innovation: a key enabler? or a distraction from action? · – infrastructure base is aging and...

TRANSCRIPT

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

©2015 Energy Technologies Institute LLP The information in this document is the property of Energy Technologies Institute LLP and may not be copied or communicated to a third party, or used for any purpose other than that for which it is supplied without the express written consent of Energy Technologies Institute LLP.This information is given in good faith based upon the latest information available to Energy Technologies Institute LLP, no warranty or representation is given concerning such information, which must not be taken as establishing any contractual or other commitment binding upon Energy Technologies Institute LLP or any of its subsidiary or associated companies.

Innovation: A key enabler? Or a distraction from Action?

Innovation and the path towards decarbonisationJo Coleman, Strategy Director

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

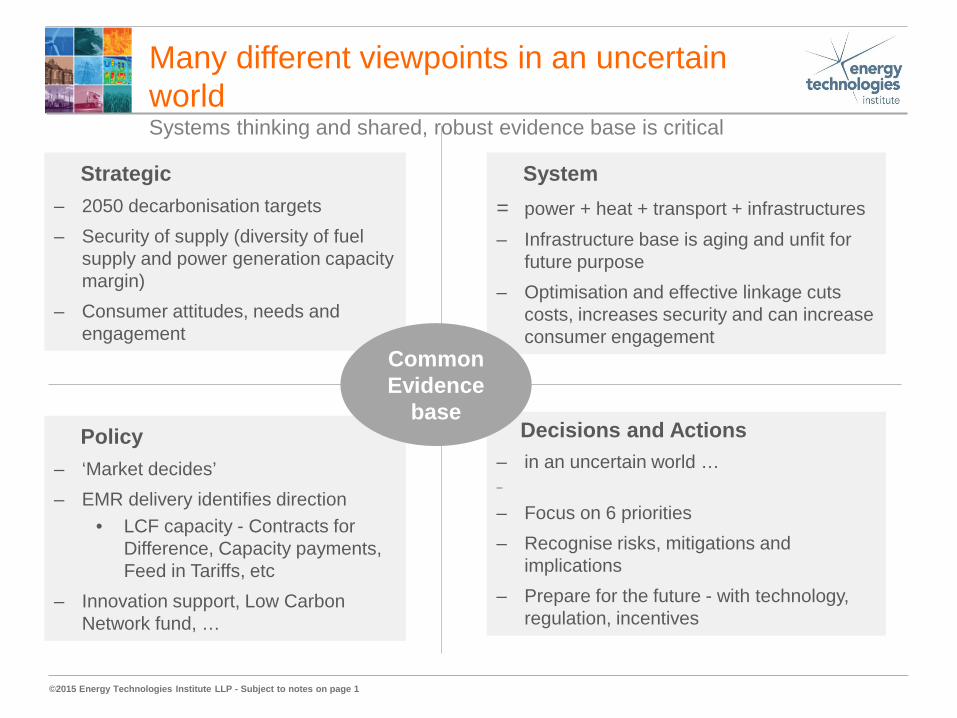

Many different viewpoints in an uncertain worldSystems thinking and shared, robust evidence base is critical

System= power + heat + transport + infrastructures– Infrastructure base is aging and unfit for

future purpose– Optimisation and effective linkage cuts

costs, increases security and can increase consumer engagement

Policy– ‘Market decides’– EMR delivery identifies direction

• LCF capacity - Contracts for Difference, Capacity payments, Feed in Tariffs, etc

– Innovation support, Low Carbon Network fund, …

Decisions and Actions – in an uncertain world …–

– Focus on 6 priorities– Recognise risks, mitigations and

implications– Prepare for the future - with technology,

regulation, incentives

Strategic– 2050 decarbonisation targets– Security of supply (diversity of fuel

supply and power generation capacity margin)

– Consumer attitudes, needs and engagement

Common Evidence

base

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

Decarbonisation pathway in the context of…

• Increasing demand to 2050– Population: 65 to 77 million– Vehicles: 28 to 35-43 million cars– Housing: 26 to 38 million houses, 90% of todays housing will remain in 2050

• Action to date– Beginning to decarbonise power sector– Increasing energy efficiency (especially in cars)

• UK energy system is a unique and complex set of interlinked assets and infrastructure– Ageing power plants need replacing– Significant wind (and marine) energy potential– Significant offshore CO2 storage potential– Significant opportunity for UK biomass – Reasonable public support for all low carbon options

– But, poor housing stock and very significant heating challenge

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

Decarbonising heat is our biggest challengeH

eat /

Ele

ctric

ity (G

W)

0

50

100

150

250

200

Jan 10 Apr 10 July 10 Oct 10

HeatElectricity

Data source: Robert Sansom, Imperial (2011)

GB 2010 heat and electricity hourly demand variability - commercial & domestic

The gas grid is our biggest energy storage device

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

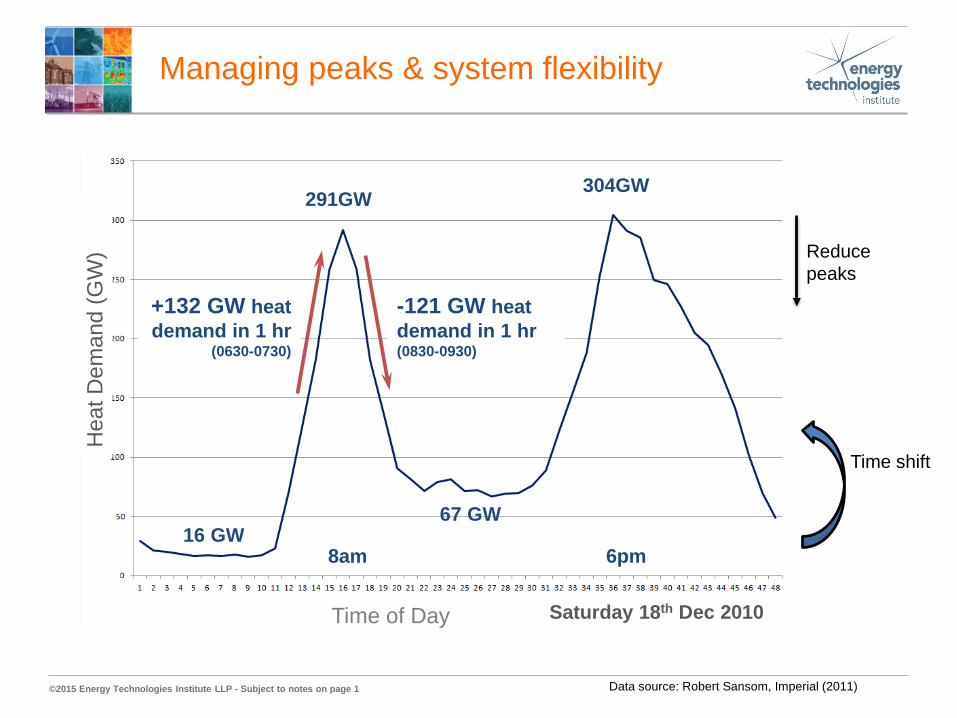

+132 GW heat demand in 1 hr

(0630-0730)

-121 GW heat demand in 1 hr(0830-0930)

291GW

8am 6pm

304GW

16 GW 67 GW

Saturday 18th Dec 2010

Hea

t Dem

and

(GW

)

Time of Day

Managing peaks & system flexibility

Reduce peaks

Time shift

Data source: Robert Sansom, Imperial (2011)

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

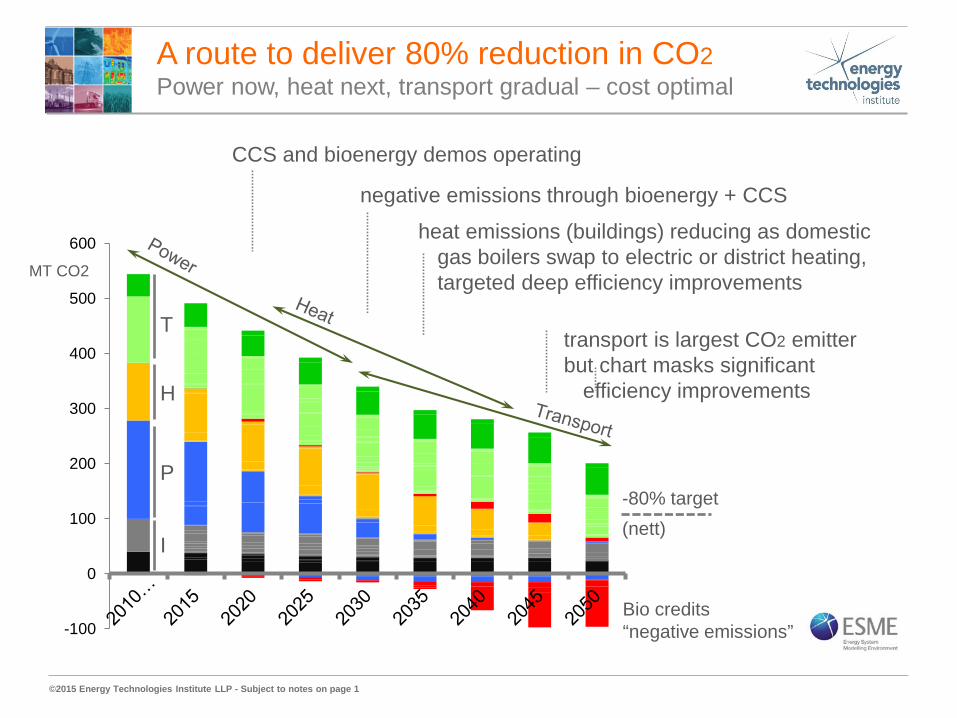

-80% target(nett)

A route to deliver 80% reduction in CO2Power now, heat next, transport gradual – cost optimal

-100

0

100

200

300

400

500

600

transport is largest CO2 emitterbut chart masks significant

efficiency improvements

heat emissions (buildings) reducing as domestic gas boilers swap to electric or district heating, targeted deep efficiency improvements

CCS and bioenergy demos operating

negative emissions through bioenergy + CCS

Bio credits“negative emissions”

P

H

T

MT CO2

I

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

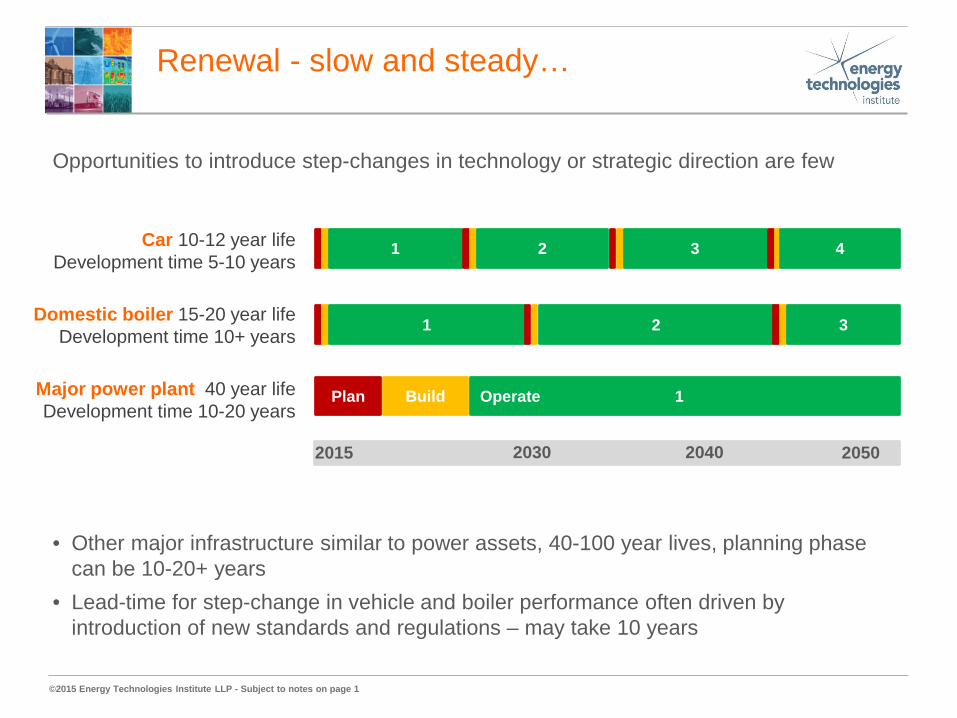

Renewal - slow and steady…

2015 2030 20502040

Plan Build Operate 1Major power plant 40 year lifeDevelopment time 10-20 years

1 2 3Domestic boiler 15-20 year lifeDevelopment time 10+ years

1 2 3 4Car 10-12 year lifeDevelopment time 5-10 years

• Other major infrastructure similar to power assets, 40-100 year lives, planning phase can be 10-20+ years

• Lead-time for step-change in vehicle and boiler performance often driven by introduction of new standards and regulations – may take 10 years

Opportunities to introduce step-changes in technology or strategic direction are few

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

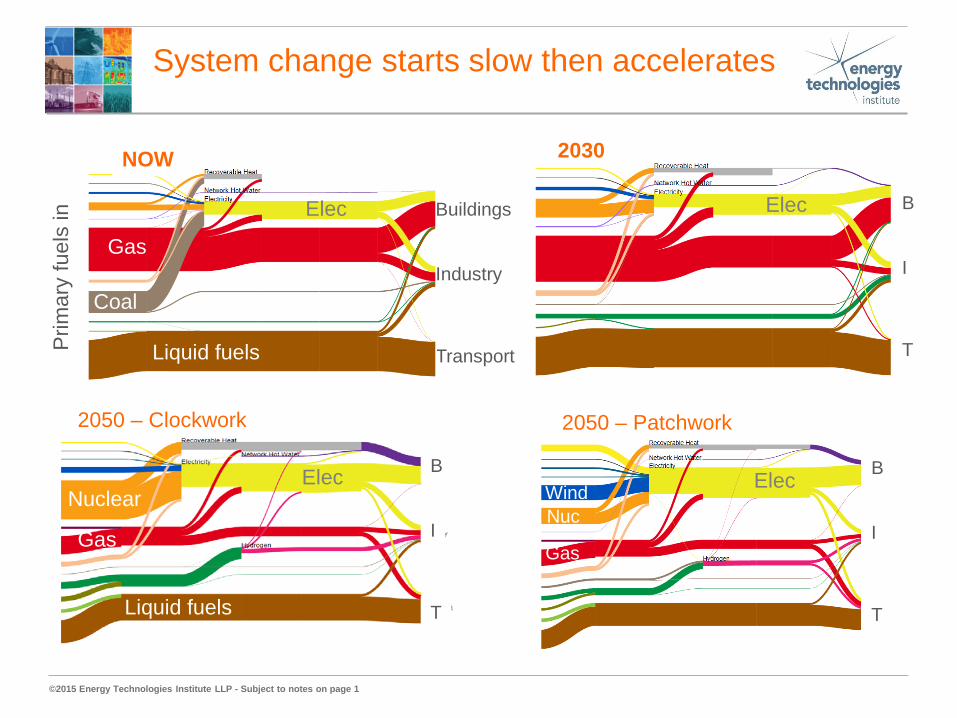

System change starts slow then accelerates

Buildings

Industry

TransportLiquid fuels

Gas

Coal

NOW

Elec

Liquid fuels

Gas

Nuclear

B

I

T

2030

Elec

Prim

ary

fuel

s in

Liquid fuels

Gas

B

I

T

2050 – Clockwork

NuclearElec Elec B

I

T

2050 – Patchwork

Gas

NucWind

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

The next decade is critical in preparing for transition

• The UK transition is affordable (~1% of GDP) and achievable, by developing, commercialising and integrating known - but currently underdeveloped –solutions

• We need to focus deployment on a basket of leading contender technologies – Efficiency of vehicles, efficiency and low carbon heat for buildings, Nuclear, CCS,

Bio, Offshore Wind, Gases (NG, H2, SNG…..)– Develop and prove options, prepare for widescale deployment

• There is enormous potential and value of CCS and bioenergy– The ability (or failure) to deploy these two technologies will have a huge impact on

the cost of achieving the climate change targets and the national architecture of low carbon systems and future infrastructure requirements

• To avoid wasting investment, crucial decisions must be made about the design of the future energy system, driven by choices on infrastructure

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

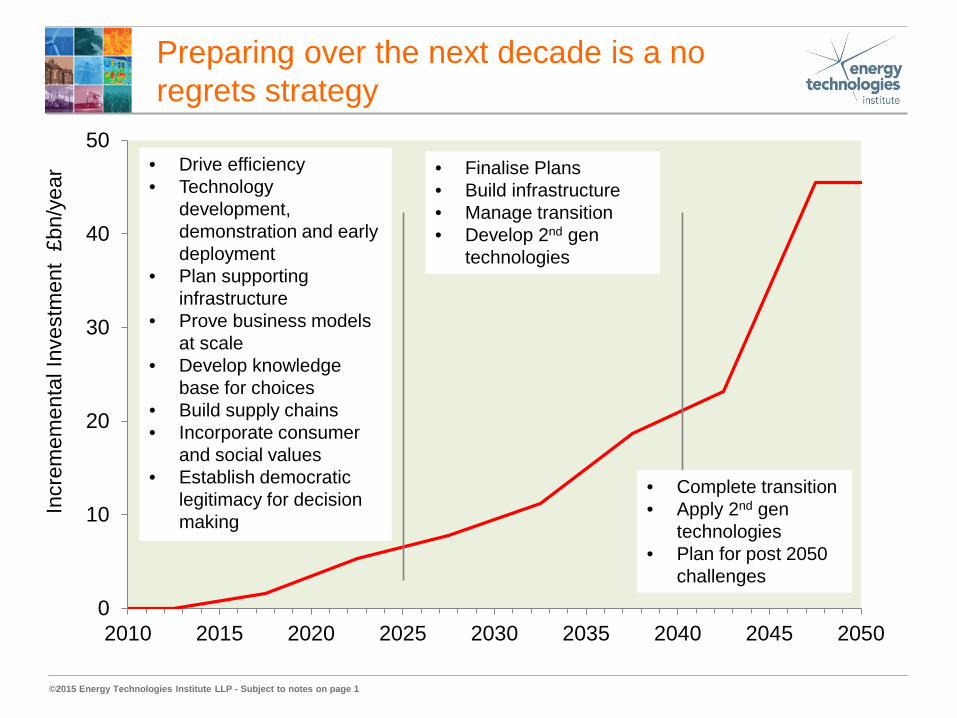

0

10

20

30

40

50

2010 2015 2020 2025 2030 2035 2040 2045 2050

Incr

emem

enta

l Inv

estm

ent

£bn/

year

Preparing over the next decade is a no regrets strategy

• Drive efficiency• Technology

development, demonstration and early deployment

• Plan supporting infrastructure

• Prove business models at scale

• Develop knowledge base for choices

• Build supply chains• Incorporate consumer

and social values• Establish democratic

legitimacy for decision making

• Finalise Plans• Build infrastructure• Manage transition• Develop 2nd gen

technologies

• Complete transition• Apply 2nd gen

technologies• Plan for post 2050

challenges

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

What role for innovation?

• Deploy ‘Known but underdeveloped’ technologies

• Drive down cost, increase performance and integrate into our energy system– Regulate (eg cars)– Market (eg wind turbines)– Target innovation interventions (eg floating wind)– Supply chain & delivery skills (eg heat solutions)

• Business models, policy mechanisms, consumer propositions and community engagement activities

• Silver bullets are rare and unpredictable

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

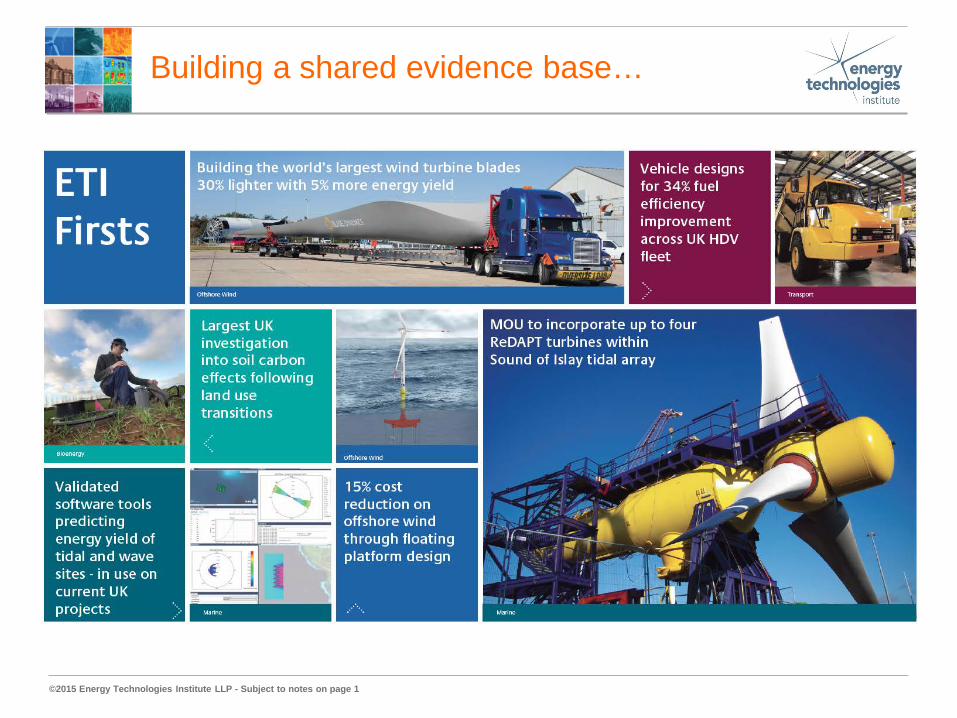

Building a shared evidence base…

©2015 Energy Technologies Institute LLP - Subject to notes on page 1

For more information about the ETI visit www.eti.co.uk

For the latest ETI news and announcements email [email protected]

The ETI can also be followed on Twitter @the_ETI

Registered Office Energy Technologies InstituteHolywell BuildingHolywell ParkLoughboroughLE11 3UZ

For all general enquiries telephone the ETI on 01509 202020.