staff appraisal report eritrea ports rehabilitation...

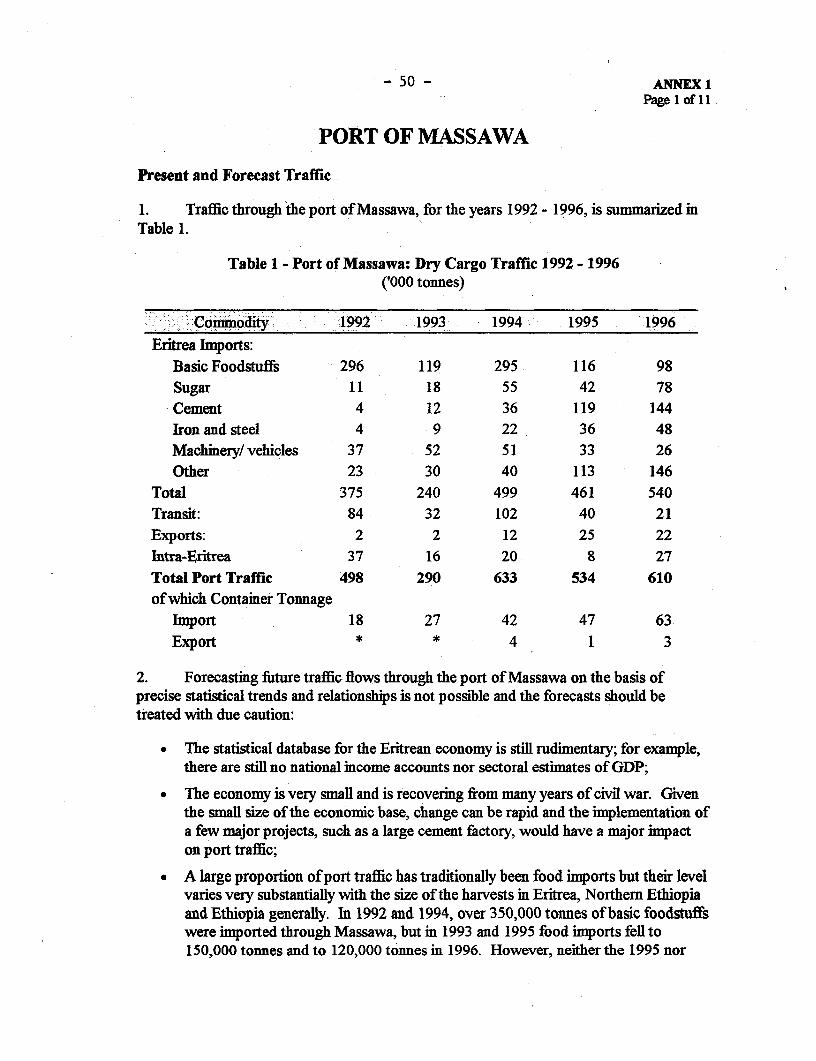

TRANSCRIPT

Document of

The World Bank

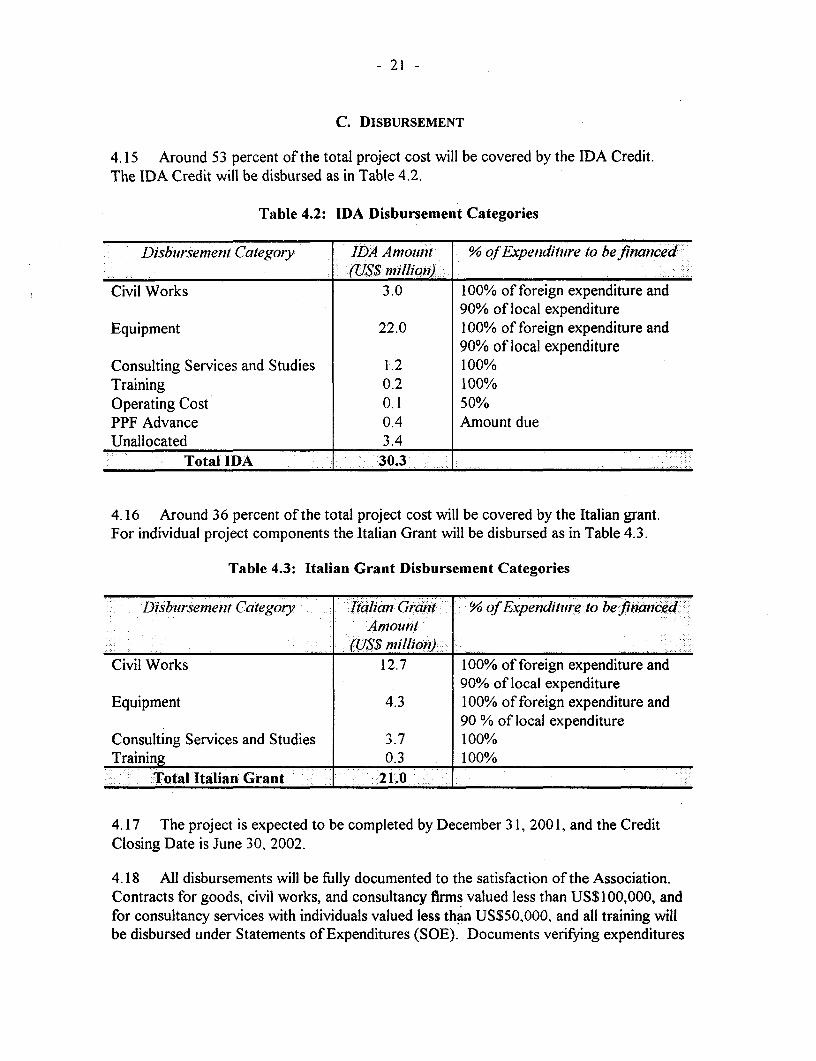

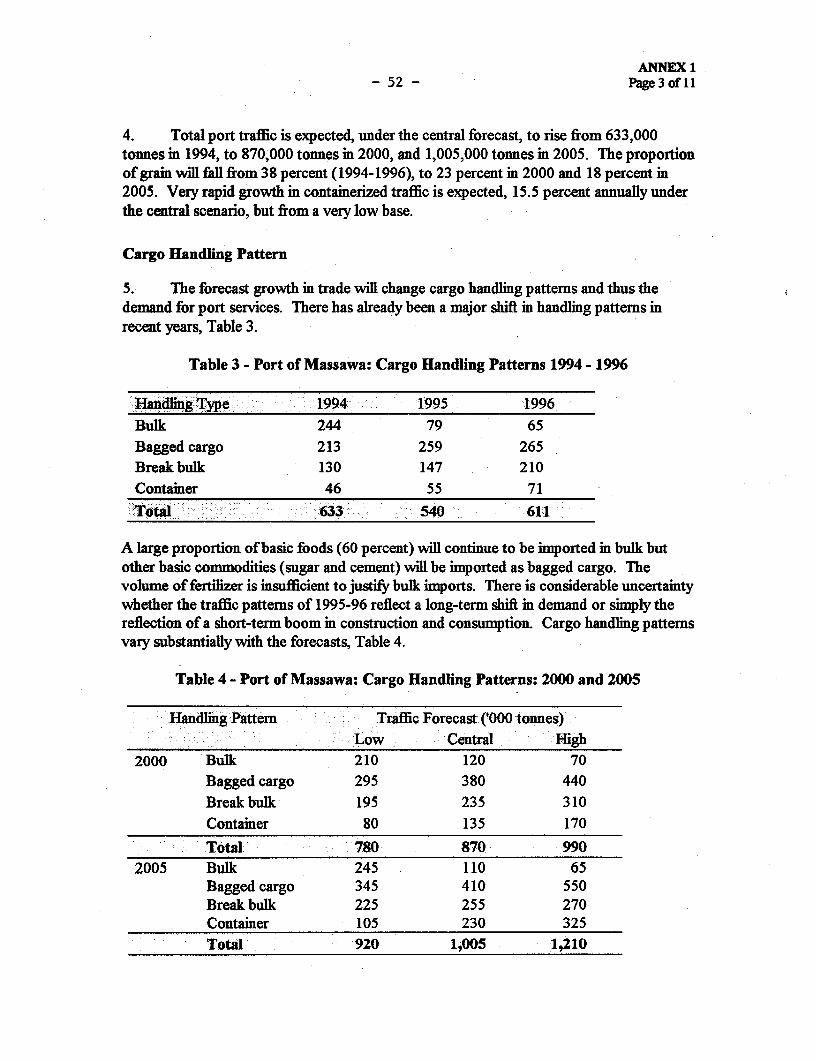

Report No. 15547 ER

STAFF APPRAISAL REPORT

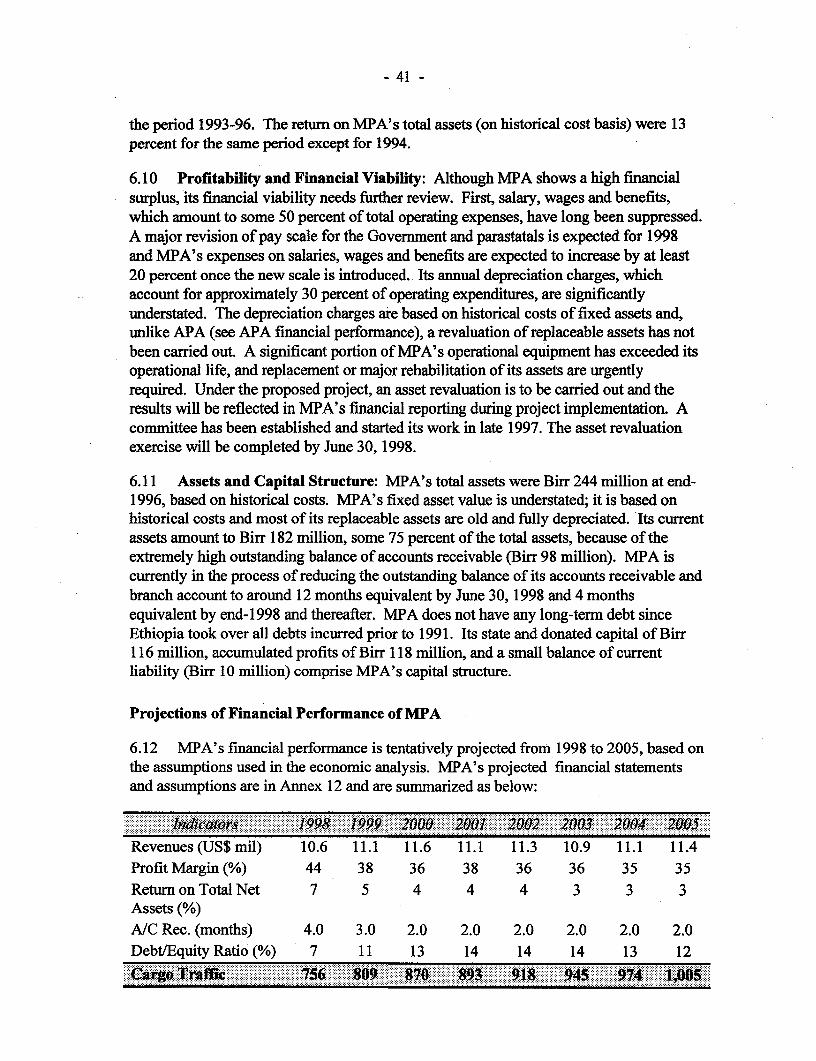

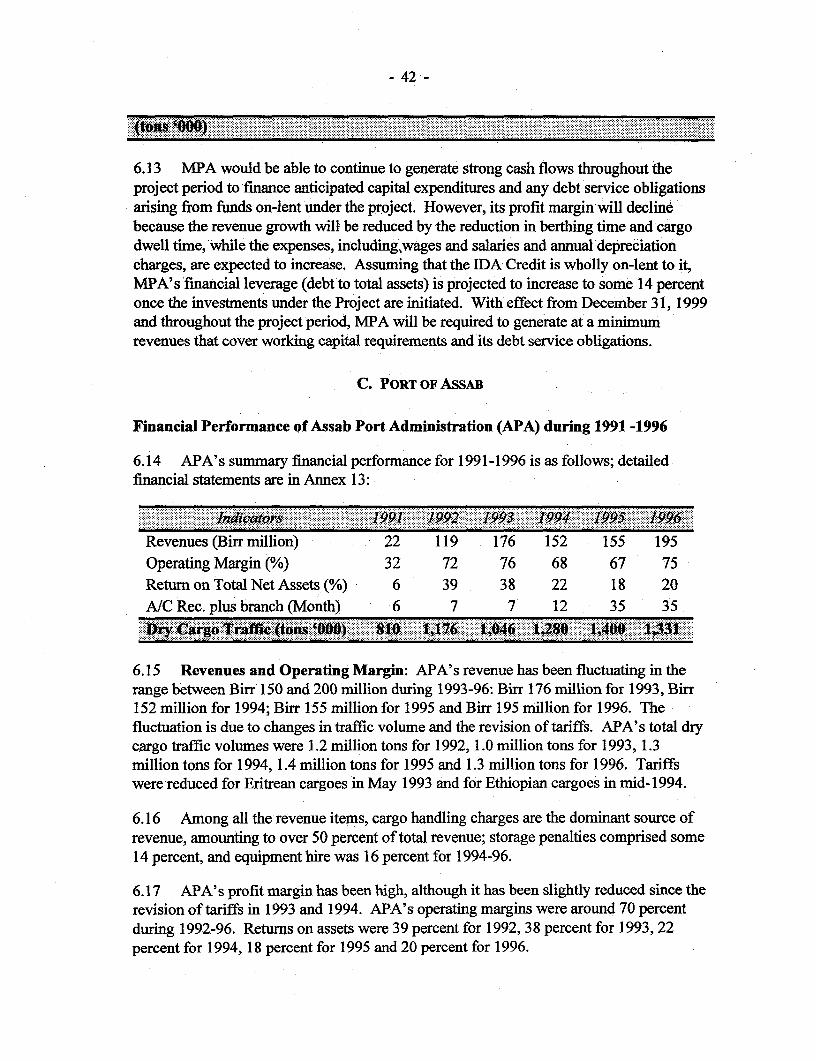

ERITREA

PORTS REHABILITATION PROJECT

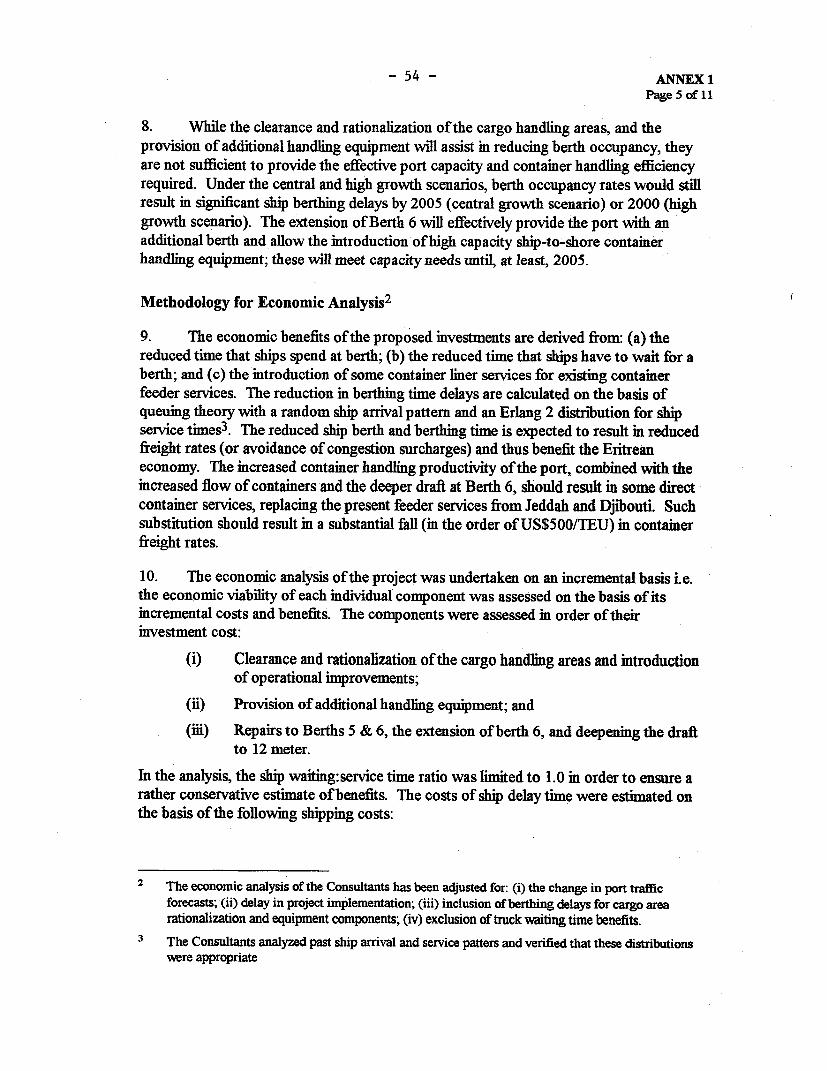

October 20, 1997

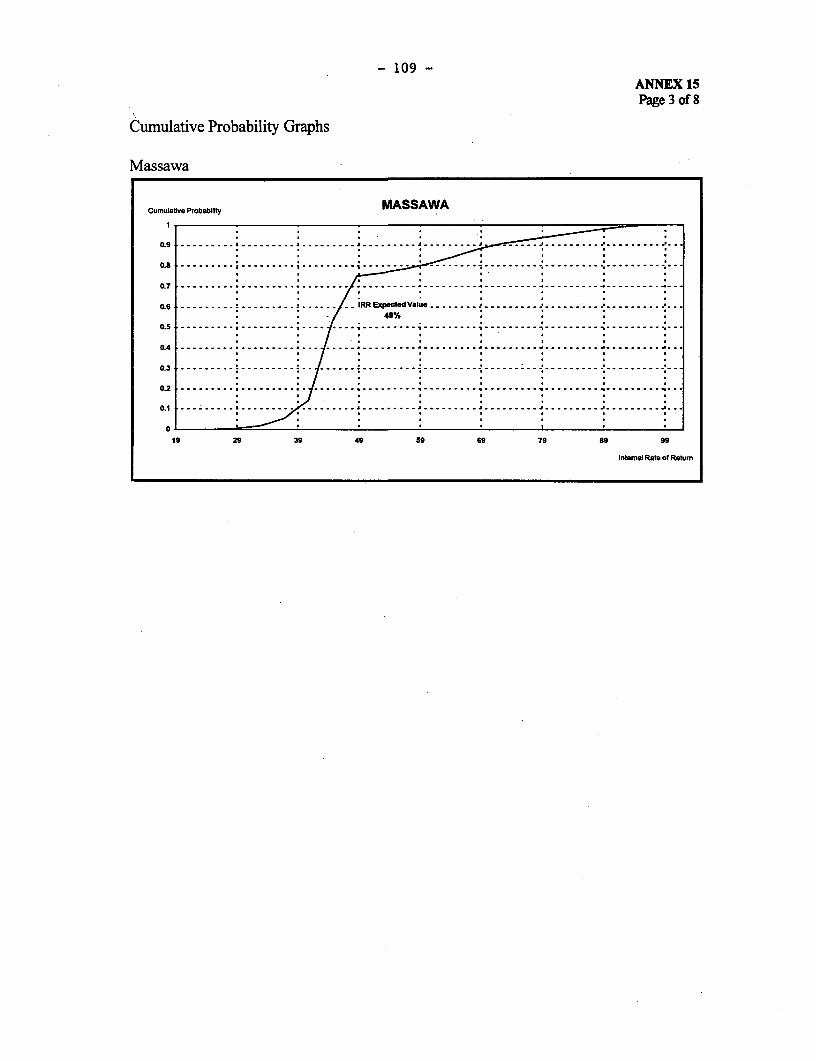

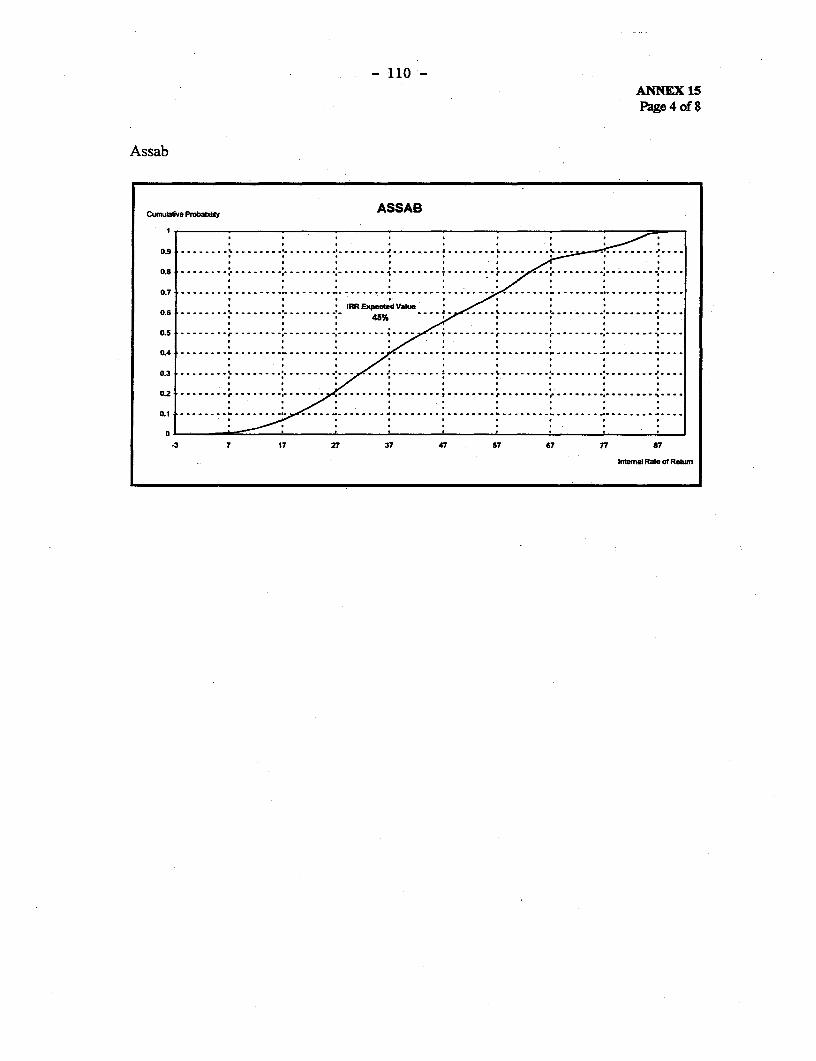

Transport 1Eastern and Southern Africa

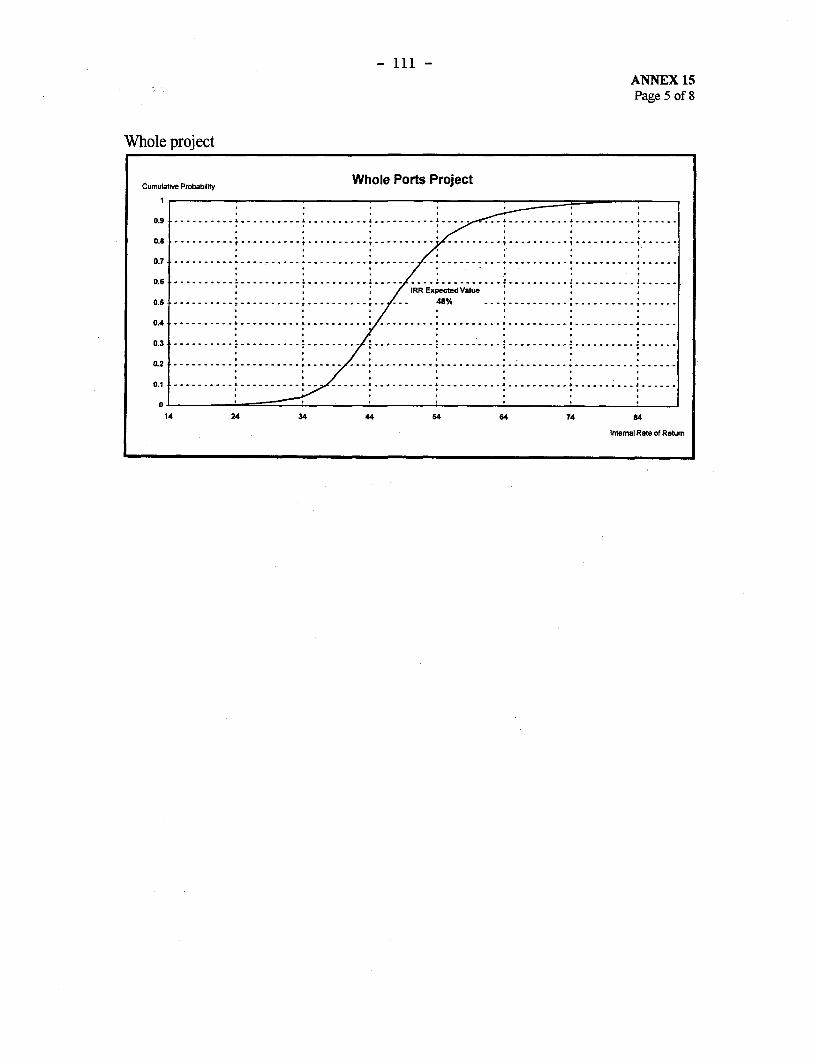

Pub

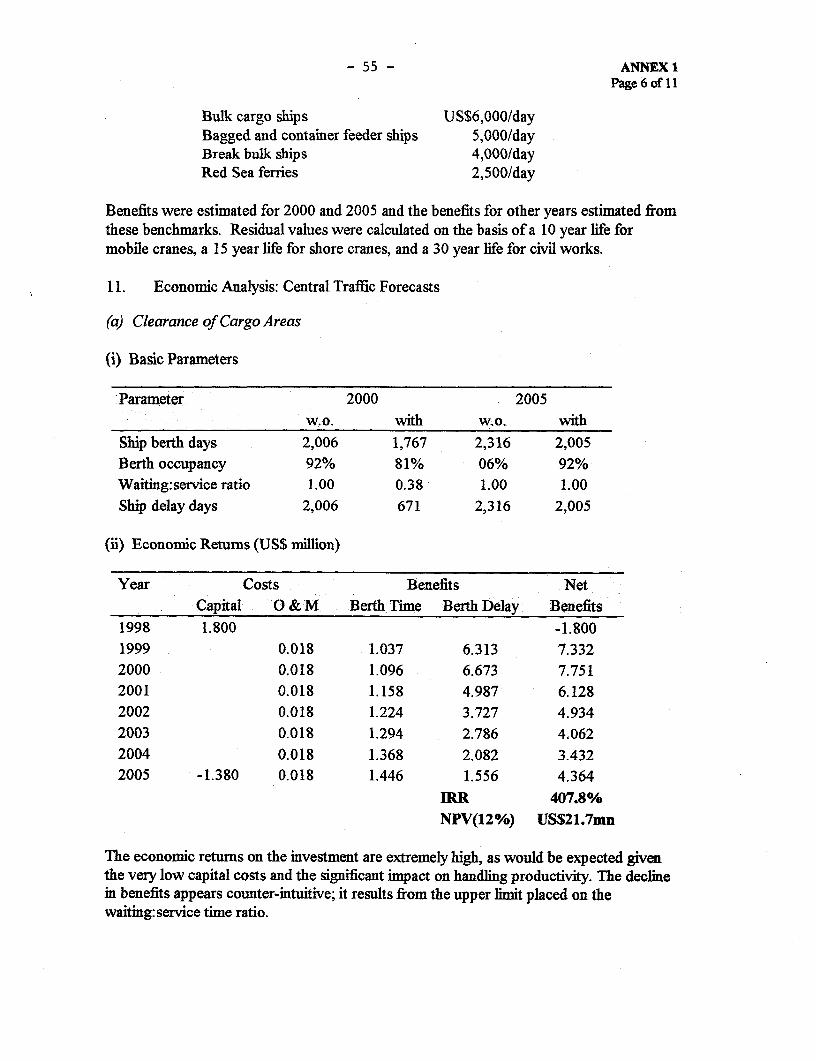

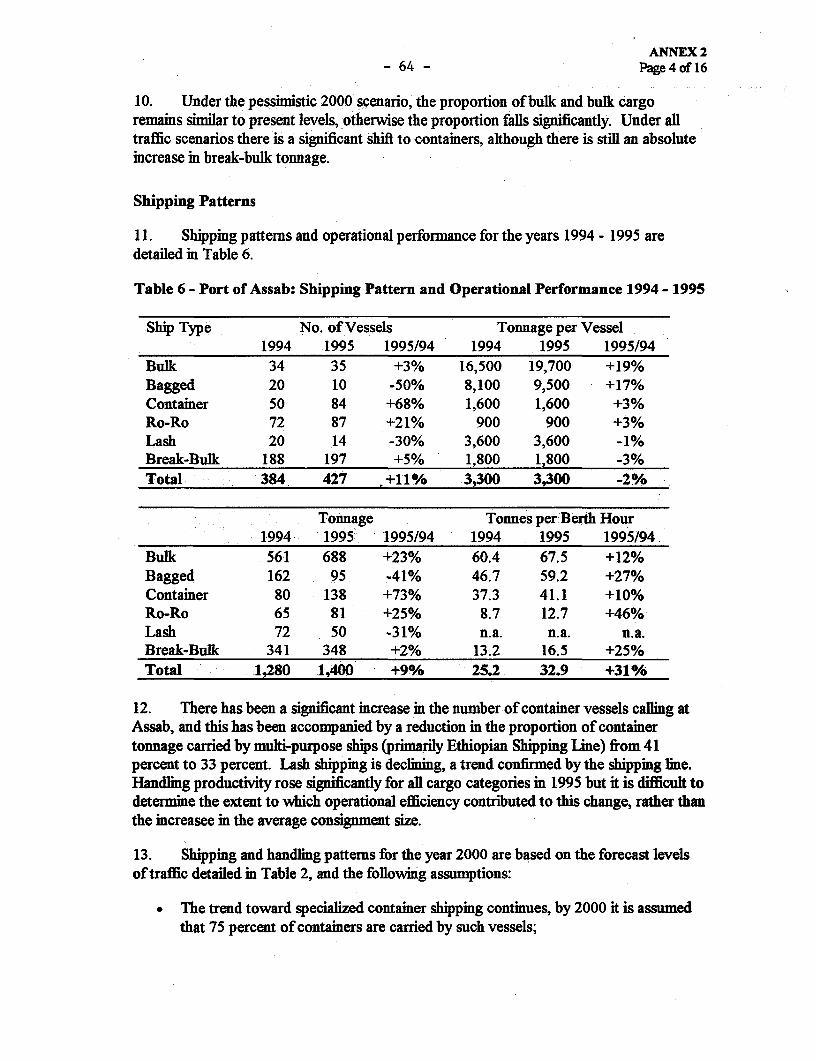

lic D

iscl

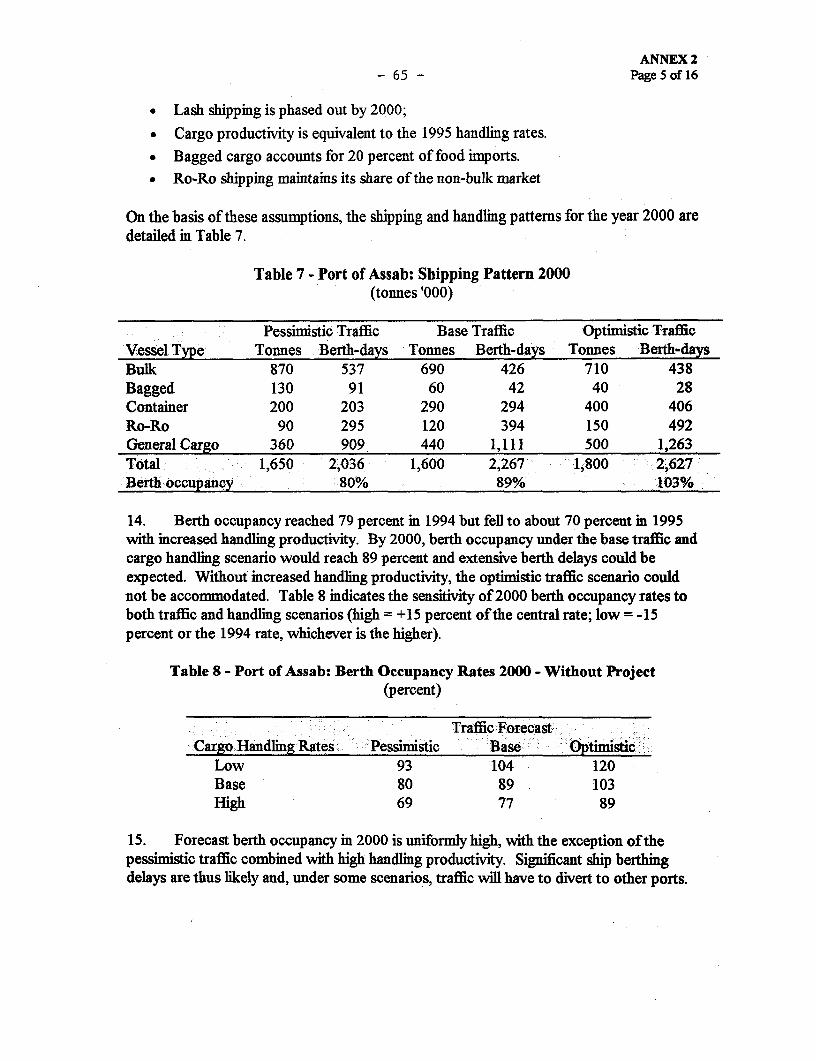

osur

e A

utho

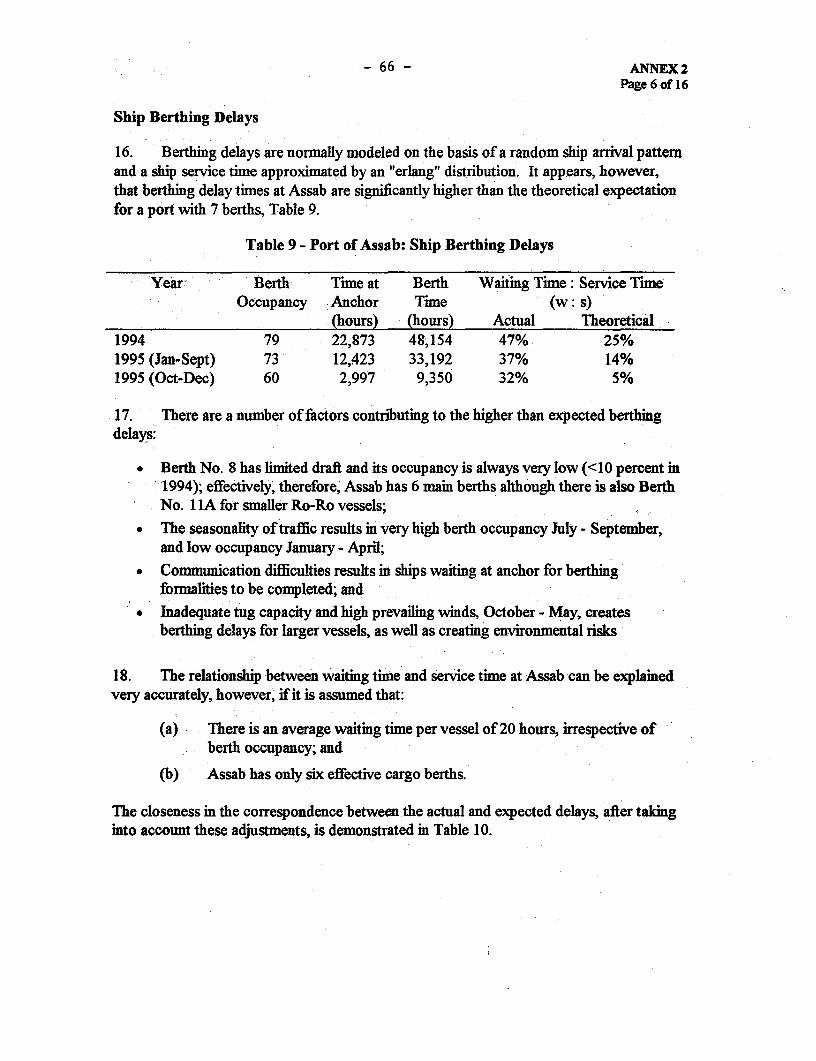

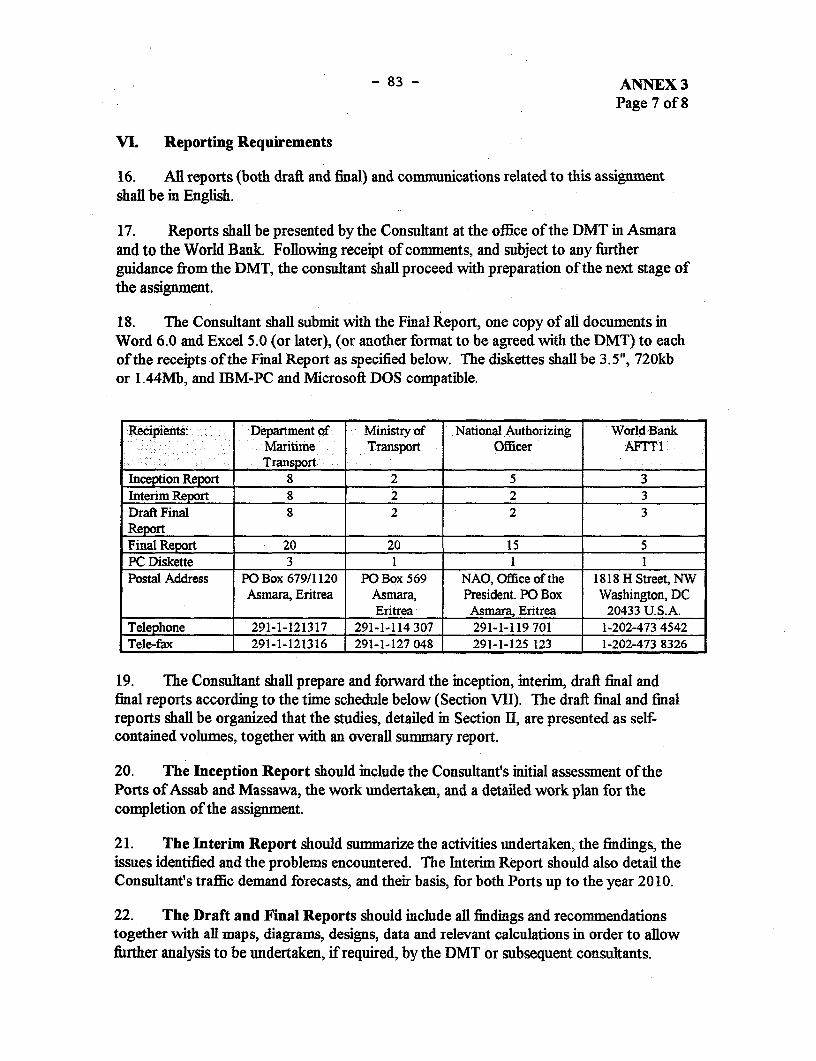

rized

Pub

lic D

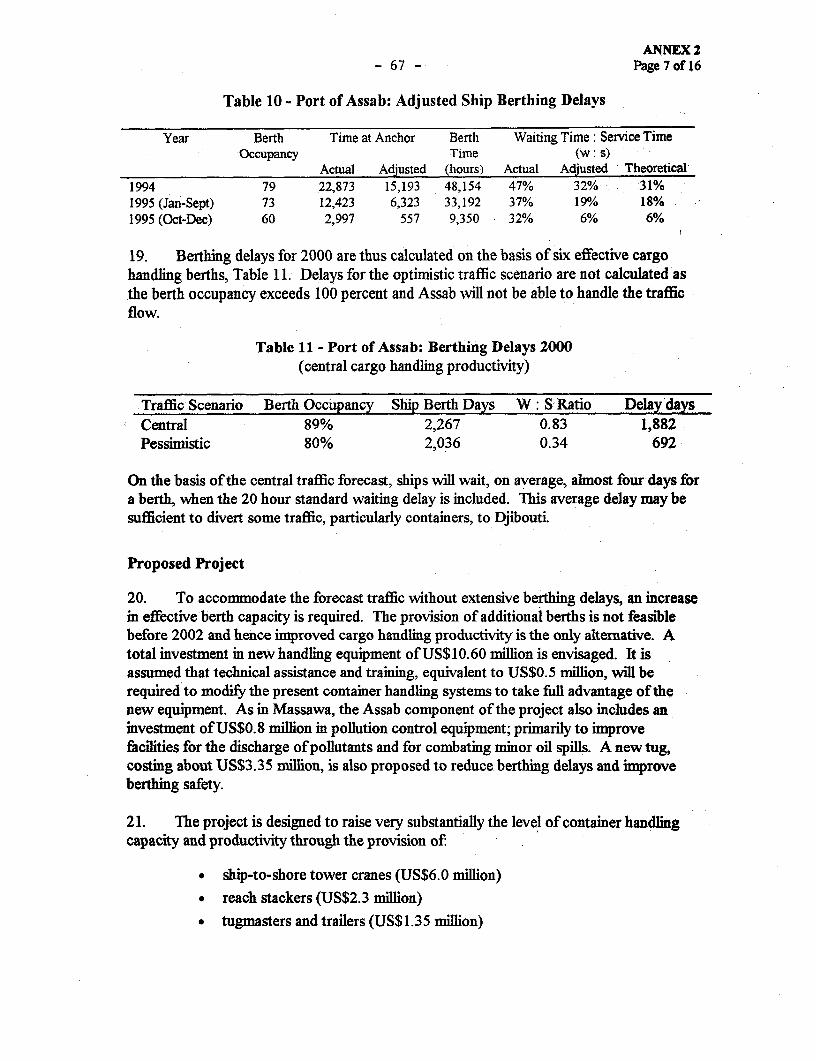

iscl

osur

e A

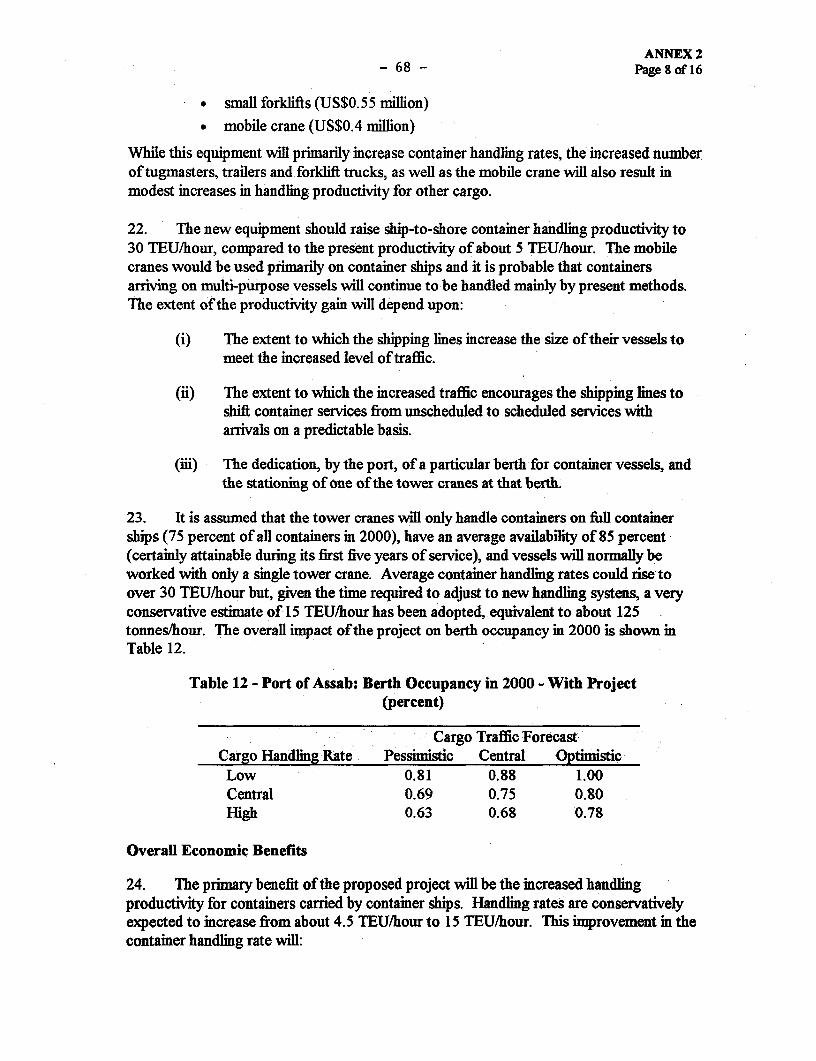

utho

rized

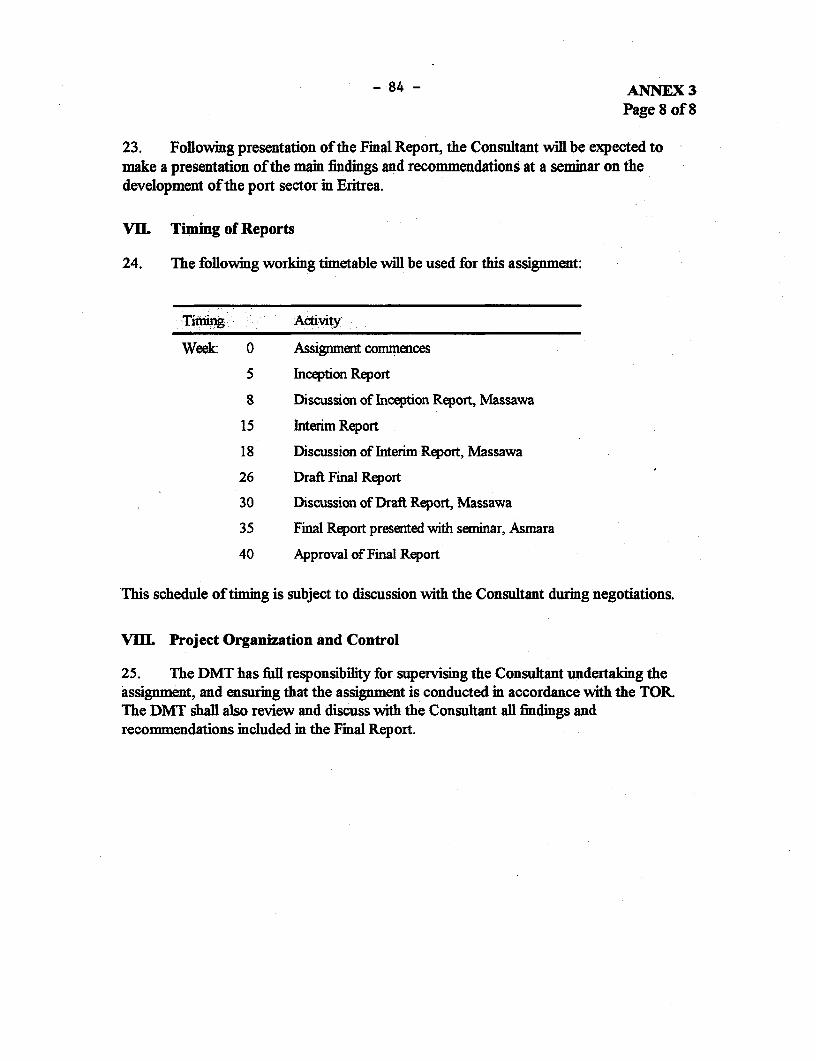

Pub

lic D

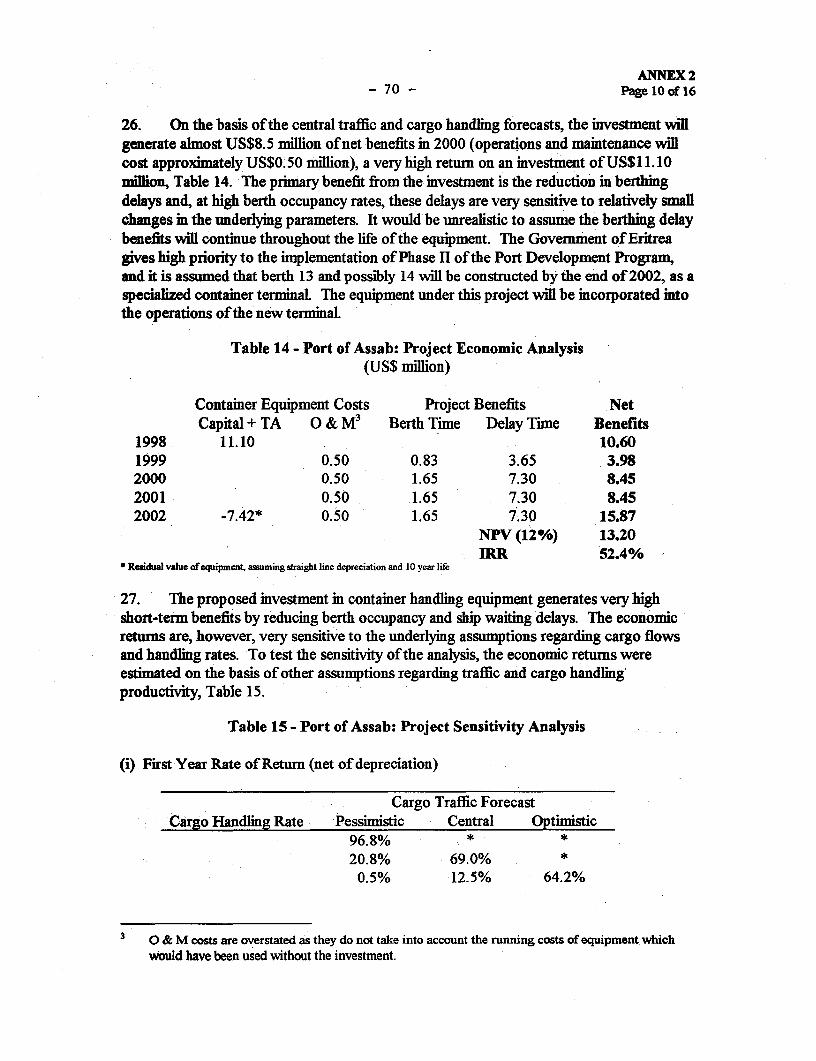

iscl

osur

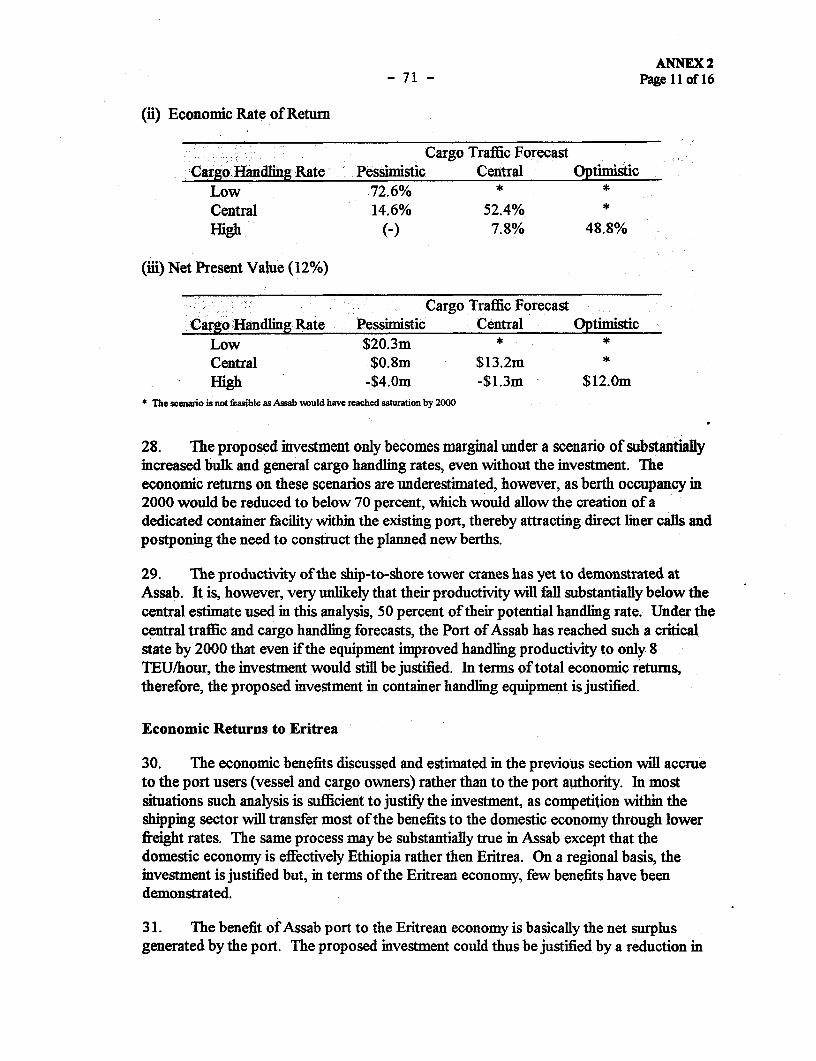

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency unit = BirrUS$ 1.00 = Birr 6.30 (As of June 1996)Birr I.00 US$ 0.16

WEIGHT AND MEASURES

Metric System

GOVERNMENT FISCAL YEAR

January 1 - December 3 1

GLOSSARY OF ABBREVIATIONS

APA Assab Port AdministrationASYCUDA Automated System for Customs DataDMT Department of Maritime TransportEA Envirorunmental Impact AssessmentEPA Eritrea Ports AuthoritvEPDP Eritrea-Gernan Port Development ProjectEPLF Eritrean Peoples' Liberation FrontERSTAS Eritrean Shipping Transit Agencies ServicesEU European UnionGOE Govermnent of EntreaGRT Gross Register TonsGTZ Deutsche Gesellschaft fiir Technisclie ZusammnenarbeitICB International Competitive BiddingICR Implementation Completion ReportIDA International Development AssociationIFC International Finance CorporationIMF International Monetary FundIMO International Maritime OrganizationMTC Ministry of Transport amd CommunicationMPA Massawva Port AdministrationNCB National Competitive BiddingPCU Project Coordination UnitPIP Project Implementation PlanPPF Project Preparation FacilityRo/Ro Roll on -Roll offRRPE Recovery and Rehabilitation Project for EritreaSDR Special Drawings RightsSOE Statement of ExpensesTEU Twenty Foot Equivalent Unit (containers)UNCTAD United Nations Conference on Trade and DevelopmentWFP World Food Program

This report is based on the findings of 13ank's pre-appraisal, appraisal and post-appraisal missions in January 1996, April1996, and April 1997 respectively. Thc mission members included: Mr. Sturc Karlsson (Task Manager -Sr. Port rngincer);Mr. Simon Thomas (Sr. Transport Economist); Mr. Takuya Kaniata (Sr. Financial Analyst); Ms. Charlotte Jones (OperationsAnalyst); Mr. RolfBolin (Port Management and Operations Expert- Consultant); Mr. Norbert Zimmert (luman ResourcesDevelopment Expert -Consultant); and Dr. Klaus Beplat (Port Operations and Management Specialist -Consultant). Leadadvisor for the project was Mr. Ismail Mobarek (Principal Port Engineer), and peer reviewers werc Mr. Kek Chung (Sr. PortOperations Specialist), Mr. Joris Van der Ven (Sr. Transport Economist) and Mr. Carl G. I.undin (Environmental Specialist).Secretarial support and report production was done by Ms. Marie Claire Li Tin Yue, Task Assistant. Mr. Yusupha Crookesand Ms. Oey Astra Meesook are the Sector Manager and Country Director, rcspectively, for the operation.

ERITREA

PORTS REHABILITATION PROJECT

TABLE OF CONTENTSPage No.

CREDIT AND PROJECT SUMMARY ........................................................... ;1. TRANSPORT SECTOR ........................................................... I

A. BACKGROIJND ........................................................... IB. THE ERITREAN TRANSPORT SYSTEM ........................................................... 2C. ROLE OF TRANSPORT IN THE ECONOMY ............................................................ .3D. CRITICAL TRANSPORT ISSUES IN ERITREA ........................................................... 3E. BANK STRATEGY ............................................................. 4F. PREVIOUIS BANK GROUP INVOLVEMENT IN THE ERITREA PORT SECTOR ..................... 5G. RATIONALE FOR IDA INVOLVEMENT ........................................................... 5

2. THE PORT SUB-SECTOR ........................................................... 6A. ORGANIZATI(N ........................................................... 6B. PORT OF MASSAWA ........................................................... 7C. PORT OF ASSAB ............................................................ 10D. STRATEGY FOR THE PORT SECTOR ............................ ............................... 12

3. THE PROJECT ........................................................... 13A. IDENTIFICATION AND PREPARATION ....... ................................... 13B. OBJECTIVES ........................................................... 13C. PROJECT DESCRIPTION ........................................................... 13

Project Components ........................................................... 13D. COST ESTIMAT'ES ........................................................... 15E. FINANCING ............................................................ 16

4. PROJECT IMPLEMENTATION ........................................................... 17A. INSTITUTiONAL RESPONSIBLITIES ........................................................... 17B. PROCUREMEN1 ........................................................... 18C. DISBURSEMENT ............................................................ 2 1D. REPORTING AND A ITING ........................................................... 22E. MONITORING AND SIJPERVISION ........................................................... 22

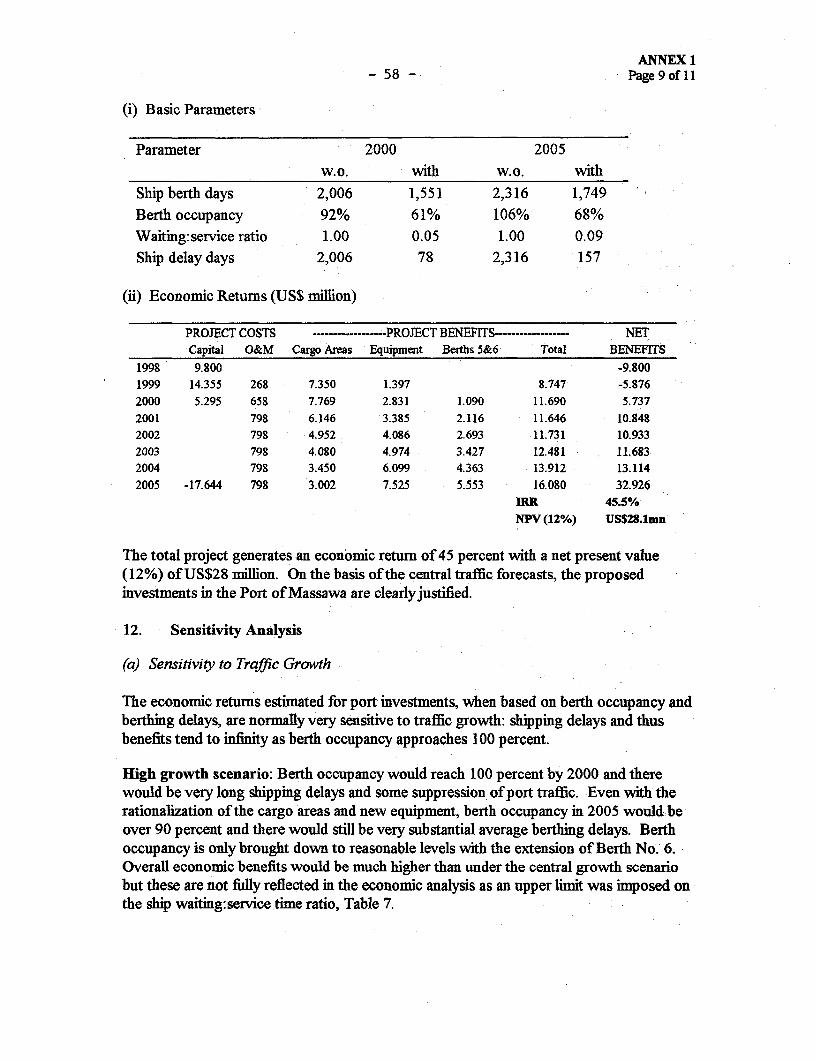

5. ECONOMIC ANALYSIS ........................................................... 24A. BACKGROUND ........................................................... 24B. MASSAWA PORTI INVESSTMENT ................. .......................................... 25

The Demand for Port Services ........................................................... 24Operational Impact of Proposed Investments .................................................... 26Economic Impact of Investments ........................................................... 27Sensitivity Analysis ........................................................... 29

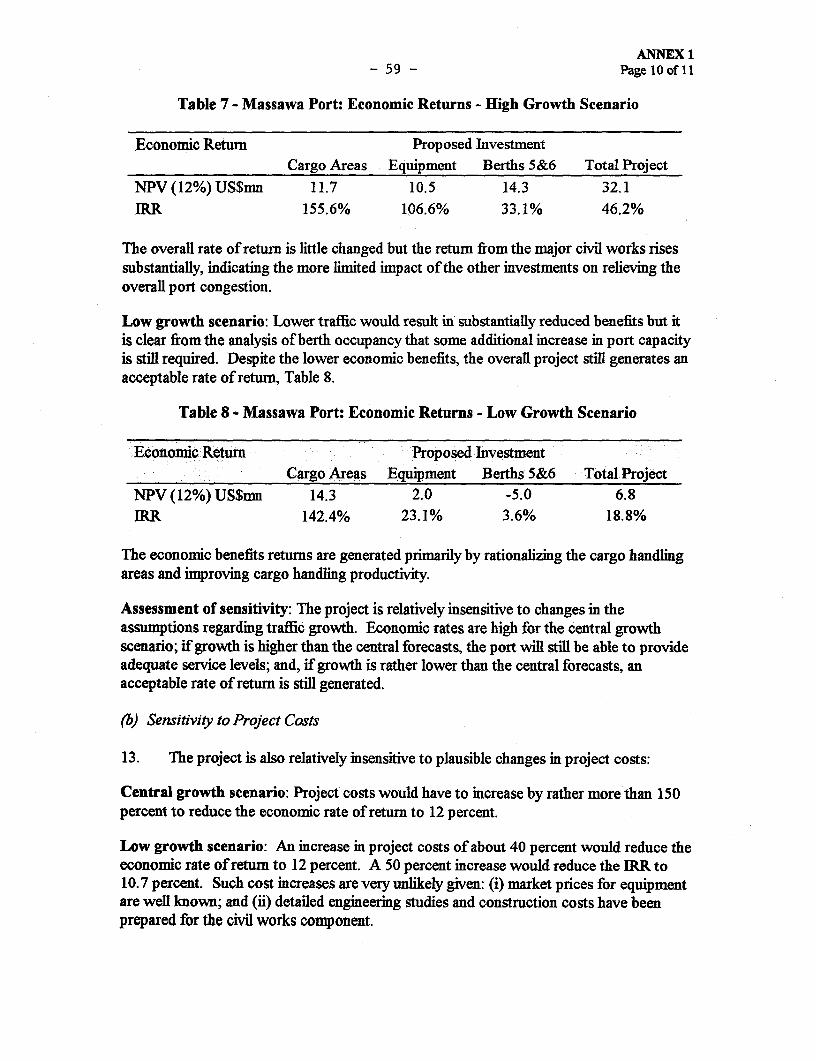

C. ASSAB PORT INVESTMENT ........................................................... 30The Demand for Port Services ........................................................... 30Operational Impact of Proposed Investment ....................................................... 31Economic Impact of Investment ........................................................... 33Sensitivity Analysis for Container Handling ...................................................... 36

D. OVERALL PROJECT ECONOMIC RETURNS ........... ............................ 376. FINANCIAL ANALYSIS ........................................................... 39

A. SECTOR FINANCiAL uISSUES ............................................................. 39

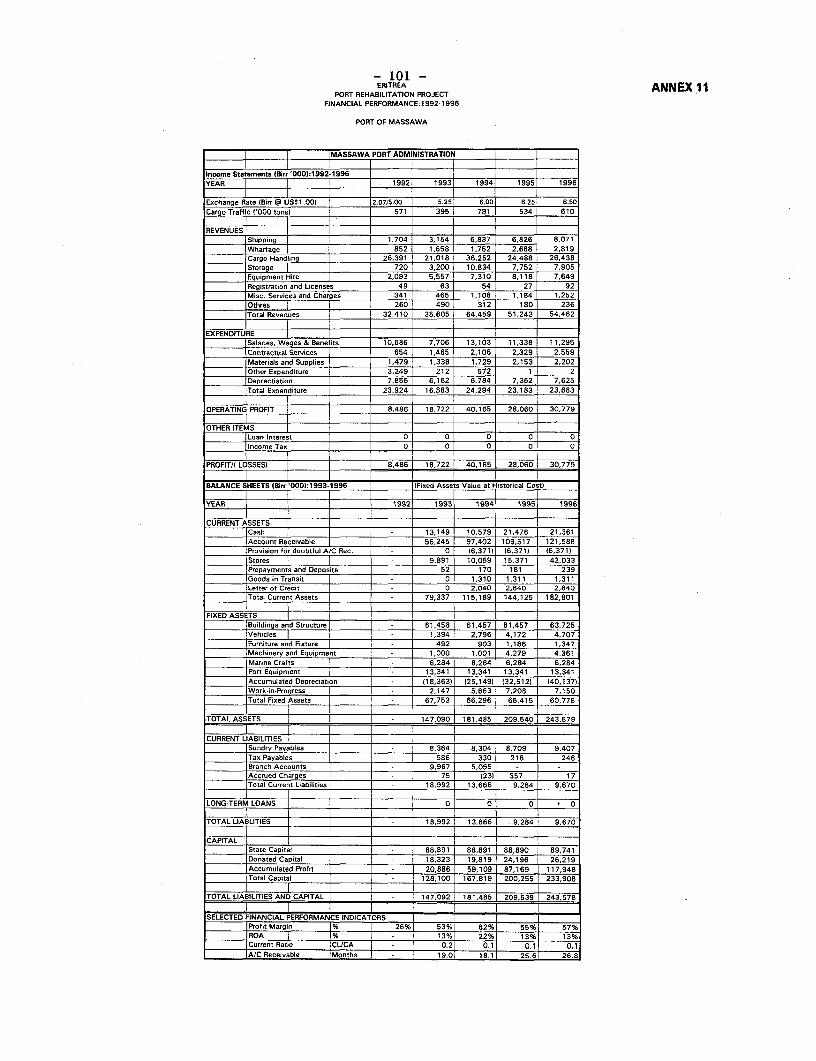

B. PORT OF MASSAWA ............................................................ 40Financial Performnance of the Massawa Port Administrationduring 1992-1996 ............ : 40

Projections of Financial Performance of MPA ................................................... 41C. PORT OF ASSAB ........................................................... 41

Financial Performance of Assab Port Administration (APA)during 1991 -1996 ........................................................ 42Projections of Financial Performance of APA .................................................... 43

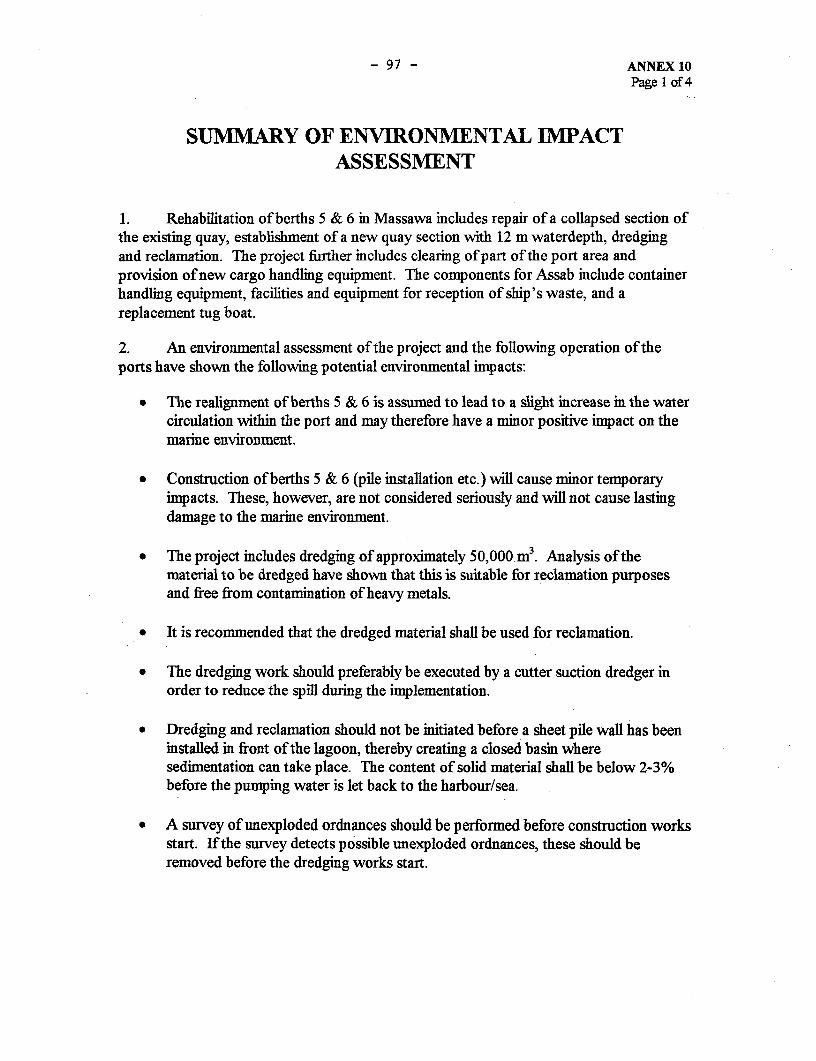

7. ENVIRONMENTAL IMPACT, PROJECT SUSTAINABILITY AND RISK ........................ 45A. ENVIRONMENTAL IMPACT .......................................................... 45

Environmental Impacts During Construction ...................................................... 45Treatment of Hazardous and Noxious Cargo ...................................................... 46Handling of Ship's Wastes ........................................................ 46National Oil Spill Contingency Plan ........................................ ................ 46Maritime Safety ........................................................ 47

B. PROJECT SUSTAINABILITY .......................................................... 47C. PROJECT RISK ........................................................ 47

8. AGREEMENTS AND RECOMMENDATION ........................................... 49A. AGREEMENTS REACHED DURING NEGOTATIONS ....................................................... 49B. RECOMMENDATION ........................................................ 49

ANNEXESAnnex 1 Port of MassawaAnnex 2 Port of AssabAnnex 3 TOR Development StudyAnnex 4 Letter of Port Sector PolicyAnnex 5 Supervision Strategy and Staff InputAnnex 6 Key Performance IndicatorsAnnex 7 Project Implementation Plan (PIP)Annex 8 Estimated Schedule of DisbursementAnnex 9 Project Implementation ScheduleAnnex 10 Summary of Environmental Impact AssessmentAnnex 11 Financial Performance, Massawa Port, 1992 - 1996Annex 12 Financial Projections, Massawa Port, 1997 - 2005Annex 13 Financial Performance, Assab Port, 1991 - 1996Annex 14 Financial Projections, Assab Port, 1997 - 2003Annex 15 Risk AnalysisAnnex 16 Organizational Charts - Massawa & AssabAnnex 17 Documents in Project File

MAP IBRD Nos. 27961 and 27962

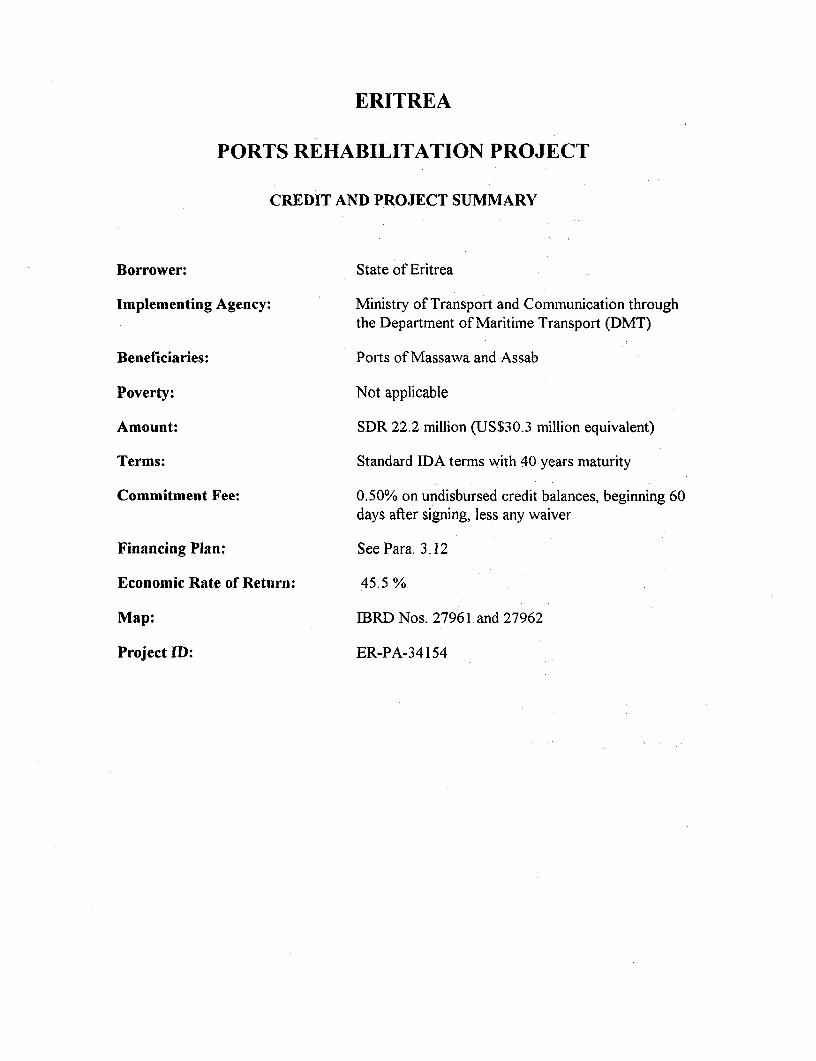

ERITREA

PORTS REHABILITATION PROJECT

CREDIT AND PROJECT SUMMARY

Borrower: State of Eritrea

Implementing Agency: Ministry of Transport and Communication throughthe Department of Maritime Transport (DMT)

Beneficiaries: Ports of Massawa and Assab

Poverty: Not applicable

Amount: SDR 22.2 million (US$30.3 million equivalent)

Terms: Standard IDA terms with 40 years maturity

Commitment Fee: 0.50% on undisbursed credit balances, beginning 60days after signing, less any waiver

Financing Plan: See Para. 3.12

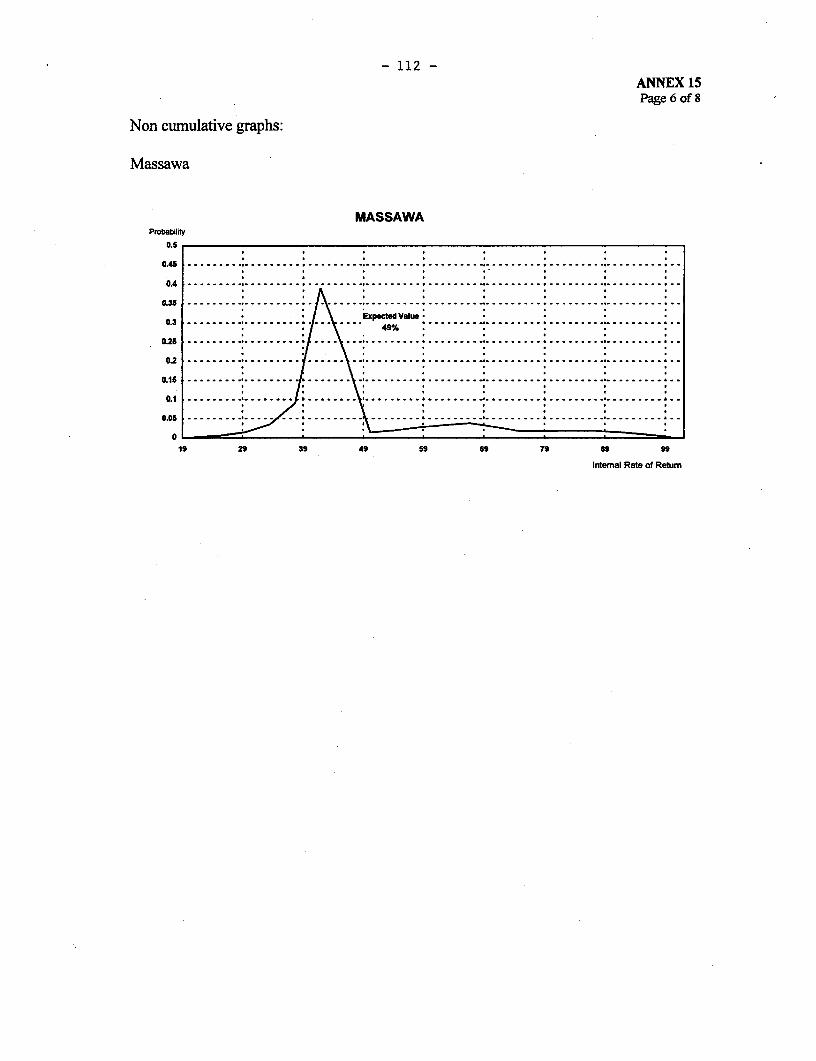

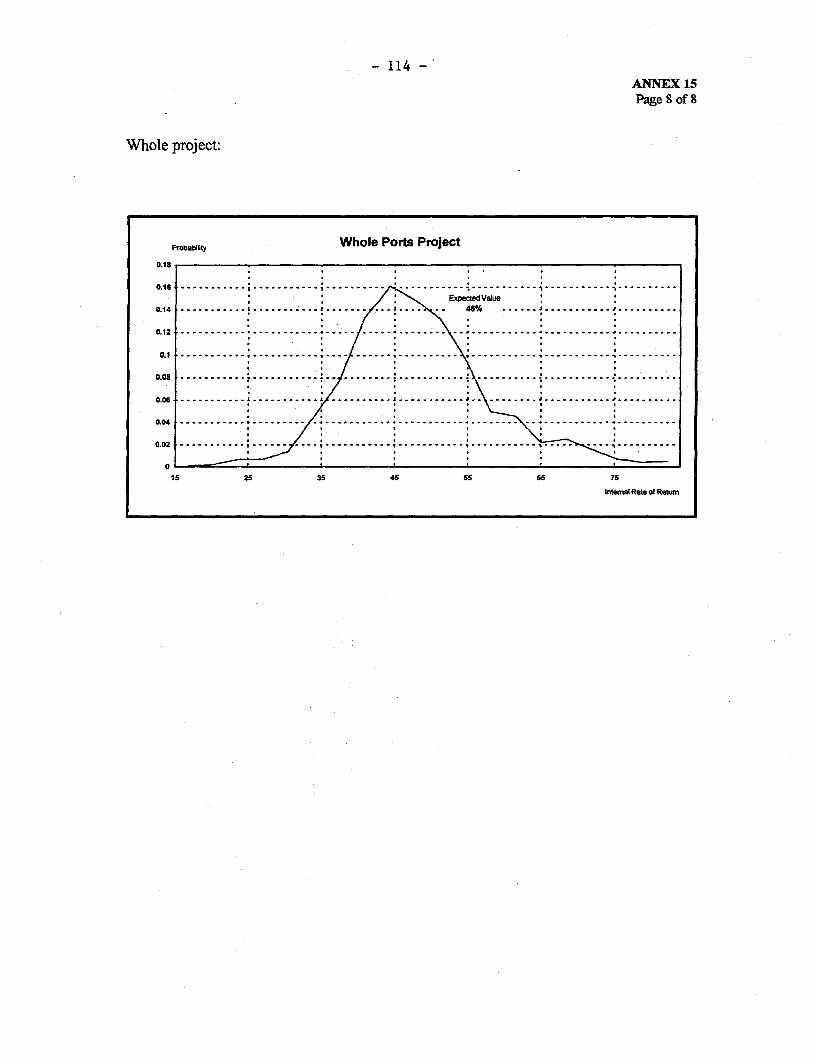

Economic Rate of Return: 45.5 %

Map: IBRD Nos. 27961 and 27962

Project ID: ER-PA-34154

I

1. TRANSPORT SECTOR

A. BACKGROUND

1.1 Eritrea's struggle for independence began in earnest in 1961 following theannexation of Eritrea by Ethiopia, and further intensified following the military coup inEthiopia in 1974. The Eritrean Peoples Liberation Front (EPLF), which had begun tocontrol parts of the country since the mid- 1970s, finally managed to fully liberate Eritreain May 1991. This coincided with the Ethiopian People's Revolutionary DemocraticFront's victory over the military regime in Ethiopia. Following an internationallysupervised referendum, Eritrea formally gained its independence on May 24, 1993.Ethiopia was among the first nations to recognize Eritrea' s independence, and the twocountries have established a close relationship. Eritrea became the 178th member ofIBRD and the 157th member of IDA on July 6, 1994. In October 1995, it became amember of IFC.

1.2 Eritrea is strategically located in the northeast of Africa, with a 1000 km coastlineon the Red Sea. It is a land of varied topography, climate and rainfall, and it lies in theSahelian rainfall zone. There is good potential to extract petroleum from the Red Sea.The country's coastal waters are also believed to be among the most potentiallyproductive fishing grounds in the Red Sea. Eritrea's population is estimated to be in therange of 3-3.5 million, including nearly 500,000 Eritrean refugees in Sudan.

1.3 The Eritrean economy has a relatively diverse productive base. In comparison toother African countries, agriculture accounts for a lower share of the GDP - 15 to 25percent depending on the rainfall. Industry accounts for 20 percent of GDP and itscontribution varies less. Services accounts for the bulk of national output at 50 to 60percent of GDP. The rehabilitation and expansion of these sectors will increase growth inthe medium term. In the long-run, growth will be boosted by the fruits of the on-goingprivate investments in mining, fishery and tourism sectors. These sectors have madeprogress in attracting direct foreign investment.

1.4 The return to peace, the recovery and the rehabilitation efforts, institutionalreforms, and policy developments, have contributed to reviving a run-down economy.After contracting by more than one percent per annum during the period 1985 to 1993,real GDP grew by almost 8 percent per annum on average during 1994 and 1996.Industrial production as well as service activities have continued to expand in the recentpast due primarily to a growing private micro-enterprise sector, the partial rehabilitation ofa few large-scale industrial enterprises, a strong pick-up of construction activity, and agood harvest. Sustaining such high growth rates will require maintaining the momentumtowards improving macroeconomic policies and further strengthening sectoral policies toencourage investment, as well as substantial external assistance.

-2-

1.5 One of the initial successes of the Government's reform and recovery program hasbeen the growth and some diversification in foreign trade. Exports have recoveredsignificantly, starting from an extremely low base, and have increased by almost 50 percentper annum in US dollar terms in the last two years. Preliminary data show that exports tothe non-Birr area have risen from US$1 million in 1992 to US$29 million in 1994 whilethose to the Birr area (Ethiopia) rose from US$14 million to US$26 million. Merchandiseimports also increased substantially and it is estimated that in 1994, they amounted toUS$41 million from the Birr area and US$348 million from the non-Birr area. Salt iscurrently the most important export item, follow by beverages and tobacco. Broaderefforts are required to put Eritrea's export sector on a sustainable path of growth with theassistance of private investment, improvement in the macroeconomic framework, andstrengthening of the enabling environment at the micro-level.

B. THE ERITREAN TRANSPORT SYSTEM

1.6 More than thirty years of war have left Eritrea's transport infrastructure in aseverely dilapidated state. The road network and port facilities require extensiverehabilitation. Failure to rectify these deficiencies will impede the flow of goods andservices, hamper the development of export-oriented agriculture and industry, increasetransport costs and ultimately retard economic growth.

1.7 The road network in Eritrea is small, under 6000 km of main and rural roads, ofwhich less than 1000 km can be considered all-weather. At one time, they represented awell developed road system. A complete absence of even routine maintenance, due mainlyto the prolonged war situation, has led to severe deterioration of the system Someimportant improvements are under way, particularly the rehabilitation and widening of theAsmara - Massawa road, and the detailed design of the Nefasit - Tera Imni road isexpected to start in the near.future.

1.8 The land transport previously included railways which ran between Bisria andMassawa via Asmara - Keren - Agordat, and a shorter line which ran between MersaFatma and Colluli in the Eastern part of the country. Eritrea was also the site of theteleferrica, the longest overhead tramway in the world which carried freight betweenMassawa and Asmara. The railways had ceased operations by the early years of theDergue regime while the teleferrica was dismantled at the end of the British trusteeship in1952.

1.9 The commercial trucking fleet is currently underutilized, although there is someindication that some rural areas are not well served because drivers refuse to take theirtrucks over the existing poor roads and, as a result, farmers find it difficult to marketcrops. In contrast to the trucking fleet, there is shortage of commercial passengervehicles, which has led the Government to regulate the sector to prevent a concentrationof services around Asmara. Currently, the sector is performing reasonably well in terms ofcost recovery.

1.10 Eritrea has two outlets to the sea located at Massawa and Assab. The port ofMassawa developed its present facilities between 1885 and 1940. The port of Assab wasconstructed in 1959 and serves as the major gateway for Ethiopia, and is also important inthat the refinery is located there. As with the road infrastructure, both ports suffered fromdamage and lack of maintenance during the Liberation War.

1.11 Civil aviation is presently focused on the international airport of Asmara and to alesser extent the commercially important airport of Assab. There are currently a numberof regional air services operated by Egypt, Yemenia and Ethiopian Airlines. Ethiopianalso operates Asmara-Assab-Addis services twice a week, and daily regional andEuropean services are provided by Ethiopian as well as Lufthansa. The passenger andfreight terminals at Asmara International Airport have recently undergone a majorrehabilitation and expansion program, although it still would require substantial investmentin navigational aids and communications in order to meet ICAO standards. Nonetheless,operations are currently carried out on a 24-hour basis.

C. ROLE OF TRANSPORT IN THE ECONOMY

1.12 The transport system is essential for the domestic economy and is also one of themost important sources of foreign exchange earnings. The once well developedinfrastructure of Eritrea has been severely damaged by the war. This is currently a majorconstraint on growth, especially by limiting access of producers to the markets. Ports androads in particular are constraints in need of immediate attention.

D. CRITICAL TRANSPORT ISSUES IN ERITREA

1.13 Transport conditions are major constraints to economic and social development inEritrea. Under the emergency RRPE, some initial and urgent support has been providedby the IDA and other donors for the purpose of essential equipment and material to repairand rehabilitate the most important roads (particularly the Asmara - Massawa road) andsome bridges.

1.14 A coherent transport strategy for Eritrea is under development with EU funding.A consultant was appointed in January 1996 to assist the Government to carry out a studywith the following objectives:

* carry out a base-line survey of the transport sector identifying its maincharacteristics, main problems and opportunities in all areas including policy,strategy, infrastructure, institutions, and management capability,

* to set out and assess options for the development of the transport sectorcovering reforms, investments, and donor mobilization; and

-4-

* to make recommendations and a plan of action for developing the transportsector to the benefit of Eritrea covering policy reforms, investments, anddonor mobilization; and including the ranking and prioritization of bothreforms and investments within the transport sector as a whole and betweensub-sectors.

1.15 The draft findings and recommendations of the study, which has been looking intothe sub-sectors of roads, ports and shipping, aviation and railways, are presently underdiscussion within the Government.

1.16 Without a significant increase in effective port capacity in the country, Massawaand Assab would not be able to handle the base traffic forecasts, which are predicted togrow at a relative modest rate but with a significant shift to containers and general cargo.

E. BANK STRATEGY

1.17 Country Assistance Strategy: The long-term goal of Eritrea, once recovery andreconstruction tasks have been completed, is to build a modern, technologically advanced,export-oriented economy, which will capitalize on its strategic position and naturalresources, and based on self-reliance, technology transfer, and private investment. Privateinvestment has been identified as the engine of growth and development, although Eritreahas not inherited a working private sector. The strategy seeks to accomplish this objectiveby:

* creating an environment in which the private sector will develop and flourish,in partnership with foreign investors;

* reducing infrastructure constraints; and* investing in human resources.

1.18 In order to build a strong partnership with Eritrea, the Bank Group's assistancestrategy will continue to be governed by the principle of maintaining clear governmentownership of the programs.

1.19 The once well developed infrastructure of Eritrea has been severely damaged bythe war. This is currently a major constraint on growth, especially limiting access ofproducers to the markets. Ports, roads, energy, and telecoms are constraints in need ofimmediate attention.

1.20 Critical issues now facing the port industry are being addressed through theproposed project (see Sections 2 and 3), and in the preparatory works for Phase II and IIIof the development of the sector.

F. PREVIOUS BANK GROUP INVOLVEMENT IN THE ERITREA PORT SECTOR

1.21 This will be the first IDA operation in Eritrea's port sector involving substantialrehabilitation. However, the expansion of facilities at Assab Port to provide the port withthe capacity and ability to handle containerized traffic was a component of the EthiopiaTransport Project, Credit 2002-ET. The construction of two new container berths hadjust started in 1991/92, when control of the port changed and the project was terminated.

G. RATIONALE FOR IDA INVOLVEMENT

1.22 The rationale for IDA involvement is based on: (i) the importance of the portsector to a successful economic recovery program; (ii) IDA's previous involvement in theport sector in Ethiopia (Assab); and (iii) the contribution IDA can make to the reformprocess based on its experience in taking the lead role in formulating port modernizationprograms in neighboring countries along the east coast of Africa.

-6-

2. THE PORT SUB-SECTOR

A. ORGANIZATION

2.1 With the end of the war in May 1991, the Provisional Government of Eritreaestablished the Department of Ports and Maritime Transport (DPMT) by proclamationNo. 23/92, Art. 7 No. 1.17. The department was established to develop, improve,maintain, operate and regulate the port and shipping industry in Eritrea. The DPMT,under the President's Office, was legally responsible for: (i) all port activities in Massawaand Assab; (ii) a ship repair yard in Massawa; and (iii) Eritrea Shipping Transit AgenciesServices (ERSTAS - the sole ship's agent, and major freight forwarding agent), and theEritrea Shipping Lines'. In May, 1993 the DPMT was re-established as the Ports &Maritime Authority (PMTA), and in early 1994 when the headquarters was relocated toMassawa, the PMTA was re-established as the Eritrea Ports Authority (EPA), stillreporting to the President's Office. In 1995 the Government decided to organize the portswithin a Department of Maritime Transport (DMT) under the Ministry of Transport andCommunication, and the two ports were established as autonomous commercial entitiesunder the supervision of a sector board chaired by the Minister of Transport andCommunication.

2.2 The port of Massawa serves as the major port for import/export of Eritrean cargo,and for an increasing volume of traffic for northern Ethiopia (Tigray), while Assab isprimarily a transit port for Ethiopian trade, accounting for about 85 percent of Ethiopia'stotal external trade. Over 95 percent of the dry cargo passing through port of Assab isEthiopian trade.

2.3 The organizational structures of two ports, employing the following staff, areshown in Annex 16:

Massawa AssabPermanent- Monthly paid 276 684

- Dockers 281 985

Contractual 8 7

Daily 164 440

Casual Dockers 1,054 1,128

Eritrea Shipping Lines. with its three coastal vessels (one tanker and two general break bulk cargo)has since 1994. been under the jurisdiction of Peoples Front For Democracy and Justice.

-7-

2.4 Lack of maintenance and damages by the war have left the infrastructure of thetwo ports in a dilapidated shape, and it has been with great difficulty that the ports havemanaged to handle the increasing traffic. The two ports suffer from slow cargo handlingrates (especially for containers) and shortage of suitable equipment.

2.5 Problems and weaknesses in the Customs Administration include outdated andinefficient operational systems and procedures, and lack of skilled staff. Specificweaknesses include an antiquated import declaration system, characterized by inefficientand superfluous formalities and procedural steps, and lack of selectivity in checking thegoods. This results sometimes in cumbersome and slow goods clearance process, whichin turn increases the cargo dwell time in the ports. The Government has started to addressthe shortcomings and to simplify documentation and procedures, and has also decided toinstall the customs computerized system ASYCUDA at the two ports and the airport.This component, originally planned to be part of the project, will be implementedsimultaneously with the project under Italian funding. Included in the project, however, isthe construction of a customs building in Massawa.

2.6 In order to transform the two ports into modern, efficient, commercially-orientedand profit-generating enterprises, higher and middle management staff will need to betrained in leadership, personnel management planning and decision-making techniques,information and communication, economics and financial management, and safety andenvironmental aspects. The port management staff in Eritrea is highly motivated anddetermined to succeed. The ports are already enjoying technical assistance from theFederal Republic of Germany within the scope of bilateral technical cooperation. ThisEritrean-German Port Development Project (EPDP) started in early July 1995 andcomprises a total of 48 man-months (mm) of technical assistance including 12 mm in thefield of training with a clear emphasis on train-the-trainer programs. Additional training,particularly in the fields of port operations and equipment maintenance, will be providedunder the project (para. 3.8).

B. PORT OF MASSAWA

2.7 Massawa port was founded in 1665 by the Turks and took its present shape duringthe Italian rule (1885-194 1). The port is situated on the northern shore of MassawaIsland, and consists of six general purpose berths with a port area inside a customs wallwith sheds, warehouses and open storage facilities. The exact timing of developments andthe order of berth construction are not known as there are no reliable records available. Itis believed that the most recent construction was that of Berths 5 (half) and Berth 6around 1940, and that all the present berths were constructed in the period 1926 to 1940.

2.8 The enclosed harbor is given additional protection by short breakwater armsextending south from Abd-el-Kader Peninsula and north from Massawa Island. Bothbreakwaters were constructed in 1926 and are rubble mound constructions protected byarmor stones or concrete capping. The breakwaters are both in relatively good condition.

-8-

2.9 The commercial port consists of six general purpose berths, aprons, warehouses,open sheds and open storage areas. Other facilities at Massawa are:

* Bulk salt loading jetties located on the south shore of Gherar Peninsula;* Ship repair facilities administered by the DMT and located west of the salt

jetties;* An oil termninal and a jetty at Taulud Bay. The terminal is operated by Total

and Mobil Oil;* Another oil terminal at Hargigo Bay, towards the south operated by Agip Oil;

and* A naval base at the southern part of the Abd-el-Kader Peninsula.

2.10 The approaches to Massawa port are without major difficulties. The port iscovered by Admiralty Chart No. 460. The channels used are north and south. Theentrance to the commercial port is navigational 24 hours a day, and is lighted with greenand red lights. There are two leading marks with red lights to assist maneuvering day andnight. The Massawa port is in charge of eight lighthouses in the Red Sea, of which onlyone, Mdote, vAth a light range of 13 nautical miles, is functional. The main MassawaLight House (Risi Midri), with a light range of 16 miles, is also run by Massawa port.

2.11 There are no significant currents inside the harbor, and the tidal range of springtides is 1.5 meters at the maximum. The port provides pilotage from dawn to dusk, andthe pilotage is compulsory for all ships over 100 GRT. Calling ships should give sevendays notice of arrival. Tug and pilot boats are available.

2.12 The port is served by five rail mounted quay cranes. The cranes cover berths 3, 4and 5. A sixth quay crane is not working. The cranes, built in 1975, are in a poorcondition due to lack of maintenance. The lifting capacity is 5 tons at 20 meters and 6tons at 16 meters. The cranes can be mounted with grabs for discharging bulk cargo.

2.13 The port fleet of lifting equipment also includes seven mobile cranes. Most ofthese are in a bad condition. A 50-ton crane lacks spare parts and has thus not been inoperation since November 1994. A 100-ton crane is the only one in a good condition.The mobile cranes are used for discharging and loading general cargo onto vessels, andare also often used for loading and unloading cargo onto trucks in the storage areas.

2.14 In April 1997 the port acquired cargo handling equipment worth US$2.0 millionunder a Japanese Grant, including a reach stacker for handling of 40 foot containers, 10fork lift trucks, and 4 tugmasters with trailers.

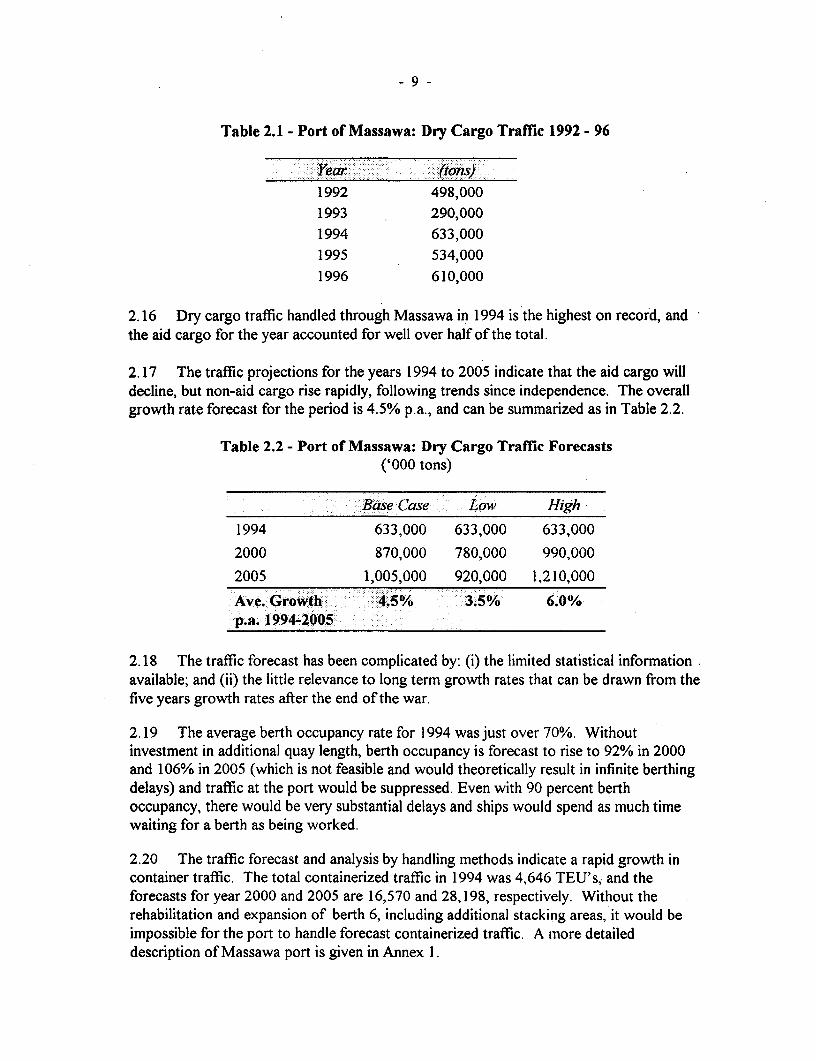

2.15 The port handled 610,000 tons of cargo at its own berths in 1996. In addition,local oil terminals handled a further 160,000 tons, giving a total of 770,000 tons.International cargo accounted for 97% of the total handled at the port, and almost 97% ofthe cargo was imports. Cargo volumes have fluctuated erratically since independence in1991, mainly because food aid cargoes have varied. The total cargo (excluding petroleumproducts) at the main port are detailed in Table 2.1:

-9-

Table 2.1 - Port of Massawa: Dry Cargo Traffic 1992 - 96

- - .Year ( - ztons)1992 498,0001993 290,0001994 633,0001995 534,0001996 610,000

2.16 Dry cargo traffic handled through Massawa in 1994 is the highest on record, andthe aid cargo for the year accounted for well over half of the total.

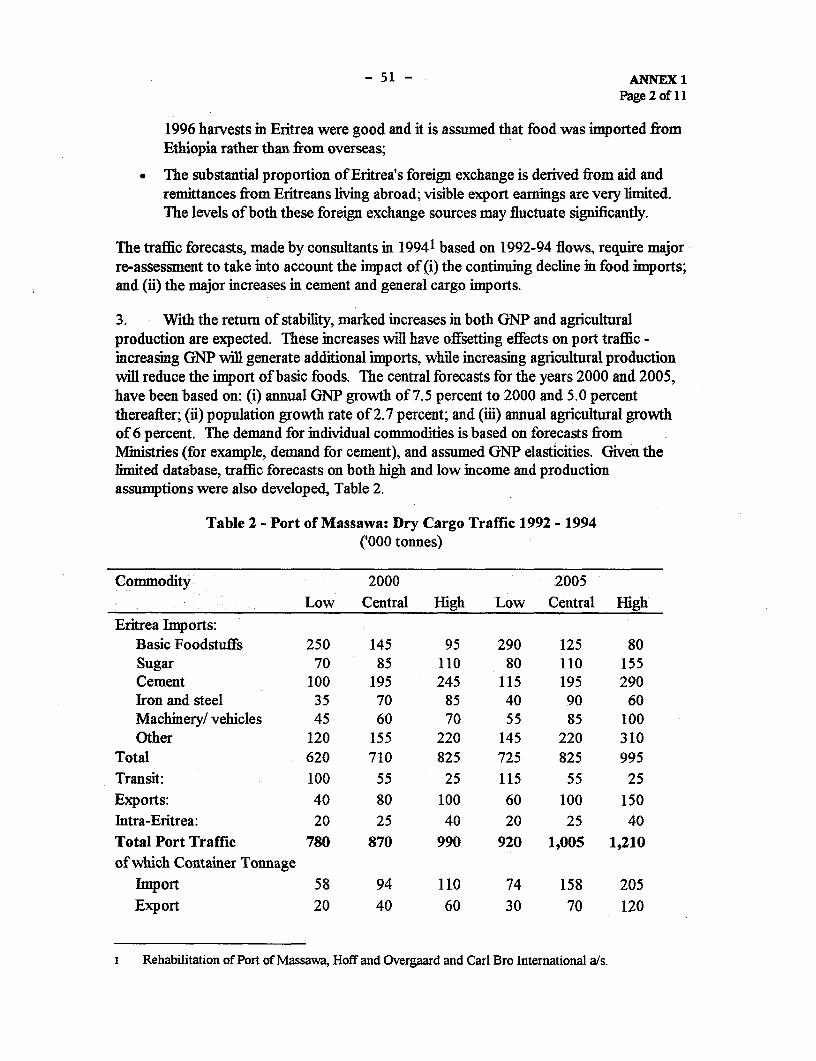

2.17 The traffic projections for the years 1994 to 2005 indicate that the aid cargo willdecline, but non-aid cargo rise rapidly, following trends since independence. The overallgrowth rate forecast for the period is 4.5% p.a., and can be summarized as in Table 2.2.

Table 2.2 - Port of Massawa: Dry Cargo Traffic Forecasts('000 tons)

Base (:ase Low High

1994 633,000 633,000 633,000

2000 870,000 780,000 990,000

2005 1,005,000 920,000 1,210,000

Ave. Growth 4.5% 3.5% 6.0%p.a. 1994-2005

2.18 The traffic forecast has been complicated by: (i) the limited statistical informationavailable; and (ii) the little relevance to long term growth rates that can be drawn from thefive years growth rates after the end of the war.

2.19 The average berth occupancy rate for 1994 was just over 70%. Withoutinvestment in additional quay length, berth occupancy is forecast to rise to 92% in 2000and 106% in 2005 (which is not feasible and would theoretically result in infinite berthingdelays) and traffic at the port would be suppressed. Even with 90 percent berthoccupancy, there would be very substantial delays and ships would spend as much timewaiting for a berth as being worked.

2.20 The traffic forecast and analysis by handling methods indicate a rapid growth incontainer traffic. The total containerized traffic in 1994 was 4,646 TEU's, and theforecasts for year 2000 and 2005 are 16,570 and 28,198, respectively. Without therehabilitation and expansion of berth 6, including additional stacking areas, it would beimpossible for the port to handle forecast containerized traffic. A more detaileddescription of Massawa port is given in Annex 1.

- 10 -

C. PORT OF ASSAB

2.21 The present commercial port was completed in 1959 and consists of two jettieswhich extend SSE from the shore forning a basin 300 m wide. The general cargo berthsare aligned to the predominant wind direction on the inner faces of the jetties. The berthsare protected from waves generated by SE winds by a detached breakwater.

2.22 The North Jetty provides a total berth length of 490 m which is divided into 3berths (berths 1, 2 and 3). All berths provide 11.0 m depth of water alongside. The SouthJetty provides a total berth length of 530 m which is divided into 4 berths (Berths 8 to 1 1).The available depths of water alongside are between 5.8 m (Berth 8) to 10.0 m (Berths 10and 1-1). The berths on both jetties are of concrete block construction, and the overallwidth of the jetties is around 100 m. At the outer end of the South Jetty is a smallconcrete Ro/Ro ramp for berthing Ro/Ro vessels with either stern or bow ramp. To thesouth of the port is the Assab Oil Refinery and a number of marine oil terminal facilitiesfor discharging/loading of crude oil and refined products.

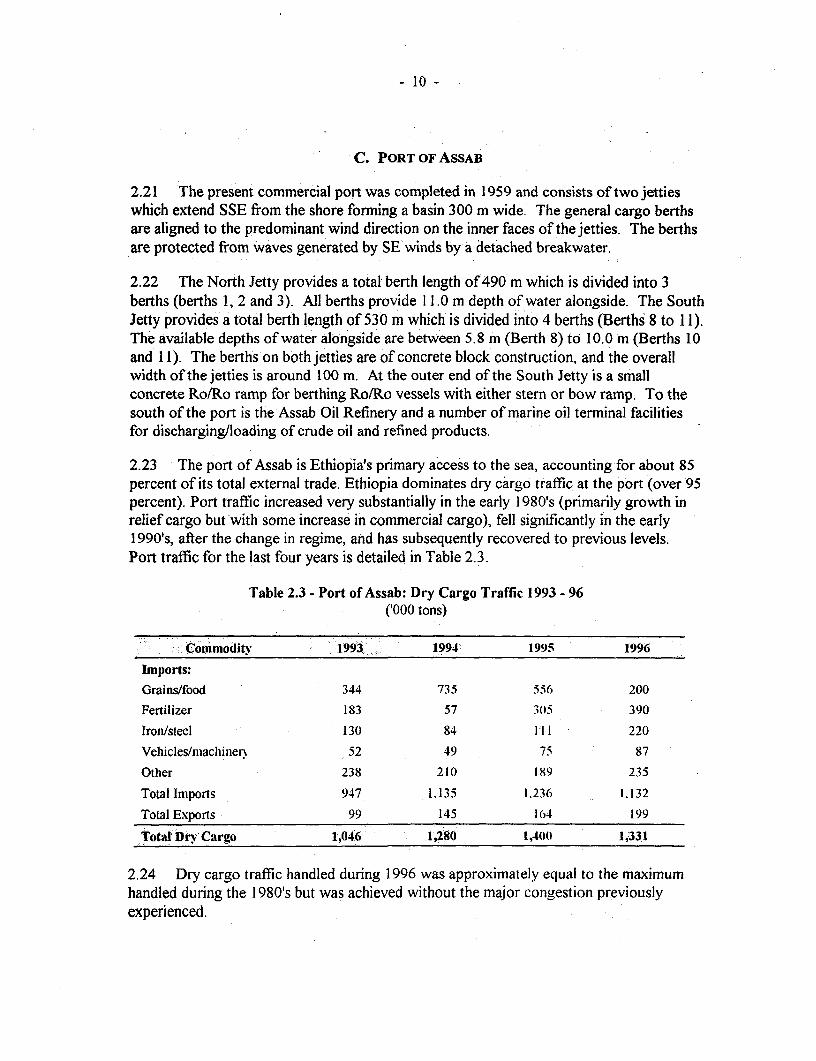

2.23 The port of Assab is Ethiopia's primary access to the sea, accounting for about 85percent of its total external trade. Ethiopia dominates dry cargo traffic at the port (over 95percent). Port traffic increased very substantially in the early 1980's (primarily growth inrelief cargo but 'with some increase in commercial cargo), fell significantly in the early1990's, after the change in regime, and has subsequently recovered to previous levels.Port traffic for the last four years is detailed in Table 2.3.

Table 2.3 - Port of Assab: Dry Cargo Traffic 1993 - 96('000 tons)

Commodity 1993. 1994: 1995 1996

Imports:Grains/food 344 735 5s6 200Fertilizer 183 57 3(05 390

Iron/steel 130 84 111 220Vehicles/machinmer 52 49 75 87Other 238 210 189 235

Total Imports 947 1.135 1.236 1.132

Total Exports 99 145 164 199

Total Dry Cargo 1,04 6 1,280 1,40(1 1,331

2.24 Dry cargo traffic handled during 1996 was approximately equal to the maximumhandled during the 1980's but was achieved without the major congestion previouslyexperienced.

2.25 Major increases in the total volume of dry cargo traffic are not expected but verysubstantial shifts in the commodity distribution are probable:

* the high level of 1996 fertilizer imports is expected to continue, even if donorassistance is reduced;

* grain production in Ethiopia will expand significantly and there will be agradual decline in the average level of food imports, although there will still bemarked fluctuations depending upon rainfall and domestic production;

* economic growth in Ethiopia will result in a continued increase in imports ofraw materials, vehicles and machinery and other general cargo. The growthrate is expected to be approximately equal to the growth in GDP, i.e. about 6percent per annum; and

* coffee and other agricultural exports have increased since 1992, and thisgrowth is expected to continue.

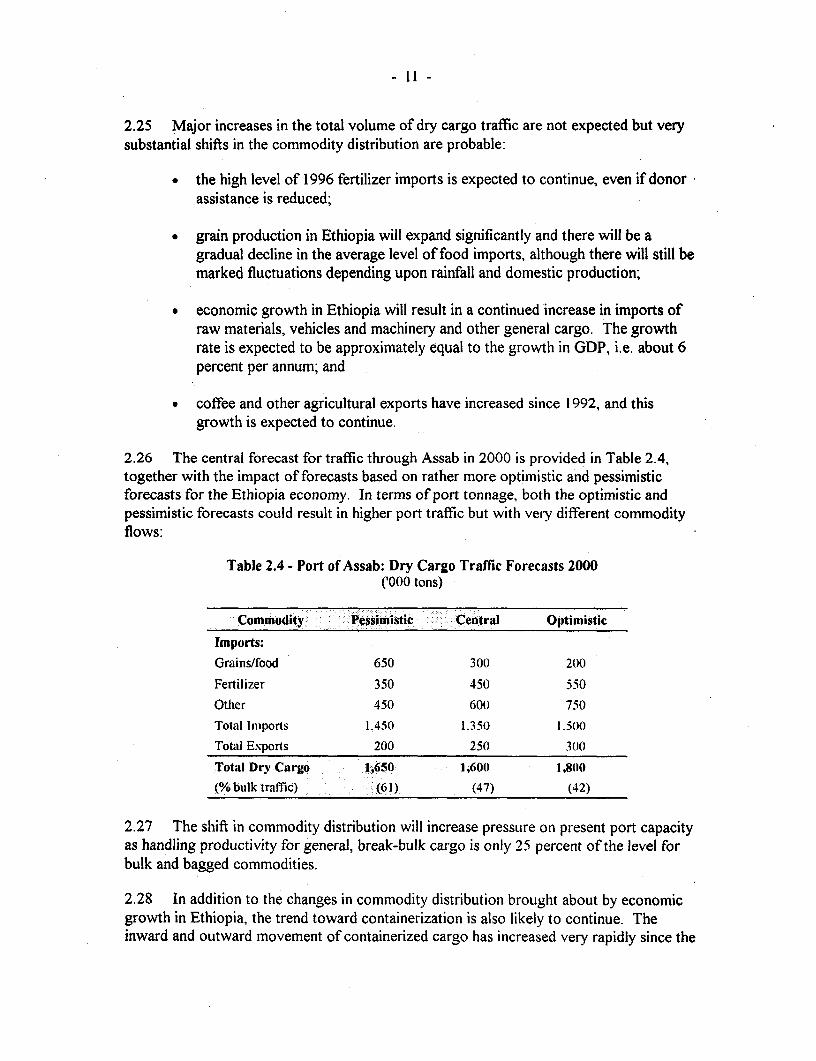

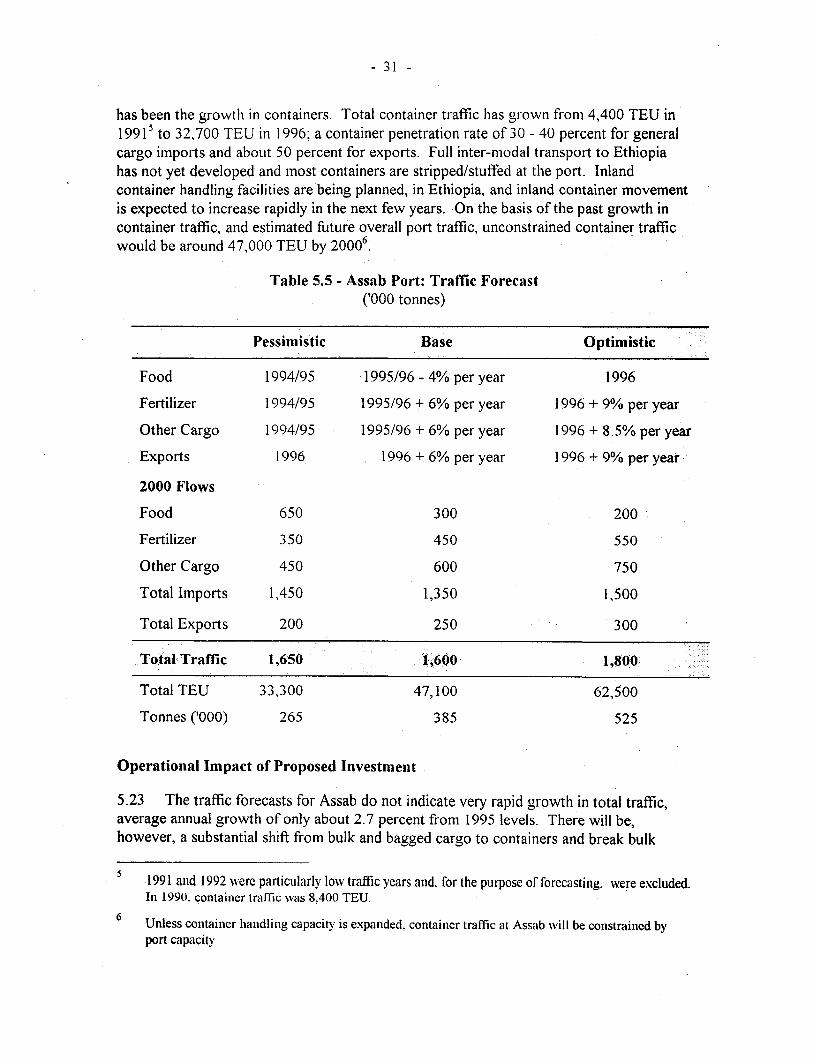

2.26 The central forecast for traffic through Assab in 2000 is provided in Table 2.4,together with the impact of forecasts based on rather more optimistic and pessimisticforecasts for the Ethiopia economy. In terms of port tonnage, both the optimistic andpessimistic forecasts could result in higher port traffic but with veiy different commodityflows:

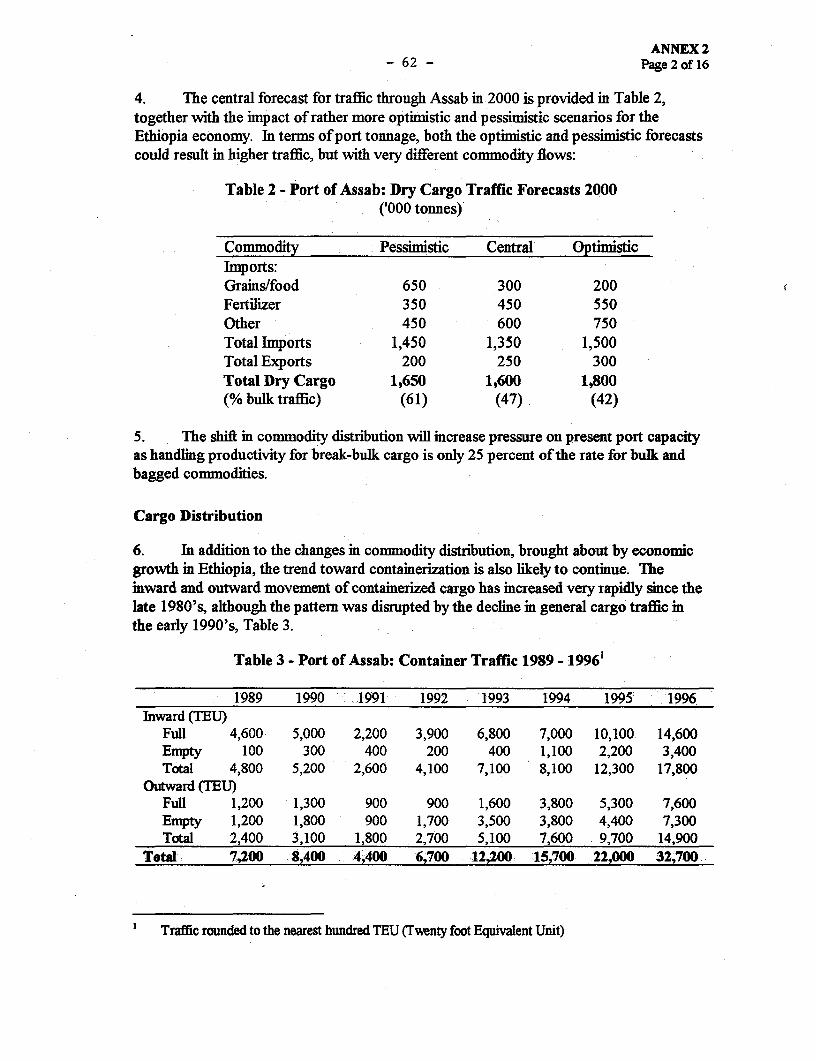

Table 2.4 - Port of Assab: Dry Cargo Traffic Forecasts 2000('000 tons)

Commodity Pessimistic Central Optimistic

Imports:

Grains/food 650 300 200

Fertilizer 350 450 550Other 450 600 750

Total Imports 1,450 1.350 1.500

Total Exports 200 250 3((

Total Dry Cargo 1,650 1,600 1,8(10

(% bulk traffic) (61) (47) (42)

2.27 The shift in commodity distribution will increase pressure on present port capacityas handling productivity for general, break-bulk cargo is only 25 percent of the level forbulk and bagged commodities.

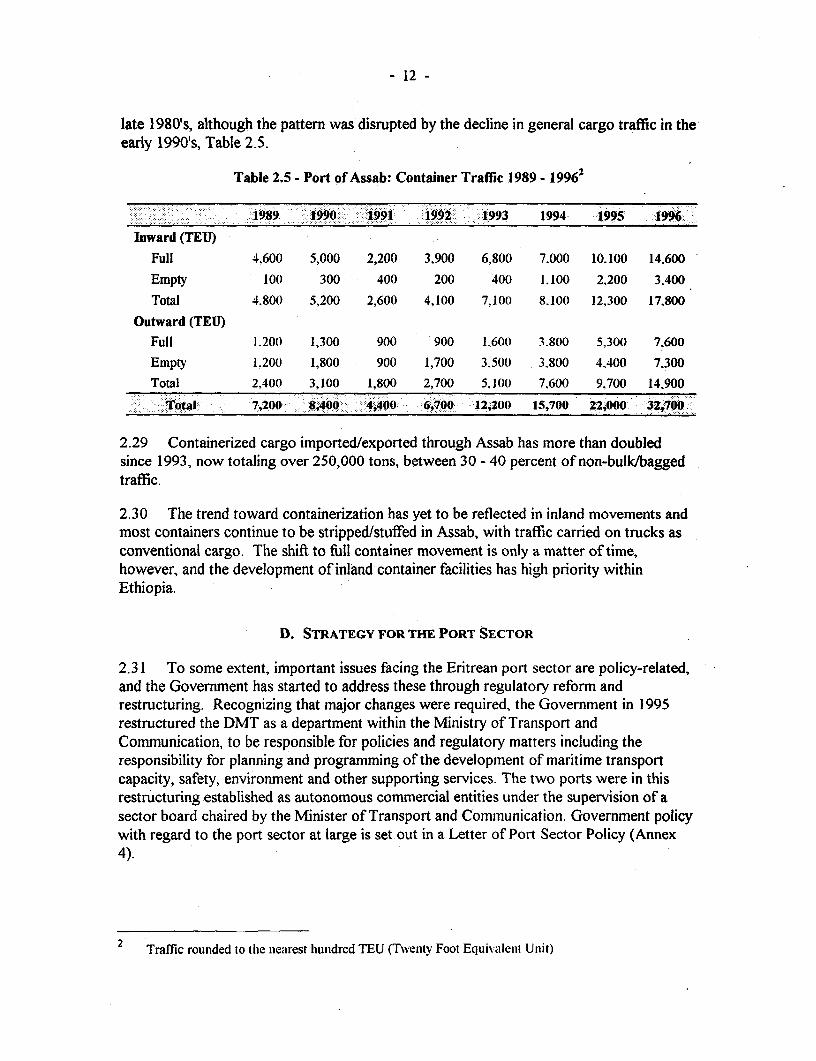

2.28 In addition to the changes in commodity distribution brought about by economicgrowth in Ethiopia, the trend toward containerization is also likely to continue. Theinward and outward movement of containerized cargo has increased very rapidly since the

- 12 -

late 1980's, although the pattern was disrupted by the decline in general cargo traffic in theearly 1990's, Table 2.5.

Table 2.5 - Port of Assab: Container Traffic 1989 - 19962

-- ;: 1989. 1$g990:0 190 i 910- 0-199 2-" 1993 1994 1995 19I:

Inward (TEU)Full 4,600 5,000 2,200 3,900 6,800 7.000 10.100 14.600

Empty 100 300 400 200 400 1.100 2.200 3,400

Total 4.800 5,200 2,600 4,100 7.100 8.100 12,300 17.800

Outward (TEU)

Full 1.200 1,300 900 900 1.600 3.800 5,300 7.600

Empty 1.200 1,800 900 1,700 3.500 3.800 4.400 7,300

Total 2.400 3,100 1,800 2,700 5.100 7.600 9,700 14.900To': ' "Qtal; 0 7,200 8,400 4,400 6,700 12,200 15,700 22,000 32,700

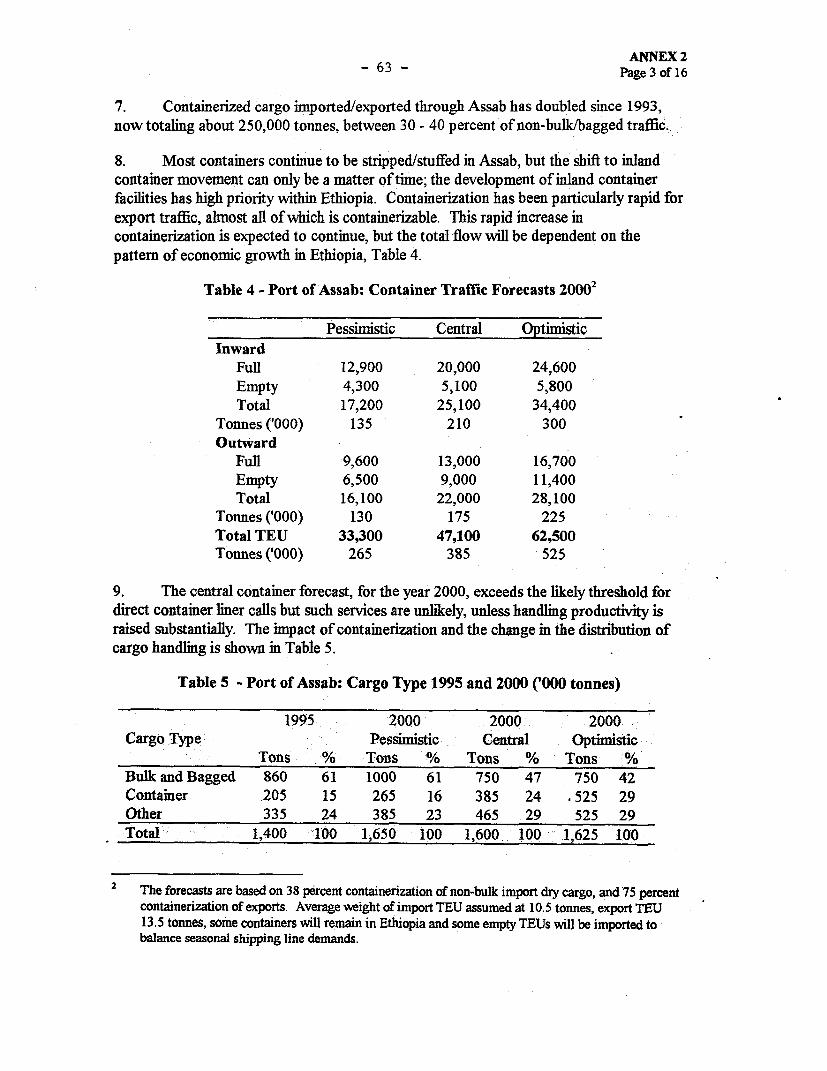

2.29 Containerized cargo imported/exported through Assab has more than doubledsince 1993, now totaling over 250,000 tons, between 30 - 40 percent of non-bulk/baggedtraffic.

2.30 The trend toward containerization has yet to be reflected in inland movements andmost containers continue to be stripped/stuffed in Assab, with traffic carried on trucks asconventional cargo. The shift to full container movement is only a matter of time,however, and the development of inland container facilities has high priority withinEthiopia.

D. STRATEGY FOR THE PORT SECTOR

2.31 To some extent, important issues facing the Eritrean port sector are policy-related,and the Government has started to address these through regulatory reform andrestructuring. Recognizing that major changes were required, the Government in 1995restructured the DMT as a department within the Ministry of Transport andCommunication, to be responsible for policies and regulatory matters including theresponsibility for planning and programming of the development of maritime transportcapacity, safety, environment and other supporting services. The two ports were in thisrestructuring established as autonomous commercial entities under the supervision of asector board chaired by the Minister of Transport and Communication. Government policywith regard to the port sector at large is set out in a Letter of Port Sector Policy (Annex4).

2 Traffic rounded to the nearest hunidred TEU (Twenty Foot Equivalenl Unit)

- 13 -

3. THE PROJECT

A. IDENTIFICATION AND PREPARATION

3.1 Following the Government's request in January 1995 for World Bank assistance inthe ports sector, an identification mission was launched in February 1995 to discuss thestrategies and key issues, and to start preparatory works. A study was commissioned inlate May 1995 under Danish Trust Fund financing to: (i) prepare an overall portdevelopment program for Massawa (Phase I for the year 1995 to 2005) including trafficforecasting and engineering works for the rehabilitation of Berths 5 and 6; (ii) prepare aprogram for improvements in port operations; and (iii) recommend appropriateimprovements in administrative and management systems. The project was pre-appraisedin January 1996, appraised in April 1996, and post-appraised in April 1997.

B. OBJECTIVES

3.2 The proposed project is the first phase of the Government's program fordevelopment of the port sector. (The second and third phases wi]l be the subject of aDevelopment Study to be carried out under the project.) It supports the economic andrecovery program contained in the Government's Policy and Sector Strategy Papers(Macro-Policy), and in the Country Assistance Strategy (Report # 15324-ER, February 5,1996). The aim is for Eritrea to be an outward oriented and trading nation, and ports willtherefore play a critical role in the future expansion of the economy.

3.3 To address the urgent capacity requirements up to the year 2005, the proposedproject is designed to increase substantially the productivity and capacity of the two portsof Massawa and Assab. To this end, the project would provide the financial and technicalassistance required to rehabilitate and upgrade the two ports, optimizing the use ofexisting facilities, and to raise the quality and level of services to international standards.

C. PROJECT DESCRIPTION

3.4 In addition to the changes which are needed in the institutional set-up and in themanagement and operation of the two ports, investments in the infrastructure arenecessary to provide the capacity necessary to meet the forecast traffic demands. Theoverall composition of the proposed project is as follows:

Project Components

3.5 Civil Works (US$18.65 million)'. This component consists of repair,rehabilitation and extension of berths 5 and 6, dredging in front of the new berth 6 to 12 m

Amounts shown are basc costs.

- 14 -

depth, reclamation of land behind berth 6, and heavy duty pavement for the new containerstacking yard. Also included under this component are clearing of the apron and storageareas adjacent to berths 5 and 6, rehabilitation of the electrical and storm drainagesystems, a building for the port administration and customs authorities, a workshop, anequipment shed and improvements to warehouses in the port.

3.6 Cargo Handling Equipment (US$22.65 million). Most of the equipmentincluded in this component is for handling of containers. Investment in Massawa is for amobile container handling crane, tugmasters and trailers, a 20 ton mobile crane, a firefighting truck, shore cranes and cargo handling and communication equipment. Aprovisional sum for spare parts for repairs of old fork lift trucks and shore cranes, and apilot boat is also included. For Assab are included two mobile cranes to carry out ship-to-shore handling of containers, reach stackers for full and empty containers at the stackingyard, tugmasters and trailers, small fork lift trucks for stripping and stuffing containers andfor operating in the ship's hold, a 50 ton mobile crane and a fire fighting truck. Areplacement tugboat for Assab has also been included under this component.

3.7 Environment (US$1.6 million). Facilities and equipment, estimated atUS$800,000 for each of the two ports, have been included in the project to improveoperating practices regarding handling of hazardous cargo, as well as control of dischargeof bilge water and solid waste from ships, and oil spill combat equipment includingsupport in institutional building and training for the two ports to comply with a NationalOil Spill Contingency Plan, presently under preparation with assistance from theInternational Maritime Organization (IMO).

3.8 Training (US$0.6 million). The project will provide funds for training programs,particularly in the fields of port operations and equipment maintenance, including overseastraining at recognized international institutes, and/or at overseas ports with similarfacilities and operational constraints and systems. The training component will be closelycoordinated with the ongoing EPDP program (para. 2.6). Included in this component isalso equipment and non-wage operating costs for the Project Coordination Unit (PCU,para. 4. 1).

3.9 Consultancy Services (US$4.5 million). The project will include financing ofconsultancy services for: (i) supervision of the civil works in Massawa; (ii) short termexperts to assist in drafting technical specifications and bidding documents for equipmentand spare parts procurement, evaluation of bids and recommendations for award ofcontracts; (iii) specific studies in the field of maritime and port legislation, MIS, costaccounting, tariff analysis and commercialization of port activities; (iv) a study of the longterm development of the port sector (Phases II and III); and (v) short term technicalassistance in port management and operations, and equipment maintenance.

- 15 -

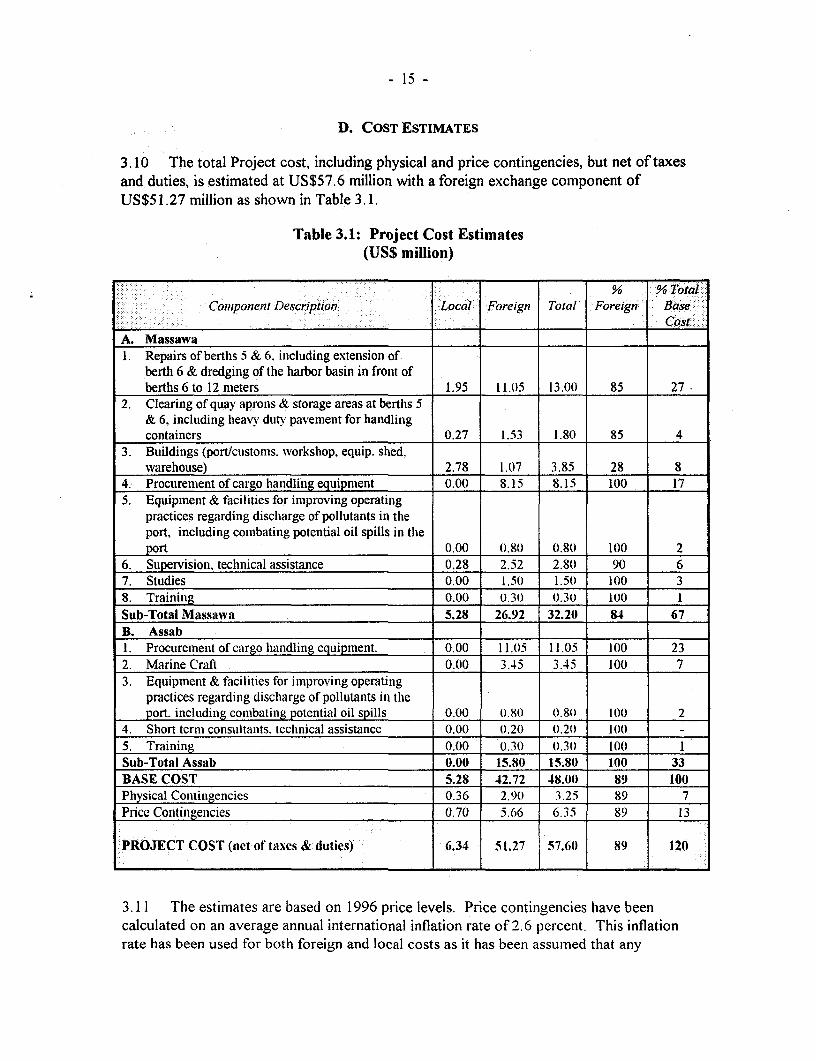

D. COST ESTIMATES

3.10 The total Project cost, including physical and price contingencies, but net of taxesand duties, is estimated at US$57.6 million with a foreign exchange component ofUS$51.27 million as shown in Table 3.1.

Table 3.1: Project Cost Estimates(US$ million)

% % Total..Component Description Local Foreign Total Foreign Base

-__________________________________________________ ._____ -___-__. Cost:A. Massawa1. Repairs of berths 5 & 6. including extension of

berth 6 & dredging of the harbor basin in front ofberths 6 to 12 meters 1.95 11.05 13.00 85 27

2. Clearing of quay aprons & storage areas at berths 5& 6, including heavy duty pavement for handlingcontainers 0.27 1.53 1.80 85 4

3. Buildings (port/customs. workshop, equip. shed.warehouse) 2.78 1.07 3.85 28 8

4. Procurement of cargo haiidling equipment 0.00 8.15 8.15 100 175. Equipment & facilities for improving operating

practices regarding disclharge of pollutants in theport, including combating potential oil spills in theport 0.00 0.80 0.80 100 2

6. Supervision, techniical assistance 0.28 2.52 2.80) 90 67. Studies 0.00 1.50 1.50( 100 38. Training 0.00 0.30 0.30 100 1Sub-Total Massawa 5.28 26.92 32.21 84 67B. Assab1. Procurement of cargo hanidling equipment. 0.00 11.0 11.05 100 232. Marine Crafi 0.00 3.45 3.45 100 73. Equipment & facilities for improving operating

practices regarding discharge of pollutants in theport. including combating potential oil spills 0.00 (.8( t).80 100 2

4. Short term consultanits. techliical assistance 0.00 0.2() 0.20 100 -

5. Training 0.00 0.30 0.30) 100 1Sub-Total Assab 0.00 15.80 15.80 100 33BASE COST 5.28 42.72 48.00 89 100Physical Continigencies 0.36 2.90 3.25 89 7Price Contingenicies 0.70 5.66 6.35 89 13

PROJECT COST (net of taxes & duties) 6.34 51.27 57.60 89 120

3.11 The estimates are based on 1996 price levels. Price contingencies have beencalculated on an average annual international inflation rate of 2.6 percent. This inflationrate has been used for both foreign and local costs as it has been assumed that any

- 16

differences between local and international price inflation will be offset by equivalentadjustments in Eritrea's foreign exchange rate. Physical contingencies of 10 percent havebeen added to the base cost of civil works. Price and physical contingencies total US$9.6million, or 20 percent of the total project cost.

E. FINANCING

3.12 IDA's contribution will be US$30.3 million, or 53 percent of the total project costnet of taxes. Italy has agreed to co-finance US$21.0 million of the cost of the Massawacomponent under an untied grant. The Grant Agreement was approved by the Board ofItalian Cooperation on July 26, 1996, and a Trust Fund Agreement was signed betweenItaly and IDA on October 22, 1996. An Agreement between Eritrea and IDA on purposesand terms and conditions for withdrawal of the Italian Grant was signed on June 9, 1997.The State of Eritrea will finance the local component of the project, estimated at theequivalent of US$6.3 million.

Table 3.2: Financing Plan(US$ million)

Project Con poM ent MDA Italy GOE Total %:IDA..7...... ... po GOE Tot.al7..... ..

A. Massawa 11.3 21.0 6.3 38.6 29

B. Assab 19.0 0.0 0.0 19.0 100

Total Project -30. 21.0 6.3 57.6 53

3.13 The Government's policy is that commercial entities like the ports would berequired to generate at a minimum revenues sufficient to cover working capitalrequirements and debt service obligations. The intention is therefore that the proposedIDA Credit of US$30.3 million, as well as the Italian Grant of US$2 1.0 equivalent, will beon-lent to the two ports at an interest rate equivalent to a commercial loan, and that theports would bear the foreign exchange risk.

3.14 Subsidiary loan agreements between the Government and each of the ports ofMassawa and Assab will be signed as soon as the new maritime and port legislation hasbeen completed, and the two ports have been granted their own financial autonomy. Asindicated in the Letter of Port Sector Policy, it is estimated that subsidiary loanagreements with the ports will signed and effective as of December 3 1, 1999.

- 17

4. PROJECT IMPLEMENTATION

A. INSTITUTIONAL RESPONSIBILITIES

4.1 Implementation of the project will be the responsibility of the Ministry ofTransport and Communication (MTC) through its Department of Maritime Transport(DMT). A Project Coordination Unit (PCU) has already been established for the life ofthe project and is located at the Port Liaison Office in Asmara. The unit is headed by aProject Coordinator, and includes financial and procurement expertise. The functions ofthe unit will include:

* Overall coordination of project activities

* Supervision of short-term consultants

* Project monitoring and evaluation:

Keeping project recordsPreparing project accountsMonitoring of procurementMonitoring of key performance indicatorsPreparing project reports (quarterly and annually)

- DisbursementsPreparing withdrawal applicationsMonitoring disbursementsOpening letters of creditSpecial Account

3 Procurement (either directly or through supervision of consultants)

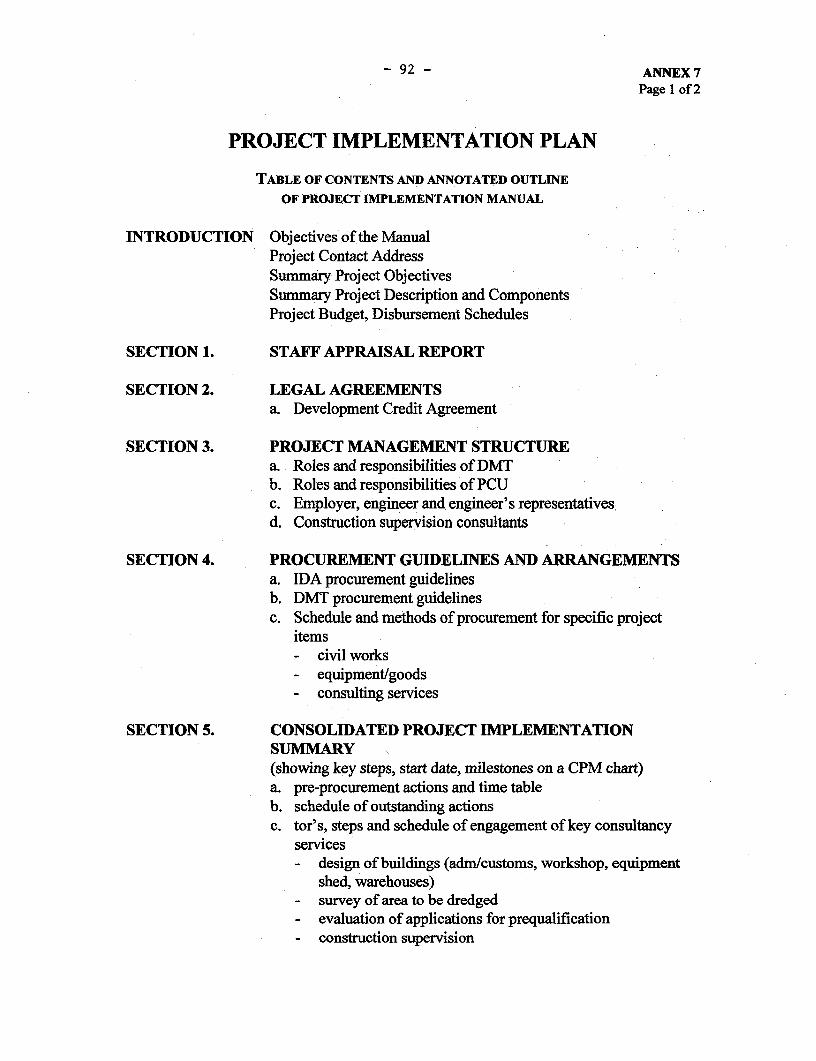

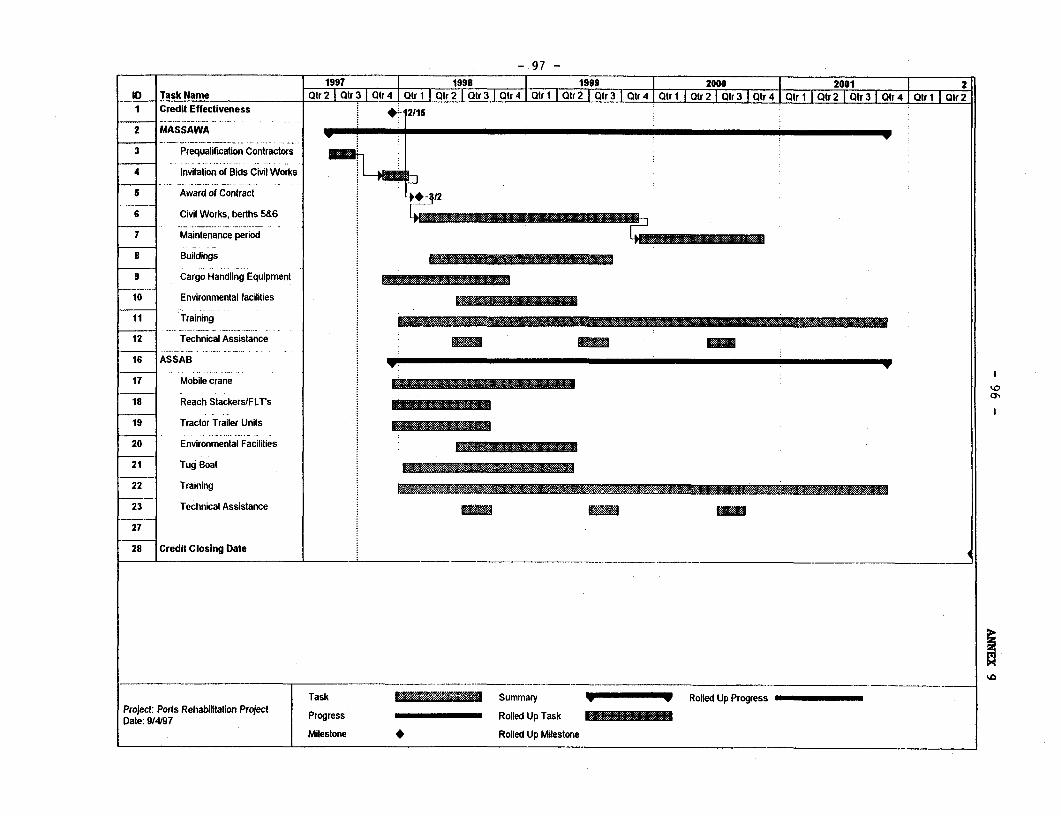

4.2 To clarify the roles and responsibilities of each entity involved in projectimplementation, a Project Implementation Plan (PIP) has been prepared. The content ofthe PIP was discussed and agreed during negotiations. Annex 7 gives a summary chart of.the key project implementation steps; detailed implementation plans for the project as awhole and specific components are included in the PIP (copy in the Project Files).

4.3 A meeting of port users (port authorities, customs, representatives of the truckingindustry, shipping agencies, etc.) will be convened regularly (once every quarter) at eachport to report on project progress and discuss issues which may affect the port users in thecourse of project implementation.

- 18 -

B. PRoCuREMENT

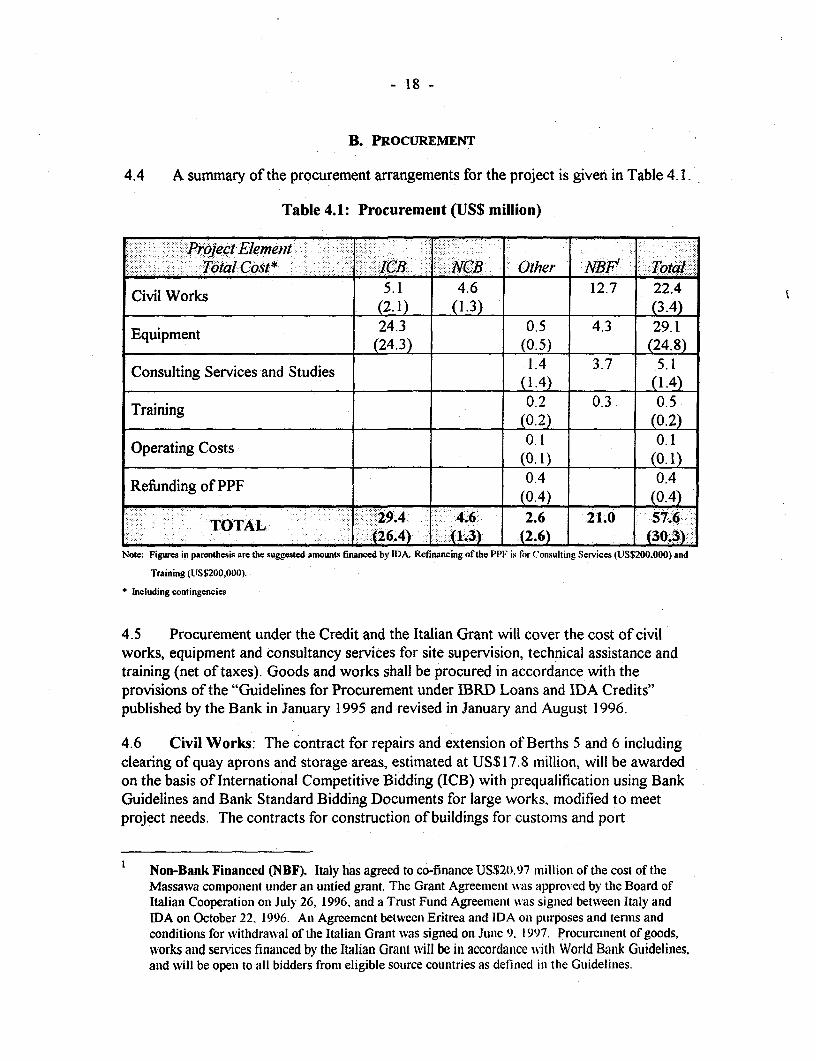

4.4 A summary of the procurement arrangements for the project is given in Table 4. 1.

Table 4.1: Procurement (US$ million)

Poect Element.... ... .T otal Cost*; IC NCB Other NBP Tolat.

Civil Works 5.1 4.6 12.7 22.4(2.1) (1.3) (3.4)

Equipment 24.3 0.5 4.3 29.1(24.3) (0.5) (24.8)

Consulting Services and Studies (1.4) 3.7 5.1_~~~~~~14 (1.)

Training (0.2 0.3 0.5Training ~~~______ (0.2) _ __ (0.2)

Operating Costs 0.1 0.1(0.1) (0.1)

Refunding of PPF 0.4 0.4(0.4) 0.4)Refunding of PPF (0.4) __2_.4 (014)

29.4- T A -4.6 2.6 21.0 57.6TOTAL:: :::E::;i : : ::: ;t -i(V26.4) (1.3) (2.) : (30.3-)

Note: Figures in parcnthesis are the suggested amounts financed by IDA. Refinancing of the PPF is for Consulting Services (US$200.000) and

Training (USS200.000).

* Including contingencies

4.5 Procurement under the Credit and the Italian Grant will cover the cost of civilworks, equipment and consultancy services for site supervision, technical assistance andtraining (net of taxes). Goods and works shall be procured in accordance with theprovisions of the "Guidelines for Procurement under IBRD Loans and IDA Credits"published by the Bank in January 1995 and revised in January and August 1996.

4.6 Civil Works: The contract for repairs and extension of Berths 5 and 6 includingclearing of quay aprons and storage areas, estimated at US$17.8 million, will be awardedon the basis of International Competitive Bidding (ICB) with prequalification using BankGuidelines and Bank Standard Bidding Documents for large works, modified to meetproject needs. The contracts for construction of buildings for customs and port

Non-Bank Financed (NBF). Italy has agreed to co-finance US$20.97 million of the cost of theMassawa component under an untied grant. The Grant Agreement was approved by the Board ofItalian Cooperation on July 26, 1996. and a Trust Fund Agreemenit was signed between Italy andIDA on October 22. 1996. An Agreement between Eritrea and IDA on purposes and termis andconditions for withdrawal of the Italian Grant was signed onl June 9. 1997. Procurement of goods,works and services financed by the Italian Grant wvill be in accordance with World Bank Guidelines,and will be open to all bidders from eligible source countries as defined in the Guidelinies.

- 19 -

administration, as well as a workshop, an equipment shed and improvements towarehouses in the port of Massawa, estimated at less than US$500,000 equivalent percontract up to an aggregate amount of US$4.6 million, will be awarded on the basis ofNational Competitive Bidding (NCB) procedures acceptable to IDA. This would includeadvertising the works, public opening of bids, clearly stated evaluation criteria and awardto the lowest bidder. Foreign bidders, if interested, would not be precluded fromparticipation. Assurances to this effect have been obtained and the NCB documents,based on World Bank Standard Bidding Documents, will be subject to prior review byIDA. The Civil Works contracts will be supervised by consulting firms appointed inaccordance with Bank guidelines.

4.7 Equipment: The different contracts for procurement of general cargo andcontainer handling equipment, as well as for the tug boat and equipment and facilities forimproving operating practices in the two ports, including equipment for fire fighting andcombating potential oil spills, estimated at in total US$28.6 million, will be procuredthrough ICB following the Bank guidelines and using Bank Standard Bidding Documentswith appropriate modifications. Small quantities of goods such as office equipment andsupplies, consumable materials and spare parts, which are normally available off-the shelfat competitive prices and cannot be grouped into packages of at least US$25,000, wouldbe procured through prudent national shopping, based on price quotations obtained fromat least three reliable suppliers, provided that the aggregate amount does not exceedUS$500,000.

4.8 Consultancy Services and Studies: Consultancy services funded under the Creditand the Italian Grant, totaling US$5.4 million, would be for: (i) supervision of civil works;(ii) short term experts to assist in drafting technical specifications and bidding documents.for equipment and spare parts procurement, evaluation of bids and recommendations foraward of contracts; (iii) specific studies in the field of maritime and port legislation, MIS,cost accounting, tariff analysis and commercialization of port activities; (iv) a study of thelong term development of the port sector (Phases II and III); and (v) short term technicalassistance in port management and operations, and equipment maintenance.

4.9 The consultancy services will be procured in accordance with the Bank'sGuidelines for the Selection and Employment of Consultants published in January 1997and using the Standard Form of Contract for Consultants Services. The services will beprocured through competition among qualified short-listed firms in which selection will bebased on Quality-and Cost-Based Selection (QCBS). For short term assignments(assistance in drafting bidding documents, specific studies in port legislation, MIS, costaccounting, tariff analysis and commercialization of port activities, technical assistance inport management and equipment maintenance) estimated to cost less than US$75,000 percontract up to an aggregate of US$500,000, the selection would be based on theConsultants' Qualifications. Single-Source Selection will be exceptionally used forvery small (short term) assignments estimated to cost less than US$25,000 per contract upto an aggregate of US$150,000, where a rapid selection is required and/or only onefirm/individual is qualified.

- 20 -

4.10 Short-lists for contracts (estimated at less than US$200,000 per contract) for thedesign and site supervision of buildings to be constructed in the port of Massawa (portadministration, customs, workshop, equipment shed, warehouses) may be comprisedentirely of national consultants if a sufficient number of qualified firms (at least three) areavailable at competitive costs. However, if foreign firms have expressed interest for thosecontracts, they will not be excluded from consideration. The standard Letter of Invitationand Form of Contracts as developed by the Bank will be used for appointment ofconsultants. Simplified contracts will be used for short-term assignments, i.e. those notexceeding three months, carried out by firms or individual consultants. The Governmenthas been briefed about the features of the new Consultants Guidelines (January 1997), inparticular with regard to advertisement and public bid opening.

4.11 Training: Selection of consultants and firms providing services for lectures andtraining, estimated to cost less than US$100,000 per contract up to an aggregate ofUS$700,000 will be based on the Consultants' Qualifications among those expressinginterests in the assignment or approached directly. Single Source Selection, estimated atless than US$25,000 per contract up to an aggregate of US$100,000, will be exceptionallyused for the training of management staff.

4.12 All IDA and Italian grant financed contracts for goods and works aboveUS$100,000 would be subject to prior review by IDA, as would all consultancy contractsfor firms above US$100,000 and for individuals above US$75,000. A GeneralProcurement Notice (GPN) was initially published in the Development Business Forum onJune 16, 1996, and an update of the GPN was published in issue 464 of June 16, 1997.An invitation for prequalification of civil works contractors was published on June 16,1997. Specific procurement notices will be published as per the Guidelines.

4.13 The PCU established for the project has already sent two of its key staff to attend aBank sponsored seminar in procurement of Goods and Equipment. The same staff arescheduled for similar training in Procurement of Works and Consulting Services, to becompleted by March 31, 1998. In preparing TORs, technical specifications and biddingdocuments, as well as for evaluating proposals and negotiating contracts, the PCU willalso have access to expertise from DMT's Engineering Department, and short termConsultants from specialized firms. The importance of having PCU adequately staffed forcarrying out procurement efficiently during the implementation of the project wasdiscussed and agreed with the Borrower during post-appraisal.

4.14 At negotiations, standard procurement processing time for key activities wereagreed with the Borrower, and are reflected in the PIP.

- 21 -

C. DISBURSEMENT

4.15 Around 53 percent of the total project cost will be covered by the IDA Credit.The IDA Credit will be disbursed as in Table 4.2.

Table 4.2: IDA Disbursement Categories

Disbutrsenenil (Category IDA Amount % of Expenidituire to be financed-(USS nillion,)

Civil Works 3.0 100% of foreign expenditure and90% of local expenditure

Equipment 22.0 100% of foreign expenditure and90% of local expenditure

Consulting Services and Studies 1.2 100%Training 0.2 100%Operating Cost 0.1 50%PPF Advance 0.4 Amount dueUnallocated 3.4

Total IDA 30.3 _-

4.16 Around 36 percent of the total project cost will be covered by the Italian grant.For individual project components the Italian Grant will be disbursed as in Table 4.3.

Table 4.3: Italian Grant Disbursement Categories

Disbtursemetnt Category Italian Grant % of Expendituire to be finanicedAmounit

(USS million) :-Civil Works 12.7 100% of foreign expenditure and

90% of local expenditureEquipment 4.3 100% of foreign expenditure and

90 % of local expenditureConsulting Services and Studies 3.7 100%Training 0.3 100%

Total Italian Grant 21.0

4.17 The project is expected to be completed by December 3 1, 200 1, and the CreditClosing Date is June 30, 2002.

4.18 All disbursements will be frilly documented to the satisfaction of the Association.Contracts for goods, civil works, and consultancy firms valued less than US$ 100,000, andfor consultancy services with individuals valued less than US$50,000, and all training willbe disbursed under Statements of Expenditures (SOE). Documents verifying expenditures

- 22 -

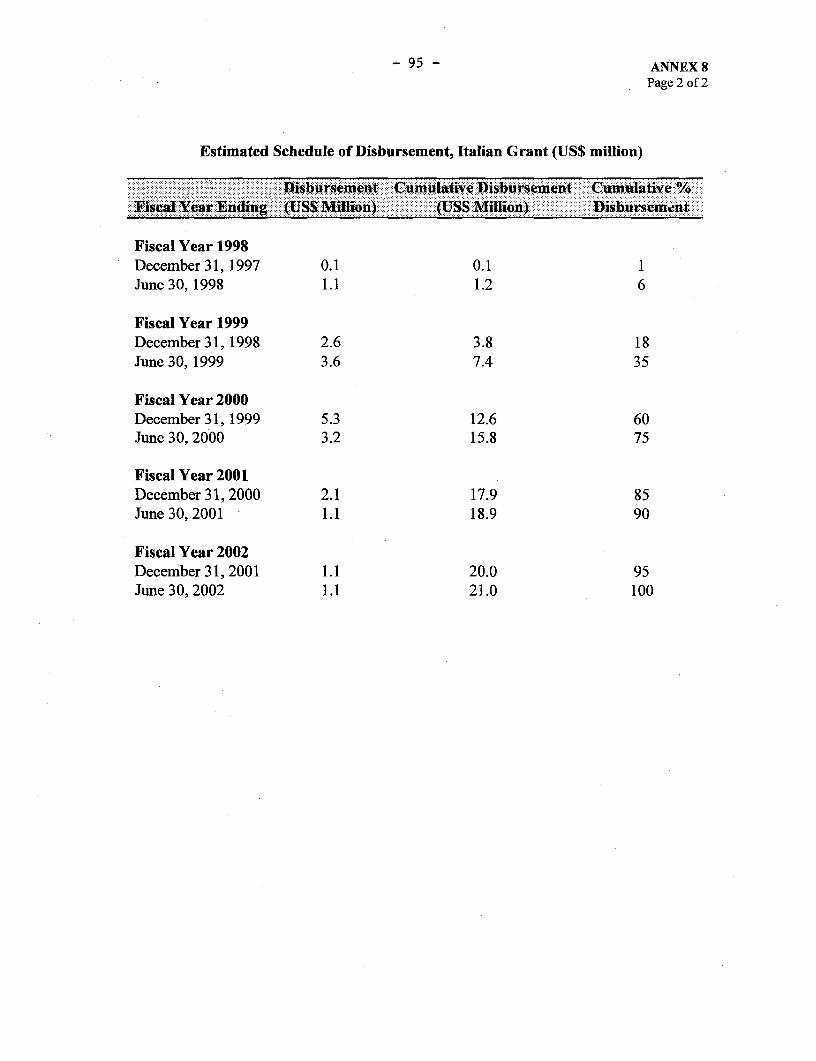

under the SOE procedures will be retained for review by IDA supervision missions. Tofacilitate the availability of funds for the Project, a Special Account would be establishedand maintained on terms and conditions satisfactory to IDA. An initial deposit ofUS$500,000 will be replenished on the basis of satisfactory documentary evidence,provided to IDA, of eligible payments made from the account for goods and servicesrequired for the Project. An estimated schedule of disbursement of the proceeds from the.IDA Credit and the Italian Grant are in Annex 8.

D. REPORTING AND AUDITING

4.19 The PCU (DMT) will be responsible for accounting, audit and financial reportingactivities. Funds accounts will be maintained in accordance with Generally AcceptedAccounting Standards (GAAS) on a PC-based accounting program. Training will beprovided to the PCU staff to familiarize them with the accounting and MIS programsbefore the beginning of project implementation. The annual financial statements will beaudited in accordance with International Standards of Auditing by independent auditorsacceptable to the Government and IDA.

4.20 The Project's audited financial statements with the auditor's report thereon, andthe auditor's management letter covering internal control and any accounting proceduresweaknesses discovered as a result of the audit, will be sent to IDA within six months ofthe end of the period audited.

4.21 The DMT will also have the financial statements of Massawa and Assab portsaudited by independent auditors acceptable to the Government and IDA. The auditedaccounts of the two ports will be sent to IDA not later than six months after the end of thefiscal year.

4.22 DMT through the PCU will be responsible for overall Project reporting and willprovide quarterly progress reports. DMT will also be responsible for the preparation of anevaluation report on the project's execution and initial operation, which will be annexedunedited to the Implementation Completion Report (ICR) to be finalized within sixmonths of the closing date of the proposed project.

E. MONITORING AND SUPERVISION

4.23 To facilitate control and monitoring, the PCU will maintain a projectimplementation schedule which is being prepared using computerized network software.This will enable the PCU to monitor and track project progress in procurement,disbursements and implementation, and to take remedial action where necessary.

4.24 The PIP includes an agreed format of a quarterly progress report, which IDAshould receive from the PCU on implementation progress of the project. The quarterlyreport will also include port statistics including operational performances of the two ports.

- 23 -

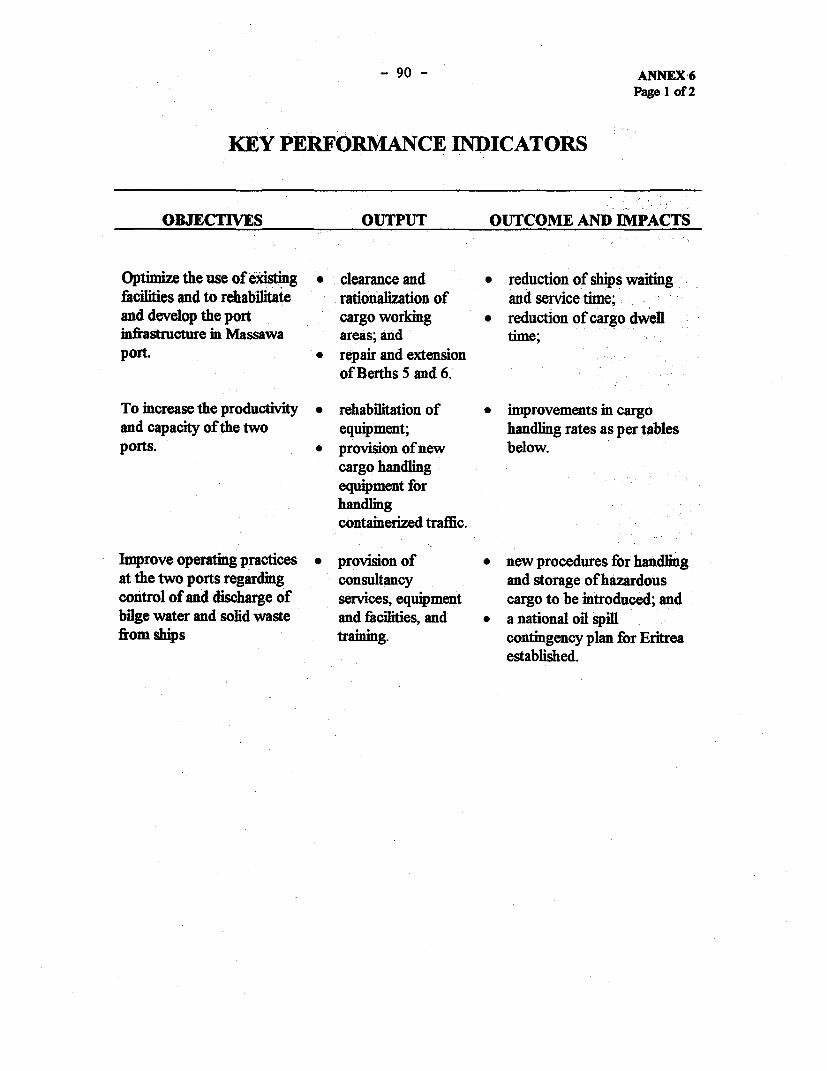

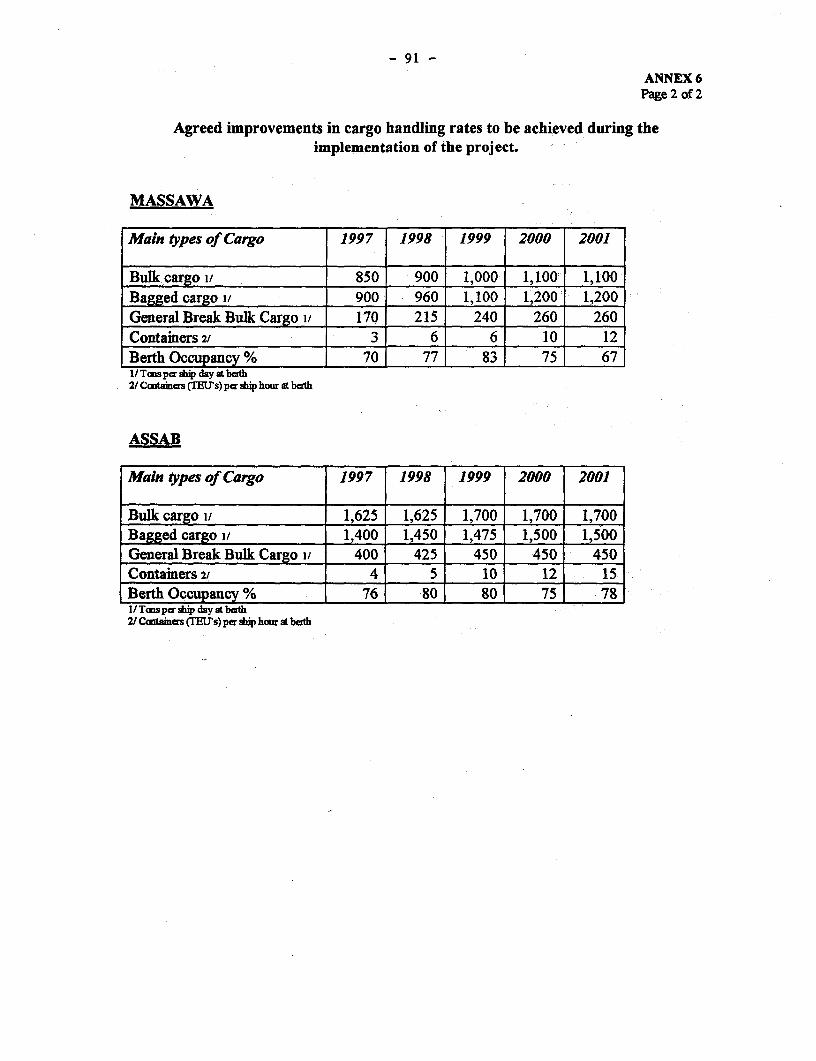

A set of key performance indicators on improvements in cargo handling capacities andoperational productivity to be attained during the implementation of the project have beenagreed with DMT and are included in Annex 6.

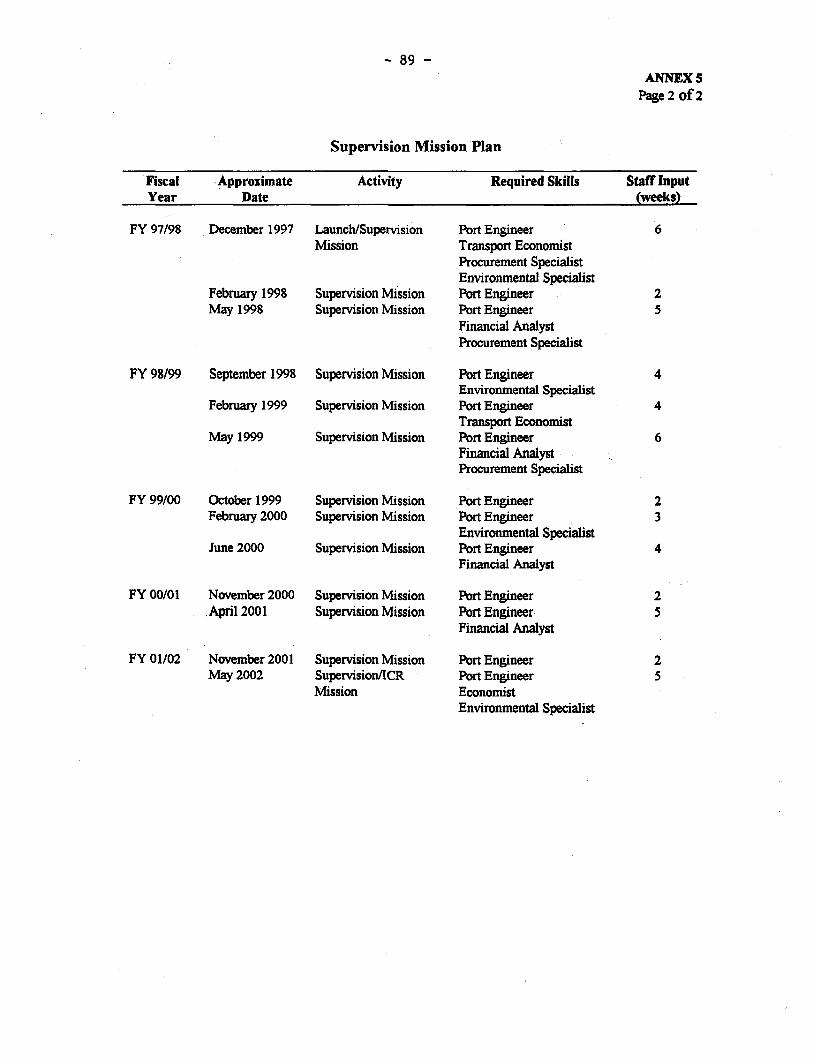

4.25 IDA would monitor project implementation through field visits, implementationsupport missions, reviews of progress reports and consultations with the borrower and thetwo ports. Estimates of timing of IDA missions, areas of focus, skills requirements andinputs are outlined in Annex 5. On or around November 30, 1999, the Government wouldconvene a mid-term review mission. The objective of the mission would be to review theoverall status of project implementation, adherence to the implementation plan, anddetermine any required changes in design or implementation arrangements needed toensure achievement of the project's development objectives. Specifically, the reviewmeeting would focus on the status of progress in: (i) revise and enact the country'smaritime legislation; (ii) revise and enact legislation to establish the two ports as separatejuridical authorities; (iii) establish the minimum return the Government expects the portsto generate from their operations; (iv) establish a capital structure for each port authority,including the terms and conditions of long-term debt in this structure; and (v) establish apolicy for the financing of future investments in the port sector.

- 24 -

5. ECONOMIC ANALYSIS

A. BACKGROUND

5.1 The ports of Massawa and Assab perform substantially different roles for theEritrean economy:

Massawa: the port is the land-sea interface for Eritrean overseas trade. The porthas been used quite extensively for food relief to Northern Ethiopia but transittraffic now forms only a small part of total port traffic. The port has littlecompetition for Eritrean cargo as both Assab and Port Sudan are very inadequatesubstitutes.

Assab: the main transit port for Ethiopian trade which handles very little Eritreandry cargo. The oil refinery does supply Eritrea but oil traffic will be little affectedby the proposed project. The port could be characterized as a revenue andemployment generating enterprise for the Eritrean economy. While Assabpresently handles 85 percent of Ethiopia's overseas trade, Djibouti is a potentialalternative and increasing efforts are being made to improve its links with Ethiopia.

5.2 These rather different roles have important implications for the distribution ofbenefits generated by the proposed port investments. Such benefits are normallydistributed between the port operator and the port users. In the case of Assab, many ofthe port user benefits will accrue to the Ethiopian economy and this, together with thepotential competition from the port of Djibouti, has to be factored into the analysis inorder to obtain the likely benefits to the Eritrean economy.

5.3 The proposed investments have been evaluated using standard port appraisalmethodology and techniques, assessing the implications of port traffic, cargo handlingrates and berth capacity on berth occupancy, shipping delays and thus user costs. Theanalysis is based on queuing theory with a random arrival pattern for ships and 'Erlang 2'distributions for ship service times'. These statistical distributions were validated bycomparison to the actual arrival and service patterns at the two ports. The costs andbenefits of the proposed investments are estimated net of indirect taxes and other transferpayments. Shadow pricing of unskilled labor and other local costs was not consideredrelevant to the analysis because:

* a very high proportion of the costs (almost 90 percent) and all the benefits(reduced shipping costs) will be in foreign exchange; and

* unskilled labor will form a very small proportion of total construction costs and aneven smaller proportion of changes in port operating costs, given the type ofequipment used.

UNCTAD "Port Development", Second Edition. New York, 1985

- 25 -

B. MASSAWA PORT INVESTMENT2

The Demand for Port Services

5.4 Traffic at the port of Massawa has undergone very substantial changes since 1994with a major decline in food imports and increases in cement and general cargo imports.There is an extremely limited database upon which to forecast future traffic and,consequently, forecasts must be treated with caution and additional weight given to theproject sensitivity analysis.

Table 5.1 - Massawa Port: Traffic Forecasts

Low Traffic Base Traffic High Traffic

Population growth p.a. (%) 2.7 2.7 2.7

GNP growth p.a. (%) 3.0 7.5 9.0

Cereals production p.a. (%) 3.0 6.0 8.0

Traffic 2000 '000 tonnes

Bulk 210 120 70

Bagged 295 380 440

Break bulk 195 235 310

Container 80 135 170

Total 780 870 990

Traffic 2005 '00 toines

Bulk 245 110 65

Bagged 345 410 550

Break bulk -225 255 270

Container 105 230 325

Total 920 1,005 1,210

5.5 In terms of port services, there is relatively little difference in the handling rates forbulk and bagged cargo. The important differences are with respect to break bulk andcontainer traffic which presently have very low handling productivity at Massawa.

2 The analysis of the Massawa Port Component is detailed in Annex I

- 26 -

Operational Impact of Proposed Investments

5.6 Without a significant increase in effective port capacity, Massawa will not be ableto handle the base traffic forecast. The total forecast tonnage grows at a relatively modestrate but there is a significant shift to containers and general cargo. Berth occupancy willbe 92 percent in 2000, with very long berthing delays, and 106 percent in 2005, which isnot feasible (100 percent berth occupancy would theoretically result in an infinite berthingdelay). Some expansion in port capacity is thus urgently required, if Massawa is to servicethe expanding Eritrean economy.

5.7 The investment proposed for the port of Massawa can be conceptually consideredas three distinct and separable components:

* Clearance and rationalization of cargo handling and storage areas, combined withimproved handling operations and management;

* New general cargo handling equipment which will only become fully effective withthe rationalized cargo working areas; and

* Repair of berths Nos. 5 & 6, extension of berth 6, deepening of the berth draft to12 meter, and the provision of specialized ship-to-shore container handlingequipment.

5.8 The expected impact of the investment on cargo handling productivity, berthoccupancy.and berthing delays is detailed in Table 5.2. The effects of each component areassessed sequentially, in order of their cost.

Table 5.2 - Massawa Port: Impact of Port Investments

(i) Cargo Handling Productivity (tonnes/day)

ACargo Category Without Rationalization of New HandlingProect -Cargo Handling Areas Equipment

Bulk Cargo 850 950 1100

Bagged Cargo 900 1,000 1200

Break Bulk Cargo 200 230 270

Containers 720 1,375 2,350*

Ferry Cargo 65 65 65* possible only with extension of Berth No. 6

- 27 -

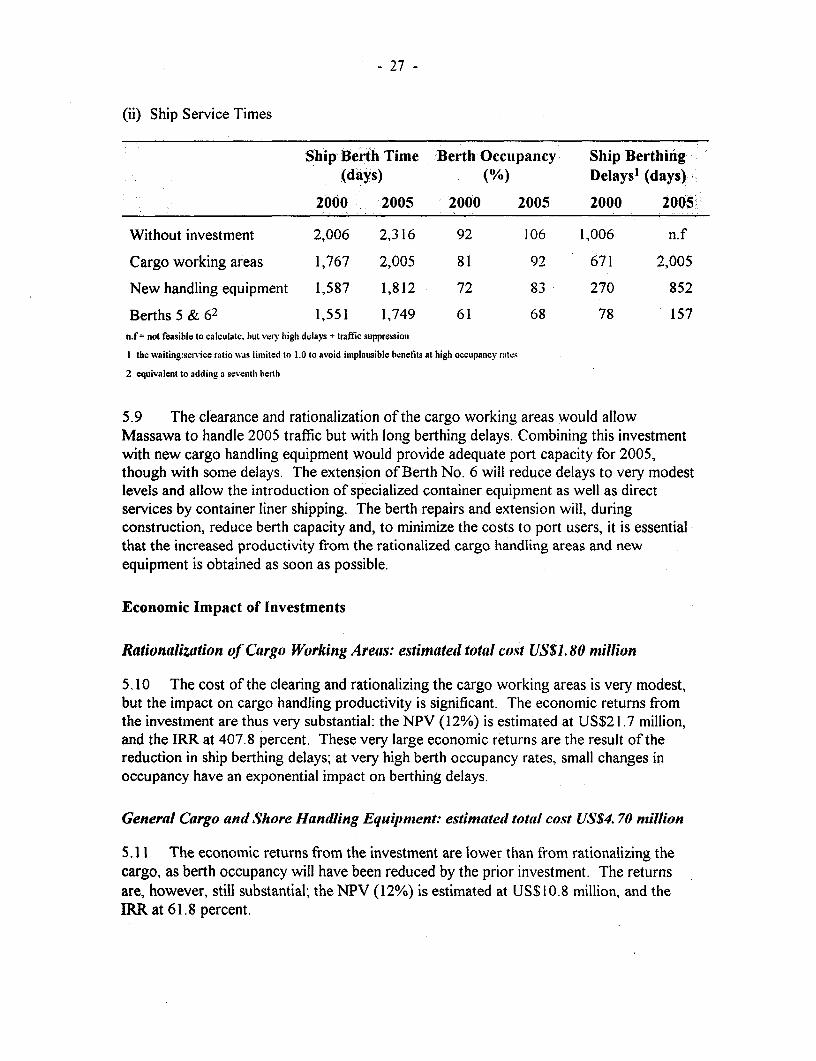

(ii) Ship Service Times

Ship Berth Time Berth Occupancy Ship Berthing(days) (8/e) Delays' (days)

2000 2005 2000 2005 2000 2005

Without investment 2,006 2,316 92 106 1,006 n.f

Cargo working areas 1,767 2,005 81 92 671 2,005

New handling equipment 1,587 1,812 72 83 270 852

Berths 5 & 62 1,551 1,749 61 68 78 157n.f = not feasible to calculate. hut very high dolays + traffic suppression

I the waiting:service ratio %%as limited to 1.0 to avoid inmplausible benefits at high occupancy ratczi

2 equivalent to adding a seventh berth

5.9 The clearance and rationalization of the cargo working areas would allowMassawa to handle 2005 traffic but with long berthing delays. Combining this investmentwith new cargo handling equipment would provide adequate port capacity for 2005,though with some delays. The extension of Berth No. 6 will reduce delays to very modestlevels and allow the introduction of specialized container equipment as well as directservices by container liner shipping. The berth repairs and extension will, duringconstruction, reduce berth capacity and, to minimize the costs to port users, it is essential*that the increased productivity from the rationalized cargo handling areas and newequipment is obtained as soon as possible.

Economic Impact of Investments

Rationalization of Cargo Working Areas: estimated total cost US$1. 80 million

5.10 The cost of the clearing and rationalizing the cargo working areas is very modest,but the impact on cargo handling productivity is significant. The economic returns fromthe investment are thus very substantial: the NPV (12%) is estimated at US$21.7 million,and the IRR at 407.8 percent. These very large economic returns are the result of thereduction in ship berthing delays; at very high berth occupancy rates, small changes inoccupancy have an exponential impact on berthing delays.

General Cargo and Shore Handlling Equipment: estimatedl total cost US$4.70 million

5.11 The economic returns from the investment are lower than from rationalizing thecargo, as berth occupancy will have been reduced by the prior investment. The returnsare, however, still substantial; the NPV (12%) is estimated at US$10.8 million, and theIRR at 61.8 percent.

- 28 -

Berths 5 & 6 and Container Tower Crane: estimated total cost US$17. 65 million

5.12 The repair and extension of the berths will effectively add another berth and thussubstantially increase port capacity. The construction will allow the introduction ofspecialized container ship-to-shore handling equipment and the deepening of the draft to12 meters will allow Massawa to handle container liner ships. The analysis of the benefitsfrom direct liner services is based on the very modest assumption that 25 percent ofinbound containers will be landed from direct services. The overall economic returns, forthe period to 2005, are modest; the IRR is estimated at 12 percent, and the NPV(12%) iszero.

5.13 Benefits increase substantially in the later years of the appraisal period (the annualrate of return is over 25 percent in 2005) and a longer appraisal period, rather than the useof a residual value, would increase estimated returns significantly. Postponingimplementation of the component is not justified as the increased congestion costs duringthe construction period, when there will only be five operational berths, are greater thanthe increase in benefits from postponement.

Total Massaiva Investment: estintated total cost US$29.45 million

5.14 In addition to the specific investments, technical assistance, training and someexpansion in administrative facilities are also required to achieve the overall improvementin port performance. These complementary activities are expected to cost approximatelyUS$5.30 million. It is not feasible to assign specific benefits to these inputs and they arethus treated as an essential project overhead.

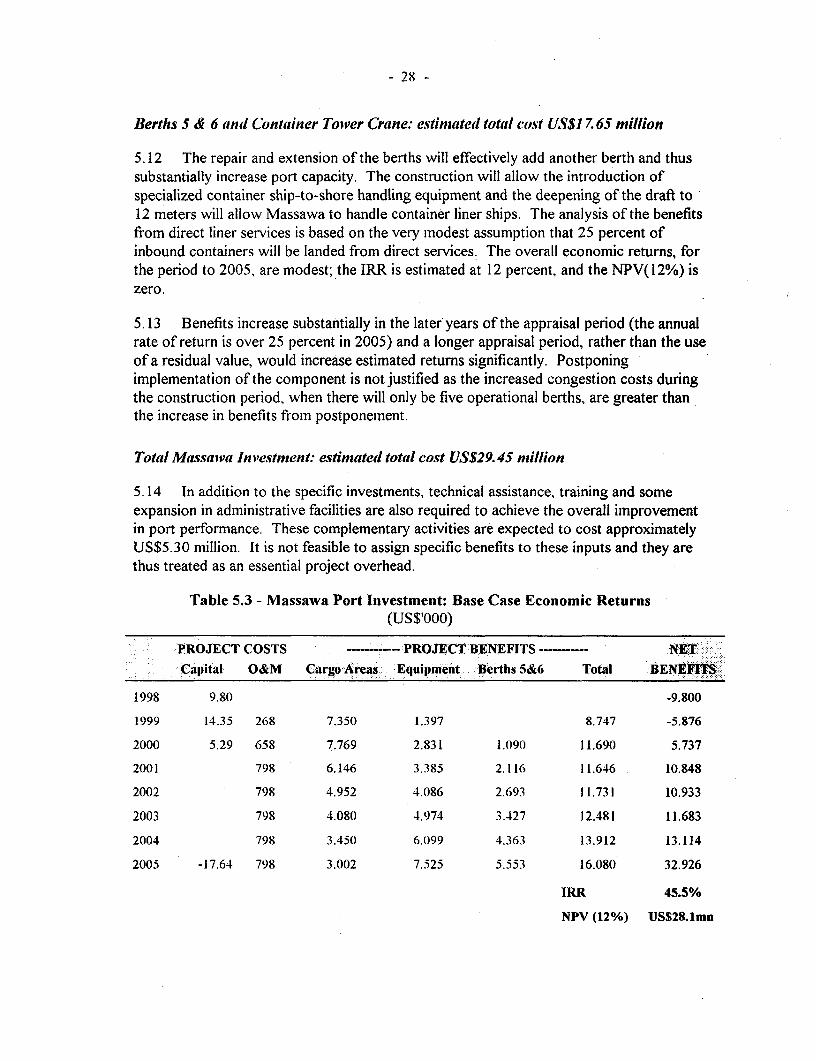

Table 5.3 - Massawa Port Investment: Base Case Economic Returns(US$'000)

PROJECT COSTS ------- PROJECT BENEFITS -------- NET -Capital O&M CargoAreas& -Equipmentt, Berths 5&6 Total BENEFTS.

1998 9.80 -9.800

1999 14.35 268 7.350 1.397 8.747 -5.876

2000 5.29 658 7.769 2.831 1.09() 11.690 5.737

2001 798 6.146 3.385 2.116 11.646 10.848

2002 798 4.952 4.086 2.693 11.731 10.933

2003 798 4.080 4.974 3.427 12.481 11.683

2004 798 3.450 6.099 4.363 13.912 13.114

2005 -17.64 798 3.002 7.525 5.553 16.080 32.926

IRR 45.5%

NPV (12%) US$28.1mn

- 29

5.15 Overall, the project generates a high economic rate of return which is notunexpected given that, without the investment, the port will become totally congested bythe year 2005 and Eritrea does not have a satisfactory alternative access to the sea trade.

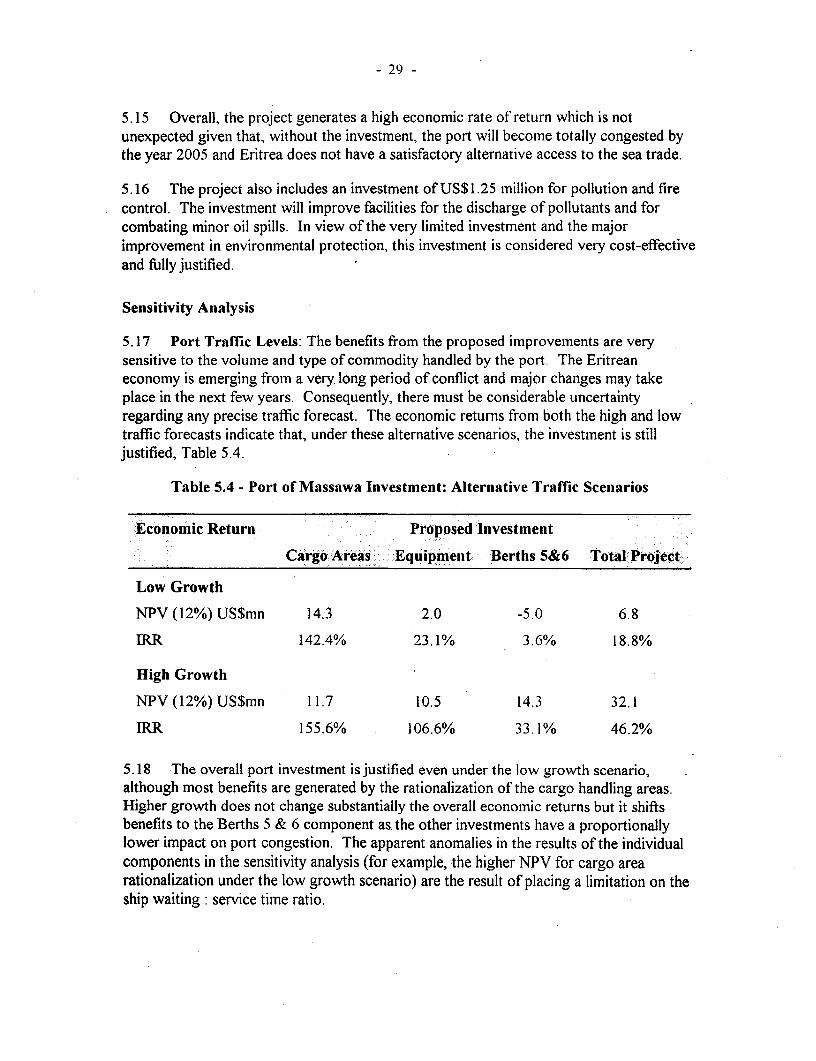

5.16 The project also includes an investment of US$1.25 million for pollution and firecontrol. The investment will improve facilities for the discharge of pollutants and forcombating minor oil spills. In view of the very limited investment and the majorimprovement in environmental protection, this investment is considered very cost-effectiveand fully justified.

Sensitivity Analysis

5.17 Port Traffic Levels: The benefits from the proposed improvements are verysensitive to the volume and type of commodity handled by the port. The Eritreaneconomy is emerging from a very long period of conflict and major changes may takeplace in the next few years. Consequently, there must be considerable uncertaintyregarding any precise traffic forecast. The economic returns from both the high and lowtraffic forecasts indicate that, under these alternative scenarios, the investment is stilljustified, Table 5.4.

Table 5.4 - Port of Massawa Investment: Alternative Traffic Scenarios

:Economic Return Proposed Investment

Cargo Areas- Equipment Berths 5&6 Total Project

Low Growth

NPV (12%) US$mn 14.3 2.0 -5.0 6.8

IRR 142.4% 23.1% 3.6% 18.8%

High Growth

NPV (12%) US$mn 11.7 10.5 14.3 32.1

IRR 155.6% 106.6% 33.1% 46.2%

5.18 The overall port investment is justified even under the low growth scenario,although most benefits are generated by the rationalization of the cargo handling areas.Higher growth does not change substantially the overall economic returns but it shiftsbenefits to the Berths 5 & 6 component as, the other investments have a proportionallylower impact on port congestion. The apparent anomalies in the results of the individualcomponents in the sensitivity analysis (for example, the higher NPV for cargo arearationalization under the low growth scenario) are the result of placing a limitation on theship waiting: service time ratio.

- 30 -

5.19 Project Investmeint Costs: The project is relatively insensitive to plausiblechanges in investment costs. Under the base level estimates, project costs would have toincrease by over 150 percent to reduce the economic return to 12 percent. Under the lowgrowth scenario, a 40 percent increase in project costs would reduce the economic returnto 12 percent. Such cost escalation is unlikely as the costs of the equipment (30 percentof project costs) are known, and detailed engineering studies have been undertaken.

5.20 Cargo Handling Rates: If the improvements in cargo handling rates are reducedto 50 percent of their expected levels, project benefits will be reduced significantly. Theproject is still, however, justified as the addition of the additional berth provides theadditional capacity required. The economic returns under the base and high growthscenarios remain over 30 percent but, under the low traffic scenario, the economic returnsfall to a rather marginal 12.2 percent. The estimated gains in cargo handling rates atMassawa will, however, only bring rates for bulk, bagged and break bulk cargo to levelsalready achieved at Assab and are considered fuilly feasible.

5.21 Overall Assessment of Project Sensitivity: the proposed project is justified as arelatively short-term capacity enhancing investment, irrespective of the traffic scenario.Even under the low traffic scenario (considered highly unlikely by the Government and thePort Authority), a satisfactory rate of return is generated and it would require almost a 40percent increase in project costs to reduce the rate of return to a marginal 12 percent.Under the high traffic scenario, additional port capacity would become desirable towardthe end of the project period, justifying the inclusion of a longer term planning componentwithin this project.

C. ASSAB PORT INVESTMENT 3

The Demand for Port Services

5.22 Over 95 percent of dry cargo transiting the port are Ethiopian imports or exports.Traffic demand is thus determined by the development of the Ethiopian economy and, inthe longer term, by Ethiopia's development of alternative transit routes4 . During theperiod 1994 - 1996, overall port tonnage changed little but there was a major shift fromfood imports to fertilizer and other imports. Economic growth in Ethiopia is still heavilydependent on agriculture which, in turn, depends on rainfall. Marked fluctuations in thevolume and composition in Ethiopian cargo are thus likely until the economy becomes lessdependent on agriculture. Traffic forecasts have been based on three scenarios for theEthiopian economy, Table 5.5. The most marked change in Assab traffic in recent years

For more detailed analvsis of the Assab Port Investment, see Anne.N 2