innovation, competitiveness and economic development

TRANSCRIPT

INNOVATION, COMPETITIVENESS AND ECONOMIC DEVELOPMENTUNDERSTANDING THE SITUATION FOR STARTUPS IN INDIA

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

WHAT IS COMPETITIVENESS?

• Competitiveness is the productivity (value per unit of input) with which a nation, region, or cluster utilizes its human, capital, and natural resources. Productivity sets a nationʼs or regionʼs standard of living (wages, returns on capital, returns on natural resources)• Productivity depends both on the value of products and services (e.g. uniqueness, quality) as well as the

efficiency with which they are produced. • It is not what industries a nation or region competes in that matters for prosperity, but how firms compete

in those industries• Productivity in a nation or region is a reflection of what both domestic and foreign firms choose to do in

that location. The location of ownership is secondary for prosperity.• The productivity of “local” industries is of fundamental importance to competitiveness, not just that of

traded industries• Devaluation and revaluation do not make a country more or less “competitive”

• Nations and regions compete in offering the most productive environment for business

Source: Michael E. Porter and Institute for Strategy and Competitiveness

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

WHAT DETERMINES COMPETITIVENESS

Source: Michael E. Porter and Institute for Strategy and Competitiveness

Microeconomic Competitiveness

Quality of Business Environment

State of Cluster Development

Sophistication of Company Operations & Strategy

Macroeconomic Competitiveness

Sound Monetary and Fiscal Policy

Human Development and Effective Public Institutions

Endowments

Sophistication of Company Operations & Strategy

Clusters are “geographically

proximate group of interconnected companies and

associated institutions in a particular field,

linked by commonalities and complementarities.

The geographic scope of clusters ranges from

a region, a state, or even a single city to

span nearby or neighboring countries.”

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

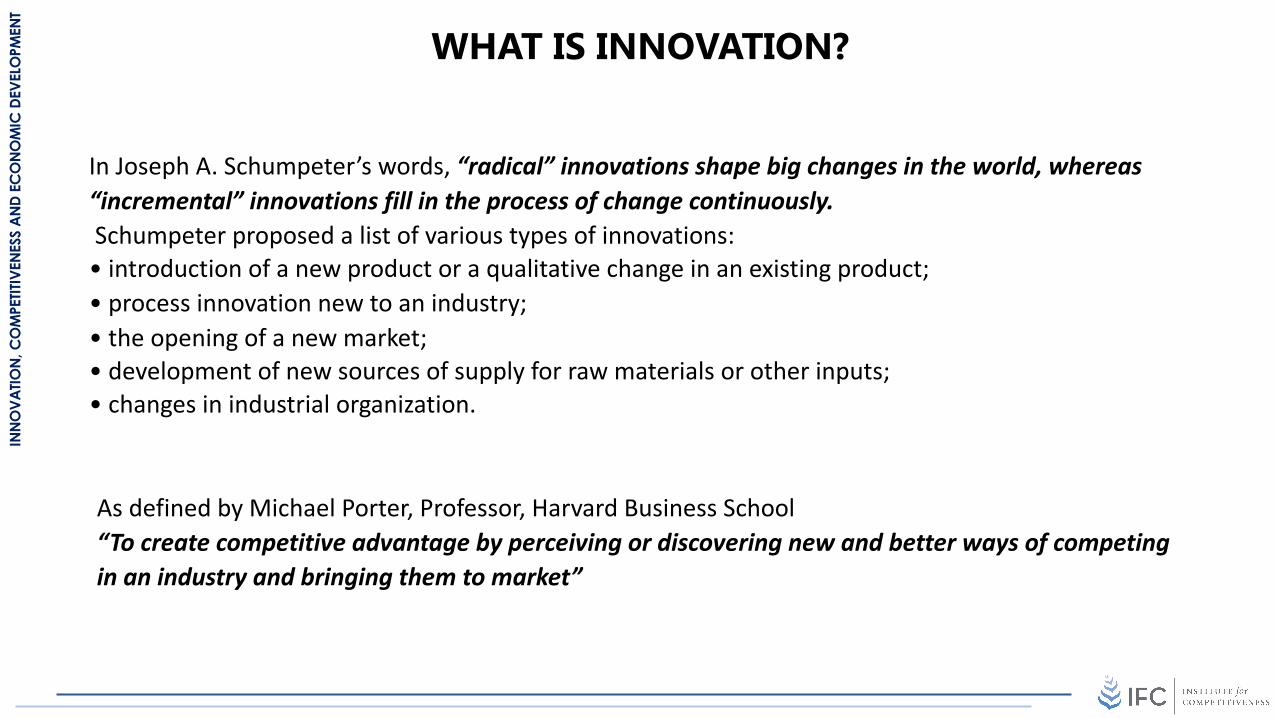

WHAT IS INNOVATION?

In Joseph A. Schumpeter’s words, “radical” innovations shape big changes in the world, whereas “incremental” innovations fill in the process of change continuously.Schumpeter proposed a list of various types of innovations: • introduction of a new product or a qualitative change in an existing product; • process innovation new to an industry; • the opening of a new market; • development of new sources of supply for raw materials or other inputs;• changes in industrial organization.

As defined by Michael Porter, Professor, Harvard Business School“To create competitive advantage by perceiving or discovering new and better ways of competing in an industry and bringing them to market”

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

WHY INNOVATE?

The capability to innovate and to bring innovation successfully to market is a crucial determinant of the global competitiveness of nations.

• Firms create value adding goods and services by realizing the potential of natural resources

Inherited Prosperity(Natural Resources)

Created Prosperity

Government

• Land• Labour• Capital

• To create conducive conditions to enable innovation

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

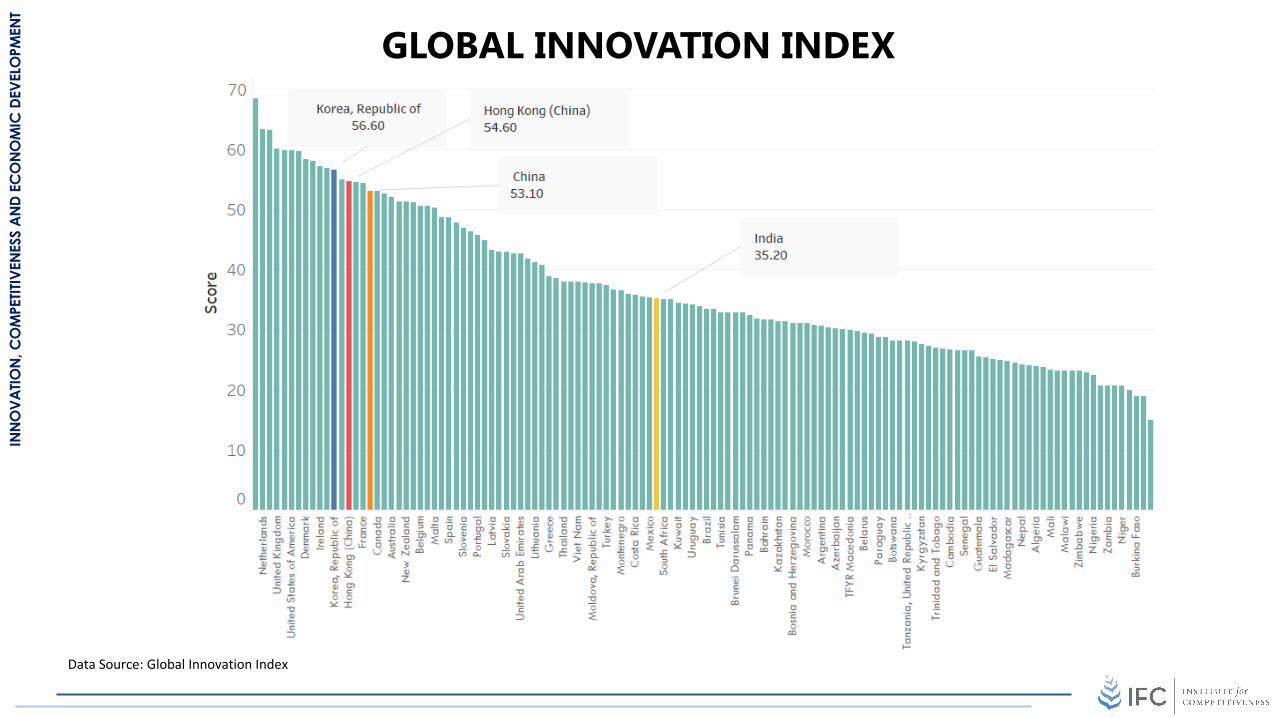

GLOBAL INNOVATION

Data Source: Global Innovation Index

GLOBAL INNOVATION INDEX

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

COUNTRY-WISE GROWTH IN PATENTSUNITED STATES

JAPAN

GERMANY SOUTH KOREATAIWAN

UNITED KINGDOMFRANCE CANADA

SWITZERLANDNETHERLANDS

SWEDEN

CHINA

ISRAELAUSTRALIA

FINLANDBELGIUMAUSTRIA

INDIA

DENMARK SPAINSINGAPORENORWAY IRELAND

NEW ZEALANDRUSSIA

SOUTH AFRICA

BRAZIL

HUNGARYMEXICO MALAYSIA

SAUDI ARABIA

ARGENTINA

POLANDTHAILAND

GREECE

VENEZUELA

TURKEY

BULGARIAPHILIPPINES

CHILEPORTUGALUKRAINE ICELAND ROMANIAKUWAIT

COLOMBIACOSTA RICAINDONESIA

EGYPTUNITED ARAB EMIRATESESTONIA

URUGUAY

CUBALEBANON

PERU

LITHUANIA PAKISTAN

SRI LANKA

BERMUDA KENYA

1

10

100

1000

10000

100000

1000000

-10 -5 0 5 10 15 20 25 30 35

Tota

l Num

ber o

f Pat

ents

gra

nted

in 2

015

CAGR Growth Rate of Patents granted from 2002-2015Source: USPTO, http://www.uspto.gov/web/offices/ac/ido/oeip/taf/cst_utlh.htm

COUNTRY WISE GROWTH IN PATENTS

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

LINK BETWEEN PATENTS AND COMPETITIVENESS

Delhi

Goa

Haryana

Maharashtra

Tamil Nadu

Uttarakhand

Gujarat

Kerala

Karnataka

Punjab

Himachal Pradesh

Andhra Pradesh

West Bengal

Rajasthan

Chhattisgarh

Madhya Pradesh

Odisha

Jammu & Kashmir

Jharkhand

Uttar Pradesh

Bihar

Sikkim

Nagaland

MizoramTripura

Assam

y = 118.32x - 6267.6R² = 0.5581

1

10

100

1000

10000

50.00 52.00 54.00 56.00 58.00 60.00 62.00 64.00 66.00 68.00 70.00

Num

ber o

f Pat

ents

file

d in

201

5-16

(in

log

scal

e)

State Competitiveness Index Scores 2016Source: Annual Reports of CGPDTM Various Rounds

LINK BETWEEN PATENTS AND COMPETITIVENESS

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

Switzerland

SwedenNetherlands

United States of America

United Kingdom

Denmark

Singapore

Finland

Germany

Ireland

South Korea

Luxembourg

Iceland

Japan

France

Hong Kong (China)

IsraelCanada

Norway

AustriaNew Zealand

China

Australia

Czech RepublicEstonia

Malta

Belgium

Spain

Italy

Cyprus

PortugalSloveniaLatvia

Slovakia

United Arab Emirates

Bulgaria

Malaysia

Poland

Hungary

Lithuania

Croatia

RomaniaTurkey

Greece

Russian FederationChile

Vietnam

Montenegro

Qatar

Ukraine

Thailand

Mongolia

Costa Rica

Moldova

Saudi Arabia

KuwaitSouth AfricaMexico

Armenia

India

Macedonia

Serbia

PanamaMauritius

Colombia

Bahrain

UruguayGeorgia

BrazilPeruMorocco

Philippines

Tunisia

Iran

Argentina

OmanKazakhstan

Dominican RepublicKenyaLebanon

Azerbaijan

Jordan

Jamaica

Paraguay

Indonesia

BotswanaSri Lanka

Trinidad and TobagoEcuador

AlbaniaTajikistan

KyrgyzstanTanzania

NamibiaGuatemala

Rwanda

Senegal

Cambodia

UgandaEl Salvador

Honduras

Egypt

Bolivia

Mozambique

AlgeriaNepalEthiopia

Madagascar

Cote dIvoire

Pakistan

Bangladesh

Malawi

BeninCameroonMali

NigeriaZimbabwe

Burundi

Zambia

Yemen

y = 0.0495x + 2.4882R² = 0.8064

2

3

4

5

6

7

10 20 30 40 50 60 70

Glo

bal C

ompe

titiv

enes

s Ind

ex 2

016-

17

Global Innovation index Score 2017

COUNTRY-WISE GROWTH IN PATENTSINNOVATION & COMPETITIVENESS: GLOBAL LEVEL

INDIA INNOVATION INDEX

ANALYSING INNOVATION ECOSYSTEM AT THE SUB-REGIONAL LEVEL IN INDIA

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

WHY INDIA INNOVATION INDEX?

• The Global Innovation Index reveals the variation in performance across countries. It helps our policymakers in identifying the areas in which our country is lagging behind.

• But the conditions vary significantly within the country. Region specific insights are important as different regions have disparate needs and challenges. And therefore policies driving progress in these regions should also be framed accordingly. Thus, India Innovation Index is conceptualised to analyse innovation ecosystem at sub-regional level in India.

• India Innovation Index intends to help in better understanding of a state’s innovation ranking and its performance relative to its economic peers. It incorporates key indicators relating to six pillars that can be used to understand the performance of a state with regards to innovation capabilities. The pillar performance rankings can also serve to identify key areas where a state is under or over performing.

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

WHY INDIA INNOVATION INDEX?

CHALLENGES & OPPORTUNITIES

Identifying key challenges and opportunities for

policymakers, businesses and state governments

RANKINGS

Ranking of Indian states to measure the current

state of innovation

ACTIONS

Assisting in tailoring governmental policies to

foster innovation by providing focus areas and identifying opportunities.

I N D I A I N N O V AT I O N I N D E X

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

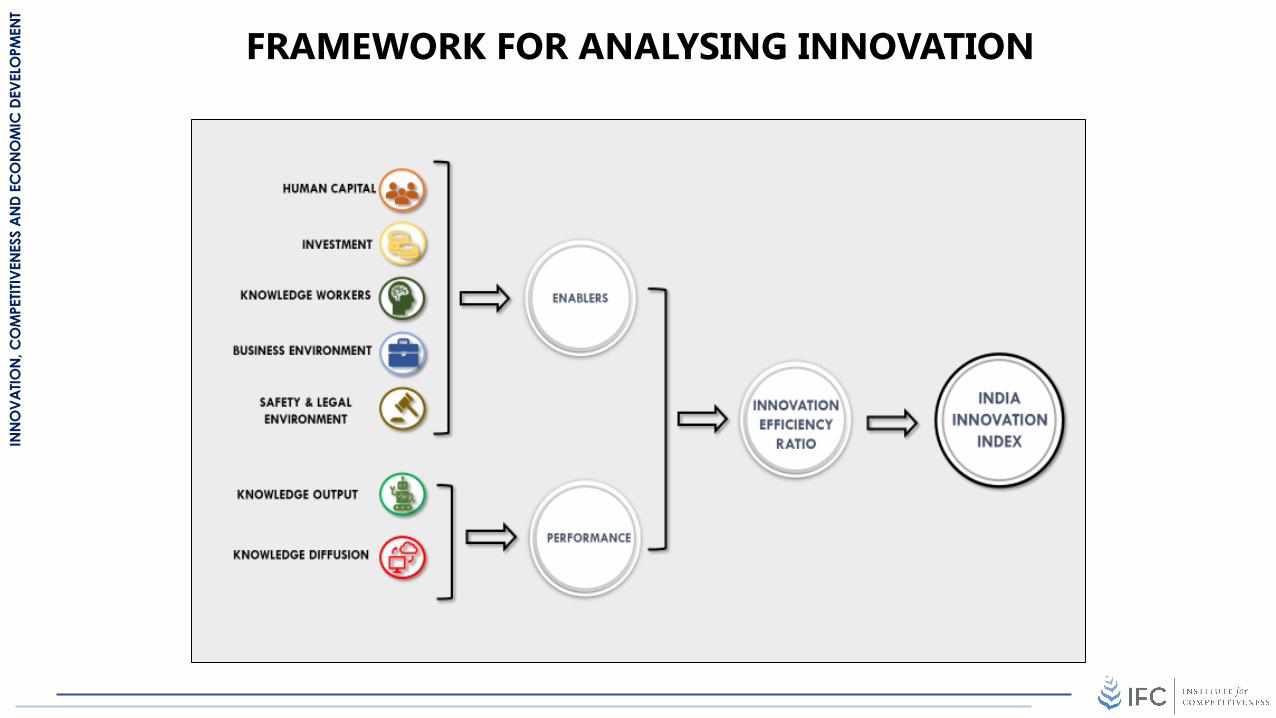

FRAMEWORK FOR ANALYSING INNOVATION

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

INNOVATION SCORES

Insights

• The states show variation across innovation scores with scores ranging from 42.9 to 6.2.

• Karnataka, Delhi, Tamil Nadu and Maharashtra are the best performing states.

• 11 out of thirty-six states register single digit score.

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

HOW INNOVATION HAS CHANGED?

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

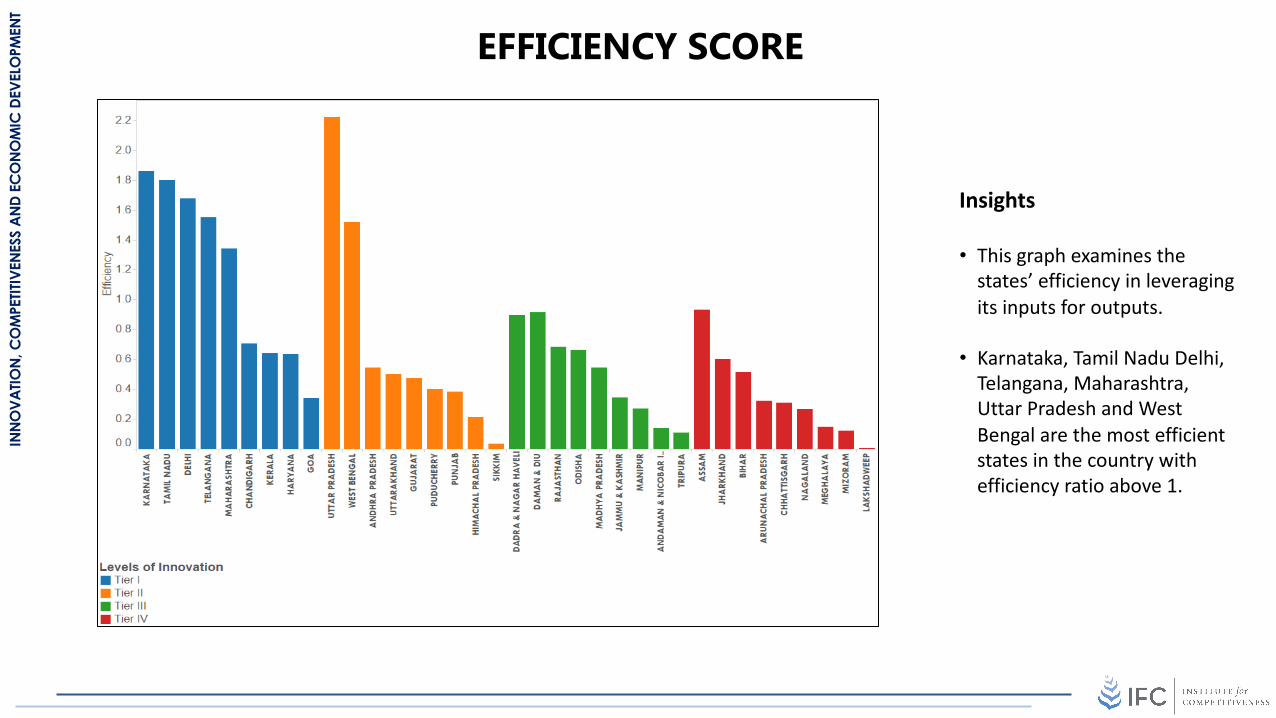

EFFICIENCY SCORE

Insights

• This graph examines the states’ efficiency in leveraging its inputs for outputs.

• Karnataka, Tamil Nadu Delhi, Telangana, Maharashtra, Uttar Pradesh and West Bengal are the most efficient states in the country with efficiency ratio above 1.

INNOVATION, CLUSTERS AND COMPETITIVENESS

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CLUSTER BASED ECONOMIC DEVELOPMENT:PROCESS

CLUSTER IDENTIFICATION

CLUSTER ASSESSMENT

POLICY FORMULATION

Cluster mapping aims at creating a detailed record of all the existing clusters across all sectors in India.

A comprehensive evaluation of the clusters identified in Stage 1 is conducted.

The detailed assessment of clusters conducted in Stage 2 helps in designing effective cluster based strategies for economic development.

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CLUSTER IDENTIFICATION

TYPES OF INDUSTRIES

Traded Industries

Copyright ©

Local Industries

• Traded industries are those that concentrate inparticular regions but sell products acrossregions and countries. (Delgado, Bryden, & Zyontz)

• Examples of traded industries include apparel, automotive, textiles etc.

• Local industries are dispersed throughout thenation. Their presence in a particular region isgenerally proportional to the region’s size asthey primarily serve the local market. (Delgado,Bryden, & Zyontz)

• Examples of local industries are real estateservices, hospitals, etc.

Traded Clusters are formed by grouping traded industries and likewise, the groups of local industries form local clusters.

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CLUSTER ASSESSMENT

Cluster Assessment

Analysing Business

Environment

Identifying the productivity of

clusters

Ascertaining barriers to

growth

Recognising Export Oriented

Clusters, Emerging Clusters

Analysing the relationship

between clusters and economic development

Role of clusters

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

POLICY FORMULATION

ROLE OF GOVERNMENT

Attracting FDI Workforce Training and Skill Upgrading

Addressing Bottlenecks by Public-Private

CollaborationsInfrastructure Development Export Promotion

A successful cluster policy is based on overall economic policies.

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CLUSTER PERFORMANCE

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CLUSTER STRENGTH

• A clear geographical distinction is observed, with the Southern region having a stronger cluster profile than the rest of the country.

• 32 percent of the regions have less than 20 stars, implying the lack of strong clusters that can enhance competitiveness and increase prosperity in the region.

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CLUSTER MAP

MAHARASHTRA• Video Production &

Distribution• Local Commercial Services• Furniture

GUJARAT• Non-Metal Mining• Jewelry and Precious

Metals• Upstream Chemical

Products

TAMIL NADU• Footwear• Information Technology• Textile Manufacturing

UTTAR PRADESH• Livestock Processing• Communication

Equipment & Services• Footwear

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

HOW CLUSTERS IMPACT COMPETITIVENESS

By increasing the current (static) productivity of constituent firms or industries

By increasing the capacity of cluster participants for innovation and productivity growth

By stimulating new business formation that supports innovation and expands the cluster

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CLUSTERS AND COMPETITIVENESS

Andhra Pradesh

Assam

Bihar

Chhattisgarh

Delhi

Goa

Gujarat

Haryana

Himachal PradeshJammu & Kashmir

Jharkhand

Karnataka

Kerala

Madhya Pradesh

Maharashtra

Manipur MeghalayaNagaland

Odisha

Punjab

Rajasthan

Sikkim

Tamil Nadu

Tripura

Uttar Pradesh

UttarakhandWest Bengal

0

20

40

60

80

100

120

140

0 5 10 15 20 25 30 35

Clus

ter S

tren

gth

State Competitiveness Rank

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CLUSTERS AND PRODUCTIVITY

The productivity within clusters is enhanced as:

• clusters provide highly specialized inputs at a low cost

• clusters lead to a reduction in the transaction cost

• clusters facilitate complementarities between activities of cluster members

• clusters provide easy access to information, thereby reducing if not eliminating the information asymmetries

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CLUSTERS AND INNOVATION

Clusters contribute to innovation in the following ways:• by easier and faster access to new processes needed for innovation

• by proceeding faster with innovations due to the proximity of potential suppliers•• by making the availability of specialized professionals easy

• by identifying new technological, operating and delivery opportunities

• by direct observation of other firms

• by utilizing complementarities of local innovation partners

• by reducing transaction costs of innovation

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CLUSTERS AND INNOVATION

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CLUSTERS AND BUSINESS FORMATION

Clusters lead to new business formation as:

• they offer lower barriers to entry (and exit) as the cost of specialized inputs is lower compared to non-cluster areas

• they provide information about new business opportunities

• they provide environment rich in social capital

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

INNOVATION AND EMPLOYMENT

Karnataka

Maharashtra

Kerala West Bengal

Tamil NaduAndhra PradeshJharkhand

Uttar PradeshHaryana

Gujarat

RajasthanPunjab

y = 4E-05x + 26.817R² = 0.3286

0

20

40

60

80

100

120

140

160

180

200

0 500000 1000000 1500000 2000000 2500000

Pate

nts p

er 1

0000

0 Em

ploy

ees

Employment

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

INNOVATION AND COMPETITIVENESS

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CITIES & INNOVATION

THE DRIVERS OF INNOVATION

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

INDIA’S URBANISATION

290 million2001

340 million2008

590 million

2030

DATA SOURCE: MCKINSEY REPORT

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

NSDP VS URBANISATION

APAR

AS

BR

CH

DL

GA*

GJ*

HR

HP

JKJH

KAKL*

MP

MH

MN

MLMZ*

NL

OR

PB

RJ*

SK

TN

TR

UP

UK

WB

y = 1731.3x + 19928R² = 0.5605

0

50000

100000

150000

200000

250000

0.00 20.00 40.00 60.00 80.00 100.00 120.00

NSD

P pe

r cap

ita (a

t 200

4-05

pric

es) i

n 20

10-1

1

% of People residing in Urban Areas in 2011

* depicts states with NSDP per capita in 2011-12 all other figures for 2012-13

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CONTRIBUTION OF URBAN AREAS TO INDIAN ECONOMY

70 %

More than 70 percent of India’s GDP will be generated by urban areas by 2020

8.8 %

The real GDP growth rate of urban India is 8.8 compared to 4 % of rural India

DATA SOURCE: MCKINSEY REPORT

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

HOW CLUSTERS IMPACT COMPETITIVENESS OF CITIES

HyderabadVijayawadaVishakhapatnam

GuwahatiPatna

Raipur

Delhi

AhmedabadRajkotSuratVadodara

ChandigarhFaridabad GurgaonShimla

JammuSrinagar

DhanbadJamshedpurRanchi

BengaluruMysore

KochiKozhikodeThiruvananthapuram

BhopalIndoreJabalpur

MumbaiNagpurNashik Pune

Bhubaneswar

Amritsar Ludhiana

JaipurKota

ChennaiCoimbatoreMadurai

AgraAllahabadKanpurLucknowMeerut NoidaVaranasi

DehradunAsansol Kolkata

y = 1.5677x + 3.5079

0

20

40

60

80

100

120

140

0.00 10.00 20.00 30.00 40.00 50.00 60.00 70.00

Stat

e Cl

uste

r Str

engt

h

Competitiveness Score

The presence of clusters and thelinkages between them in a stateimpact the competitiveness of itscities. In India, most of the highlycompetitive cities belong to asmall group of industrializedstates (including Maharashtra,Tamil Nadu, Gujarat andKarnataka) while the leastcompetitive cities belong to lessindustrialized states likeJharkhand, Bihar, Chhattisgarh,Jammu and Kashmir, etc.

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

INDIAN START-UP ECOSYSTEM

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

GLOBAL DISTRIBUTION OF STARTUPS

© GeoNames, HERE, MSFT, Microsoft, NavInfo, Thinkware Extract, WikipediaPowered by Bing

US83,000+

Canada6,100+

UK7,900+

China10,000+

India10,000+

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

$ 2.2 Bn Revenue(2016)

Over 23.7 Mn Total transactions(2016)

80 % Revenue Growth Y-O-Y(2017)

7 Mn +Transactions a day(2017)

$ 1 Bn Valuation(2017)

4x increase in number of rides

Raised over $ 115 Mn Funding till date(2017)

100% + Revenue Growth Y-O-Y(2017)

Data Source: NASSCOM Start-Up Report 2017

SELECT INDIAN START-UPS

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

Stages of a start-up lifecycle

PRE-STARTUP

GROWTH

STARTUP

DiscoveryIdentify a potential scalable product/service idea for a big enough target market

ValidationThe service or product discovered hits the market, looking for the first clients ready to pay for it

EfficiencyThe entrepreneur begins to define his/her business model and looks for ways to increase customer base

ScalePushing the growth of the business aggressively while increasing its capacity to grow in a sustainable manner

MaintenanceMaximising benefits and facing problems derived from the global dimension that the business has achieved

Sale or RenewalThe decision to sell the startup to a giant or acquire huge resources that the brand will need to continue growing

START-UP LIFECYCLE

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

GROWTH OF START-UPS

Data Source: NASSCOM Start-Up Report 2017

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

REGIONAL ANALYSIS

DELHI25 percent of the total start-ups

BANGALORE27 percent of the total start-upsMUMBAI

16 percent of the total start-ups

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

CHALLENGES FACED BY STARTUPS

FUNDING

PRODUCT MANAGEMENT

MARKET ACCESS

GOVERNMENT POLICIES

TALENT

START-UP CHALLENGES

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

SHARE OF FAILED START-UPS

64

36

80

30

0

10

20

30

40

50

60

70

80

90

B2C B2B

2016 2017

B2B start-ups show higher stability with further fall in share of failed B2B Start-ups Data Source: NASSCOM Start-Up Report 2017

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

SOCIAL PROGRESS

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

A unique tool to complement GDP

§The Social Progress Index provides the first concrete framework to measuresocial progress independent of GDP.

§It is an actionable tool designed in a way to helpleaders, policymakers, civilsociety and businesses to make policy decisions and CSR investments.

§It provides a holisticmeasure of social progress that encompasses the many aspects of health of societies.

§The core principle of the index is to measure theoutcomes that matter to the people, and not the inputs.The dimensions are further disaggregated into actionable components to allow for a multifaceted view of

welfare. Components are designed to reflect different aspects that make up the dimension. At the most granular level we have the outcome indicators which are aggregated to form components.

WHAT IS SOCIAL PROGRESS INDEX?The Social Progress Index is a comprehensive framework designed to measure the wellbeing of individuals,assessed through social and environmental indicators conceived on the understanding that regardless of theeconomic achievements, a region can’t be termed as successful if it fails to provide for people’s most essentialneeds, protect its environment, deliver building blocks to enhance and sustain individual’s wellbeing or helpcommunities to grow.

It is the starting point of a strategy that seeks to improve the quality of lives of millions of people in India.

Social Progress Index measures the progress based on three dimensions.

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

SOCIAL PROGRESS: FRAMEWORK

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

SOCIAL PROGRESS: OVERALL SCORES

STATE LEVEL DISTRICT LEVEL

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

INNOVATION AND SOCIAL PROGRESS

ANDHRA PRADESH

ARUNACHAL PRADESH

ASSAM

BIHAR

CHHATTISGARH

DELHIGOA

GUJARAT HARYANA

HIMACHAL PRADESH

JAMMU & KASHMIR

JHARKHAND

KARNATAKA

KERALA

MADHYA PRADESH

MAHARASHTRA

MANIPUR

MEGHALAYA

MIZORAM

NAGALAND

ODISHA

PUNJAB

RAJASTHAN

SIKKIM

TAMIL NADU

TRIPURA

UTTAR PRADESH

UTTARAKHAND

WEST BENGAL

40

45

50

55

60

65

70

0 5 10 15 20 25 30 35 40 45 50

Soci

al P

rogr

ess

Innovation

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

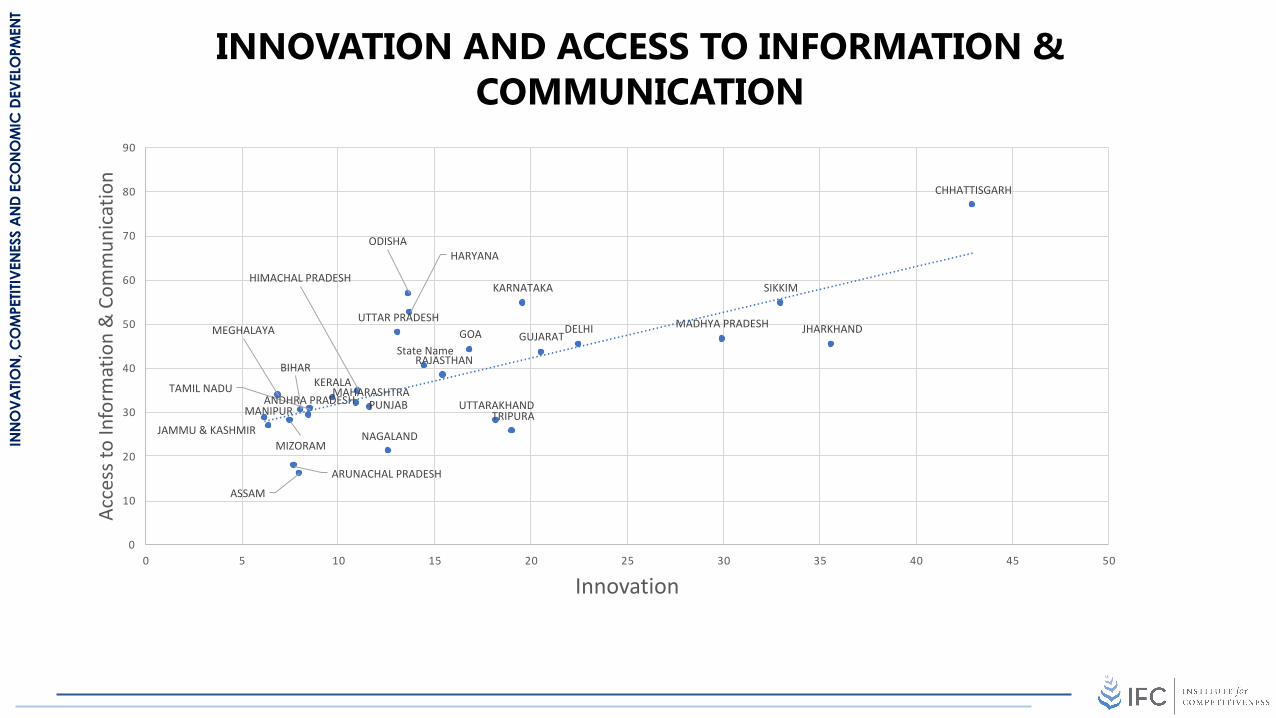

INNOVATION AND ACCESS TO INFORMATION & COMMUNICATION

State Name

ANDHRA PRADESH

ARUNACHAL PRADESH

ASSAM

BIHAR

CHHATTISGARH

DELHIGOA GUJARAT

HARYANA

HIMACHAL PRADESH

JAMMU & KASHMIR

JHARKHAND

KARNATAKA

KERALA

MADHYA PRADESH

MAHARASHTRAMANIPUR

MEGHALAYA

MIZORAMNAGALAND

ODISHA

PUNJAB

RAJASTHAN

SIKKIM

TAMIL NADU

TRIPURA

UTTAR PRADESH

UTTARAKHAND

0

10

20

30

40

50

60

70

80

90

0 5 10 15 20 25 30 35 40 45 50

Acce

ss to

Info

rmat

ion

& C

omm

unic

atio

n

Innovation

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

INNOVATION AND ACCESS TO ADVANCED EDUCATION

ANDHRA PRADESH

ARUNACHAL PRADESH

ASSAM

BIHAR

CHHATTISGARH

DELHI

GOA

GUJARAT

HARYANA

HIMACHAL PRADESH

JAMMU & KASHMIR

JHARKHAND

KARNATAKA

KERALA

MADHYA PRADESH

MAHARASHTRA

MANIPUR

MEGHALAYA

MIZORAMNAGALAND ODISHA

PUNJAB

RAJASTHANSIKKIM

TAMIL NADU

TRIPURA

UTTAR PRADESH

UTTARAKHAND

WEST BENGAL

0

10

20

30

40

50

60

70

0 5 10 15 20 25 30 35 40 45 50

Acce

ss to

Adv

ance

d Ed

ucat

ion

Innovation

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

SOCIAL PROGRESS: COUNTRY LEVEL PERFORMANCE

0

10

20

30

40

50

60

70

80

90So

cial

Pro

gres

s In

dex

Nut

ritio

n &

Bas

ic M

edic

al C

are

Wat

er &

San

itatio

n

Shel

ter

Pers

onal

Saf

ety

Acc

ess

to B

asic

Kno

wle

dge

Acc

ess

to In

form

atio

n &

Com

mun

icat

ion

Hea

lth &

Wel

lnes

s

Envi

ronm

enta

l Qua

lity

Pers

onal

Rig

hts

Pers

onal

Fre

edom

& C

hoic

e

Incl

usio

n

Adv

ance

d Ed

ucat

ion

Districts perform the beston knowledge, an areathat has been a focus ofMDGs, SDGs and theIndian government

India’s districts struggle with Advanced Education landscape and communication facilities.

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

SOCIAL PROGRESS: COMPONENT LEVEL PERFORMANCE

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

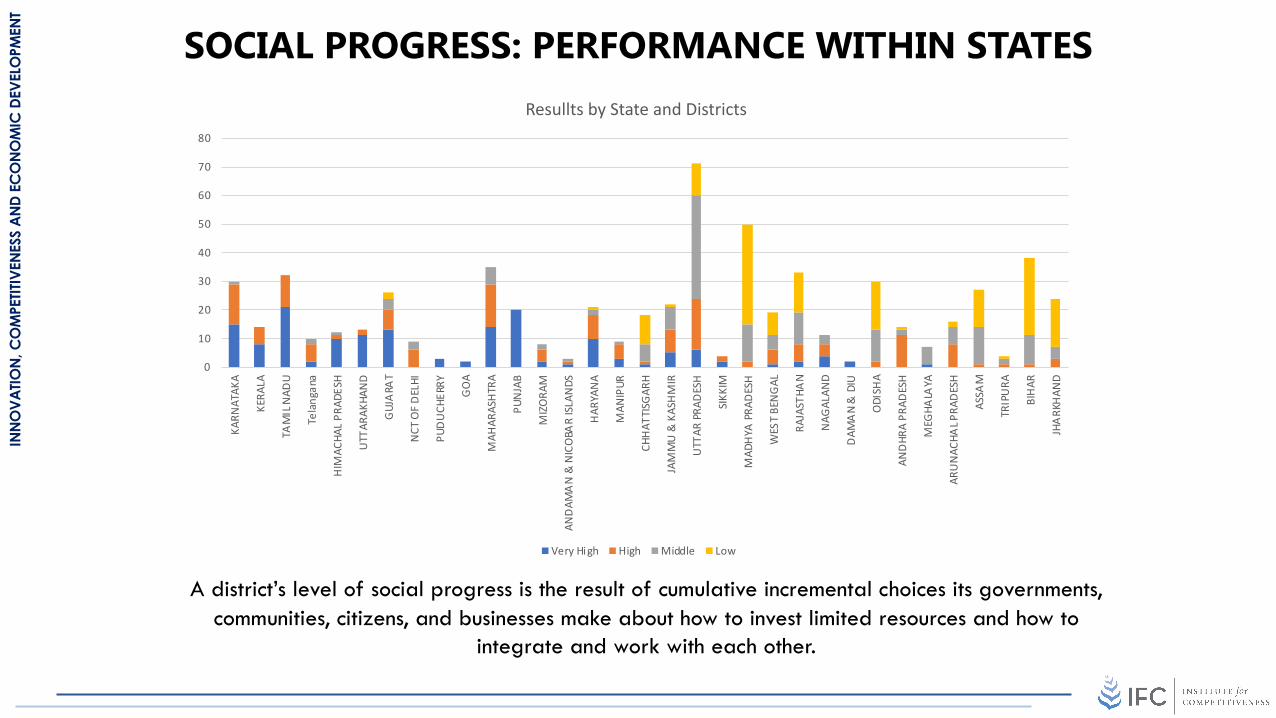

SOCIAL PROGRESS: PERFORMANCE WITHIN STATES

0

10

20

30

40

50

60

70

80

KARN

ATAK

A

KERA

LA

TAM

IL N

ADU

Tela

ngan

a

HIM

ACHA

L PR

ADES

H

UTT

ARAK

HAN

D

GUJ

ARA

T

NCT

OF

DEL

HI

PUD

UCH

ERRY

GO

A

MAH

ARAS

HTR

A

PUN

JAB

MIZ

ORA

M

AND

AMA

N &

NIC

OBA

R IS

LAN

DS

HAR

YAN

A

MAN

IPUR

CHH

ATTI

SGAR

H

JAM

MU

& K

ASH

MIR

UTT

AR P

RAD

ESH

SIKK

IM

MAD

HYA

PRA

DES

H

WES

T BE

NG

AL

RAJA

STHA

N

NAG

ALAN

D

DAM

AN

& D

IU

ODI

SHA

AND

HRA

PRAD

ESH

MEG

HALA

YA

ARU

NAC

HAL P

RAD

ESH

ASSA

M

TRIP

URA

BIH

AR

JHA

RKH

AND

Resullts by State and Districts

Very High High Middle Low

A district’s level of social progress is the result of cumulative incremental choices its governments, communities, citizens, and businesses make about how to invest limited resources and how to

integrate and work with each other.

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

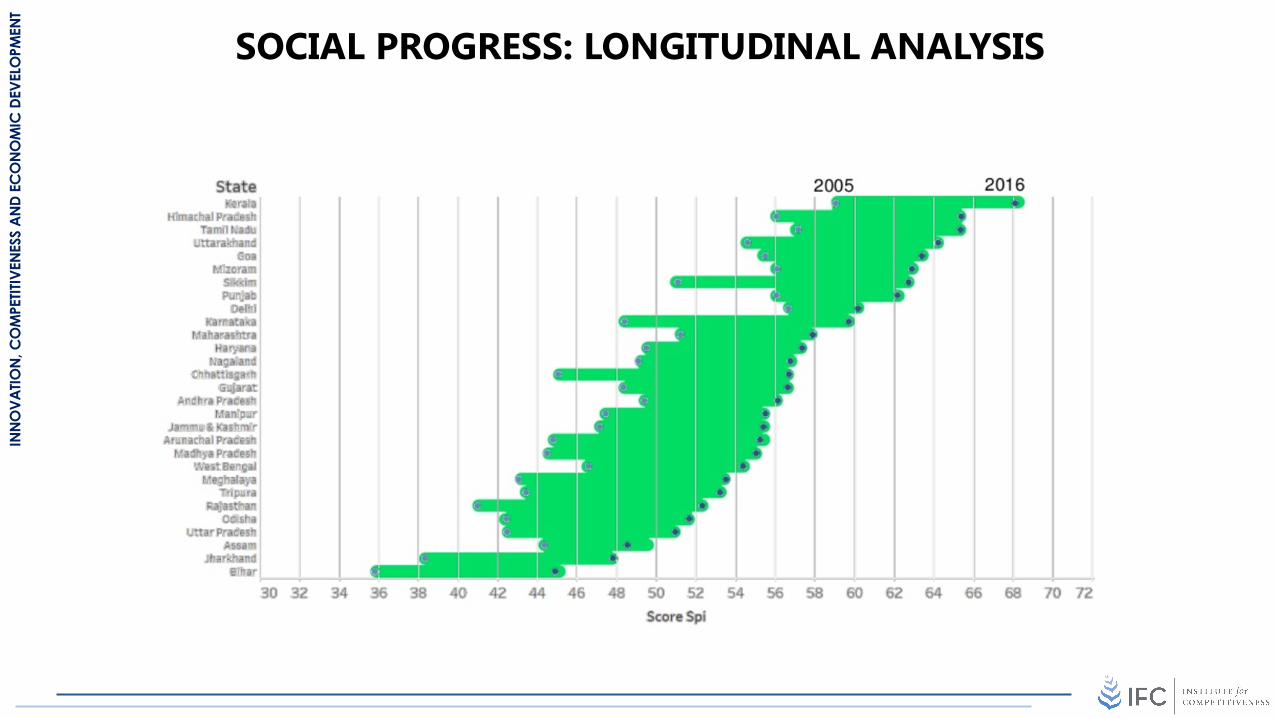

SOCIAL PROGRESS: LONGITUDINAL ANALYSIS

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

WHAT IF A COUNTRY LACKS A

ROBUST IP REGIME

Local rules and incentives that encourage productivity and investment are decreased :• Lower salaries due to low end work.• Lower capital investments as companies

want adequate standards.• Lesser incentive to innovate as knowledge

is not adequately protected.• Competition between companies becomes

more distorted as there is an absence of a level playing field.

• Companies reduce spending on R and D as they expect others to invest while they reap the benefits.

• IPR rules if they are not adequately present.• Distort incentives to share knowledge.• Adverse impact on innovation at the related

and supporting industry level.• It also results in a reduced network effect in

clusters as different firms in clusters are adamant about sharing their business knowhow.

Sophisticated and demanding local customers and needs .

• Strict quality, safety , and environmental standards are not met as IPR laws are weaker.

• Greater imports as companies are not able to meet sophisticated demand.

• Government procurement of advanced technology as no laws are in place.

Distortion in access to high quality business inputs especially in :-• Information• Scientific and Technological

infrastructure.• ‘Intellectual’ capital is not being

recognised.• In case of no protection this may

result in companies’ having no incentive to innovate.

Related, Supporting Industries And Institutions

Demand ConditionsFactor Conditions

Context for Firms Strategy And Rivalry

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

Dimensions of Innovation Policy

RESEARCH EDUCATION FINANCE INDUSTRY

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

Role of the Government

321ESTABLISH

INSTITUTIONS TO FACILITATE

RESEARCH AND

DEVELOPMENT

INCENTIVES TO SUPPORT

INNOVATORS

PROVIDE ENVIRONMENT TO SUPPORT INNOVATION BY REMOVING

OBSTACLES FACED BY

COMPANIES

4

INVEST IN CREATION OF KNOWLEDGE

WORKRS

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

RESEARCH & DEVELOPMENT EXPENDITURE

1ESTABLISH

INSTITUTIONS TO FACILITATE

RESEARCH AND

DEVELOPMENT

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

GERD

1ESTABLISH

INSTITUTIONS TO FACILITATE

RESEARCH AND

DEVELOPMENT

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

Business Environment

2

INCENTIVES TO SUPPORT

INNOVATORS

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

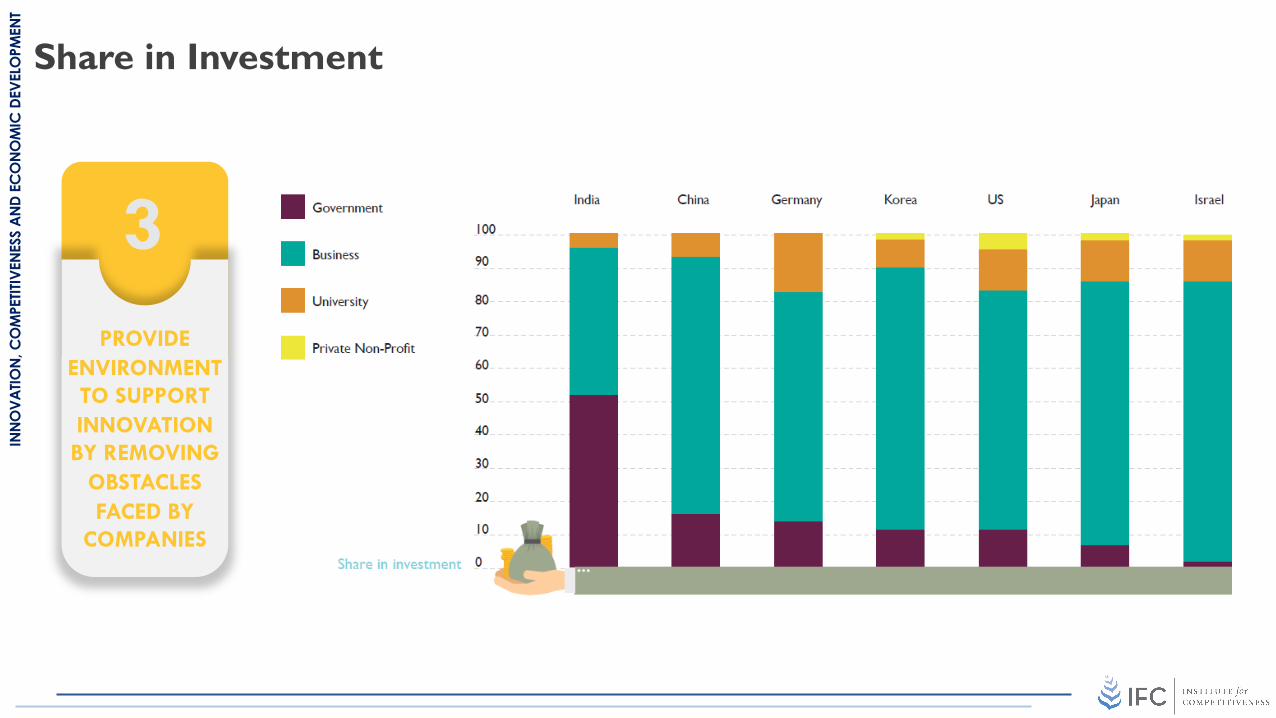

Share in Investment

3PROVIDE

ENVIRONMENT TO SUPPORT INNOVATION BY REMOVING

OBSTACLES FACED BY

COMPANIES

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

Regulatory Environment

3PROVIDE

ENVIRONMENT TO SUPPORT INNOVATION BY REMOVING

OBSTACLES FACED BY

COMPANIES

INNO

VATIO

N, C

OM

PETIT

IVEN

ESS

AND

ECO

NOM

IC D

EVEL

OPM

ENT

4

INVEST IN CREATION OF KNOWLEDGE

WORKERS

Institute for CompetitivenessU 24 / 8

DLF Phase 3Gurgaon 122 002

Haryana, IndiaPhone: +91 124 437 6676

www.competitiveness.in