indicators of the strength of public management systems...

TRANSCRIPT

INDICATORS OF THE STRENGTH OF

PUBLIC MANAGEMENT SYSTEMS

JANUARY 29, 2014

GOVNET MEETING, BRUSSELS

Jordan Holt, [email protected]

1

What are we trying to do?

Identify a comprehensive and comprehensible set of

indicators of the strength of public management systems

with the following characteristics:

Governments can improve upon the scores

There is evidence of instrumental value or consensus on

intrinsic value

They should be easy to collect regularly for a large enough

set of countries at reasonable cost

2

Who are the indicators for? 3

Governments

• Set targets for reforms and monitor and evaluate progress

• Strengthen ownership of reform objectives

Donors

•Set targets for projects, track impact, and hold themselves accountable

•Make decisions about using country systems

Researchers

• Build an evidence base of what reforms work in what contexts and what really matters for development outcomes

Citizens and civil society

• Monitor performance

• Hold governments to account and advocate for change

Where in the results chain are we

measuring?

Support for reforms

(inputs)

Institutional strength/quality

(processes, outputs and intermediate outcomes)

Development outcomes

4

Indicators of institutional quality that focus on functionality

rather than form and measure aspects of institutions that lead

to improvements in development outcomes

What public management systems are

we focusing on? 5

The focus is on upstream systems and institutions

Public

Financial

Management

Procurement Tax Admin. Public Admin.

and Civil

Service

Public

Information

Transparency, Accountability & Participation

*The scope of the project may be expanded to cover

more public management systems such as public

investment management, intergovernmental systems,

regulatory management, policy management and

oversight systems

Effective Institutions Platform 6

Ma

king

Refo

rm H

ap

pen

Ind

ica

tors

for

Succ

ess

Dom

est

ic R

eso

urce

Mob

iliza

tion

Use

of

Count

ry S

yst

em

s

Acc

ount

ab

le a

nd

Incl

usive

Inst

itutions

ISPMS is conducted under “Indicators for Success” but can contribute to other

pillars too

What is our approach?

1. Identify a set of “systems”

2. Agree on a set of criteria

3. Apply criteria to available indicators

4. Are there gaps? What stories can

we tell?

5. Identify strategy to fill in

gaps 6. Build consensus

Overarching principle: Draw on existing efforts, avoid duplication

and enable sustainable collection

7

-Effective Institutions Platform

-Steering Group (BMZ, DFID, ADB, DFAT Canada, SIDA,

AusAid, OECD, Global Integrity, IBP,

Transparency International)

What have we done so far?

Launched Secretariat (housed in World Bank)

Set up Steering Group and Technical Expert Groups

3 virtual meetings (May 2013, July 2013, and

November 2013)

1 in-person meeting in Bonn in August 2013

Established set of criteria for a “good” indicator

Completed phase 1: 100 existing indicators meet

criteria, gaps and challenges identified

3 discussion notes describe: how the criteria were

applied, challenges in their application, and gaps

8

ISPMS Criteria

ISPMS should meet 4 “utility” criteria…

Criterion Definition

1. Action-worthy

(Salient)

We know (or strongly believe) that they contribute to results

2. Actionable They are amenable to government action and project interventions

3. Behavioral Focus on de facto changes in behavior/performance

(implementation) rather than the de jure

4. Replicable Generated transparently and can be reproduced by others

…and a “feasibility” criterion.

Criterion Definition

Sustainability Should be amenable to cost-effective and regular collection

9

Of about 750 existing indicators, only

about 100 meet the criteria

0 5 10 15 20 25

Public Information Systems

Procurement

Tax

Public Adminsitration and CivilService

PFM

Number of indicators that meet ISPMScriteria

Don’t yet

meet

feasibility

criteria

Shortlist of most “action-

worthy”

10

Key challenges in applying

the criteria to existing

indicators:

• How strictly should the action-

worthiness and behavioral

criteria be applied? (For

example, is publication of

information enough or should

we be concerned with how it

is used?)

• Trade-offs among criteria

(e.g. actionable and action-

worthy)

[See discussion notes]

Focus on the public availability

of key pieces of information

Where does this leave us?

Key gaps in existing indicators identified

Not comprehensive: not enough to tell a clear story

Inadequate coverage across time, countries and systems

Mainly based on expert assessments; limited involvement of country

governments in developing indicators and collecting data

Specific challenges identified

No “burning platform” to motivate the development of better quality indicators

Some systems are conceptually difficult to measure: characterized by

intangible concepts, difficult to observe the behavior of multiple actors, little

theory or evidence to provide guidance

Need to better involve country governments in the initiative

Develop proposal for phase 2: strategy to fill in gaps

11

What’s next? Phase 2 of ISPMS

1. Indicator marketplace

2. Incubate conceptually difficult areas

3. Administrative data sources

Fill in gaps in coverage of existing cross-national

indicators via 3 work streams

12

ISPMS Secretariat will continue to

work with PEFA, MAPS and

TADAT tools to identify indicators

that meet the ISPMS criteria

1. Indicator Marketplace 13

Publicize existing indicators

Hold competition for "new" indicators

Launch at April 2014 Global

Partnership Mtg

Connect winners with data

collectors and funding

Approach

Why? Need for more inclusive approach to developing indicators and broader

discussion about what should be measured and how

Targeted participants: both data collectors and idea generators from the

general public, civil society/international NGOs, researchers,

development practitioners/agencies, private entrepreneurs

Financial and reputational incentives to participate will be provided

Focus areas All public management systems; indicators that are either entirely new

(untested) or have been piloted but are worth scaling up

2. Incubating indicators in difficult areas 14

Approach

Public administration & civil service Public information systems

“A PEFA for PACS”: develop

international consensus around a

set of indicators

Focus on right to information

regimes. Test indicators in pilot

countries to learn more about what

is appropriate in different contexts.

Why?

Focus areas

• Limited theory/evidence/consensus connecting “systems” to

development outcomes

• Difficult to operationalize certain concepts for measurement without

relying on “form” (e.g. transparency or meritocracy)

• Difficult to observe the behavior of multiple actors

3. Administrative data sources 15

Approach Take stock of

publicly reported data

Identify potential indicators

(Compare/build on PEFA and

MAPS)

Analyze comparability

Develop mechanism to collect and

report data on a regular basis

Public financial management Procurement

Why?

Focus areas

Most existing indicators are based on expert assessments; data from

administrative sources can be collected more frequently (and sustainably)

and can be better suited for research

Examples:

• Contract management (share of contracts with

schedule delays or cost overruns)

• Data on PEFA indicators (system outturns)

How can you contribute?

Participate in the Steering Group or Technical Expert Groups

Participate in the marketplace: share your indicator ideas!

Promote the marketplace to your networks.

Provide us feedback on what types of data and indicators you need for

your projects.

Help us reach out to your counterparts in country governments.

Country governments are invited to participate in the Steering Group or

individually in various work streams to provide input and feedback on what

indicators are the most useful and feasible in their contexts.

Countries could share ideas for indicators via the marketplace or help pilot new

indicators.

Vietnam, Bangladesh and the Pacific Islands Forum have all expressed interest in

joining the initiative

16

Thank you!

Full set of indicators is available at:

http://go.worldbank.org/99F3LCSFR0

17

ISPMS Datasets 18

ILO Public Sector Employment Data

BEEPS

Doing Business

Enterprise Surveys

Global Integrity Indicators

Institutional Profiles Database

International Budget Practices and Procedures

Database

Methodology for Assessing

Procurement Systems (MAPS)

Open Budget Survey

Transparency International

Global Corruption Barometer

OECD Comparative

Information Series (Tax)

Wage and Bill Pay Compression

Public Expenditures and

Financial Accountability

IMF Government Financial

Statistics/ fiscal decentralization

Afro/Arab/Asian barometer

Human Resource Management AGI

IAMTAX

Medium-Term Expenditure Framework

Dataset

Public Investment Management

Public Accountability

Mechanism

World Bank GAC Diagnostic Surveys

Regional tax administration

datasets

Evans and Rauch

Quality of Government

Bertelsman Transformation

Index

Country Policy and Institutional

Assessments (CPIA)

Contain indicators that meet ISPMS criteria Do not meet feasibility criteria Not actionable

PACS indicators 19

Subsystem Indicator Value Year Value Year Value Year Value Year Value YearIn practice, civi l servants are appointed and evaluated according to profess ional

cri teria . (Global integri ty 45b) (100 = high, 0 = low) 50 2011 25 2010 50 2010 50 2006 50 2011

In practice, civi l service management actions (e.g. hi ring, fi ring, promotions) are not

based on nepotism, cronyism, or patronage. (Global Integri ty 45c) (100 = high, 0 = low) 50 2011 25 2010 50 2010 50 2006 50 2011

How do graduates of the country's most el i te univers i ty(ies ) view a publ ic sector

career? (Evans and Rauch 19)

(1 = best possible career option, 4 = second best option relative to private sector) 3.25

1970-

1990 4

1970-

1990 3.67

1970-

1990

How do members of the educated middle class who are not in a pos i tion to attend the

most el i te univers i ties view a publ ic sector career? (Evans and Rauch 20)

(1 = best possible career option, 4 = second best option relative to private sector) 3

1970-

1990 2.5

1970-

1990 4

1970-

1990

Senior officia ls have sa laries that are comparable with the sa laries of private sector

managers with roughly s imi lar tra ining and respons ibi l i ties? (Qual i ty of Government 2j)

(1 = hardly ever, 7 = almost always) 3.27

2008-

2012 2.73

2008-

2012 1.5

2008-

2012 3.25

2008-

2012

Wage Compress ion Ratio (the ratio of the highest sa lary to the lowest on the centra l

government's main sa lary sca le) 9.5 2008 4 2003

Centra l government wages as % of expenditures

Centra l government wages as % of GDP 3.55 2008 6.93 2008 7.25 2008

Centra l government wages as % of revenue 31.95 2008 33.51 2008 29.63 2008 32.74 2008

General government wages as % of expenditures 24.02 2005

General government wages as % of GDP 10.08 2005

General government wages as % of revenue 24.09 2005

When deciding how to implement pol icies in individual cases , publ ic sector employees

treat some groups in society unfa irly? (Qual i ty of Government 2h)

(1 = hardly ever, 7 = almost always) 4.47

2008-

2012 4.71

2008-

2012 5.67

2008-

2012 4.50

2008-

2012

How often would you say that publ ic sector employees today act impartia l ly when

deciding how to implement a pol icy in an individual case? (Qual i ty of Government 4)

(1 = not at all, 7 = to a very large extent) 3.67

2008-

2012 3.75

2008-

2012 3.00

2008-

2012 3.80

2008-

2012

Publ ic sector employees s trive to fol low rules . (Qual i ty of Government 8d)

(1 = not at all, 7 = to a very large extent) 4.53

2008-

2012 4.80

2008-

2012 4.33

2008-

2012 5.25

2008-

2012

Publ ic sector employees s trive to help ci tizens . (Qual i ty of Government 8c)

(1 = not at all, 7 = to a very large extent) 4.27

2008-

2012 4.93

2008-

2012 3.50

2008-

2012 5.25

2008-

2012

Publ ic sector employees s trive to implement the pol icies decided upon by the top

pol i tica l leadership. (Qual i ty of Government 8b) (1 = not at all, 7 = to a very large extent) 5.00

2008-

2012 4.73

2008-

2012 3.80

2008-

2012 5.50

2008-

2012

Publ ic sector employees s trive to ful fi l l the ideology of the party/parties in government.

(Qual i ty of Government 8e) (1 = not at all, 7 = to a very large extent) 5.13

2008-

2012 3.53

2008-

2012 5.67

2008-

2012 5.25

2008-

2012

Public Administration and Civil Service

Access on meri t

and competition

Accountabi l i ty

Attractiveness

Affordabi l i ty

Colombia Philippines Bangladesh Congo, DR Kenya

Indicators highlighted in grey do not meet the ISPMS feasibility criteria because time series data are not available.

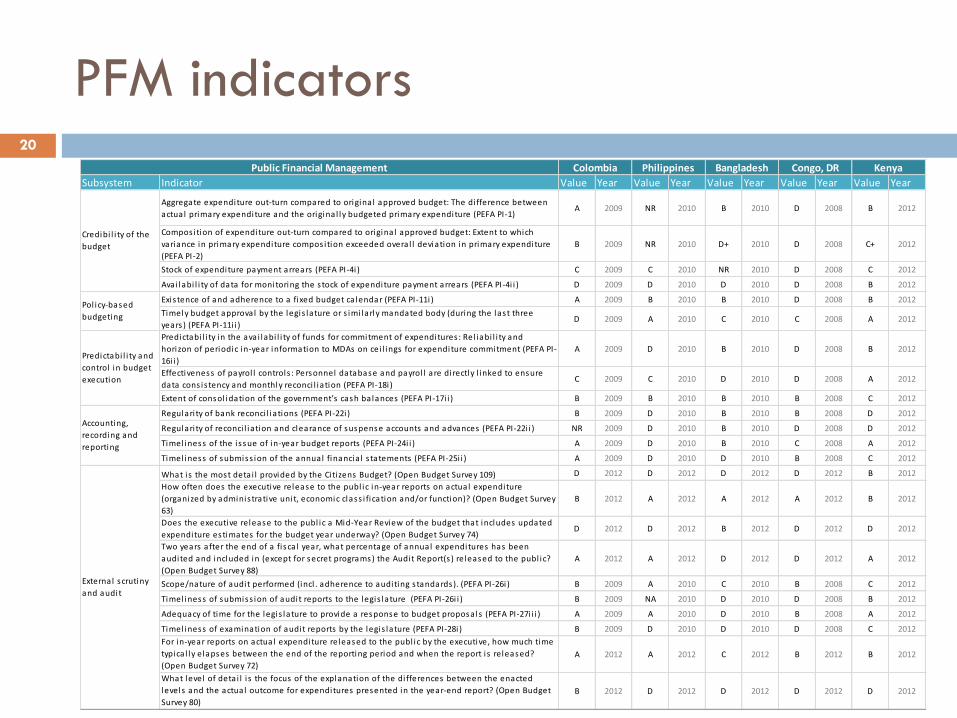

PFM indicators 20

Subsystem Indicator Value Year Value Year Value Year Value Year Value Year

Aggregate expenditure out-turn compared to origina l approved budget: The di fference between

actual primary expenditure and the origina l ly budgeted primary expenditure (PEFA PI-1)A 2009 NR 2010 B 2010 D 2008 B 2012

Compos ition of expenditure out-turn compared to origina l approved budget: Extent to which

variance in primary expenditure compos ition exceeded overa l l deviation in primary expenditure

(PEFA PI-2)

B 2009 NR 2010 D+ 2010 D 2008 C+ 2012

Stock of expenditure payment arrears (PEFA PI-4i ) C 2009 C 2010 NR 2010 D 2008 C 2012

Avai labi l i ty of data for monitoring the s tock of expenditure payment arrears (PEFA PI-4i i ) D 2009 D 2010 D 2010 D 2008 B 2012

Exis tence of and adherence to a fixed budget ca lendar (PEFA PI-11i ) A 2009 B 2010 B 2010 D 2008 B 2012

Timely budget approval by the legis lature or s imi larly mandated body (during the last three

years ) (PEFA PI-11i i )D 2009 A 2010 C 2010 C 2008 A 2012

Predictabi l i ty in the ava i labi l i ty of funds for commitment of expenditures : Rel iabi l i ty and

horizon of periodic in-year information to MDAs on cei l ings for expenditure commitment (PEFA PI-

16i i )

A 2009 D 2010 B 2010 D 2008 B 2012

Effectiveness of payrol l controls : Personnel database and payrol l are di rectly l inked to ensure

data cons is tency and monthly reconci l iation (PEFA PI-18i )C 2009 C 2010 D 2010 D 2008 A 2012

Extent of consol idation of the government’s cash balances (PEFA PI-17i i ) B 2009 B 2010 B 2010 B 2008 C 2012

Regulari ty of bank reconci l iations (PEFA PI-22i ) B 2009 D 2010 B 2010 B 2008 D 2012

Regulari ty of reconci l iation and clearance of suspense accounts and advances (PEFA PI-22i i ) NR 2009 D 2010 B 2010 D 2008 D 2012

Timel iness of the i ssue of in-year budget reports (PEFA PI-24i i ) A 2009 D 2010 B 2010 C 2008 A 2012

Timel iness of submiss ion of the annual financia l s tatements (PEFA PI-25i i ) A 2009 D 2010 D 2010 B 2008 C 2012

What i s the most deta i l provided by the Ci tizens Budget? (Open Budget Survey 109) D 2012 D 2012 D 2012 D 2012 B 2012

How often does the executive release to the publ ic in-year reports on actual expenditure

(organized by adminis trative unit, economic class i fication and/or function)? (Open Budget Survey

63)

B 2012 A 2012 A 2012 A 2012 B 2012

Does the executive release to the publ ic a Mid-Year Review of the budget that includes updated

expenditure estimates for the budget year underway? (Open Budget Survey 74)D 2012 D 2012 B 2012 D 2012 D 2012

Two years after the end of a fi sca l year, what percentage of annual expenditures has been

audited and included in (except for secret programs) the Audit Report(s ) released to the publ ic?

(Open Budget Survey 88)

A 2012 A 2012 D 2012 D 2012 A 2012

Scope/nature of audit performed (incl . adherence to auditing s tandards). (PEFA PI-26i ) B 2009 A 2010 C 2010 B 2008 C 2012

Timel iness of submiss ion of audit reports to the legis lature (PEFA PI-26i i ) B 2009 NA 2010 D 2010 D 2008 B 2012

Adequacy of time for the legis lature to provide a response to budget proposals (PEFA PI-27i i i ) A 2009 A 2010 D 2010 B 2008 A 2012

Timel iness of examination of audit reports by the legis lature (PEFA PI-28i ) B 2009 D 2010 D 2010 D 2008 C 2012

For in-year reports on actual expenditure released to the publ ic by the executive, how much time

typica l ly elapses between the end of the reporting period and when the report i s released?

(Open Budget Survey 72)

A 2012 A 2012 C 2012 B 2012 B 2012

What level of deta i l i s the focus of the explanation of the di fferences between the enacted

levels and the actual outcome for expenditures presented in the year-end report? (Open Budget

Survey 80)

B 2012 D 2012 D 2012 D 2012 D 2012

Kenya

External scrutiny

and audit

Colombia Philippines Bangladesh Congo, DRPublic Financial Management

Credibi l i ty of the

budget

Predictabi l i ty and

control in budget

execution

Pol icy-based

budgeting

Accounting,

recording and

reporting

Procurement indicators 21

Subsystem Indicator Value Year Value Year Value Year Value Year Value YearDuring the past year, have there been credible reported instances in which the procurement of

goods and services has not fol lowed an open and competitive process in practice? (response

options include: no credible reported instances , some reported instances , s igni ficant reported

examples of i rregulari ties , and the process was not open and competitive in practice) (Open

Budget Survey 97)

C 2010 C 2010 C 2010 D 2010 C 2010

When contracts are awarded by methods other than open competition, they are justi fied in

accordance with the legal requirements (in a l l cases , in at least 80% of cases , in at least 60%

of cases , in less than 60% of cases) (PEFA PI-19i i )

A 2009 B 2010 B 2010 D 2008 D 2012

Are the results of national publ ic procurement bids predictable? (Insti tutional Profi les

Database A3040) (1 = low, 4 = high)2 2009 3 2009 2 2009 2 2009 2 2009

Are the results of loca l publ ic procurement bids predictable? (Insti tutional Profi les Database

A3041) (1 = low, 4 = high)2 2009 2 2009 1 2009 1 2009 2 2009

Gifts to secure publ ic contracts (% of fi rms) (Enterprise Surveys corr2) 32.8 2010 58.5 2009 26.7 2007 75.7 2010 71 2007

Value of gi ft to secure government contract (% of contract) (Enterprise Surveys corr3) 2.6 2010 16.4 2009 1.2 2007 9.3 2010 7.8 2007

In practice, companies gui l ty of major violations of procurement regulations (i .e. bribery) are

prohibi ted from participating in future procurement bids . (Global Integri ty 51j)

(100 = high, 0 = low)

75 2011 25 2010 75 2010 0 2006 25 2011

In practice, the confl icts of interest regulations for publ ic procurement officia ls are enforced.

(Global Integri ty 51c) (100 = high, 0 = low)50 2011 75 2010 50 2010 25 2006 50 2011

Appeals/compla ints system: decis ions are del iberated on the bas is of ava i lable information,

and the fina l decis ion can be reviewed and ruled upon by a body (or authori ty) with

enforcement capacity under the law. (Methodology for Assess ing Procurement Systems)

Fairness of the compla ints system: Procedures governing the decis ion making process of the

review body provide that decis ions are a) based on info relevant to the case, b) ba lanced and

unbiased in cons ideration of the relevant information, c) can be subject to higher level review,

d) result in remedies that are relevant to correcting the implementation process or

procedures . (Methodology for Assess ing Procurement Systems)

Exis tence of an independent adminis trative procurement compla ints system. (PEFA PI-19iv) B 2009 NU 2010 B 2010 NU 2008 B 2012

The legal and regulatory framework is freely and eas i ly access ible to the publ ic through

appropriate means . (PEFA PI-19i )B 2009 B 2010 B 2010 D 2008 B 2012

Publ ic access to complete, rel iable and timely procurement information

The extent to which key procurement information (government procurement plans , bidding

opportunities , contract awards , and data on resolution of procurement compla ints ) i s made

avai lable to the publ ic through appropriate means . (PEFA PI-19i i i )

C 2009 B 2010 C 2010 D 2008 B 2012

Competition

Efficiency and

effectiveness

Integri ty

Fair and

equitable

treatment

Transparency

Procurement Colombia Philippines Bangladesh Congo, DR Kenya

Data not publ icly

ava i lable

Data not publ icly

ava i lable

Data not publ icly

ava i lable

Data not publ icly

ava i lable

Data not publ icly

ava i lable

Data not publ icly

ava i lable

Data not publ icly

ava i lable

Data not publ icly

ava i lable

Data not publ icly

ava i lable

Data not publ icly

ava i lable

Tax indicators 22

Subsystem Indicator Value Year Value Year Value Year Value Year Value YearTotal time spent to pay taxes (hours )

(Doing Bus iness )203 2013 193 2013 302 2013 336 2013 340 2013

The percentage of ci tizens who have come into contact with tax officia ls over the past year who

have paid bribes . (Transparency International Q7 Global Corruption Barometer)22 2013 12 2013 39 2013 46 2013 70 2013

Percent of Fi rms expected to give gi fts in meetings with tax officia ls . (Enterprise Survey corr 1) 2.8 2010 18.6 2009 85.1 2007 65.7 2010 79.2 2007

The total tax adminis tration cost as a percent of the total revenue col lections (OECD CIS) 0.68 2011

The extent to which taxpayers are regis tered in a complete database system with

comprehens ive direct l inkages to other relevant government regis tration systems and financia l

sector regulations . (PEFA PI-14i )

B 2009 C 2010 C 2010 D 2008 C 2012

Percent of fi rms formal ly regis tered when began operations (Enterprise Survey infor4) 94.3 2010 97.5 2009 61.9 2010

Number of years fi rms operated without formal regis tration (Enterprise Survey infor5) 0.5 2010 0.5 2009 1.9 2010

Clari ty and comprehens iveness of tax l iabi l i ties : The extent to which legis lation and procedures

for a l l major taxes are comprehens ive and clear, with s trictly l imited discretionary powers of a l l

government enti ties involved. (PEFA PI-13i )

D 2009 D 2010 D 2010 D 2008 B 2012

Taxpayer access to information on tax l iabi l i ty: The extent to which taxpayers have easy access

to comprehens ive, user friendly and up-to-date information on tax l iabi l i ties and adminis trative

procedures for a l l major taxes , supplemented with active taxpayer education campaigns .

(PEFA PI-13i i )

A 2009 C 2010 B 2010 C 2008 A 2012

Percentage of fi rms identi fying tax adminis tration as a “major” or “very severe” obstacle

(Enterprise Survey reg 5)28.6 2010 15.2 2009 30 2007 56.8 2010 32 2007

Percentage of establ ishments that cons ider the tax adminis tration to be the biggest obstacle

(Enterprise Survey obst13)0.5 2010 1.6 2009 0.3 2007 6 2010 1.7 2007

Payment gap (proxy): Aggregated revenue outturn compared to budget (PEFA PI-3) A 2009 A 2010 B 2010 D 2008 B 2012

Effectiveness of transfer of tax col lection to the Treasury: The frequency with which a l l tax

revenue is transferred into accounts control led by the Treasury (da i ly, weekly, monthly, etc.)

(PEFA PI-15i i )

A 2009 C 2010 B 2010 B 2008 B 2012

Frequency of complete account reconci l iation between tax assessments , col lections , arrears

records and receipts by the Treasury (monthly, quarterly, annual ly, etc.) (PEFA PI-15i i i )D 2009 D 2010 D 2010 A 2008 A 2012

Arrears

Col lection ratio for gross tax arrears : Percentage of tax arrears at the beginning of a fi sca l year,

which was col lected during that fi sca l year (average of the last two fisca l years ). (PEFA PI-15i )D 2009 A 2010 D 2010 D 2008 D 2012

Appeals

Exis tence and functioning of a tax appeals mechanism: The extent to which the tax appeals

system has transparent adminis trative procedures with appropriate checks and balances ,

implemented through independent insti tutional s tructures and completely set up and

effectively operating with satis factory access and fa i rness , and i ts decis ions are promptly acted

upon. (PEFA PI-13i i i )

B 2009 B 2010 C 2010 D 2008 B 2012

Percent of e-fi led returns - Personal Income Tax (OECD CIS) 6 2011

Percent of e-fi led returns - Corporate Income Tax (OECD CIS) 23 2011

Percent of e-fi led returns - VAT (OECD CIS) 24 2011

Revenue Administration

Strategic

Payment

Return fi l ing

Regis tration

Taxpayer service

Colombia Philippines Bangladesh Congo, DR Kenya

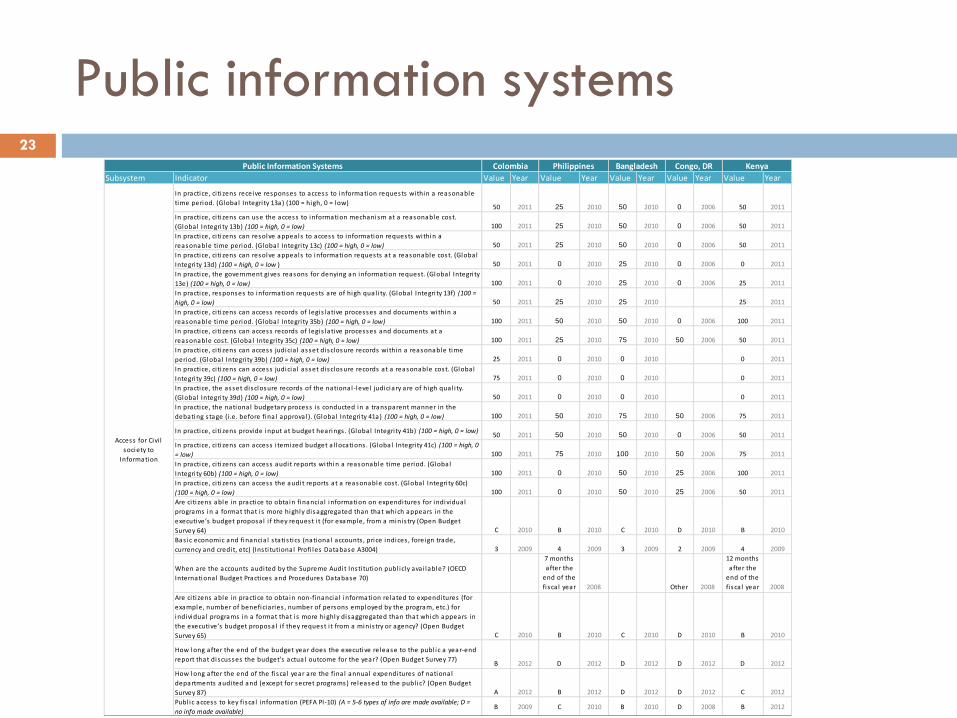

Public information systems 23

Subsystem Indicator Value Year Value Year Value Year Value Year Value Year

In practice, ci ti zens receive responses to access to information requests within a reasonable

time period. (Global Integri ty 13a) (100 = high, 0 = low)50 2011 25 2010 50 2010 0 2006 50 2011

In practice, ci ti zens can use the access to information mechanism at a reasonable cost.

(Global Integri ty 13b) (100 = high, 0 = low) 100 2011 25 2010 50 2010 0 2006 50 2011

In practice, ci ti zens can resolve appeals to access to information requests within a

reasonable time period. (Global Integri ty 13c) (100 = high, 0 = low) 50 2011 25 2010 50 2010 0 2006 50 2011

In practice, ci ti zens can resolve appeals to information requests at a reasonable cost. (Global

Integri ty 13d) (100 = high, 0 = low ) 50 2011 0 2010 25 2010 0 2006 0 2011

In practice, the government gives reasons for denying an information request. (Global Integri ty

13e) (100 = high, 0 = low) 100 2011 0 2010 25 2010 0 2006 25 2011

In practice, responses to information requests are of high qual i ty. (Global Integri ty 13f) (100 =

high, 0 = low) 50 2011 25 2010 25 2010 25 2011

In practice, ci ti zens can access records of legis lative processes and documents within a

reasonable time period. (Global Integri ty 35b) (100 = high, 0 = low) 100 2011 50 2010 50 2010 0 2006 100 2011

In practice, ci ti zens can access records of legis lative processes and documents at a

reasonable cost. (Global Integri ty 35c) (100 = high, 0 = low) 100 2011 25 2010 75 2010 50 2006 50 2011

In practice, ci ti zens can access judicia l asset disclosure records within a reasonable time

period. (Global Integri ty 39b) (100 = high, 0 = low) 25 2011 0 2010 0 2010 0 2011

In practice, ci ti zens can access judicia l asset disclosure records at a reasonable cost. (Global

Integri ty 39c) (100 = high, 0 = low) 75 2011 0 2010 0 2010 0 2011

In practice, the asset disclosure records of the national -level judiciary are of high qual i ty.

(Global Integri ty 39d) (100 = high, 0 = low) 50 2011 0 2010 0 2010 0 2011

In practice, the national budgetary process i s conducted in a transparent manner in the

debating s tage (i .e. before fina l approval ). (Global Integri ty 41a) (100 = high, 0 = low) 100 2011 50 2010 75 2010 50 2006 75 2011

In practice, ci ti zens provide input at budget hearings . (Global Integri ty 41b) (100 = high, 0 = low)50 2011 50 2010 50 2010 0 2006 50 2011

In practice, ci ti zens can access i temized budget a l locations . (Global Integri ty 41c) (100 = high, 0

= low) 100 2011 75 2010 100 2010 50 2006 75 2011

In practice, ci ti zens can access audit reports within a reasonable time period. (Global

Integri ty 60b) (100 = high, 0 = low) 100 2011 0 2010 50 2010 25 2006 100 2011

In practice, ci ti zens can access the audit reports at a reasonable cost. (Global Integri ty 60c)

(100 = high, 0 = low) 100 2011 0 2010 50 2010 25 2006 50 2011

Are ci ti zens able in practice to obta in financia l information on expenditures for individual

programs in a format that i s more highly disaggregated than that which appears in the

executive’s budget proposal i f they request i t (for example, from a minis try (Open Budget

Survey 64) C 2010 B 2010 C 2010 D 2010 B 2010

Bas ic economic and financia l s tatis tics (national accounts , price indices , foreign trade,

currency and credit, etc) (Insti tutional Profi les Database A3004) 3 2009 4 2009 3 2009 2 2009 4 2009

When are the accounts audited by the Supreme Audit Insti tution publ icly ava i lable? (OECD

International Budget Practices and Procedures Database 70)

7 months

after the

end of the

fi sca l year 2008 Other 2008

12 months

after the

end of the

fi sca l year 2008

Are ci ti zens able in practice to obta in non-financia l information related to expenditures (for

example, number of beneficiaries , number of persons employed by the program, etc.) for

individual programs in a format that i s more highly disaggregated than that which appears in

the executive’s budget proposal i f they request i t from a minis try or agency? (Open Budget

Survey 65) C 2010 B 2010 C 2010 D 2010 B 2010

How long after the end of the budget year does the executive release to the publ ic a year-end

report that discusses the budget’s actual outcome for the year? (Open Budget Survey 77)B 2012 D 2012 D 2012 D 2012 D 2012

How long after the end of the fi sca l year are the fina l annual expenditures of national

departments audited and (except for secret programs) released to the publ ic? (Open Budget

Survey 87) A 2012 B 2012 D 2012 D 2012 C 2012

Publ ic access to key fi sca l information (PEFA PI-10) (A = 5-6 types of info are made available; D =

no info made available)B 2009 C 2010 B 2010 D 2008 B 2012

Congo, DR Kenya

Access for Civi l

society to

Information

Public Information Systems Colombia Philippines Bangladesh