industrial machinery & goods - sustainability …...3 the entity shall disclose (3) the...

TRANSCRIPT

RESOURCE TRANSFORMATION SECTOR

INDUSTRIAL MACHINERY & GOODSSustainability Accounting Standard

Sustainable Industry Classification System® (SICS®) RT-IG

Prepared by theSustainability Accounting Standards Board

October 2018

INDUSTRY STANDARD | VERSION 2018-10

© 2018 The SASB Foundation. All Rights Reserved. sasb.org

INDUSTRIAL MACHINERY & GOODSSustainability Accounting Standard

About SASB

The SASB Foundation was founded in 2011 as a not-for-profit, independent standards-setting organization. The SASB

Foundation’s mission is to establish and maintain industry-specific standards that assist companies in disclosing financially

material, decision-useful sustainability information to investors.

The SASB Foundation operates in a governance structure similar to the structure adopted by other internationally

recognized bodies that set standards for disclosure to investors, including the Financial Accounting Standards Board

(FASB) and the International Accounting Standards Board (IASB). This structure includes a board of directors (“the

Foundation Board”) and a standards-setting board (“the Standards Board” or "the SASB"). The Standards Board

develops, issues, and maintains the SASB standards. The Foundation Board oversees the strategy, finances and operations

of the entire organization, and appoints the members of the Standards Board.

The Foundation Board is not involved in setting standards, but is responsible for overseeing the Standards Board’s

compliance with the organization’s due process requirements. As set out in the SASB Rules of Procedure, the SASB’s

standards-setting activities are transparent and follow careful due process, including extensive consultation with

companies, investors, and relevant experts.

The SASB Foundation is funded by a range of sources, including contributions from philanthropies, companies, and

individuals, as well as through the sale and licensing of publications, educational materials, and other products. The SASB

Foundation receives no government financing and is not affiliated with any governmental body, the FASB, the IASB, or

any other financial accounting standards-setting body.

SUSTAINABILITY ACCOUNTING STANDARDS BOARD

1045 Sansome Street, Suite 450

San Francisco, CA 94111

415.830.9220

sasb.org

The information, text, and graphics in this publication (the “Content”) are owned by The SASB Foundation. All rights reserved. The Content may be used only for non-commercial, informational, or scholarly use, provided that all copyright and other proprietary notices related to the Content are kept intact, and that no modifications are made to the Content. The Content may not be otherwise disseminated, distributed, republished, reproduced, or modified without the prior written permission of The SASB Foundation. To requestpermission, please contact us at [email protected].

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 2

Table of Contents

Introduction....................................................................................................................................................................4

Purpose of SASB Standards.........................................................................................................................................4

Overview of SASB Standards.......................................................................................................................................4

Use of the Standards...................................................................................................................................................5

Industry Description.....................................................................................................................................................5

Sustainability Disclosure Topics & Accounting Metrics...............................................................................................6

Energy Management...................................................................................................................................................7

Employee Health & Safety...........................................................................................................................................9

Fuel Economy & Emissions in Use-phase....................................................................................................................11

Materials Sourcing.....................................................................................................................................................14

Remanufacturing Design & Services...........................................................................................................................16

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 3

INTRODUCTION

Purpose of SASB Standards The SASB’s use of the term “sustainability” refers to corporate activities that maintain or enhance the ability of the

company to create value over the long term. Sustainability accounting reflects the governance and management of a

company’s environmental and social impacts arising from production of goods and services, as well as its governance and

management of the environmental and social capitals necessary to create long-term value. The SASB also refers to

sustainability as “ESG” (environmental, social, and governance), though traditional corporate governance issues such as

board composition are not included within the scope of the SASB’s standards-setting activities.

SASB standards are designed to identify a minimum set of sustainability issues most likely to impact the operating

performance or financial condition of the typical company in an industry, regardless of location. SASB standards are

designed to enable communications on corporate performance on industry-level sustainability issues in a cost-effective

and decision-useful manner using existing disclosure and reporting mechanisms.

Businesses can use the SASB standards to better identify, manage, and communicate to investors sustainability

information that is financially material. Use of the standards can benefit businesses by improving transparency, risk

management, and performance. SASB standards can help investors by encouraging reporting that is comparable,

consistent, and financially material, thereby enabling investors to make better investment and voting decisions.

Overview of SASB Standards The SASB has developed a set of 77 industry-specific sustainability accounting standards (“SASB standards” or “industry

standards”), categorized pursuant to SASB’s Sustainable Industry Classification System® (SICS®). Each SASB standard

describes the industry that is the subject of the standard, including any assumptions about the predominant business

model and industry segments that are included. SASB standards include:

1. Disclosure topics – A minimum set of industry-specific disclosure topics reasonably likely to constitute material

information, and a brief description of how management or mismanagement of each topic may affect value creation.

2. Accounting metrics – A set of quantitative and/or qualitative accounting metrics intended to measure performance

on each topic.

3. Technical protocols – Each accounting metric is accompanied by a technical protocol that provides guidance on

definitions, scope, implementation, compilation, and presentation, all of which are intended to constitute suitable criteria

for third-party assurance.

4. Activity metrics – A set of metrics that quantify the scale of a company’s business and are intended for use in

conjunction with accounting metrics to normalize data and facilitate comparison.

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 4

Furthermore, the SASB Standards Application Guidance establishes guidance applicable to the use of all industry

standards and is considered part of the standards. Unless otherwise specified in the technical protocols contained in the

industry standards, the guidance in the SASB Standards Application Guidance applies to the definitions, scope,

implementation, compilation, and presentation of the metrics in the industry standards.

The SASB Conceptual Framework sets out the basic concepts, principles, definitions, and objectives that guide the

Standards Board in its approach to setting standards for sustainability accounting. The SASB Rules of Procedure is focused

on the governance processes and practices for standards setting.

Use of the Standards SASB standards are intended for use in communications to investors regarding sustainability issues that are likely to

impact corporate ability to create value over the long term. Use of SASB standards is voluntary. A company determines

which standard(s) is relevant to the company, which disclosure topics are financially material to its business, and which

associated metrics to report, taking relevant legal requirements into account1. In general, a company would use the SASB

standard specific to its primary industry as identified in SICS® . However, companies with substantial business in multiple

SICS® industries can consider reporting on these additional SASB industry standards.

It is up to a company to determine the means by which it reports SASB information to investors. One benefit of using

SASB standards may be achieving regulatory compliance in some markets. Other investor communications using SASB

information could be sustainability reports, integrated reports, websites, or annual reports to shareholders. There is no

guarantee that SASB standards address all financially material sustainability risks or opportunities unique to a company’s

business model.

Industry Description The Industrial Machinery & Goods industry manufactures equipment for a variety of industries including construction,

agriculture, energy, utility, mining, manufacturing, automotive, and transportation. Products include engines, earth-

moving equipment, trucks, tractors, ships, industrial pumps, locomotives, and turbines. Machinery manufacturers utilize

large amounts of raw materials for production, including steel, plastics, rubber, paints, and glass. Manufacturers may also

perform the machining and casting of parts before final assembly. Demand in the industry is closely tied to industrial

production, while government emissions standards and customer demand are driving innovations to improve energy

efficiency and limit air emissions during product use.

1 Legal Note: SASB standards are not intended to, and indeed cannot, replace any legal or regulatory requirements that may be applicable to a reporting entity’s operations.

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 5

SUSTAINABILITY DISCLOSURE TOPICS & ACCOUNTING METRICS

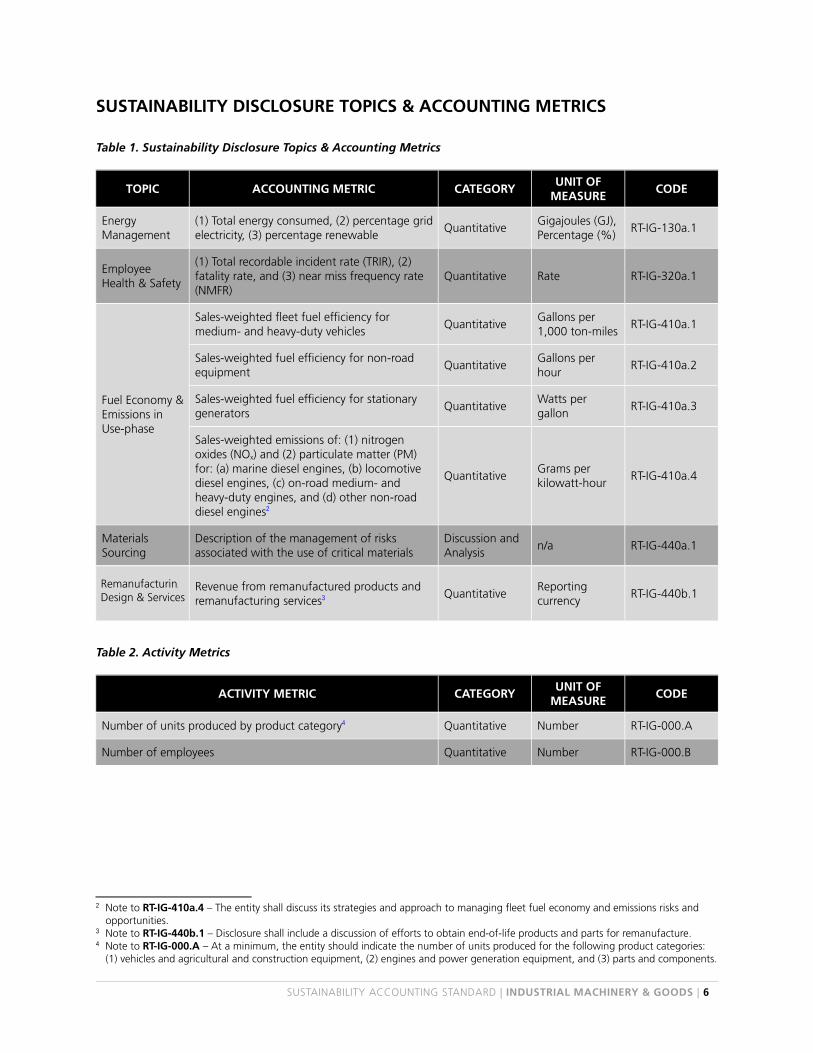

Table 1. Sustainability Disclosure Topics & Accounting Metrics

TOPIC ACCOUNTING METRIC CATEGORYUNIT OF

MEASURECODE

Energy Management

(1) Total energy consumed, (2) percentage gridelectricity, (3) percentage renewable

QuantitativeGigajoules (GJ), Percentage (%)

RT-IG-130a.1

Employee Health & Safety

(1) Total recordable incident rate (TRIR), (2) fatality rate, and (3) near miss frequency rate (NMFR)

Quantitative Rate RT-IG-320a.1

Fuel Economy &Emissions in Use-phase

Sales-weighted fleet fuel efficiency for medium- and heavy-duty vehicles

QuantitativeGallons per 1,000 ton-miles

RT-IG-410a.1

Sales-weighted fuel efficiency for non-road equipment

QuantitativeGallons per hour

RT-IG-410a.2

Sales-weighted fuel efficiency for stationary generators

QuantitativeWatts per gallon

RT-IG-410a.3

Sales-weighted emissions of: (1) nitrogen oxides (NOx) and (2) particulate matter (PM) for: (a) marine diesel engines, (b) locomotive diesel engines, (c) on-road medium- and heavy-duty engines, and (d) other non-road diesel engines2

QuantitativeGrams per kilowatt-hour

RT-IG-410a.4

Materials Sourcing

Description of the management of risks associated with the use of critical materials

Discussion and Analysis

n/a RT-IG-440a.1

Remanufacturing Design & Services

Revenue from remanufactured products and remanufacturing services3

QuantitativeReporting currency

RT-IG-440b.1

Table 2. Activity Metrics

ACTIVITY METRIC CATEGORYUNIT OF

MEASURECODE

Number of units produced by product category4 Quantitative Number RT-IG-000.A

Number of employees Quantitative Number RT-IG-000.B

2 Note to RT-IG-410a.4 – The entity shall discuss its strategies and approach to managing fleet fuel economy and emissions risks and opportunities.

3 Note to RT-IG-440b.1 – Disclosure shall include a discussion of efforts to obtain end-of-life products and parts for remanufacture.4 Note to RT-IG-000.A – At a minimum, the entity should indicate the number of units produced for the following product categories:

(1) vehicles and agricultural and construction equipment, (2) engines and power generation equipment, and (3) parts and components.

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 6

Energy Management

Topic Summary Energy is a critical input in industrial machinery manufacturing. Purchased electricity represents the largest share of energy

expenditures in the industry, followed by purchased fuels. The type of energy used, magnitude of consumption, and

energy management strategies depends on the type of products manufactured. A company’s energy mix, including the

use of electricity generated on-site, grid-sourced electricity, and the use of alternative energy, can play an important role

in influencing the cost and reliability of energy supply, and ultimately affect the company’s cost structure and regulatory

risk.

Accounting Metrics

RT-IG-130a.1. (1) Total energy consumed, (2) percentage grid electricity, (3) percentage renewable

1 The entity shall disclose (1) the total amount of energy it consumed as an aggregate figure, in gigajoules (GJ).

1.1 The scope of energy consumption includes energy from all sources, including energy purchased from sources

external to the entity and energy produced by the entity itself (self-generated). For example, direct fuel usage,

purchased electricity, and heating, cooling, and steam energy are all included within the scope of energy

consumption.

1.2 The scope of energy consumption includes only energy directly consumed by the entity during the reporting

period.

1.3 In calculating energy consumption from fuels and biofuels, the entity shall use higher heating values (HHV),

also known as gross calorific values (GCV), which are directly measured or taken from the Intergovernmental

Panel on Climate Change (IPCC), the U.S. Department of Energy (DOE), or the U.S. Energy Information

Administration (EIA).

2 The entity shall disclose (2) the percentage of energy it consumed that was supplied from grid electricity.

2.1 The percentage shall be calculated as purchased grid electricity consumption divided by total energy

consumption.

3 The entity shall disclose (3) the percentage of energy it consumed that is renewable energy.

3.1 Renewable energy is defined as energy from sources that are replenished at a rate greater than or equal to

their rate of depletion, such as geothermal, wind, solar, hydro, and biomass.

3.2 The percentage shall be calculated as renewable energy consumption divided by total energy consumption.

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 7

3.3 The scope of renewable energy includes renewable fuel the entity consumed, renewable energy the entity

directly produced, and renewable energy the entity purchased, if purchased through a renewable power

purchase agreement (PPA) that explicitly includes renewable energy certificates (RECs) or Guarantees of Origin

(GOs), a Green e Energy Certified utility or supplier program, or other green power products that explicitly ‐

include RECs or GOs, or for which Green e Energy Certified RECs are paired with grid electricity.‐

3.3.1 For any renewable electricity generated on-site, any RECs and GOs must be retained (i.e., not sold) and

retired or cancelled on behalf of the entity in order for the entity to claim them as renewable energy.

3.3.2 For renewable PPAs and green power products, the agreement must explicitly include and convey that

RECs and GOs be retained or replaced and retired or cancelled on behalf of the entity in order for the

entity to claim them as renewable energy.

3.3.3 The renewable portion of the electricity grid mix that is outside of the control or influence of the entity

is excluded from the scope of renewable energy.

3.4 For the purposes of this disclosure, the scope of renewable energy from hydro and biomass sources is limited

to the following:

3.4.1 Energy from hydro sources is limited to those that are certified by the Low Impact Hydropower Institute

or that are eligible for a state Renewable Portfolio Standard;

3.4.2 Energy from biomass sources is limited to materials certified to a third-party standard (e.g., Forest

Stewardship Council, Sustainable Forest Initiative, Programme for the Endorsement of Forest

Certification, or American Tree Farm System), materials considered eligible sources of supply according

to the Green-e Framework for Renewable Energy Certification, Version 1.0 (2017) or Green-e regional

standards, and/or materials that are eligible for an applicable state renewable portfolio standard.

4 The entity shall apply conversion factors consistently for all data reported under this disclosure, such as the use of

HHVs for fuel usage (including biofuels) and conversion of kilowatt hours (kWh) to GJ (for energy data including

electricity from solar or wind energy).

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 8

Employee Health & Safety

Topic Summary Employees in industrial machinery manufacturing facilities face health and safety risks from exposure to heavy machinery,

moving equipment, and electrical hazards, among others. Creating an effective safety culture is critical to proactively

mitigate safety incidents, which could result in higher healthcare costs, litigation, and work disruption. By implementing

strong safety protocols, including incident reporting and investigation, and promoting a culture of safety, companies can

minimize safety-related expenses and potentially improve productivity in the long term.

Accounting Metrics

RT-IG-320a.1. (1) Total recordable incident rate (TRIR), (2) fatality rate, and (3) near miss frequency rate (NMFR)

1 The entity shall disclose its total recordable incident rate (TRIR) for work-related injuries and illnesses.

1.1 An injury or illness is considered a recordable incident if it results in any of the following: death, days away

from work, restricted work or transfer to another job, medical treatment beyond first aid, or loss of

consciousness. Additionally, a significant injury or illness diagnosed by a physician or other licensed health care

professional is considered a recordable incident, even if it does not result in death, days away from work,

restricted work or job transfer, medical treatment beyond first aid, or loss of consciousness. This definition is

derived from U.S. 29 CFR 1904.7.

1.2 The U.S. Occupational Safety and Health Administration (OSHA) provides additional resources for determining

if injuries or illnesses are considered recordable incidents in its guidance for OSHA Forms 300, 300A, and 301.

2 The entity shall disclose its fatality rate for work-related fatalities.

3 The entity shall disclose its near miss frequency rate (NMFR) for work-related near misses.

3.1 A near miss is defined as an unplanned incident in which no property or environmental damage or personal

injury occurred, but where damage or personal injury easily could have occurred but for a slight circumstantial

shift.

3.2 The U.S. National Safety Council (NSC) provides guidance on implementing near miss reporting, including in,

“Near Miss Reporting Systems.”

3.3 The entity may disclose its process for classifying, identifying, and reporting near misses.

4 Rates shall be calculated as: (statistic count x 200,000) / hours worked

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 9

4.1 The U.S. Bureau of Labor Statistics (BLS) provides additional guidance for the calculation of rates in, “How to

Compute a Firm’s Incidence Rate for Safety Management” and “Incidence Rate Calculator and Comparison

Tool.”

5 The scope of disclosure includes work-related incidents only.

5.1 OSHA guidance for Forms 300, 300A, and 301 provides guidance on determining whether an incident is

work-related, as well as definitions for exemptions for incidents that occur in the work environment but are

not work-related.

6 The scope of disclosure includes all employees regardless of employee location and type of employment, such as full-

time, part-time, direct, contract, executive, labor, salary, hourly, and seasonal employees.

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 10

Fuel Economy & Emissions in Use-phase

Topic Summary Many of the Industrial Machinery & Goods industry’s products are powered by fossil fuels and therefore release

greenhouse gases (GHGs) and other air emissions during use. Customer preferences for improved fuel economy

combined with regulations addressing emissions are increasing the demand for energy-efficient and lower-emission

products in the industry. As such, companies that develop products with these characteristics may be well-positioned to

capture expanding market share, reduce regulatory risk, and improve brand value.

Accounting Metrics

RT-IG-410a.1. Sales-weighted fleet fuel efficiency for medium- and heavy-duty vehicles

1 The entity shall disclose its sales-weighted average fleet fuel efficiency for medium- and heavy-duty vehicles, where:

1.1 Fleet fuel efficiency is defined as the average fuel economy of its medium- and heavy-duty commercial

vehicles, weighted by the number of each sold during the reporting period and measured in gallons per 1,000

ton-miles.

1.2 The scope of disclosure includes vehicles in the fleet that weigh 8,500 pounds or more, and which are covered

under the U.S. Heavy Duty (HD) National Program, including combination tractors (commonly known as semi-

trucks), heavy-duty pickup trucks and vans, and vocational vehicles.

1.3 Where fleet averages are calculated by model year for regulatory purposes, the entity shall use these

performance data.

1.4 In the absence of regulatory guidance on calculating a fleet average, the entity shall calculate performance

based on the fuel economy of vehicles sold during the reporting period, weighted by sales volume.

2 The entity shall disclose the sales-weighted fuel efficiency requirement for its medium- and heavy-duty vehicles,

pursuant to U.S. HD National Program Fuel Consumption Standards, as issued and regulated by the U.S. National

Highway Traffic Safety Administration (NHTSA) and U.S. Environmental Protection Agency (EPA).

RT-IG-410a.2. Sales-weighted fuel efficiency for non-road equipment

1 The entity shall disclose its sales-weighted average fuel efficiency for its non-road equipment and vehicles, where:

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 11

1.1 Fuel efficiency is defined as the average fuel economy of its non-road equipment, weighted by the number of

each unit sold during the reporting period and measured in gallons of fuel consumed per hour of operation

(gallons per hour).

1.1.1 In calculating gallons per hour, the entity shall use the model-rated fuel efficiency value for each piece

of equipment where available.

1.1.2 Where model-rated fuel efficiency values are not available, the entity shall calculate a gallons-per-hour

operational efficiency for the equipment, assuming normal, reasonable operating conditions (e.g., for

load factor, speed, and environmental conditions).

1.2 Non-road equipment includes, but is not limited to, excavators and other construction equipment, farm

tractors and other agricultural equipment, heavy forklifts, airport ground service equipment, and utility

equipment such as generators, pumps, and compressors.

RT-IG-410a.3. Sales-weighted fuel efficiency for stationary generators

1 The entity shall disclose the sales-weighted average fuel efficiency of its stationary generators, where:

1.1 Sales-weighted fuel efficiency is the average fuel efficiency of stationary generators sold during the reporting

period, measured in watts per gallon.

2 Sales-weighted fuel efficiency is calculated as the harmonic mean of design fuel efficiency in watts per gallon, where:

2.1 The harmonic mean captures the average amount of fuel needed by each generator to produce a given

amount of power.

2.2 The harmonic mean is the reciprocal of the average of the reciprocal values.

RT-IG-410a.4. Sales-weighted emissions of: (1) nitrogen oxides (NOx) and (2) particulate matter (PM) for: (a) marine diesel engines, (b) locomotive diesel engines, (c) on-road medium- and heavy-duty engines, and (d) other non-road diesel engines

1 The entity shall disclose the sales-weighted average emissions of (1) nitrogen oxides (NOx) and (2) particulate matter

(PM) for each of the following product categories: (a) marine diesel engines, (b) locomotive diesel engines, (c) on-

road heavy-duty engines, and (d) other non-road diesel engines, where:

1.1 Emissions are calculated as the average emissions of (1) NOx and (2) PM for engines, weighted by the number

of each sold during the reporting period and measured in grams per kilowatt hour.

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 12

1.2 Marine diesel engines are defined as those that are addressed within the scope of U.S. 40 CFR Part 1042, 40

CFR Part 94, 40 CFR Part 89, or non-U.S. equivalent.

1.3 Locomotive diesel engines are defined as those that are addressed within the scope of U.S. 40 CFR Part 1033,

or non-U.S. equivalent.

1.4 On-road heavy-duty engines are defined as those that are addressed within the scope of U.S. 40 CFR Chapter

1 Subchapter C Part 86, or non-U.S. equivalent.

1.5 Other non-road diesel engines are defined as those that are addressed within the scope of U.S. 40 CFR Part

1039, or non-U.S. equivalent, and typically include excavators and other construction equipment, farm tractors

and other agricultural equipment, heavy forklifts, airport ground service equipment, and utility equipment

such as generators, pumps, and compressors.

1.6 Emissions shall be calculated according to the test method described in U.S. 40 CFR Part 1065, or non-U.S.

equivalent.

1.7 The entity may disclose if any products do not meet current emission standards established in the above-

referenced U.S. 40 CFR Part 1042, 40 CFR Part 94, and 40 CFR Part 89 for marine diesel engines; 40 CFR Part

1033 for locomotive diesel engines; 40 CFR Part 86 Subpart A for heavy-duty on-road engines; 40 CFR Part

1039 for other non-road diesel engines, or non-U.S. equivalents.

2 The entity may discuss its progress toward, and readiness for, future U.S. federal- and state-level, or non-U.S.

equivalent, emissions standards that could affect its products.

Note to RT-IG-410a.4

1 The entity shall discuss its strategies and approach to managing fleet fuel economy and emissions risks and

opportunities.

2 Relevant aspects of the approach and strategy to discuss include improvements to existing products and

technologies, the introduction of new technologies, research and development efforts into advanced technologies,

and partnerships with peers, academic institutions, and/or customers (including governmental customers).

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 13

Materials Sourcing

Topic Summary Industrial machinery companies are exposed to supply chain risks when critical materials are used in products. Companies

in the industry manufacture products using critical materials with few or no available substitutes, many of which are

sourced from deposits concentrated in only a few countries, which are subject to geopolitical uncertainty. Companies in

this industry also face competition due to increasing global demand for these materials from other sectors, which can

result in price increases and supply risks. Companies that are able to limit the use of critical materials through use of

alternatives, as well as secure their supply, can mitigate the potential for financial impacts stemming from supply

disruptions and volatile input prices.

Accounting Metrics

RT-IG-440a.1. Description of the management of risks associated with the use of critical materials

1 The entity shall describe its strategic approach to managing its risks associated with the use of critical materials in its

products, including physical limits on availability and access, changes in price, and regulatory and reputational risks,

where:

1.1 A critical material is defined as a material that is both essential in use and subject to the risk of supply

restriction. This definition is derived from the U.S. National Research Council of the National Academies’

Minerals, Critical Minerals, and the U.S. Economy .

1.2 Examples of critical materials include, but are not limited to, the following as defined by the National Research

Council:

1.2.1 Antimony, cobalt, fluorspar, gallium, germanium, graphite, indium, magnesium, niobium, tantalum,

and tungsten;

1.2.2 Platinum group metals (platinum, palladium, iridium, rhodium, ruthenium, and osmium); and

1.2.3 Rare earth elements, which include yttrium, scandium, lanthanum, and the lanthanides (cerium,

praseodymium, neodymium, promethium, samarium, europium, gadolinium, terbium, dysprosium,

holmium, erbium, thulium, ytterbium, and lutetium).

2 The entity shall identify the critical materials that present a significant risk to its operations, the type of risk(s) they

represent, and the strategies the entity uses to mitigate the risk(s).

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 14

2.1 Relevant strategies may include diversification of suppliers, stockpiling of materials, development or

procurement of alternative and substitute materials, and investments in recycling technology for critical

materials.

3 All disclosure shall be sufficient such that it is specific to the risks the entity faces but disclosure itself would not

compromise the entity‘s ability to maintain confidential information.

3.1 For example, if an entity determines not to identify a specific critical material that presents a significant risk to

its operations due to competitive harm that could result from the disclosure, the entity shall disclose the

existence of such risk(s), the type of risk(s), and the strategies used to mitigate the risk(s), but is not required to

disclose the relevant critical material.

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 15

Remanufacturing Design & Services

Topic Summary Industrial machinery and goods manufacturing uses large quantities of steel, iron, aluminum, glass, plastics, and other

materials. Remanufacturing of industrial machinery systems (called "cores") is an opportunity for industrial machinery

companies to limit the amount of raw materials needed to produce new machinery, as well as the time and other

resources required to produce finished goods. Remanufactured products can also create value from products otherwise

destined for disposal or recycling. Industrial machinery companies can achieve cost savings by reusing end-of-life parts to

build remanufactured machines, which may be resold to customers. Thus, remanufacturing in process and design can

reduce demand for raw materials, reduce manufacturing costs, and create new sales channels.

Accounting Metrics

RT-IG-440b.1. Revenue from remanufactured products and remanufacturing services

1 The entity shall disclose the amount of revenue from products that are remanufactured and services associated with

remanufacturing goods, where:

1.1 A remanufactured product is defined as an end-of-life product or component (i.e., one that was previously

sold, worn, or non-functional) that has undergone an industrial process to be returned to original working

condition (i.e., is considered “like new”).

1.2 Remanufacturing services are defined as providing the service of repairing, restoring, and/or remanufacturing

end-of-life goods to original working condition.

2 The scope of disclosure excludes servicing of products that are in-warranty and have been collected for repairs.

Note to RT-IG-440b.1

1 The entity shall discuss its initiatives employed to obtain end-of-life products and parts for remanufacturing, including

product take-back programs.

2 Relevant disclosures include customer and supplier engagement efforts, equipment servicing or exchange programs,

and other incentives to encourage end-of-life parts remanufacturing, such as dealer deposits that are refunded when

used parts or products (also referred to as “cores”) are returned to the manufacturer within the specified timeframe.

SUSTAINABILITY ACCOUNTING STANDARD | INDUSTRIAL MACHINERY & GOODS | 16

SUSTAINABILITY ACCOUNTING STANDARDS BOARD

1045 Sansome Street, Suite 450

San Francisco, CA 94111

415.830.9220

sasb.org