introduction to hedge fund data

TRANSCRIPT

Contents

• Data evidence: MBA/COO/CFO viewpoint

• Product: (private) investment fund

– Alternative investment strategies: reference, business and market data; regulatory data

– Threats: oversized, gentrification, smart Beta

• Legal: Regulated “alternative” investments

– “Ex-offshore“; market size, growth, distribution

• Business: Entrepreneurial

– Mostly micro, private (craftsman) businesses

2010s

• Financial crisis and “repression”

– Hedge funds as the investment banking career

exit strategy; Volcker Rule s. 619 Dodd-

Frank’s Act proprietary trading ban (Apr 2014)

– An ex-employee becomes an entrepreneur -

funding the venture and raising assets

– Regulation, business costs, clearing fees etc

increasing; less start-up and early stage

investing

Growth of Alternatives

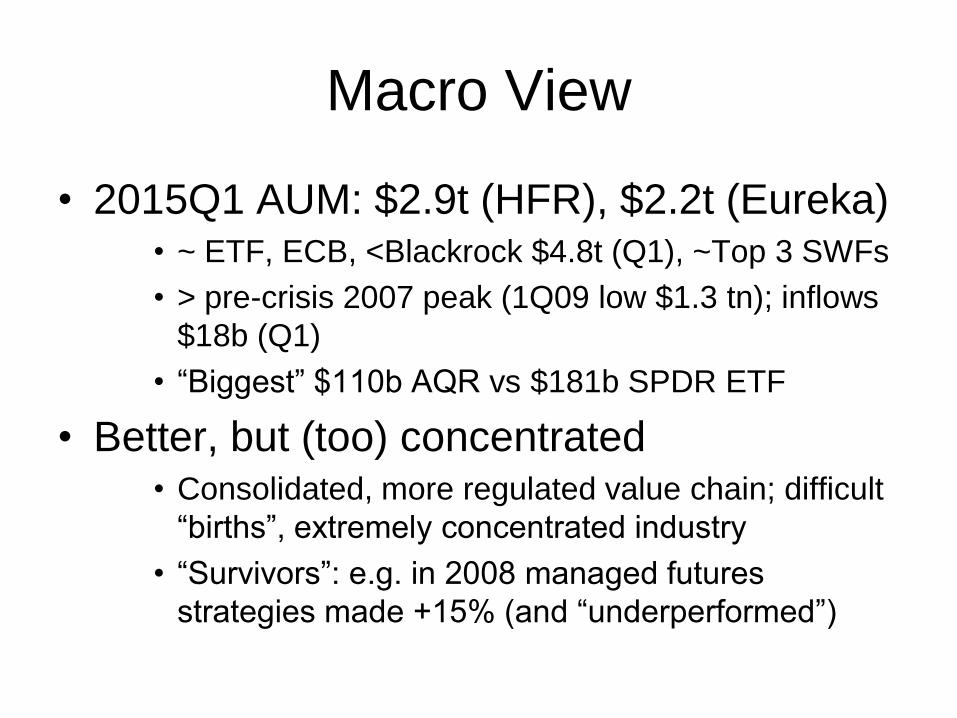

Macro View

• 2015Q1 AUM: $2.9t (HFR), $2.2t (Eureka) • ~ ETF, ECB, <Blackrock $4.8t (Q1), ~Top 3 SWFs

• > pre-crisis 2007 peak (1Q09 low $1.3 tn); inflows

$18b (Q1)

• “Biggest” $110b AQR vs $181b SPDR ETF

• Better, but (too) concentrated • Consolidated, more regulated value chain; difficult

“births”, extremely concentrated industry

• “Survivors”: e.g. in 2008 managed futures

strategies made +15% (and “underperformed”)

Flows

• Note lagged NAV reporting: “based on 41% reported Mar 2015 fund

returns as at 15 April 2015”

2015 Outlook (Barclays)

• “AUM doubled since 2008: ~90% of the

asset growth attributable to performance,

not inflows”.

• While the largest funds continue to receive

a majority of the flows, in recent years the

proportion of flows they receive has been

declining (more are now hard/soft-closed).

• Q: Scalability? Aging?

Flows (Gini)

• Jones (2015), HFR (20 Apr 15)

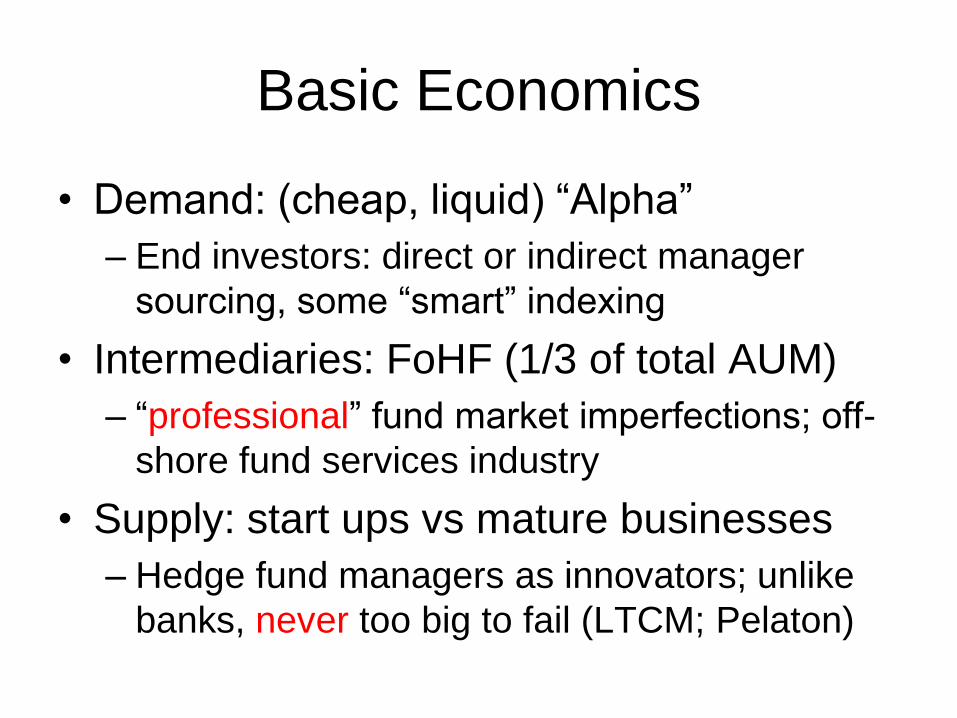

Basic Economics

• Demand: (cheap, liquid) “Alpha”

– End investors: direct or indirect manager

sourcing, some “smart” indexing

• Intermediaries: FoHF (1/3 of total AUM)

– “professional” fund market imperfections; off-

shore fund services industry

• Supply: start ups vs mature businesses

– Hedge fund managers as innovators; unlike

banks, never too big to fail (LTCM; Pelaton)

Demand

• Institutional investors - “unconstrained”

– Pension funds (CALPERS exit in Sep 2014)

– Strategic asset allocation: DGF

• %alternatives (PE, RE); % HFs; %”strategies”

• “Private” (HNW) vs retail (UCITS)

– “An investor domiciled in X buys units of fund domiciled in jurisdiction Y”

– GACTA, KYC, AML client classification

Supply: Fund Manager

• Approved personnel in the regulated entity • On-shore, taxed: (UK: FCA) LLP (private LLP

agreements); staff, systems, service contracts

• Initially, cheaper Off-shore Ltd, manages off-shore

fund: corporate “substance” and governance, off-

shore authorised (eg. Guernsey FSC)

• Start-up, not a listed company • True Hedge Fund: Manager(s) = Founders-

owners; micro-enterprise (think credit score); cash-

flow sensitive; taxable; Careful structuring

Legals

• Authorised People in Partnership • LLP agreement: equity%’s; control and economics;

designated partners(not salaried)

• Fund management company • Articles of incorporation: fund governance issues

• Investment management agreement with the fund

• Fund: (private placing) memorandum • Subscription forms (often “non US”); governance

• Service agreements/contracts

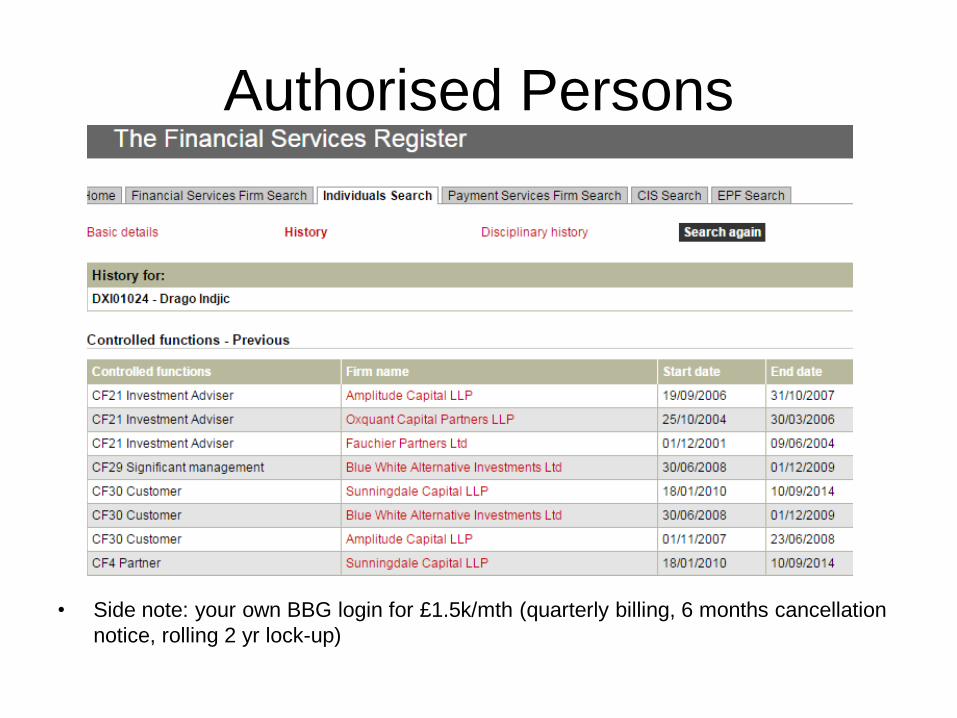

Authorised Persons

• Side note: your own BBG login for £1.5k/mth (quarterly billing, 6 months cancellation

notice, rolling 2 yr lock-up)

Service Agreements

• Counterparties

– Prime broker: Global investment bank(s): (+) securities custody, lending and financing (-) Most senior creditor: re-hypothecation (Lehman; MF Global), cash (Sentinel)

– Fund Administrator (NAV Calculator, registrar and transfer), depositary bank etc

• Legal, auditor(s), (off-shore) directors, secretarial services, compliance, 3rd party marketing, IT, office … not in Mayfair?

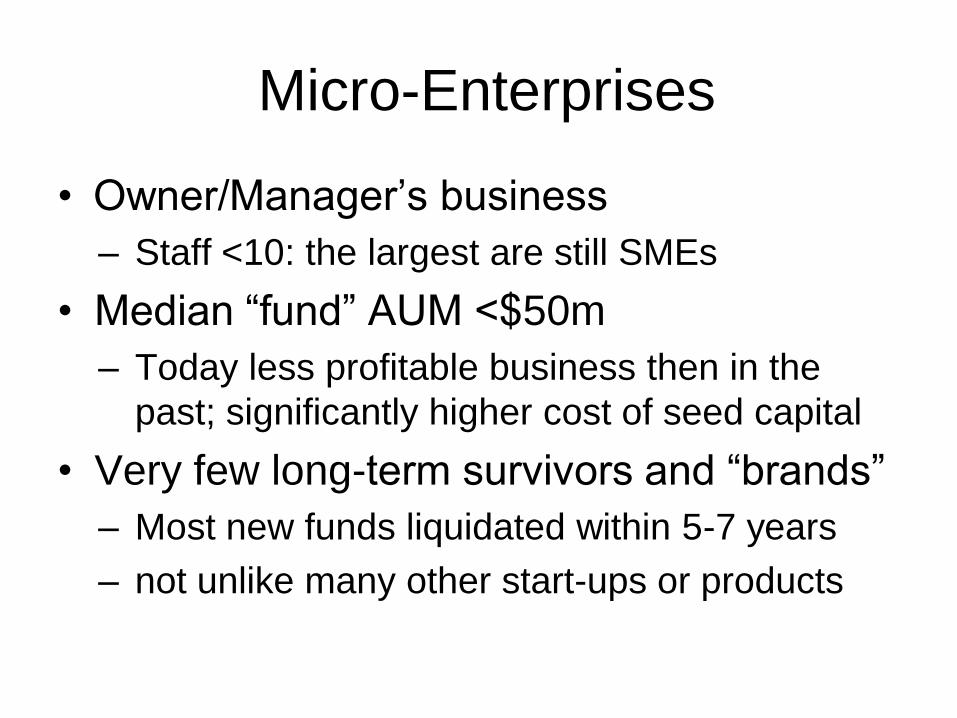

Micro-Enterprises

• Owner/Manager’s business

– Staff <10: the largest are still SMEs

• Median “fund” AUM <$50m

– Today less profitable business then in the

past; significantly higher cost of seed capital

• Very few long-term survivors and “brands”

– Most new funds liquidated within 5-7 years

– not unlike many other start-ups or products

Performance Data

• Voluntary disclosure • HFR, Lipper, Morningstar: not prices (NAVs) but

lagged, non-verified performance estimates for

many fund share classes and fund “boiler plates”

• Contact “catalogues” of 1,000+ management

companies by market research specialists

• No standard identifiers • Self-selection and survivorship bias: the largest,

the smallest and “defunct” funds excluded

• No CUSIPs/LEI. Bloomberg etc blank; data is not

for sale by fund administrators or brokers

Fund Labeling

• What exactly is an investment strategy?

– 1980s descriptive taxonomies: no standards

beyond labelling: elicited by interviews and

case studies; exposures vary across assets

universe and over time

• Lack of verification

– Transparency: necessary, not sufficient

criteria; Silver bullet: pre-trade controls

– Danger: overpaying for Beta-like service

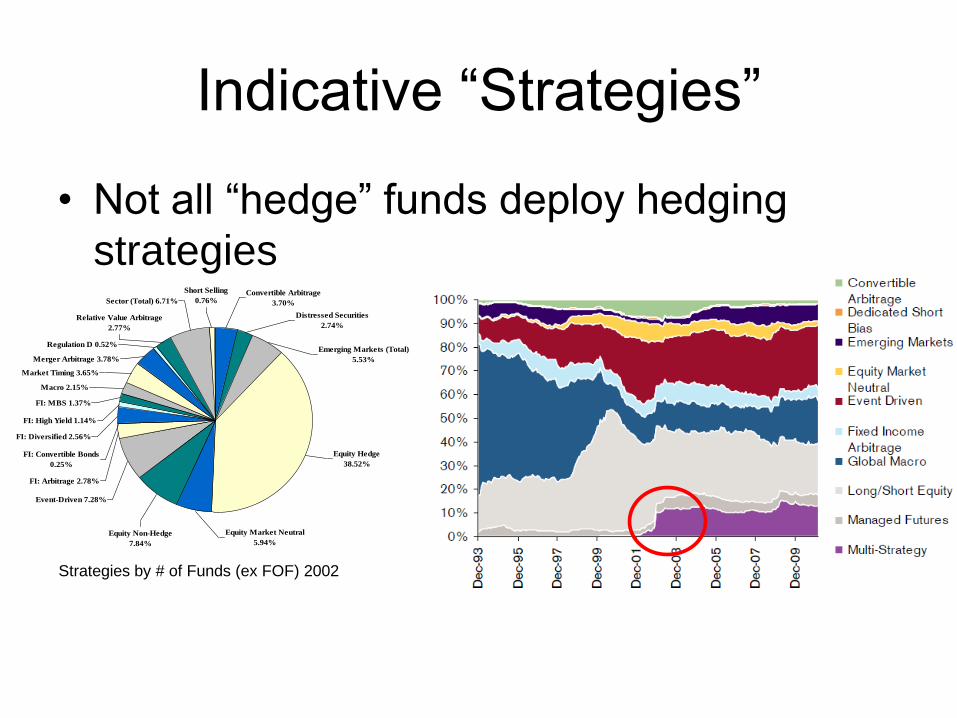

Indicative “Strategies”

• Not all “hedge” funds deploy hedging

strategies

Equity Hedge

38.52%

Emerging Markets (Total)

5.53%

Distressed Securities

2.74%

Equity Market Neutral

5.94%

Equity Non-Hedge

7.84%

Event-Driven 7.28%

FI: Arbitrage 2.78%

FI: Convertible Bonds

0.25%

FI: Diversified 2.56%

FI: High Yield 1.14%

FI: MBS 1.37%

Convertible Arbitrage

3.70%

Short Selling

0.76%Sector (Total) 6.71%

Macro 2.15%

Market Timing 3.65%

Merger Arbitrage 3.78%

Regulation D 0.52%

Relative Value Arbitrage

2.77%

Strategies by # of Funds (ex FOF) 2002

What about index(es)?

• Plus by region, FX hedge etc, but is it investable?

Creating HF Exposure

• Thriving • Direct, but advised: outsourced due diligence, non-

discretionary

• Segregated Managed Accounts and Platforms

• 2010s: Retail products by large funds • Liquid Alternatives: UCITS and index products

• Extinct and endangered • FoHF: full outsourcing - consultant’s stronghold

• Disappeared: Structured (capital protected)

Alpha Needle - Rotten Apple?

• Less systemic risk concern today

Investor’s Risk/Reward

• Evaluate Total Hedge Fund Risk

– Mostly business risk: contractual, SME, “key man” (“exit” - no EV), equity financed

– Lesser portfolio and market risk (“hedged”)

• Benefits

– Unique profiles (NAV in gold or oil): not dependant on underlying assets (Betas)

– Negotiable; business co-ownership (PE-like);

– Opportunity to price “Alpha”

Portfolio Construction

• “Strategy allocation” (%weight)

• Fund “selection” (often binary: yes or no)

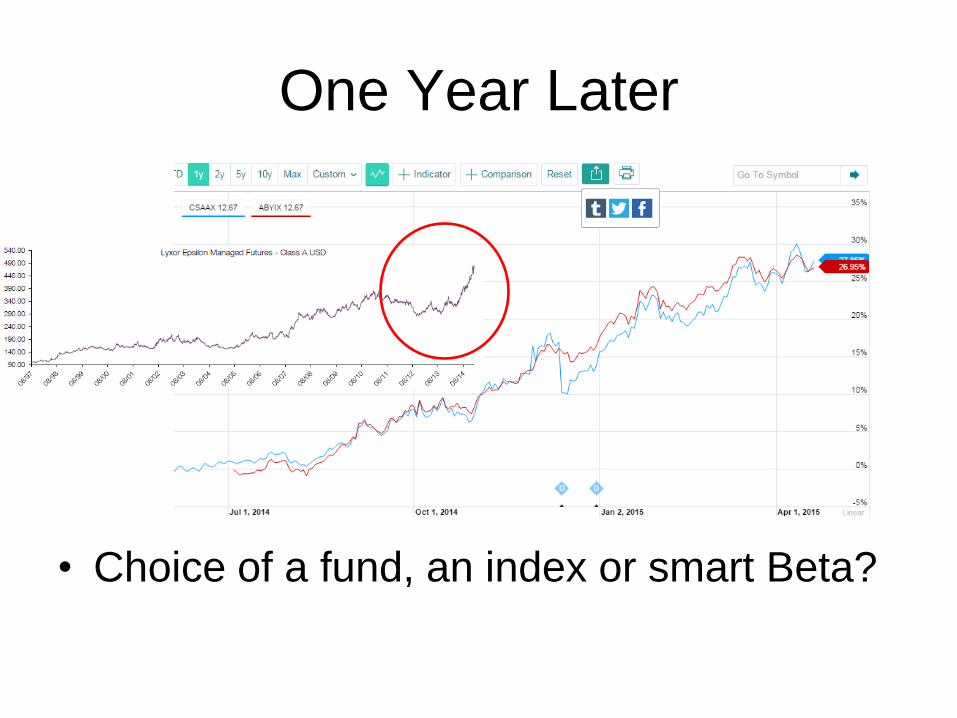

One Year Later

• Choice of a fund, an index or smart Beta?

“Stars” and “Awards”

• Hedge Fund Review Americas 2014: NYC, July 24th

”Hedge funds reporting to the BarclayHedge database are

automatically entered in the performance categories. All other

managers are encouraged to download and complete an entry form

... (and) also invited to enter the qualitative categories, which reward

achievements in product development, innovation and client service”

“This year the awards also recognise best bespoke FoHF provider

and best advisory team from a fund of funds” .....

“The hedge fund investment process relies on more than just

numbers and the evaluation process recognises this” .....

Business Data

• Mostly private, lagged and age fast

– Static reference data

• Fund offering memorandum, counterparties

– Business

• Due diligence: staffing, references, accounts

– Portfolio

• Classic: investor letters, weekly NAVs, portfolio

exposure and holdings: “Opera” vs AIFMD

standard; real-time: HedgeMark

Transparency

• Full position transparency (to institutions)

• Regulatory: AIFMD, funding liquidity and leverage etc

Incentives

• Morningstar (2015): “It turns out that manager investment does have predictive power”

• Barclays (2015): “Hurdle rate adoption has remained low at ~15%; investors have preferred up-front discounts on management fees

• Start-ups ... but gentrification – “The top 50 HF firms have been in business for

an average of 22 years. The average age of the founders of the top 50 funds is 54”

Births and Deaths

• HFR (March 20, 2015) - The number of new hedge fund

launches fell, the 3rd consecutive year of decline, while

liquidations saw their first drop since 2010. Hedge fund

launches totalled 1,040 for 2014, a decline of 20 funds

from the 1,060 funds launched in 2013. While launches

have trended in a narrow range, they remain well below

the peak of 2,073 funds launched in 2005.

• Tyranny of TER:

– AUM <$100m for a long time (e.g. Cumulus)

– “Soft” performance/flows/age factors

Start-Up Investment Puzzle

• Minimum required AUM to consider a fund

• “high %AUM is the partner’s capital”, “stamp of

approval from a respected seeder”

• Average investment size

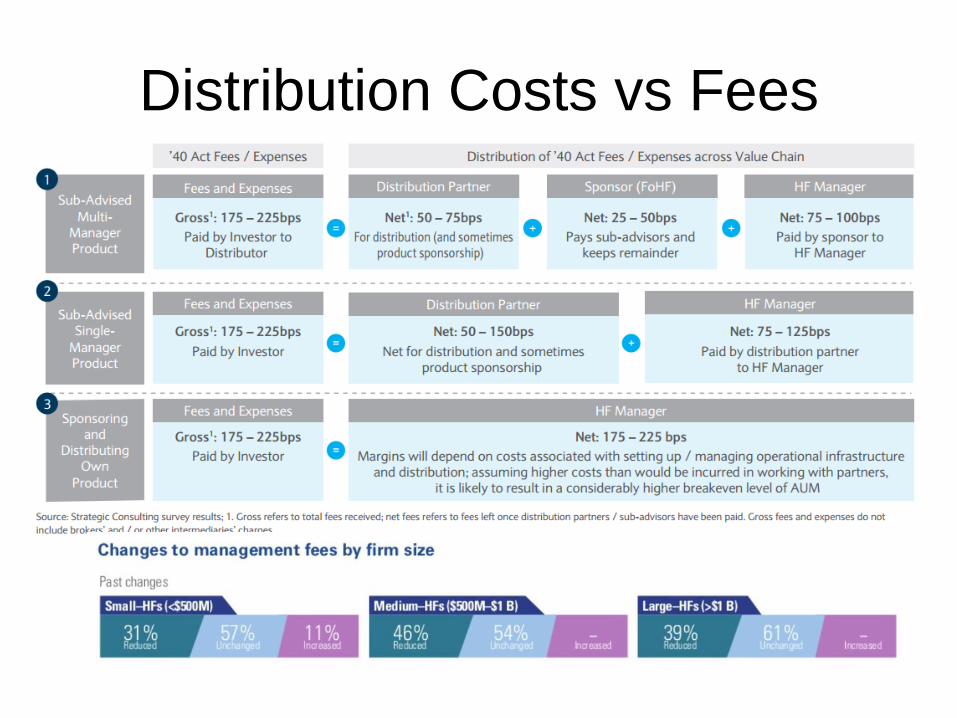

Distribution Costs vs Fees

Future

• Better focused role in (DGF) portfolios

• “Liquid alternatives”

– 10% of hedge funds are UCITS; 1% of US

Mutual Funds are “Alternative”

– Unlike traditional hedge funds, daily or weekly

redemption. Deutsche Bank (Sep 14): est.

$49b inflows (44% jump) the fastest growing

part of the asset management industry

Future

• Some UK data: FCA: 450 AIFM firms; AUM Top 49: $480b.

Conclusions

• Global political economy

– ZIRP, deflationary, “re-regulated”, “de-risking”

• Innovation

– investment contracting; passive / active mix

– Aligned interests and governance: separation of funds and managers (e.g. fund investors’ right to claim management companies’ residual earnings or “profits”)

• Risks: hedgies demographic pyramid

References

• HFR (2015) Global Hedge Fund Industry Report, HFR Webcast ,

Apr 21, 2015; http://www.thehedgefundjournal.com/node/10031

• Jones, M. (2015) http://www.aboutmjones.com/blog/2015/3/19/fun-

with-dots-visualizing-bifucation-in-the-hedge-fund-industry

• Barclays (2015) Global Hedge Fund Industry Trends and Allocation

Outlook

• Morningstar (2015) “Why You Should Invest With Managers Who

Eat Their Own Cooking”; SEC Statement of Additional Information,

Fund Spy tool, Spy Selector, on mfi.morningstar.com.

• CIO (2015) The Hierarchy of Alpha, March 19, 2015

• ESMA (2015) http://www.esma.europa.eu/system/files/2015-

630_qa_aifmd_march_update.pdf

CA

#1

00

03

7

• Deep Asset Management, M&A, Risk Control and Market experience

Chief Executive Officer - Jon Oyvind Eriksen

─ 15 years of international CEO experience. Executed several M&A opportunities.

Chief Risk officer - Sanjay Agarwal

─ 7 years of International and emerging markets M&A risk control experience with 8 years of corporate treasury experience. Chartered Certified Accountant in UK and India.

Chief Financial Officer - Livia Popa

─ 7 years of Hedge Fund financial controller experience. Specialist in acquisition analysis.

Client Relationship Manager - Mike Huang

─ Product specialist with Halbis, a leading global asset management company. 3 years of sales and marketing experience in structured products with HSBC.

Head of Research - Stefan Slowinski

─ 8 years Equity Research experience with SG. 2 years M&A experience at Salomon Brothers.

Head of Trading - Jun Lin

─ Futures trading specialist, 5 years experience of trading experience.

36

The Alpha Team – Absolute Return M&A specialists

Group 5

Jun Lin

05/05/2009

Sanjay Agarwal

Jon Oyvind Eriksen

Livia Popa

Mike Huang

Stefan Slowinski