india - emerging healthcare destination - vfinal-1

TRANSCRIPT

6th World Medical Tourism Congress India, Potential Healthcare Destination

A Value Perspective

S Premkumar Group CEO, Apollo Hospitals Group

Historical Cost Analysis of US Products & Services

Source: http://www.thepeoplehistory.com/70yearsofpricechange.html, http://link.springer.com/chapter/10.1007%2F978-3-642-69855-2_42#page-1, http://www.foodtimeline.org/foodfaq5.html#restaurant , www.eia.gov , http://www.census.gov/construction/nrs/pdf/uspricemon.pdf

1980

Average cost of home

2013 $ 105,000

$ 22,500

Average cost of cardiac

surgery in India

$ 3000

?

Average cost of car

$ 7,200

$ 28,000

$ 76,425

$ 260,500

Cost of a Gallon on gas

$ 1.19

$ 3.29

Cost of Coke

$ 0.89

$ 1.99

Cost of a loaf of bread

$ 0.50

$ 2.79

Average cost of cardiac surgery in US

2

Cost Reduction despite

Steep Inflationary pressures | Exchange rate variations

Over a period of 30 Years (1983 – 2013)

Historical Cost Analysis of US Products & Services

Plus..

While..

Average Cost of Cardiac Surgery in India

$2900!

$3000

2013

1983

3 Source: http://in.reuters.com/article/2010/06/25/india-fuel-reforms-idINSGE65209520100625. www.tradingeconomics.com

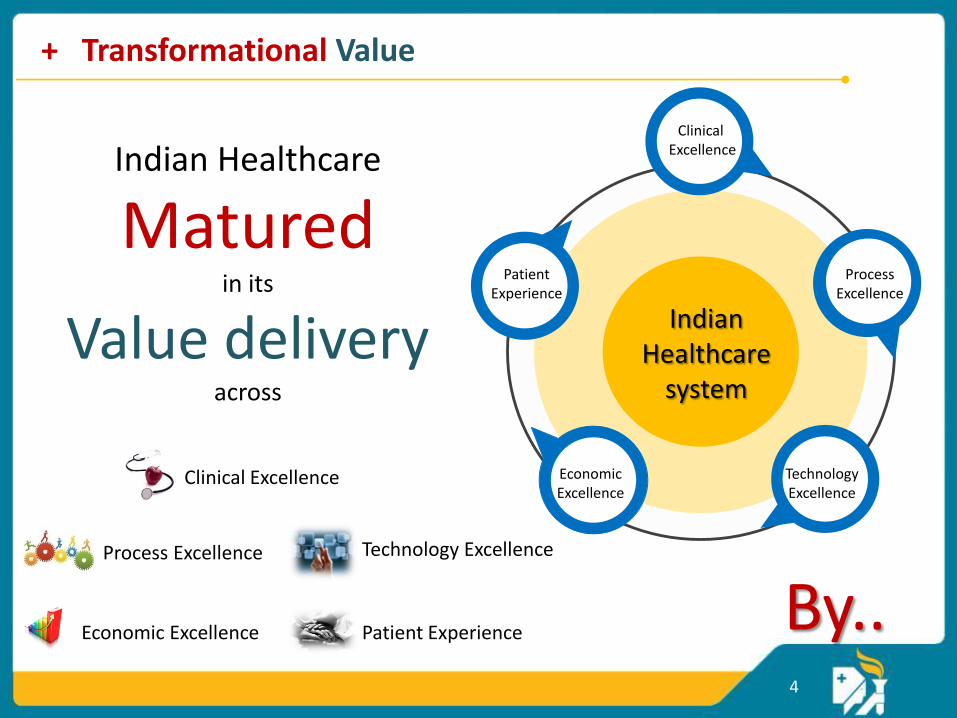

Indian Healthcare

Matured in its

Value delivery across

Clinical Excellence

Process Excellence

Technology Excellence

Economic Excellence

Patient Experience

Indian Healthcare

system

+ Transformational Value

By.. 4

Economic Excellence

Technology Excellence

Patient Experience

Process Excellence

Clinical Excellence

1983

Below the best On-par with the best On-par/Better than the Best

..Aligning with the World’s BEST Clinical Outcomes!!!

2013

5

Thus…

6

India becoming the Preferred Destination for Medical Tourism

7

850,000 Year 2012

3,200,000 Year 2015

Medical Tourists visiting India

CAGR of 55%

Source: ASSOCHAM, http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/studyreports/Med.pdf

Medical Tourism: Landscape

8

Is there an

Industry model of Scaled Maturity to

Serve the West?

9

Nascent to Mature An Example of Transformational Model

10

IT/ITES Industry

Opportunity Size

Investment

Infrastructure

Talent

Engagement Model

Employment

Growth in BFSI, Telecom, Retail & Aviation

IT Sector revenue - $2 Billion GDP Contribution – 0.62% (1994-95)

0.12 Million IT professionals (1994-95)

2.8 Million IT professionals (2011-12), 8.9M Indirect job creation

Low-level design, coding & maintenance Services

Re-engineering & Conversion projects

On-site & Off-shore model matures

End-to-End projects Integrated Outsourcing (ADM +BPO+

Infrastructure)

Increased skin in the game

Outcome based engagement models

Time & Material Cost Arbitrage Projects Business Outcome basis Transaction based

776 Engineering colleges

3393 Engineering colleges National Skill Development

(10 Million trained by 2012) Private training

(NIIT, APTECH, SSI)

Airport modernization

STPI/SEZ Zones (45/52 STPI parks in Tier II/III cities)

Significant development across Telecom, Transports, Power,

Hotels & Townships

Pre Y2K Y2K T&M Total Outsourcing Transformation

Up to 1996 1997-2000 2001 - 2005 2005 - 2010 From 2010….

Industry Maturity Time Line

Cross functional industry movement

IT / ITES Industry Life Cycle – Maturity Journey

High Private sector investments with conducive business reforms by Government, Tax SOPS

Low spending on Science, Technology &

Communication

Sector revenue - $101 Billion (2.7% of global market share),

GDP Contribution – 7.5% (2011-12)

Source: NASSCOM report 2012, Planning commission of India, Information Technology in India: Present Status and Future Prospects for Economic Development – By Sanjay K Singh, Indian Information technology industry: Past, Present & Future & A tool for national development

11

Is Healthcare the Next IT?

12

Arguably yes…

Opportunity Size

Investment

Infrastructure

Talent

Market Addressal

Employment

Public Healthcare Small & Medium Hospitals Corporate Hospitals Medical Tourism Globalization

15+ JCI Accredited hospitals 12 Beds, 0.6 Doctors, 1.3 Nurses (Per 1000 population) Significant leverage of

Medical Technology

1980s-2000 2000 - 2012 Vision 2020

Industry Maturity

Finishing School 335 Medical colleges

45629 Doctors per year

Limited number of Government medical and nursing colleges

Established nursing/ paramedical colleges

Primary & Secondary Care Hub & Spoke for tertiary care

First corporate tertiary care hospital (Clinical outcomes focused)

Management of Global hospitals

Preferred Medical tourism destination

2.96 Million Healthcare professionals (1997-98)

10 Million Doctors, Nurses & other healthcare professionals (2011-12)

Rise of NCDs/Lifestyle diseases, Growth in Medical Tourism

Sector revenue - $10 Billion Mostly Government driven

Sector revenue - $79 Billion GDP Contribution – 4.1% (2011-12)

Healthcare Industry Life Cycle – Maturity Measurement

Time Line

No JCI/NABH Accreditation – Predominantly government run

Spending - 82% Private & 18% Public Predominantly

Government spending Liberalization & Tax exemption (Private insurance)

Private investment in

Healthcare

Source: MCI India Annual report 2012, Indian Nursing council annual report, Planning commission of India, Healthcare in India – Emerging market report by PWC, IBEF report on Indian healthcare (2011)

13

Major presence of Accredited hospitals

2 Million additional beds

Projected revenue $280 Billion By 2020

Predominantly Private sector spending

600 new Medical colleges 1500 new Nursing colleges

Innovation at Indian hospitals result not from a grand design but from constant experimentation, adaptation and necessity … snippet from article in Harvard Business Review, Nov 2013

14

Quality

Talent

Patient Experience

..Building Value

Source: http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/studyreports/Med.pdf

‘Mark of Excellence’ standard for AYUSH Hospitals & Wellness

centers

Joint Commission International (JCI) accredited Hospitals with Standard

Clinical Governance Tools

National Accreditation Body of Hospitals (NABH)

with High Standard Operating procedures & Excellence

15+ 30+ 200+

International & National Accreditation of Hospitals

Instills Confidence in patients in terms of Quality standardization

Expectations mapping indicates Quality of Treatment

at the pre-procedural and procedural stage as the primary concern for

Medical travelers

Building Quality: Accreditation & Process Improvement

15

Building Quality: Quality Benchmarking : The Apollo Way ! ACE 25

Process Standardization & Improvement through

Six-Sigma, 5S Kaizen process

A Comprehensive Dashboard to monitor

Clinical parameters

Continuous Quality Improvement in Key Success Factors that

drives Clinical outcomes

A Quality Benchmarking Scorecard to stay ahead

of the World’s Best

CABG mortality rate ALOS of stroke cases in ICU

ALOS 1 Year Survival Rate For

Liver Transplants

TKR complication rate

Kt/V Measurement Avg Urea Reduction Ratio in Hemodialysis patients

ALOS post angioplasty

ALOS Post Renal Transplant

ALOS for large bowel resection

ALOS Post Microdisctomy ALOS Post TURP

ALOS Modified Radical Mastectomy

Medication Errors

Door to Thrombolysis Time in Ischemic Stroke in ER

Surgical Site Infection Rate Catheter-related UTI

Ventilator Associated Pneumonia

16 Note: The respective brands are the Copyright owners of all the logos and images

Minimally Invasive | Faster Recovery | Shorter Hospital Stay Better Clinical outcome | Simplifies Complex surgeries |

Safe, accurate & Precise

Localize radiation dosage| Superior dose distribution | Fewer side effects | Spares healthy surrounding tissues

Robotic Surgery across multiple specialties

Proton Beam Therapy for Cancer Treatment

Building Quality: Technology Excellence

Source: Internal data

Tomorrow’s Technology for Today’s care

17

Procedure USA India Thailand Singapore

Coronary artery bypass surgery $70,000-133,000 $7,000 $22,000 $16,300

Bypass surgery with heart valve replacement

$75,000-140,000 $9,500 $25,000 $22,000

Hip replacement $33,000-57,000 $7,200 $12,700 $12,000

Knee replacement $30,000-53,000 $7,200 $11,500 $9,600

Hip Resurfacing $50,000 $7,000 $16,000 $12,100

Prostate surgery (TURP procedure) $10,000-16,000 $3,600 $4,400 $5,300

Kidney Transplant Up to $ 150,000 $14000 $36,421-$37,397

Liver Transplant Up to $315,000 $55,000 $300,000

Note: U.S. charges are Average RAC rates. Indian prices are average prices (incremental/loaded costs are excluded)

Physician and certain other fees are generally excluded. Prices at non-U.S. hospitals are all-inclusive other than for Panama, which does not include surgeon’s fee. Only data from Joint Commission International accredited hospitals considered.

Competitive Economic Advantage on a Global Map

achieved through

Infrastructure | Technology | Talent | Process | Clinical Outcomes

Economic Excellence

Source: http://www.indianmedicaltravelassociation.com/India-Cost-Advantage.php 18

360° Patient Experience

19

Service Excellence

TENDER LOVING CARE IS THE WAY TO SERVE

VOICE OF CUSTOMERS LISTENING & ACTING TO

FEEDBACK IS THE WAY TO SERVE

BETTER

DISNEY EXPERIENCE PHILOSOPHY

@ HOSPITALS IN ENSURING SAFE &

COMFORTABLE STAY

20

360°

Patient

Experience

US Shore Home Healthcare Partners

Door-to-Door Concierge

Translator

Service (if required)

Best in Class

Clinical Outcomes

with TLC

Comfortable

Suites

Rehabilitation

Center

International

Cuisine

Care giver

Engagement

Counseling &

Follow-up through

Tele-Health

Service Excellence in Patient Experience

21

CAUTION!!!

22

To deliver the Best..

Selecting the Key Expertise Areas for the Medical value travelers

Non-Emergency | Elective Procedures Category

Specialty

Orthopedics Cardiac Sciences Functional Neurosurgery

Urology Gastroenterology

23

Presence of an On-shore partner for

“First-Mile & the Back-Home Mile”

Is Critical Treatment execution in India

Patient returns home

1 2

3

4 5

Patient Travels to India

Home health & Pre-operative Care

Post-operative Care & Rehabilitation

6 Continues engagement with Physician to

Tele Health

23

Hence…

24

Cross border & Offshore expertise offer a significant opportunity for Medical value travel

USA Outbound Patient flow

@ 1.6 million in 2012 with a significant 35% growth rate

over a 10-year projection (2007-17)

USA Outbound Patient flow

Opportunity Realization

Health plans to incentivize Medical travel

Collaboration with Accredited partners in leveraging Globalization

Deliver First-mile & Back-Home mile experience through On-shore partner

Creating Win-Win equation for all stakeholders

Need for Innovation in business models and service delivery

The Opportunity Ahead…

Forbes report on Medical tourism 22 Oct 2013, Deloitte – Medical Tourism – Consumers in search of value, Deloitte – Medical Tourism – Update and Implication

Desirability (Market)

Viability (Business)

Feasibility (Financial)

Operability (Regulatory)

Sustainability (Growth)

25

• Over 2200 Admissions

• Over 40,000 footfalls

• 3000 Emergency Cases

• 800 Major Surgeries

• 40 Cardiac Surgeries

• 700 Dialysis

• Over 60,000 Laboratory Tests

• 2-3 Organ Transplants

• Over 6000 Outpatient Volumes

• 800 CT Scans/ 400 MRI’s

A DAY AT

APOLLO HOSPITALS

• 30 years of Holistic Healing

• Touched 33 million lives

• 1200+ Transplants in 2012 (World’s Busiest Center

of Excellence for Solid organ Transplants)

• Pioneered Health checks - 8.5 million people

benefitted

• 155,000+ Heart Surgeries

• Over 10,000 Joint Replacements

• Patients from 120 countries

• First Liver Transplant in Children & Adults

• First Multi-Organ Transplant

• Over 8000 Kidney Transplants (Best Clinical

Outcomes)

BEING PATIENT-CENTRIC IS NOT A

GOAL, IT IS THE CORE OF OUR

EXISTENCE. TENDER LOVING CARE IS

OUR WAY OF LIFE

APOLLO HOSPITALS, INTRODUCED CLINICAL

EXCELLENCE IN THE INDIAN HEALTHCARE

LEXICON.

26

27

Departure Arrival

Thank You!

Apollo Hospitals have recorded equivalent or better outcomes than the international standards for medical complications associated with knee, coronary and prostrate as well as for infections relating to operating theatres

and catheters …..HBR November 2013 ( Delivering World -class Healthcare, Affordably )