· · 2015-05-11filing information: april 2010, idc #222605, volume: 1 enterprise servers:...

TRANSCRIPT

Filing Information: April 2010, IDC #222605, Volume: 1Enterprise Servers: Technology Markets: Market Analysis

M A R K E T A N A L Y S I S

W o r l d w i d e a n d R e g i o n a l S e r v e r 2 0 1 0 – 2 0 1 4 F o r e c a s tLloyd Cohen Daniel HarringtonStefania Lorenz Nathaniel MartinezJed Scaramella Mathew EastwoodRajnish Arora Lidice FernandezThomas Meyer Roman MaceškaJason Bremer Giorgio NebuloniHiroyuki-Tsuzuki Juan pablo SeminaraTarun Bhasin Satoshi FukutomiKazuhiko Hayashi

I D C O P I N I O NThe worldwide server market saw a sharp downturn in 2009, as the economic downturn pushed revenue down by double digits compared with CY08 and unit shipments dipped below the 8-million-unit record set in 2008. IDC believes that the server market will see single-digit growth in 2010 and overall stabilization of demand for new servers. And yet, there will be a new "normal" whose shape has not yet been seen. New factors in the mix are increased virtualization of physical servers, more powerful microprocessors, and new types of servers designed to meet new use-case requirements. From a geographic perspective, pockets of faster growth may emerge in some areas of Asia/Pacific in 2010, but most geographic regions will see moderate improvements in revenue and unit shipments compared with 2009. Key highlights:

Currently, the x86 market is driven over volume. Most x86 servers are shipped with two or four sockets as rack optimized or blade servers and are outfitted with quad-core processors. IDC expects a bifurcation of the volume-driven x86 market, with microservers at the low end and scalable and multicore servers at the high end. Over the long term, IDC sees the x86 market being pulled in two directions.

Worldwide customer revenue declined 3.9% year over year to $13.8 billion in the fourth quarter of 2009. This is the sixth consecutive quarter of year-over-year revenue decline, but the percentage decline was relatively quite small this quarter. Sequentially, customer revenue grew 24.0%. This increase was driven by growth in mostly by strong growth in the United States (24.0%) and in Western Europe (32.0%). Combined, these two geographic regions account for 60.1% of the server customer revenue.

IDC expects a recovery to take place in 2010 as IT budgets begin to free up, and aging systems are retired and replaced with more powerful and cost-efficient servers. The long-term forecast for the worldwide market has been increased in 2013 by 317,515 units and $2.4 billion from the previous forecast. This new IDC forecast is extended now to include 2014.

Glo

bal H

eadq

uart

ers:

5 S

peen

Str

eet

Fram

ingh

am, M

A 0

1701

USA

P

.508

.872

.820

0

F.50

8.93

5.40

15

ww

w.id

c.co

m

#222605 ©2010 IDC

T A B L E O F C O N T E N T S

P

In This Study 1

Methodology ............................................................................................................................................. 1

Situat ion Overview 12

Future Out look 14

Forecast and Assumptions ....................................................................................................................... 14Market Context ......................................................................................................................................... 135

Essential Guidance 139

Learn More 140

Related Research..................................................................................................................................... 140Methodology ............................................................................................................................................. 141

©2010 IDC #222605

L I S T O F T A B L E S

P

1 Worldwide Server Customer Revenue by Operating System, 2008–2014................................... 15

2 Worldwide Server Shipments by Operating System, 2008–2014................................................. 16

3 Americas Server Customer Revenue by Operating System, 2008–2014..................................... 17

4 Americas Server Shipments by Operating System, 2008–2014................................................... 18

5 EMEA Server Customer Revenue by Operating System, 2008–2014 ......................................... 19

6 EMEA Server Shipments by Operating System, 2008–2014 ....................................................... 20

7 Asia/Pacific Server Customer Revenue by Operating System, 2008–2014 ................................. 21

8 Asia/Pacific Server Shipments by Operating System, 2008–2014 ............................................... 22

9 Worldwide Server Customer Revenue by Chip and Operating System, 2008–2014.................... 23

10 Worldwide Server Shipments by Chip and Operating System, 2008–2014 ................................. 24

11 Americas Server Customer Revenue by Chip and Operating System, 2008–2014 ..................... 26

12 Americas Server Shipments by Chip and Operating System, 2008–2014 ................................... 27

13 EMEA Server Customer Revenue by Chip and Operating System, 2008–2014 .......................... 29

14 EMEA Server Shipments by Chip and Operating System, 2008–2014 ........................................ 30

15 Asia/Pacific Server Customer Revenue by Chip and Operating System, 2008–2014.................. 32

16 Asia/Pacific Server Shipments by Chip and Operating System, 2008–2014................................ 33

17 Worldwide Server Customer Revenue by Price Band, 2008–2014 .............................................. 35

18 Worldwide Server Shipments by Price Band, 2008–2014............................................................ 36

19 Americas Server Customer Revenue by Price Band, 2008–2014................................................ 37

20 Americas Server Shipments by Price Band, 2008–2014.............................................................. 38

21 EMEA Server Customer Revenue by Price Band, 2008–2014..................................................... 39

22 EMEA Server Shipments by Price Band, 2008–2014 .................................................................. 40

23 Asia/Pacific Server Customer Revenue by Price Band, 2008–2014 ............................................ 41

24 Asia/Pacific Server Shipments by Price Band, 2008–2014 .......................................................... 42

25 Worldwide Server Customer Revenue by Operating System and IDC Class, 2008–2014........... 43

26 Worldwide Server Shipments by Operating System and IDC Class, 2008–2014......................... 45

27 Americas Server Customer Revenue by Operating System and IDC Class, 2008–2014............. 47

28 Americas Server Shipments by Operating System and IDC Class, 2008–2014........................... 49

29 EMEA Server Customer Revenue by Operating System and IDC Class, 2008–2014 ................. 51

30 EMEA Server Shipments by Operating System and IDC Class, 2008–2014 ............................... 53

31 Asia/Pacific Server Customer Revenue by Operating System and IDC Class, 2008–2014 ......... 54

32 Asia/Pacific Server Shipments by Operating System and IDC Class, 2008–2014 ....................... 56

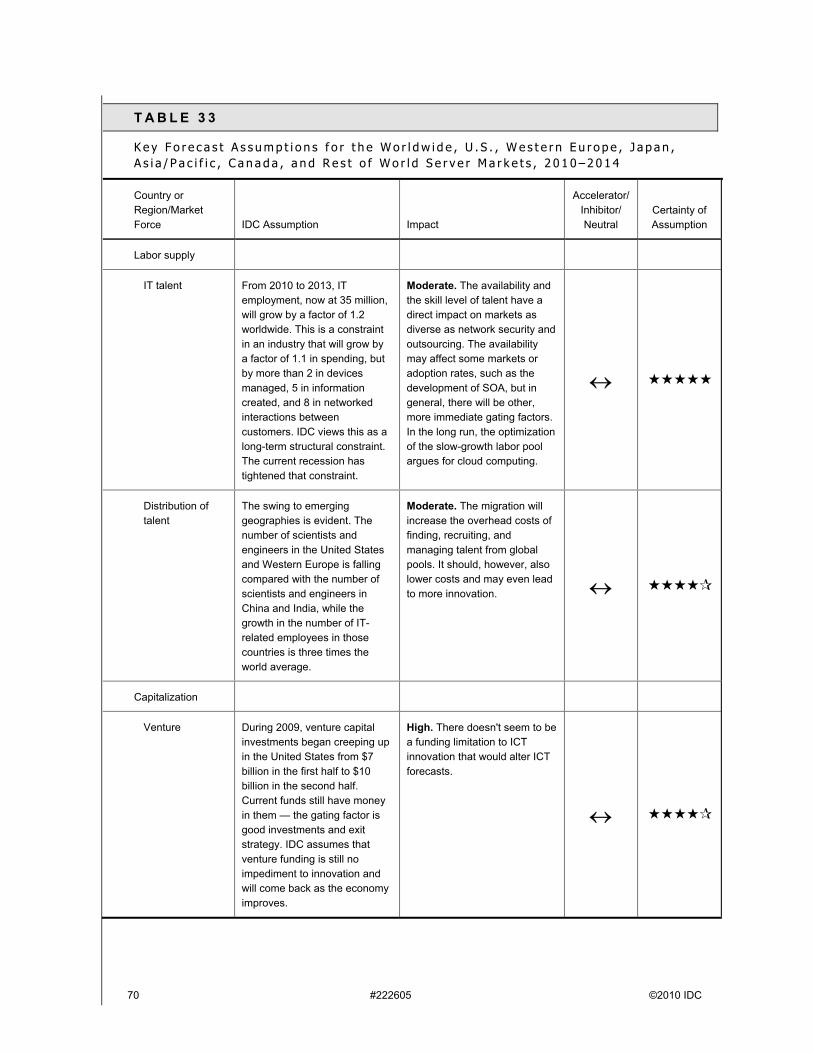

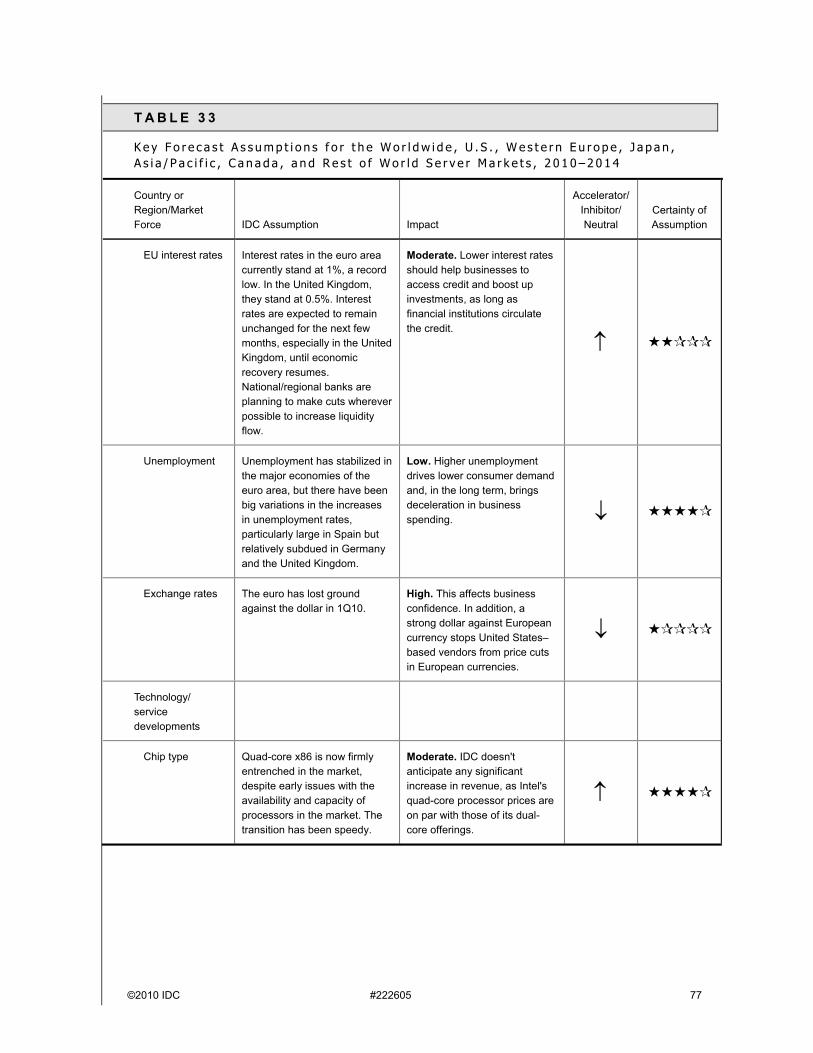

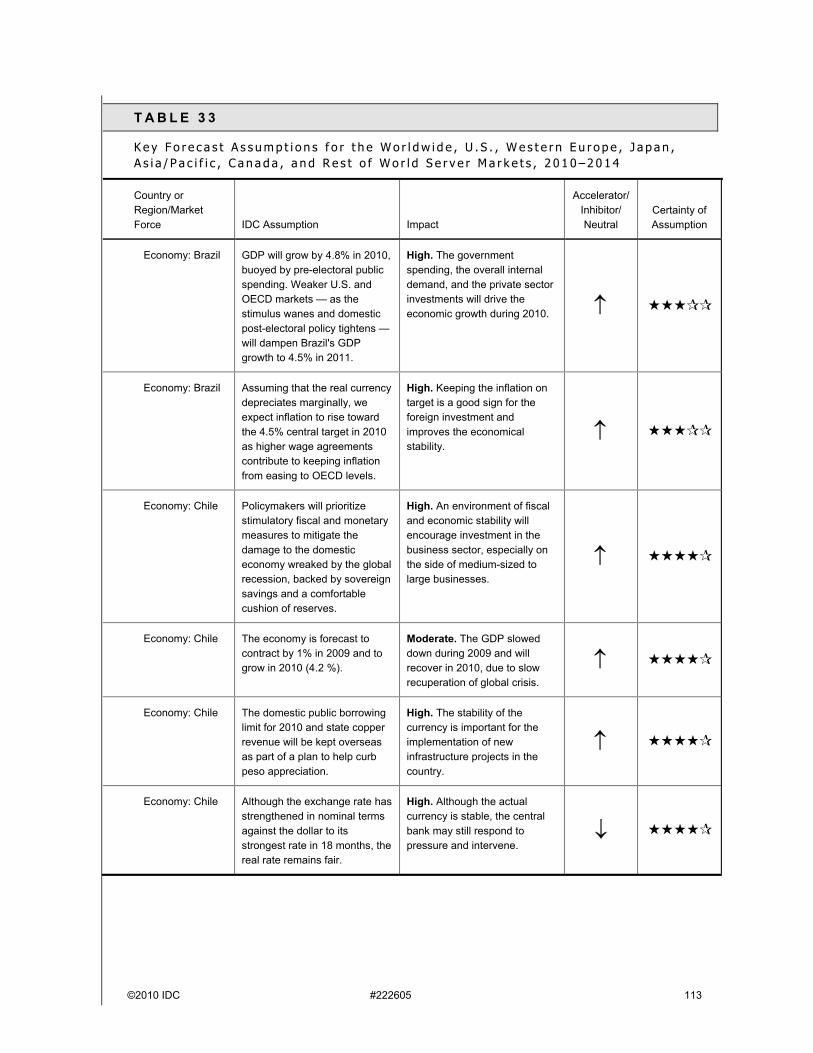

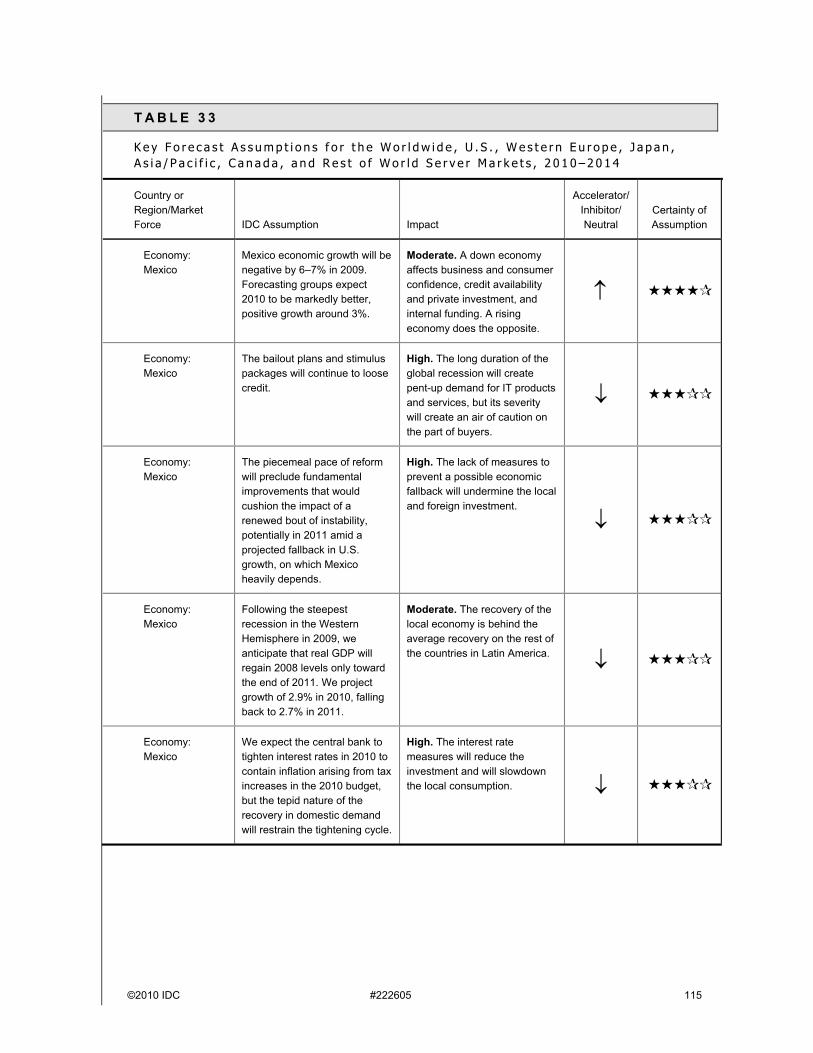

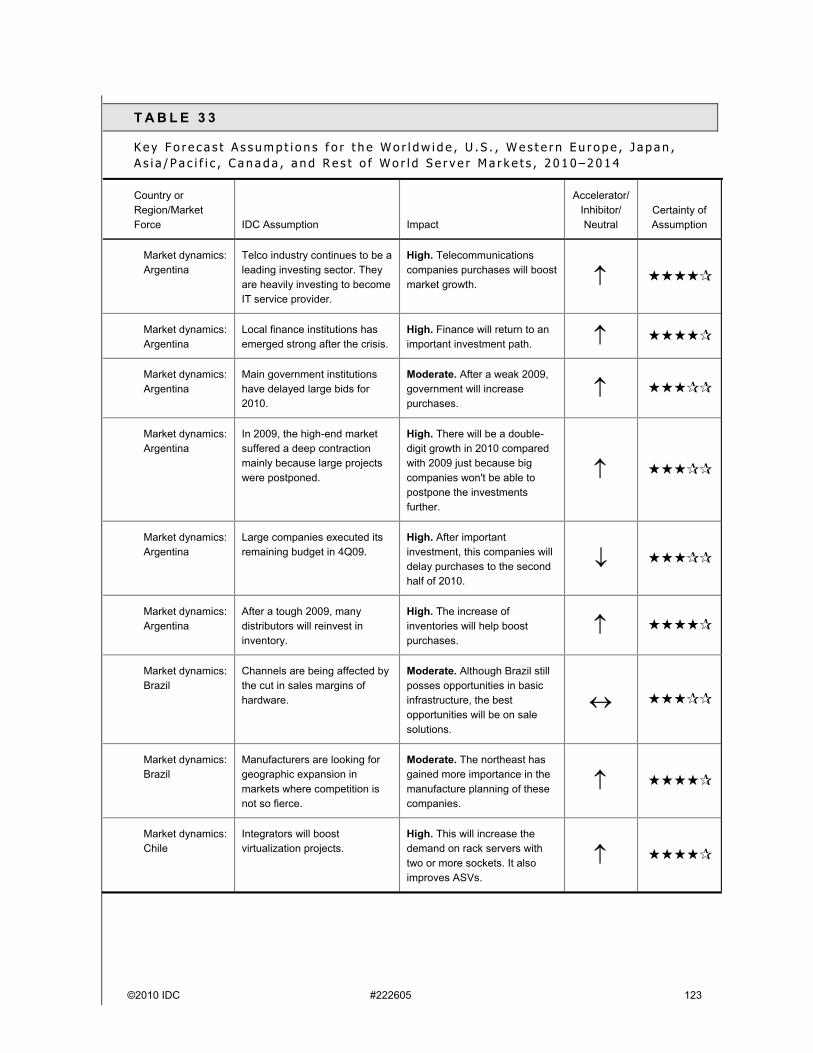

33 Key Forecast Assumptions for the Worldwide, U.S., Western Europe, Japan, Asia/Pacific, Canada, and Rest of World Server Markets, 2010–2014............................................................. 59

34 Worldwide Server Customer Revenue by Region 2007–2014: Comparison of December 2009 and March 2010 Forecasts.................................................................................................. 136

#222605 ©2010 IDC

L I S T O F T A B L E S — C o n t i n u e d

P

35 Worldwide Server Shipments by Region, 2007–2014: Comparison of December 2009 and March 2010 Forecasts ................................................................................................................. 137

36 Exchange Rates, 2003–2009 ....................................................................................................... 142

©2010 IDC #222605

L I S T O F F I G U R E S

P

1 Worldwide Server Customer Revenue by Chip Technology, 2002–2014..................................... 57

2 Worldwide Server Customer Revenue by Operating System, 2002–2014................................... 58

3 Worldwide Server Customer Revenue, 2005–2013: Comparison of December 2009 and March 2010 Forecasts ................................................................................................................. 138

4 Worldwide Server Shipments, 2005–2013: Comparison of December 2009 and March 2010 Forecasts ..................................................................................................................................... 139

©2010 IDC #222605 1

I N T H I S S T U D Y

This study presents clients of IDC's Enterprise Servers Technology: Markets service with the foundation of market and technology assumptions that our regional analysts used to generate our current expectations for server market growth and directions. In a market as broad and complex as the enterprise server market, not all assumptions that lead to specific technology or product segment growth predictions can be listed in a concise document. Nevertheless, this document is intended to provide clients with some of the fundamental drivers for the server market course. IDC clients are encouraged to contact our worldwide or regional analysts if they have specific inquiries regarding our forecasts to get more detail on specific category or segment trends.

M e t h o d o l o g y

Server Taxonomy

IDC categorizes servers into two main groups:

Servers. This category comprises all server hardware sales for all purposes, applications, and industries, including volume, midrange enterprise, and high-end enterprise servers; server blades; and technical servers. Primary server segmentations are based on server class/price band, chip type, and operating system (OS).

Technical servers. Technical servers (also referred to as high-performance computers [HPCs]) represent a specialized view of the server market. Technical servers are designed, sold, and used to support scientific research, engineering development, and other numerically intensive applications (i.e., technical computing) in government, industry, and academia. Technical computing segmentations are based on a number of parameters (i.e., price bands, architectures, and application workloads).

A typical server configuration consists of processors, memory, disk storage, and any bundled operating system, database, and networking software. IDC defines a server as having two primary characteristics:

Multiuser device. A server is a computer device that accesses services via the network. Servers and the applications that run on them are typically shared by multiple users.

No user interface. Unlike a client device, a server does not have a user interface that is intended for human-machine interaction.

Servers

S e r v e r M a r k e t S e g m e n t a t i o n

IDC's server market definitions and taxonomy include the following server segmentations:

2 #222605 ©2010 IDC

Server type. IDC categorizes all server hardware as x86 or non-x86. The x86 servers are Intel- or AMD-based instruction set of architecture, while non-x86 include all CISC, RISC, and EPIC servers. Following the increasing use of x86 servers, IDC further segments the market by end-user segments and channels.

Central processing unit (CPU) type. To account for products that represent 64-bit extensions to existing 32-bit processor technology, IDC utilizes a CPU-type category. IDC illustrates processor product families (such as SPARC, Pentium, and PowerPC) as a subcategory in our research taxonomy.

Server class/price band. To represent the reality of price erosion among server systems and the increased capabilities of servers with lower price points, IDC has redefined the categories that represent the volume server market and midrange and high-end enterprise servers.

The server market is further segmented by operating system and geographic region. In addition, following is a discussion on how IDC currently addresses the multicore and multithreaded server environment. This is followed by general market definitions and IDC's methodology for server blades.

C P U T y p e

IDC categorizes the server market according to the design of the CPU and the software programming model. The actual metadata (i.e., data about data) for CPU designs is CISC, RISC, EPIC (the Itanium-based 64-bit Intel architecture), and x86 (the current Intel architecture CISC design, which includes AMD's Athlon and Opteron):

Complex instruction set computer (CISC). This design is the traditional type of computer processor. CISCs have large instruction sets with simple and complex instructions of variable lengths. Although x86 chip types (such as those produced by Intel and AMD) are CISC processor designs, they are separated into their own chip-type categories because of their high volume. In IDC's server taxonomy, CISC-based systems refer to proprietary systems, such as those produced by IBM for its zSeries servers.

Reduced instruction set computer (RISC). This processor design is produced by IBM, HP, Sun Microsystems, and others. RISCs have smaller instruction sets, and each instruction is usually of limited function with fixed-length formats. RISC servers typically support Unix and other (e.g., NonStop) platform software. Sun's SPARC, HP's PA-RISC, and IBM's POWER processors are all examples of RISC architecture.

Explicitly Parallel Instruction Computing (EPIC). This processor design is produced by Intel and represents its 64-bit Itanium processor family (codeveloped by Intel and HP). Several server OEMs have products that utilize the 64-bit Itanium processor.

©2010 IDC #222605 3

x86. What was once referred to as the Standard Intel Architecture Server (SIAS) market will now encompass all x86(32)- and x86(64)-based systems and will be referred to as the x86 server market in IDC publications and databases. The x86 server market includes all systems that fit IDC chip-type definitions, regardless of form factor (such as blades) and price band or CPU capacity (i.e., systems with price points above $25,000 and/or containing more than eight processors will still be in the x86 server category as long as they meet chip-type definitions):

x86(64). This processor design refers to x86 architecture systems that have 64-bit extensions. x86(64) processor designs enable 64-bit computing while remaining compatible with existing x86 software infrastructure. AMD's Opteron processor and Intel's EM64T are examples of x86(64) processors.

x86(32). x86(32) refers to volume 32-bit CISC processors developed and produced by companies such as Intel and AMD. Intel's Pentium and XEON processor families and AMD's Athlon processors are examples of this architecture. x86(32)-based systems run Microsoft Windows, Novell NetWare, Linux, Unix, and other operating system environments.

S e r v e r C l a s s / P r i c e B a n d

IDC has reclassified and made adjustments to the price bands that fall into the various size classed this year. IDC's server class taxonomy segments the server market into three server classes: the volume server market (consisting of all systems with an average selling value [ASV] below $25,000), the midrange enterprise server market (consisting of all systems with an ASV from $25,000 to $249,999), and the high-end enterprise server market (consisting of all systems with an ASV of $250,000 and above).

The midrange enterprise and high-end enterprise markets will be referred to collectively as the enterprise server market. IDC's 23 price bands will remain unchanged from our historical taxonomy to provide clients with a seamless transition to the new terminology. Therefore, the price bands included in the three new server classes are as follows:

Volume server market:

Price band 1: $0–499 ASV

Price band 2: $500–999 ASV

Price band 3: $1,000–1,499 ASV

Price band 4: $1,500–1,999 ASV

Price band 5: $2,000–2,499 ASV

Price band 6: $2,500–2,999 ASV

Price band 7: $3,000–3,999 ASV

4 #222605 ©2010 IDC

Price band 8: $4,000–4,999 ASV

Price band 9: $5,000–5,999 ASV

Price band 10: $6,000–6,999 ASV

Price band 11: $7,000–7,999 ASV

Price band 12: $8,000–8,999 ASV

Price band 13: $9,000–9,999 ASV

Price band 14: $10,000–14,999 ASV

Price band 15: $15,000–19,999 ASV

Price band 16: $20,000–24,999 ASV

Midrange enterprise server market:

Price band 17: $25,000–49,999 ASV

Price band 18: $50,000–99,999 ASV

Price band 19: $100,000–249,999 ASV

High-end enterprise server market:

Price band 20: $250,000–499,999 ASV

Price band 21: $500,000–999,999 ASV

Price band 22: $1 million to $2.99 million ASV

Price band 23: $3+ million ASV

O p e r a t i n g S y s t e m

IDC assumes that all servers are shipped with an operating system. A portion of the operating system license fee that is shipped with the server is included in the factory-revenue figures. This operating system portion ranges from 5% to 20% of the average selling value, depending on the type of system; it is associated only with new operating systems' licenses and not with installed base licenses.

According to our current methodology, primary operating systems and operating systems that run within a partition of a scalable system are not currently counted. Only the primary, or booting, operating system is identified in our server data. IDC continues to use its knowledge of system software environments as a key factor in developing these hardware forecasts. The following operating systems are covered:

Novell NetWare

Windows

©2010 IDC #222605 5

Unix

Linux

i5/OS

z/OS

Other

M u l t i c o r e a n d M u l t i t h r e a d S e r v e r S y s t e m s

Several chip makers are looking to dual-core designs as a way to increase the performance of next-generation processors without the constraints imposed by rising levels of power consumption in single-core processors. Two common methods of improving the performance of a single-core chip are increasing clock speed or adding cache memory, both of which require more power.

A dual-core chip is two separate processors on a single chip. These two processors can often outperform single-core processors on most multithreaded applications while running at lower clock speeds and consuming less power.

An application with multiple software threads will run faster on a dual-core processor because the operating system can assign an individual thread to its own processor core. Multithreaded applications running on a single-core processor must wait for one thread to finish before another thread can be processed.

Servers with chip architectures that expand on their processing capabilities based on the number of processor sockets are tracked in IDC's server taxonomy using the number of processor sockets as the cornerstone. In addition, the number of processing cores that are on the socket will be equally important. Finally, the product of the number of sockets and cores will represent the new server capability. IDC will eventually add two new fields (socket count and core count) into its tracker and forecast products to count the cores and sockets. The server capability will be used to forecast the size of the future server market, while market segmentation can be performed using the socket count and core count fields.

To this end, the following are examples of how IDC will interpret the new server and chip platforms:

The number of processor sockets within a server will be used to determine the n-way factor of that server. For example, a server with one processor socket will be classified as a 1-way server, and a server with two processor sockets will be a 2-way server.

A single socket may have one or more cores on that socket. It may have two or more physical cores on its socket. For example, a server with a single socket and dual cores (two processors) will have its socket count at 1, core count at 2, and server capability set to 2.

IDC will not define the type of server (i.e., n-way) by the number of threads that are used in the server packaging to assist performance or throughput.

6 #222605 ©2010 IDC

IDC believes that IT executives will continue to view the size of the server based on the number of processor sockets and therefore exert pressure on the independent software vendors (ISVs) to price accordingly.

Multicore, multithread, and socket layouts are designed to improve the overall performance and throughput of the system. IDC believes this will allow system vendors to differentiate themselves from their competitors in the volume server market via the benchmarking and workload processing capabilities.

O t h e r S e r v e r D e f i n i t i o n s

The following are definitions of terms and methodology approaches used in IDC's ongoing research process:

Average selling value. ASV is the value of an initial server shipment (ISS) unit configured as it is typically sold. The ASV will include the base configuration plus any add-ons or upgrades typically sold when the system or server is first delivered to a customer. It can be stated at both factory- and customer-installed levels.

Customer revenue. Customer revenue represents the amount of money paid by end users for products. IDC uses customer revenue to illustrate its server forecasts because many of its clients find spending to be a more useful concept than vendor revenue in market plans. Customer, or end-user, revenue (spending) represents those dollars ultimately spent by the end customer for the following embedded server components:

Frame or cabinet and all cables

Processors

Memory

Storage

Communications boards

Operating system software

Other bundled software

Initial internal and external disk shipments, either from the manufacturer or from the channel

To a large degree, most of the aforementioned components are sold today as a server bundle, with the possible exception of the OS software. IDC's revenue figures are based on street (i.e., realistic) pricing for the average model as it is assembled when the user plugs it in. OS software is included only when it is bundled with the server sale and when it represents the base number of users supported by that initial license.

©2010 IDC #222605 7

IDC does not explicitly attempt to uplift server ASVs to accommodate an additional number of users. No other peripherals (e.g., printers and modems), except initial disk shipments, are included in our revenue data.

Direct shipment. A direct shipment is any unit sold from a system vendor's own sales force or through direct Internet sales to the end customer. Server vendors realize all revenue from these sales.

Factory revenue. Factory revenue represents the amount of money recognized by the vendor for the sale of products. Factory revenue represents those dollars recognized by multiuser system and server vendors for ISS and upgrade units sold through direct and indirect channels. In IDC's server research, factory revenue refers to the sums associated with server hardware. Factory revenue is used by IDC to calculate vendor market shares because it excludes channel margin and channel-added peripherals that are not part of a vendor's own finances.

High-end enterprise server. High-end enterprise server markets consist of all systems with an average selling value of $250,000 and above.

Installed base. Installed base is composite shipments and ISS shipments plus upgrades minus retirements. If a vendor was acquired in 1999, the total installed base is credited to the new vendor regardless of which quarter the acquisition took place in. In this document, the customer price band is set annually, not quarterly, and as a result, shipments by price band and installed base by price band will not always match up.

Note: If a vendor was acquired during the year, all of the vendor's shipments and installed base were credited to the new vendor. Sequent is listed under IBM; Digital and Compaq are listed under HP; Fujitsu Siemens is listed under Fujitsu; NEC CI, NEC, and NEC/Groupe Bull are listed under NEC.

Installed price. Installed price equals worldwide ISS customer revenue divided by ISS units.

Initial server shipment. ISS characterizes the first sale of a server (previously referred to as a "new footprint"). An ISS server unit consists of processors, memory, disk storage, and any bundled operating system, database, and networking software that would typically be configured when it leaves the OEM's factory floor. Guidance for these average configurations is normally received from server vendors. For this study only, if a vendor was acquired in 1999, ISS shipments are credited to the new vendor regardless of which quarter the acquisition took place in. ISS prices are net prices, meaning that IDC subtracts the value of a trade-in server from the price for a new system. The use of net pricing was necessitated by the data-reporting abilities of server vendors. Much of the guidance that we receive does not account for trade-ins and discounting.

List price. This is the non-discounted direct price for a server model. List prices are typically found in vendor pricing books.

8 #222605 ©2010 IDC

Midrange enterprise server. Midrange enterprise server markets consist of all systems with an average selling value of $25,000–249,999.

Price band. A price band is a range of server values with an upper and lower bound. It is based on the end-user price of a server. Typically, the lower bound will be the round number and the upper bound will end with a 9. We have defined the following 23 distinct bands for dividing our market shares and platform forecasts:

Price band 1: $0–499 (volume server)

Price band 2: $500–999 (volume server)

Price band 3: $1,000–1,499 (volume server)

Price band 4: $1,500–1,999 (volume server)

Price band 5: $2,000–2,499 (volume server)

Price band 6: $2,500–2,999 (volume server)

Price band 7: $3,000–3,999 (volume server)

Price band 8: $4,000–4,999 (volume server)

Price band 9: $5,000–5,999 (volume server)

Price band 10: $6,000–6,999 (volume server)

Price band 11: $7,000–7,999 (volume server)

Price band 12: $8,000–8,999 (volume server)

Price band 13: $9,000–9,999 (volume server)

Price band 14: $10,000–14,999 (volume server)

Price band 15: $15,000–19,999 (volume server)

Price band 16: $20,000–24,999 (volume server)

Price band 17: $25,000–49,999 (midrange enterprise server)

Price band 18: $50,000–99,999 (midrange enterprise server)

Price band 19: $100,000–249,999 (midrange enterprise server)

Price band 20: $250,000–499,999 (high-end enterprise server)

Price band 21: $500,000–999,999 (high-end enterprise server)

Price band 22: $1 million to $2.99 million (high-end enterprise server)

©2010 IDC #222605 9

Price band 23: $3+ million (high-end enterprise server)

Processor designs. IDC categorized the server market according to the design of the chip and the software programming model. The actual metadata — data about data — for chip designs is CISC, RISC, x86(32), x86(64) (the current AMD and Intel architecture CISC design), and EPIC (the Itanium-based 64-bit Intel architecture).

Rackmounted server. Rackmounted servers are those that are specifically designed to fit into 19in. racks. They have been used for a number of products in industries such as manufacturing, telecommunications, and defense. They are growing in importance for servers, allowing multiple machines to be clustered (or at least managed) in a single location. The height of rackmounted servers is measured in the number of standard rack units and expressed as 1U, 2U, and so on. Often, rackmounted servers include only limited amounts of disk capacity; additional storage is frequently provided in other rack units. Non-rack-optimized servers, on the other hand, are servers expressed as zero rack units. Rack-optimized, non-rack-optimized, and blade server categories are reported under the "rack factor" field in the tracker.

Rackable servers. Since the second half of 2009, IDC also tracks with more granularity all models that can, but not necessarily will, be used within a 19in. rack, and they include rack-optimized models, as well as some non-rack-optimized models, that nevertheless allow users to store them in a rack in horizontal position. Within the "form factor" field, IDC will thus report the category "rackable," as opposed to "tower" and "blade," to define all servers that can potentially be stored in a rack, even if they are not specifically designed to do so. This additional field does not influence the "rack factor" field, as defined previously.

Revenue. IDC's server research includes the amount recognized by the hardware vendor (the factory revenue items), the channel margin (when a product is sold through a third-party sales organization), and any peripherals added to a system in the channel before shipping to end users that do not originate with the named server hardware manufacturer. IDC presents data in factory revenue to determine market share position. IDC also presents data in customer or end-user spending revenue to better represent the total amount of spending in the server market for forecasting purposes.

The formula for calculating revenue is as follows:

Factory revenue = ISS revenue + upgrade revenue

Customer revenue (i.e., end-user spending) = factory revenue + channel revenue

10 #222605 ©2010 IDC

Server blades. To provide clients with a clear definition of server blades — and to permit a framework for following the modular computing market as it evolves — IDC has further defined the server blade segment. IDC began to track a new form factor, server blades, beginning in 1Q02. The definition of a server blade is as follows: A server blade is an inclusive computing system that includes processor, memory, network connections, and associated electronics on a single motherboard. The server blade is also known as a single-board computer and is typically associated with an enclosure system that allows multiple blades to be housed in a standard server "chassis" or enclosure that shares resources such as power supplies and cooling fans. Blades are easily accessible, are typically found in a sub-U form factor, and may be associated with content blades and network blades that contain the storage capacity and networking capabilities, respectively. The server blade architecture is designed primarily for computing density, along with a universal modular architecture that ensures flexibility and scalability, as well as easier deployment and manageability.

For the purposes of IDC market sizing and forecasting, we currently count each blade as a server unit, with multiple blades or units in a single chassis. The cost of the chassis, as well as network and storage blades in the chassis, will be distributed across the average number of server blades in a chassis to calculate the average selling value of a server blade.

Therefore, the average selling value of a server blade will be calculated as follows: cost of individual blade + (cost of chassis [including power supplies and other shared subsystems] + cost of network blades + cost of storage blades)/average number of blades in a chassis.

Today, the prevailing line of thought in the industry is that a server blade or a "modular server" is a server in its own right and competes directly with rack-optimized server products for market share (i.e., largely, the industry views the server blade as a unit). The disaggregation of servers into processing, I/O, and storage modules, however, may mean that we will view a server "unit" as something very different in the near future. A "server" may be a number of processor, I/O, and storage modules sharing multiple chassis that together deliver a service to an application or a business unit. This is largely the view the industry takes with large service provider (SP) RISC-based Unix servers and modular midrange and high-end systems in the market today. IBM's x440 eServer is an example of a system that straddles these competing views of what a server unit is. Is the x440 one 16-way system built upon four 4-way nodes, or is it four 4-way blades that fit within two to three processor and I/O chassis?

IDC recognizes this inconsistency in our definition of a server unit. Indeed, as the hardware infrastructure becomes even more virtual and modular, this inconsistency may become unsustainable. Currently, however, the industry as a whole views server blades very differently from large symmetric multiprocessing (SMP) systems built using modular building block processor and I/O nodes —even though, increasingly, the definition of what separates server blades from large SMP nodes is becoming very blurred.

©2010 IDC #222605 11

For this reason, in addition to server blades, IDC will track shipments of server blade chassis, I/O blades, and storage blades in the server market. If the disaggregation of server resources and the virtualization of services deployed on server hardware continue, IDC will be prepared to view and account for market dynamics accordingly.

Unit. Unit shipment figures represent the number of products of a given type delivered to customers within a specific period. In IDC's server data, we differentiate between an ISS and an upgrade shipment. The former represents the delivery of a new server, while the latter involves the upgrading of the processor through either replacement or addition of extra CPUs.

Upgrade. An upgrade is the opposite of an ISS, but not all equipment additions qualify as upgrades. IDC recognizes a server upgrade unit only if it results in a model name or number change to an installed ISS unit. Server upgrades normally entail the addition of another processor to an SMP unit through a board addition or swap. Along with the processor, more memory is typically added, and possibly more disk storage. In most cases, upgrades don't change the serial number of the system unit. For this document only, if a vendor was acquired in 1999, upgrade shipments are credited to the new vendor regardless of which quarter the acquisition took place in.

Volume server. Volume servers consist of all systems with an average selling value below $25,000.

White-box server. A white-box server is primarily assembled by resellers. The following are attributes of typical white boxes:

No global or nationwide presence

Rebranded, assembled products/supplies

Lack of branded support products

Server revenue of less than $50 million

Products valued under $25,000

12 #222605 ©2010 IDC

S I T U A T I O N O V E R V I E W

IDC's forecast for the server market was slightly adjusted upward from the previously published forecast in Worldwide and Regional Server 2009–2013 Forecast Update(IDC #221439, December 2009). The significant global recession caused massive volatility to the hardware market throughout the end of 2008 and during 2009. IDC sees a return to normalcy in seasonal patterns toward the end of 2010. The expectation for worldwide spending on server customer revenue in 2010 year-on-year change is positive, 6.8%, to $49.3 billion. IDC expects the volume server segment to continue to be the driver of growth through the forecast period fuelled by rackable servers. IDC had anticipated a "U" type of recession, but results in 3Q09 suggest it may be more of a "V" shape, and data from 4Q09 shows as starting up on the right side of the "V".IDC expects the market in the first quarter of 2010 to be seasonably down compared with 4Q09, but less than one would normally expect with customer revenue in totaling $12.0 billion with 1,770,720 units.

Shipments in the x86 market invariably drive the server market growth or decline as the market controlled 96.3% of the server market in 2009. In 4Q09, the x86 market grew 14.9% sequentially in terms of units and 24.0% in revenue. Average selling prices remained above $7,000 overall but are expected to slightly decline over the forecast period. IDC believes it is prudent to look at sequential results more closely throughout 2010 as we come out of the recession rather than just looking at year-over-year results. One should not simply assume quarterly results are a result of seasonality.

As forecast previously, IDC expected growth in the x86 segment in all geographic regions and this did come to fruition. All regions experienced strong double-digit growth, except Japan which had a sequential unit shipment increase of 2.4%. Year-over-year results for the x86 segment in 4Q09 show that units increased 3.8%, while revenue was up an impressive 12.4%.

Worldwide competition remains strong, yet average x86 server prices continue to increase year over year and the average system price increased 8.2% to $4,233 while sequentially they grew 4.8%. One-socket systems lost a small amount of share worldwide, as the more popular two-socket configurations gained in popularity. x86 blades continue to control a fair share of the server market and are forecast to grow as a percentage of the total server market. The converged nature of the blade platform and the high rate of virtualization on blade servers are two key drivers of theblade market. Given the increased pressure on IT budgets, IT organizations are leveraging the operational benefits of the blade platform. IDC's analysis, coupled with end-user research, indicates that migrating from a complex, heterogeneous legacy server environment to a managed blade environment wil l optimize the IT infrastructure by reducing IT costs while developing a more flexible and agile infrastructure to support business opportunities.

©2010 IDC #222605 13

In 3Q09, IDC changed the size class definitions to reflect changing market dynamics. Entry-level systems are still priced less than $25,000. Midrange enterprise servers are now reclassified to include systems priced at $25,000 to less than $500,000 and high-end enterprise systems are classified as being priced at greater than $500,000. Readers are cautioned in making comparisons with previously published documents that have size class data comparisons.

Worldwide spending for midrange enterprise servers declined in 4Q09, dropping 5.1% to $2.1 billion in year-over-year comparisons. However, sequentially, spending increased 41.9%. With the new size class price bands, IDC now expects spending in the midrange enterprise segment to grow at a 6.7% CAGR through 2014 to about $9.2 billion.

Spending for high-end enterprise servers continues to decline as users continue to migrate to lower-cost modular systems. Year over year, the high-end enterprise segment fell 21.1% in terms of customer revenue but improved -12.1% sequentially. This represented a disappointing fourth-quarter year-end for IBM which usually relies on strong results for its high-end devices. We believe the longer-term trend will show a slow but steady decline in high-end enterprise spending as customers move select workloads to smaller form factors. This is one of the reasons the midrange enterprise segment will see a small compound growth increase. The forecast for high-end enterprise server spending is expected to decline at a 5.6% CAGR from $13.2 billion in 2009 to $9.9 billion in 2014.

Tables 1–32 present regional forecast information from 2008 to 2014.

14 #222605 ©2010 IDC

F U T U R E O U T L O O K

F o r e c a s t a n d A s s u m p t i o n s

IDC is forecasting the worldwide server market to increase over the forecast horizon with revenue of $52.6 billion by 2014, which represents a five-year CAGR of 2.6%. Just as there was a wave with the recession starting in the United states and then moving over seas, the recovery is expected to have a similar trend across the globe with all regions feeling some level of economic recovery. The United States has begun to show some signs of improvement with the compound growth rate between 2009 and 2014 to be 2.6%. Western Europe, on the other hand, has been hard hit by the recession and will be slower to recover. IDC is forecasting Western Europe to have a -2.8% compound growth decline over the five-year forecast period. Even though the international markets will be slower to recover, there could still be pockets of positive server hardware spending in the short term for individual technologies or countries where the necessity to build out infrastructure has either been underway or where financial commitments to the incoming capacity is under contract. This is especially true in areas, such as India and China, which are major factors toward APEJ growth. As pointed out in the Market Context section of this document, year-over-year comparisons suggest the server market is worse off than it really was, and readers should pay closer attention to sequential results.

While the severity of this crisis has thrown the world economy into uncharted waters, IDC does see light at the end of the tunnel and expects to see more predictability in results over the forecast period.

We still believe the decision-making process for purchasing server hardware will be driven by many of the same underlying elements that we have identified in the past. Therefore, IDC expects customer spending on server systems to be significantly influenced by form factors, energy specifications, and virtualization technologies. Customers will continue to deploy highly dense servers, including blades, based on space constraints and the flexibility inherent to the blade chassis. The shift toward high density, combined with rising energy costs, will result in power and cooling system requirements being just as important as performance and price in terms of purchasing criteria. Finally, virtualization and multicore technologies will enable customers to migrate higher-end enterprise workloads from Unix and mainframes to x86 server platforms. The combination of these x86 technologies will keep x86 growth rates above the overall market rate over the forecast period. IDC sees a built-up demand for new servers and expects an increase in the number of servers being retired in 2010.

©2010 IDC #222605 15

T A B L E 1

W o r l d w i d e S e r v e r C u s t o m e r R e v e n u e b y O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Revenue ($M)

Windows 22,078.7 18,830.6 20,572.3 21,117.3 22,126.2 22,771.2 23,290.7 4.3

Unix 18,035.8 13,965.7 15,551.9 15,994.0 15,681.1 15,711.9 15,593.9 2.2

Linux 7,801.1 6,660.2 6,973.4 7,239.2 7,787.7 8,353.9 8,639.5 5.3

z/OS 5,332.5 3,800.2 3,689.7 3,787.4 3,436.9 3,249.4 3,139.4 -3.7

i5/OS 1,075.5 729.3 655.5 597.2 513.2 438.8 351.8 -13.6

NetWare 261.7 76.3 81.5 53.5 29.7 27.6 26.2 -19.2

Other 2,403.2 2,103.1 1,803.3 1,726.3 1,697.4 1,601.4 1,560.7 -5.8

Total 56,988.5 46,165.3 49,327.5 50,515.0 51,272.2 52,154.1 52,602.2 2.6

Growth (%) NA -19.0 6.8 2.4 1.5 1.7 0.9

Share (%)

Windows 38.7 40.8 41.7 41.8 43.2 43.7 44.3

Unix 31.6 30.3 31.5 31.7 30.6 30.1 29.6

Linux 13.7 14.4 14.1 14.3 15.2 16.0 16.4

z/OS 9.4 8.2 7.5 7.5 6.7 6.2 6.0

i5/OS 1.9 1.6 1.3 1.2 1.0 0.8 0.7

NetWare 0.5 0.2 0.2 0.1 0.1 0.1 0.0

Other 4.2 4.6 3.7 3.4 3.3 3.1 3.0

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

16 #222605 ©2010 IDC

T A B L E 2

W o r l d w i d e S e r v e r S h i p m e n t s b y O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Shipments

Windows 5,761,454 4,834,288 5,299,913 5,649,139 6,018,727 6,292,767 6,536,168 6.2

Unix 504,164 322,862 353,426 362,630 359,467 369,739 377,239 3.2

Linux 1,766,833 1,412,585 1,593,552 1,735,532 1,923,864 2,114,654 2,234,248 9.6

z/OS 2,387 1,244 1,157 1,208 1,203 1,209 1,204 -0.7

i5/OS 7,158 6,279 7,037 7,176 6,741 6,366 5,914 -1.2

NetWare 74,524 24,559 26,534 17,728 11,135 10,933 10,997 -14.8

Other 17,903 15,886 10,922 8,592 4,818 5,377 6,204 -17.1

Total 8,134,423 6,617,703 7,292,542 7,782,006 8,325,955 8,801,045 9,171,974 6.7

Growth (%) NA -18.6 10.2 6.7 7.0 5.7 4.2

Share (%)

Windows 70.8 73.1 72.7 72.6 72.3 71.5 71.3

Unix 6.2 4.9 4.8 4.7 4.3 4.2 4.1

Linux 21.7 21.3 21.9 22.3 23.1 24.0 24.4

z/OS 0.0 0.0 0.0 0.0 0.0 0.0 0.0

i5/OS 0.1 0.1 0.1 0.1 0.1 0.1 0.1

NetWare 0.9 0.4 0.4 0.2 0.1 0.1 0.1

Other 0.2 0.2 0.1 0.1 0.1 0.1 0.1

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

©2010 IDC #222605 17

T A B L E 3

A m e r i c a s S e r v e r C u s t o m e r R e v e n u e b y O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Revenue ($M)

Windows 9,687.1 8,476.5 9,443.6 9,476.7 10,168.9 10,495.4 10,864.6 5.1

Unix 7,220.4 5,817.2 6,767.4 6,920.5 6,748.3 6,577.2 6,424.0 2.0

Linux 3,386.3 2,754.6 3,103.1 3,159.0 3,396.8 3,762.3 3,920.6 7.3

z/OS 2,786.7 1,895.6 1,874.4 1,978.6 1,750.5 1,670.9 1,666.7 -2.5

i5/OS 414.5 256.5 376.5 334.4 273.8 212.1 140.3 -11.4

NetWare 113.0 20.9 5.5 0.7 0.7 0.7 0.6 -51.6

Other 490.0 396.0 432.5 371.5 331.7 332.5 336.3 -3.2

Total 24,097.9 19,617.4 22,003.0 22,241.4 22,670.7 23,051.2 23,353.0 3.5

Growth (%) NA -18.6 12.2 1.1 1.9 1.7 1.3

Share (%)

Windows 40.2 43.2 42.9 42.6 44.9 45.5 46.5

Unix 30.0 29.7 30.8 31.1 29.8 28.5 27.5

Linux 14.1 14.0 14.1 14.2 15.0 16.3 16.8

z/OS 11.6 9.7 8.5 8.9 7.7 7.2 7.1

i5/OS 1.7 1.3 1.7 1.5 1.2 0.9 0.6

NetWare 0.5 0.1 0.0 0.0 0.0 0.0 0.0

Other 2.0 2.0 2.0 1.7 1.5 1.4 1.4

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

18 #222605 ©2010 IDC

T A B L E 4

A m e r i c a s S e r v e r S h i p m e n t s b y O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Shipments

Windows 2,342,146 1,936,295 2,185,197 2,302,235 2,469,205 2,561,428 2,656,466 6.5

Unix 218,757 140,861 143,195 159,486 168,215 175,966 182,529 5.3

Linux 781,657 580,865 664,603 708,961 764,006 855,819 892,630 9.0

z/OS 1,076 338 359 416 396 410 425 4.7

i5/OS 2,683 2,721 4,950 5,158 4,897 4,585 4,185 9.0

NetWare 26,514 6,422 2,154 175 185 162 171 -51.6

Other 11,158 6,568 7,340 5,247 1,692 2,325 3,226 -13.3

Total 3,383,990 2,674,071 3,007,798 3,181,678 3,408,596 3,600,695 3,739,633 6.9

Growth (%) NA -21.0 12.5 5.8 7.1 5.6 3.9

Share (%)

Windows 69.2 72.4 72.7 72.4 72.4 71.1 71.0

Unix 6.5 5.3 4.8 5.0 4.9 4.9 4.9

Linux 23.1 21.7 22.1 22.3 22.4 23.8 23.9

z/OS 0.0 0.0 0.0 0.0 0.0 0.0 0.0

i5/OS 0.1 0.1 0.2 0.2 0.1 0.1 0.1

NetWare 0.8 0.2 0.1 0.0 0.0 0.0 0.0

Other 0.3 0.2 0.2 0.2 0.0 0.1 0.1

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

©2010 IDC #222605 19

T A B L E 5

E M E A S e r v e r C u s t o m e r R e v e n u e b y O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Revenue ($M)

Windows 7,092.4 5,587.3 5,923.4 6,090.0 6,127.3 6,164.8 6,281.6 2.4

Unix 5,802.9 3,907.5 4,396.3 4,514.2 4,275.9 4,225.3 4,170.8 1.3

Linux 2,657.4 2,197.5 1,969.9 1,990.9 2,008.9 1,972.0 1,959.2 -2.3

z/OS 1,729.5 1,066.9 1,003.0 1,022.6 902.1 856.5 801.0 -5.6

i5/OS 374.9 282.3 92.6 84.3 66.3 60.6 60.2 -26.6

NetWare 82.3 29.0 75.0 51.8 28.1 26.0 24.8 -3.1

Other 627.8 467.0 396.9 442.1 504.8 463.1 451.5 -0.7

Total 18,367.3 13,537.5 13,857.0 14,195.9 13,913.4 13,768.2 13,749.0 0.3

Growth (%) NA -26.3 2.4 2.4 -2.0 -1.0 -0.1

Share (%)

Windows 38.6 41.3 42.7 42.9 44.0 44.8 45.7

Unix 31.6 28.9 31.7 31.8 30.7 30.7 30.3

Linux 14.5 16.2 14.2 14.0 14.4 14.3 14.2

z/OS 9.4 7.9 7.2 7.2 6.5 6.2 5.8

i5/OS 2.0 2.1 0.7 0.6 0.5 0.4 0.4

NetWare 0.4 0.2 0.5 0.4 0.2 0.2 0.2

Other 3.4 3.4 2.9 3.1 3.6 3.4 3.3

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

20 #222605 ©2010 IDC

T A B L E 6

E M E A S e r v e r S h i p m e n t s b y O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Shipments

Windows 1,930,076 1,523,152 1,617,468 1,729,152 1,821,400 1,882,916 1,974,687 5.3

Unix 149,658 87,603 108,535 97,966 83,980 83,217 82,369 -1.2

Linux 566,396 418,340 453,308 476,980 506,902 516,917 534,654 5.0

z/OS 1,038 652 577 561 550 551 538 -3.8

i5/OS 2,812 2,240 850 829 712 675 677 -21.3

NetWare 26,702 9,848 24,051 17,232 10,634 10,460 10,517 1.3

Other 4,079 7,198 1,766 1,657 1,508 1,513 1,513 -26.8

Total 2,680,761 2,049,033 2,206,556 2,324,377 2,425,686 2,496,250 2,604,955 4.9

Growth (%) NA -23.6 7.7 5.3 4.4 2.9 4.4

Share (%)

Windows 72.0 74.3 73.3 74.4 75.1 75.4 75.8

Unix 5.6 4.3 4.9 4.2 3.5 3.3 3.2

Linux 21.1 20.4 20.5 20.5 20.9 20.7 20.5

z/OS 0.0 0.0 0.0 0.0 0.0 0.0 0.0

i5/OS 0.1 0.1 0.0 0.0 0.0 0.0 0.0

NetWare 1.0 0.5 1.1 0.7 0.4 0.4 0.4

Other 0.2 0.4 0.1 0.1 0.1 0.1 0.1

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

©2010 IDC #222605 21

T A B L E 7

A s i a / P a c i f i c S e r v e r C u s t o m e r R e v e n u e b y O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Revenue ($M)

Windows 5,299.2 4,766.8 5,205.2 5,550.7 5,830.0 6,110.9 6,144.6 5.2

Unix 5,012.6 4,241.0 4,388.2 4,559.4 4,657.0 4,909.4 4,999.2 3.3

Linux 1,757.5 1,708.0 1,900.3 2,089.3 2,382.0 2,619.6 2,759.6 10.1

z/OS 816.3 837.6 812.3 786.3 784.4 722.0 671.7 -4.3

i5/OS 286.0 190.5 186.4 178.5 173.0 166.1 151.3 -4.5

NetWare 66.4 26.4 1.0 0.9 0.9 0.9 0.9 -49.4

Other 1,285.3 1,240.1 973.9 912.7 860.8 805.8 772.9 -9.0

Total 14,523.4 13,010.4 13,467.4 14,077.7 14,688.1 15,334.7 15,500.2 3.6

Growth (%) NA -10.4 3.5 4.5 4.3 4.4 1.1

Share (%)

Windows 36.5 36.6 38.7 39.4 39.7 39.9 39.6

Unix 34.5 32.6 32.6 32.4 31.7 32.0 32.3

Linux 12.1 13.1 14.1 14.8 16.2 17.1 17.8

z/OS 5.6 6.4 6.0 5.6 5.3 4.7 4.3

i5/OS 2.0 1.5 1.4 1.3 1.2 1.1 1.0

NetWare 0.5 0.2 0.0 0.0 0.0 0.0 0.0

Other 8.8 9.5 7.2 6.5 5.9 5.3 5.0

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

22 #222605 ©2010 IDC

T A B L E 8

A s i a / P a c i f i c S e r v e r S h i p m e n t s b y O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Shipments

Windows 1,489,233 1,374,841 1,497,248 1,617,752 1,728,122 1,848,423 1,905,015 6.7

Unix 135,749 94,398 101,695 105,179 107,272 110,556 112,340 3.5

Linux 418,780 413,380 475,641 549,592 652,956 741,918 806,964 14.3

z/OS 273 254 221 230 256 247 241 -1.0

i5/OS 1,663 1,318 1,236 1,189 1,133 1,106 1,052 -4.4

NetWare 21,308 8,289 330 322 316 311 309 -48.2

Other 2,666 2,120 1,816 1,688 1,618 1,539 1,465 -7.1

Total 2,069,672 1,894,599 2,078,188 2,275,951 2,491,673 2,704,100 2,827,386 8.3

Growth (%) NA -8.5 9.7 9.5 9.5 8.5 4.6

Share (%)

Windows 72.0 72.6 72.0 71.1 69.4 68.4 67.4

Unix 6.6 5.0 4.9 4.6 4.3 4.1 4.0

Linux 20.2 21.8 22.9 24.1 26.2 27.4 28.5

z/OS 0.0 0.0 0.0 0.0 0.0 0.0 0.0

i5/OS 0.1 0.1 0.1 0.1 0.0 0.0 0.0

NetWare 1.0 0.4 0.0 0.0 0.0 0.0 0.0

Other 0.1 0.1 0.1 0.1 0.1 0.1 0.1

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

©2010 IDC #222605 23

T A B L E 9

W o r l d w i d e S e r v e r C u s t o m e r R e v e n u e b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4 ( $ M )

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

CISC

Unix 83.0 177.0 74.5 66.3 63.8 140.0 76.4 -15.5

z/OS 5,332.5 3,800.2 3,689.7 3,787.4 3,436.9 3,249.4 3,139.4 -3.7

Other 1,109.5 1,187.9 962.5 968.4 935.1 840.1 789.3 -7.9

Subtotal 6,525.0 5,165.1 4,726.7 4,822.1 4,435.8 4,229.5 4,005.0 -5.0

Growth (%) NA -20.8 -8.5 2.0 -8.0 -4.7 -5.3

EPIC

Windows 274.5 123.4 145.5 157.7 171.0 196.8 226.5 12.9

Unix 3,699.6 3,271.9 3,696.2 3,838.7 3,963.7 4,187.9 4,330.9 5.8

Linux 432.7 291.1 276.0 301.8 338.8 362.3 391.5 6.1

Other 777.6 537.7 493.0 477.8 518.8 521.0 531.4 -0.2

Subtotal 5,184.3 4,224.1 4,610.9 4,776.2 4,992.5 5,268.2 5,480.3 5.3

Growth (%) NA -18.5 9.2 3.6 4.5 5.5 4.0

RISC

Unix 13,478.6 9,934.4 11,053.5 11,432.2 11,036.7 10,759.1 10,561.4 1.2

Linux 236.1 265.7 148.4 196.3 230.9 260.0 285.7 1.5

i5/OS 1,075.5 729.3 655.5 597.2 513.2 438.8 351.8 -13.6

Other 309.2 152.2 163.7 152.9 160.3 162.0 163.2 1.4

Subtotal 15,099.4 11,081.7 12,021.1 12,378.7 11,941.1 11,619.8 11,362.1 0.5

Growth (%) NA -26.6 8.5 3.0 -3.5 -2.7 -2.2

x86

Windows 21,804.2 18,707.2 20,426.8 20,959.6 21,955.2 22,574.3 23,064.2 4.3

Unix 774.6 582.4 727.6 656.7 616.9 624.9 625.2 1.4

Linux 7,132.4 6,103.4 6,549.0 6,741.1 7,217.9 7,731.6 7,962.3 5.5

24 #222605 ©2010 IDC

T A B L E 9

W o r l d w i d e S e r v e r C u s t o m e r R e v e n u e b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4 ( $ M )

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

NetWare 261.7 76.2 81.3 53.3 29.5 27.4 26.1 -19.3

Other 206.9 225.2 184.2 127.2 83.2 78.3 76.8 -19.4

Subtotal 30,179.8 25,694.5 27,968.9 28,538.0 29,902.9 31,036.6 31,754.6 4.3

Growth (%) NA -14.9 8.9 2.0 4.8 3.8 2.3

Total 56,988.5 46,165.3 49,327.5 50,515.0 51,272.2 52,154.1 52,602.2 2.6

Growth (%) NA -19.0 6.8 2.4 1.5 1.7 0.9

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

T A B L E 1 0

W o r l d w i d e S e r v e r S h i p m e n t s b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

CISC

Unix 91 201 71 55 54 118 67 -19.7

z/OS 2,387 1,244 1,157 1,208 1,203 1,209 1,204 -0.7

Other 1,110 527 500 529 506 494 475 -2.1

Subtotal 3,588 1,972 1,728 1,791 1,763 1,821 1,746 -2.4

Growth (%) NA -45.0 -12.4 3.7 -1.6 3.3 -4.1

EPIC

Windows 4,574 2,294 3,066 3,133 3,608 4,345 5,327 18.4

Unix 41,408 34,812 37,722 40,431 43,182 47,372 51,067 8.0

Linux 9,544 4,957 5,234 5,459 5,965 6,960 8,644 11.8

Other 2,894 2,051 2,053 2,187 2,392 2,865 3,627 12.1

Subtotal 58,420 44,115 48,074 51,209 55,148 61,541 68,665 9.3

Growth (%) NA -24.5 9.0 6.5 7.7 11.6 11.6

©2010 IDC #222605 25

T A B L E 1 0

W o r l d w i d e S e r v e r S h i p m e n t s b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

RISC

Windows 1 1 – – – – – NA

Unix 304,740 184,556 189,186 199,757 197,193 195,671 193,891 1.0

Linux 7,877 8,333 8,527 11,664 13,289 14,722 15,158 12.7

i5/OS 7,158 6,279 7,037 7,176 6,741 6,366 5,914 -1.2

NetWare 1 – – – – – – NA

Other 866 367 561 621 716 825 917 20.1

Subtotal 320,642 199,536 205,311 219,218 217,939 217,584 215,880 1.6

Growth (%) NA -37.8 2.9 6.8 -0.6 -0.2 -0.8

x86

Windows 5,756,880 4,831,993 5,296,848 5,646,007 6,015,119 6,288,423 6,530,841 6.2

Unix 157,925 103,292 126,447 122,387 119,038 126,578 132,214 5.1

Linux 1,749,412 1,399,295 1,579,791 1,718,409 1,904,610 2,092,972 2,210,446 9.6

NetWare 74,523 24,559 26,534 17,728 11,135 10,933 10,997 -14.8

Other 13,034 12,940 7,810 5,256 1,204 1,193 1,185 -38.0

Subtotal 7,751,773 6,372,080 7,037,430 7,509,787 8,051,105 8,520,099 8,885,683 6.9

Growth (%) NA -17.8 10.4 6.7 7.2 5.8 4.3

Total 8,134,423 6,617,703 7,292,542 7,782,006 8,325,955 8,801,045 9,171,974 6.7

Growth (%) NA -18.6 10.2 6.7 7.0 5.7 4.2

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

26 #222605 ©2010 IDC

T A B L E 1 1

A m e r i c a s S e r v e r C u s t o m e r R e v e n u e b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4 ( $ M )

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

CISC

z/OS 2,786.7 1,895.6 1,874.4 1,978.6 1,750.5 1,670.9 1,666.7 -2.5

Other 113.8 118.7 99.7 89.9 65.8 50.1 36.7 -20.9

Subtotal 2,900.5 2,014.3 1,974.1 2,068.5 1,816.3 1,721.0 1,703.3 -3.3

Growth (%) NA -30.6 -2.0 4.8 -12.2 -5.2 -1.0

EPIC

Windows 130.0 66.0 75.4 81.3 94.0 110.7 135.0 15.4

Unix 1,142.2 1,083.6 1,114.9 1,121.9 1,220.9 1,311.3 1,390.5 5.1

Linux 108.5 62.4 86.4 97.3 113.2 130.6 152.0 19.5

NetWare – 0.0 0.1 0.2 0.2 0.2 0.1 22.5

Other 226.1 144.8 224.7 215.4 229.0 241.4 253.7 11.9

Subtotal 1,606.9 1,356.8 1,501.5 1,516.2 1,657.4 1,794.3 1,931.3 7.3

Growth (%) NA -15.6 10.7 1.0 9.3 8.3 7.6

RISC

Unix 5,640.2 4,348.8 5,237.0 5,392.9 5,100.6 4,825.4 4,586.6 1.1

Linux 88.6 107.9 113.5 152.5 173.9 194.7 221.8 15.5

i5/OS 414.5 256.5 376.5 334.4 273.8 212.1 140.3 -11.4

Other 71.6 26.0 25.0 32.3 36.9 41.0 45.9 12.1

Subtotal 6,214.9 4,739.1 5,752.1 5,912.1 5,585.2 5,273.3 4,994.6 1.1

Growth (%) NA -23.7 21.4 2.8 -5.5 -5.6 -5.3

©2010 IDC #222605 27

T A B L E 1 1

A m e r i c a s S e r v e r C u s t o m e r R e v e n u e b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4 ( $ M )

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

x86

Windows 9,557.0 8,410.5 9,368.2 9,395.3 10,074.9 10,384.7 10,729.5 5.0

Unix 438.0 384.8 415.5 405.6 426.7 440.5 446.9 3.0

Linux 3,189.2 2,584.3 2,903.2 2,909.2 3,109.7 3,436.9 3,546.9 6.5

NetWare 112.9 20.9 5.4 0.5 0.5 0.5 0.5 -52.8

Other 78.5 106.6 83.0 34.0 – – – NA

Subtotal 13,375.6 11,507.1 12,775.3 12,744.6 13,611.8 14,262.7 14,723.8 5.1

Growth (%) NA -14.0 11.0 -0.2 6.8 4.8 3.2

Total 24,097.9 19,617.4 22,003.0 22,241.4 22,670.7 23,051.2 23,353.0 3.5

Growth (%) NA -18.6 12.2 1.1 1.9 1.7 1.3

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

T A B L E 1 2

A m e r i c a s S e r v e r S h i p m e n t s b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

CISC

z/OS 1,076 338 359 416 396 410 425 4.7

Other 75 87 76 82 70 64 55 -8.7

Subtotal 1,151 425 435 498 466 474 480 2.4

Growth (%) NA -63.0 2.4 14.5 -6.6 1.8 1.2

EPIC

Windows 2,045 1,218 1,792 1,920 2,349 2,989 3,846 25.9

Unix 11,752 10,421 11,548 12,802 15,159 17,645 20,137 14.1

28 #222605 ©2010 IDC

T A B L E 1 2

A m e r i c a s S e r v e r S h i p m e n t s b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Linux 3,444 1,100 1,796 2,229 2,954 3,979 5,563 38.3

Other 1,184 719 929 1,004 1,308 1,851 2,655 29.9

Subtotal 18,425 13,459 16,065 17,955 21,770 26,463 32,202 19.1

Growth (%) NA -27.0 19.4 11.8 21.2 21.6 21.7

RISC

Windows 1 1 – – – – – NA

Unix 130,384 74,219 74,051 82,594 80,878 78,847 77,224 0.8

Linux 6,077 6,553 5,714 8,146 9,519 10,625 11,184 11.3

i5/OS 2,683 2,721 4,950 5,158 4,897 4,585 4,185 9.0

NetWare 1 – – – – – – NA

Other 177 56 137 225 315 410 516 55.8

Subtotal 139,322 83,550 84,852 96,122 95,609 94,467 93,108 2.2

Growth (%) NA -40.0 1.6 13.3 -0.5 -1.2 -1.4

x86

Windows 2,340,100 1,935,077 2,183,405 2,300,316 2,466,856 2,558,440 2,652,620 6.5

Unix 76,621 56,220 57,597 64,091 72,178 79,474 85,168 8.7

Linux 772,136 573,212 657,093 698,586 751,532 841,215 875,882 8.8

NetWare 26,513 6,422 2,154 175 185 162 171 -51.6

Other 9,723 5,706 6,198 3,936 – – – NA

Subtotal 3,225,092 2,576,637 2,906,446 3,067,103 3,290,751 3,479,291 3,613,843 7.0

Growth (%) NA -20.1 12.8 5.5 7.3 5.7 3.9

Total 3,383,990 2,674,071 3,007,798 3,181,678 3,408,596 3,600,695 3,739,633 6.9

Growth (%) NA -21.0 12.5 5.8 7.1 5.6 3.9

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

©2010 IDC #222605 29

T A B L E 1 3

E M E A S e r v e r C u s t o m e r R e v e n u e b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4 ( $ M )

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

CISC

Unix 22.3 12.7 12.5 12.9 13.2 14.8 13.8 1.7

z/OS 1,729.5 1,066.9 1,003.0 1,022.6 902.1 856.5 801.0 -5.6

Other 297.1 270.7 265.0 316.1 343.4 307.1 289.4 1.4

Subtotal 2,049.0 1,350.2 1,280.5 1,351.6 1,258.7 1,178.4 1,104.2 -3.9

Growth (%) NA -34.1 -5.2 5.5 -6.9 -6.4 -6.3

EPIC

Windows 79.7 38.4 48.0 53.4 50.0 56.9 59.9 9.3

Unix 1,270.9 924.7 1,250.0 1,288.3 1,234.1 1,274.1 1,304.4 7.1

Linux 222.4 151.6 123.9 138.3 158.6 164.1 171.7 2.5

Other 203.5 125.5 95.4 92.3 127.3 123.1 130.2 0.7

Subtotal 1,776.5 1,240.2 1,517.4 1,572.3 1,570.1 1,618.2 1,666.2 6.1

Growth (%) NA -30.2 22.4 3.6 -0.1 3.1 3.0

RISC

Unix 4,308.4 2,850.4 2,907.1 3,049.5 2,929.6 2,845.7 2,765.2 -0.6

Linux 146.1 152.5 34.3 42.8 55.8 63.9 62.6 -16.3

i5/OS 374.9 282.3 92.6 84.3 66.3 60.6 60.2 -26.6

Other 112.4 46.3 34.6 32.7 33.5 32.2 31.2 -7.6

Subtotal 4,941.9 3,331.5 3,068.6 3,209.3 3,085.2 3,002.4 2,919.1 -2.6

Growth (%) NA -32.6 -7.9 4.6 -3.9 -2.7 -2.8

30 #222605 ©2010 IDC

T A B L E 1 3

E M E A S e r v e r C u s t o m e r R e v e n u e b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4 ( $ M )

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

x86

Windows 7,012.7 5,548.9 5,875.4 6,036.5 6,077.3 6,107.9 6,221.7 2.3

Unix 201.2 119.7 226.6 163.5 99.0 90.7 87.4 -6.1

Linux 2,288.9 1,893.4 1,811.7 1,809.9 1,794.4 1,743.9 1,724.9 -1.8

NetWare 82.3 29.0 75.0 51.8 28.1 26.0 24.8 -3.1

Other 14.8 24.6 1.8 1.0 0.6 0.7 0.7 -50.8

Subtotal 9,599.9 7,615.6 7,990.5 8,062.7 7,999.5 7,969.2 8,059.5 1.1

Growth (%) NA 66.3 -92.6 -46.2 -35.1 2.6 8.5

Total 18,367.3 13,537.5 13,857.0 14,195.9 13,913.4 13,768.2 13,749.0 0.3

Growth (%) NA -26.3 2.4 2.4 -2.0 -1.0 -0.1

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

T A B L E 1 4

E M E A S e r v e r S h i p m e n t s b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

CISC

Unix 49 29 28 15 14 18 17 -10.0

z/OS 1,038 652 577 561 550 551 538 -3.8

Other 117 66 138 189 192 200 198 24.5

Subtotal 1,204 747 743 766 756 769 753 0.2

Growth (%) NA -38.0 -0.6 3.1 -1.3 1.7 -2.0

©2010 IDC #222605 31

T A B L E 1 4

E M E A S e r v e r S h i p m e n t s b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

EPIC

Windows 1,366 633 795 762 735 782 873 6.6

Unix 12,875 7,938 8,801 8,909 8,175 8,420 9,013 2.6

Linux 5,005 2,871 2,693 2,317 2,044 2,000 2,074 -6.3

Other 1,211 931 718 785 706 666 654 -6.8

Subtotal 20,457 12,373 13,007 12,773 11,659 11,868 12,615 0.4

Growth (%) NA -39.5 5.1 -1.8 -8.7 1.8 6.3

RISC

Unix 89,177 52,281 52,860 53,810 53,441 52,839 51,104 -0.5

Linux 1,644 1,720 2,765 3,451 3,695 4,017 3,892 17.7

i5/OS 2,812 2,240 850 829 712 675 677 -21.3

Other 460 220 343 346 344 362 351 9.8

Subtotal 94,093 56,461 56,818 58,436 58,192 57,893 56,024 -0.2

Growth (%) NA -40.0 0.6 2.8 -0.4 -0.5 -3.2

x86

Windows 1,928,710 1,522,519 1,616,673 1,728,391 1,820,666 1,882,134 1,973,813 5.3

Unix 47,557 27,355 46,846 35,231 22,350 21,940 22,235 -4.1

Linux 559,747 413,749 447,851 471,211 501,163 510,899 528,688 5.0

NetWare 26,702 9,848 24,051 17,232 10,634 10,460 10,517 1.3

Other 2,291 5,981 567 337 267 285 310 -44.7

Subtotal 2,565,007 1,979,452 2,135,989 2,252,402 2,355,080 2,425,719 2,535,563 5.1

Growth (%) NA -22.8 7.9 5.5 4.6 3.0 4.5

Total 2,680,761 2,049,033 2,206,556 2,324,377 2,425,686 2,496,250 2,604,955 4.9

Growth (%) NA -23.6 7.7 5.3 4.4 2.9 4.4

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

32 #222605 ©2010 IDC

T A B L E 1 5

A s i a / P a c i f i c S e r v e r C u s t o m e r R e v e n u e b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4 ( $ M )

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

CISC

Unix 60.7 164.3 62.0 53.4 50.6 125.2 62.6 -17.6

z/OS 816.3 837.6 812.3 786.3 784.4 722.0 671.7 -4.3

Other 698.5 798.6 597.7 562.4 525.8 482.9 463.2 -10.3

Subtotal 1,575.5 1,800.5 1,472.1 1,402.0 1,360.8 1,330.1 1,197.5 -7.8

Growth (%) NA 14.3 -18.2 -4.8 -2.9 -2.3 -10.0

EPIC

Windows 64.7 19.0 22.0 22.9 27.0 29.2 31.6 10.7

Unix 1,286.4 1,263.6 1,331.3 1,428.5 1,508.7 1,602.5 1,635.9 5.3

Linux 101.8 77.1 65.8 66.2 67.0 67.5 67.8 -2.5

Other 348.0 267.4 172.8 170.1 162.5 156.5 147.6 -11.2

Subtotal 1,801.0 1,627.0 1,591.9 1,687.7 1,765.1 1,855.7 1,883.0 3.0

Growth (%) NA -9.7 -2.2 6.0 4.6 5.1 1.5

RISC

Unix 3,530.1 2,735.3 2,909.3 2,989.8 3,006.5 3,088.0 3,209.6 3.3

Linux 1.4 5.2 0.5 1.0 1.2 1.3 1.4 -23.4

i5/OS 286.0 190.5 186.4 178.5 173.0 166.1 151.3 -4.5

Other 125.1 80.0 104.1 87.9 89.9 88.8 86.1 1.5

Subtotal 3,942.6 3,011.1 3,200.3 3,257.2 3,270.7 3,344.2 3,448.4 2.7

Growth (%) NA -23.6 6.3 1.8 0.4 2.2 3.1

x86

Windows 5,234.5 4,747.8 5,183.2 5,527.8 5,803.0 6,081.7 6,112.9 5.2

Unix 135.4 77.9 85.5 87.6 91.2 93.7 91.0 3.2

©2010 IDC #222605 33

T A B L E 1 5

A s i a / P a c i f i c S e r v e r C u s t o m e r R e v e n u e b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4 ( $ M )

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Linux 1,654.4 1,625.7 1,834.0 2,022.1 2,313.9 2,550.8 2,690.4 10.6

NetWare 66.4 26.4 1.0 0.9 0.9 0.9 0.9 -49.4

Other 113.6 94.0 99.3 92.2 82.6 77.7 76.1 -4.1

Subtotal 7,204.3 6,571.8 7,203.1 7,730.7 8,291.6 8,804.8 8,971.4 6.4

Growth (%) NA -8.8 9.6 7.3 7.3 6.2 1.9

Total 14,523.4 13,010.4 13,467.4 14,077.7 14,688.1 15,334.7 15,500.2 3.6

Growth (%) NA -10.4 3.5 4.5 4.3 4.4 1.1

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

T A B L E 1 6

A s i a / P a c i f i c S e r v e r S h i p m e n t s b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4 ( $ M )

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

CISC

Unix 42 172 43 40 40 100 50 -21.9

z/OS 273 254 221 230 256 247 241 -1.0

Other 918 374 285 257 245 230 222 -9.9

Subtotal 1,233 800 550 527 541 578 513 -8.5

Growth (%) NA -35.1 -31.3 -4.1 2.7 6.8 -11.2

EPIC

Windows 1,163 443 479 451 525 574 608 6.5

Unix 16,781 16,453 17,374 18,720 19,849 21,308 21,916 5.9

Linux 1,095 986 745 913 967 981 1,006 0.4

34 #222605 ©2010 IDC

T A B L E 1 6

A s i a / P a c i f i c S e r v e r S h i p m e n t s b y C h i p a n d O p e r a t i n g S y s t e m , 2 0 0 8 – 2 0 1 4 ( $ M )

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Other 499 401 405 398 379 348 317 -4.6

Subtotal 19,538 18,283 19,003 20,481 21,719 23,210 23,848 5.5

Growth (%) NA -6.4 3.9 7.8 6.0 6.9 2.7

RISC

Unix 85,179 58,056 62,275 63,353 62,873 63,984 65,563 2.5

Linux 156 60 48 67 74 80 82 6.5

i5/OS 1,663 1,318 1,236 1,189 1,133 1,106 1,052 -4.4

Other 229 91 81 50 58 53 51 -11.0

Subtotal 87,227 59,525 63,640 64,660 64,138 65,223 66,748 2.3

Growth (%) NA -31.8 6.9 1.6 -0.8 1.7 2.3

x86

Windows 1,488,070 1,374,398 1,496,770 1,617,301 1,727,597 1,847,849 1,904,407 6.7

Unix 33,747 19,717 22,003 23,065 24,509 25,164 24,811 4.7

Linux 417,529 412,334 474,847 548,612 651,915 740,857 805,876 14.3

NetWare 21,308 8,289 330 322 316 311 309 -48.2

Other 1,020 1,254 1,045 983 937 908 875 -6.9

Subtotal 1,961,674 1,815,991 1,994,995 2,190,282 2,405,275 2,615,089 2,736,277 8.5

Growth (%) NA -7.4 9.9 9.8 9.8 8.7 4.6

Total 2,069,672 1,894,599 2,078,188 2,275,951 2,491,673 2,704,100 2,827,386 8.3

Growth (%) NA -8.5 9.7 9.5 9.5 8.5 4.6

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

©2010 IDC #222605 35

T A B L E 1 7

W o r l d w i d e S e r v e r C u s t o m e r R e v e n u e b y P r i c e B a n d , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Revenue ($M)

$0–2,999 6,338.3 4,755.8 7,208.6 7,398.4 7,620.2 8,759.7 9,465.1 14.8

$3,000–5,999 15,625.2 12,825.6 13,398.5 13,435.6 14,116.2 13,778.6 13,701.2 1.3

$6,000–9,999 3,481.7 3,363.0 2,928.8 3,476.2 3,994.5 5,040.2 5,605.9 10.8

$10,000–24,999 6,156.3 5,336.8 5,273.8 5,566.0 5,701.5 5,071.5 4,674.6 -2.6

$25,000–49,999 2,756.8 2,488.8 2,915.9 2,930.8 2,917.9 3,065.5 2,901.6 3.1

$50,000–99,999 3,025.7 2,228.7 2,651.7 2,688.7 2,621.7 2,565.5 3,087.9 6.7

$100,000–249,999 2,887.1 1,972.1 3,352.8 3,416.8 3,361.1 3,456.3 3,253.8 10.5

$250,000–499,999 3,583.5 2,576.6 2,608.6 2,625.7 2,537.6 2,434.3 2,539.8 -0.3

$500,000–999,999 3,643.6 3,106.4 2,491.5 2,701.2 2,757.2 2,830.2 2,583.8 -3.6

$1M–2.9M 4,478.9 3,558.3 3,147.4 3,101.1 3,004.7 2,727.1 2,385.7 -7.7

$3M+ 5,011.4 3,953.2 3,350.0 3,174.4 2,639.8 2,425.1 2,402.7 -9.5

Total 56,988.5 46,165.3 49,327.5 50,515.0 51,272.2 52,154.1 52,602.2 2.6

Share (%)

$0–2,999 11.1 10.3 14.6 14.6 14.9 16.8 18.0

$3,000–5,999 27.4 27.8 27.2 26.6 27.5 26.4 26.0

$6,000–9,999 6.1 7.3 5.9 6.9 7.8 9.7 10.7

$10,000–24,999 10.8 11.6 10.7 11.0 11.1 9.7 8.9

$25,000–49,999 4.8 5.4 5.9 5.8 5.7 5.9 5.5

$50,000–99,999 5.3 4.8 5.4 5.3 5.1 4.9 5.9

$100,000–249,999 5.1 4.3 6.8 6.8 6.6 6.6 6.2

$250,000–499,999 6.3 5.6 5.3 5.2 4.9 4.7 4.8

$500,000–999,999 6.4 6.7 5.1 5.3 5.4 5.4 4.9

$1M–2.9M 7.9 7.7 6.4 6.1 5.9 5.2 4.5

$3M+ 8.8 8.6 6.8 6.3 5.1 4.6 4.6

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

36 #222605 ©2010 IDC

T A B L E 1 8

W o r l d w i d e S e r v e r S h i p m e n t s b y P r i c e B a n d , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Shipments

$0–2,999 3,347,123 2,636,529 3,408,414 3,637,530 3,825,865 4,313,600 4,654,908 12.0

$3,000–5,999 3,766,756 3,045,429 3,020,807 3,186,403 3,450,771 3,377,107 3,377,295 2.1

$6,000–9,999 450,184 440,513 370,735 444,605 518,779 637,525 702,732 9.8

$10,000–24,999 412,651 367,518 352,998 371,221 387,160 325,749 286,674 -4.8

$25,000–49,999 80,895 71,791 77,625 78,216 78,414 82,092 78,180 1.7

$50,000–99,999 40,586 29,605 32,242 32,511 31,965 31,189 40,778 6.6

$100,000–249,999 18,507 12,842 16,830 18,343 19,380 20,280 18,154 7.2

$250,000–499,999 9,701 6,958 7,297 7,376 7,552 7,447 7,606 1.8

$500,000–999,999 4,812 4,103 3,527 3,678 3,963 4,043 3,774 -1.7

$1M–2.9M 2,725 1,967 1,721 1,785 1,817 1,736 1,576 -4.3

$3M+ 484 448 348 338 288 279 296 -8.0

Total 8,134,423 6,617,703 7,292,542 7,782,006 8,325,955 8,801,045 9,171,974 6.7

Share (%)

$0–2,999 41.1 39.8 46.7 46.7 46.0 49.0 50.8

$3,000–5,999 46.3 46.0 41.4 40.9 41.4 38.4 36.8

$6,000–9,999 5.5 6.7 5.1 5.7 6.2 7.2 7.7

$10,000–24,999 5.1 5.6 4.8 4.8 4.7 3.7 3.1

$25,000–49,999 1.0 1.1 1.1 1.0 0.9 0.9 0.9

$50,000–99,999 0.5 0.4 0.4 0.4 0.4 0.4 0.4

$100,000–249,999 0.2 0.2 0.2 0.2 0.2 0.2 0.2

$250,000–499,999 0.1 0.1 0.1 0.1 0.1 0.1 0.1

$500,000–999,999 0.1 0.1 0.0 0.0 0.0 0.0 0.0

$1M–2.9M 0.0 0.0 0.0 0.0 0.0 0.0 0.0

$3M+ 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

©2010 IDC #222605 37

T A B L E 1 9

A m e r i c a s S e r v e r C u s t o m e r R e v e n u e b y P r i c e B a n d , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Revenue ($M)

$0–2,999 2,189.2 1,393.9 2,228.1 2,349.3 2,519.4 2,655.8 2,767.8 14.7

$3,000–5,999 8,184.6 6,877.0 7,905.1 7,841.5 8,355.0 8,750.2 9,021.6 5.6

$6,000–9,999 993.2 1,085.6 842.3 822.9 985.6 1,197.1 1,442.1 5.8

$10,000–24,999 2,648.8 2,299.7 1,940.3 2,068.2 2,151.3 2,129.1 2,034.5 -2.4

$25,000–49,999 936.4 1,041.9 1,323.1 1,371.3 1,392.5 1,383.9 1,337.4 5.1

$50,000–99,999 1,191.1 660.6 1,089.5 1,120.0 1,079.9 1,035.0 950.2 7.5

$100,000–249,999 865.3 571.4 1,128.3 1,147.0 1,172.6 1,221.3 1,370.2 19.1

$250,000–499,999 1,500.2 888.1 1,020.5 1,109.1 1,044.9 1,013.3 981.6 2.0

$500,000–999,999 1,214.5 1,245.8 1,055.7 1,000.7 1,000.6 986.3 957.5 -5.1

$1M–2.9M 1,923.7 1,780.6 1,596.4 1,580.9 1,417.9 1,248.0 1,050.7 -10.0

$3M+ 2,450.9 1,772.7 1,873.7 1,830.3 1,551.1 1,431.2 1,439.2 -4.1

Total 24,097.9 19,617.4 22,003.0 22,241.4 22,670.7 23,051.2 23,353.0 3.5

Share (%)

$0–2,999 9.1 7.1 10.1 10.6 11.1 11.5 11.9

$3,000–5,999 34.0 35.1 35.9 35.3 36.9 38.0 38.6

$6,000–9,999 4.1 5.5 3.8 3.7 4.3 5.2 6.2

$10,000–24,999 11.0 11.7 8.8 9.3 9.5 9.2 8.7

$25,000–49,999 3.9 5.3 6.0 6.2 6.1 6.0 5.7

$50,000–99,999 4.9 3.4 5.0 5.0 4.8 4.5 4.1

$100,000–249,999 3.6 2.9 5.1 5.2 5.2 5.3 5.9

$250,000–499,999 6.2 4.5 4.6 5.0 4.6 4.4 4.2

$500,000–999,999 5.0 6.4 4.8 4.5 4.4 4.3 4.1

$1M–2.9M 8.0 9.1 7.3 7.1 6.3 5.4 4.5

$3M+ 10.2 9.0 8.5 8.2 6.8 6.2 6.2

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

38 #222605 ©2010 IDC

T A B L E 2 0

A m e r i c a s S e r v e r S h i p m e n t s b y P r i c e B a n d , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Shipments

$0–2,999 1,021,547 685,670 939,697 1,027,908 1,103,903 1,170,234 1,222,069 12.3

$3,000–5,999 1,997,888 1,642,365 1,759,612 1,824,584 1,945,123 2,050,336 2,119,445 5.2

$6,000–9,999 127,275 141,092 113,475 116,189 139,086 165,623 196,254 6.8

$10,000–24,999 183,052 157,891 133,573 149,480 158,064 153,639 142,321 -2.1

$25,000–49,999 27,264 29,561 37,848 39,443 39,568 38,756 37,199 4.7

$50,000–99,999 14,969 8,465 11,426 11,614 10,831 10,293 10,130 3.7

$100,000–249,999 5,063 3,811 6,523 6,542 6,370 6,356 6,928 12.7

$250,000–499,999 4,013 2,383 3,107 3,443 3,252 3,161 3,097 5.4

$500,000–999,999 1,513 1,735 1,489 1,397 1,425 1,408 1,363 -4.7

$1M–2.9M 1,197 924 851 874 806 725 645 -6.9

$3M+ 209 172 195 203 168 164 182 1.1

Total 3,383,990 2,674,071 3,007,798 3,181,678 3,408,596 3,600,695 3,739,633 6.9

Share (%)

$0–2,999 30.2 25.6 31.2 32.3 32.4 32.5 32.7

$3,000–5,999 59.0 61.4 58.5 57.3 57.1 56.9 56.7

$6,000–9,999 3.8 5.3 3.8 3.7 4.1 4.6 5.2

$10,000–24,999 5.4 5.9 4.4 4.7 4.6 4.3 3.8

$25,000–49,999 0.8 1.1 1.3 1.2 1.2 1.1 1.0

$50,000–99,999 0.4 0.3 0.4 0.4 0.3 0.3 0.3

$100,000–249,999 0.1 0.1 0.2 0.2 0.2 0.2 0.2

$250,000–499,999 0.1 0.1 0.1 0.1 0.1 0.1 0.1

$500,000–999,999 0.0 0.1 0.0 0.0 0.0 0.0 0.0

$1M–2.9M 0.0 0.0 0.0 0.0 0.0 0.0 0.0

$3M+ 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

©2010 IDC #222605 39

T A B L E 2 1

E M E A S e r v e r C u s t o m e r R e v e n u e b y P r i c e B a n d , 2 0 0 8 – 2 0 1 4 ( $ M )

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Revenue ($M)

$0–2,999 2,076.2 1,381.1 1,878.5 1,957.7 2,061.4 2,128.5 2,181.3 9.6

$3,000–5,999 5,244.2 4,191.4 4,262.3 4,259.8 4,139.9 4,070.2 4,076.4 -0.6

$6,000–9,999 691.6 755.2 432.8 544.5 632.6 670.6 713.9 -1.1

$10,000–24,999 1,925.1 1,434.8 1,678.6 1,809.4 1,805.9 1,756.2 1,779.4 4.4

$25,000–49,999 1,051.4 824.2 837.2 791.6 762.6 835.1 872.1 1.1

$50,000–99,999 908.8 538.8 624.4 545.9 489.4 491.5 486.5 -2.0

$100,000–249,999 1,000.2 700.2 1,491.4 1,505.4 1,369.5 1,358.0 1,311.6 13.4

$250,000–499,999 1,176.6 944.7 753.1 743.4 769.4 708.9 689.5 -6.1

$500,000–999,999 1,342.5 816.3 686.2 896.7 835.6 817.0 773.6 -1.1

$1M–2.9M 1,383.5 982.2 548.0 480.1 479.9 416.2 389.5 -16.9

$3M+ 1,567.0 968.7 664.4 661.5 567.2 516.0 475.3 -13.3

Total 18,367.3 13,537.5 13,857.0 14,195.9 13,913.4 13,768.2 13,749.0 0.3

Share (%)

$0–2,999 11.3 10.2 13.6 13.8 14.8 15.5 15.9

$3,000–5,999 28.6 31.0 30.8 30.0 29.8 29.6 29.6

$6,000–9,999 3.8 5.6 3.1 3.8 4.5 4.9 5.2

$10,000–24,999 10.5 10.6 12.1 12.7 13.0 12.8 12.9

$25,000–49,999 5.7 6.1 6.0 5.6 5.5 6.1 6.3

$50,000–99,999 4.9 4.0 4.5 3.8 3.5 3.6 3.5

$100,000–249,999 5.4 5.2 10.8 10.6 9.8 9.9 9.5

$250,000–499,999 6.4 7.0 5.4 5.2 5.5 5.1 5.0

$500,000–999,999 7.3 6.0 5.0 6.3 6.0 5.9 5.6

$1M–2.9M 7.5 7.3 4.0 3.4 3.4 3.0 2.8

$3M+ 8.5 7.2 4.8 4.7 4.1 3.7 3.5

Note: See Table 33 for key forecast assumptions.

Source: IDC, 2010

40 #222605 ©2010 IDC

T A B L E 2 2

E M E A S e r v e r S h i p m e n t s b y P r i c e B a n d , 2 0 0 8 – 2 0 1 4

2008 2009 2010 2011 2012 2013 20142009–2014 CAGR (%)

Shipments

$0–2,999 1,158,664 822,050 1,061,723 1,128,372 1,187,491 1,227,094 1,285,876 9.4

$3,000–5,999 1,248,642 988,749 968,836 1,008,459 1,042,514 1,068,280 1,112,028 2.4

$6,000–9,999 95,324 104,008 45,724 57,485 66,436 71,264 75,034 -6.3

$10,000–24,999 121,602 92,820 92,675 92,920 91,790 89,903 91,914 -0.2

$25,000–49,999 31,210 24,798 19,378 18,682 18,549 20,753 21,585 -2.7

$50,000–99,999 12,607 7,764 8,405 7,620 7,073 7,172 7,089 -1.8