innovative computing on finance dept. of finance, cyut a novel prediction model for credit card risk...

TRANSCRIPT

Innovative Computing on Finance

Dept. of Finance, CYUT

A Novel Prediction Model for Credit Card Risk Management

Tsung-Nan Chou

Department of Finance, Chaoyang University of Technology168 Jifong E. Rd., Wufong Township, Taichung County, 41349, Taiwan

E-mail: [email protected]

Innovative Computing on Finance

Dept. of Finance, CYUT

Outline

1. Introduction

2. Integrated Model

3. Research Methodologies– Evolutional neural network– Grey incidence analysis– Dempster-Shafer theory

4. Experiment Results

5. Conclusion

Innovative Computing on Finance

Dept. of Finance, CYUT

Introduction

Credit Card Business in Taiwan

• The severe competition of credit card market in Taiwan.

• The amount of issued credit cards has increased rapidly and is sixteen times the size of the past decade issues

• The annual amount of credit has also growth 9.54 times.

Innovative Computing on Finance

Dept. of Finance, CYUT

Introduction

The Truths of Applying Credit Card• Everyone is easy to apply for the credit cards.• One existed card applied for another cards

without verification in promotion campaign.• Platinum card holders are everywhere in Taiwan.• Most financial institutions focus on the prior

process of credit card verification instead of the posterior process of the risk management after cards issued.

Innovative Computing on Finance

Dept. of Finance, CYUT

Introduction

What the Card Issuers Need ?• Credit risk management is critical safeguard

against the possible losses. • A credit risk management alert system will be

able to freeze the credit usage or to reject the on-going transaction and to prevent the potential bad debts over the credit limit.

• Banking industrial need to construct an efficient credit risk prediction system to detect the default of card holders correctly.

Innovative Computing on Finance

Dept. of Finance, CYUT

IntroductionResearch Work in Credit Assessment• Some researches applied trandional statistic regression

models such as Orgler(1970) Steenackers & Goovaerts (1989)

• Many method in statistics ,such as regression analysis ,variance analysis and principal component require a large amount of samples and satisfy certain probability distribution.

• Recent studies use Artificial Intelligence (AI) methods for credit assessment. Neural network is the more recently in support of both business and financial applications.

• Many applications of AI can be found in (Brause, Langsdorf, and Hepp, 1999), (Aleskerov, Freisleben and Rao, 1997), (West, 2000) (Donato et. al., 1999)

Innovative Computing on Finance

Dept. of Finance, CYUT

Objective of the system

1. The aim of this study is to construct an efficient risk prediction system to detect the default of credit card holders correctly.

2. The system collects the personal and financial information of credit card holders and then applies evolutional neural network which integrated with grey incidence analysis and Dempster-Shafer theory of evidence to predict the default cases and trace the behaviors of the card holders and manage the default risks.

Innovative Computing on Finance

Dept. of Finance, CYUT

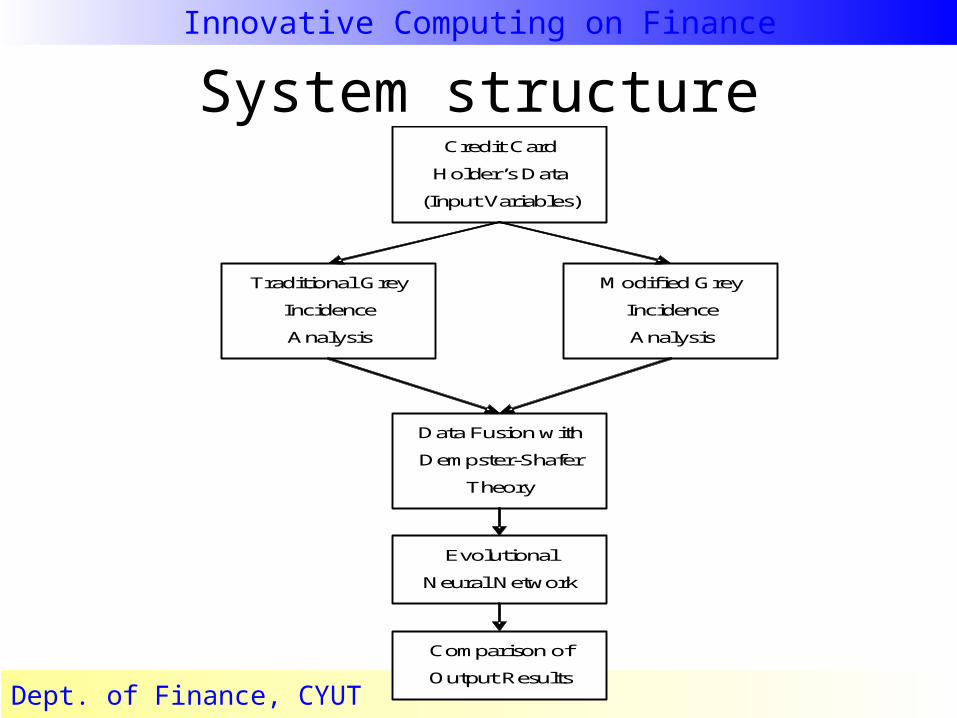

System structure Credit Card

Holder’s Data

(Input Variables)

Data Fusion with

Dempster-Shafer

Theory

Evolutional

Neural Network

Comparison of

Output Results

Traditional Grey

Incidence

Analysis

Modified Grey

Incidence

Analysis

Innovative Computing on Finance

Dept. of Finance, CYUT

Research Methodologies

1. Evolutional neural network2. Grey incidence analysis

– Ju-Long Deng, 1998, Essential Topics on Grey System, Theory and Application, China Ocean Press.

– Kun-Li Wen, 2004, Grey System Modeling and Prediction, Yang’s Scientific Research Institute, USA.

3. Dempster-Shafer theory– G.. Shafer, “A Mathematical Theory of Evidence”, Princeton, NJ,

Princeton, University Press, 1976.– G.. Shafer, “Probability Judgement in Artificial Intelligence”,

Uncertainty in Artificial Intelligence. L. N. Kanal and J. F. Lemmer. New York, Elsevier Science, 1986.

Innovative Computing on Finance

Dept. of Finance, CYUT

Evolutional neural network

Limitation of Neural Network Training• The back-propagation learning algorithm cannot

guarantee an optimal solution as it might converge to a local optimal weights. As a result, the neural network is often unable to find a desirable solution to a problem.

• The other difficulty is to selecting an optimal topology for the neural network. The network architecture for a particular problem is often chosen by means of heuristics.

Innovative Computing on Finance

Dept. of Finance, CYUT

Evolutional neural network

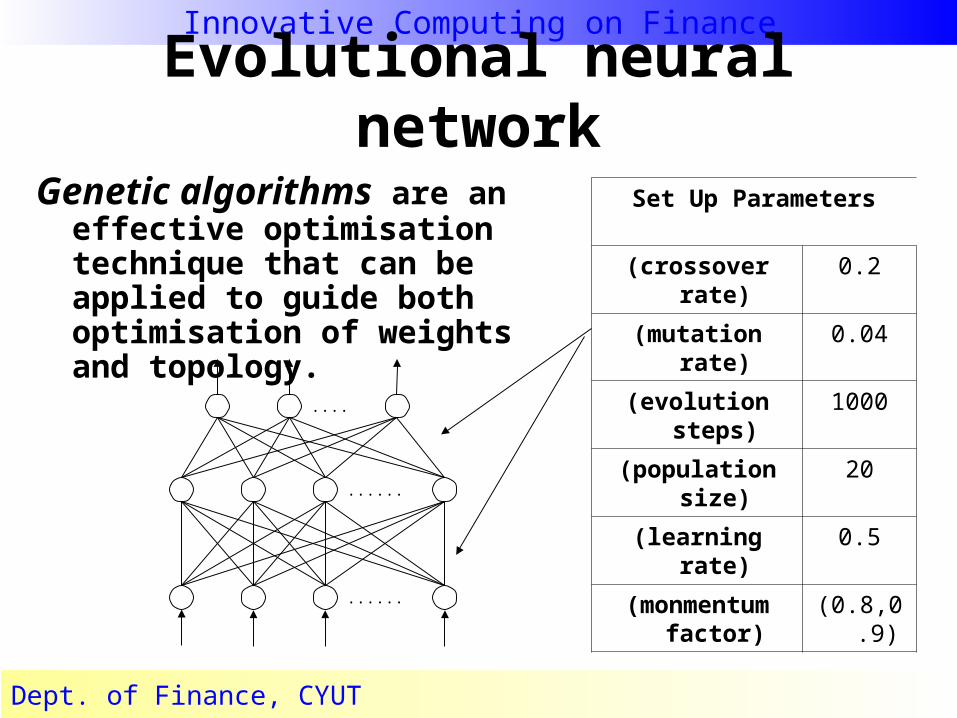

Genetic algorithms are an effective optimisation technique that can be applied to guide both optimisation of weights and topology.

‧‧‧‧

‧‧‧‧‧‧

‧‧‧‧‧‧

Set Up Parameters

(crossover rate) 0.2

(mutation rate) 0.04

(evolution steps) 1000

(population size) 20

(learning rate) 0.5

(monmentum factor)

(0.8,0.9)

Innovative Computing on Finance

Dept. of Finance, CYUTBy courtesy of Negnevitsky, Pearson Education, 2002

Innovative Computing on Finance

Dept. of Finance, CYUT

Evolutional neural network

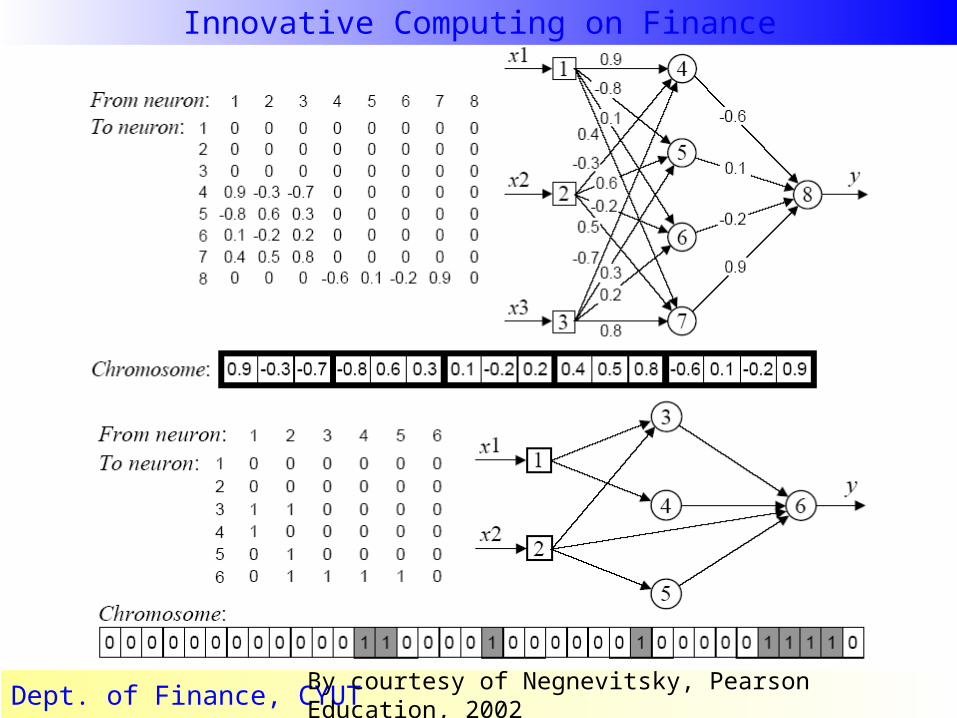

Execution Step:• Step 1: Randomly generate an initial population of

chromosomes which represents the topology of the neural networks.

• Step 2: Calculate the fitness of each individual chromosome.

• Step 3: Create a pair of offspring chromosomes by applying the genetic operations such as reproduction, crossover and mutation operations.

• Step 4: Replace the initial chromosome population with the new population.

• Step 5: Go to Step 2, and repeat the process until the termination criterion is satisfied.

Innovative Computing on Finance

Dept. of Finance, CYUT

Grey incidence analysis

1. The fundamental idea of the grey incidence analysis is that the closeness of a relation is judged based on the similarity level of the geometrical patterns of sequence curves. The more similar the curves are ,the higher degree of incidence between sequence.

• Generation technique of grey Sequences: to realize the data pretreatment with analysis of object system and applying operators of sequences.

• Grey incidence analysis techniques: to find out relationship of sequences based on the geometry comparability of these sequences.

Innovative Computing on Finance

Dept. of Finance, CYUT

Grey incidence analysis

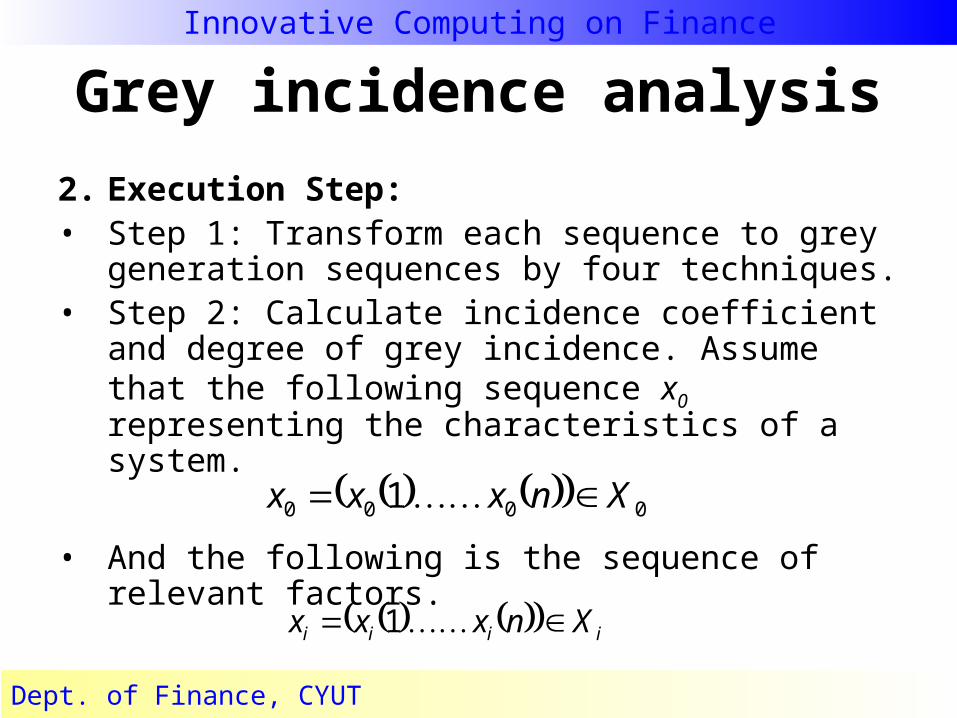

2. Execution Step:• Step 1: Transform each sequence to grey

generation sequences by four techniques.• Step 2: Calculate incidence coefficient and

degree of grey incidence. Assume that the following sequence x0 representing the characteristics of a system.

• And the following is the sequence of relevant factors.

0000 1 Xnxxx

iiii Xnxxx 1

Innovative Computing on Finance

Dept. of Finance, CYUT

Grey incidence analysis

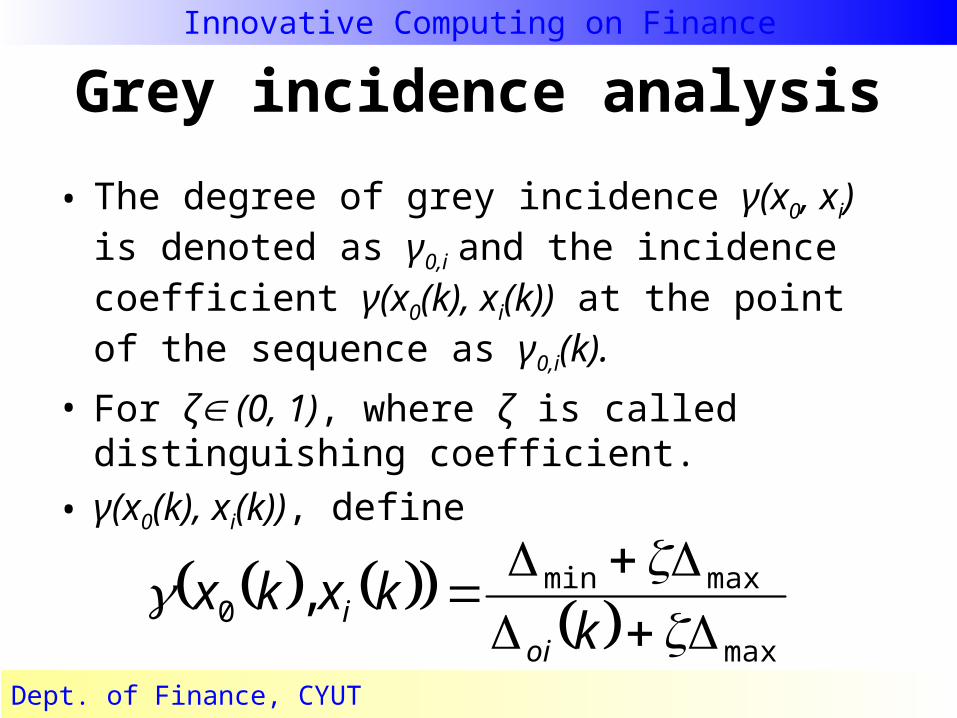

• The degree of grey incidence γ(x0, xi) is denoted as γ0,i and the incidence coefficient γ(x0(k), xi(k)) at the point of the sequence as γ0,i(k).

• For ζ (0, 1), where ζ is called distinguishing coefficient.

• γ(x0(k), xi(k)), define

max

maxmin0 ,

k

kxkxoi

i

Innovative Computing on Finance

Dept. of Finance, CYUT

Grey incidence analysis

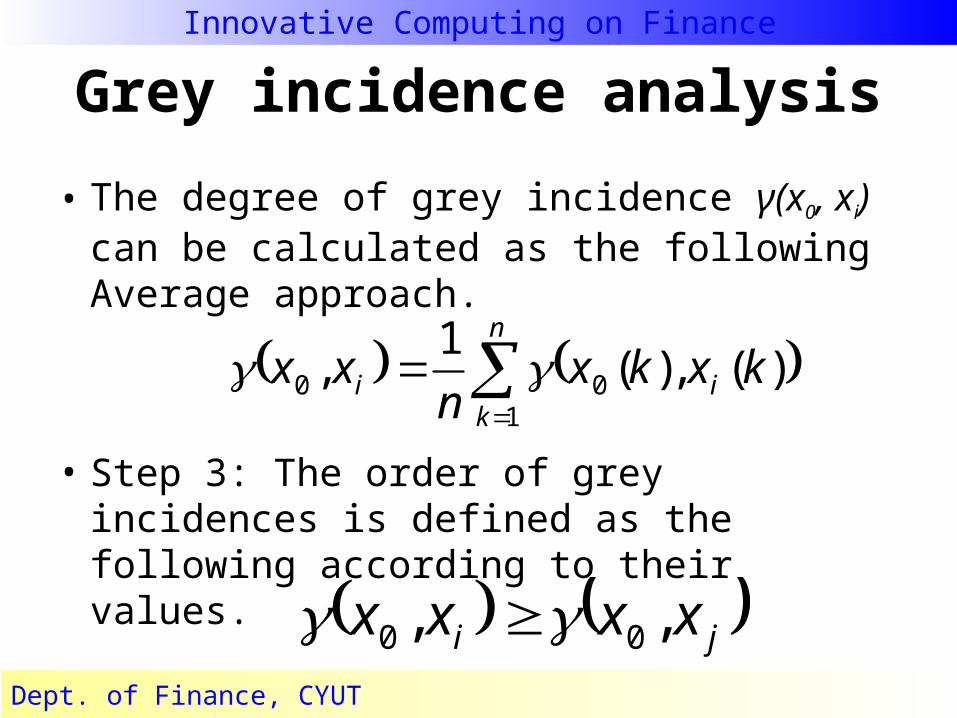

• The degree of grey incidence γ(x0, xi) can be calculated as the following Average approach.

• Step 3: The order of grey incidences is defined as the following according to their values.

n

kii kxkx

nxx

100 )(),(

1,

ji xxxx ,, 00

Innovative Computing on Finance

Dept. of Finance, CYUT

Dempster-Shafer theory

• The Dempster-Shafer decision theory is considered a generalized Bayesian theory which is traditional method to deal with statistical problems.

• The Dempster-Shafer theory is a mathematical theory of evidence based on belief functions and plausible reasoning, which is used to combine separate pieces of information (evidence) to calculate the probability of an event.

• The Dempster-Shafer (D-S) theory of evidence was created by Glen Shafer [Shafer, 1976] at Princeton. He built on earlier work performed by Arthur P. Dempster. The theory is a broad treatment of probabilities, and includes classical probability and certainty factors as subsets.

Innovative Computing on Finance

Dept. of Finance, CYUT

Dempster-Shafer theory

Consider the nature of evidence. • Some evidence is not reliable (the weatherman is

wrong sometimes and right sometimes). • Some evidence is uncertain (an intermittent

atmospheric reading). • Some is incomplete (the wind speed by itself does not

tell us much). • Some evidence is contradictory (the weatherman's

forecast and the atmospheric conditions). • Some evidence is incorrect (a broken atmospheric

data source or a wrong weather forecast).

Innovative Computing on Finance

Dept. of Finance, CYUT

Dempster-Shafer theory• In the D-S theory of evidence, the set of all

hypotheses that describes a situation is the frame of discernment. The hypotheses should be mutually exclusive and exhaustive, meaning that they must cover all the possibilities and that the individual hypotheses cannot overlap.

• The D-S theory mirrors human reasoning by narrowing its reasoning gradually as more evidence becomes available. Two properties of the D-S theory permit this process: – the ability to assign belief to ignorance– the ability to assign belief to subsets of hypotheses.

Innovative Computing on Finance

Dept. of Finance, CYUT

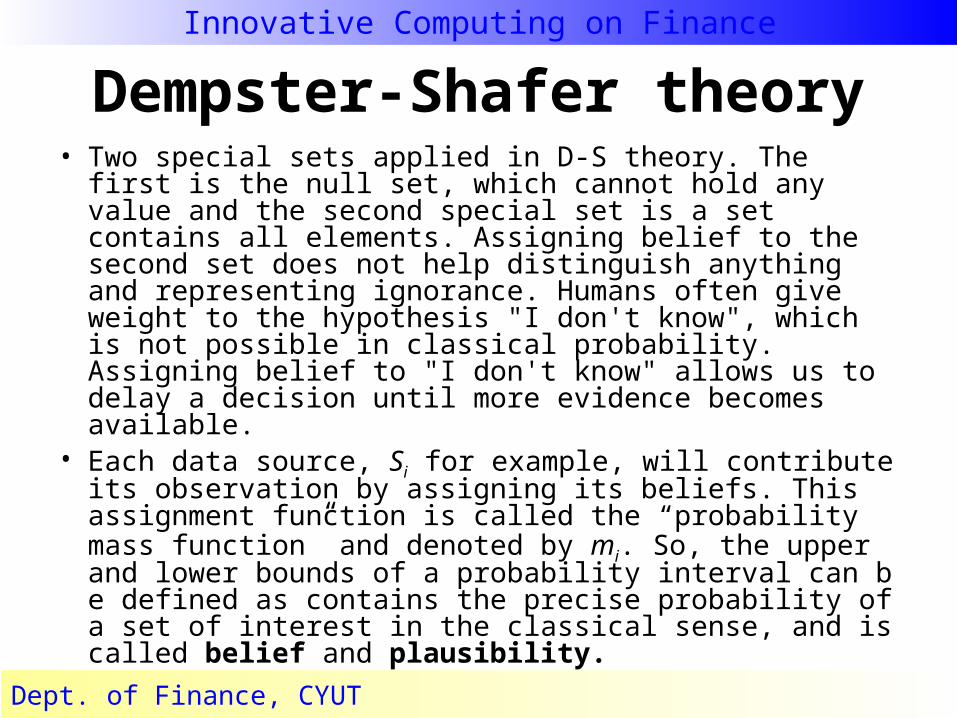

Dempster-Shafer theory• Two special sets applied in D-S theory. The first is the

null set, which cannot hold any value and the second special set is a set contains all elements. Assigning belief to the second set does not help distinguish anything and representing ignorance. Humans often give weight to the hypothesis "I don't know", which is not possible in classical probability. Assigning belief to "I don't know" allows us to delay a decision until more evidence becomes available.

• Each data source, Si for example, will contribute its observation by assigning its beliefs. This assignment function is called the “probability mass function” and denoted by mi. So, the upper and lower bounds of a probability interval can be defined as contains the precise probability of a set of interest in the classical sense, and is called belief and plausibility.

Innovative Computing on Finance

Dept. of Finance, CYUT

Dempster-Shafer theory

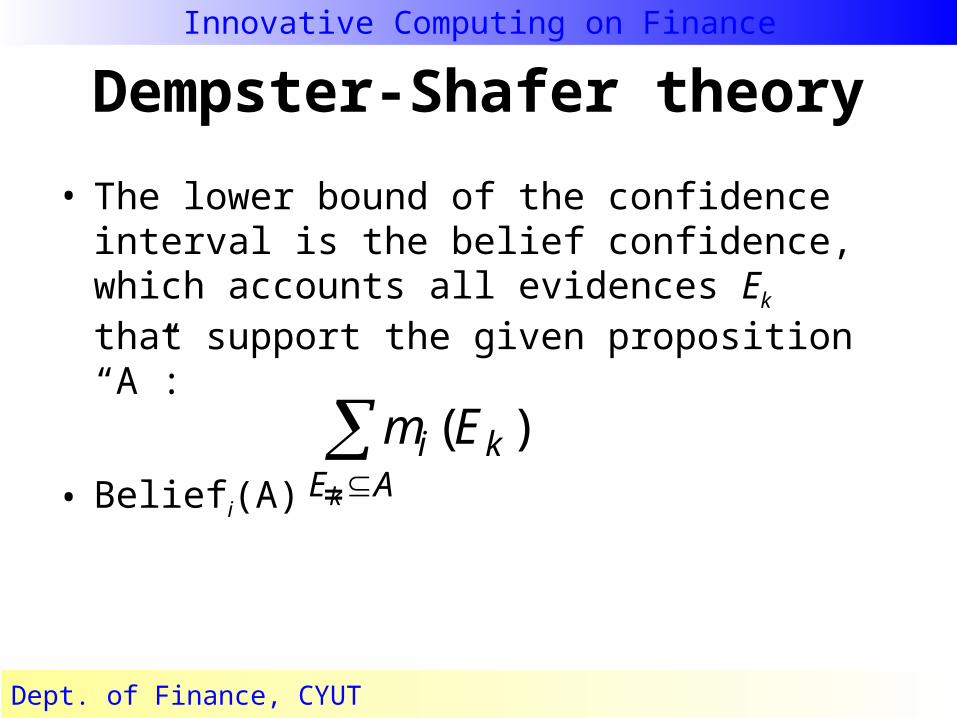

• The lower bound of the confidence interval is the belief confidence, which accounts all evidences Ek that support the given proposition “A”:

• Beliefi(A) = AE

ki

k

Em )(

Innovative Computing on Finance

Dept. of Finance, CYUT

Dempster-Shafer theory

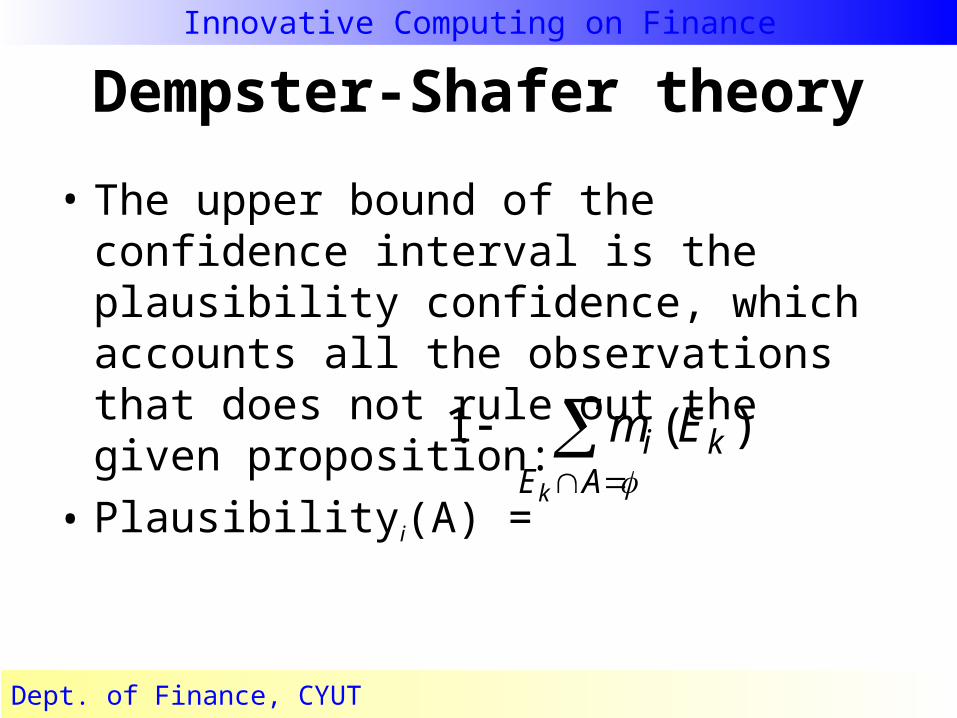

• The upper bound of the confidence interval is the plausibility confidence, which accounts all the observations that does not rule out the given proposition:

• Plausibilityi(A) =

AE

ki

k

Em )(1

Innovative Computing on Finance

Dept. of Finance, CYUT

Dempster-Shafer theory

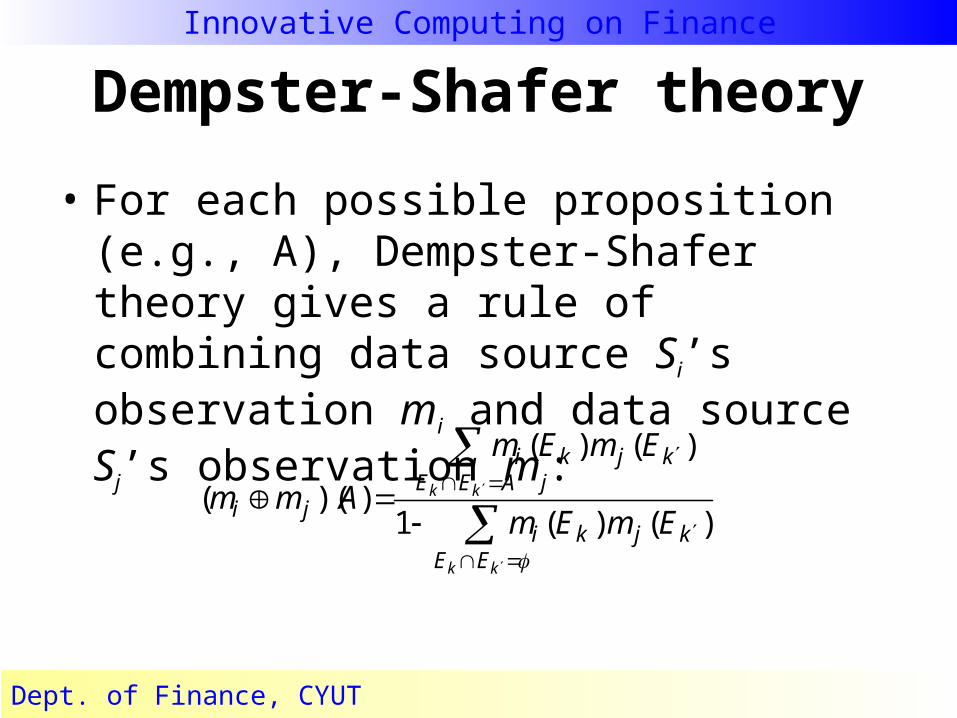

• For each possible proposition (e.g., A), Dempster-Shafer theory gives a rule of combining data source Si’s observation mi and data source Sj’s observation mj:

kk

kk

EEkjki

AEEkjki

ji EmEm

EmEm

Amm)()(1

)()(

))((

Innovative Computing on Finance

Dept. of Finance, CYUT

Dempster-Shafer theory• The Dempster's rule of combination, is a general

ization of Bayes' rule. This rule strongly emphasises the agreement between multiple sources and ignores all the conflicting evidence through a normalization factor.

• Compared with Bayesian theory, the Dempster-Shafer theory of evidence is much more analogous to our human perception-reasoning processes. Its capability to assign uncertainty or ignorance to propositions is a powerful tool for dealing with a large range of problems that otherwise would be intractable.

Innovative Computing on Finance

Dept. of Finance, CYUT

Experiment Results

Data Processing• The raw data are segmented into good records

and bad records for two successive terms and then are randomized to improve the performance of the training process.

• To provide sufficient and adequate data for the system evaluation, total of 4000 records are collected and subdivided into 1000 for the training set and 3000 for the cross validation set.

Innovative Computing on Finance

Dept. of Finance, CYUT

Experiment Results

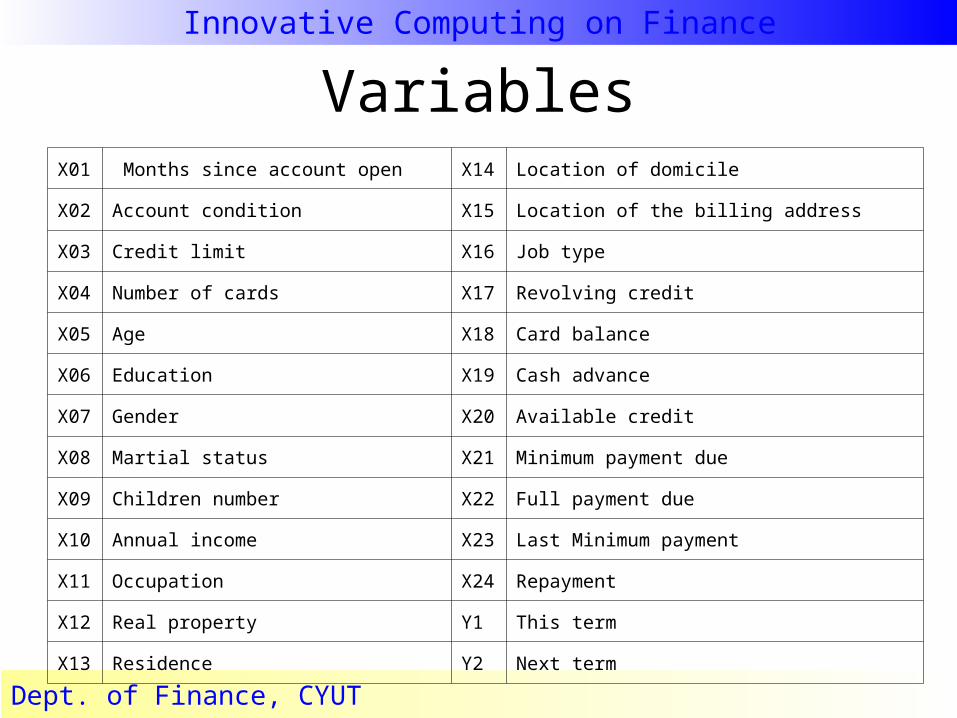

• Minimum Payment Due (X21)• Last Minimum Payment (X23) • Gender (X07)• Number of Cards Held (X04)• Martial Status (X08)• Card Holder’s Age (X05)• Revolving Credit (X17)• Account Duration (X01)• Available Credit (X20) • Annual Income (X10

Among 24 explanatory variables , it is found that a total of 10 variables have higher ranking derived from the integrated model.

Innovative Computing on Finance

Dept. of Finance, CYUT

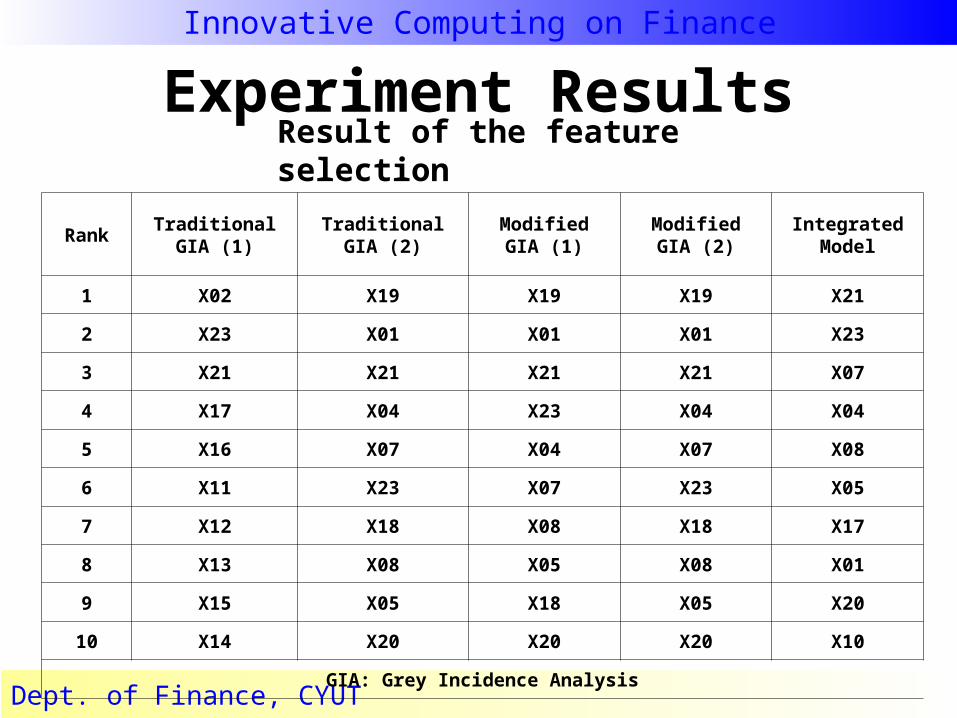

Experiment ResultsResult of the feature selection

RankTraditional

GIA (1)Traditional

GIA (2)ModifiedGIA (1)

ModifiedGIA (2)

IntegratedModel

1 X02 X19 X19 X19 X21

2 X23 X01 X01 X01 X23

3 X21 X21 X21 X21 X07

4 X17 X04 X23 X04 X04

5 X16 X07 X04 X07 X08

6 X11 X23 X07 X23 X05

7 X12 X18 X08 X18 X17

8 X13 X08 X05 X08 X01

9 X15 X05 X18 X05 X20

10 X14 X20 X20 X20 X10

GIA: Grey Incidence Analysis

Innovative Computing on Finance

Dept. of Finance, CYUT

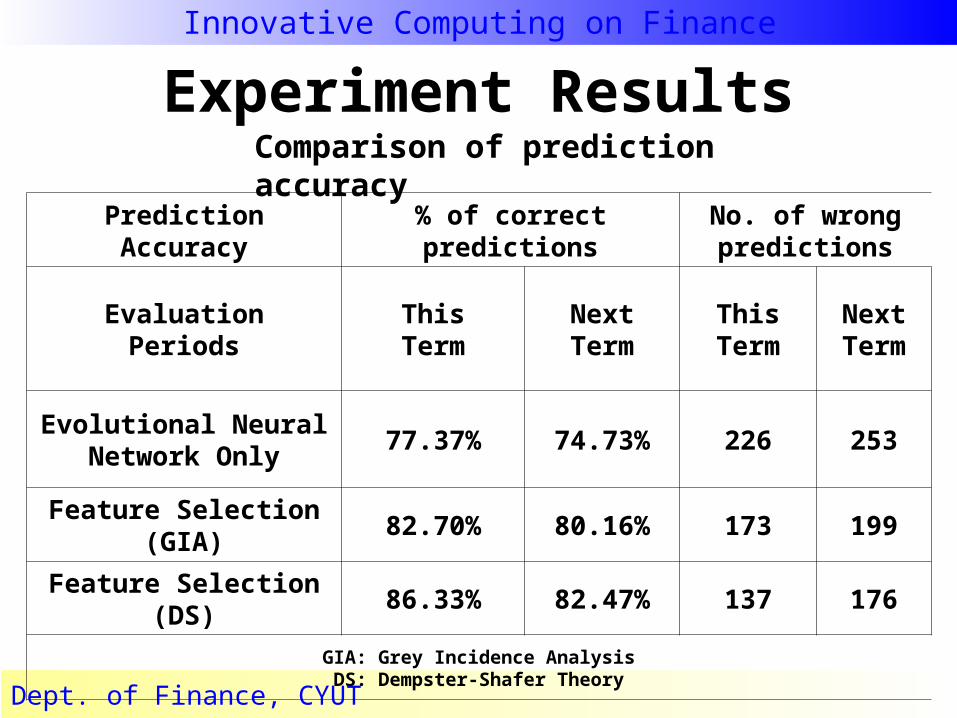

Experiment ResultsComparison of prediction accuracy

PredictionAccuracy

% of correctpredictions

No. of wrongpredictions

EvaluationPeriods

ThisTerm

NextTerm

ThisTerm

NextTerm

Evolutional NeuralNetwork Only

77.37% 74.73% 226 253

Feature Selection(GIA)

82.70% 80.16% 173 199

Feature Selection(DS)

86.33% 82.47% 137 176

GIA: Grey Incidence AnalysisDS: Dempster-Shafer Theory

Innovative Computing on Finance

Dept. of Finance, CYUT

Conclusion

• We have found this integrated feature selection approach performs better than that of applying grey incidence analysis only in terms of the rate of prediction accuracy.

• The former correctly predicts the default cases to an average of nearly 86.33% of all cases, which is about 3.63% higher than the latter. As both methods results in different order for the variables, the DS method is able to combine the different outcomes of the grey incidence analysis and perform the task of data fusion.

• We discovered that using grey incidence analysis leads us to the reduction of the variables during the process of feature selection and understood that more additional variables can not improve the accuracy of the perdition.

Innovative Computing on Finance

Dept. of Finance, CYUT

Conclusion

• This study also shows evolutional neural network with feature selection (GIA) is superior to the evolutional neural network with no feature selection. The former correctly predicts the default cases to an average of nearly 82.7% of all cases, which is about 5.4% higher than the latter.

• This study collected the real data from only one financial institute to evaluate the performance of the integrated model. Further research could follow this line to collect more real data from other financial institutions located in different geographic regions and investigate whether there is different ranking priority with the input variables and produce the inconsistent results with this study.

Innovative Computing on Finance

Dept. of Finance, CYUT

VariablesX01 Months since account open X14 Location of domicile

X02 Account condition X15 Location of the billing address

X03 Credit limit X16 Job type

X04 Number of cards X17 Revolving credit

X05 Age X18 Card balance

X06 Education X19 Cash advance

X07 Gender X20 Available credit

X08 Martial status X21 Minimum payment due

X09 Children number X22 Full payment due

X10 Annual income X23 Last Minimum payment

X11 Occupation X24 Repayment

X12 Real property Y1 This term

X13 Residence Y2 Next term