innovative tools for funding - wirc-icai.org innovative tools for funding...companies •sme stock...

TRANSCRIPT

Innovating Cost Effective Tools for Funding

Trade Finance

Private Equity

CGTMSE

SME

Exchange

Subsidy schemes

ECB

Financial Solutions through the

Business Life Cycle

Unsecured Business Loans

Financing

Receivables

Banking Transactions

CP/NCD

Commercial

Papers

IPO/FPO

Mortgage Loans

Commodity Finance

MSME

MSME sector

32 Million MSMEs - 95% of industrial units

Manufacturing 8000+ products

Employment to 73 million

people

40% Manufacturing

output

45% of total Indian Exports

8.7% of Indian GDP

MSME Overview

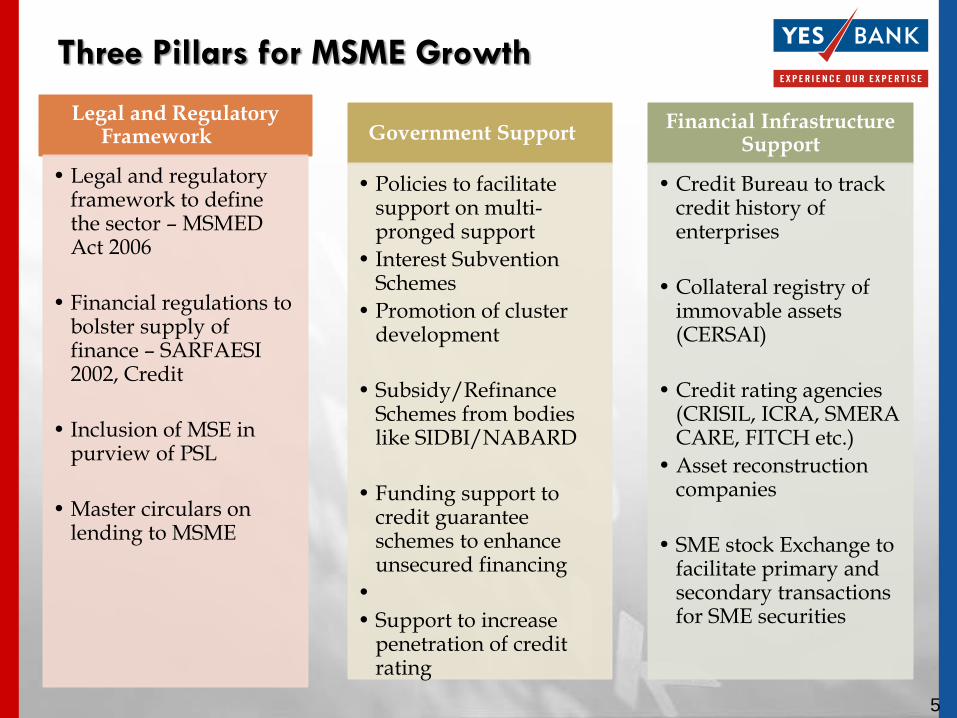

Three Pillars for MSME Growth

Legal and Regulatory Framework

• Legal and regulatory framework to define the sector – MSMED Act 2006

• Financial regulations to bolster supply of finance – SARFAESI 2002, Credit

• Inclusion of MSE in purview of PSL

• Master circulars on lending to MSME

Government Support

• Policies to facilitate support on multi-pronged support

• Interest Subvention Schemes

• Promotion of cluster development

• Subsidy/Refinance Schemes from bodies like SIDBI/NABARD

• Funding support to credit guarantee schemes to enhance unsecured financing

•

• Support to increase penetration of credit rating

Financial Infrastructure Support

• Credit Bureau to track credit history of enterprises

• Collateral registry of immovable assets (CERSAI)

• Credit rating agencies (CRISIL, ICRA, SMERA CARE, FITCH etc.)

• Asset reconstruction companies

• SME stock Exchange to facilitate primary and secondary transactions for SME securities

5

Govt. Schemes for Small & Medium Enterprises

1. Scheme of Fund for Regeneration of Traditional Industries (SFURTI)

2. Marketing Assistance Scheme

3. Subsidy and Credit Rating Scheme

4. Scheme of Interest Subsidy Eligibility Certification (ISEC)

5. Scheme for Enhancing Productivity and Competitiveness of Khadi

Industry and Artisans

6. National Manufacturing Competitiveness Program

7. Credit Linked Capital subsidy Scheme (CLCSS) for Technology Up-

gradation of the Small Scale Industries

8. Credit Guarantee Fund Scheme for Micro and Small Enterprise (CGTMSE)

9. Assistance for Strengthening of Training Infrastructure of existing and

new Entrepreneurship Development Institutions

10.Scheme for Micro Finance Program

The Government is working proactively to find innovative solutions to the

problems being faced by MSME Sector of India. The number of Financial

Assistance Schemes have been formulated to enable the Indian MSMEs to be

the major player in the International Markets. Few of the Schemes are as below:

6

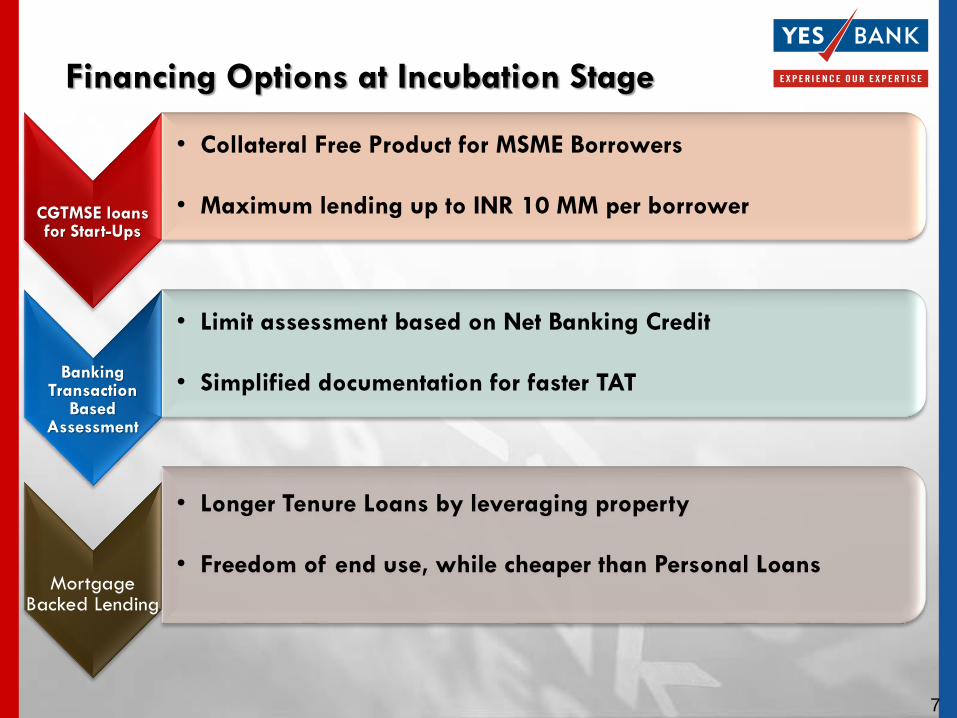

Financing Options at Incubation Stage

CGTMSE loans for Start-Ups

• Collateral Free Product for MSME Borrowers

• Maximum lending up to INR 10 MM per borrower

Banking Transaction

Based Assessment

• Limit assessment based on Net Banking Credit

• Simplified documentation for faster TAT

Mortgage Backed Lending

• Longer Tenure Loans by leveraging property

• Freedom of end use, while cheaper than Personal Loans

7

Short term, self-liquidating finance against pledge of commodity

Borrower to stock commodity at the desired warehouse and

pledge the warehouse receipt to the lender

Provides liquidity management and risk mitigation

Value of the loan = Value of commodity - commodity specific margin

amount

Loans to farmers up to 50 lacs for a period not exceeding 12 months

is classified under Direct Agri fincnce

Commodity Finance

8

Kisan

Credit

Card

Lending to Individual Farmers

Loans for “Seasonal Agricultural operations”

Short Term and Long Term funding

Credit call based on group financial comfort

Applicable for Agricultural land owned or leased by

the borrowers

Promoter Agri Funding

9

Emerging/Growth Enterprises

10

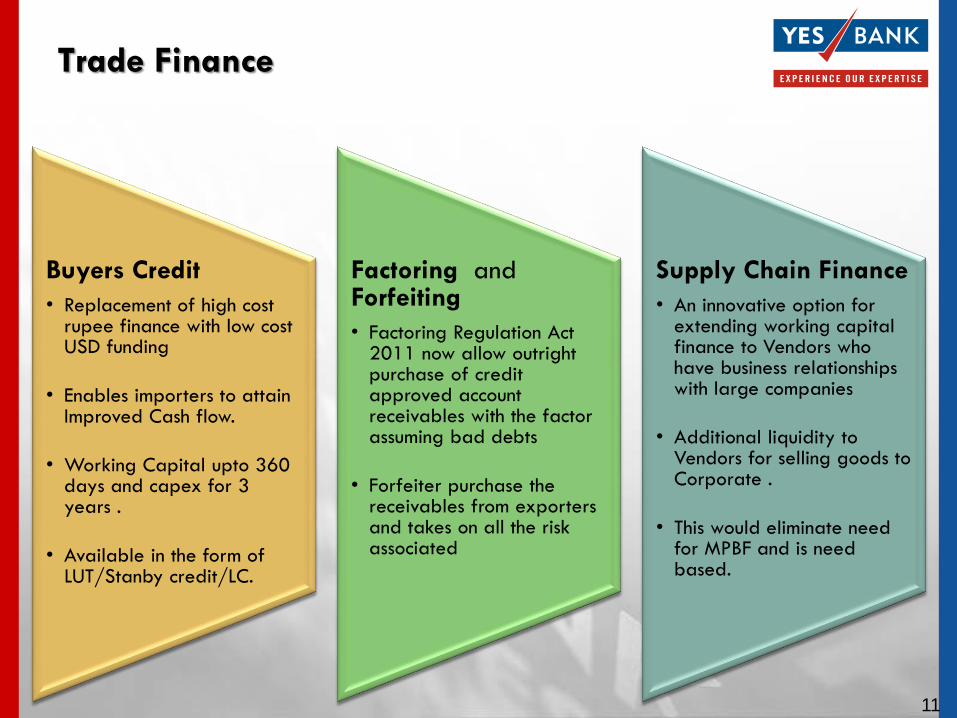

Buyers Credit

• Replacement of high cost rupee finance with low cost USD funding

• Enables importers to attain Improved Cash flow.

• Working Capital upto 360 days and capex for 3 years .

• Available in the form of LUT/Stanby credit/LC.

Factoring and Forfeiting

• Factoring Regulation Act 2011 now allow outright purchase of credit approved account receivables with the factor assuming bad debts

• Forfeiter purchase the receivables from exporters and takes on all the risk associated

Supply Chain Finance

• An innovative option for extending working capital finance to Vendors who have business relationships with large companies

• Additional liquidity to Vendors for selling goods to Corporate .

• This would eliminate need for MPBF and is need based.

Trade Finance

11

Right product if any of these questions is a YES

Receivables Financing

Do you deal with credit

worthy buyers

Are you facing a working capital

shortage

Selling to many buyers

on open account credit

terms?

Is tied up capital in a/c receivables

limiting your growth

Financing Receivables is the solution

Advance funds up to 90% of the invoice value compared to limited funding offer by traditional lending facilities

Higher limits assigned on the basis of

Quality of receivables

Underlying goods and services

Management of the company

Focus on quality of receivables as well as strength of relationship with buyers

12

Eligible Borrowers

•Corporate other than hotel, hospital and software up to USD 750 MM

•Corporate in service sector viz. Hotel, Hospital, software up to USD 200 MM

•Units in SEZ

•NGO engaged in micro finance activities

Permissible End use

• Import of Capital goods

• Implementation of new projects

•Modernization/Expansion of existing production units

•Overseas investment in JV/WOS

•First stage of acquisition in the disinvestment process

Commercial loans availed from non-resident lenders

Source of finance for corporate to expand their existing capacity & for fresh investment

Minimum average maturity of 3 years.

Priority for projects in Infrastructure, power, oil, telecom, railways, roads, & bridges, ports, urban infrastructure, & export sectors

External Commercial Borrowings

13

Equity Capital Not quoted on public exchange and raised primarily from institutional investors

Unlisted companies with high growth potential share risk and return in the company

Various types are Leveraged buyout, Venture capital, Growth capital, Mezzanine capital

Advantages to retain operational and majority control, lower regulatory compliance than Listing, Strategic and

operational support

Private Equity

14

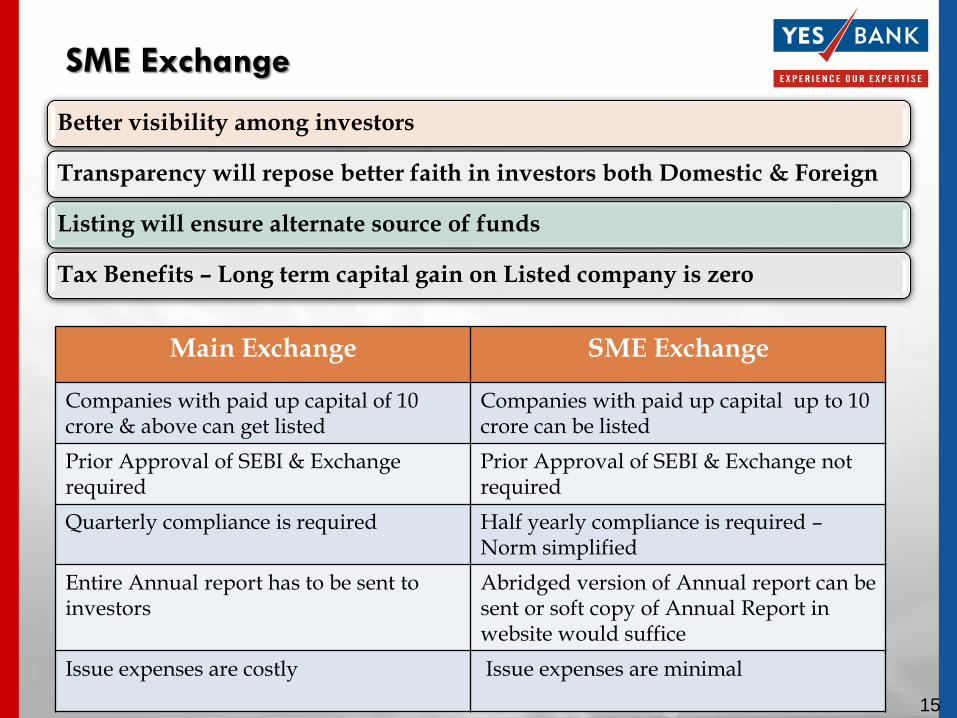

SME Exchange

Main Exchange SME Exchange

Companies with paid up capital of 10 crore & above can get listed

Companies with paid up capital up to 10 crore can be listed

Prior Approval of SEBI & Exchange required

Prior Approval of SEBI & Exchange not required

Quarterly compliance is required Half yearly compliance is required – Norm simplified

Entire Annual report has to be sent to investors

Abridged version of Annual report can be sent or soft copy of Annual Report in website would suffice

Issue expenses are costly Issue expenses are minimal

Better visibility among investors

Transparency will repose better faith in investors both Domestic & Foreign

Listing will ensure alternate source of funds

Tax Benefits – Long term capital gain on Listed company is zero

15

Corporate or Large companies

16

An innovative option for extending working capital finance to Vendors who have business relationships with large corporate.

Vendor Financing meets the funds requirement of the suppliers of the Large corporate through sales bill/invoice discounting facility

Dealer Financing meets the working capital needs by providing additional liquidity to dealers for procuring goods from Corporate

Revolving line of credit in the nature of Overdraft

SUPPLY CHAIN FINANCE

17

Commercial Paper

Unsecured money market instrument issued in the form of promissory note

Enabling highly rated corporate borrowers to diversify their sources of short term borrowings

Guidelines for issue governed by various directives issued by RBI

Wide range of maturity resulting in more flexibility

No lien on assets of the company

CP tradability provides investor with exit options

Helps Financial institutions in asset-liability and risk management

18

Non-Convertible Debentures

Fixed income debt instruments issued by a company to raise long term funds

Manage liquidity & mitigate risk to great extent

Benefits of investing

• Listing on NSE & BSE providing liquidity

• Rated by credit rating agencies to assess the quality of debt papers

• Limited lock –in period from 2 to 20 providing ample options

Tax Implications

• Held till maturity: Interest added to total income & taxed at marginal rate

• Sold on exchange before one year: Short term capital gains tax

• Sold on exchange after one year: Long term capital gains tax at 20% with indexation & 10% without indexation

19

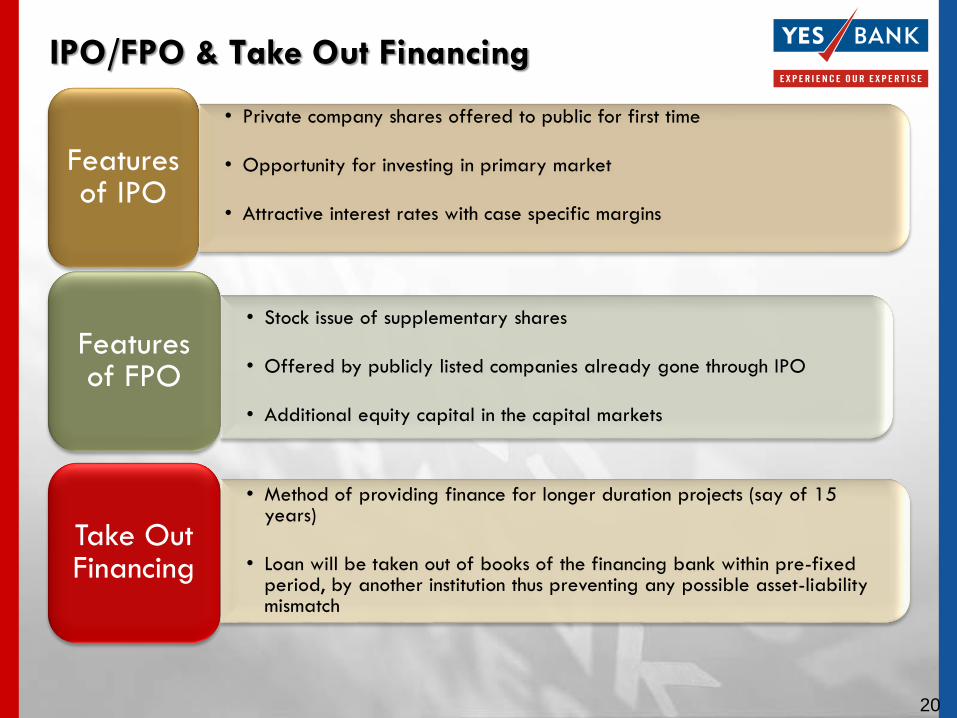

IPO/FPO & Take Out Financing

• Private company shares offered to public for first time

• Opportunity for investing in primary market

• Attractive interest rates with case specific margins

Features of IPO

• Stock issue of supplementary shares

• Offered by publicly listed companies already gone through IPO

• Additional equity capital in the capital markets

Features of FPO

• Method of providing finance for longer duration projects (say of 15 years)

• Loan will be taken out of books of the financing bank within pre-fixed period, by another institution thus preventing any possible asset-liability mismatch

Take Out Financing

20

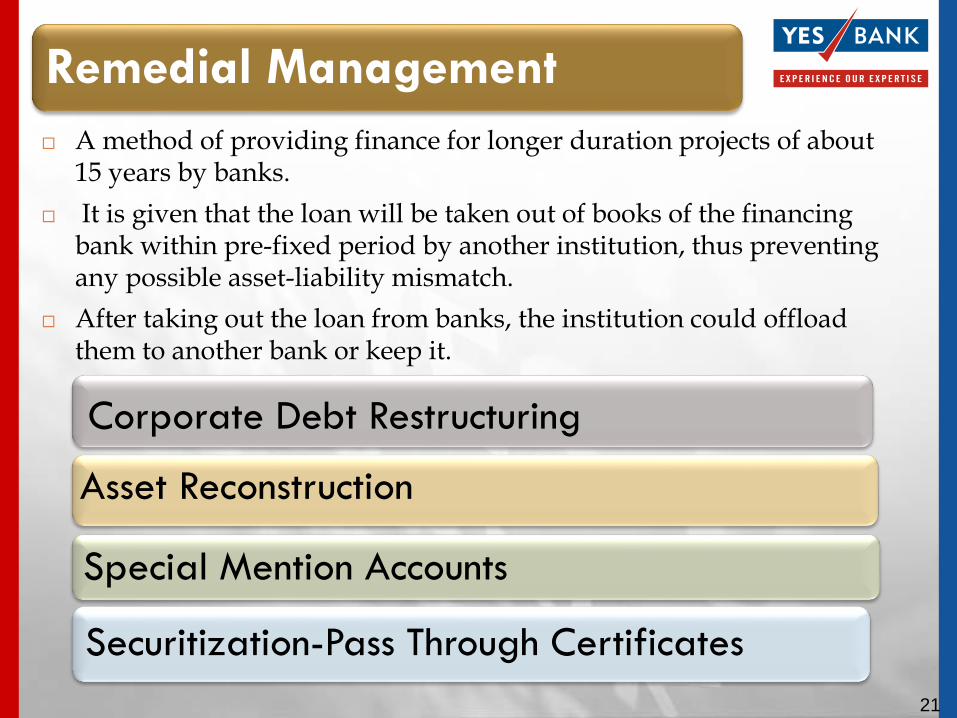

A method of providing finance for longer duration projects of about 15 years by banks.

It is given that the loan will be taken out of books of the financing bank within pre-fixed period by another institution, thus preventing any possible asset-liability mismatch.

After taking out the loan from banks, the institution could offload them to another bank or keep it.

Remedial Management

Corporate Debt Restructuring

Asset Reconstruction

Special Mention Accounts

Securitization-Pass Through Certificates

21

Thank You

22