inspire | seminar: chinese tourists in hong kong

TRANSCRIPT

h1: Title Text

Hong Kong London Shanghai Singapore Yangon

h1: Client SectorChinese Tourists in Hong Kong: How much they spend, How satisfied they are, Where they shop, and What they buy.

Chinese Tourists in Hong Kong

Contact: Hendrik Kühl [email protected]

Dec 2015

© 2015 Sedgwick Richardson

The Challenge 2

Times of uncertainty: Hong Kong retail & tourism worries

”Hong Kong retail sales fell for a seventh straight month in September, as a drop in Chinese tourists and weak consumer sentiment amid a volatile stock market hurt retailers.

Retail sales dropped 6.4 percent from a year earlier, the biggest percentage decline since January this year, to HK$35.2 billion ($4.54 billion). That followed a revised 5.3 percent fall in August. In volume terms, September sales slipped 3.1 percent.

“The subdued performance of retail sales reflected the weakening of inbound tourism and, to some extent, the spillover of heightened stock market volatility during the summer on consumer sentiment," the government said in a statement.“

Source: Reuters (2015)

3

© 2015 Sedgwick Richardson

Between August and September 2015 Sedgwick Richardson polled 498 Chinese citizens visiting Hong Kong. Cohorts of equal sizes were prompted in close proximity to these malls: Times Square, IFC, Harbour City, Festival Walk and Hysan Place.

4

Contents

© 2015 Sedgwick Richardson

1. Research Demographics

2. Total Wallet

3. Shopper Satisfaction

4. Shopper Interests

5. Chinese Millennials

6. Recommendations

17%

13%

9%

5% 3%

53%

Guangdong Province

Shenzhen

Beijing

Fujian Province

Shanghai

Other

57%

35%

8%

Up to one week

One day

Long-term

© 2015 Sedgwick Richardson

Research Demographics 5

57%

35%

8%

Up to one week

One day

Long-term

Origin Duration

Who did we ask?

17%

13%

9%

5% 3%

53%

Guangdong Province

Shenzhen

Beijing

Fujian Province

Shanghai

Other

17%

13%

9%

5% 3%

53%

Guangdong Province

Shenzhen

Beijing

Fujian Province

Shanghai

Other

All respondents included in the survey were Chinese nationals. Genders were roughly evenly split (56% female) and Hong Kong first-time visitors accounted for 53% of the sample.

6

© 2015 Sedgwick Richardson

Total WalletHow much money do Chinese visitors plan to spend during their stay in Hong Kong?

© 2015 Sedgwick Richardson

Total Wallet

Total wallets

7

40%<5k HKD

3%>50k HKD

16%10k - 50k HKD

41%5k - 10k HKD

19% of the tourist from Mainland China have a

shopping wallet > 10k HKD.

© 2015 Sedgwick Richardson

8

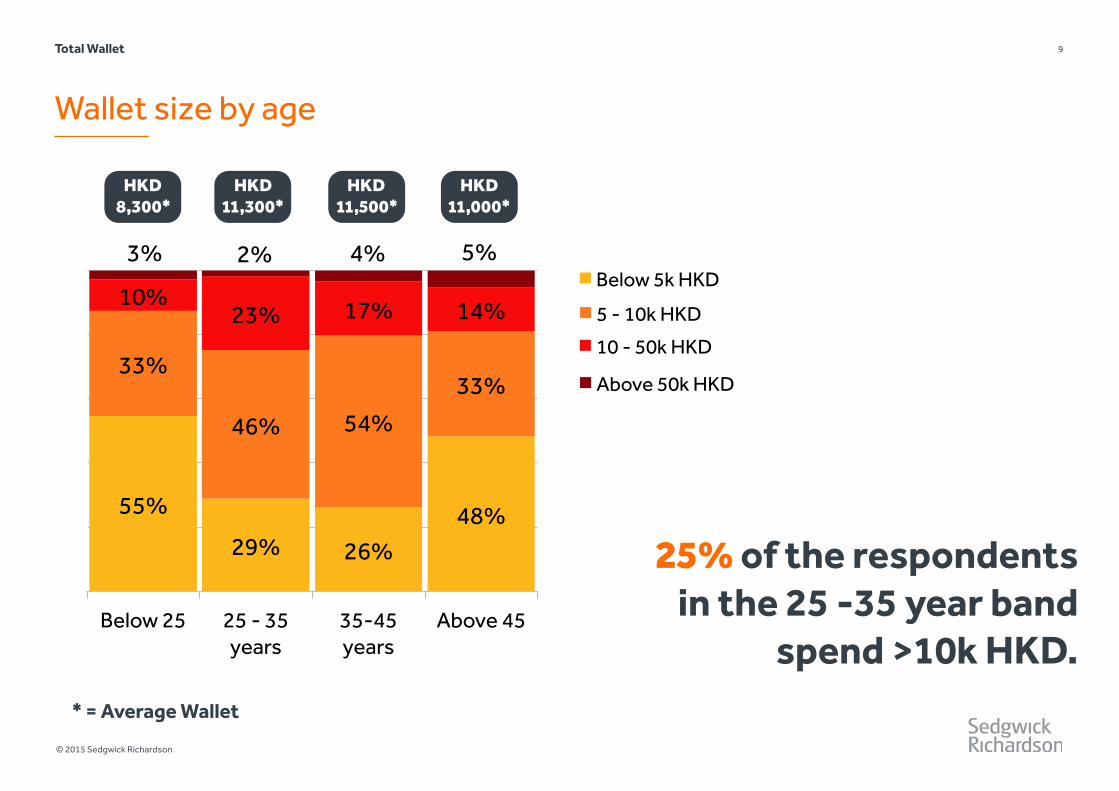

Do wallets differ by age?

Total Wallet

55%

29% 26%

48%

33%

46% 54%

33%

10% 23% 17% 14%

3% 2% 4% 5%

Below 25 25 - 35 years

35-45 years

Above 45

Below 5k HKD 5 - 10k HKD 10 - 50k HKD Above 50k HKD

© 2015 Sedgwick Richardson

Wallet size by age

9

HKD 8,300*

HKD 11,300*

HKD 11,500*

HKD 11,000*

Total Wallet

* = Average Wallet

25% of the respondents in the 25 -35 year band

spend >10k HKD.

55%

29% 26%

48%

33%

46% 54%

33%

10% 23% 17% 14%

3% 2% 4% 5%

Below 25 25 - 35 years

35-45 years

Above 45

Below 5k HKD 5 - 10k HKD 10 - 50k HKD Above 50k HKD

55%

29% 26%

48%

33%

46% 54%

33%

10% 23% 17% 14%

3% 2% 4% 5%

Below 25 25 - 35 years

35-45 years

Above 45

Below 5k HKD 5 - 10k HKD 10 - 50k HKD Above 50k HKD

55%

29% 26%

48%

33%

46% 54%

33%

10% 23% 17% 14%

3% 2% 4% 5%

Below 25 25 - 35 years

35-45 years

Above 45

Below 5k HKD 5 - 10k HKD 10 - 50k HKD Above 50k HKD

55%

29% 26%

48%

33%

46% 54%

33%

10% 23% 17% 14%

3% 2% 4% 5%

Below 25 25 - 35 years

35-45 years

Above 45

Below 5k HKD 5 - 10k HKD 10 - 50k HKD Above 50k HKD

10

© 2015 Sedgwick Richardson

Shopper SatisfactionHow satisfied are Chinese shoppers with the overall shopping experience?

11

© 2015 Sedgwick Richardson

Shopper Satisfaction

The Net Promoter Score (NPS)

Number of ‘Promoters’ —————————

Sample Size( )-

Number of ‘Detractors’ —————————

Sample Size( )= NPS

How likely is it that you will recommend mall x to a friend? ( x = the mall they were polled at)

‘Very likely’ ‘Very unlikely’

12345678910

Promoters Passives Detractors

12

© 2015 Sedgwick Richardson

Shopper Satisfaction

Limitations of the NPS

One factor that needs to be considered is that Asian research participants tend to stay away from ‘extremes’, which will skew the NPS score negatively (compare Lee, 2015: goo.gl/v2QkRx). For this reason it will be difficult for the malls assessed to achieve strong, positive NPS’.

What is more interesting is how the different malls score in relation to each other.

© 2015 Sedgwick Richardson

Harbour City and Times Square with strongest score

13Shopper Satisfaction

-69

-66

-40

-39

-30

-100 -50 0 50 100

IFC

Hysan Place

Festival Walk

Times Square

Harbour City

The fact that all malls score a negative NPS may indicate that low

recommendation rates are not a mall specific problem, but that the

overall experience of coming to Hong Kong is not as positive.

© 2015 Sedgwick Richardson

14

Wallet share capturedQ: “How much money do you plan to spend during your stay in Hong Kong and how much of that at this specific mall?”

Shopper Satisfaction

0%

20%

40%

60%

80%

100%

Festival Walk

Harbour City

Times Square

IFC Hysan Place

Share of Total Planned Spend Captured

© 2015 Sedgwick Richardson

Festival Walk captures 81% of visitors’ total budget

15

49%55%62%76%81%

Share captured Share not captured

Share of total wallet captured

Shopper Satisfaction

© 2015 Sedgwick Richardson

16

Shopper Satisfaction vs Wallet Share Captured Is there a link between shopper satisfaction (= NPS) and the wallet share captured by a mall?

Shopper Satisfaction

17

© 2015 Sedgwick Richardson

Shopper satisfaction is crucial to maximising wallet share

This research indicates that there is an 82% correlation between shoppers’ satisfaction (NPS) and the wallet share captured by a mall.

Times Square

Harbour City

Festival Walk

IFC

Hysan Place

Shopper Satisfaction

NPS

Wallet Share Captured

-80 -70 -60 -50 -40 -30 -20

90%

80%

70%

60%

50%

40%

18

© 2015 Sedgwick Richardson

Shopper Satisfaction

Driving shopper satisfaction is key to their wallet

The implication for Hong Kong mall operators is clear: Assessing NPS on a regular basis provides important insights into how much further organic sales growth can be achieved by maximising the wallet share captured.

19

© 2015 Sedgwick Richardson

Shopper Interests What do Chinese tourists want to buy?

20

© 2015 Sedgwick Richardson

Shopper Interests

What they want to buy: Everything (almost)

8%

16%

33%

34%

35%

35%

0% 10% 20% 30% 40%

Baby & Infant

Luxury

Products for daily use

Electronics

Clothing

Cosmetics

Hong Kong may be a great place to get a little bit of everything,

but it lacks the brand appeal that other Asian countries are developing: between January

and July 2015 Korean cosmetics imports into China rose by 251% (Korea International

Trade Association).

Luxury goods

11% 19% 15% 19% 18%

45% 26%

20%

48%

31%

47%

32%

35%

29%

20%

30%

33% 45%

21%

46%

21%

41% 41% 28%

45%

Festival Walk Harbour City Hysan Place IFC Times Square Luxury Electronics

Products for daily use Clothing

Cosmetics

21

© 2015 Sedgwick Richardson

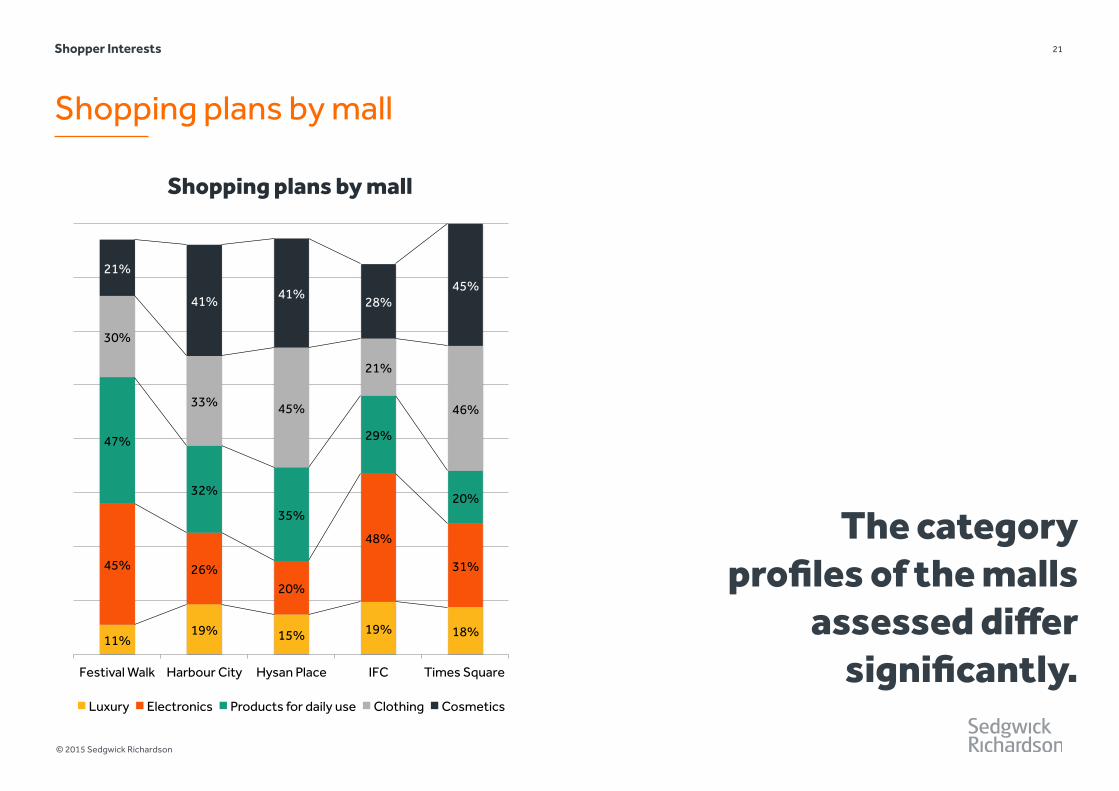

Shopper Interests

Shopping plans by mall

Shopping plans by mall

11% 19% 15% 19% 18%

45% 26% 20%

48%

31%

47%

32%

35%

29%

20%

30%

33% 45%

21%

46%

21%

41% 41% 28%

45%

Festival Walk Harbour City Hysan Place IFC Times Square

Luxury Electronics Products for daily use Clothing Cosmetics

The category profiles of the malls

assessed differ significantly.

67%

27%

4%

1%

51%

35%

10%

3%

Shopping

Food

Sightseeing

Theme Parks

22

© 2015 Sedgwick Richardson

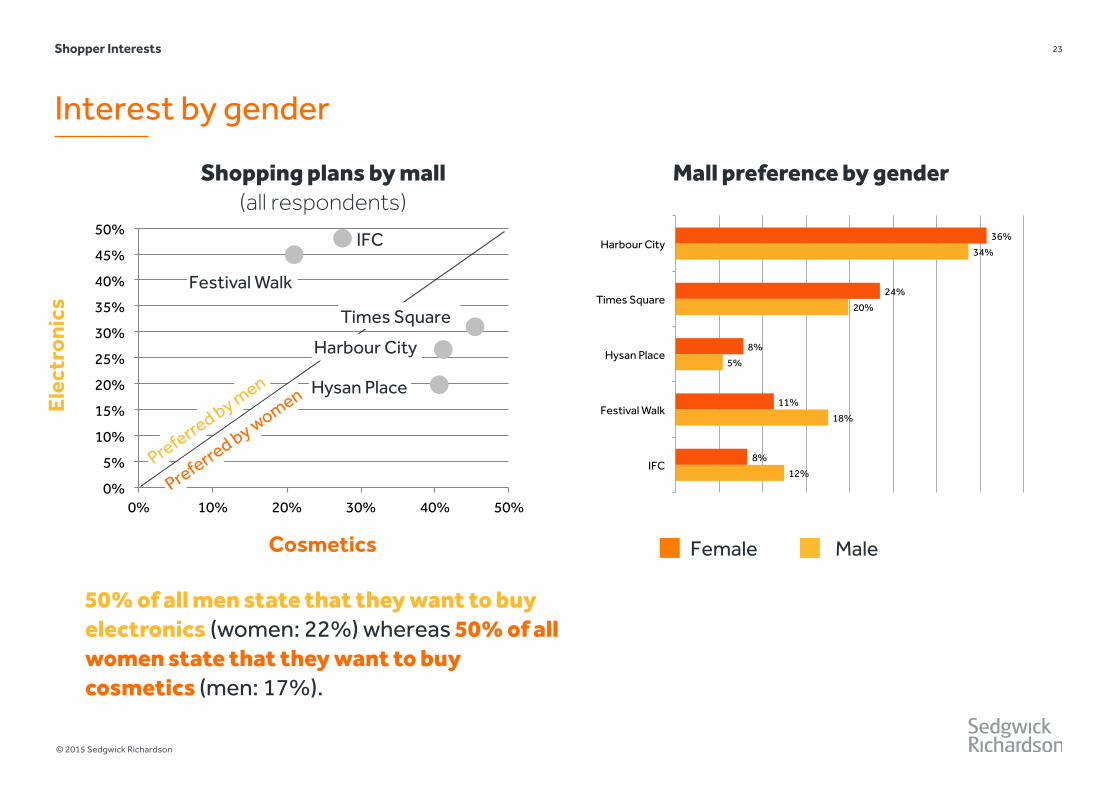

Shopper Interests

Interest by gender

Female Male

-40NPS

-57Interests

23

© 2015 Sedgwick Richardson

Shopper Interests

Interest by gender

50% of all men state that they want to buy electronics (women: 22%) whereas 50% of all women state that they want to buy cosmetics (men: 17%).

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0% 10% 20% 30% 40% 50%

Elec

tron

ics

Cosmetics

Shopping plans by mall (all respondents)

Festival Walk

Hysan Place

IFC

Preferred by women

Preferred by men

Times Square

Harbour City

Elec

tron

ics

Cosmetics

Mall preference by gender

Female Male

36%

24%

8%

11%

8%

34%

20%

5%

18%

12%

Harbour City

Times Square

Hysan Place

Festival Walk

IFC

24

© 2015 Sedgwick Richardson

Shopper Interests

Targeting female shoppers: Lifestyle is key

of female Chinese consumers agreed that doing regular exercise is the most important factor for a healthy lifestyle (up from 47% in 2014).

Sources: Nike (2014), Mintel (2015)

61%

Female Chinese shoppers in Hong Kong still focus on traditional “female” goods

(i.e. cosmetics). In China, brands are targeting female shoppers with

lifestyle focused strategies.

25

© 2015 Sedgwick Richardson

Chinese Millennials Chinese Millennials in Hong Kong: How satisfied they are and what they shop for

26

© 2015 Sedgwick Richardson

Chinese Millennials

Sample share

37% 35%

17% 12%

0%

10%

20%

30%

40%

Below 25 25 - 35 years 35 - 45 years Above 45

MILLENNIALS

27

© 2015 Sedgwick Richardson

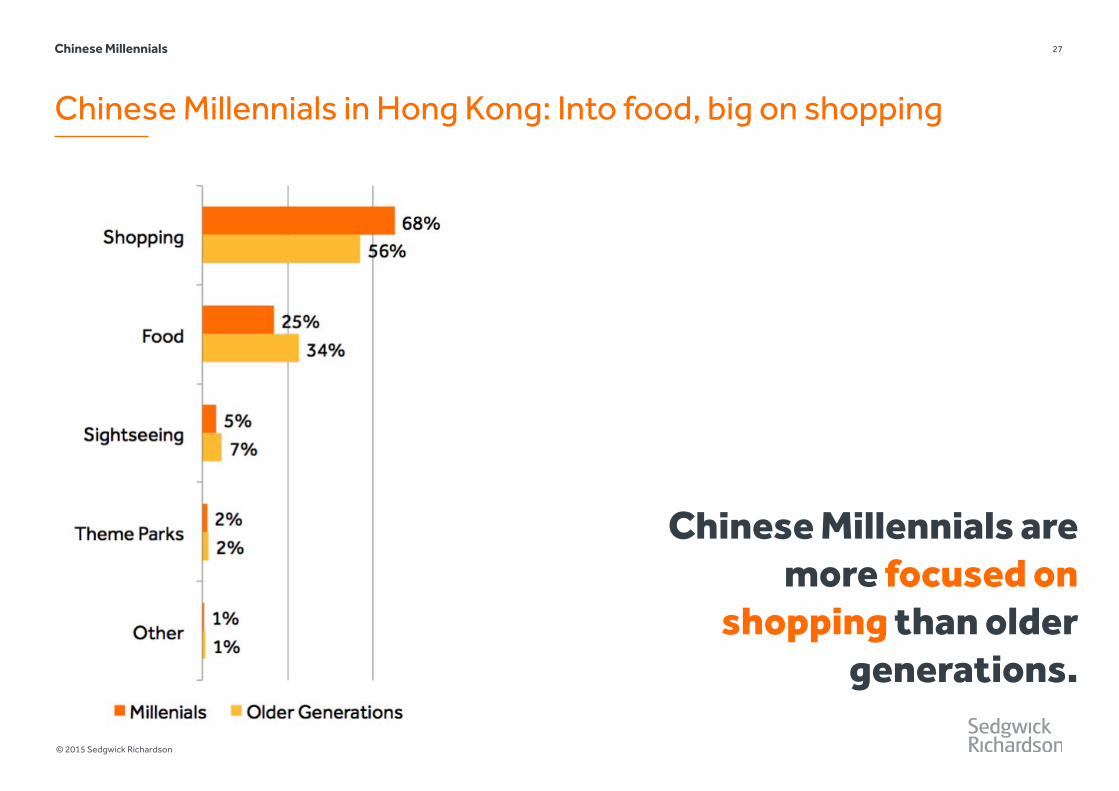

Chinese Millennials in Hong Kong: Into food, big on shopping

Chinese Millennials

Chinese Millennials are more focused on

shopping than older generations.

© 2015 Sedgwick Richardson

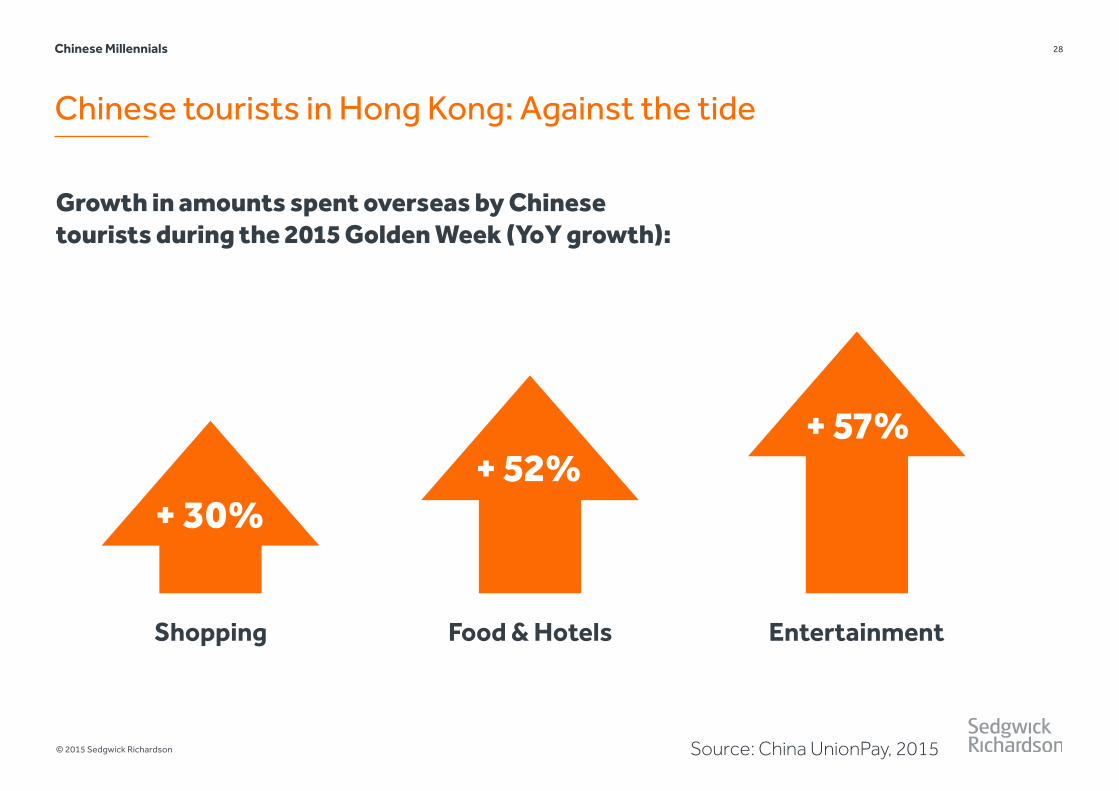

Chinese tourists in Hong Kong: Against the tide

28Chinese Millennials

Growth in amounts spent overseas by Chinese tourists during the 2015 Golden Week (YoY growth):

+ 52%

Food & Hotels

+ 57%

EntertainmentShopping

+ 30%

Source: China UnionPay, 2015

6%

10%

13%

15%

22%

34%

8%

10%

12%

13%

22%

36%

0% 10% 20% 30% 40%

Hysan Place

IFC

Other

Festival Walk

Time Square

Harbour City

Millennials Older Generations

29

© 2015 Sedgwick Richardson

Top mall: Harbour City; Hysan Place more popular with Millennials

Chinese Millennials

We asked all research respondents which malls

they would definitely visit while in Hong Kong if they

only stayed for one day.

12%

17%

36%

32%

32%

30%

2%

16%

31%

33%

40%

43%

0% 10% 20% 30% 40% 50%

Baby & Infant products

Luxury brands

Electronics

Products for daily use

Clothing

Cosmetics

Millennials Older Generations

30

© 2015 Sedgwick Richardson

Millennials: Cosmetics and clothing

Chinese Millennials

Chinese Millennials are more interested in

lifestyle related brands.

31

© 2015 Sedgwick Richardson

-45

Experiences that don’t impress

Millennials NPS-56

Older Generations NPS

Chinese Millennials

Looking at these numbers one needs to factor in that younger

Chinese consumers tend to be more critical than older

generations (Tencent, 2015).

72%

24%

4%

Yes

Unsure

No

32

© 2015 Sedgwick Richardson

Millennials plan to return to Hong Kong

Millennials

66%

22%

11%

Yes

Unsure

No

Older Generations

Chinese Millennials

38%

44%

34% 36% 38% 40% 42% 44% 46%

Millennials Older Generations

33

© 2015 Sedgwick Richardson

Millennials: They know what they want

Chinese Millennials

Share of tourists that has a specific shopping list

Chinese Millennials know what they want to buy —

which is why Hong Kong brands need to reach them

before they arrive in the city.

© 2015 Sedgwick Richardson

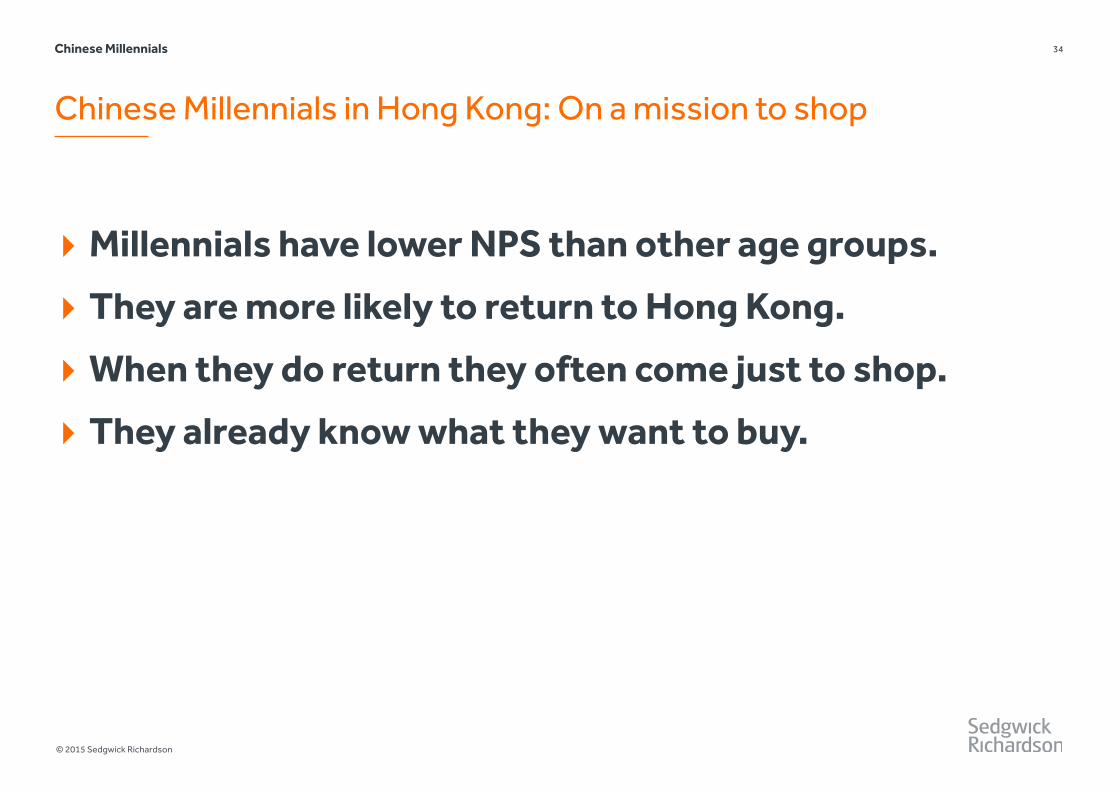

Chinese Millennials in Hong Kong: On a mission to shop

34Chinese Millennials

‣ Millennials have lower NPS than other age groups.

‣ They are more likely to return to Hong Kong.

‣ When they do return they often come just to shop.

‣ They already know what they want to buy.

© 2015 Sedgwick Richardson

A wakeup call for Hong Kong

35

This research indicates that Hong Kong needs to work harder to satisfy Chinese millennials (and Chinese visitors overall).

Even though millennials state that they do plan to return to the city to execute their well planned shopping trips, given that

their overall NPS is low there is the risk that this may change in the future.

Chinese Millennials

© 2015 Sedgwick Richardson

Top destinations vs Spend

36Chinese Millennials

Sources: Ctrip, Fung Business Intelligence Centre, China Luxury Advisors(2015)

Japan

South Korea

Thailand

Hong KongTaiw

anUSA

Singapore

Indonesia

MaldivesItaly

$x,xxx = Average spend of Chinese tourists on retail purchases (USD); Jan - May 2015

$2,270

$1,696

$1,290

$1,256

$1,922

Top 10 Golden Week travel destinations

According to Ctrip.com, Hong

Kong has lost some of its appeal.

37

© 2015 Sedgwick Richardson

Recommendations To stay relevant Hong Kong malls need to embrace not only changing Chinese consumer tastes, but also develop a more effective communications approach.

© 2015 Sedgwick Richardson

38Recommendations

CHINA GLOBAL

Awareness Conversion Loyalty

Search 33% 56%

Brand’s Website

32% 19%

Social Media 12% 4%

Physical Store

11% 13%

Brand’s app

4% 2%

Consideration

Attractive Deals

41% 45%

Learning about new product offerings

40% 33%

Interacting with the brand or its online followers

20% 11%

Want to see & touch the product (off.)

83% 71%

More convenient to have item delivered (on.)

63% 45%

Better prices online (on.) 91% 85%

Comment on a product experience

41% 23%

Follow a favourite brand or retailer

44% 34%

Channels used as a first step to research a brand

Reasons for visiting a particular brand's social

media page

Percentage of consumers who use social media to …

Factors affecting consumers’ decisions to buy

online/ offline

The new marketing funnel

Source: PwC, 2015

© 2015 Sedgwick Richardson

WeChat: Not an optional channel

39

For Chinese consumers WeChat is the most critical social media channel. With more than 400m monthly active users it dominates all other social platforms.

Recommendations

Of the five malls assessed in this research only Harbour City, IFC and Festival Walk had WeChat channels.

However, IFC posted few relevant contents, and during the period reviewed, Festival Walk had not posted anything.

© 2015 Sedgwick Richardson

WeChat: Key to brands and mall operators in China

40

In China virtually every consumer brand and many mall operators use WeChat as an integral part of their marketing communications.

Recommendations

The screenshots to the left show two WeChat campaigns (lucky draw & follower acquisition campaign) run by New World Development in Shenzhen.

© 2015 Sedgwick Richardson

The importance of an O2O strategy

41

In Hong Kong, where space is limited and malls and shops are often busy during peak hours, developing O2O solutions that enhance the customer experience is absolutely vital.

Recommendations

JD.com: a major Chinese e-commerce website operates self-collect stations in subway lines in Beijing, Shanghai and Guangzhou.

42

© 2015 Sedgwick Richardson

Key Opportunities:

• Measuring mall efficiency via the NPS • Creating more diverse experiences that match

the interests of female shoppers and millennials • Developing WeChat capabilities and O2O

strategies

© 2015 Sedgwick Richardson

43

Do wallets differ by age?

Total Wallet

Follow us on LinkedIn: www.linkedin.com/company/sedgwick-richardsonVisit www.sedgwick-richardson.com to get more information

Chinese Tourists in Hong Kong

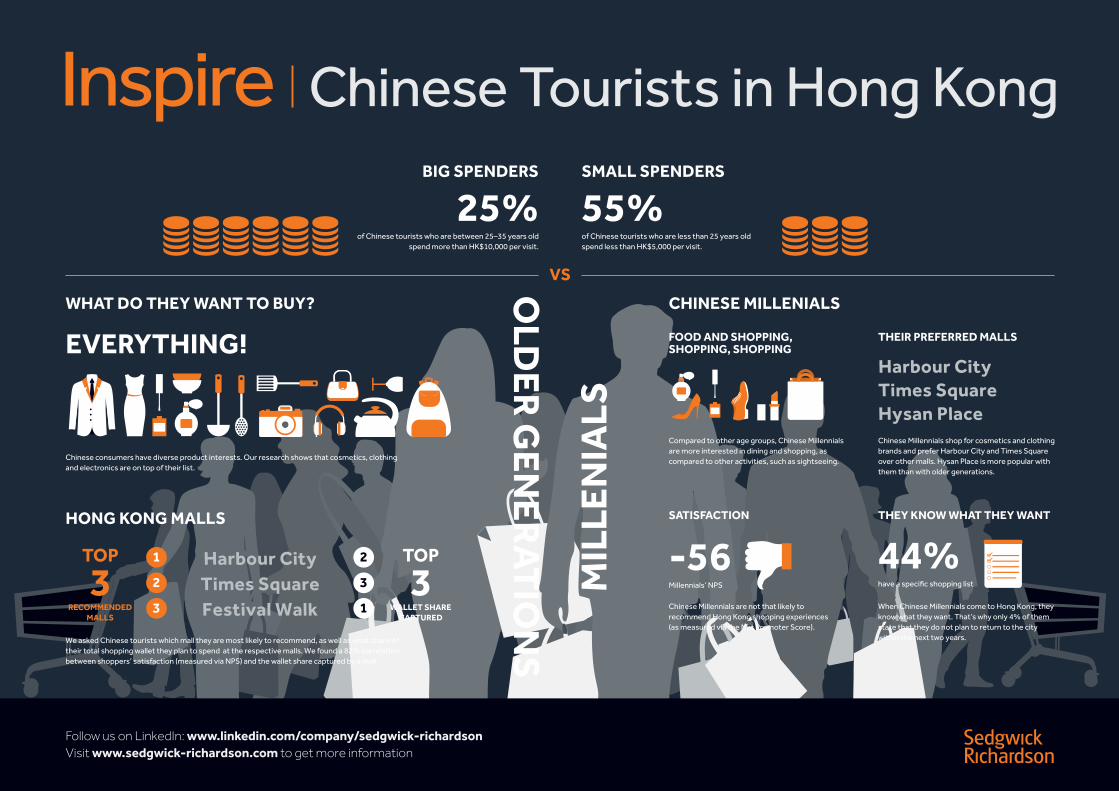

FOOD AND SHOPPING, SHOPPING, SHOPPING

Compared to other age groups, Chinese Millennials are more interested in dining and shopping, as compared to other activities, such as sightseeing.

THEIR PREFERRED MALLS

Chinese Millennials shop for cosmetics and clothing brands and prefer Harbour City and Times Square over other malls. Hysan Place is more popular with them than with older generations.

Harbour CityTimes SquareHysan Place

CHINESE MILLENIALS

THEY KNOW WHAT THEY WANT

44%have a specific shopping list

When Chinese Millennials come to Hong Kong, they know what they want. That’s why only 4% of them state that they do not plan to return to the city within the next two years.

SATISFACTION

Chinese Millennials are not that likely to recommend Hong Kong shopping experiences (as measured via the Net Promoter Score).

-56Millennials’ NPS

EVERYTHING!

Chinese consumers have diverse product interests. Our research shows that cosmetics, clothing and electronics are on top of their list.

WHAT DO THEY WANT TO BUY?

MIL

LEN

IALS

OLD

ER

GE

NE

RA

TIO

NS

VS

We asked Chinese tourists which mall they are most likely to recommend, as well as what share of their total shopping wallet they plan to spend at the respective malls. We found a 82% correlation between shoppers’ satisfaction (measured via NPS) and the wallet share captured by a mall.

Harbour CityTimes SquareFestival Walk3

2

1

31

3

2

HONG KONG MALLS

TOP

RECOMMENDEDMALLS

3TOP

WALLET SHARECAPTURED

55%of Chinese tourists who are less than 25 years old spend less than HK$5,000 per visit.

SMALL SPENDERS

25%of Chinese tourists who are between 25–35 years old

spend more than HK$10,000 per visit.

BIG SPENDERS

Sedgwick Richardson (Hong Kong)

10/F, 1 Hollywood RoadCentralHong Kong

By Hendrik Kühl Branding Director

T +852 [email protected]

1 3

Thank you.

© 2015 Sedgwick Richardson

44