has also picked up pace again recently and USD/CNY

continues to trade in the lower end of the daily trading band, underscoring continued

underlying appreciation pressure on CNY.

The economic policy in China should also continue to favour a stronger CNY – at least in

the short run. The People’s Bank of China ( PBoC) has de facto started to move monetary

policy in a tightening direction on the back of higher inflation and renewed acceleration

in house prices. In general, PBoC has tended to allow a faster appreciation of CNY when

monetary policy is tightened. In addition, the Chinese government believes that a stronger

CNY will support its long-term goal of rebalancing the Chinese economy more towards

private consumption (implication #3).

The longer-term goal for China’s exchange rate system is a floating exchange rate and a

fully convertible currency. The implication of full convertibility is that external capital

flows will gradually be liberalised. However, the liberalisation of the capital account will

be cautious and China’s capital account remains relatively closed compared with other

Asian countries. Hence, CNY will continue to be a relatively “safe haven” when if stress

emerges in emerging markets on a broader scale and for that reason CNY is our preferred

pick among the Asian currencies for 2014 (implication #4).

In recent years it has be favourable to be long CNY against USD. We continue to

recommend being long CNY based on our expectations that the Chinese economy will

continue to muddle through. If, on the other hand, one believes that the Chinese economy

faces a severe hard landing, this is not the trade to consider. In addition, it should stressed

that with China moving towards a floating exchange rate and convertibility, CNY will

gradually become a less one-sided bet. There will be more two-way volatility in the

USD/CNY exchange rate and further ahead capital account liberalisation could add

deprecation pressure.

In the FX market both the offshore market in Hong Kong (USD/CNH) and the non-

deliverable forward market (USD/CNY NDF) currently discount a slight depreciation of

CNY against the USD. Because the USD/CNY NDF uses the PBoC reference exchange

rate (used to fix the daily trading band) and not the spot exchange rate for settlement at

expiry, the discounted depreciation in the NDF is extremely modest (see chart). Instead,

we recommend using the USD/CNH forwards where the 12M USD/CNH currently

discounts a 1% depreciation of CNH over the next year.

Trading strategy

Sell 12M USD/CNH (forward) @

6.1360 for target @ 5.96 and

stop @ 6.23.

Position for China continuing to

muddle through and continued

moderate appreciation of CNY.

Continued depreciation, albeit at slower pace

Source: Reuters EcoWin

FX reserves increasing again

Source: Reuters EcoWin

Offshore CNH market discount largest depreciation

Source: Bloomberg

Apr11

Aug Dec12

Apr Aug Dec13

Apr Aug

6.0

6.1

6.2

6.3

6.4

6.5

6.6

6.0

6.1

6.2

6.3

6.4

6.5

6.6USD/CNY exchange rate

PBoC reference rate

Daily trading band

Spot

10 11 12 13

-400

-200

0

200

400

600

-400

-200

0

200

400

600

Banks purchase of foreign exchange from clients

Bn CNYBn CNY

Change in FX reserves, smoothed

6.04

6.06

6.08

6.1

6.12

6.14

6.16

6.18

6.2

0 0.2 0.4 0.6 0.8 1

Non-deliverable forward

CNH deliverable forward

USD /CNY forwards on offshore market

Year forward

PBoC referenceexchange rate

Spot USD/CNH

18 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

Trade #10: long RON/PLN on divergent growth and monetary policy

The Polish economy is still weak, inflation is well below target and the Polish central

bank (NBP) remains behind the curve. The likelihood of the ECB stepping up

monetary easing is increasing, which would put pressure on the NBP. The weak

economy and inflation well below target are likely to weigh on the PLN. While we

expect the PLN to remain under pressure next year, the RON is set to get some support

from improving economic activity and even though this trade does not provide much

carry, we nonetheless believe that RON should outperform PLN.

NBP should ease again...

We believe the NBP is falling behind the curve. Inflation continues to decline and

remains well below the NBP’s official 2.5% inflation target. Indeed, we expect inflation

to average less than 1% in 2014 and even though there are signs of a slight pick-up in

Polish growth, the output gap remains negative and growth seems set to be well below

potential growth in the coming one to two years.

Even though the NBP is keeping a fairly hawkish tone and is quite upbeat about growth

prospects, in our view it clearly downplays the risk of deflation and that it is considerably

undershooting its inflation target. Furthermore, according to our inflation models,

inflation is set to remain well below target over the coming two years. Even though the

NBP continues to say that the easing cycle is over and further rate cuts are not

forthcoming, in our view, low inflation combined with further downside risks to the

outlook mean that the NBP has to soften its rhetoric and reinitiate the easing cycle. Our

outlook for lower Polish interest rates is likely to weigh on the PLN (cf implication 2).

...while the NBR�s room for manoeuvre is limited

The Romanian economy saw some slowdown in 2012 but it started to recover in 2013

(Q3 GDP showed very nice growth of 4.1% y/y). We expect the Romanian economy to

continue to recover and next year’s GDP growth could be decent at more than 2.5%. As

inflation seems well contained and below the official target of 2.5%, we do not think that

more aggressive monetary easing is forthcoming. Indeed, we expect the Romanian central

bank (NBR) to keep interest rates at higher levels compared with its neighbouring

countries, which should support the currency. Furthermore, we expect the central bank to

prop up the currency if a sharp sell-off occurs given the large foreign exchange exposure

of Romanian households and companies. Hence, we expect the RON to be supported by

relatively high interest rates, the continued economic recovery (see implication #1) and

the sound external position of the economy (sustainable current account and budget

deficit).

Risks mainly on PLN

We are not that worried about the outlook for the RON given the sound economic

fundamentals and improving economic activity and the risk to our trade is mostly on the

PLN side. If the Polish economy performs better, we believe the NBP will remain fairly

hawkish and refrain from cutting interest rates further, while still ignoring well below

target inflation.

Trading strategy

Buy RON/PLN spot @ 0.9410 for

a target @ 0.985 and stop @

0.915.

RON/PLN to move higher in 2014

Jan11

May Sep Jan12

May Sep Jan13

May Sep0.875

0.900

0.925

0.950

0.975

1.000

1.025

1.050

1.075

0.875

0.900

0.925

0.950

0.975

1.000

1.025

1.050

1.075RON/PLN

Source: Reuters EcoWin

Deposit rates 12 months

08 09 10 11 12 132.5

5.0

7.5

10.0

12.5

15.0

17.5

20.0

2.5

5.0

7.5

10.0

12.5

15.0

17.5

20.0

Poland

Romania

Source: Reuters EcoWin

19 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

FX Research

Title Phone MailArne Lohmann Rasmussen Head of Strategy Chief Analyst +45 45 12 85 32 [email protected] Helt G10 Senior Analyst +45 45 12 85 18 [email protected] Tuxen G10 Senior Analyst +45 45 13 78 67 [email protected] Nærvig Pedersen Commodities Analyst +45 45 12 80 61 [email protected] Mellin SEK Senior Analyst +46 8 568 805 92 [email protected] Christensen EM Chief Analyst +45 45 12 85 30 [email protected] Pravdova-Nielsen EM Analyst +45 45 12 80 71 [email protected] Jegbjærg Nielsen Asia Senior Analyst +45 45 12 85 35 [email protected] Lomholt G10 Assistant Analyst [email protected]

Editorial deadline December 6, 14.00 cet.

20 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

Disclosure This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske

Bank’). The author of the research report is Arne Lohmann Rasmussen, Chief Analyst.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the

research report accurately reflect the research analyst’s personal view about the financial instruments and issuers

covered by the research report. Each responsible research analyst further certifies that no part of the compensation

of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed

in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject

to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske

Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority

(UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation

Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Society of Financial Analysts’

rules of ethics and the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-

quality research based on research objectivity and independence. These procedures are documented in Danske

Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any

request that might impair the objectivity and independence of research shall be referred to Research Management

and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do

not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes

investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate

finance or debt capital transactions.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology

as well as publicly available statistics for each individual security, issuer and/or country. Documentation can be

obtained from the authors on request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including a sensitivity analysis

of relevant assumptions, are stated throughout the text.

Date of first publication

See the front page of this research report for the date of first publication.

General disclaimer This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for

informational purposes only. It does not constitute or form part of, and shall under no circumstances be

considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments

(i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or

options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial

Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that

Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not

untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates

and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation

any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and

reflect their judgement as of the date hereof. These opinions are subject to change, and Danske Bank does not

undertake to notify any recipient of this research report of any such change nor of any other changes related to the

information provided in this research report.

This research report is not intended for retail customers in the United Kingdom or the United States.

21 | 9 December 2013 www.danskeresearch.com

FX Top Trades 2014

This research report is protected by copyright and is intended solely for the designated addressee. It may not be

reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior

written consent.