investment opportunities and policies in thailand board of... · investment opportunities and...

TRANSCRIPT

Investment Opportunities and Policies in Thailand

February 2016

Mr. Chokedee Kaewsang,

Deputy Secretary General

Office of the Board of Investment 1

2

2 Thailand as the ASEAN Hub

3 Cattle and Food Industry

1 Thailand at a Glance

4 Investment Incentives and BOI Services

Contents

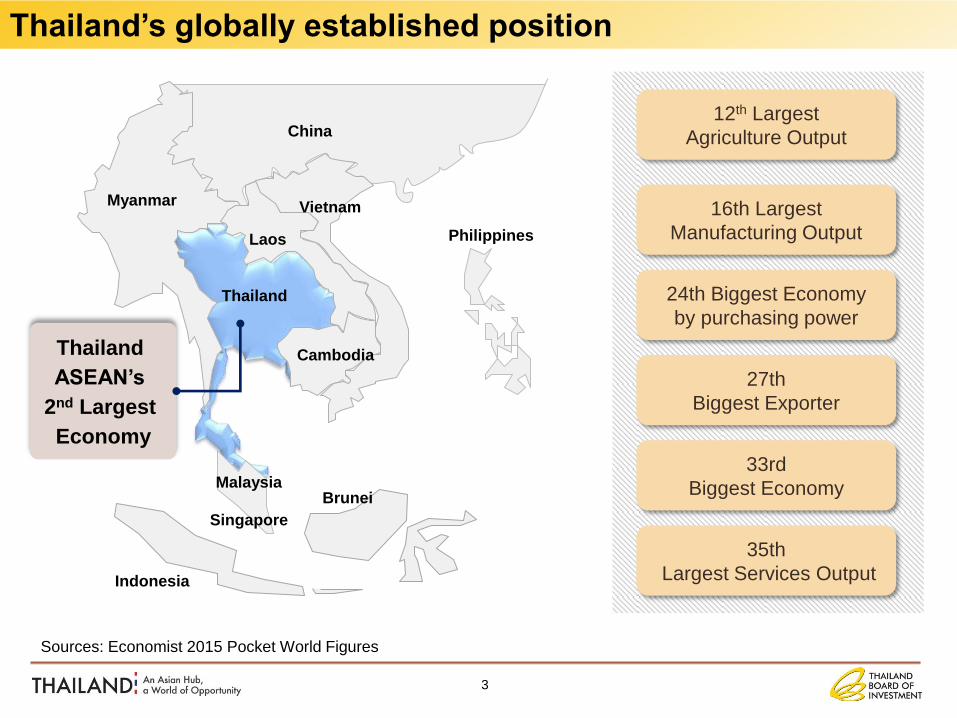

Sources: Economist 2015 Pocket World Figures

Vietnam

Cambodia

Thailand

Myanmar

China

Laos Philippines

Malaysia

Singapore

Indonesia

Thailand

ASEAN’s

2nd Largest

Economy

12th Largest

Agriculture Output

16th Largest

Manufacturing Output

24th Biggest Economy

by purchasing power

27th

Biggest Exporter

33rd

Biggest Economy

35th

Largest Services Output

Brunei

3

Thailand’s globally established position

4

Sources: World Bank, NESDB, Ministry of Commerce, Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

1 GDP AUD 528 billion, (per capita) AUD 8,111

Growth 3.5-4.5%

Thailand

2 Total Export Value AUD 318 billion

3 Population 68 million,

97% literacy rate

4 Taxation

• Corporate: 20%

• Withholding: 5%

• VAT: 7%

Economic Overview

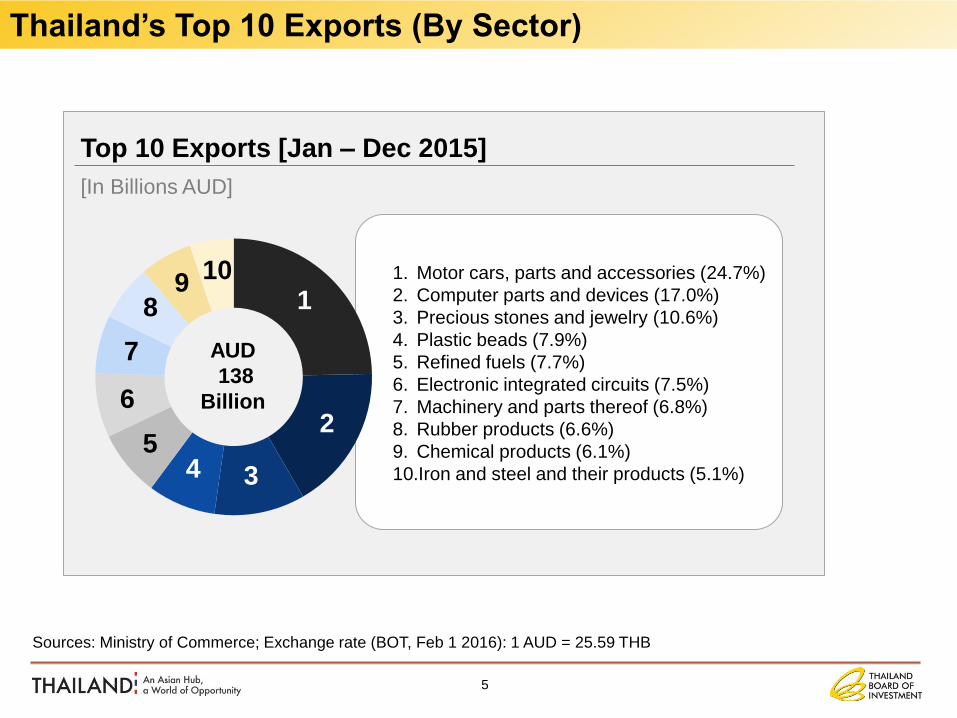

Top 10 Exports [Jan – Dec 2015]

1. Motor cars, parts and accessories (24.7%)

2. Computer parts and devices (17.0%)

3. Precious stones and jewelry (10.6%)

4. Plastic beads (7.9%)

5. Refined fuels (7.7%)

6. Electronic integrated circuits (7.5%)

7. Machinery and parts thereof (6.8%)

8. Rubber products (6.6%)

9. Chemical products (6.1%)

10.Iron and steel and their products (5.1%)

AUD

138

Billion

1

2

3 4 5

6

7

8 9

10

Sources: Ministry of Commerce; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

Thailand’s Top 10 Exports (By Sector)

[In Billions AUD]

5

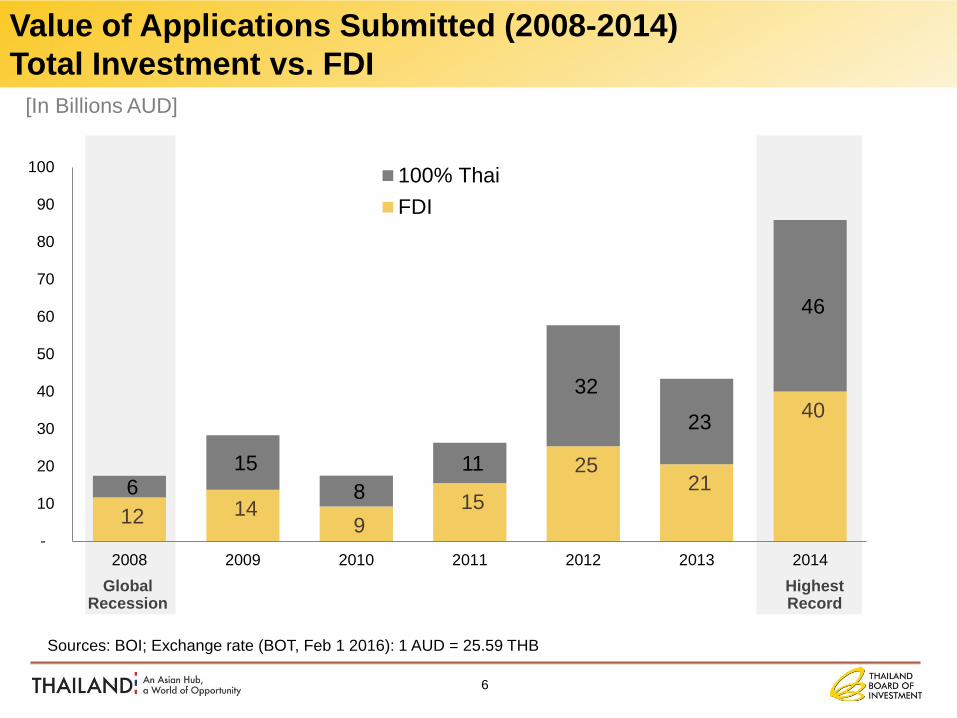

Sources: BOI; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

[In Billions AUD]

Global Recession

Highest Record

12 14 9

15

25 21

40

6 15

8

11

32

23

46

-

10

20

30

40

50

60

70

80

90

100

2008 2009 2010 2011 2012 2013 2014

100% Thai

FDI

6

Value of Applications Submitted (2008-2014)

Total Investment vs. FDI

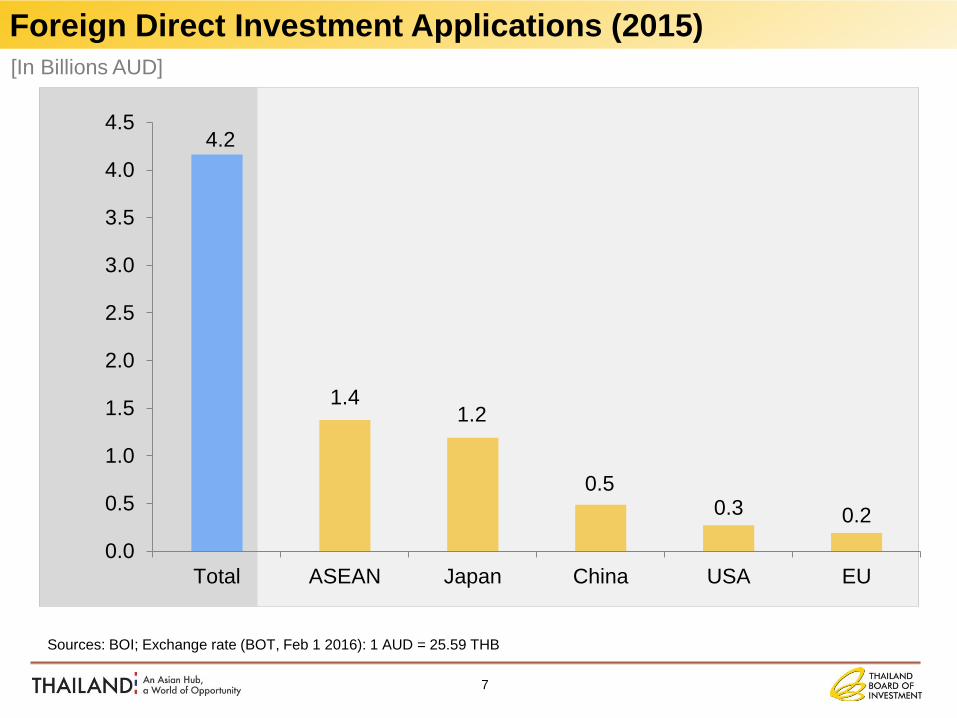

4.2

1.4 1.2

0.5 0.3 0.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Total ASEAN Japan China USA EU

[In Billions AUD]

7

Sources: BOI; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

Foreign Direct Investment Applications (2015)

Sources: BOI; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

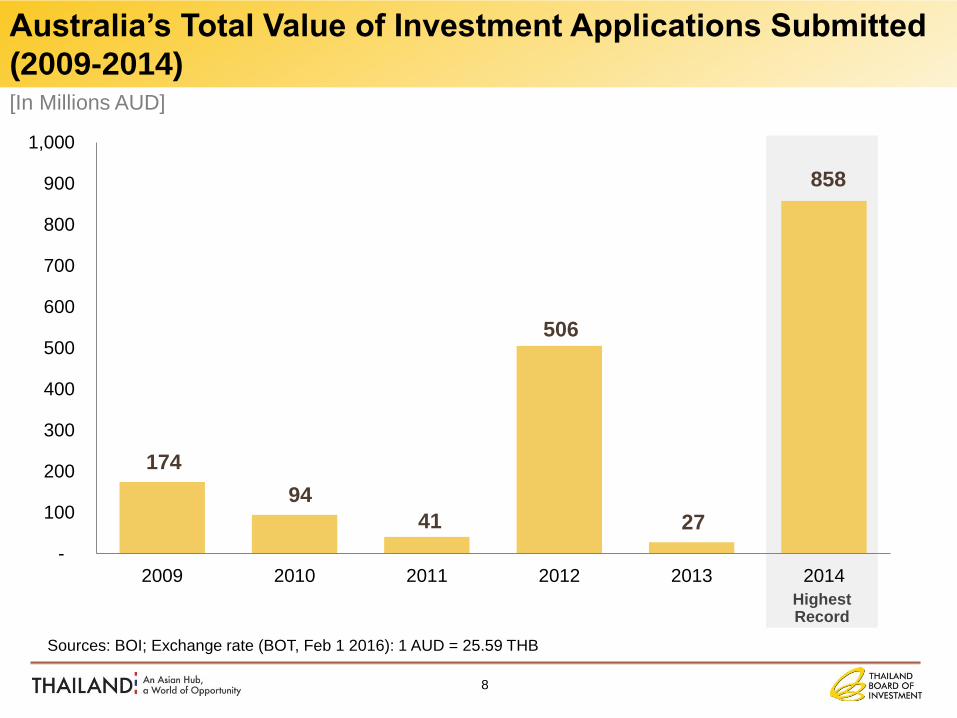

[In Millions AUD]

Highest Record

174

94

41

506

27

858

-

100

200

300

400

500

600

700

800

900

1,000

2009 2010 2011 2012 2013 2014

8

Australia’s Total Value of Investment Applications Submitted

(2009-2014)

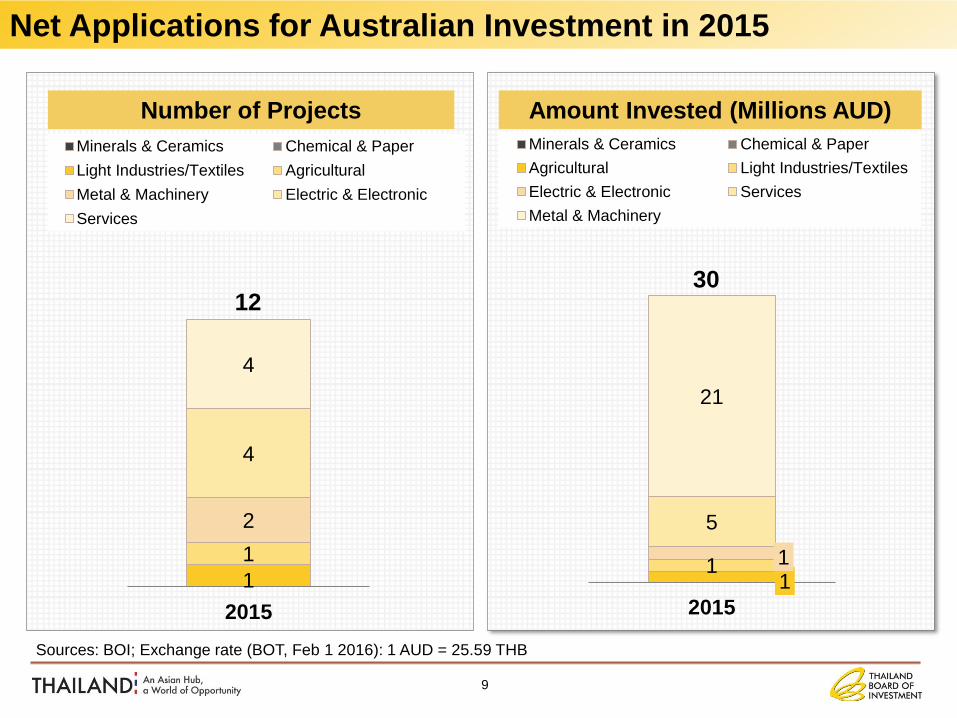

Number of Projects

1

1

2

4

4

2015

Minerals & Ceramics Chemical & Paper

Light Industries/Textiles Agricultural

Metal & Machinery Electric & Electronic

Services

Amount Invested (Millions AUD)

1 1 1

5

21

2015

Minerals & Ceramics Chemical & Paper

Agricultural Light Industries/Textiles

Electric & Electronic Services

Metal & Machinery

Sources: BOI; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

12 30

9

Net Applications for Australian Investment in 2015

10

2 Thailand as the ASEAN Hub

3 Cattle and Food Industry

1 Thailand at a Glance

4 Investment Incentives and BOI Services

Contents

11

AEC

Asia &

Oceania

“We are surrounded by the

world’s economic powerhouses”

1 Strategic Location – right at the

Center of Mainland ASEAN

2 Strategic Location – gateway to

ASEAN

Thailand’s Strategic Location Offers Many Advantages

12

Sources: IMF as of 2014, Ministry of Foreign Affairs of March 2015

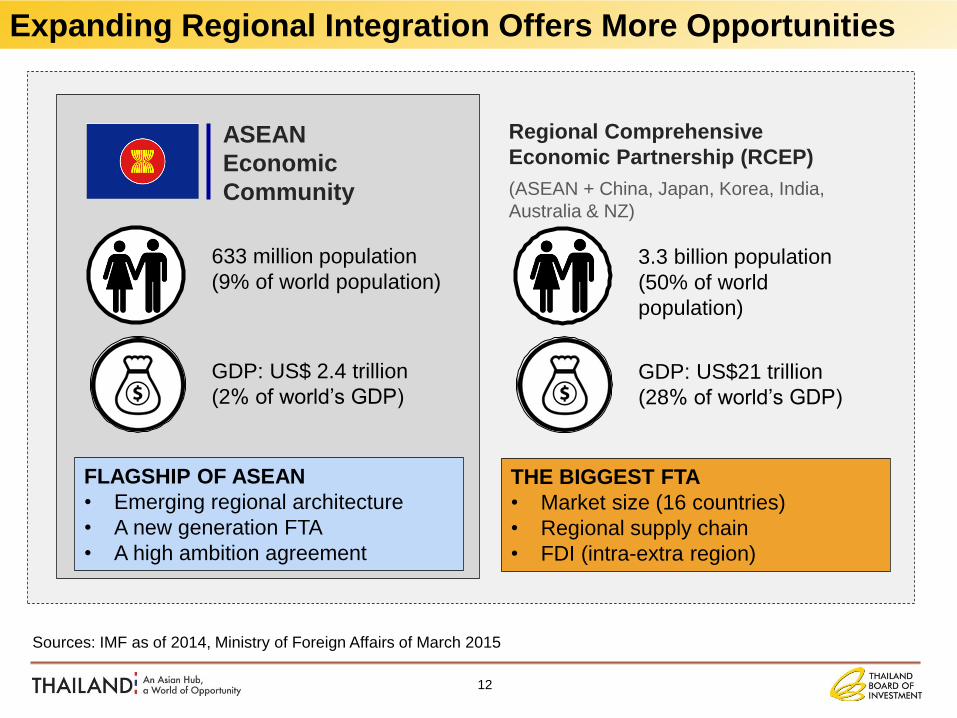

ASEAN

Economic

Community

633 million population

(9% of world population)

GDP: US$ 2.4 trillion

(2% of world’s GDP)

FLAGSHIP OF ASEAN

• Emerging regional architecture

• A new generation FTA

• A high ambition agreement

Regional Comprehensive

Economic Partnership (RCEP)

(ASEAN + China, Japan, Korea, India,

Australia & NZ)

3.3 billion population

(50% of world

population)

GDP: US$21 trillion

(28% of world’s GDP)

THE BIGGEST FTA

• Market size (16 countries)

• Regional supply chain

• FDI (intra-extra region)

Expanding Regional Integration Offers More Opportunities

13

2 Thailand as the ASEAN Hub

3 Cattle and Food Industry

1 Thailand at a Glance

4 Investment Incentives and BOI Services

Contents

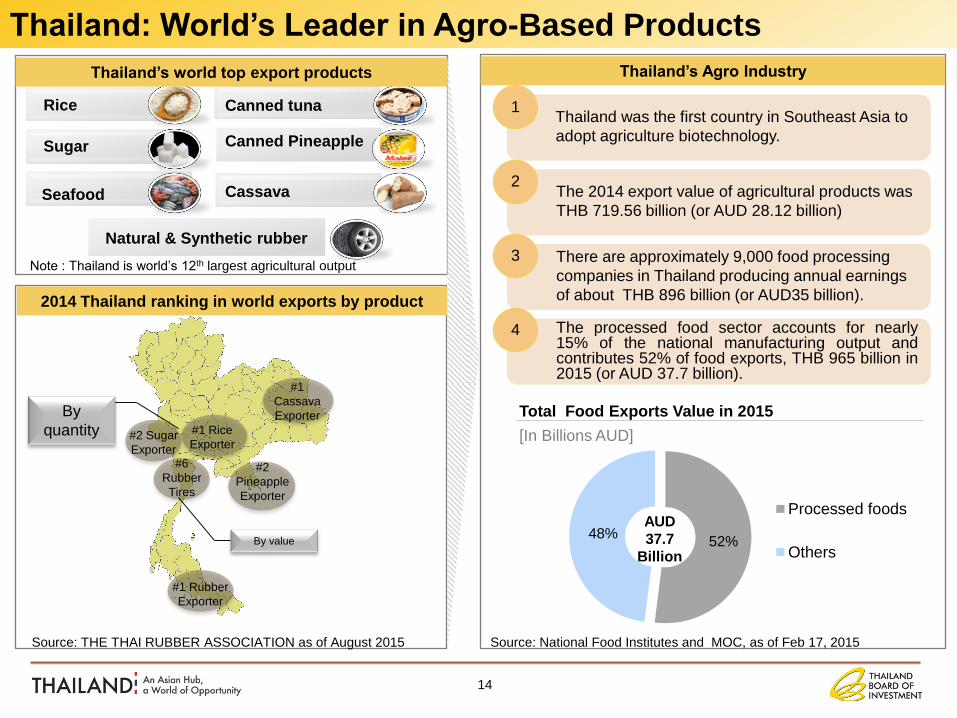

2014 Thailand ranking in world exports by product

#1

Cassava

Exporter

#1 Rubber

Exporter

#1 Rice

Exporter

#2

Pineapple

Exporter

#2 Sugar

Exporter #6

Rubber

Tires

Note : Thailand is world’s 12th largest agricultural output

Sugar

Seafood

Canned tuna

Canned Pineapple

Cassava

Natural & Synthetic rubber

Rice

Thailand’s world top export products

Thailand was the first country in Southeast Asia to

adopt agriculture biotechnology.

The 2014 export value of agricultural products was

THB 719.56 billion (or AUD 28.12 billion)

There are approximately 9,000 food processing

companies in Thailand producing annual earnings

of about THB 896 billion (or AUD35 billion).

52% 48%

Processed foods

Others

1

3

2

The processed food sector accounts for nearly 15% of the national manufacturing output and contributes 52% of food exports, THB 965 billion in 2015 (or AUD 37.7 billion).

4

[In Billions AUD]

Total Food Exports Value in 2015

Thailand’s Agro Industry

AUD

37.7

Billion

Source: National Food Institutes and MOC, as of Feb 17, 2015 Source: THE THAI RUBBER ASSOCIATION as of August 2015

By

quantity

By value

14

Thailand: World’s Leader in Agro-Based Products

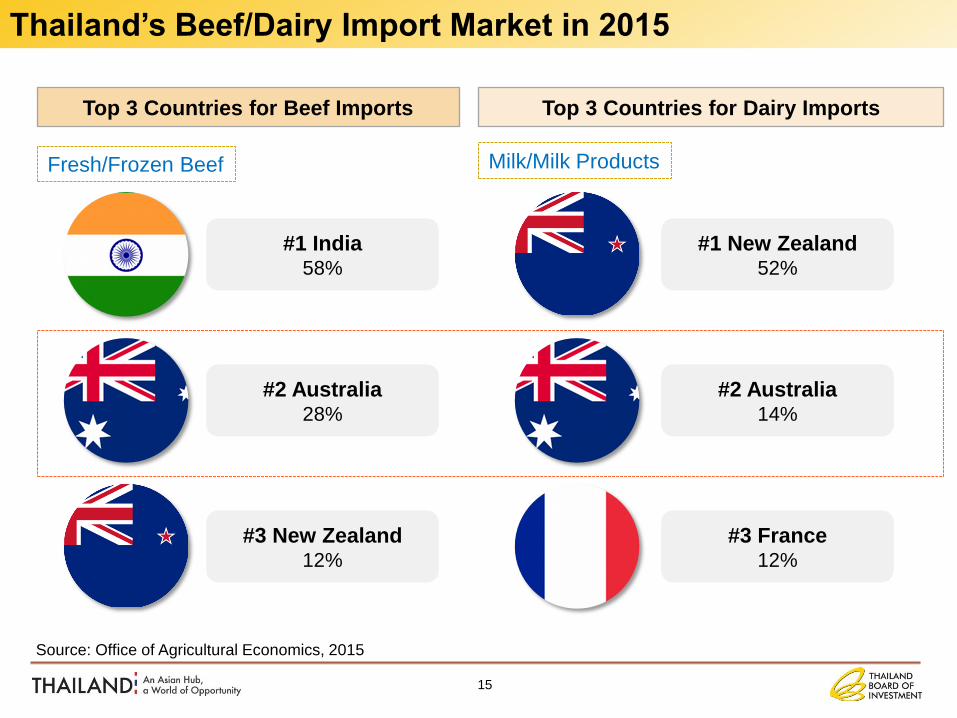

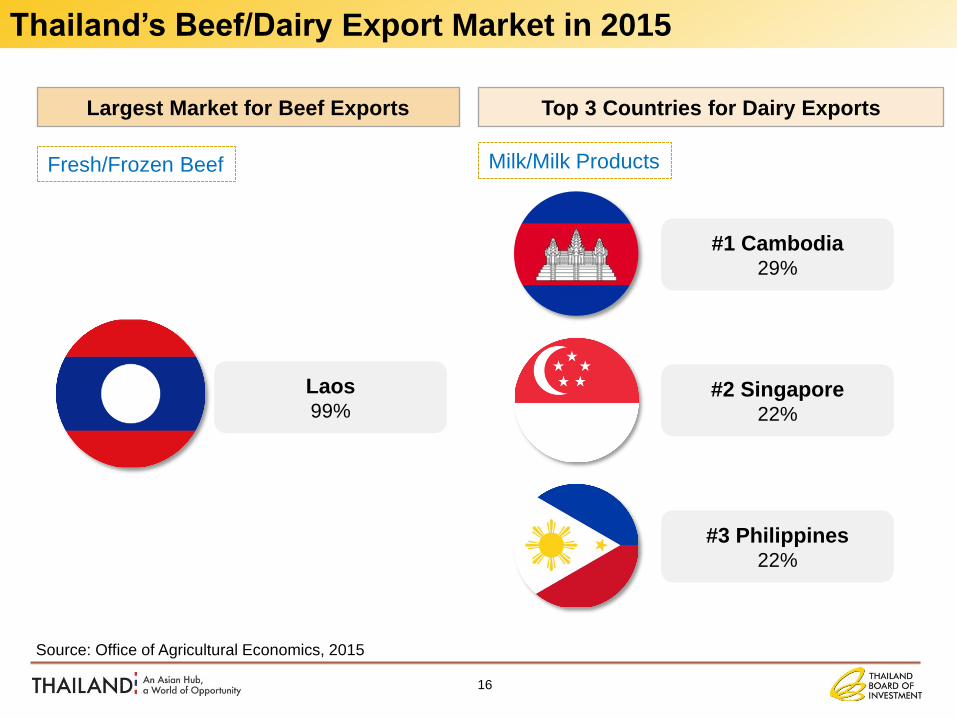

Fresh/Frozen Beef

15

Top 3 Countries for Beef Imports Top 3 Countries for Dairy Imports

Thailand’s Beef/Dairy Import Market in 2015

Source: Office of Agricultural Economics, 2015

Milk/Milk Products

#1 India 58%

#2 Australia 28%

#3 New Zealand 12%

#1 New Zealand 52%

#2 Australia 14%

#3 France 12%

Fresh/Frozen Beef

16

Largest Market for Beef Exports Top 3 Countries for Dairy Exports

Thailand’s Beef/Dairy Export Market in 2015

Source: Office of Agricultural Economics, 2015

Milk/Milk Products

#1 Cambodia 29%

#2 Singapore 22%

#3 Philippines 22%

Laos 99%

17

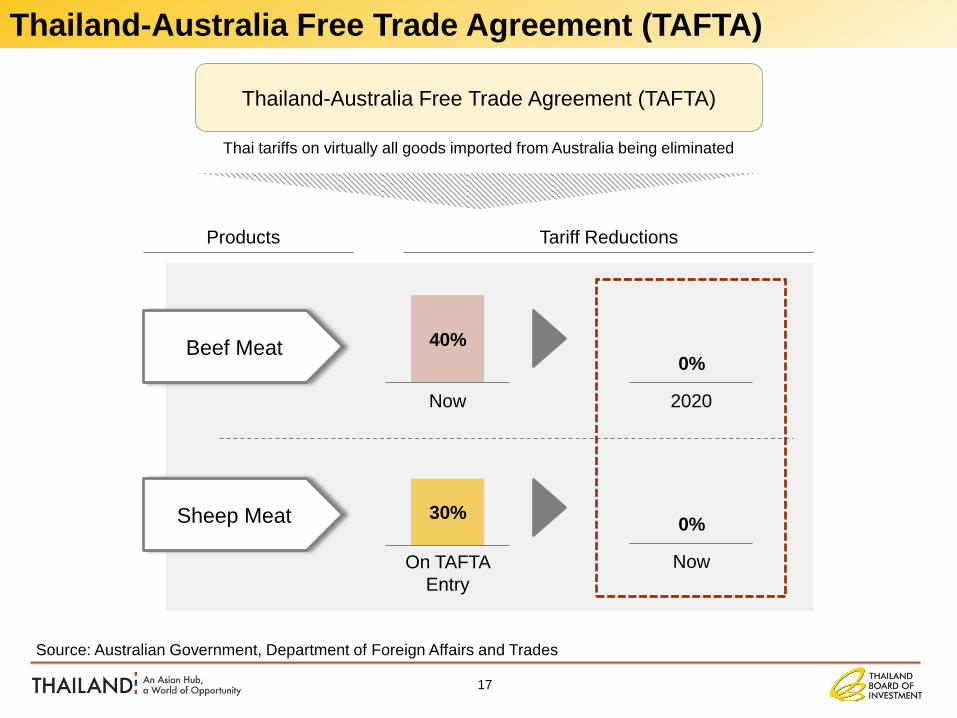

Source: Australian Government, Department of Foreign Affairs and Trades

Thailand-Australia Free Trade Agreement (TAFTA)

Thai tariffs on virtually all goods imported from Australia being eliminated

40%

Now

Beef Meat

2020

0%

Sheep Meat 30%

On TAFTA

Entry

Now

0%

Products Tariff Reductions

Thailand-Australia Free Trade Agreement (TAFTA)

Thailand’s Investment Sector in the Cattle Industry

Source: National Food Institutes, BOI

Slaughtering

Animal Propagation/Husbandry

ex: Beef cattle farming/ Dairy Farming

Plant/Animal Bleeding

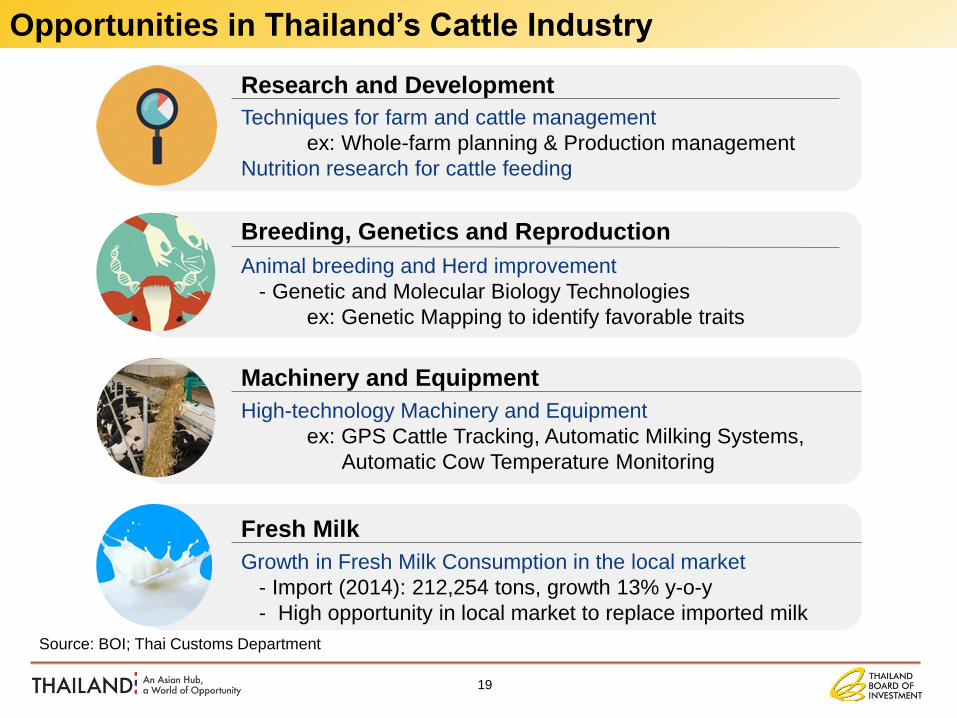

Opportunities in Thailand’s Cattle Industry

Source: BOI; Thai Customs Department

Breeding, Genetics and Reproduction

Animal breeding and Herd improvement

- Genetic and Molecular Biology Technologies

ex: Genetic Mapping to identify favorable traits

Research and Development

Techniques for farm and cattle management

ex: Whole-farm planning & Production management

Nutrition research for cattle feeding

Machinery and Equipment

High-technology Machinery and Equipment

ex: GPS Cattle Tracking, Automatic Milking Systems,

Automatic Cow Temperature Monitoring

Fresh Milk

Growth in Fresh Milk Consumption in the local market

- Import (2014): 212,254 tons, growth 13% y-o-y

- High opportunity in local market to replace imported milk

19

20

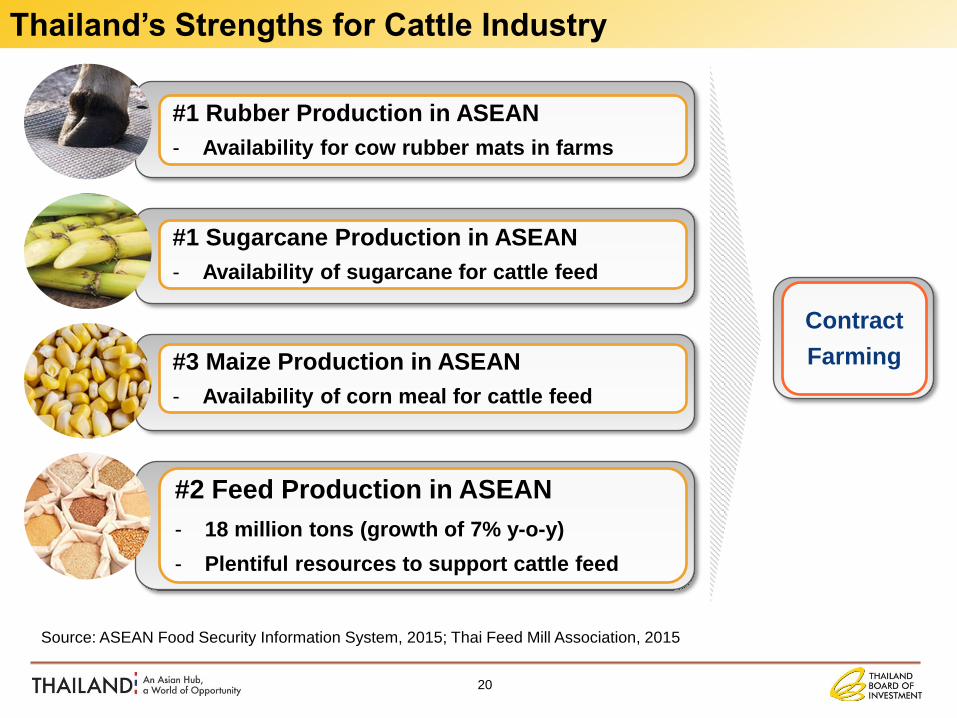

Thailand’s Strengths for Cattle Industry

Source: ASEAN Food Security Information System, 2015; Thai Feed Mill Association, 2015

#3 Maize Production in ASEAN

- Availability of corn meal for cattle feed

#1 Sugarcane Production in ASEAN

- Availability of sugarcane for cattle feed

#1 Rubber Production in ASEAN

- Availability for cow rubber mats in farms

Contract

Farming

#2 Feed Production in ASEAN

- 18 million tons (growth of 7% y-o-y)

- Plentiful resources to support cattle feed

Thailand: Food Safety Standards

Source: National Food Institutes, BOI

Thai food factories must apply for:

GMP

ISO

HACCP

TQM

Water and

Carbon foot print

Food exports must be applied for:

BRC

IFS

SQF

Standards applied to agricultural

commodities and food products are

certified by the National Bureau of

Agricultural Commodity and Food

Standards (ACFS) which include:

Good Manufacturing Practice (GMP)

Good Hygienic Practice (GHP)

ISO 22000 (Safety on Food Supply

Chain)

22

2 Thailand as the ASEAN Hub

3 Cattle and Food Industry

1 Thailand at a Glance

4 Investment Incentives and BOI Services

Contents

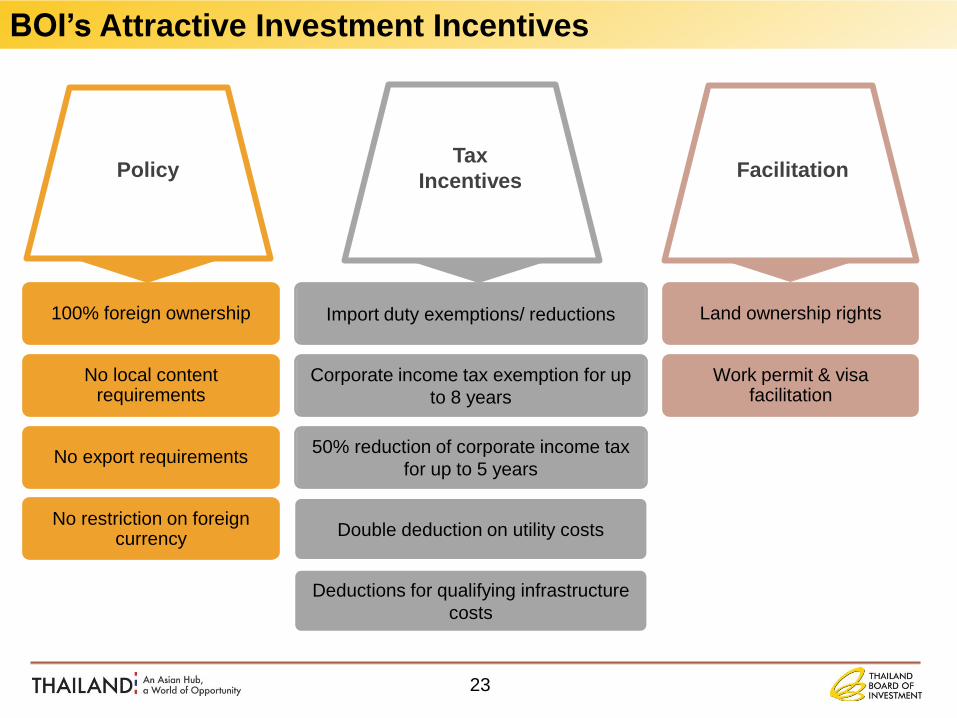

Policy Tax

Incentives Facilitation

100% foreign ownership

No local content requirements

No export requirements

No restriction on foreign currency

Import duty exemptions/ reductions

Corporate income tax exemption for up

to 8 years

50% reduction of corporate income tax

for up to 5 years

Double deduction on utility costs

Deductions for qualifying infrastructure

costs

Land ownership rights

Work permit & visa facilitation

23

BOI’s Attractive Investment Incentives

BOI Support Services Investment Matchmaking Program

1-Stop for visas & work permits:

work permits in 3 hours

Subcontracting Development

Program by BUILD Unit

ASEAN Supporting Industry Database

Interaction with other govt. agencies

on behalf of investors

Country desks

Overseas offices

24

BOI Offers Manifold Support Services

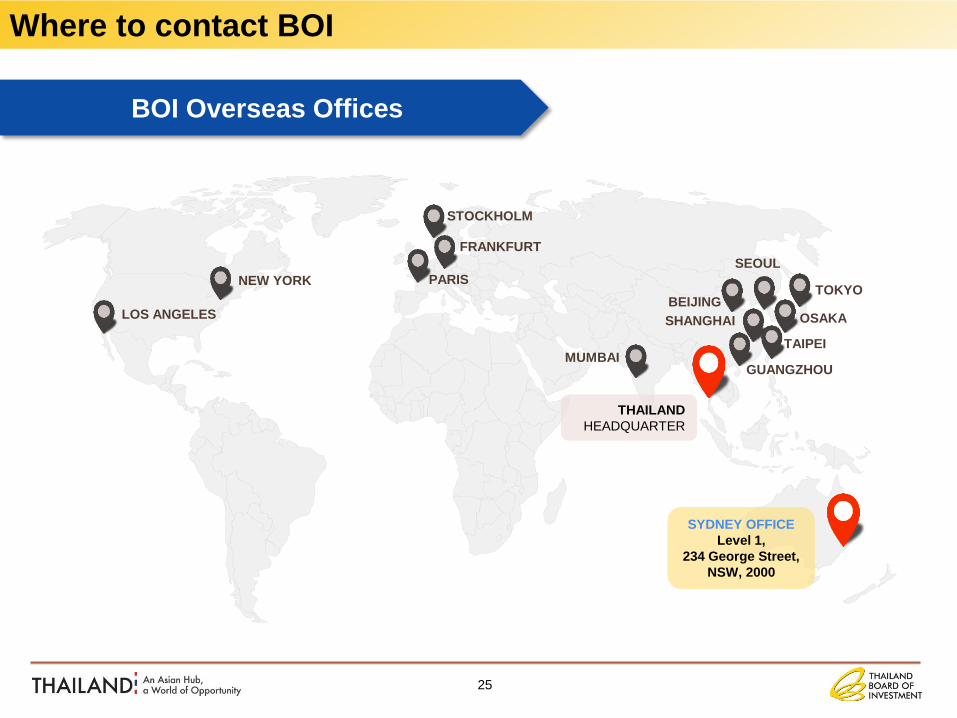

25

THAILAND

HEADQUARTER

BEIJING

FRANKFURT

GUANGZHOU

LOS ANGELES

MUMBAI

NEW YORK

OSAKA

TOKYO PARIS

SEOUL

SHANGHAI

STOCKHOLM

TAIPEI

BOI Overseas Offices

Where to contact BOI

SYDNEY OFFICE

Level 1,

234 George Street,

NSW, 2000

Annex

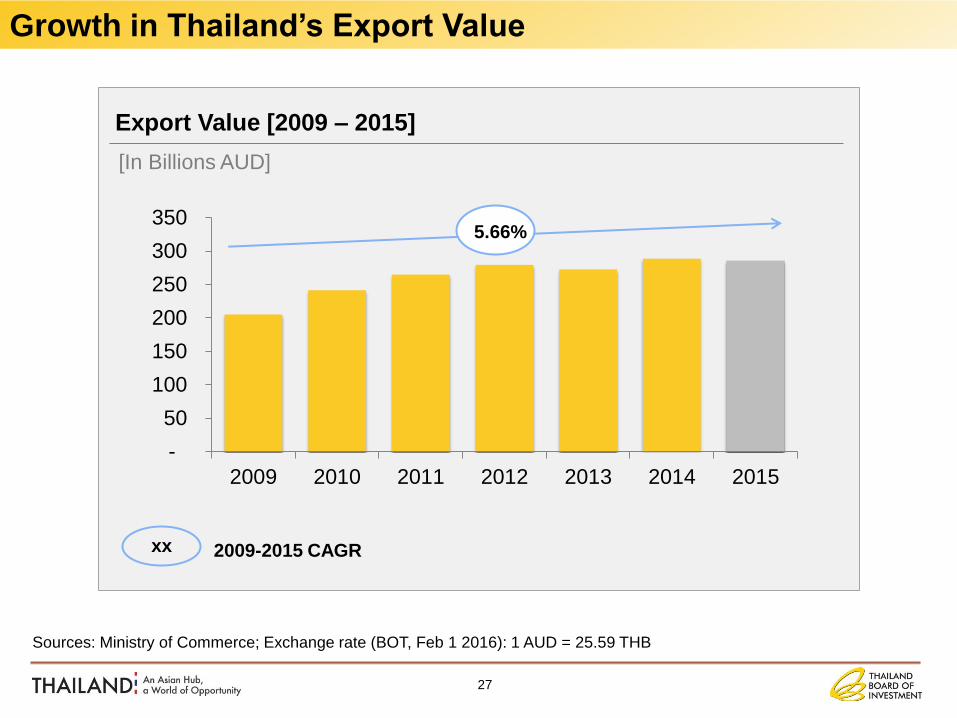

Sources: Ministry of Commerce; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

Export Value [2009 – 2015]

-

50

100

150

200

250

300

350

2009 2010 2011 2012 2013 2014 2015

5.66%

xx 2009-2015 CAGR

27

Growth in Thailand’s Export Value

[In Billions AUD]

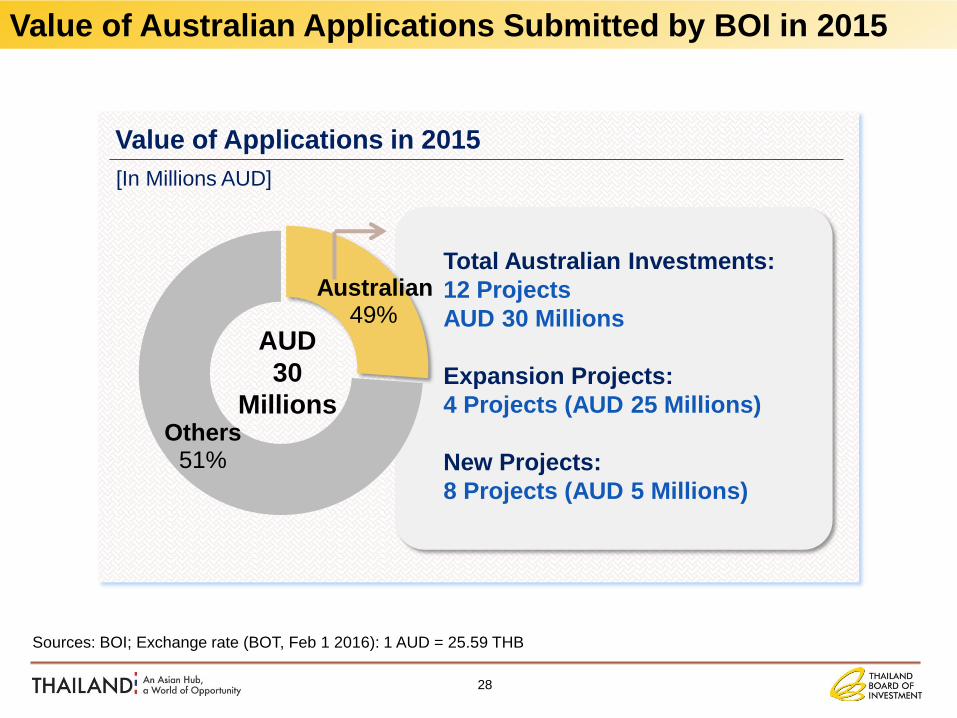

Value of Applications in 2015 [In Millions AUD]

Sources: BOI; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

49%

Others 51%

AUD

30

Millions

28

Value of Australian Applications Submitted by BOI in 2015

Total Australian Investments:

12 Projects

AUD 30 Millions

Expansion Projects:

4 Projects (AUD 25 Millions)

New Projects:

8 Projects (AUD 5 Millions)

Australian

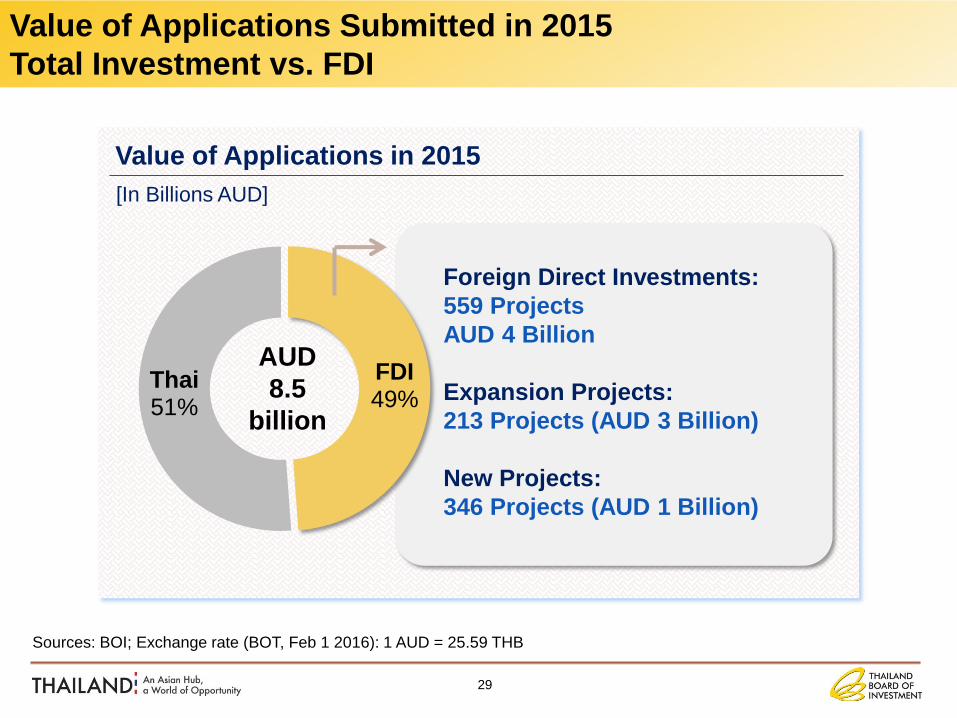

Value of Applications in 2015 [In Billions AUD]

Sources: BOI; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

FDI 49%

Thai 51%

AUD

8.5

billion

29

Value of Applications Submitted in 2015

Total Investment vs. FDI

Foreign Direct Investments:

559 Projects

AUD 4 Billion

Expansion Projects:

213 Projects (AUD 3 Billion)

New Projects:

346 Projects (AUD 1 Billion)

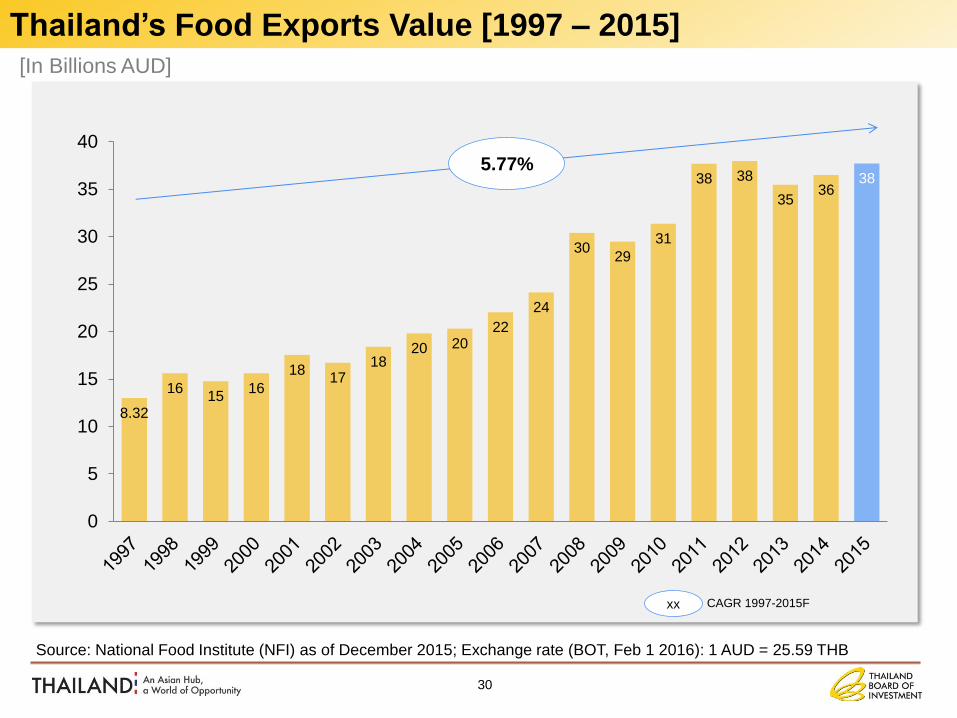

8.32

16 15

16

18 17

18 20 20

22

24

30 29

31

38 38

35 36

38

0

5

10

15

20

25

30

35

40

5.77%

[In Billions AUD]

Source: National Food Institute (NFI) as of December 2015; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

30

CAGR 1997-2015F xx

Thailand’s Food Exports Value [1997 – 2015]

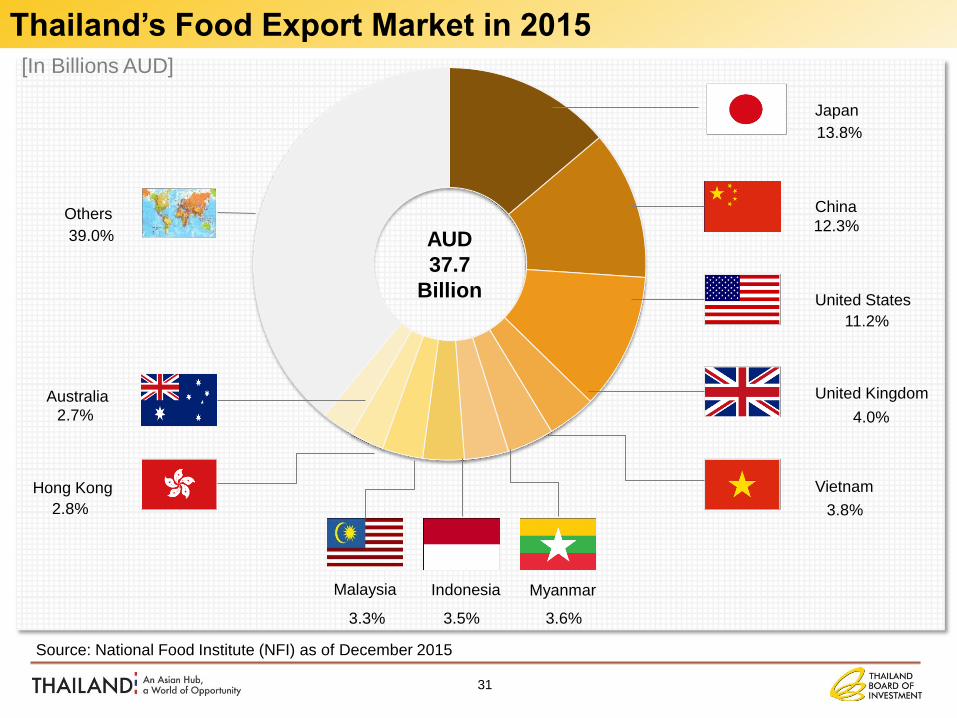

13.8%

12.3%

11.2%

4.0%

3.8% 2.8%

2.7%

39.0%

[In Billions AUD]

Source: National Food Institute (NFI) as of December 2015

31

Indonesia Myanmar Malaysia

Japan

United States

China

United Kingdom

Vietnam

Australia

Hong Kong

Others

AUD

37.7

Billion

3.3% 3.5% 3.6%

Thailand’s Food Export Market in 2015

32

[In Billions AUD]

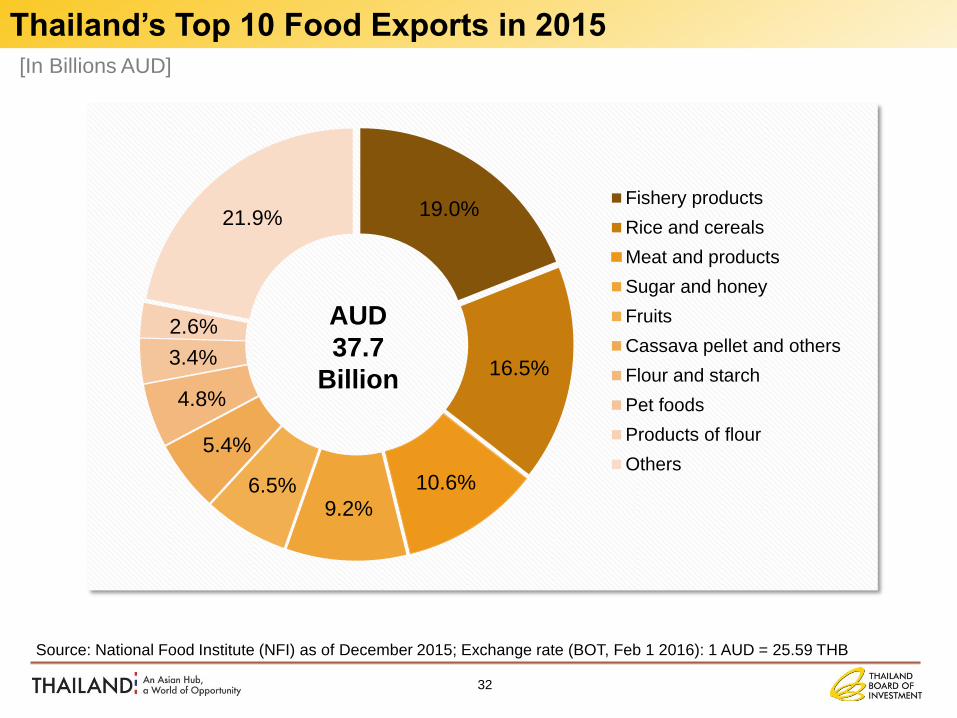

19.0%

16.5%

10.6%

9.2% 6.5%

5.4%

4.8%

3.4%

2.6%

21.9% Fishery products

Rice and cereals

Meat and products

Sugar and honey

Fruits

Cassava pellet and others

Flour and starch

Pet foods

Products of flour

Others

AUD

37.7

Billion

Source: National Food Institute (NFI) as of December 2015; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

Thailand’s Top 10 Food Exports in 2015

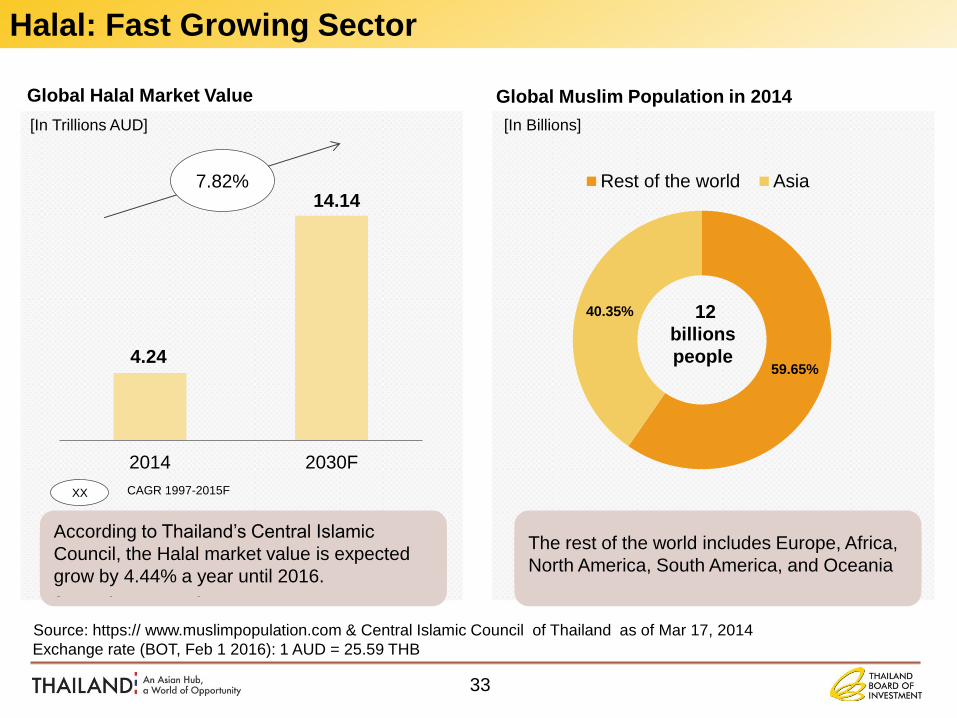

Global Muslim Population in 2014

59.65%

40.35%

Rest of the world Asia

The rest of the world includes Europe, Africa,

North America, South America, and Oceania

12

billions

people

[In Billions]

4.24

14.14

2014 2030F

7.82%

CAGR 1997-2015F

[In Trillions AUD]

According to Thailand’s Central Islamic

Council, the Halal market value is expected

grow by 4.44% a year until 2016.

Source: https:// www.muslimpopulation.com & Central Islamic Council of Thailand as of Mar 17, 2014

Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

Global Halal Market Value

XX

33

The rest of the world includes Europe, Africa,

North America, South America, and Oceania

According to Thailand’s Central Islamic

Council, the Halal market value is expected

grow by 4.44% a year until 2016.

Halal: Fast Growing Sector

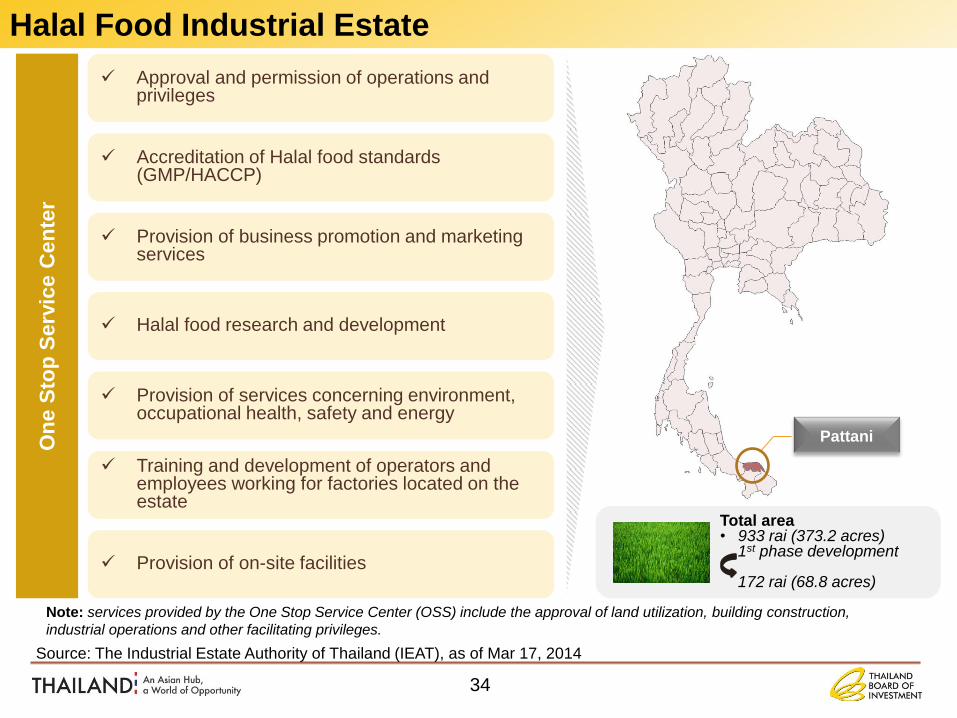

Training and development of operators and employees working for factories located on the estate

Provision of services concerning environment, occupational health, safety and energy

Halal food research and development

Provision of business promotion and marketing services

Accreditation of Halal food standards (GMP/HACCP)

Approval and permission of operations and privileges

Provision of on-site facilities

On

e S

top

Serv

ice C

en

ter

Note: services provided by the One Stop Service Center (OSS) include the approval of land utilization, building construction,

industrial operations and other facilitating privileges.

Source: The Industrial Estate Authority of Thailand (IEAT), as of Mar 17, 2014

Pattani

Total area • 933 rai (373.2 acres) 1st phase development

172 rai (68.8 acres)

34

Halal Food Industrial Estate

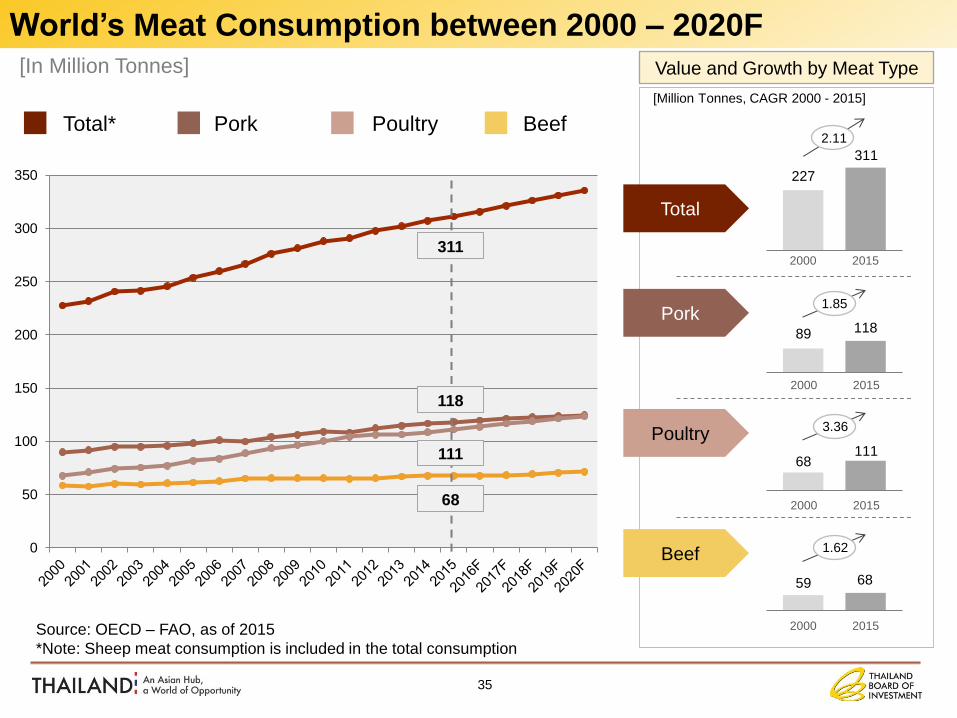

Source: OECD – FAO, as of 2015

*Note: Sheep meat consumption is included in the total consumption

35

Value and Growth by Meat Type

[Million Tonnes, CAGR 2000 - 2015]

[In Million Tonnes]

0

50

100

150

200

250

300

350

311

118

111

68

Beef

Pork

Poultry

Total

68 59

1.62

2000 2015

111 68

3.36

2000 2015

118 89

1.85

2000 2015

311

227

2.11

2000 2015

Total* Beef Poultry Pork

World’s Meat Consumption between 2000 – 2020F

[Kg/person/year]

36

0

10

20

30

40

50

60

70

80

90

100

NorthAmerica

Brazil EuropeanUnion

LatinAmerica

andCaribbean

World BRICS Asia andPacific

Africa

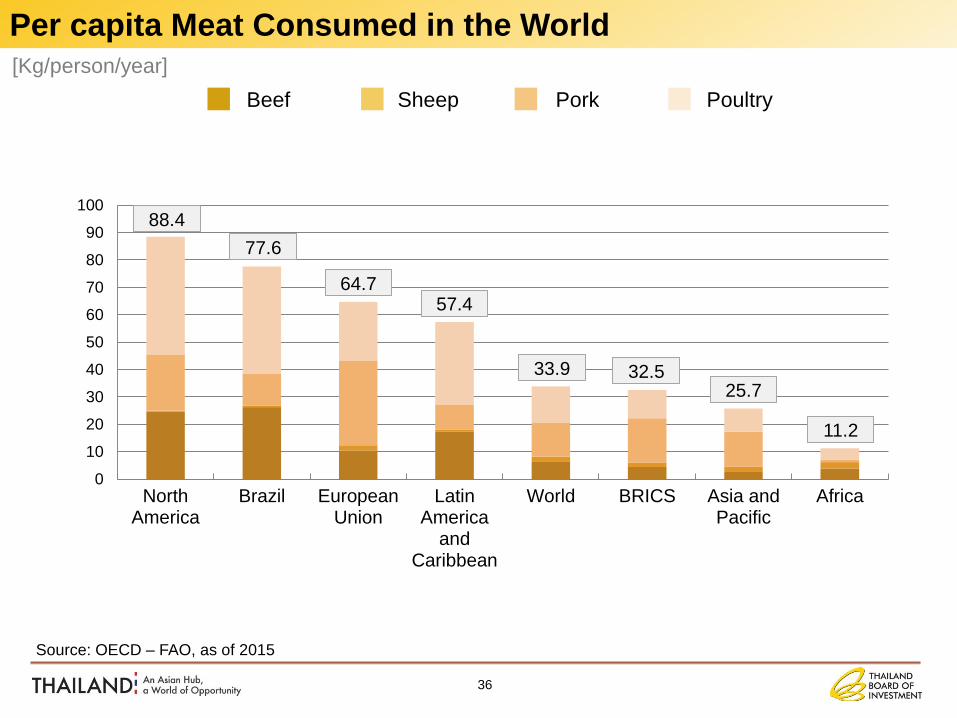

Source: OECD – FAO, as of 2015

88.4

77.6

64.7 57.4

33.9 32.5 25.7

11.2

Beef Poultry Pork Sheep

Per capita Meat Consumed in the World

37

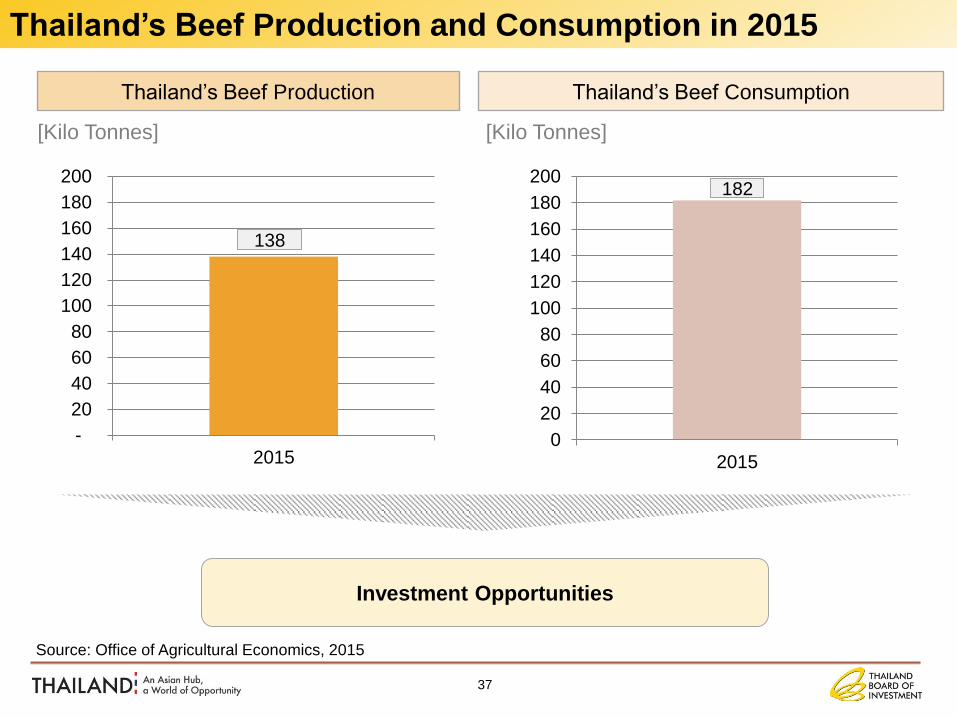

Source: Office of Agricultural Economics, 2015

Thailand’s Beef Production

-

20

40

60

80

100

120

140

160

180

200

2015

138

Thailand’s Beef Consumption

0

20

40

60

80

100

120

140

160

180

200

2015

182

[Kilo Tonnes]

Thailand’s Beef Production and Consumption in 2015

[Kilo Tonnes]

Investment Opportunities

[Million AUD]

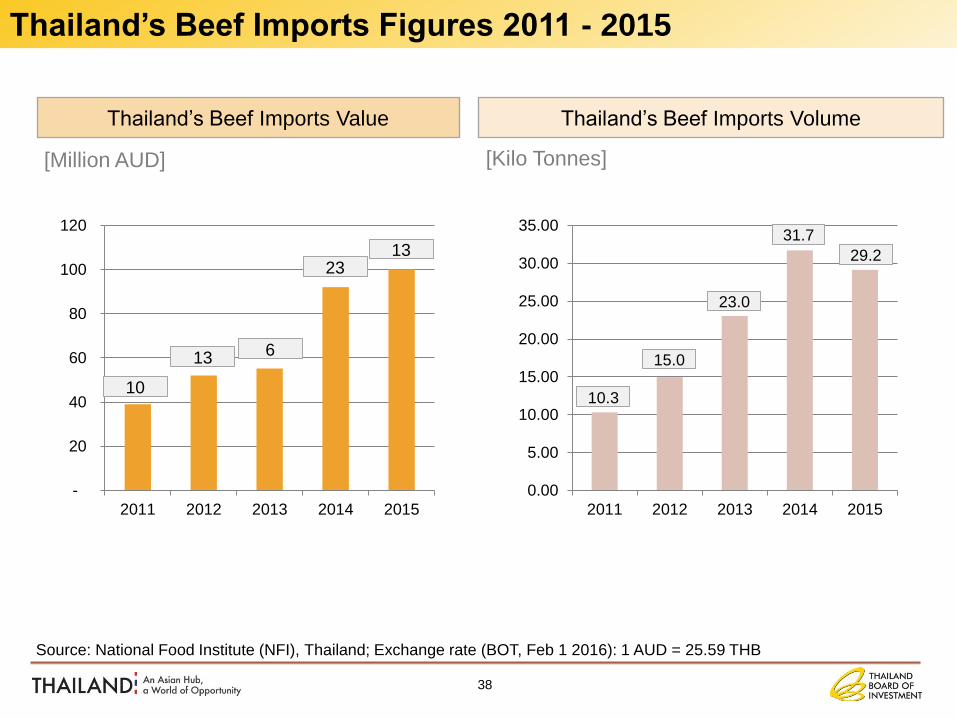

38

Source: National Food Institute (NFI), Thailand; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

Thailand’s Beef Imports Value

-

20

40

60

80

100

120

2011 2012 2013 2014 2015

10

13 6

23 13

Thailand’s Beef Imports Volume

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

2011 2012 2013 2014 2015

10.3

15.0

23.0

31.7

29.2

[Kilo Tonnes]

Thailand’s Beef Imports Figures 2011 - 2015

[Million AUD]

39

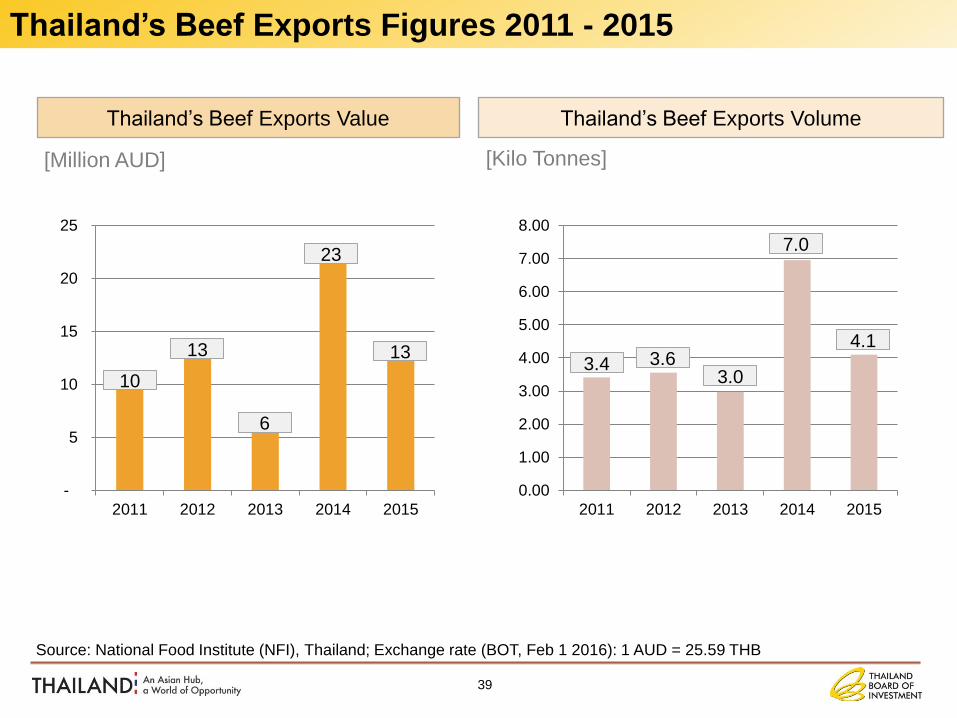

Thailand’s Beef Exports Value

-

5

10

15

20

25

2011 2012 2013 2014 2015

10

13

6

23

13

Thailand’s Beef Exports Volume

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

2011 2012 2013 2014 2015

3.4 3.6 3.0

7.0

4.1

[Kilo Tonnes]

Source: National Food Institute (NFI), Thailand; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

Thailand’s Beef Exports Figures 2011 - 2015

Strengths of Thai Food Industry

Source: National Food Institutes, BOI

Skilled & Hard Working Workforce

Currently, there are 38.47 million workers

with minimum daily wage of THB 300

Abundant Raw Material

>80% of raw materials used by

the food industry are locally

sourced at low prices

Good Quality & Safety

GMP and International Standard

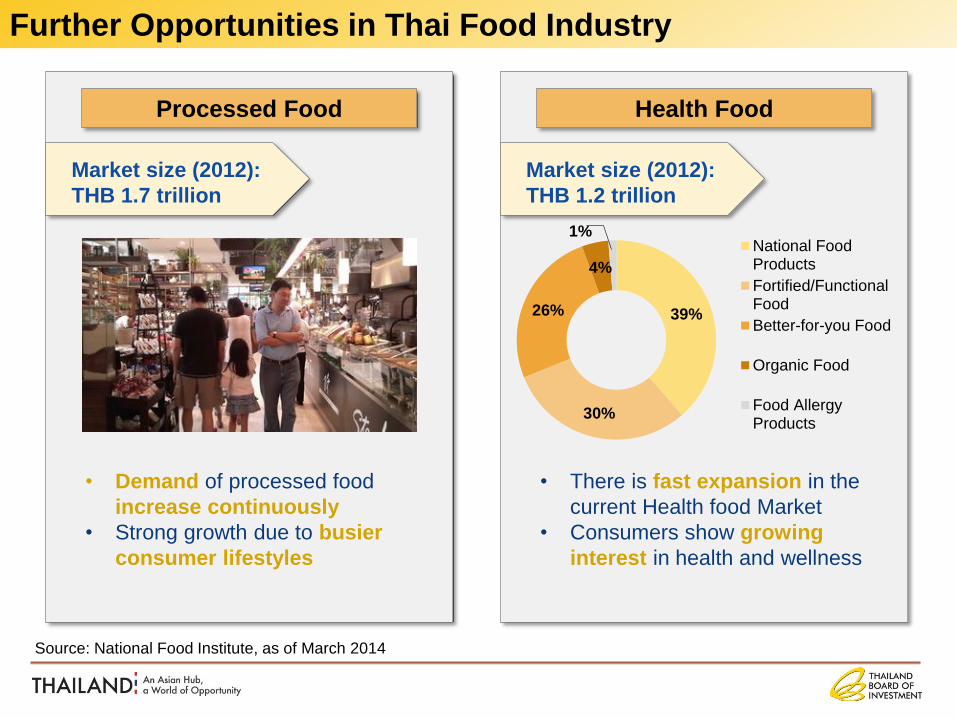

Further Opportunities in Thai Food Industry

Processed Food Health Food

• Demand of processed food

increase continuously

• Strong growth due to busier

consumer lifestyles

Market size (2012):

THB 1.7 trillion

Market size (2012):

THB 1.2 trillion

• There is fast expansion in the

current Health food Market

• Consumers show growing

interest in health and wellness

Source: National Food Institute, as of March 2014

39%

30%

26%

4%

1% National FoodProducts

Fortified/FunctionalFood

Better-for-you Food

Organic Food

Food AllergyProducts

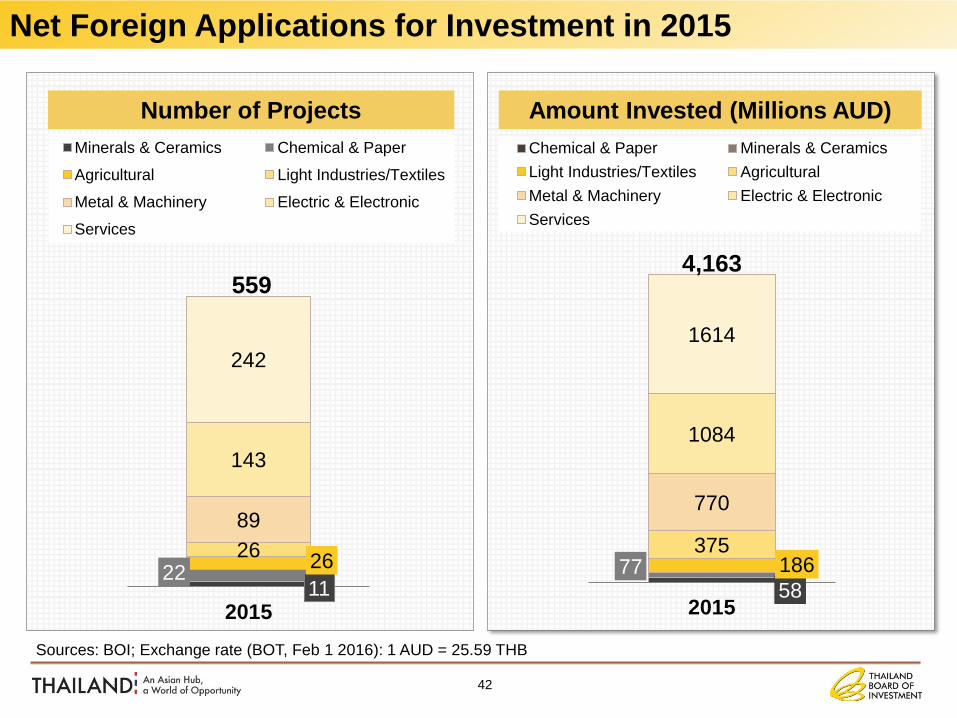

Number of Projects

22 11

26 26

89

143

242

2015

Minerals & Ceramics Chemical & Paper

Agricultural Light Industries/Textiles

Metal & Machinery Electric & Electronic

Services

Amount Invested (Millions AUD)

58 77 186

375

770

1084

1614

2015

Chemical & Paper Minerals & Ceramics

Light Industries/Textiles Agricultural

Metal & Machinery Electric & Electronic

Services

Sources: BOI; Exchange rate (BOT, Feb 1 2016): 1 AUD = 25.59 THB

559 4,163

42

Net Foreign Applications for Investment in 2015

43

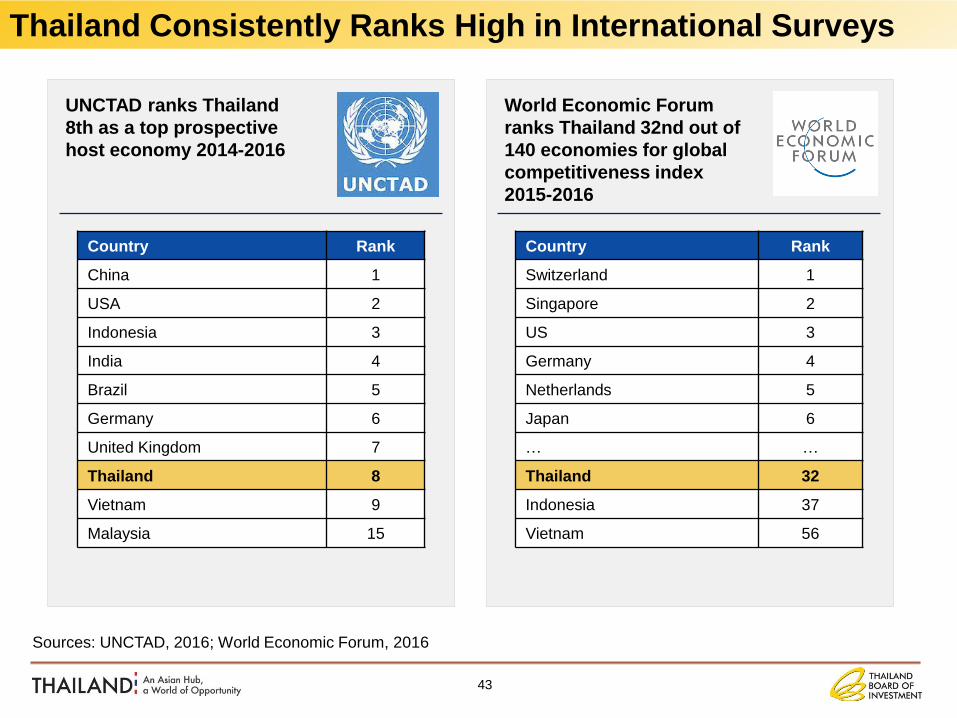

UNCTAD ranks Thailand

8th as a top prospective

host economy 2014-2016

Country Rank

China 1

USA 2

Indonesia 3

India 4

Brazil 5

Germany 6

United Kingdom 7

Thailand 8

Vietnam 9

Malaysia 15

World Economic Forum

ranks Thailand 32nd out of

140 economies for global

competitiveness index

2015-2016

Sources: UNCTAD, 2016; World Economic Forum, 2016

Country Rank

Switzerland 1

Singapore 2

US 3

Germany 4

Netherlands 5

Japan 6

… …

Thailand 32

Indonesia 37

Vietnam 56

Thailand Consistently Ranks High in International Surveys

5th Asia’s Financial Literacy Index MasterCard, 2014

The World’s Most Promising

Emerging Economies Bloomberg Business, 2014 - 2016

11th

Ease of Doing Business among

Emerging Economies in East Asia World Bank, 2016

2nd

Corruption Perception Index Transparency International, 2015 76th

44

Thailand Gains Global Recognition for its Promising

Economy

45

2nd in HDD Exports

Thailand Plays a Vital Role in the Global Supply Chain

6th Rubber Tire Exports

7th Computer Device Exports

12th Automotive Production

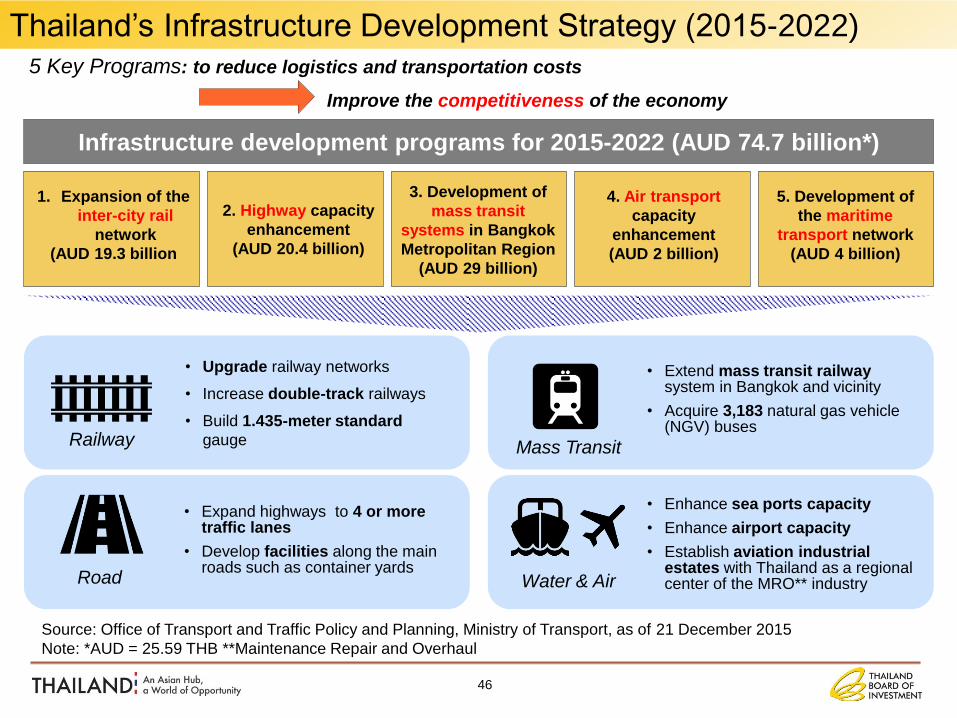

1. Expansion of the

inter-city rail

network

(AUD 19.3 billion

2. Highway capacity

enhancement

(AUD 20.4 billion)

3. Development of

mass transit

systems in Bangkok

Metropolitan Region

(AUD 29 billion)

4. Air transport

capacity

enhancement

(AUD 2 billion)

5. Development of

the maritime

transport network

(AUD 4 billion)

Infrastructure development programs for 2015-2022 (AUD 74.7 billion*)

5 Key Programs: to reduce logistics and transportation costs

Improve the competitiveness of the economy

• Upgrade railway networks

• Increase double-track railways

• Build 1.435-meter standard

gauge

• Expand highways to 4 or more traffic lanes

• Develop facilities along the main roads such as container yards

• Extend mass transit railway system in Bangkok and vicinity

• Acquire 3,183 natural gas vehicle (NGV) buses

• Enhance sea ports capacity

• Enhance airport capacity

• Establish aviation industrial estates with Thailand as a regional center of the MRO** industry

Railway

Road

Mass Transit

Water & Air

Source: Office of Transport and Traffic Policy and Planning, Ministry of Transport, as of 21 December 2015

Note: *AUD = 25.59 THB **Maintenance Repair and Overhaul

Thailand’s Infrastructure Development Strategy (2015-2022)

46

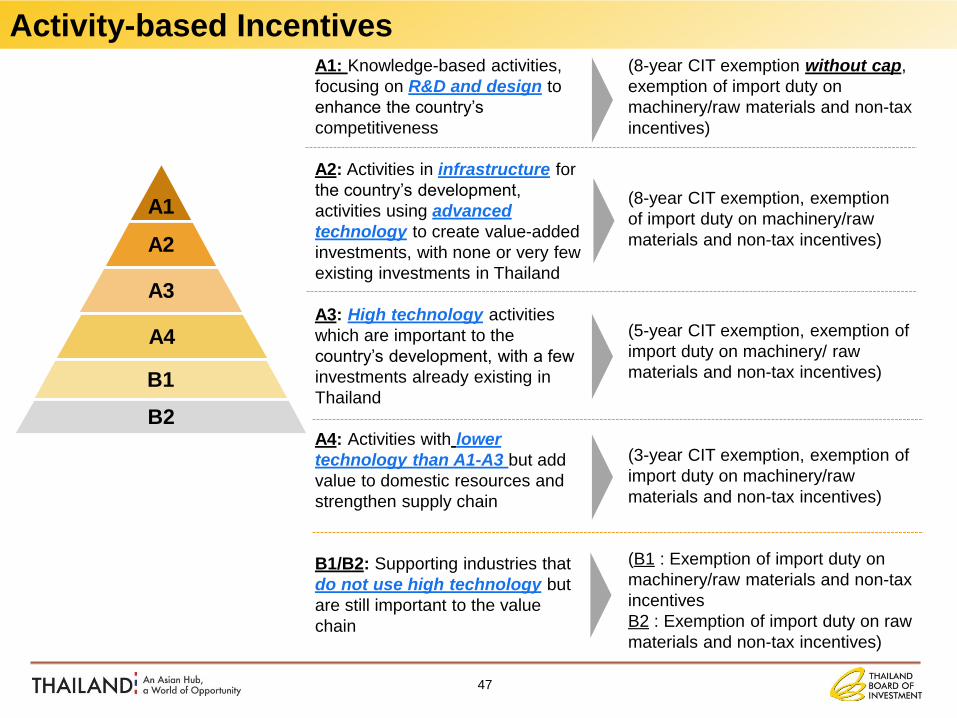

A1

A2

A3

A4

B1

B2

A1: Knowledge-based activities,

focusing on R&D and design to

enhance the country’s

competitiveness

A2: Activities in infrastructure for

the country’s development,

activities using advanced

technology to create value-added

investments, with none or very few

existing investments in Thailand

A3: High technology activities

which are important to the

country’s development, with a few

investments already existing in

Thailand

A4: Activities with lower

technology than A1-A3 but add

value to domestic resources and

strengthen supply chain

B1/B2: Supporting industries that

do not use high technology but

are still important to the value

chain

(8-year CIT exemption without cap,

exemption of import duty on

machinery/raw materials and non-tax

incentives)

(8-year CIT exemption, exemption

of import duty on machinery/raw

materials and non-tax incentives)

(5-year CIT exemption, exemption of

import duty on machinery/ raw

materials and non-tax incentives)

(3-year CIT exemption, exemption of

import duty on machinery/raw

materials and non-tax incentives)

(B1 : Exemption of import duty on

machinery/raw materials and non-tax

incentives

B2 : Exemption of import duty on raw

materials and non-tax incentives)

47

Activity-based Incentives

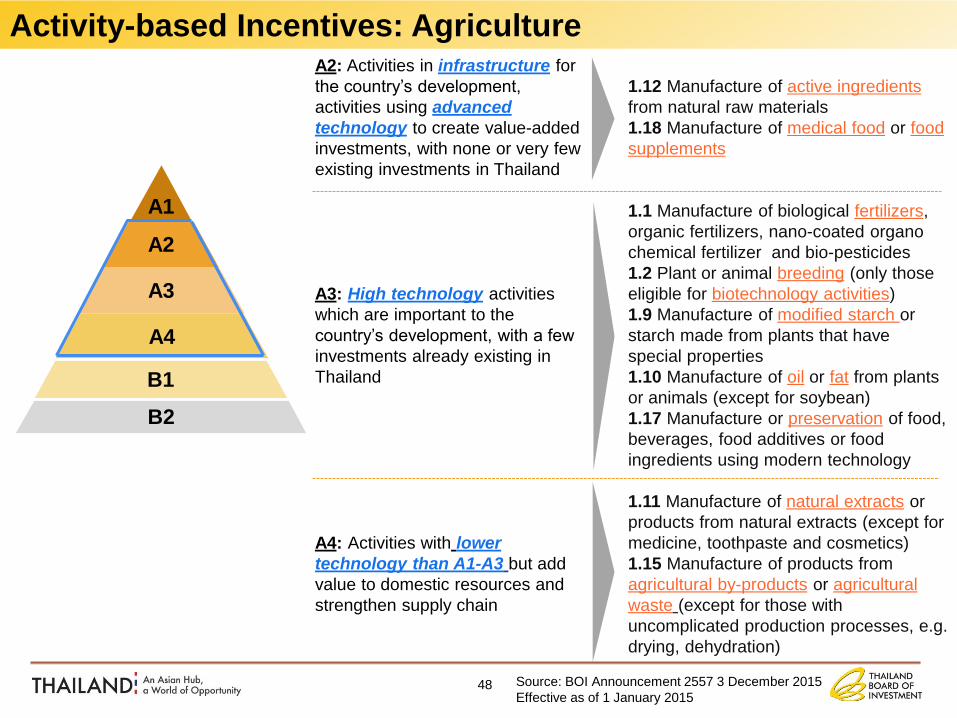

A1

A2

A3

A4

B1

B2

A2: Activities in infrastructure for

the country’s development,

activities using advanced

technology to create value-added

investments, with none or very few

existing investments in Thailand

A3: High technology activities

which are important to the

country’s development, with a few

investments already existing in

Thailand

A4: Activities with lower

technology than A1-A3 but add

value to domestic resources and

strengthen supply chain

1.12 Manufacture of active ingredients

from natural raw materials

1.18 Manufacture of medical food or food

supplements

1.1 Manufacture of biological fertilizers,

organic fertilizers, nano-coated organo

chemical fertilizer and bio-pesticides

1.2 Plant or animal breeding (only those

eligible for biotechnology activities)

1.9 Manufacture of modified starch or

starch made from plants that have

special properties

1.10 Manufacture of oil or fat from plants

or animals (except for soybean)

1.17 Manufacture or preservation of food,

beverages, food additives or food

ingredients using modern technology

1.11 Manufacture of natural extracts or

products from natural extracts (except for

medicine, toothpaste and cosmetics)

1.15 Manufacture of products from

agricultural by-products or agricultural

waste (except for those with

uncomplicated production processes, e.g.

drying, dehydration)

Source: BOI Announcement 2557 3 December 2015

Effective as of 1 January 2015

Activity-based Incentives: Agriculture

48