institutional investors corporate governance for ... investors & corporate governance for...

TRANSCRIPT

Oxford University18th May 2012

Institutional Investors & Corporate Governance for sustainability

Dr Raj Thamotheram

What I really appreciated about today

Creative/challenging/sophisticated

Inter‐discplinary

Examined most parts of the investment chain

ESG conidered in an integrated manner

Interaction of real world academics with reflective practitioners

And what would I love to see more of next time

More focus on the hidden gorillas in the ecosystem – investment consultants, analysts, financial media

Make use of the points of intellectual flux – behavioural finance

More practitioners, including mainstream

More challenging of “BAU” assumptions

Focus on what’s really critical (vs what creates papers to publish)

Think communication to the public

Action reseach – organisational transformation/management of change /immunity to change

11 fatalities 17 injuries

Latest BP cost estimate $40 billion 30% share price drop1‐year suspension of dividends

“The Dominant Narrative” – the BP example

"It's very dangerous to join up dots that may not be appropriate to join up" Tony Hayward

“I left BP a long time ago, four years” Lord Browne

“an Act of God” Rick Perry, Governor of Texas

Warning signs prior to the disaster

Source: Yahoofinance.com “ “

Up until April 19 (the day before the Deepwater Horizon explosion), his [BP’s] performance was excellent. An investor close to BP quoted by The Financial Times, July

25th 2010

TexasRefineryAccident

TexasRefineryAccident

AlaskaOil

Spill

AzerbaijanGas leak

ViolationsOf CleanWater Act

PenaltiesFrom the

OSHA

Gulf ofMexicoOil spill

ThunderHorse

Accident

Charges forManipulation

Of gasmarket

Grangemouth2000

How much attention did “sell‐side” pay to safety?

Before the oil spill, 6 occurrences every 100 pages= the vast majority of reports do not talk about these risks at all.

Behavioral finance expert: “analysts are biased”

Unicredit: analysts claim that BP has a good operational momentum because of its“first‐mover advantage in cost cutting” (17 December 2009)

5 = buy or strong buy recommendations4 = add, overweight, outperform and accumulate3 = hold, perform, neutral2 = reduce, underweight and underperform1 = sell or strong sell

Source: SHEFRIN Hersh, CERVELLATI Enrico Maria, “BP’s failure to debias: underscoring the importance of behavioral corporate finance”, 21st February 2011

Are asset owners & “buy‐side” much better?

Sadly, no!

Only 60% of capital voted at BP’s 2010 AGM

57% of votes in favour of chair of safety committee! (Only leaving in 2012!)

Even proxy voting agencies recommended abstain (ISS) or vote against (Glass Lewis)

Source: BP plc, ISS ProxyExchange

Another Narrative

In the end it all comes down to….We are all co‐creators of a dysfunctional system

Investors are very important enablers (aka “shareholder value maximisation”)

The stakeholders of investors are enablers of investors (Russian dolls)

We can therefore consciously aim to create a better system

Another Narrative

Since neither worldview can be proven, let’s choose the latter

So what went wrong?

NarrowConception of risk Shareholder

valuefundamentalism

Weak concernfor negativeexternalities

Regulatorycapture

Leadership & Governance

failuresOrganisationalLearning disabilities

Ineffectiveregulation

Focus on riskierand dirtier O&G

Outdated approachTo safety

Weak safetyculture

M&A and Outsourcing/SCM

Saviour CEO

SYSTEM O&G SECTOR BP

Fukushima

Driver Evidence?

Lack of concern for negative externalities

Full costs for dismantling plants, managing nuclear waste and damage in case of accident not “in the price”

Narrow conception of risk

Probabilistic thinking about a really severe earthquake excluded possibility of it+ failure to consider consequences of earthquake AND tsunami+ failure to consider how one accident could impact whole nuclear industry

Regulatory capture “Tepco’s cosy links to watchdogs” (FT)+ Lack of support from government for the Japanese nuclear industry regulator since nuclear was a non-negotiable matter of national energy independence

Organisational learning disabilities

Lack of learning from earlier near misses

Leadership & governance failures

Weak standards of governance (non independent board member)

Shareholder value fundamentalism

Focus on meeting investors’ expectations leading to a weak safety culture in practice

Source: THAMOTHERM Raj, LE FLOC’H Maxime, “Nuclear meltdowns are bad for returns”, FTfm talking head, Financial Times, 2ndMay 2011 with additional research by Kazutaka Kuroda

News Corporation

Driver Evidence?

Lack of concern for negative externalities

Over-dominant role of politically motivated media barons ignored in most countries & over long-term

Weak ethical standards taken as a given

Narrow conception of risk Cameron himself recognised risk from overly close lobbying relationships

Sector was widely viewed as low ESG risk

Regulatory capture NewsCorp promised end of Ofcom “as we know it”

Organisational learning disabilities

Repeated warning signs ignored

Leadership & governance failures

Over-dominant Chairmen, lack of independent directors, class B,

Shareholder value fundamentalism

Repeated examples of most investors and most analysts discounting ethical concerns & weak corporate governance

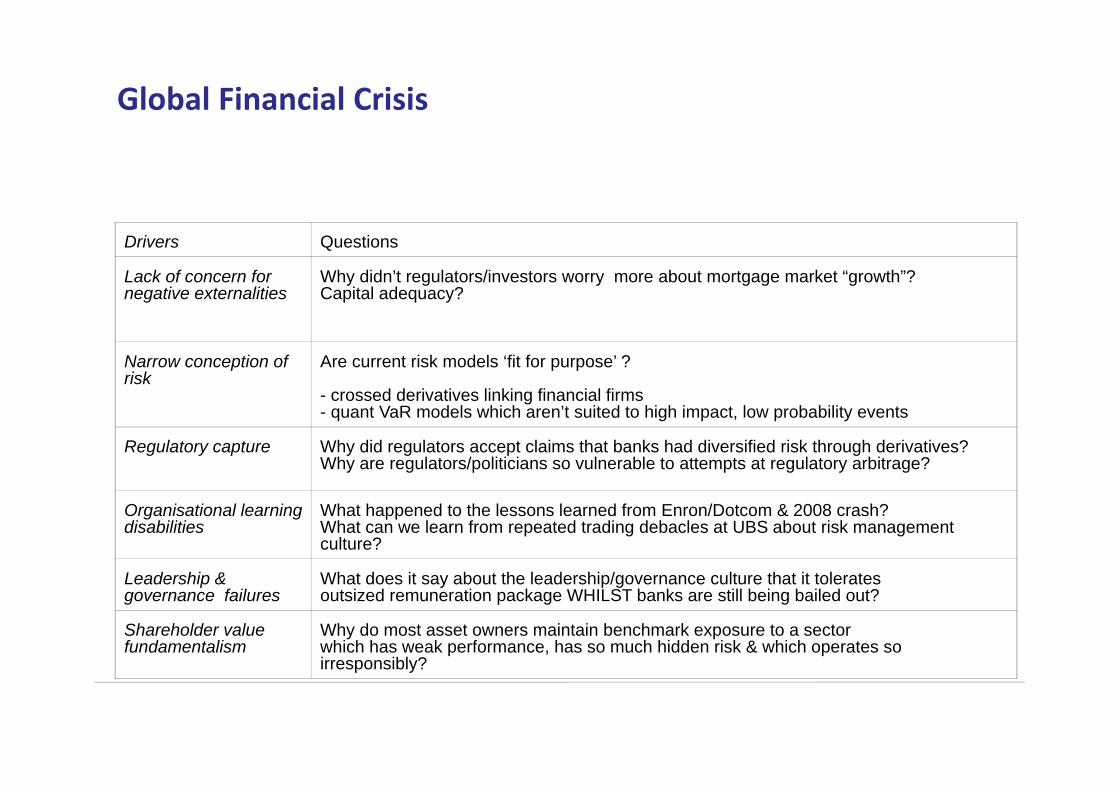

Global Financial Crisis

Drivers Questions

Lack of concern for negative externalities

Why didn’t regulators/investors worry more about mortgage market “growth”?Capital adequacy?

Narrow conception of risk

Are current risk models ‘fit for purpose’ ?

- crossed derivatives linking financial firms- quant VaR models which aren’t suited to high impact, low probability events

Regulatory capture Why did regulators accept claims that banks had diversified risk through derivatives? Why are regulators/politicians so vulnerable to attempts at regulatory arbitrage?

Organisational learning disabilities

What happened to the lessons learned from Enron/Dotcom & 2008 crash? What can we learn from repeated trading debacles at UBS about risk management culture?

Leadership & governance failures

What does it say about the leadership/governance culture that it tolerates outsized remuneration package WHILST banks are still being bailed out?

Shareholder value fundamentalism

Why do most asset owners maintain benchmark exposure to a sector which has weak performance, has so much hidden risk & which operates so irresponsibly?

Investors: our 10 deadly mistakes

Mistake Still true?

Passively/actively encouraged banks to pursue suspect / risky products & strategies

Passively/actively encouraged banks to over‐leverage on debt

Judged future performance solely on past performance

Approved pay designs which incentivised dangerous risk taking and “too big to fail” growth

Failed to get sell side/credit rating agencies to analyse bank’s corporate governance and didn’t resource/listen to independents who did do such analysis

Didn’t ensure boards were experienced enough and independent enough

Relied on the (inadequate) risk models that banks used (VaR) and didn’t invest in risk management models which they needed

Did not appreciate the systemic risks presented by the shadow banking system

Maintained excessive exposure to a high‐risk sector because of cap weighted indices.

Allowed banking lobby to set public policy agendas and capture regulators/politicians

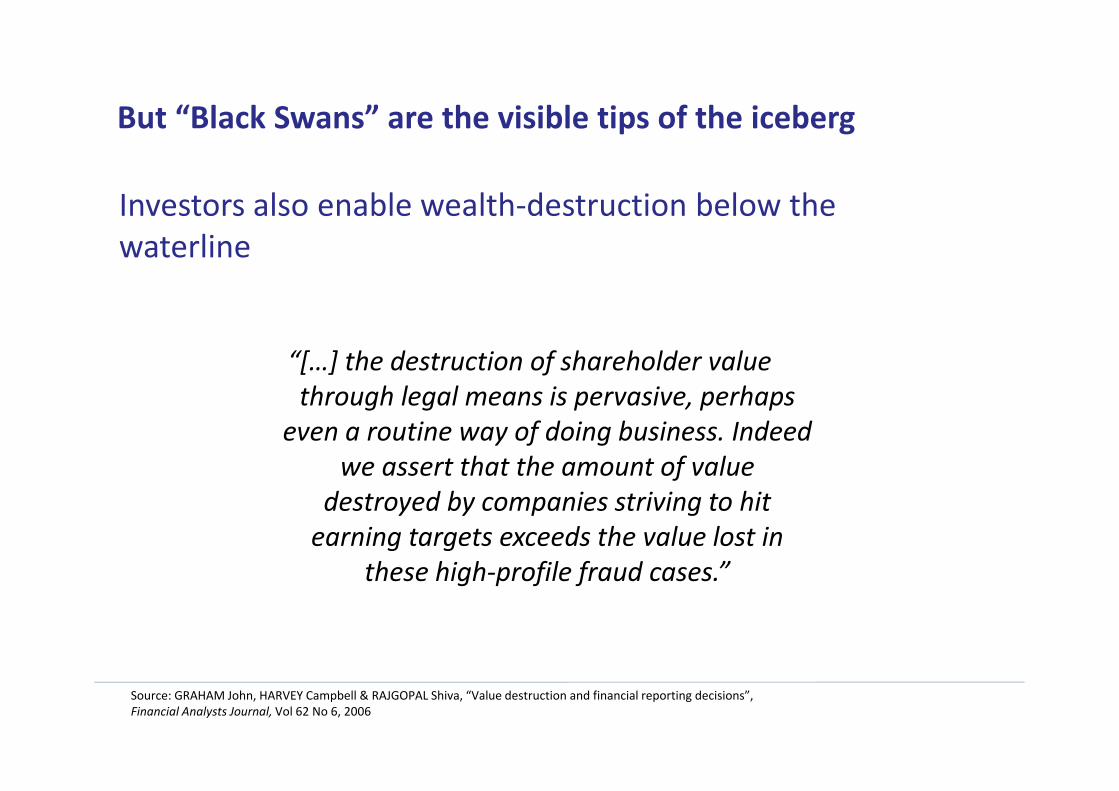

But “Black Swans” are the visible tips of the iceberg

“[…] the destruction of shareholder value through legal means is pervasive, perhaps

even a routine way of doing business. Indeed we assert that the amount of value

destroyed by companies striving to hit earning targets exceeds the value lost in

these high‐profile fraud cases.”

Source: GRAHAM John, HARVEY Campbell & RAJGOPAL Shiva, “Value destruction and financial reporting decisions”,Financial Analysts Journal, Vol 62 No 6, 2006

Investors also enable wealth‐destruction below the waterline

Dealing with our “Inner Jack Welch” – academics too!

“As long as the music is playing, you’ve got to get up and dance. We’re still dancing” Chuck Prince

Minor tweaks or fundamental changes?

The practical agenda

2. Better reporting

1. Better metrics

3. Better supply chain management

4. More respect for employees

5. Better leadership

6. Better regulation

The strategic agenda

2. CEOs enabled & held accountable for being authentic leaders

1. More diversity in corporate purpose

3. Boards are guardians of long‐term sustainable wealth creation

4. Courageous, ethical government and smarter regulation

5. Investing as if the long‐term matters

6. “Citizen investors” drive this agenda – transparency taps public pressure

Sensible investing: 7 questions for self‐assessment

2. Are our high level strategic choices re products/services made as much on the basis of the world that’s emerging as the world as it is today?

1. Are we well prepared, intellectually, to meet our clients needs in tomorrow's world?

3. Is our business as “fit for purpose” as it needs to be? Have we reviewed our organisational design to ensure good alignment with strategy?

4. Does our governance/leadership framework maximise our chances of delivering against our objectives?

5. Have we defined the battles we are committed to winning? Are we collaborating enough with other players to get system change?

6. Are we sure we are doing what we say we are doing “on the tin”?

7. Is our organisation able to do deep learning and implement this lessons?

If things can’t continue, then they will stop

On track for 6 degrees warming: International Energy Authority

Already using 1.5 planets

Income inequality levels at 1930s levels, youth unemployment is very high: a hungry man is an angry man

Growing influence of ultra‐nationalist, anti‐globalisation right‐wing parties

Democracy under threat in many countries

“State capitalism” becoming the preferred option

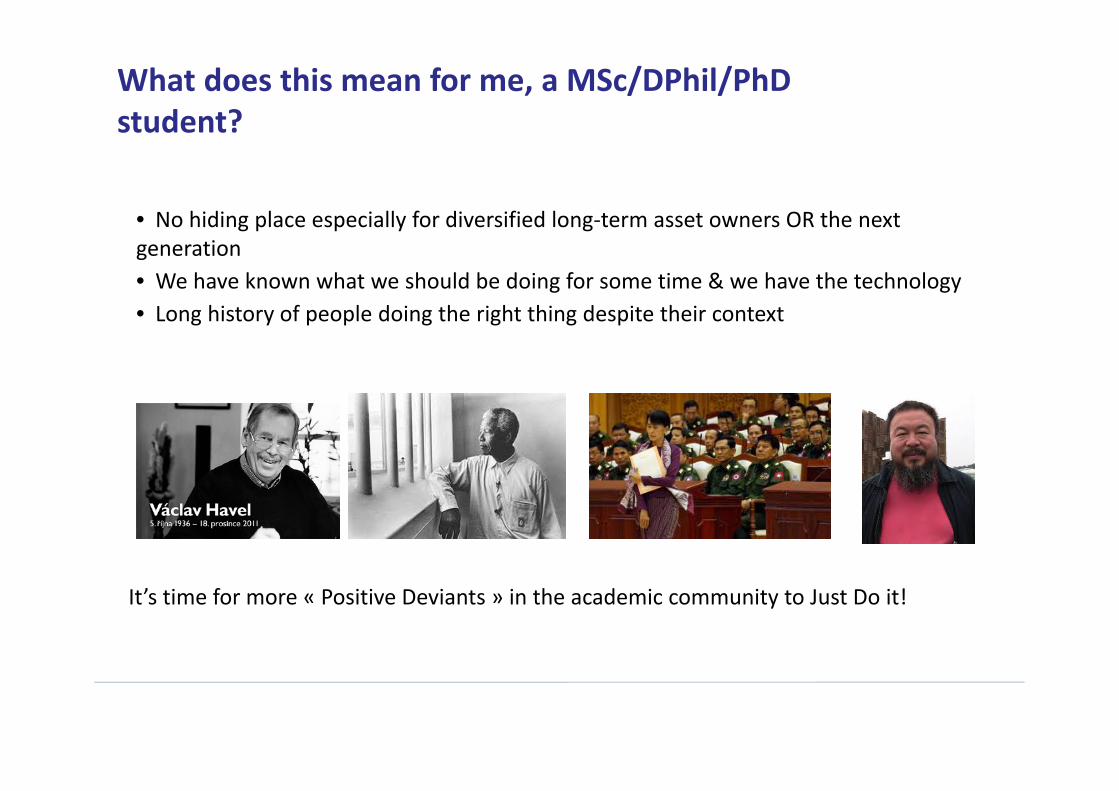

What does this mean for me, a MSc/DPhil/PhD student?

It’s time for more « Positive Deviants » in the academic community to Just Do it!

• No hiding place especially for diversified long‐term asset owners OR the nextgeneration• We have known what we should be doing for some time & we have the technology• Long history of people doing the right thing despite their context

Thank you, and please think how you can support this work!

www.sustainablefinancialmarkets.net www.preventablesurprises.com

Network for Sustainable Financial Markets