international bank for reconstruction...

TRANSCRIPT

R E S T R I C T E D

Report No. To-298b

This report was prepared for use within the Bank. It may not be publishednor may it be quoted as representing the Bank's views. The Bank accepts noresponsibility for the accuracy or completeness of the contents of the report.

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

APPRAISAL OF THE ANGAT HYDROELECTRIC PROJECT

THE NATIONAL POWER CORPORATION

PHILIPPINES

October 5, 1961

Department of Technical Operations

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

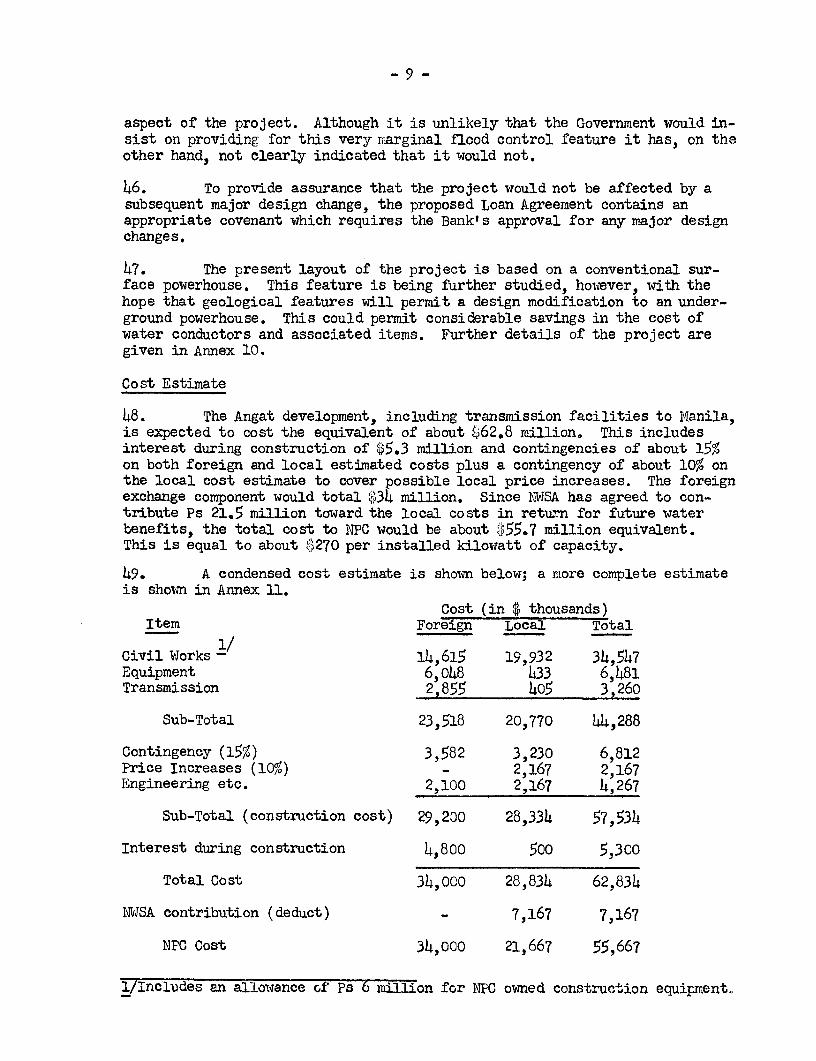

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ASSUMED CURRENCY EQUIVALENTS

1 Us $ = 3 Pesos (Ps)1 Peso = 33-1/3 US cents1 million Pesos = 333,333-1/3 US $

APPRAISAL OF THE ANGAT HYDROELECTRIC PROJECT

THE NATIONAL POWER CORPORATION

PHILIPPINES

TABLE OF CONTENTS

Page No.

SU4ARY i

I. INTRODUCTION 1

II. THE BORROWER 1Existing Facilities 2

III. THE POWER 2MARKET 3Luzon Grid 3The EMindanao Island System 4Other Operations 4

IV. THE NPC EXPANSION PROGRAM 4Luzon Grid Expansion 5The Mindanao System Expansion 6

V. THE SALES FORECAST 7Luzon Grid 7The Mindanao Island System 8

VI. THE PROJECT 8The Angat Hydroelectric Development 8Cost Estimate 9Rate of Expenditure and Method of Finance 10Engineering and Supervision of Construction 10Schedule of Construction 11

VII. JUSTIFICATION OF THE PROJECT 11

VIII. FINANCIAL ASPECTS 11present Finanpial Position 13Earnings Record 1Rates 14Financing Plan 15Estimated Future Financial Position 16Debt Limitation Covenant 17

IX. CONCLUSIONS 18

TABLE OF CONTEMTS

Page 2

ANNEXES

1. Xeralco Past and Forecast Sales

2. Provincial Past and Forecast Sales

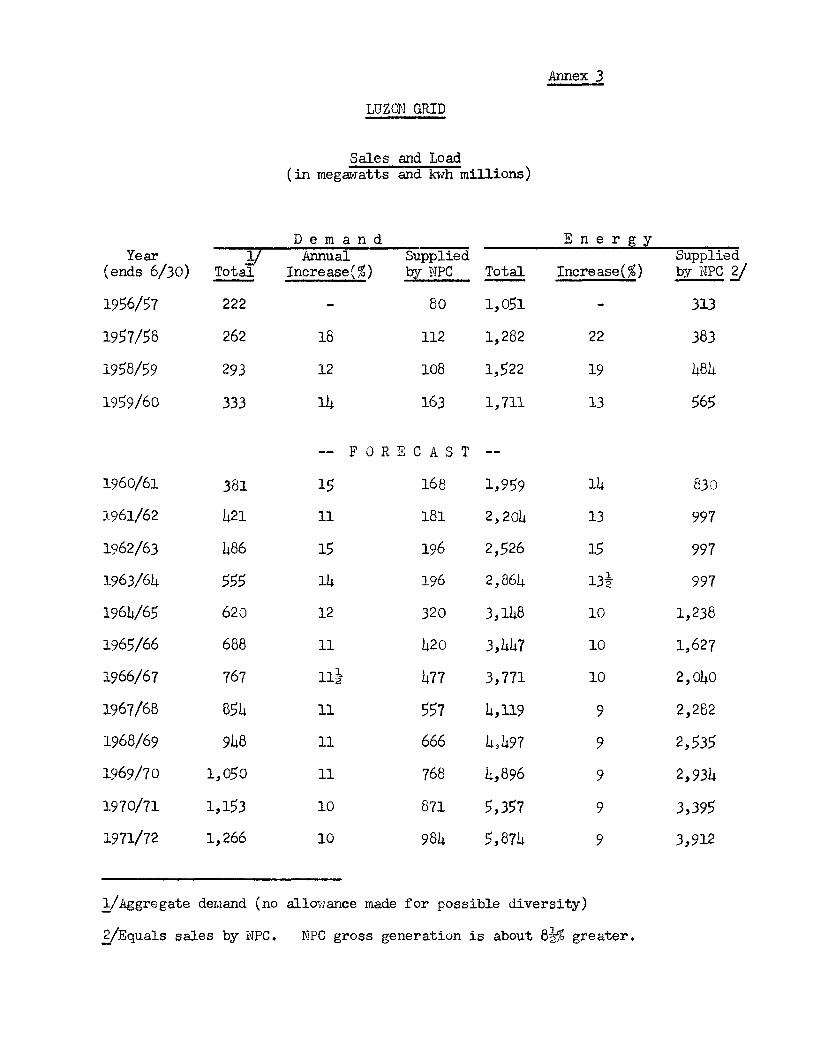

3. Luzon Grid Past and Forecast Sales

4. iIindanao (Agus) Grid Past and Forecast Sales

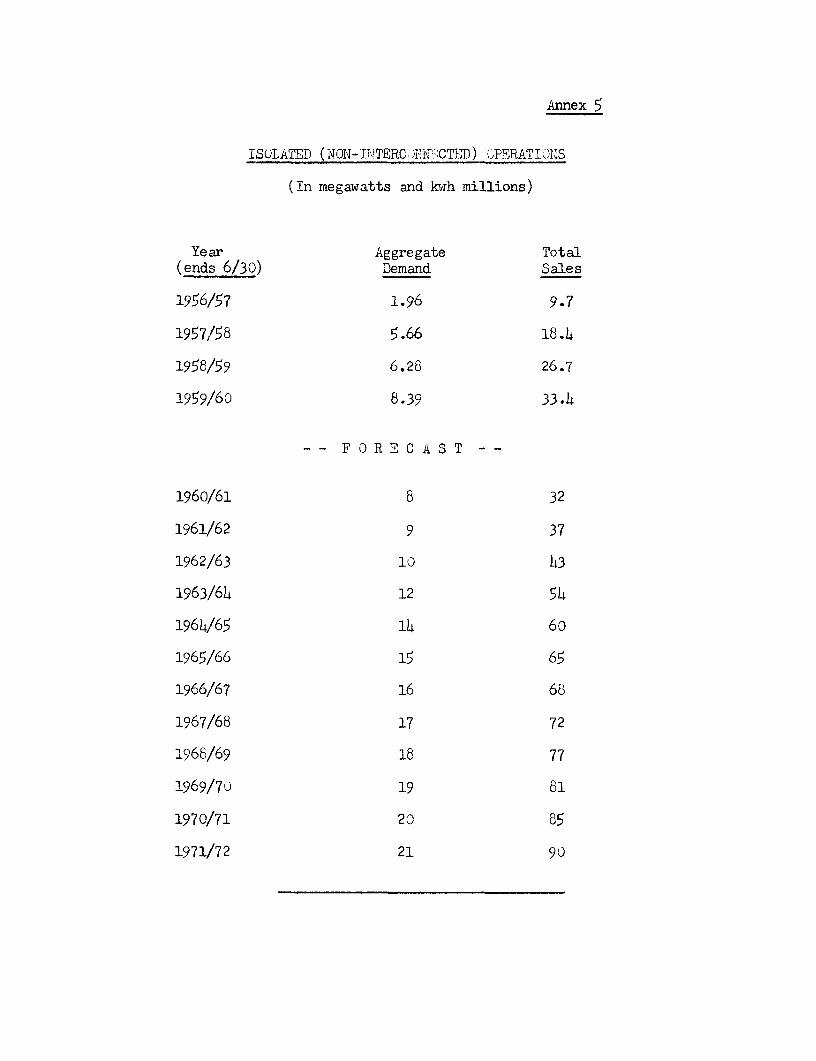

5. Isolated Operations Past and Forecast Sales

6. Summary - NPC Total Sales

7. Load and Capacity Curves - Luzon Grid

8. Load and Capacity Curves - llindanao (Agus) Grid

9. Details of Expansion Program

10. Detailed Description of Project

11. Angat Cost Estimate

12. Hydro Thermal Comparison

13. Balance Sheets 1957-58 to 1971-72

14. Income Statements 1957-58 to 1971-72

15. Net Cash from Operation Contributed towardsExpansion 1957-58 to 1964-65

16. Sources and Applications of Funds 1960-61to 1971-72

aIAP

APPRAISAL OF THE ANGAT HYDROELECTRIC PROJECT

THE NATIONAL POWER CORBORATION

PHILIPPITES

SUT214ARY

i. The National Power Corporation (NPC) asked the Bank to considera loan to help finance the cost of two power developments, the Angat hydro-electric development (206 NW) on Luzon and the addition of 50 !1W to theexisting Maria Cristina Falls hydro station on Mindanao. Both proposedundertakings were appraised but as there will likely be a delay of six toeight months before the market for the energy from the I4indanao expansionis clearly established it was agreed with NPC that only the Angat projectwould be submitted as a basis for a loan at this time. The total cost ofthe Angat project is estimated at about$62.8 million equivalent, includinginterest during construction, of which ji34 million would be in foreign cur-rencies.

ii. In 1957 the Bank made a loan of ~j21 million to NPC, later reducedto $18.5 million, to assist in financing the Binga hydroelectric project inNorthern Luzon. The project was completed about on schedule and has beenin full operation since early 1960.

iii. NPC is a Government-owned Corporation with an authorized capitalstock of Ps 250 million. It is responsible for planning and providing majorpower facilities to meet the country's requirements, except in Manila wherethis responsibility is exercised by the Manila Electric Corporation (I'leralco)which is also NPC's principal customer.

iv. The management and technical staff of NPC are experienced and ca-pable of carrying out the projects under review.

v. The project proposed for Bank financing is necessary to meet theforecast demand requirements of the Luzon grid serving MAanila and the mostpopulated areas of Luzon. The estimated cost of the project is realisticand reasonable and the investment in the proposed facilities is justified.

vi. NPC's financial position was unsatisfactory. By converting alllocal bonded indebtedness into equity at the end of fiscal year 1960-61 andby capitalizing interest thereon for the next ten years the Government hasimproved NPC's cash position so that it would be able to finance from re-tained earnings (including depreciation) about 23% of the proposed expansionprogram 1961-65. The level of earnings would still remain low, however, andNPC and the Government have agreed during negotiations that they would takeaction to remedy this situation before the end of the current fiscal year.

vii. Both satisfactory rate and debt limitation covenants were agreedupon during negotiations.

viii. The project would be suitable for a Bank loan of '34 million equiva-lent, including interest during construction of 1j.8 million, for a term of25 years including a grace period of 3-1/2 years on amortization payments.

APPRAISAL OF ThE ANQGAT HYDROEIECTRIC PROJECT

THE NATIONAL PATER CORPORATION

PHILIPPINES

I. INTRODUCTION

1. This report covers the appraisal of the 206 MW Angat hydroelectricproject on Luzon. The project would be carried out by the National PowerCorporation (NIPC) at a total cost which is estimated to be equivalent toabout $62.8 million including interest during construction on proposedforeign and local currency borrowings.

2. NPC has requested a Bank loan of $34 million equivalent to cover theforeign currency cost of the project including interest during constructionof ;4.8 million.

3. This report is based on data furnished by NPC to Bank missions whichvisited the Philippines in July 1960 and April 1961, on various data and re-ports received at the Bank through July 1961 and on discussions with NNPCmanagement during Bank visits in December 1960 and August 1961.

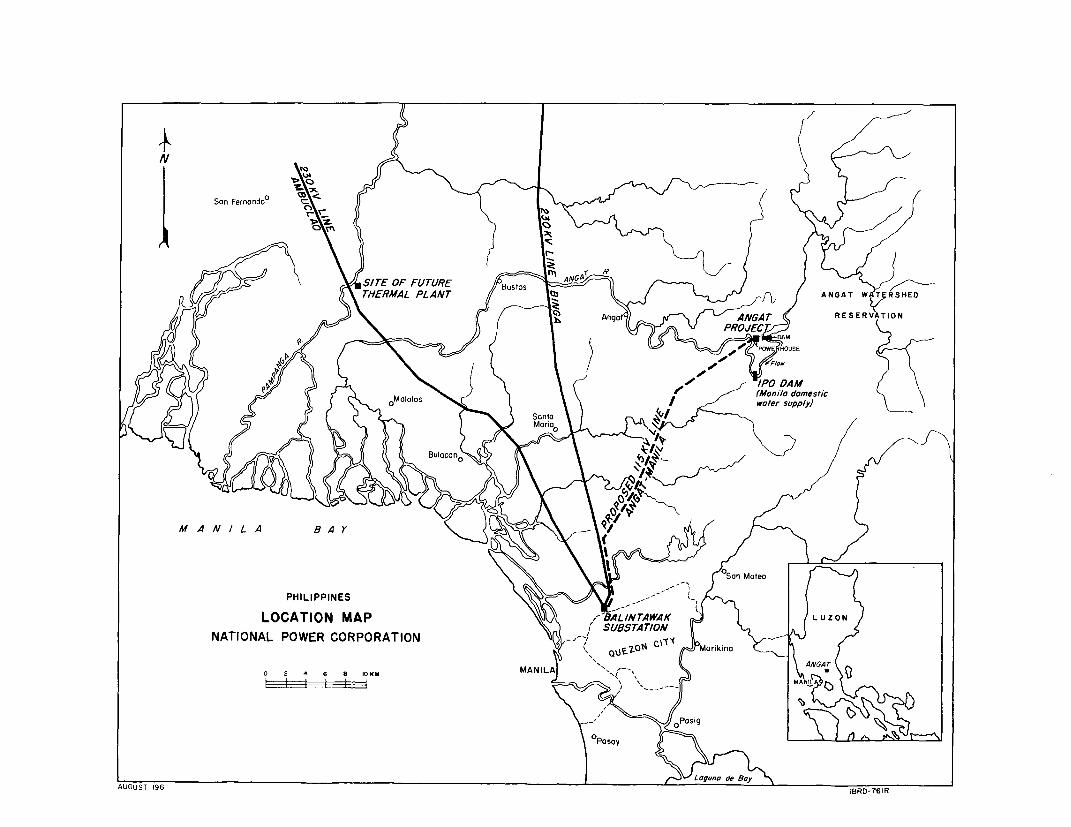

4. The Borrower would be NPC, an autonomous government-owned corporationwith headquarters in Manila. NPC is responsible for planning and providingpower facilities with which to meet the country t s requirements, except inijanila where it sells electricity wholesale to the MIanila Electric Company(Meralco) which distribut-es it in the metropolitan and surrounding area.Arrangements for the sale of this company by the General Public UtilitiesCorporation, a holding company with headquarters in New York and the presentowner, to the Meralco Securities Corporation, a Philippine investment group,were announced in Jane 19'11. The sale is subject to approval of the USSecurities and Exchange Conmission and to c;-rtain arrangaments being com-pleted by the Philippine group ind is not y:it final. There is no reason tobelieve that it will not be consummated, however.

5. The Bank has previously made one loan to NPC to assist in financ-ing the Binga hydroelectric project. This loan (183-PH) for $521 millionwas made in November 1957. It was later reduced to $18.5 million. Theproject consisted of a rockfill dam arid power plant on the Ango River innorthern Luzon with 100 EW instailled capacity plus transrmissfon to Manila.It was completed on schedule and has been in operation since early 1960.

II. THE BORROWER

6. NPC is a Government-owned corporation established by CommonwealthAct No. 120 of 1936. Subsequent amen. ments to this Act fixed the corporatelife of NPC until December 31, 2000 and converted it into a stock corporationwith an authorized stock capital of Ps 250 million.

- 2 -

7. NPC is administered by the National Power Board, composed offive members all appointed for a term of three years by the President ofthe Philippines with the consent of the Commission on Appointments of theNational Assembly. The members of the Board elect a chairman and a vice-chairman from among themselves.

8. NPC is authorized to borrow up to Ps 500 million, subject to theapproval of the President of the Philippines upon the recommendation of theNational Economic Council. Within the limits of this total borrowing power,NPC has been authorized by Republic Act No. 357 as amended by Republic ActNo. 813 and Republic Act No. 2055 to borrow up to $100 million equivalentin foreign exchange, to be guaranteed by the President of the Philippines.NPC is exempt from all duties and taxes except real property tax. It hasthe power to acquire property and to exercise the right of eminent domain.

9. The General Manager of NPC is appointed by the National PowerBoard subject to the approval of the President of the Philippines. Themanagement is experienced and capable. The operational and technical staffhave proven ability and are capable and competent of carrying out the pro-ject under review.

Existing Facilities

10. NPC's major power facilities and operations are concentrated intwo systems:

(a) Luzon Island System (Luzon Grid)

The Luzon grid is a system of high and low voltage transmissionlines extending from Baguio in the north to below Manila in thesouth. The main lines, or circuits, originate at NPC hydro sta-tions and terminate in Manila; the lower voltage circuits tapfrom the main lines at various points and extend into the marketarea. NPC owns these transmission facilities. Power is suppliedto the grid by NPC hydro plants (211 MiW) and Mleralco thermalplants (219 HW). Neralco also owns one small (15 IN) hydro plantwhich is connected to the grid and has under construction one 601NW thermal addition which is scheduled to be connected to the gridin December 1961. The Angat plant would be connected to this grid.

(b) The Mindanao Island System (Agus Grid)

This system is supplied by the existing 50 NVW Maria Cristinahydroelectric plant owned by NPC. It serves industrial develop-ment primarily and is, of course, physically separate from theLuzon grid.

NPC also operates fourteen small hydro plants with a total ca-pacity of about 10 IV! and two diesel powered plants with a capacity ofabout 1.5 MW. These facilities, which represent only a small part of NPC'stotal plant facilities, serve local isolated load centers in various loca-tions throughout the Philippines.

-3-

III. TXiE POWER MARKET

11. The relative importance of each of the operations mentioned inthe preceding paragraph can be seen from the following comparison of salesby NPC, for the year ended June 30, 1961.

Sales (millions of kwh) Installed MaximumPercent Capacity Demand

System Total of Total MiW MW

Luzon grid 830 82 211 168Agus grid 158 15 50 35All others 1/ 32 3 11 -

1,020 100

Luzon Grid

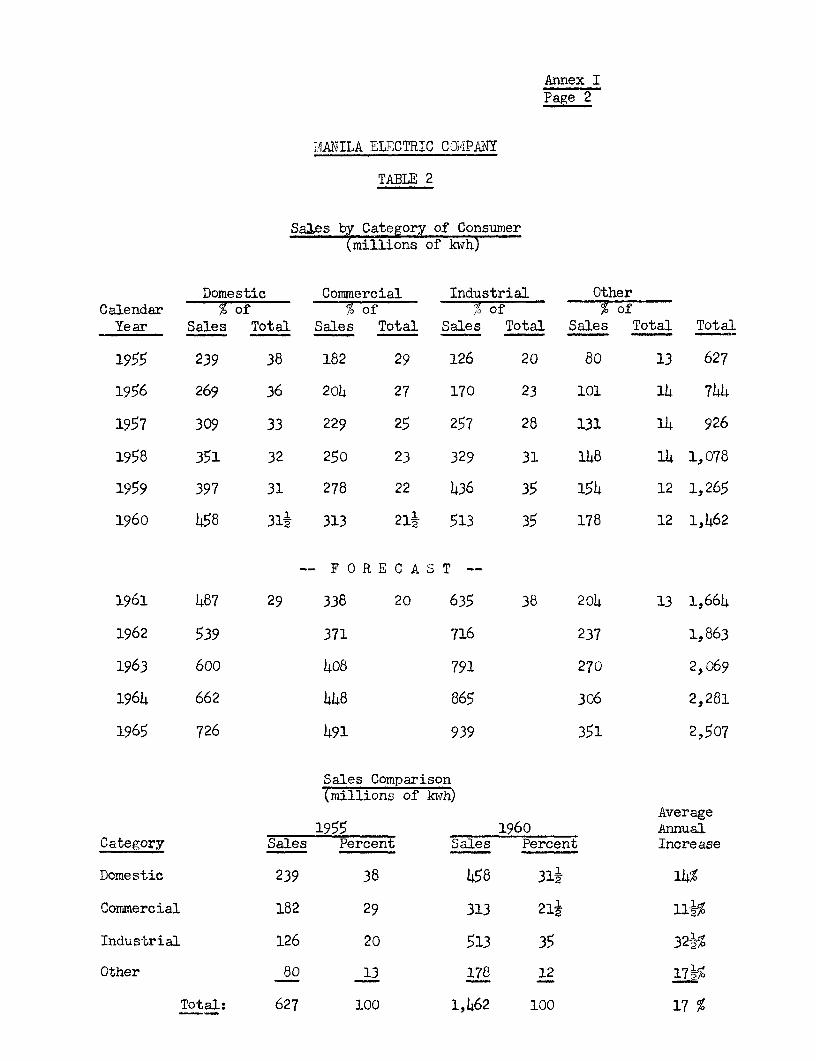

12. Meralco System: The major power market within the Luzon grid isthe Manila metropolitan area served by Meralco. In 1960-61 Meralco pur-chased 82% of the energy sold by NPC from the grid, or approximately 67% ofthe total energy sold by NPC from all its operations. Growth of energy anddemand in the Meralco system has been at a very rapid rate during the pastten years increasing slightly more than 31 times, or at an average annualrate of about 13%. Although the rate of growth was even more rapid duringthe last five years of the period the forecasts used in this report are basedon estimates prepared by Heralco which, for rate of growth, average aboutl11% annually. The forecast is probably conservative but is acceptable forpurposes of this report.

13. The forecast is shown in Annex 1, together with details of energyuse by category of consumer. In sur'iary, the maximum demand and gross en-ergy requikre.ents of the iMeraLco system are expected to increase about 3.3times and 3.0 times resnectively by 1972. The corresponding average growthrates would be about lll,% and 102%.

14. Provinc-ial System: The market area of the Luzon grid, exclusiveof the M4eral o system, is referred to as the provincial system. NPC sellspower and energy at present to some 50 small utilities plus military andother load certers connected to the system and plans to gradually extend itstransmission facilities to other utilities and load centers within the geo-graphical ar-a of the grid. The locations of the loads still to be con-nected are highly favorable to economical line extensions.

15. The forecast of demand and energy requirements for the provincialsystem is shown in Annex 2. The program of service extensions mentionedabove plus reasonable estimates of incireasing power utilization within theareas connected result in a forecast of load growth which averages about12:1% annually over the next eleven years.

1/ Estimated

- 4 -

16. A consolidated market forecast for the Luzon grid as a whole isshown in tabular form in Annex 3 and graphically (load growth) by Annex 7.The forecast shows that:

(a) Total system energy requirements for the Luzon grid are expectedto increase from 1,959 million kwh in 196o- 6 1 to 5,874 million kwhin 1971-72, an average annual increase of 10-1/2%.

(b) Total system demand would increase during the same period from381 MTiW to 1,266 ivJw, an average annual increase of 11-1/2%.

The Mindanao Island System

17. The market served by the Agus grid, supplied by the existing 50 viWMaria Cristina hydro station, consists of steel mills owned by the NationalShipyard and Steel Corporation (NASSCO), a carbide plant owned by Maria Cris-tina Chemical Industries Incorporated, an ammonium sulphate fertilizer plantsold by NPC in 1960 to the Mercelo Tire and Rubber Corporation and the fran-chise area of the Iligan Electric Company. The load on the system reachedabout 35 MWT in 1960.

18. A planned cement plant by the Mindanao Portland Cement Company, aline extension to Cagayan de Oro City and a mineral development by theMarinduque Iron Mines are expected to completely utilize the existing plantby 1962-63. Demand at that time is forecast to reach L5 MT. NASSCO hasplans which would, in addition, increase the steel mill demand from 8 to60 Dill and annual energy requirements from 18 to 430 million kwh in 1966-67.The above pattern of suddenly applied industrial loads is reflected in theforecast shown in Annex 4 which indicates that system demand would increaseseven times during the next eleven years, from 35 Mnu in 1960-61 to 254 MWin 1971-72. As could be expected, the forecast shows a series of block in-creases rather than a normal growth pattern. This forecast is also showngraphically by Annex 8.

Other Operations

19. The operations of the many small hydro and diesel plants owned bythe Corporation and not interconnected because of physical or economicalfactors can be expected to increase at a modest rate in the future. Al-though the financial results from these small isolated operations remaininsignificant compared with those of the Corporation's other activities, amarket forecast has nevertheless been prepared and is shown in Annex 5.The revenues and costs associated with this category of the Corporation'sbusiness have been included in the financial forecasts discussed later.

IV. THE NPC EXPANSION PROGRAM

20. The basic assumptions for the formulation of NPC's expansion pro-gram are that NPC will be responsible for the installations of all additionalcapacity needed to meet the demand of the Luzon grid after the completion ofthe 60 MW thermal addition now under construction by MYeralco (paragraph 20)and after the completion of one other 60 HW thermal addition wJhich Meralcohas said it would construct for completion in December 1962, and tlat it will

- 5 -

add to capacity in Mindanao as rapidly as necessary to meet increased de-mand of the Agus grid. It would also be necessary to add a small amountof new capacity to the aggregate capacity of the isolated plants but thiscategory of NPC operations is insignificant relative to other NPC opera-tions. Discussion of the expansion program in this report is thereforeconfined to the Agus and Luzon grids. The financial projections, however,include provisions for a modest expansion in the category of small plantoperations.

21. Although Meralco has not agreed that NPC would be solely responsi-ble for future capacity additions to the grid after the completion of Angat,it has agreed to re-examine the program for future plant additions so that,by early 1962, the responsibility for the next phase of capacity expansioncan be determined. For the purpose of this report it has been assumed thatNPC would bear the entire cost of the future expansion program. This isprobably a very conservative assumption but the only practical one in thecircumstances.

Luzon Grid Expansion

22. The expansion program planned for the Luzon grid would add 886 M4Wof new generation capacity to the system by the end of 1972. Of the total,510 1MW would be thermal capacity and 376 rNW would be hydro capacity. Thisis in addition to the 60 MA thermal unit being constructed by Meralco whichis scheduled for completion in December 1961.

23. The starting and completion dates and the nameplate and effectivecapacity of each of the units in the expansion program and their approximatecosts are shown in Annex 9. The effect of the expansion program is relatedgraphically to the expected load growth in Annex 7.

24. The cost assumed to be borne by NPC for the Luzon grid expansionprogram through 1972, including necessary transmission facilities but ex-cluding interest during construction, is estimated to be the equivalent ofabout $233 million of which about $145 million would be in foreign exchange.This cost obviously indicates an order of magnitude rather than an absolutevalue.

25. Means might be found to utilize existing and planned capacity moreefficiently after the completion of Angat if a study of system operatingcharacteristics should indicate, for example, an advantage in using systemhydro capacity more for peaking than has been the practice in the past. Sucha study is being made by NPC and Meralco at the present time.

26. Participation in the Marikina project is not included in the pres-ent NPC expansion program nor in the financial projections of this report.The project has been proposed as a joint undertaking by the National Water

- 6 -

and Sewer Authority (NWSA), the Government and NPC. Its assumed costs havebeen apportioned by an arbitrary allocation of benefits in the ratio of42.2% to NWSA for domestic water supply, 23.3% to Government for flood con-trol and 34.5% to NPC for power. Its benefits appear marginal at best, how-ever, and the project would be difficult to justify on any sound basis evenat the presently estimated cost of Ps 108 million. Construction would bedifficult and this estimate would very likely be exceeded by a large margin.

27. The main justification for the project by its supporters is thatit would provide a new source of domestic water supply for Manila. A powerinstallation of about 68 MW has also been proposed but the power output wouldprobably be governed by the other purposes of the project and at best wouldbe limited by water conditions to less than a 25% annual plant factor. Thenew source of water supply would probably not be needed until the mid 1970'sif Angat is constructed as proposed. In the circumstances, NPC's participa-tion in the project if constructed earlier, can only be judged by the termsof NPC's covenants to the Bank at such time as firm costs and plans for theproject financing are known.

The Mindanao System Expansion

28. The expansion of the Mindanao System to meet the estimated increasein demand discussed in paragraph 18 would utilize the excellent potential ofthe Agus River, the ultimate development of which is estimated to be about750 MW with some regulation of the outflow of Lake Lanao, the source of theAgus River. The first step would consist of the addition of a third unitof 50 MW capacity to the existing two unit (2 x 25 iMw) Maria Cristina Fallsstation.

29. This 50 MW addition would be needed to meet the increased powerdemand of the steel mill expansion. However, since it will take slightlylonger to complete the new steel facilities than it will NPC to completethe Maria Cristina addition, NPC will not start its construction untilfinancial arrangements for the steel mill expansion are completed. Theexpansion is expected to be financed primarily through an Export ImportBank loan of $62.3 million but the loan, although announced, will not be-come effective until certain legislation is passed by the Philippine Con-gress. The legislation can not be acted upon until Congress reconvenes inJanuary and it is not at this time certain that full support for the meas-ures required for the Export Import Bank loan will be forthcoming. NPChad originally asked to have about $3.8 million included in the proposedloan to cover the Maria Cristina expansion. However, for the reasons sta-ted above, it was decided to defer consideration of a Bank loan for thispurpose until the steel mill expansion is firmly financed or until justi-fied by other load growth.

30. Shortly after the completion of the third unit at the Maria Cris-tina Falls station and depending on industrial expansion on the island, asecond station (Agus No. 2) is planned to be constructed with two 50 NWunits installed. Engineering investigations are well advanced and theproject could be carried out in about three years after financing was

-7-

arranged. Cost would be very reasonable, equivalent to about 1WI?* millionor about $172 per kilowatt installed.

31. The two plants would have 200 141W (nameplate) capacity of which 188NW would be useable 100% of the time.

32. After the completion of Agus No. 2 plant NPC plans to install afourth unit of 50 UI in the Maria Cristina Falls station provided the in-crease in demand requires it.

33. The total expenditures on the Mindanao System envisaged through1972 are estimated to amount to the equivalent of about $46 million of whichabout ?15 million would be in foreign exchange.

34. In summary, during the period from 1961 to 1972 NPC plans to add1086 MIW to its two grid systems consisting of 886 MW on the island of Luzonand 200 SW on the island of Mindanao. About 10 MlW would also be added inthe category of small plant operations. This expansion is estimated tocost the equivalent of about $i;284 million exclusive of interest during con-struction of which about $160 million would be in foreign exchange. Thefirst step would be the project proposed for Bank financing.

V. THE SALES FORECAST

35. The expansion program discussed in the previous chapter will per-mit NPC to supply the forecast demand and energy requirements of both gridsystems.

Luzon Grid

36. The amount of power and energy to be supplied by NPC to Nleralcothrough calendar year 1965 is closely fixed by a iMemorandum of Understandingwhich was agreed upon by the two parties in April 1961. The basic objec-tive of the memorandum was to reach agreement on the principle of operationof plants connected to the Luzon grid. This principle, as quoted from thememorandum, is - "Operate all of the NPC and ieralco generating and relatedtransmission facilities as one common system in order to obtain optimum ef-ficiency and economy to the common system".

37. The principles of the memorandum discussed above result in esti-mated sales of power and energy by NPC to iIeralco which increase from 681million kwh and 136 mW in 1960-61 to 3,367 million kwh and 820 INW in 1971-72.The proportion of Meralco's total energy requirements supplied by NPC wouldincrease from about 38% to 63% during the same period. Further detailsare shown in Annex 1.

38. Estimates of power and energy sales to consumers in the provincialarea are based on the program of service connections discussed in paragraph14. The forecast is shown in Annex 2.

39. The preceding estimates have been combined into a forecast of NPCpower and energy sales for the Luzon grid as a whole as shown in Annex 3.MPC sales would increase from 830 million kwh in 1960-6). to 3,912 millionkwh in 1971-72 according to tile forecast. Total energy requirements

-8 -

of the grid are forecast to increase at an average annual rate of about lo1N.IPC's energy sales, howTever, due to its expansion program, are forecast toincrease during the same period at an average annual rate of about l5,.

The Mindanao Island System

4o. NPC sales from the Agus grid are expected to coincide with increas-ing requirements for power and energy in the market area as discussed in para-graph 18 and showem in Annex 4.

41. A summary of total forecast NPC energy sales through 1971-72 in-cluding those from its non-interconnected plants is shown in Annex 6. Thecomposite average annual rate of increase is expected to be about 161-: whichcould very well prove conservative.

VI. THE PROJECT

The Angat Hydroelectric Development

42. The proposed development is located on the Angat River about 40kilometers northeast of Manila and 712 kilometers upstream of the existingIpo Dam which is the present principal domestic water source for I4anila.The dam site, which is excellent, is at the upper end of a 12 kilometer longloop in the river. In the length of this loop the river falls about 30 me-ters and it is this natural head with the head from a 125 meter high earthand rockfill dam that would be utilized for power production. The dam wouldform a reservoir with useable storage of about 580 million cubic meters.

43. A pressure tunnel about 1,400 meters long, cutting across the shortbase of the loop, would carry water from the intake structure behind the damto a powerhouse located at the lower end of the loop in which four 50 '1T unitswould be installed. A secondary powerhouse wJith an initial installation of6 1IJ would be located at the outlet of one of two diversion tunnels usedduring construction. This secondary installation would utilize the hydropotential of water diverted into the Ipo reservoir.

44. The energy output from the development in an average water yearwould be about 673 million kwh. The powier installation would total 206 1suJand firm power of 147 14W would always be available with the operationa' regimeplanned for the reservoir. These values would not change materially in thefuture even though diversion to the Ipo reservoir might increase, as the sec-ondary powerhouse would be constructed to allow for future expansion.

45. Both irrigation and flood control benefits would be made possibleby the project if tentative plans of the Government are carried out. Irri-gation benefits would result from an assured 12 month water supply whichwould be made possible by construction of a small regulating dam furtherdomnstream. The Ministry of Public Works would be responsible for the con-struction of the re-regulating dam and irrigation works. -larginal floodcontrol benefits would also accrue without prejudice to the power aspects ofthe project if, by increasing the height of the dam, a flood control poolabove the power pool were provided. The Government is investigating this

aspect of the project. Although it is unlikely that the Government would in-sist on providing for this very marginal flood control feature it has, on theother hand, not clearly indicated that it would not.

46. To provide assurance that the project would not be affected by asubsequent major design change, the proposed Loan Agreement contains anappropriate covenant which requires the Bank's approval for any major designchanges.

47. The present layout of the project is based on a conventional sur-face powerhouse. This feature is being further studied, however, with thehope that geological features will permit a design modification to an under-ground powerhouse. This could permit considerable savings in the cost ofwater conductors and associated items. Further details of the project aregiven in Annex 10.

Cost Estimate

48. The Angat development, including transmission facilities to Manila,is expected to cost the equivalent of about $i62.8 million. This includesinterest during construction of $5.3 million and contingencies of about 15%on both foreign and local estimated costs plus a contingency of about 10% onthe local cost estimate to cover possible local price increases. The foreignexchange component would total $?34 million. Since NWSA has agreed to con-tribute Ps 21.5 million toward the local costs in return for future waterbenefits, the total cost to NPC would be about !55.7 million equivalent.This is equal to about $270 per installed kilowatt of capacity.

49. A condensed cost estimate is shown below; a more complete estimateis shown in Annex I1.

Cost (in $ thousands)Item Foreign Local Total

Civil Works 1/ 14,615 19,932 34,547Equipment 6,048 433 6,481Transmission 2,855 4°5 3,260

Sub-Total 23,518 20,770 44,288

Contingency (15%) 3,582 3,230 6,812Price Increases (10%) , 2,167 2320167Fngineering etc. 2,100 2,167 4,267

Sub-Total (construction cost) 29,230 28,334 57,534

Interest during construction 41,800 500 5,300

Total Cost 34,0co 28,834 62,834

NWSA contribution (deduct) _ 7,167 7,167

NPC Cost 34,000 21,667 55,667

l/Includes an allowance of Ps 6 million for NPC owned construction equipment.

- 10 -

50. If the design modifications mentioned in paragraph 47 prove feasiblethere is a possibility for foreign exchange savings in the cost of the project-perhaps as much as t2 million. A decision probably can not be made beforeearly 1962, however, but if the savings are realized the Borrower expects tocancel a portion of the proposed loan.

51. Foreign exchange cost items include additional construction equip-ment, steel, generating equipment and other items not locally available.Cement, fuel for equipment, and other associated petroleum products areavailable locally and are not included in the foreign exchange component ofthe estimate. Estimates are based on prices reported in recent internationalbidding and awards would be made after securing international competition.The local component of the civil works estimate includes an allowance for NPCowned construction equipment and spare parts valued at Ps 6 million. Thisequipment and spare parts inventory is available from previous projects. Nosalvage or resale value is assumed after the completion of Angat.

Rate of Expenditure and I4ethod of Finance

52. The estimated rates of expenditure for the project including interestduring construction are shown below:

Expenditures ($ thousands)

1961-62 1962-63 1963-64 1964-65 Total

Foreign Exchange 8,490 10,183 10,193 5,13k 34,000Local Currency 1/ 5,834 8,o00 7,867 5,133 26,834

Total 14,324 18,183 18,060 10,267 60,834

l/Excluding Ps 6 million book value of construction equipment owned by NPCbut including the Ps 21.5 million to be contributed by NWSA.

53. The foreign exchange cost of the project which totals t34 millionincluding interest during construction of $4.8 million would be financed by aBank loan. Local costs which total about 46% of total costs will be metthroughi the Ps 21.5 million contribution from NWSA, local borrowings of aboutPs 15 million and the balance from Government equity contributions and NPC'sown resources. NPCts contribution toward the total cost of the project fromits retained earnings including depreciation would be about 20%.

Engineering and Supervision of Construction

54. The engineering and construction departments of NPC are experiencedand capable and NPC as an organization has the experience gained during theconstruction of the Caliraya, Maria Cristina, Ambuklao and Binga hydro electricplants. The organization is fully capable of carrying out the project withthe advice of consultants as outlined below.

- 11-

55. The general arrangements of dam, dikes, spillway, diversion tunnels,main power tunnel, main and auxiliary power plants were prepared by the NPCstaff and reviewed by consultants engaged by NPC in June 1960. The consult-ants, the Association of Harza Engineering Company of Chicago and the Engi-neering and Development Corporation of the Philippines, and their terms ofreference are satisfactory.

56. The services already provided and to be provided in the future in-clude a thorough review of design criteria and cost estimates; assistance inthe preparation of bidding documents and analysis of bids; preparation ofdesign drawings, or, in cases where design drawings are prepared by NPC, thereview of such drawings; and assistance to NPC in setting up and carrying outengineering supervision during construction.

Schedule of Construction

57. The execution of the project is scheduled over a period of 31 yearsstarting from July 1961 with completion scheduled in December 196h. No un-usual problems are foreseen as the site is excellent and design conventional.A large inventory of construction equipment and spare parts is now owned byNPC and a good supply of construction manpower, both skilled and unskilled,is available in the Manila area.

VII. JUSTIFICATION OF THE PROJECT

58. The project is necessary to meet the forecast demand requirementsof the Luzon grid. The estimated cost is realistic and reasonable. The in-vestment in the project compares favorably with the investment that would benecessary for the most economical alternative source of power.

59. Reference to the hydro-thermal comparison shown in Annex 12 indicatesthat the return on the extra investment for Angat, compared to a thermnal plantof 150 MT rating and with conservative assumptions with regard to the priceof fuel would be about 12.3%.

60. The Angat development would also provide seasonal regulation forirrigation purposes further downstream. A re-regulating dam would be re-quired before full irrigation benefit could accrue, but such a dam wouldbe relatively inexpensive and could also provide for some additional powergeneration. No attempt was made to apportion any part of the cost of theproject to this possible irrigation benefit, however, as planning for theirrigation feature is incomplete. The Angat development would also provide afirn scurce of domestic water supply for Manila for many years.

VIII. FINANCIAL ASPECTS

Present Financial Position

61. Condensed balance sheets for the fiscal years ended June 30, 1958through 1961 are shown in Annex 13. The figures for fiscal year 1960-61 arepartially still based on estimates since audited statements are not availableyet.

- 12 -

62. As of June 30, 1961, fixed power assets and work in progress totalledabout Ps 283 million. Deducting the depreciation reserve of Ps 13 million,net fixed pouer assets were Ps 270 million. The net fertilizer investment ofPs 15.2 million represented receivables on account of the sale of NPC's fer-tilizer plant: Ps 9 million, the balance of the sales price, are payable bythe new owner over a 15 year period and Ps 6.2 million of fertilizer inventorieswithin 10 years; 6% interest is charged on all outstanding balances.

63. NPC's accounts, which are kept in accordance with accepted businessprinciples and practices, are audited by independent auditors appointed by andresponsible to the Auditor General of the Philippines.

64. During fiscal year 1959-60 legislation was enacted to convert NPCinto a stock corporation with an authorized capital stock of Ps 100 million,owned by the Government, of which Ps 92 million were issued. In May 1961 thisact was amended whereby NPCts authorized capital was increased to Ps 250million. The present authorized but unissued share capital of Ps 158 millionwas to come from a) the conversion into equity of NPC's existing bonded in-debtedness in an anount of about Ps 141 million and b) future Governmentcontributions of about Ps 17 million. It should, however, be borne in mindthat these Ps 158 million are required to be repaid starting July 1, 1970 aspointed out below in paragraph 65. Although these Ps 158 million are, underpresent legislation, formally represented by shares (as shown in Annex 13),they are in fact subordinated deferred debt and can thus not be considered trueequity. Consequently, the capitalization of the Corporation is as follows:

Capitalization as of June 30, 1960 June 30 1961pesos 75 of Pesos - of

(in millions) Total (in millions) TotalEquity

Issued share capital l/ 92,0 31.5 92.0 29.2Reserves and net surplus 11,0 3M8 16.7 5.3

Total equity -103X0 33 108.7 317.

Debt outstandingForeign currency loans (exchange rate: US,l = Ps 2 ):

Export Import Bank, 4%,23 years, 1952-75 30.5 28.5

IBRD (Binga), 6%,25 years, 1957-82 32,8 36.0Sub-Total G3T7 21.7 20.5

Local currency loans 136.5Less sinking fund assets lle0

Sub-Total 1575 43.0o

Issued share capital(repayable startingJuly 1, 1970) )/ - - 141.5 45.0

Total debt outstanding 188.8 64.7 206.0 65.5Total capitalization 291.8 100.0 314.7 100.0

17or the breakdowm of authorized share capital see table after paragraph 65.

-13 -

65. The original capitalization law left NPC with a high debt to equityratio of 65/35 and did not materially affect its cash position. The initialstock was issued by converting Ps 10 million of surplus and Ps 82 million ofGovernment advances which carried 4% interest but had no maturities or sink-ing fund provisions. The 1961 amendment of the law did not, in fact, improveNPC's capital structure as shown above (debt/equity ratio of 65/35), but itwill relieve the Corporation's cash position through a reduction of debtservice until 1970. Specifically, the new law provided that up to July 30,1970, all interest payments on capital stock were to be capitalized as addi-tional authorized share capital. The resulting annual savings in interestand sinking fund payments will amount to about Ps 13 million for the next 9years. After June 30, 1970 cumulative fixed interest will again be payableout of net earnings on Ps 2t0 million of authorized, issued share capital; inaddition, Ps 158 million of this issued capital stock will be repayable on asinking fund basis and will thus, in fact, assume the character of a long-termdebt. The following table summarizes the provision of the law:

Authorized Share Capital

Amount Origin Annual Interest RedemptionPayable 1/

a) Ps 10 mi7lion Surplus none none

b) Ps 82 " Government advances 4% none

c) Ps 158 " i) Bonded debt )(Ps 141 million) 4% ) 30-year sinking

ii) Future Government ) fund, 3N,start-contributions ) ing July 1, 1970(Ps 17 million) 6% )

d) Ps 85 k Accumulated capitalized(estimated) interest on b) and c)

above none none

1/ Capitalized up to June 30, 1970.

66. About 21% of NPC's present capitalization is in foreign currencyloans consisting of a US$ 20 million loan from the Export Import Bank forconstruction of the Ambuklao project and of the World Bank loan of US$M 21million, later reduced to US$ 18.5 million, for the construction of the Bingaproject.

67. Foreign exchange loans were serviced at the official exchange rateof US$ 1 = Ps 2,0 until September 1960. As a result of the liberalization ofthse foreign exchange control, loans incurred after that date, including theproposed IERD loan, will be serviced at the free exchange rate - presumablyUS8f'l = Ps 3.0. Loans approved prior to that date will continue to be serviced

- 14 -

at a preferential rate of US$1 = Ps 2.0 until December 1961. According toMEPC and the Governor of the Central Bank, however, the preferential rate willapply to the Export Import Bank loan until maturity.

68. Almost all the local currency loans which were converted into equityas of June 30, 1961 were represented by 4% 30-year bonds placed with govern-ment financial institutions and issued with Central Bank guarantee. Sinkingfund payments based on 30 years are deposited with the Treasury, where theyare credited with interest at 31% per annum. It is understood that futurelocal currency borrowings would take the form of bond issues without CentralBank guarantee carrying a higher interest of 6% (see also paragraph 79f below).

Earnings Record

69. As shown in Annex 14 which contains summarized income statementsfor the four fiscal years ended June 30, 1961, the rate of return on netpower assets in operation (excluding the fertilizer investment) averaged only5.4% in the past four years since the Binga loan was made, despite the factthat depreciation allowances are on the low side. In the same years con-tribution of earnings to expansion was only about 5% as shown in Annex 15.Tnterest and debt service were barely covered although artificially lowbecause interest on the local currency debt was only 4% and Ps 82 millionof government advances had no sinking fund provisions. These unsatisfactoryresults were caused mostly by low rates and delays in obtaining rate increases,as will be further discussed below.

Rates

70. NPC's power rates are subject to the approval of the Office ofZconomic Coordination (OEC) an agency responsible for supervising government-owned corporations. The 0EC in turn submits its decision to the Cabinet forapproval. This procedure has led to delays in the past. Most of NPC's powercontracts, with the major exception of those with Meralco, contain provisionsfor rate adjustments if general adjustments are approved by OEC. The contractswith Meralco, however, are in the form of long term supply contracts with nopro,.ision for adjustment and subject to cancellation only upon three yearwritten notice by either party. The Yemorandum of Understanding mentionedearlier (paragraph 36) does provide a means for periodically adjusting theamount of power and energy to be supplied by NPC, but not its price, whiclh isfixed by the long term contract. NPC thus has no recourse on Meralco ratematters, except contract cancellation after three year written notice, ifunable to reach satisfactory agreement with Meralco. Because of the initialdelays inherent in obtaining OEC approval, and the further problem of havingno unilateral means of adjusting tariffs to Meralco, a two year delay was ex-perienced in implementing the rate increase which NPC had undertaken to seekas a condition of the Binga loan. Furthermore, the increases obtained re-sulted in an increment of about 18% in revenue, instead of the expected 25%.

- 15 _

71. As a result of the delays and shortfalls in obtaining rate in-creases, NPC did not earn a "reasonable return on its investment" enablingit to net an "appropriate part of the cost of future expansion of its fa-cilities" as stipulated by the rate covenant in Section 5.09 of the BingaLoan Agreement. In spite of a 50% increase in the 14indanao rates (January1959) and of a 10% increase applying to sales to Meralco (April 1960), fore-cast earnings were still inadequate to finance a reasonable proportion ofthe proposed expansion after meeting the expected increase of debt service.

72. Since the most appropriate solution in these circumstances, namelyfurther rate increases for NPC, seemed at the time impractical, the Govern-ment decided to reduce NPC's annual debt service by deferring sinking fundpayments and by capitalizing interest on certain local debts (see paragraph65). Although this provided a considerable relief to the Corporation's cashposition, it left the basic problem of a low level of earnings unchanged.

73. As was indicated in paragraph 70 there is no provision yet in thepresent contract with Meralco to revise rates periodically or to adjust themfor increases in production cost. NPC and the Government agreed that thisshould be remedied as soon as possible.

Financing Plan

74. A forecast of sources and applications of funds for the eleven yearsthrough 1972 is given in Annex 16. This forecast is based on present tariffsand the legislation described above under paragraph 64.

75. During the four year period ending June 30, 1965, when the Angatplant would start operation, plant additions including interest charged toconstruction would amount to about Ps 328 million (Annex 15). This is aftercrediting the Ps 21.5 million participation of NWSA in the cost of the Angatproject. During negotiations the Government confirmed and guaranteed theassurances of NWSA that these funds would be contributed as required.

76. Under the proposed plan NPC would finance about Ps 75 million or23% of its requirements from net cash earnings, about Ps 17 million or 5%from existing cash and construction inventories and from the proceeds of thefertilizer plant sale, roughly Ps 38 million or 12% from additional purchaseof shares by the Government and from the 1TWSA contributions, and the balanceof about Ps 198 million or 60% from borrowings.

77. The borrowings assumed are as follows:

(a) A Bank loan of US$34.0 million would be obtained in 1961-62 forthe Angat hydro project in Luzon, at an assumed interest rateof 5-3/4% and for a term of 25 years including a 32 year graceperiod.

(b) The same conditions are assumed for another foreign exchangeloan in the same year 1961-62, amounting to US$3.8 million,for the Maria Cristina 3 hydro project in Mindanao.

- 16 -

(c) A Japanese war reparations loan equivalent to US$3.7 millionat an interest rate of 3%, and for a term of 10 years will beavailable in 1961-63 for transmission expansion in Luzon andMindanao.

(d) Another foreign exchange loan of US$6.4 million would be ob-tained in 1962-63 for the Agus 2 hydro project in M4indanao, atan assumed interest rate of 5-3/4% and for a term of 25 yearsincluding a three year grace period.

(e) Further foreign exchange loans totalling about US$114 millionwould be obtained in the 9 fiscal years 1963-64 through 1971-72for the financing of NPC's future generation expansion.

(f) Local currency 6% 30-year bond issues totalling Ps 30 millionwould be required during the next four fiscal years. 50% ofthis total or Ps 15 million would be allocated to the financingof the Bank project. Additional Ps 62 rmdillion in bond issueshave been assumed for the period 1965-66 through 1971-72. Theseassumuiptions are based on the present practice that NPC is al-lowed to issue annually a certain amount of bonds without Cen-tral Bank guarantee which are placed with Government financialinstitutions.

78. The forecast of sources and application of funds for the years1966-72 should be considered as giving trends and orders of magnitude, ratherthan an exact financing plan. The estimates indicate that NPC's fixed as-sets in operation would double over this seven year period and that thisexpansion would in essence be financed 34% from its own resources and 66%from outside borrowing.

Estimated Future Financial Position

79. Forecast income statements for the 11 years ending June 30, 1972are given in Annex 14. Net income before interest is expected to rise fromPs 17.5 million in 1962 to Ps 27.3 million in 1965, and would reach Ps 61.4million in 1972. The return on net fixed assets in operation would increasefrom 6.3% in 1962 to 6.9% in 1965 and 7.7% in 1968 before it would declineto 7% in 1972. Year end interest and debt service coverages would be re-spectively 3.2 and 2.4 times in 1962 excluding capitalized interest on sharecapital as provided by the law described in paragraph 65. They would remainon a lower but acceptable level up to 1970. In 1971, when in accordancewith the new capitalization law, interest and sinking fund payments wouldcommence on share capital, interest and debt service coverage ratios woulddrop to 1.4 and 1.2 times respectively. Cash earnings (including deprecia-tion), after deduction of interest chargeable to operations and amortizationof existing and proposed debt are expected to provide about Ps 75 million or23% of total requirements between 1962-65; the equivalent figures for theperiod 1966-72 would be Ps 187 million or 33%.

80. From the above figures two facts can easily be seen. The measurestaken so far by NPC and the Government, on the one hand, have improved NPC'scash position. On the other hand, the earnings level would improve only

- 17 -

very little and would remain low throughout the period under review. NPC'searnings would become also highly vulnerable to any upward adjustment offoreign exchange rates since, within a few years, close to half of its cap-italization would be in foreign exchange debts.

81. In order to alleviate this situation and to establish a sound fi-nancial position for NPG, both NPC and the Government have agreed to takeaction with regard to rates as soon as possible. During negotiations a ratecovenant similar to the one in Section 5.09 of the Binga Loan Agreement (seeparagraph 71) was agreed upon. In an explanatory letter to this covenantthe Government and NPC both agreed to establish rates at such a level thatNPC's internal cash generation after debt service would finance, on the basisof present estimates, not less than 25% of new construction during fiscalyears 1962-63 to 1964-65. They declared their intention furthermore to takethe required action before June 30, 1962. Within three months after thisdate the Bank, the Borrower and the Guarantor would convene to review the stepstaken and to establish what further action, if any, would be required to achievethe purpose of the covenant. The letter furthermore states that the percen-tage of new investments to be contributed by NPC in subsequent years is ex-pected to exceed the above 25% and will be established from time to time onthe basis of future reviews on NPC's expansion program and earnings level.

Debt Limitation Covenant

82. NPC agreed under Section 5.10 of the Binga Loan Agreement that itwould not incur debt unless its actual net revenues of the last fiscal year(adjusted for rates in effect at the time of the calculation) plus 75% ofthe estimated net revenues from plants under construction and to be con-structed from proceeds of the proposed loan would cover at least 1.4 timesthe maximum debt service for any succeeding fiscal year on all debt out-standing and on the debt to be incurred.

83. During negotiations it was agreed that a covenant similar to theBinga debt limitation covenant be included in the loan agreement. It wasalso agreed that the interest and sinking fund payments on capital stockafter July 1, 1970 (see paragraph 65) would have to be included in the com-putation of the maximum annual debt service requirements under the terms ofthe covenant because they represent binding financial obligations of NPC.

84. On this basis NPC would not be able to incur the proposed debt forthe Angat project and comply with the covenant without having previously ob-tained a rate increase of about 20%. In the present circumstances it wouldbe unrealistic to assume an increase of this magnitude and the Bank has,therefore, agreed to waive the provisions of the debt limitation covenantfor the proposed loan for Angat. If the proposed tariff action (paragraph81) should be completed before financing is required for the Maria Cristinaaddition then NPC could, based on present forecasts, incur the necessary newdebt and still comply with the covenant. If, however, financing for MariaCristina is required in the first half of 1962 the Bank would find it neces-sary to waive the covenant again.

- 18 -

IX. CONCLUSIONS

85. The proposed project to be executed by NPC is technically soLudand economically justified. The estimated cost of the project is reason-able.

86. The project is necessary to provide the capacity required to meetthe estimated increase in power demand in the Luzon area.

87. The management of NPC is competent. Its staff, with the assist-ance of consultants, is well qualified to construct and operate the project.

88. NPC's present and projected financial position is somewhat weak.NPC and the Government have agreed to take steps to improve NPC's earningslevel before the end of the current fiscal year. The rate increase dis-cussed with NPC and the Government should put the Borrower on a sound fi-nancial basis.

89. The project would be suitable for a Bank loan of $34 millionequivalent, including interest during construction, for a term of 25 years,including a 32 year grace period on amortization.

Annex IPage I

'IANT LA ELICTRIC COIiPANfY

TABLE I

Actual and Forecast Demand, Energy and Sales(in megawatts and kwh millions)

M4aximum Demand Energy PercentYear Total Supplied Gross Purchase Total Sales

(ends 6/30) System by NPC Energy from NPC Sales Increase

1956/57 219 77 1,048 310 836 _

1957/58 253 102 1,248 349 1,017 22

1958/59 280 96 1,430 392 1,164 15

1959/60 311 141 1,610 464 1,369 17

-- F O R E C A S T--

1/1960/61 350 136- 1,810 681 1,550 13

1961/62 390 143 2,045 854 1,760 13

1962/63 44o 150 2,314 785 1,990 13

1963/64 490 140 2,564 697 2,200 11

1964/65 550 204 2,824 914 2,430 11

1965/66 614 285 3,105 1,285 2,670 10

1966/67 686 360 3,397 1,666 2,920

1967/68 767 450 3,717 1,880 3,195

1968/69 855 530 4,067 2,105 3,500 2

1969/70 950 620 4,434 2,472 3,810 9

1970/71 1,0145 720 4,849 2,887 14,160 9

1971/72 1,150 820 5,329 3,367 14,550 9

i/Averaged for revenue calculations

Annex IPage 2

iAANILA ELECTRIC COiHPANY

TABLE 2

Sales by Category of Consumer(millions of kwh)

Domestic Commercial Industrial OtherCalendar % of % oof % of

Year Sales Total Sales Total Sales Total Sales Total Total

1955 239 38 182 29 126 20 80 13 627

1956 269 36 204 27 170 23 101 14 744

1957 309 33 229 25 257 28 131 14 926

1958 351 32 250 23 329 31 148 1k 1,078

1959 397 31 278 22 436 35 154 12 1,265

1960 458 312 313 21i 513 35 178 12 1,462

-- F O R E C A S T --

1961 487 29 338 20 635 38 204 13 1,664

1962 539 371 716 237 1,863

1963 600 408 791 270 2,069

1964 662 448 865 306 2,281

1965 726 491 939 351 2,507

Sales Comparison(millions of kwh)

Average1955 1960 Annual

Category Sales Percent Sales Percent Increase

Domestic 239 38 458 3121 14%

Commercial 182 29 313 21* 11L5%

Industrial 126 20 513 35 32 B

Other 80 13 178 12 171%

Total: 627 100 1,462 100 17 %

Annex 2

PROVINCIAL SYSTEM

(in megawatts and kwh millions)

Geographical IHIarket AreaYear Aggregate Total Supplied by NPC

(ends 6/30) Demand Energy Demand Energy

1956/57 28 83 3 3

1957/58 33 115 92 34

1958/59 37 155 121 92

1959/60 39 179 22 101

-- F 0 R E C A S T --

1960/61 4o 182 32 149

1961/62 42 209 34 159

1962/63 56 296 46 212

1963/64 76 382 65 300

1964/65 78 390 70 324

1965/66 83 410 74 342

1966/67 88 430 81 374

1967/68 87 402

1968/69 93 430

1969/70 100 462

1970/71 1C8 508

1971/72 116 545

Annex 3

LUZON GRID

Sales and Load(in megawatts and kwh millions)

D e m a n d E n e r g yYear A Annual Supplied Supplied

(ends 6/30) Total Increase(%) by NPC Total Increase(%) by NPC j

1956/57 222 - 80 1,051 - 313

1957/58 262 18 112 1,282 22 383

1958/59 293 12 108 1,522 19 484

1959/60 333 14 163 1,711 13 565

-- F O R E C A S T --

1960/61 381 15 168 1,959 14 830

1961/62 421 11 181 2,204 13 997

1962/63 486 15 196 2,526 15 997

1963/64 555 14 196 2,864 1321 997

1964/65 620 12 320 3,148 10 1,238

1965/66 688 11 420 3,447 10 1,627

1966/67 767 112 477 3,771 10 2,040

1967/68 854 11 557 4,119 9 2,282

1968/69 948 11 666 4,497 9 2,535

1969/70 1,050 11 768 4,896 9 2,934

1970/71 1,153 10 871 5,357 9 3,395

1971/72 1,266 10 984 5,874 9 3,912

1/Aggregate demand (no allowance made for possible diversity)

2/Equals sales by NPC. NPC gross generation is about 8 B greater.

Annex 4

MN.INDLNAO (AGUS) GRID

(in megawatts and kwh millions)

Year Maximum Total Gross(ends 6/30) Demand Sales Generation

1956/57 33.6 145.5 147.3

1957/58 33.0 174.0 176.1

1958/59 33.0 200.6 203.9

1959/60 34h0 176.3 179.3

-- F ORE C AST --

1960/61 35 154 158

1961/62 35 160 164

1962/63 45 213 217

1963/64 54 256 261

196h/65 82 398 4161/

1965/66 109- 499 510

1966/67 164 962 983

1967/68 193 1,126 1,150

1968/69 221 1,319 1,345

1969/70 250 1,404 1,435

1970/71 253 1,410 1,440

1971/72 254 1,416 1,4h5

l/Completion of NASSCO steel complex in 1965Capacity of fertilizer plant doubled in 1967.

Annex 5

ISOLATED (NON-LWTERC &ITh3CTED) \PERATIjIlS

(In megawatts and kwh millions)

Year Aggregate Total(ends 6/30) Demand Sales

i956/57 1.96 9.7

1957,/58 5.66 18.4

1958/59 6.28 26.7

1959/60 8.39 33.4

- F O R E C A S T - -

1960/61 8 32

1961/62 9 37

1962/63 10 43

1963/6h 12 54

1964/65 14 60

1965/66 15 65

1966/67 16 66

1967/68 17 72

1966/69 18 77

1969/70 19 81

1970/71 20 85

1971/72 21 90

Annex 6

SUI¶ LARY - TOTAL NPC SALES

(in kwh millions)

Year Luzon Agus Percent(ends 6/30) Grid Grid Others Total Increase

1956/57 313 145 9 467 _

1957/58 383 174 18 575 23

1958/59 484 201 27 712 24

1959/60 565 176 33 774 9

F O R E C AST --

1960/61 830 158 32 1,020 32

1°61/62 997 164 37 1,198 18

1962/63 997 217 43 1,257 5

1963/64 997 261 54 1,312 5

1964/65 1,238 416 60 1,714 30

1965/66 1,627 510 65 2,202 28

1966/67 2,040 983 68 3,091 40

1967/68 2,282 1,150 72 3,5o4 14

1968/69 2,535 1,345 77 3,957 13

1969/70 2,934 1,435 81 4,45o 13

1970/71 3,395 1,440 85 4,920 11

1971/72 3,912 1,445 90 5,447 11

PHILIPPINES

LUZON GRIDLOAD AND CAPACITY DEVELOPMENT

1600 K -

ooX Assumed future NPC projects k z*

4100 _._ To_ b s e e o_: . . 359

w ~ ~ ~ ~ ~ ~ ~ ~ ~~~T bede costuce byrutin Meac beaC\XDt -8 g. oo o D D ; 0 D t ANPOPOSD r CAPRCICTY

1000 _____ _____~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~1

Under construction by Meralco

(Ii~~~~~~~~~~~~~~~~~~~~~~~~~i

I.-~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~79-

z60

CALNDA NTEARSIT

-J ~~~~~~~~~~~~~~~~~~~~~~~~~~~Effective Capability

Iz . ....... ~~~~~~~~~~~~~~~~~~~~~~~~~~~(T) - Thermnal

(Hf) - Hydro

1958 1959 1960 1961 1962 1963 1964 1965 1966 1967 1968 1969 1970 1971 1972 1973

CALENDAR YEARS zm

AUGUST 1961 IBRD-727RI

PH ILl PPINES

AGUS GRID-MINDANAOLOAD AND CAPACITY DEVELOPMENT

700 _______e__

600 _ _ _ _ _ _ _ _ _

0

£0~~~~~~~~~~~~~~~~~~~~~~

4 500RIA_CRISTIA_UNIS_I_a2 _ ( 5 0 W ) _- _

0 z

0~~16 196 192 16z94 16 96 167 16 99 17 9117

z~~~~~~~~~~- n~~~~~~0c

4000Z

0~~~~~~~~~~~~~~~~~~~~~10 t o z

6 N iz 0 ~~~~~~~~~~~~z I325 MW

wJ _

z 300 z -__ _ _

4 n ~~~~~~~~~~~~~~~~z0 4 CO~~~~~~~~~~~~~~~~~~~~~~~~ 250 MW

2 00 a: 200 mw ~~~~~~~~~~~~~~~~~~System capacity200 I ,'N~~~~~~~~~~~~~~~~~~~~ Aomeplat Rating)-

100 100 MW

MARIA CHRISTINA UNITS I182 (50MW)

1 96 0 1961 19 62 19 63 19 64 1 96 5 19 66 196 7 196 8 1969 1 9 70 1 971 1 97 2

CALENDAR YEARS

AUGUST 1961 IBRD 889

Annex 9

CHARACTERISTICS AND COST OF PLANNED

PLANT ADDITIONS TO THE LUZON GRID

Naeeplate Effective Capacity (MW) Construction PeriodPlant Rating (MW) June December Start Completion

Rockwell No. 7 2 60 69 69 - Dec.'61

Rockwell No. 8 60 69 69 Late t61 Dec.'63

Angat 206 146 217 Late '61 Dec.'64

Thermal 1 75 86 86 June t63 June'66

Thermal 2 75 86 86 June '64 June'67

Tabu 75 50 86 June '65 June'68

Thermal 3 100 115 115 June '66 June'69

Thermal 4 100 115 115 June '67 June'70

Tayum & Kalipkip 45 & 50 108 108 June '68 Junet7l

Thermal 5 100 115 115 June '69 June'72

1 Under construction by Meralco

Plant Assumed NPC Cost ($ millions)

Foreign Local Total

Angat 32.0 27.3 59.3

Thermal 1 10.4 2.6 13.0

Thermal 2 9.6 2.4 12.0

Tabu 15.5 13.4 28.9

Thermal 3 14.0 3.5 17.5

Thermal 4 12.8 3.2 16.0

Tayum & Kalipkip 23.8 20.0 43.8

Thermal 5 12.8 3.2 16.0

Transmission 3.0 8.8 11.8

Others 10.3 3.8 14.1

144.2 88.2 232.4

2/ Excluding interest during construction.

Annex 10

T5CIHTICAL DETAILS OF THE PROJECT

I. ANGAT

General The dam will be 125 meters high, 520 meters wide at the maximumpoint on the base and 525 meters in length along the crest. It will havean impervious inclined earth core with rockfill. The upstream slope frorrriverbed to elevation 203 meters will be 1 to 2.5 and from elevation 203to crest elevation at 220 meters will be 1 to 1.4. The downstream slopewill be 1 to 1.4. Two dikes will fill saddles on the left bank. DikeNo. 1 will be about 410 meters long with a maximum height of about 70 me-ters -and dike No. 2 will be about 70 meters long and 5 or 6 meters high.

The spillway will be located on the left ridge about 4D00 metersback from the left abutment. It will consist of a gated weir discharginginto a concrete chute. The weir will have four bays, each with a 121 me-ter wide by 15 meter high tainter gate installed. The main power intakewill be located upstream of the right abutment to feed a 7.6 meter diameterconcrete lined pressure tunnel 1,380 meters long. A 21.5 meter diametersurge tank will be located at the far end of the tunnel. Undergruund pen-stocks v&ll begin at the surge tank to feed four 50 1IW turbines located ina surface powerhouse about 12 km downstream, as the river flows, of thedam.

Two diversion tunnels will be constructed through the left abut-ment. Each will be 550 meters long, 7.6 meters in diameter, of horseshoesection and concrete lined. This provision will be adequate to divert themaximum recorded flood of August 14, 1960, with a peak discharge of 2,940m3 per second and 24 hour volume of about 140 million m3 . The power in-take to the auxiliary powerhouse, with one 6 iTW turbine initially installed,will utilize one diversion tunnel. Three 115 kv circuits will be builtbetween the main powerhouse and Balintawak substation in Manila.

Hydrology

Runoff records covering 20 full years were calculated for theAngat site by correlation with data compiled as follows:

Drainage Dates ofLocation Area Record

Norzagaray 632 km2 1904/13(23 km downstream) 1918/22

Ipo Dam 623 km2 1945/56(7 km downstream)

Angat 568 km2 1955-present

Correlation was made by assuming a lineal relationship betweenrunoff and drainage area and this relationship was checked for 1955 by

Annex 10Page 2

comparison of simultaneous data of Angat and Ipo and found valid. Theresulting average runoff for Angat was 4.15 million m3 per km2 or 2,357million m3 annually. Variations from average were 163% in 1957 and 66%in 1954.

Design Flood

Design flood studies made by NPC were revised downward by Harzaafter careful review and development of a synthetic unit hydrograph derivedfrom control points on the envelope curve of maximum world rainfall. Har-za's studies indicated that the maximum point rainfall that could occur inthe Angat basin would equal that recorded at Baguio on northern Luzon, fromwhich many of the control points on the world envelope curve, for 24 hourand 88 hour rainfalls, have been derived. The resulting sythetic stormwould produce a 24 hour rainfall of 38.2 inches, 90 hour rainfall of 80.8inches, peak flood of 7,540 m) per second, 6:1 day volume of 1,141 millionm3 and 31 day volume of 923 million m3 . The flood corresponds to a Crea-ger C of 150.

Spillway Capacity

The Angat reservoir will provide some flood storage above norrmaloperating levels. lH1aximum reservoir surcharge with four 12.5 meter wideby 15 meter high spillway gates would be 1.0 meter for the design flood.I4aximum spillway discharge would be about 6,200 m3 seconds. Surcharge of1.0 meter would leave 2 meters of freeboard below the crest of the mainrockfill dam, or 4 meters below the rock parapet.

Sedimentation

The watershed above Angat is heavily wooded and erosion is slight.Consequently the river flow, except during periods of flood is relativelyfree from suspended solids. The flat slope of the river above the damsite (average 0.3%) is another factor against rapid sedimentation. Somedirect measurements have been made at the site which tend to confirm thateffects of sedimentation would be negligible.

Geology

The geology of the project was reviewed in the field by Harzapersonnel during June and July 1960. The results of the Harza investiga-tion generally substantiated the conclusions arrived at by earlier NPC in-vestigations which had been assisted during the period 1954 through 1959by NPC's consultant geologist, the late Irving B. Crosby.

Geological investigations completed by September 1959 included4,400 meters of core drilling at 64 locations, 96 test pits and 40 trenches.The results were adequate for planning purposes and for the conclusion thatthe project was feasible from a geological point of view. Harza recom-mended a program of further investigations for detailed design of the struc-tures consisting of test pits and test blasts, which are presently beingcarried out by NPC.

Annex 10Page 3

Construction Iaterials

Quarry sites have been located upstream of the dam which, withspoil from the spillway excavations, are estimated to be able to provideabout 3 times the rock needed for the dam and dikes.

Borrow areas have also been located near the dam for supply ofimpervious core material and for earthfill of the dikes. More filtermaterial will be required, however, than available near the dam and thiswill be manufactured by crushing as had been done at Binga.

II. IiARIA CRISTINA ADDITION (for future reference)

General

The regulation dam at Lake Lanao will be built in two sections,one on each side of the river, forming extensions of the regulatory outletstructure. The left will be of rockfill with side slope of 2 on 1 andcrest width of 4 meters. It will have a crest length of 30 meters andvarying crest elevations of 705 meters to 704 meters. The right will alsobe of rockfill with side slope of 2 on 1, and will have a crest length of67.5 meters and crest elevation of 702.4 meters.

The regulatory outlet works will consist of a three-bay gatedstructure and dredged approach and outlet channels designed to pass a flowof 94.7 m3 per second when the lake level is at its established minimumelevation of 699.8 meters for this stage of development.

The Linamon River which branches from Agus River at km 30 is adistributary of the Lake Lanao-Agus River System. At present when therequired flow in the Maria Cristina Plant is only 40 m3 per second, thereis a temporary dam across the Agus River, immediately downstream of itsconfluence with the Linamon River, to divert flood flows into the LinamonRiver thus minimizing the flow passing the plant at Ian 36. At this stageof development, this temporary dam will be demolished and a rockfill cof-ferdam across the Linamon River and a dike along the left bank of the AgusRiver immediately below the effluence point will be constructed to confineat least 100 m3 per second in the Agus River.

The crest of the existing rockfill cofferdam which diverts AgusRiver flow into the liaria Cristina intake channel at Ditukalan will beraised by 3.5 meters to elevation 196 meters and will be improved to effectfull diversion into the existing channel of the incoming regulated flowfrom the lake.

The intake structure for Units 4 and 5 will be constructed atthe same time as that for Unit 3. It will be constructed initially up toelevation 197 meters and ultimately to elevation 204 meters during the in-stallation of Units 4 and 5. It will consist of six bays, two for eachunit, but only the two bays for Unit 3 will contain trash racks and in-take gates.

Annex 10Page 4

The power conduit for the third unit will consist of two sec-tions; a 362 meter long by 3.5 meter diameter steel lined cut and coversection and an underground welded steel penstock. A differential type,24 feet in diameter, welded steel surge tank will be connected to thepower conduit. Part of the powerhouse foundations for Units 4 and 5will be included in the present project but only the superstructure forUnit 3 will be constructed at this time. The powerhouse will containone 50 MTT generator driven by a vertical shaft Francis type turbine.Transmission facilities at 69 kv will be constructed to the NASSOO re-ceiving substation as part of this development. The distance is about3.5 kilometers.

Hyrdrology

The flow of the Agus River has been recorded intermittentlysince 1918. The average discharge for 23 years of complete record it asite 23 kilometers downstream of the lake outlet was 4,o05 million mThis corresponds to an average annual runoff of 1.88 million m3 per km2

of drainage area. Variations from average ranged between 55% and 174%.Flood intensities are relatively small due to the high retentive capacityof Lake Iano which has a surface area of about 370 km2 and volume of about5,700 million m3 at the controlled elevation.

The regulated discharge from the lake after completion of thecontrol works will be 94.7 m per second. The corresponding flow avail-able for power generation at the Maria Cristina site will then be 97.2 m3

per second after adding the minimum runoff from the intervening drainagearea. Average power generation of 115 1Mk will be possible at the MariaCristina site with the gross head of 157.5 meters that is available.

ANNEX 11

ANGAT COST ESTfliATE

Cost (thousands)Item Foreign Local Total

('.p) ~~(Ps) (Ps)Production Plant

Land & ROW's - 100 100Structures & Improvements 1,172 6,827 10,343Reservoir, Dams & Waterways 13,303 50,949 90,858Turbines & Generators 4,827 1,064 15,545Accessory Electrical Equipment 558 124 1,798Misc. Powerhouse Equipment 363 51 1,140Roads & Bridges 80 1,040 1,280Village 60 _ 880 1,060

Sub-total 20,363 61,035 122,124

Transmission Plant

Land & ROW's - 220 220Clearing - 20 20Structures & Improvements 1,194 122 3,704Station Equipment 571 90 1,803Towers, Poles & Fixtures 758 524 2,798Overhead Conductors 332 240 1,236

Sub-total 2,855 1,216 9,781

General Plant

Communications Equipment 300 60 960

Sub-total 300 60 960

Sub-Total Direct Cost 23,518 62,311 132,865

Contingencies (15%) 3,582 9,689 20,435Price Increases (10%) - 6,500 6,500Engineering & Supervision 2,100 6,500 12,800

Total Construction Cost 29,200 85,000 172,600

Deduct NWSA Contribution - 21,500 21,500

Add Interest During Construction 4,800 1,500 15,900

Total NPC Cost 1/ 34,000 65,000 167,000

1/ Includes an allowance of Ps 6 million for NPC owned constructionequipment that would be used on the job.

ANNEX 12

COMPARISON OF ANGATWITH EQUIVALENT THERMAL PLANT -

Thermal Hydro

Capacity (MW) 150 206Cost per kw (Ps) 2/ 555 811Total cost to NPC (Ps millions) - 83 167Additional hydro investment 84

Gross generation (kwh millions) 673 673

Cost of Operations (Ps thousands)

Fuel Y 9,900Operation and maintenance 1,210 340Administrative and general 1,170 2,030Depreciation (5% Sinking Fund)

Thermal (30 years) 1,250 _Hydro (50 years) __- 800

Total Cost 13,530 3,170

Indicated return on additional hydro investment

13,530 - 3,170 - 12.3%84,000

1/ A 2 x 75 INW unit thermal station would be most nearly equivalent toAngat in meeting the system load requirements while still providingadequate system reserve capability.

2 Capital costs of hydro include transmission. Interest during construc-tion included for both hydro and thermal. Thermal costs are the sameas those used in NPC's plant expansion program for future thermal ad-ditions.

3/ Gross generation of 673 million kwh would represent a plant factor ofabout 51% for the equivalent thermal plant of 150 1W rating which isreasonable for conditions of the NPC system.

4/ Fuel price assumed Ps 1.40 per million btu (price before decontrol Ps1.26 per million btu). Heat rate assumed 10,500 btu per kwh gross.The effect on the future price of fuel to result from the decontrolplan is not known. However, since any adjustment would be toward higherpeso costs per ton of crude oil, the price assumed (equivalent to US47 per million btu) is to the benefit of the thermal alternative. Theindicated return on the additional hydro investment is thus probably onthe conservative side.

5/ The indicated return on the additional hydro investment would be re-duced to about 10% if NPC were to bear all costs of the project i.e.if NWSA were not contributing Ps 21.5 million for water supply.

N A T I O N A L P O W E R C O 0 T IL O N

M A N I L A

Balance Sheets 1957-58 to 1971-72(In millions of Pesos - Rate of exchange: U841 = Ps 2 until 1961, Ps 3 thereafter)

--------- A C T U A L --------- ------------------------------------ F 0 R E C A S T ----------------------------------------Fiscal year ending June 30 1 1 1960 1961 163 1962 1964 1967 1968 1969 1972

ASIETS

Fixed assets in operation 169.70 170.37 264.80 269.30 290.95 304.76 337.92 498.92 555.58 598.65 640.38 755.09 818.66 876.14 1,020.76

Less: Depreciation reserve 5.46 7.35 9.86 12.78 17.78 23.15 28.81 36.90 46.59 58.76 72.28 88.34 106.48 126.47 149.32

Net fined assets in operation 164.24 163.02 254.94 256.52 273.17 281.61 309.11 462.02 508.99 539.89 568.10 666.75 712.18 749.67 871.44

Sur,eys, work in progress et. 368 77.38 13.19 13.62 68.70 118. 193.79 -107.48 _1. 146.8Q 1.7 2S. _1.

Total net fixed assets 199.92 240.40 268.13 270.14 341.87 419.72 502.90 569.50 620.79 691.45 744.39 813.55 908.97 980.21 1,030.64

liet fertilizer investment 13.10 12.10 10.99 15.20 13.98 12.76 11.54 10.32 9.10 7.88 6.66 5.44 4.22 3.00 2.40

Not cuorent and other assets 16.89 10.73 12.72 15.27 14.57 5.33 2.25 3.32 6.39 4.20 5.31 5.89 8.91 9.33 8.79

Sinking fund assets - - -_ 14.13 14.62 15.13 16.05 17.19 8.37 19.69 21.06 2 .4824.34 29.80 35.69

T3C7AJ A23ETS 229.91 263.23 2-1. 314.74 385.04 452.94 532.74 600.33 654.65 723.22 777.42 S47.436 946.44 1,022.1g 1,A77.5

LIA3ILITIES

EquityCapital stock issued - - 92.00 233.46 238.46 250.00 250.00 250.00 250.00 250.00 250.00 250.00 250.00 335.34 335.34

Interest accrued on debttransferred to equity - - - - 8.97 18.14 27.74 37.34 46.94 56.54 66.14 75.74 85.34 - -

Reserves aRd net surplus 12.19 15.37 11.02 16.78 21.91 28.68 37.43 51.64 65.99 82.36 101.88 126.02 150.85 174.56 199.40

Total Equity 12.19 15.37 103.02 250.24 269.34 296.82 315.17 338.98 362.93 388.90 418.02 451.76 486.19 509.90 534-74

DebtForeign currency loans 32

Export Import Bank loan 34.55 32.52 30.49 28.46 26.43 24.40 22.37 20.34 18.31 16.28 14.25 12.22 10.19 8.16 6.13

ILRD loan 183-PH: Binga 6.81 25.16 32.81 36.04 52.79 51.38 49.88 48.29 46.60 44.81 42.92 40.90 38.76 36.49 34.09

Proposed IBRD loan: Angat - - - - 25.47 56.02 86.60 100.76 98.22 95.54 92.70 89.70 86.53 83.18 79.63

War reparations loan - - - - 6.12 9.22 8.12 7.02 5.92 4.82 3.72 2.62 1.52 .42 -

Future loans: Maria Cristina 3 - - - - 4.89 8.96 10.66 11.15 10.85 10.53 10.19 9.83 9.45 9.05 8.63

Agus 2 - - - - - 6.14 13.70 19.31 18.86 18.38 17.88 17.35 16.79 16.19 15.56

Other foreign loans .62 .62 - - - - 6.24 24.48 62.96 108.96 142.74 187.98 242.01 278.95 306.74

Sub-Total 41.98 58.30 63.30 64.50 115.70 156.12 197.57 231.35 261.72 299.32 324.40 360.60 405.25 432.44 450.78

Local currency loans 181.93 197.46 136.56 - - - 20.00 30.00 30.00 35.00 35.00 35.00 55.00 80.00 92.00

Less: Sinking fund assets / (6.19) (7.90) (11.04) -

Sub-Total 175.74 189.56 125.52 - - - 20.00 30.00 30.00 35.00 35.00 35.00 55.00 80.00 92.00

Total Debt 217.72 247.86 188.82 64.50 115.70 156.12 217.57 261.35 291.72 334.32 359.40 395.60 460.25 512.44 542.78

TOTAL LIABIL1TIES 229.91 263.23 291.84 314.7 3854 52.94 532.74 60.33 7 777. 847.36 _L6. 1_

J Reflecting the estimated effects of the transfer of Government debt to equity and the estimated cash flow during the year as final audited data for the fiscal year are not available yet.

2/ It has been assumed that the sinking fund created for repayment of the debt transferred to equity in 1960-61 would be kept on N.F.C's books and would continue accruing at 3% per annum until

1970; from 1960-61 on it is therefore shown as an asset rather than a deduction from the long term local currency debt.

]/ Ps 158 million of the authorized, issued share capital will be repayable after July 1, 1970; see p. 13, para. 65.| The exchange rate of US$1 = Ps 2 will remain applicable throughout the life of the loan.i/ The present free exchange rate of US1 = Ps 3 will be applicable from 1961-62 on; the loan amount still outstanding was revalued at the new rate; it has been assumed that fixed assets would

be revalued to the same extent.

N A T I O N A L P O W ER C o R P o R A T I O N

MA N I L A

Income Statements 1957-58 to 1971-72(In millions of Pesos - Rate of exchange US$1 = Ps 2 until 1961, Ps 3 thereafter)

------- A C T U A L ---------- -------------------------------------- F O R E C A S T ------------------------------------------Fiscal vyr end June30: 1958 1S 1960 1961 /1962 196 1964 1965 1966 1967 1968 1969 1970 1971 1972

Sales in millions of KWH 576 712 774 941 1,194 1,253 1,307 1,696 2,191 3,070 3,480 3,931 4,419 4,890 5,418

Operating revenues 11.19 14.37 17.21 23.91 27.11 30.44 33.35 42.27 53.68 68.10 78.87 89.32 101.57 113.99 126.74

Operating costs:

Operating expenses 1.67 2.12 2.61 3.78 4.14 4.68 4.91 5.57 5.80 14.03 18.85 18.73 26.34 35.26 38.96Real estate tax .18 .51 .31 1.29 1.31 1.32 1.37 1.89 2.19 2.36 2.47 3.01 3.11 3.27 3.67

Depreciation 1.79 1.95 2.52 2.92 5.00 5.37 5.66 8.09 9.69 12.17 13.52 16.06 18.14 19.99 22.85

Total operating costs 3.64 4.58 5.44 7.99 10.45 11.37 11.94 15.55 17.68 28.56 34.84 37.80 47.59 58.52 65.48

Operating income 7.55 9.79 11.77 15.92 16.66 19.07 21.41 26.72 36.00 39.54 44.03 51.52 53.98 55.47 61.26

Other income (net) (.07) .12 .24 .91 .84 .77 .69 .62 .55 .47 .40 .33 .25 .18 .14