indonesia economic developments and outlook - world...

TRANSCRIPT

January 25, 2017

Indonesia Economic Developments and Outlook

Hans Anand Beck

Key takeawaysIndonesia showed resilience as volatility returned to

global financial markets

Thanks to strong fundamentals and macro-fiscal

management, Indonesia weathered recent volatility

better than many peers:

Efficiencies in the 2016 budget and a more

credible 2017 budget

Low inflation; a pause in accommodative

monetary policy

Policy packages have made it easier to do

business

However, risks have intensified and remain tilted to

the downside

External, as well as domestic risks remain

Global policy uncertainty, trade deals and

revenue collection

This emphasizes the importance of sustaining

reform momentum to mitigate risk and foster

inclusive growth

Fiscal reforms to spend with greater impact, and

stem the decline in revenues

Investment climate reforms to accelerate private

investment

Investing in human capital through education

0

2

4

6

8

2014 2015 2016 2017 2018

Indonesia remains resilient to sluggish global growth

3Source: World Bank Global Economic Prospects

Economic growth (Annual percentage change)

Forecasts

World

Indonesia

Philippines

East Asia ex China

Malaysia

Thailand

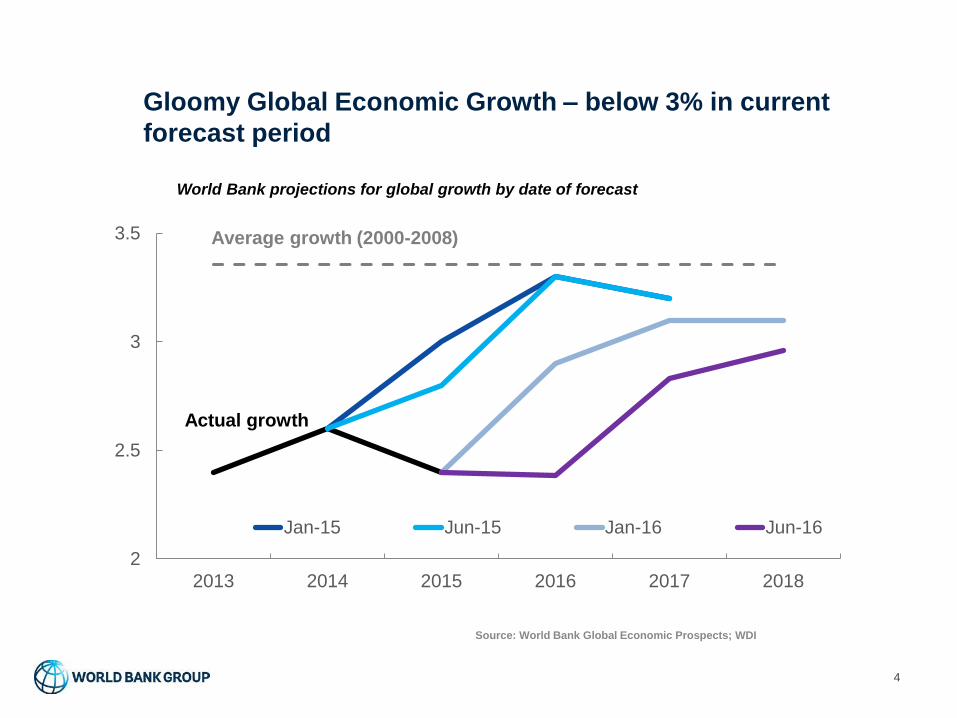

Gloomy Global Economic Growth – below 3% in current

forecast period

4

Source: World Bank Global Economic Prospects; WDI

World Bank projections for global growth by date of forecast

2

2.5

3

3.5

2013 2014 2015 2016 2017 2018

Jan-15 Jun-15 Jan-16 Jun-16

Average growth (2000-2008)

Actual growth

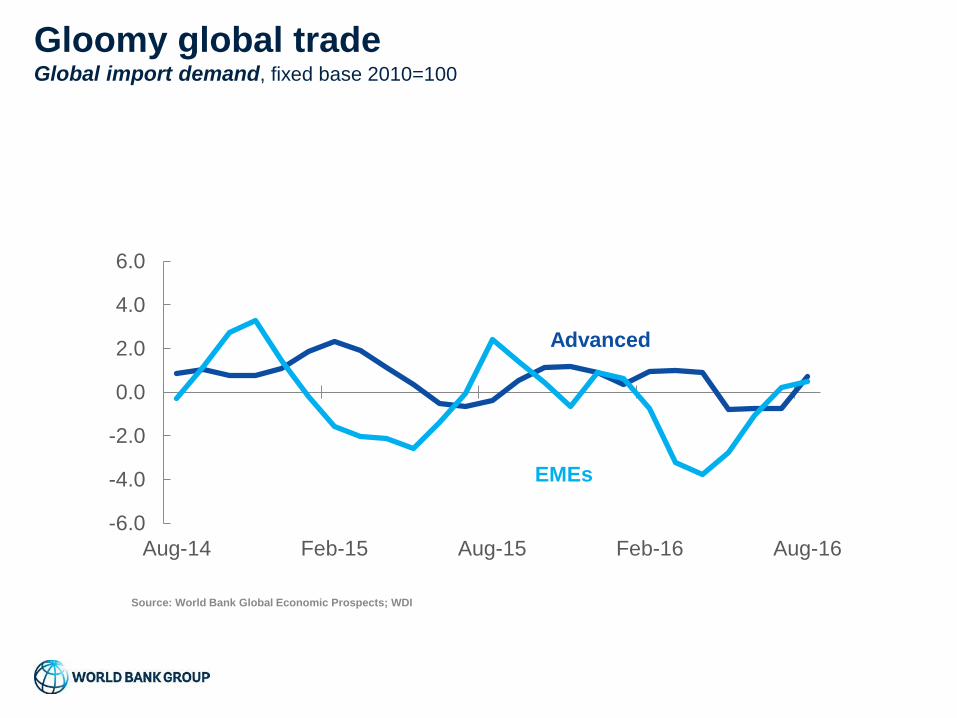

Gloomy global tradeGlobal import demand, fixed base 2010=100

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

Aug-14 Feb-15 Aug-15 Feb-16 Aug-16

Advanced

EMEs

Source: World Bank Global Economic Prospects; WDI

85

90

95

100

105

Apr-2016 Jun-2016 Aug-2016 Oct-2016 Dec-2016

Malaysia Philippines Thailand Singapore Indonesia EMCI

Indonesia remains resilient to global financial volatility

6

Exchange rates against USD (index, April 1=100)

Source: CEIC; WB Staff Calculation

US electionBrexit

Exports in the region Depend On Global Growth Outlook

(Gross exports, percent of GDP, 2015)

0

10

20

30

40

50

60

70

80C

am

bo

dia

Fiji

Ind

on

esia

La

o P

DR

Ma

laysia

Mo

ngo

lia

Myan

mar

Papu

a N

ew

Guin

ea

Phili

ppin

es

Solo

mon

Isla

nds

Tha

iland

Vie

tna

m

China Emerging and dev. Asia excl. China

Emerging and dev. excl. EAP European Union

Japan United States

Source: World Bank Global EAP Update November 2016

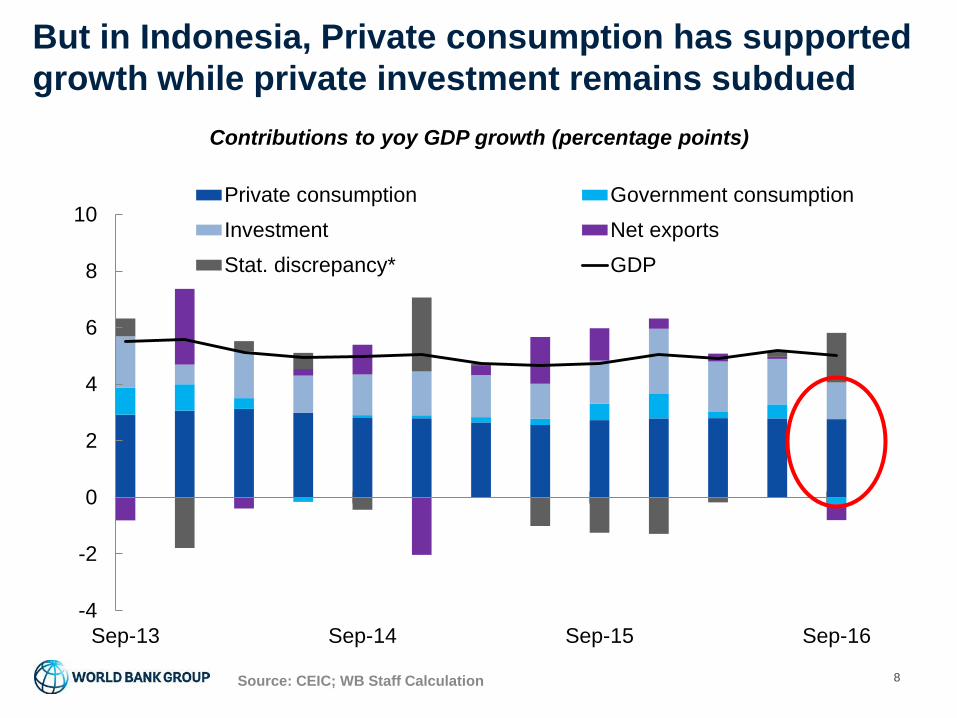

But in Indonesia, Private consumption has supported

growth while private investment remains subdued

8

Contributions to yoy GDP growth (percentage points)

Source: CEIC; WB Staff Calculation

-4

-2

0

2

4

6

8

10

Sep-13 Sep-14 Sep-15 Sep-16

Private consumption Government consumption

Investment Net exports

Stat. discrepancy* GDP

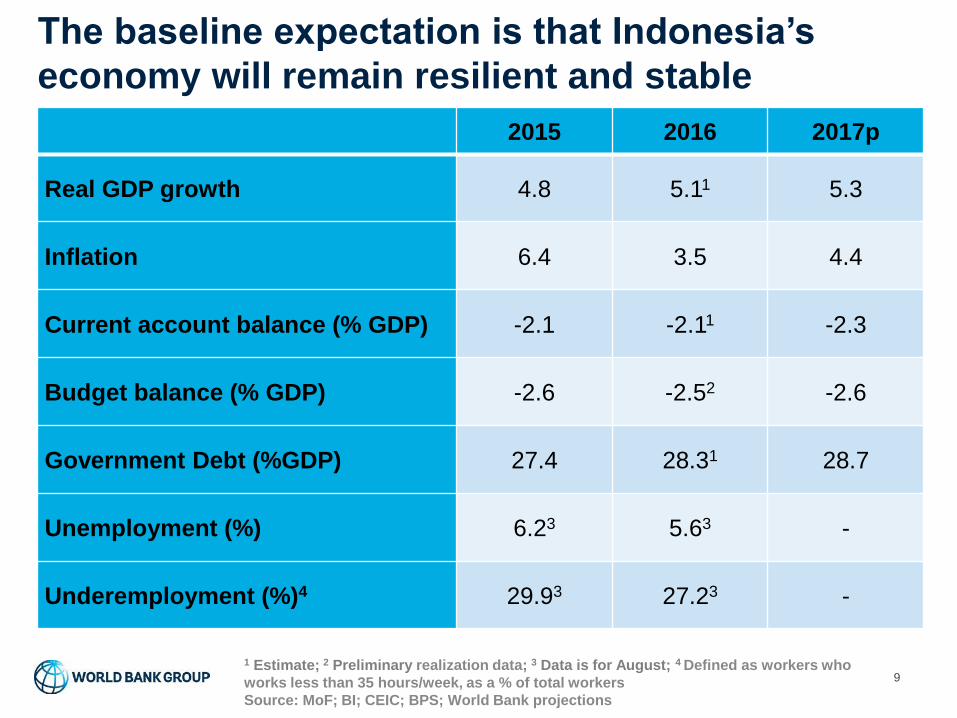

The baseline expectation is that Indonesia’s

economy will remain resilient and stable

9

1 Estimate; 2 Preliminary realization data; 3 Data is for August; 4 Defined as workers who

works less than 35 hours/week, as a % of total workers

Source: MoF; BI; CEIC; BPS; World Bank projections

2015 2016 2017p

Real GDP growth 4.8 5.11 5.3

Inflation 6.4 3.5 4.4

Current account balance (% GDP) -2.1 -2.11 -2.3

Budget balance (% GDP) -2.6 -2.52 -2.6

Government Debt (%GDP) 27.4 28.31 28.7

Unemployment (%) 6.23 5.63 -

Underemployment (%)4 29.93 27.23 -

10

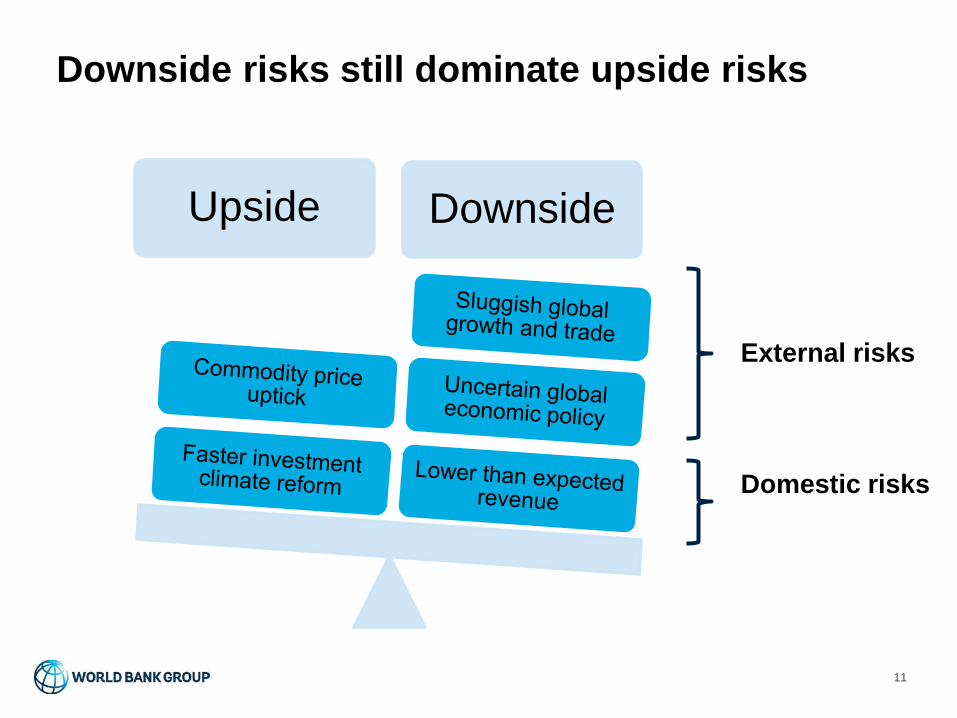

But downside risks have intensified

Indonesia remains resilient

Sustaining reform momentum is essential to withstand risks

and promote inclusive growth

Downside risks still dominate upside risks

11

Upside Downside

External risks

Domestic risks

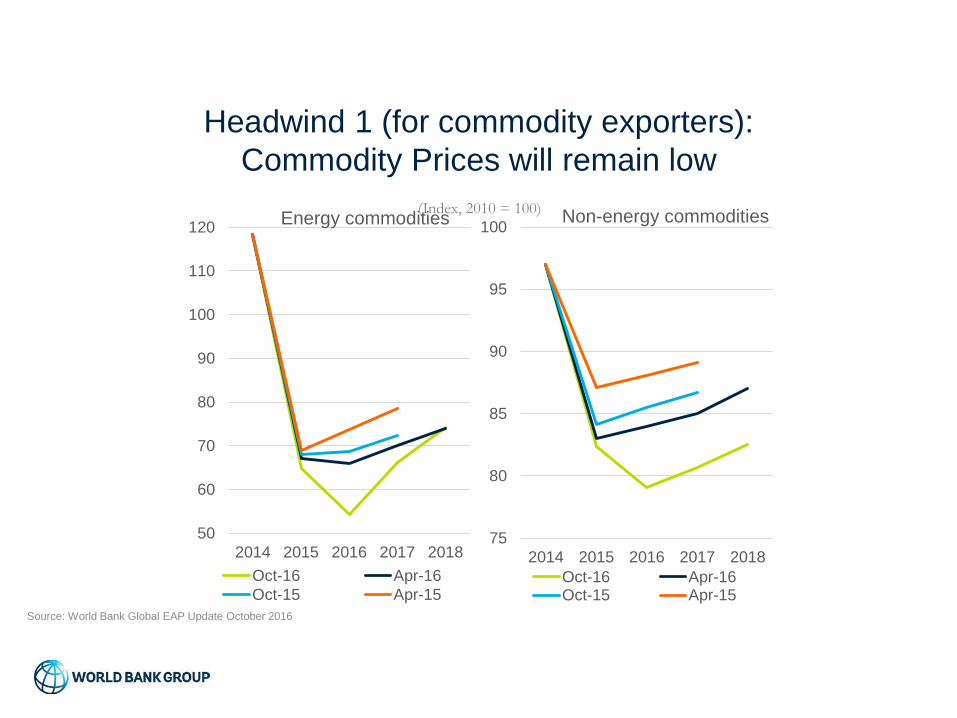

Headwind 1 (for commodity exporters):

Commodity Prices will remain low

(Index, 2010 = 100)

50

60

70

80

90

100

110

120

2014 2015 2016 2017 2018

Energy commodities

Oct-16 Apr-16

Oct-15 Apr-15

75

80

85

90

95

100

2014 2015 2016 2017 2018

Non-energy commodities

Oct-16 Apr-16Oct-15 Apr-15

Source: World Bank Global EAP Update October 2016

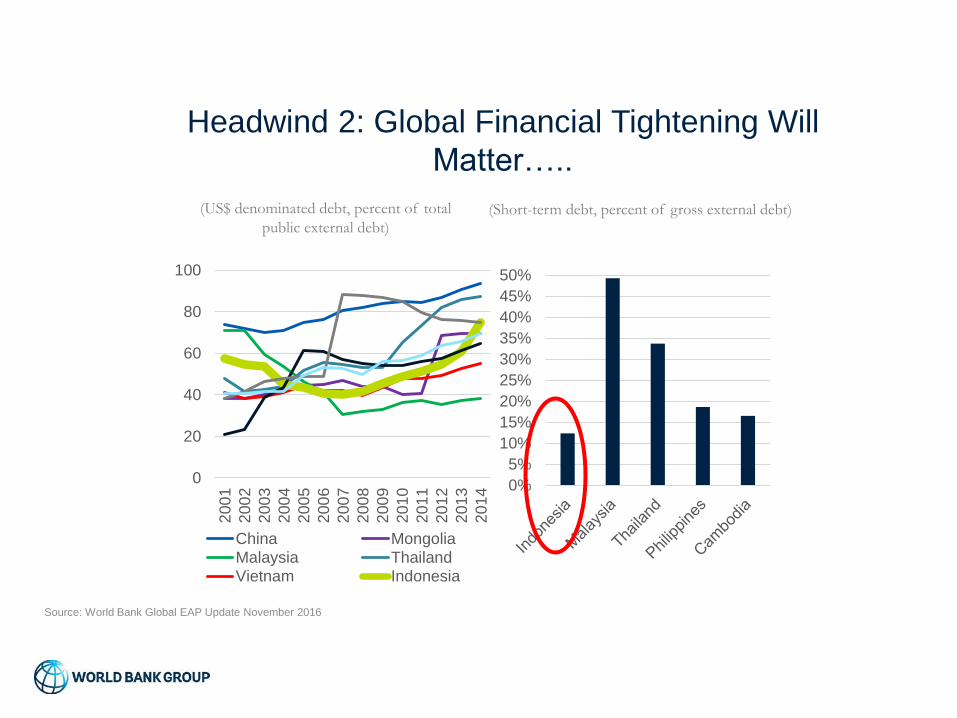

Headwind 2: Global Financial Tightening Will

Matter…..

0

20

40

60

80

100

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

China Mongolia

Malaysia ThailandVietnam Indonesia

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

(US$ denominated debt, percent of total

public external debt)(Short-term debt, percent of gross external debt)

Source: World Bank Global EAP Update November 2016

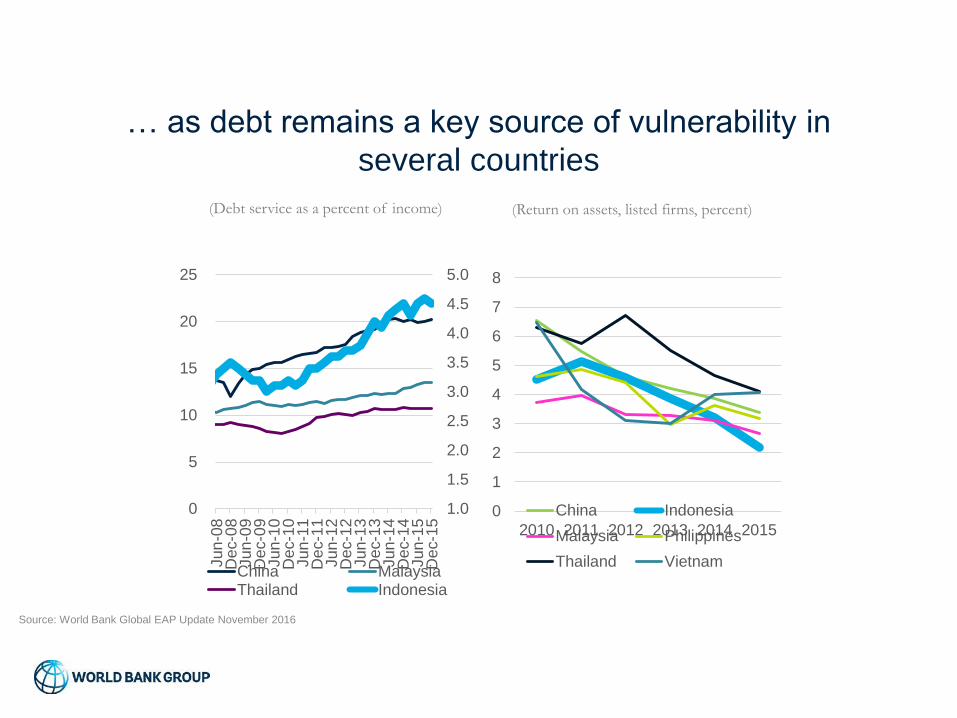

… as debt remains a key source of vulnerability in

several countries

0

1

2

3

4

5

6

7

8

2010 2011 2012 2013 2014 2015

China Indonesia

Malaysia Philippines

Thailand Vietnam

(Debt service as a percent of income) (Return on assets, listed firms, percent)

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0

5

10

15

20

25

Jun

-08

Dec-0

8Jun

-09

Dec-0

9Jun

-10

Dec-1

0Jun

-11

Dec-1

1Jun

-12

Dec-1

2Jun

-13

Dec-1

3Jun

-14

Dec-1

4Jun

-15

Dec-1

5

China MalaysiaThailand Indonesia

Source: World Bank Global EAP Update November 2016

15

Sustaining reform momentum is essential to withstand risks

and promote inclusive growth

But downside risks have intensified

Indonesia remains resilient

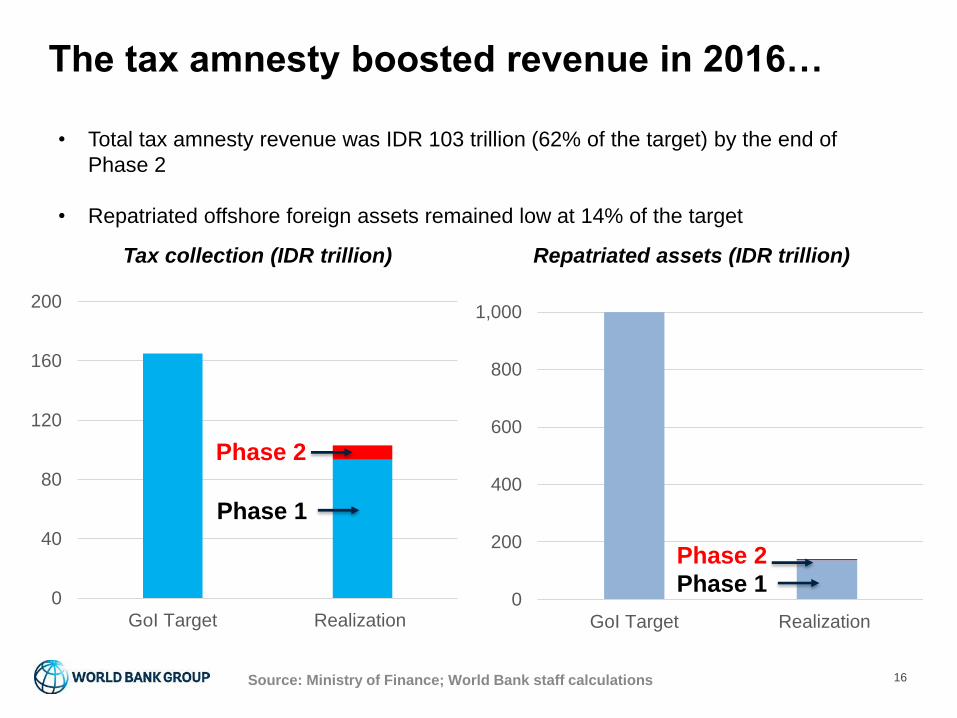

16Source: Ministry of Finance; World Bank staff calculations

The tax amnesty boosted revenue in 2016…

• Total tax amnesty revenue was IDR 103 trillion (62% of the target) by the end of

Phase 2

• Repatriated offshore foreign assets remained low at 14% of the target

Repatriated assets (IDR trillion)Tax collection (IDR trillion)

0

200

400

600

800

1,000

GoI Target Realization

0

40

80

120

160

200

GoI Target Realization

Phase 2

Phase 2

Phase 1

Phase 1

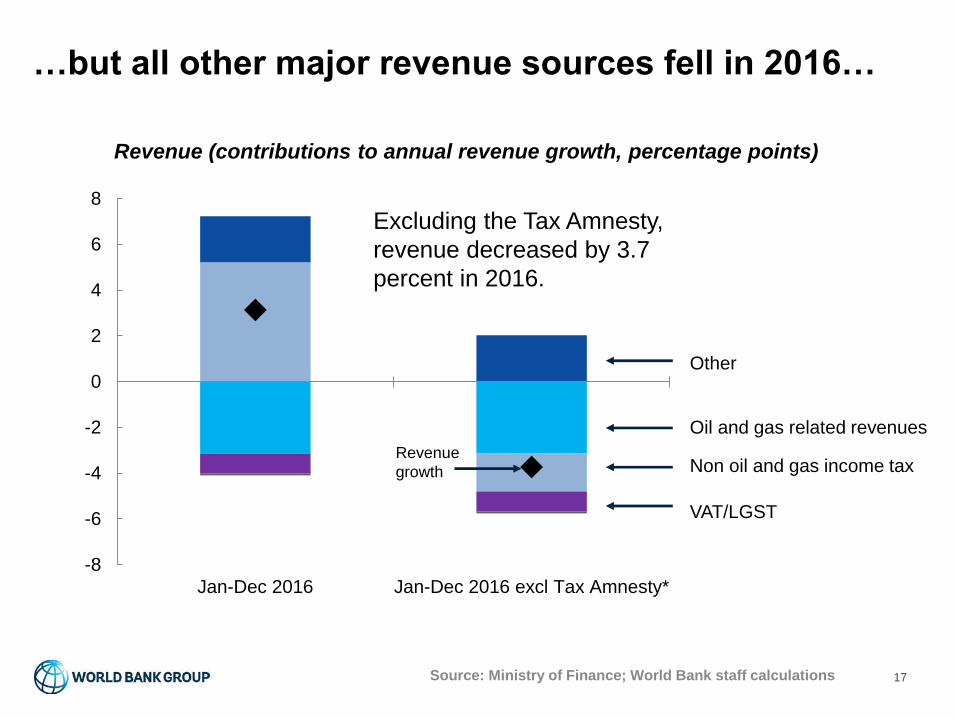

17Source: Ministry of Finance; World Bank staff calculations

…but all other major revenue sources fell in 2016…

Other

-8

-6

-4

-2

0

2

4

6

8

Jan-Dec 2016 Jan-Dec 2016 excl Tax Amnesty*

Excluding the Tax Amnesty,

revenue decreased by 3.7

percent in 2016.

Revenue (contributions to annual revenue growth, percentage points)

Non oil and gas income tax

Oil and gas related revenues

VAT/LGST

Revenue

growth

18Source: Ministry of Finance; World Bank staff calculations

...emphasizing the need to accelerate revenue reform

• VAT e-filing and e-invoicing

• Formation of Tim Reformasi Perpajakan (Tax Reform Team)

Implemented

• Use new Tax Amnesty data to improve compliance and expand tax base

• Reform VAT law (reduce exemptions, lower VAT threshold)

• Income tax law

• Strengthen measures to reduce base erosion and profit shifting (BEPS)

• Reform tax administration (KUP law, business processes and IT)

Ongoing

-2.7

-2.6

-2.5

-2.4

-2.30

500

1,000

1,500

2,000

2,500

Revised Budget Actual (Prelim) Budget World Bank

Revenues Expenditures Budget Deficit (RHS, inverse)

2016 2017

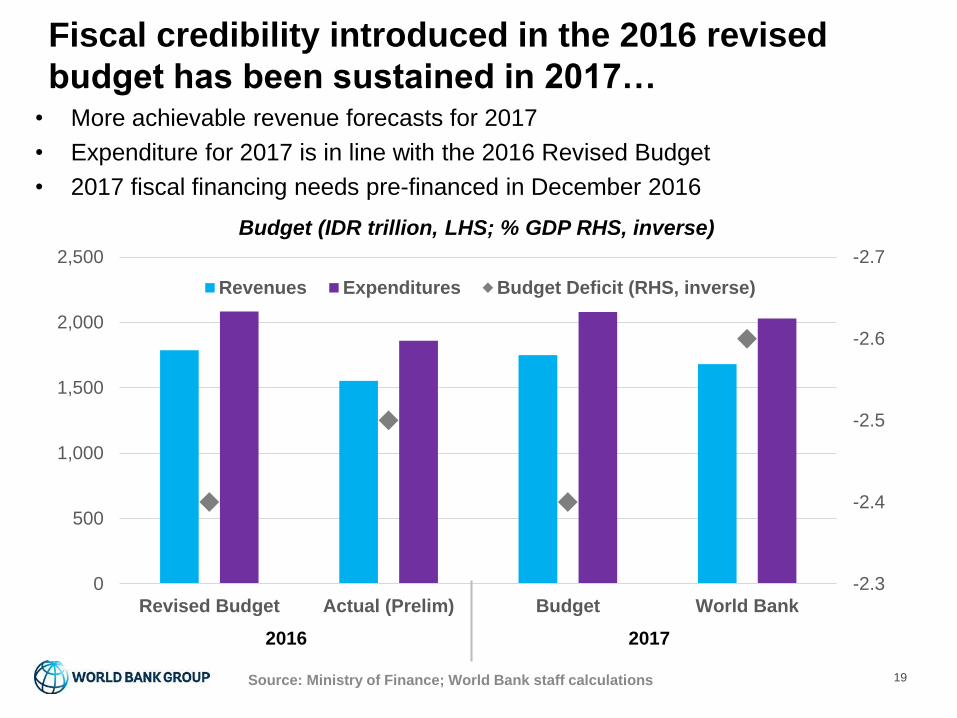

19Source: Ministry of Finance; World Bank staff calculations

• More achievable revenue forecasts for 2017

• Expenditure for 2017 is in line with the 2016 Revised Budget

• 2017 fiscal financing needs pre-financed in December 2016

Fiscal credibility introduced in the 2016 revised

budget has been sustained in 2017…

Budget (IDR trillion, LHS; % GDP RHS, inverse)

20Source: Ministry of Finance; World Bank staff calculations

• Capital expenditure fell by 23% in

2016:

• Base effect

• Several projects deferred

• The government maintained lower

subsidy spending in 2016 and in

the 2017 Budget, along with other

improvements to the quality of

spending

• improved targeting of energy

subsidies

• mandated higher infrastructure

spending at the sub-national

level

Government expenditure (IDR trillion)

…with room for improvements to the quality of

spending, particularly capital spending…

-

50

100

150

200

250

300

2014 2015 2016 2017

Capital Subsidies

…and in other priority sectors

21

Government expenditure (% GDP)

Note: Infrastructure and social assistance data use World Bank sectoral definitions

Source: Ministry of Finance; World Bank staff calculations

0 1 2 3 4 5

Infrastructure

Health

Social assistance

Subsidies

Personnel (CG)

2016 Revised Budget 2017 approved Budget World Bank target (2020)

22Source: World Bank

Sustain investment climate reform momentum

• The investment climate is improving - Indonesia was a top 10 reformer in

the 2017 Doing Business Report

• But more needs to be done, especially to meet the government’s target

Doing Business rank of 30 in 2019

• Need to move beyond “quick win” reforms and implement medium-term

structural reforms

Overall ranking 106 91

Starting a business (days) 48 25

Getting electricity (days) 76 56

Compliance for exporting (cost, $) 170 139

DB 2016 DB 2017

30

Target 2019

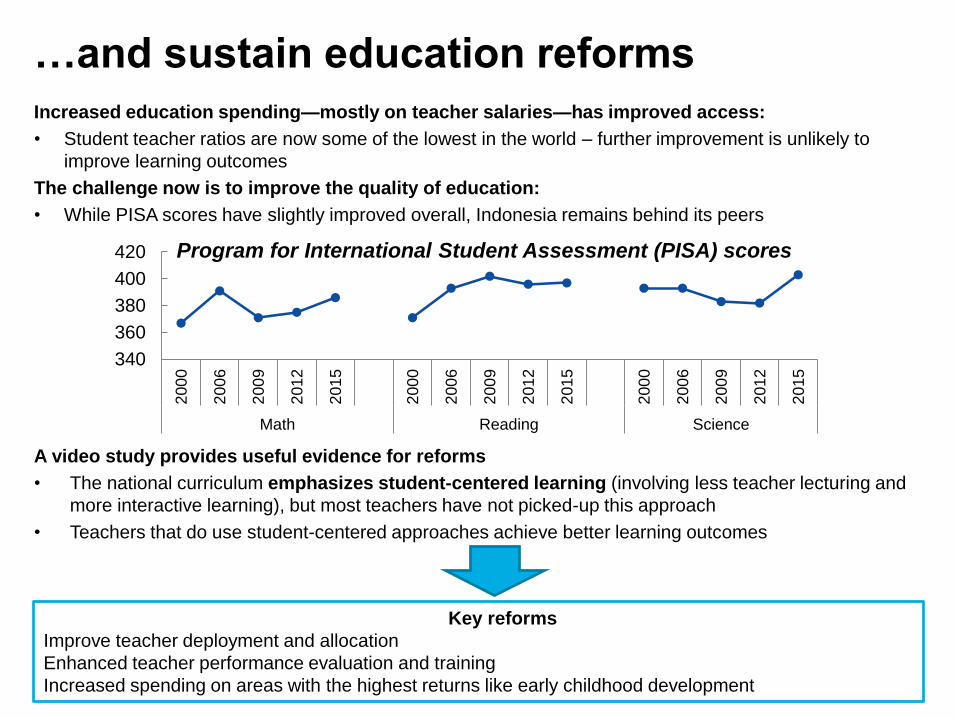

…and sustain education reforms

Increased education spending—mostly on teacher salaries—has improved access:

• Student teacher ratios are now some of the lowest in the world – further improvement is unlikely to

improve learning outcomes

The challenge now is to improve the quality of education:

• While PISA scores have slightly improved overall, Indonesia remains behind its peers

A video study provides useful evidence for reforms

• The national curriculum emphasizes student-centered learning (involving less teacher lecturing and

more interactive learning), but most teachers have not picked-up this approach

• Teachers that do use student-centered approaches achieve better learning outcomes

23

340

360

380

400

420

200

0

200

6

200

9

201

2

201

5

200

0

200

6

200

9

201

2

201

5

200

0

200

6

200

9

201

2

201

5

Math Reading Science

Program for International Student Assessment (PISA) scores

Key reforms

Improve teacher deployment and allocation

Enhanced teacher performance evaluation and training

Increased spending on areas with the highest returns like early childhood development

Terima Kasih