india automotive industry scenario 2020 report - a small ... · 8 although suzuki motor corporation...

TRANSCRIPT

Automotive Intelligence Research Series

India Automotive Industry

Scenario 2020 Report

- A Small Car Focus -

Prof. Dr. Roger Moser Asia Connect Center, University of St.Gallen & IIM Bangalore

Christian Kuklinski Automotive Institute for Management, EBS Business School

i

Content

Content ....................................................................................................................................... i Figures ...................................................................................................................................... iii

Tables ........................................................................................................................................ iii

1 India: THE Market for Small Cars? .................................................................................. 1

2 Methodology ..................................................................................................................... 4

3 Quantitative Results: The Perspective of (Re)Action .................................................... 8

3.3 Curtailing the PEST-Environment ............................................................................ 8

3.4 Anticipating the Industry Stakeholders’ Behavior ................................................ 11

4 Scenario Development for the Political Environment of India’s (Small Car) Automotive Industry in 2020 ....................................................................................... 17

4.1 Political Environment Scenarios ............................................................................ 17

4.2 Reduced Tax Rates for Small Cars in 2020 (PP1) ................................................. 21 4.2.1 Analysis of the Industry Expert’s Arguments on Projection PP1

(Reduced Tax Rates) ........................................................................................... 21

4.2.2 Roadmap for Projection PP1 (Reduced Tax Rates) ............................................ 23

4.3 Harmonization of Emission Standards (PP2) ........................................................ 25

4.3.1 Analysis of Expert’s Argument on Projection PP2 ............................................. 26 4.3.2 Roadmap for Projection PP2 ............................................................................... 27

5 Scenario Development for the Economic Value Chain of India’s (Small Car) Automotive Industry in 2020 ....................................................................................... 30

5.1 Economic Value Chain Scenarios ............................................................................ 30

5.2 Foreign Dominance of the Market (VP1) ............................................................... 34 5.2.1 Analysis of Expert’s Argument on Projection VP1 ............................................ 34

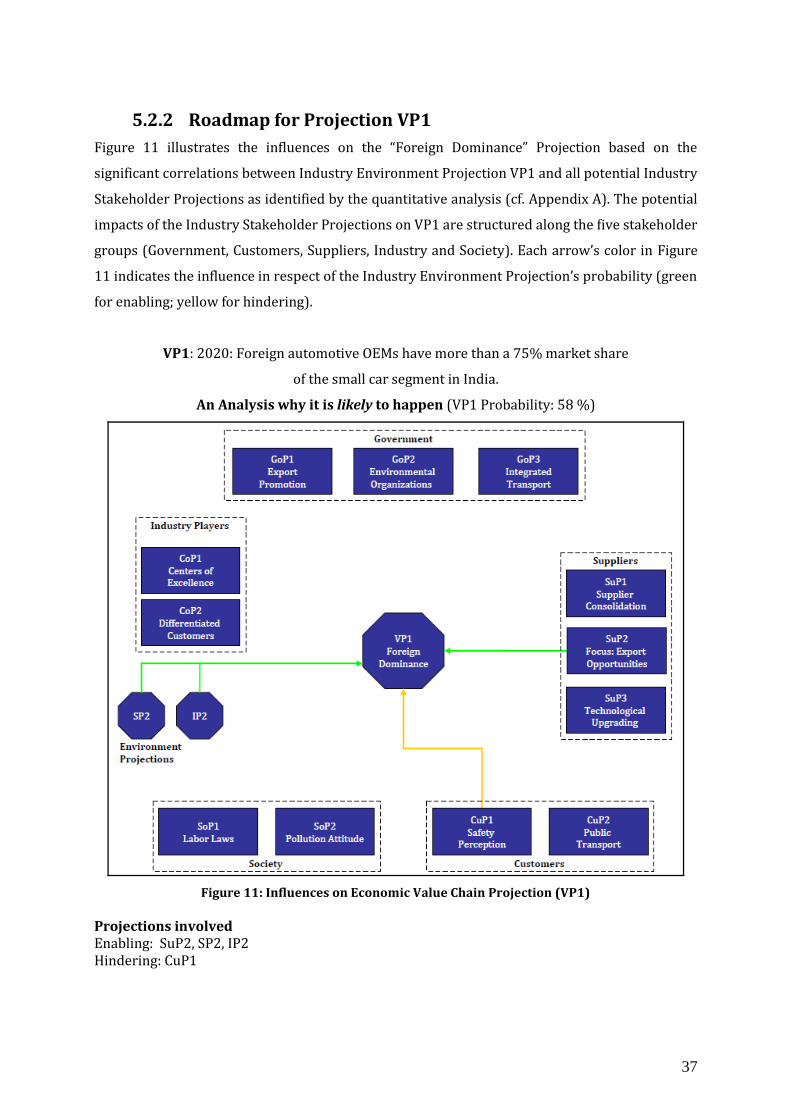

5.2.2 Roadmap for Projection VP1 .............................................................................. 37

5.3 OEMs and their Exclusive Supplier Networks (VP2) ............................................ 39 5.3.1 Analysis of Expert’s Argument on Projection VP2 ............................................ 40 5.3.2 Roadmap for Projection VP2 .............................................................................. 42

6 Scenario Development for the Social Environment of India’s (Small Car) Automotive Industry in 2020 ............................................................................................................ 44

6.1 Social Environment Scenarios ................................................................................ 44

6.2 Green Society (SP1) ................................................................................................. 48 6.2.1 Analysis of Expert’s Argument on Projection SP1 ............................................. 49

6.2.2 Roadmap for Projection SP1 ............................................................................... 50

6.3 Reasonable Cars (SP2) ............................................................................................ 52 6.3.1 Analysis of Expert’s Argument on Projection SP2 ............................................. 53

6.3.2 Roadmap for Projection SP2 ............................................................................... 54

7 Scenario Development for the Technological Infrastructure of India’s (Small Car) Automotive Industry in 2020 ....................................................................................... 57

7.1 Technological Infrastructure Scenarios ................................................................. 57

7.2 Local High-Tech Engineers (IP1) ............................................................................ 61 7.2.1 Analysis of Expert’s Argument on Projection IP1 .............................................. 62 7.2.2 Roadmap for Projection IP1 ................................................................................ 64

7.3 Mobility Infrastructure (IP2) .................................................................................. 66 7.3.1 Analysis of Expert’s Argument on Projection IP2 .............................................. 67 7.3.2 Roadmap for Projection IP2 ................................................................................ 68

8 References ....................................................................................................................... 71

Contact Information ............................................................................................................... 72

Appendix A .............................................................................................................................. 73

Correlation Analysis: Industry Environment and Stakeholder Projections ................. 73

ii

Appendix B .............................................................................................................................. 74

Crossroad Events ................................................................................................................ 74

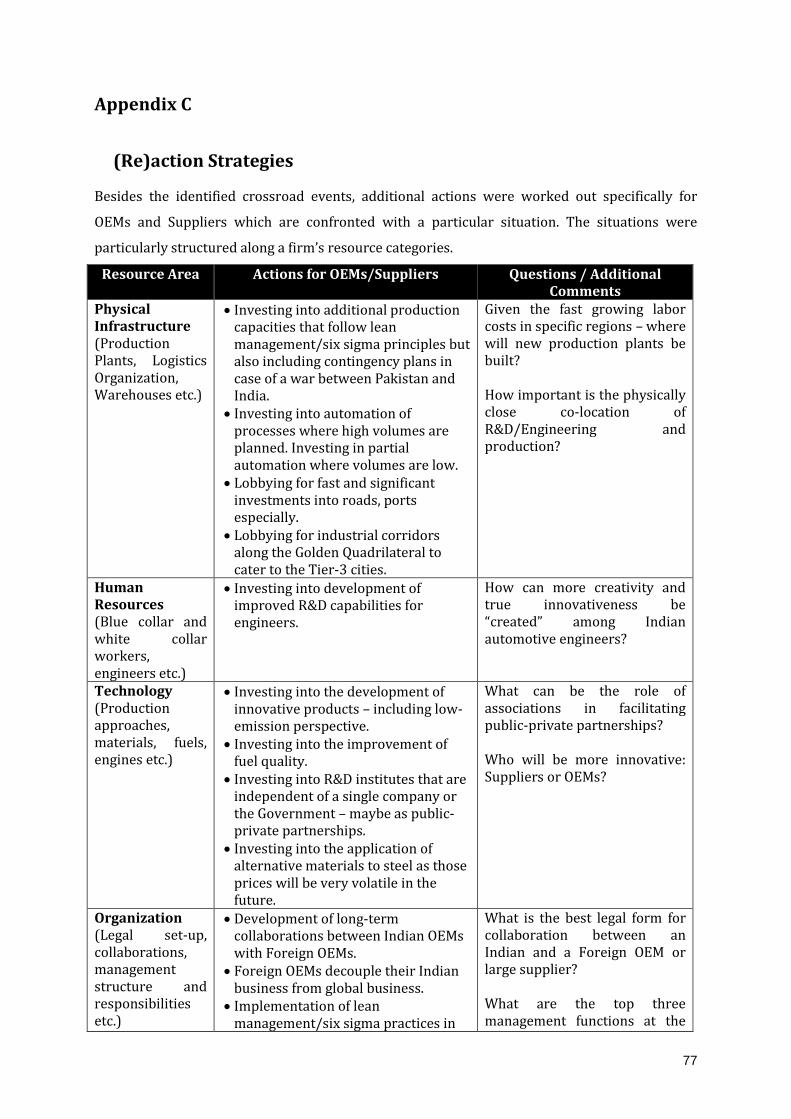

Appendix C .............................................................................................................................. 77

(Re)action Strategies .......................................................................................................... 77

Appendix D .............................................................................................................................. 79

Industry Stakeholder Projections: Consensus Analysis .................................................. 79

Customers ........................................................................................................................ 79

Suppliers .......................................................................................................................... 80

Industry / OEMs .............................................................................................................. 81

Government ..................................................................................................................... 82

Society 84

iii

Figures

Figure 1: Study approach for “Scenario 2020 Report” ....................................................................................... 3 Figure 2: PEST-Industry Environment Projections: Probability and Impact ......................................... 11 Figure 3: Industry Stakeholder Projections: Probability and Impact........................................................ 16 Figure 4: Political Environment Scenario Matrix ............................................................................................... 18 Figure 5: Consensus Analysis for “Reduced Tax Rates” Projection PP1 ................................................... 21 Figure 6: Influences on Political Industry Environment Projection 1 (PP1) .......................................... 23 Figure 7: Consensus Analysis for “Harmonization of Emissions” Projection PP2 ............................... 25 Figure 8: Influences on Political Industry Environment Projection (PP2) ............................................. 28 Figure 9: Economic Value Chain Scenario Matrix .............................................................................................. 31 Figure 10 : Consensus Analysis for “Foreign Dominance” Projection VP1 ............................................. 34 Figure 11: Influences on Economic Value Chain Projection (VP1) ............................................................. 37 Figure 12 : Consensus Analysis for “Exclusive Supplier Networks” Projection VP2 .......................... 39 Figure 13: Influences on Economic Value Chain Projection (VP2) ............................................................. 42 Figure 14: Social Environment Scenario Matrix ................................................................................................. 45 Figure 15: Consensus Analysis for “Green Society” Projection SP1 ........................................................... 48 Figure 16: Influences on Social Industry Environment Projections (SP1) .............................................. 51 Figure 17: Consensus Analysis for “Reasonable Cars” Projection SP2 ..................................................... 53 Figure 18: Influences on Social Industry Environment Projection (SP2) ................................................ 55 Figure 19: Technological Infrastructure Scenario Matrix .............................................................................. 58 Figure 20: Consensus Analysis for “Local High-Tech Engineers” Projection IP1 ................................. 61 Figure 21: Influences on Technological Infrastructure Projection (IP1) ................................................. 64 Figure 22: Consensus Analysis for “Mobility Infrastructure” Projection IP2......................................... 66 Figure 23: Influences on Technological Infrastructure Projection (IP2) ................................................. 68 Figure 24: Industry Environment and Stakeholder Projections: Probability and Impact ..... Fehler! Textmarke nicht definiert. Figure 25: Industry Environment and Stakeholder Projections: Probability and Consensus .......................................................................................................................... Fehler! Textmarke nicht definiert.

Tables

Table 1: Industry Environment Projections: Overview Quantitative Results........................................ 10 Table 2: Industry Stakeholder Projections: Overview Quantitative Results .......................................... 15 Table 3: Political Environment Scenarios: Consequences for Industry Stakeholders........................ 20 Table 4: Political Industry Environment Projection PP1................................................................................ 21 Table 5: Political Industry Environment Projection PP2................................................................................ 25 Table 6: Economic Value Chain Scenarios: Consequences for Industry Stakeholders ....................... 33 Table 7: Economic Industry Environment Projection VP1 ............................................................................ 34 Table 8: Economic Industry Environment Projection VP2 ............................................................................ 39 Table 9: Social Environment Scenarios: Consequences for Industry Stakeholders ............................ 47 Table 10: Social Industry Environment Projection SP1 .................................................................................. 48 Table 11: Social Industry Environment Projection SP2 .................................................................................. 52 Table 12: Technological Infrastructure Scenarios: Consequences for Industry Stakeholders ....... 60 Table 13: Technological Industry Environment Projection IP1 .................................................................. 61 Table 14: Technological Industry Environment Projection IP2 .................................................................. 66

1

1 India: THE Market for Small Cars?

Over the last two decades, India has received increased attention from Western firms as a large

country (3,3 Mio. km2) with a huge population (over 1.1 bn. people), and an impressive

economic development in the last few years.1 2 In particular, India’s consumer market is highly

attractive for Western firms as private consumption as well as the savings of private households

have risen substantially in recent years.

However, in order to be successful in India, product offerings need to be specifically designed for

the Indian market. With respect to small cars, the majority of consumers may emphasize rather a

car’s functionality (e.g., number of persons to fit in and flat front space for the placement of

religious figures) than safety features (such as airbags) or the latest emission reduction

technologies. A further – and major – necessity for local small cars: the purchase price needs to

account for the low average incomes but also fit into the “value for money” paradigm that mostly

influences the Indian mass markets for almost any product. A key challenge for any automotive

company active in the small car segment is therefore to understand what really creates “value”

for potential buyers and “how cheap is cheap enough”. The rather simple approach to build the

cheapest car in the world and wait for the Indian buyers to run for it has turned out to be rather

a wish than reality so far.

In general, the private expenditures for individual transportation have risen at a comparable

rate to overall consumption of private households;3 still, two-wheelers account for most of the

individual transportation purchases (75 % in 2010).4 Combined with the improvement of the

financial situation of private households, an inherent potential for the passenger (small) car

market to gain a higher share in India’s transportation market (16 % in 2010) seems realistic:5

For example, the domestic passenger car sales have more than doubled (138 %) within the past

five years resulting in more than 2.5 mio. units sold in 2010. Besides, the annual exports have

risen by an impressive 173 % – almost half a million passenger cars were exported in 2010.6

At the same time, local production capacities for passenger vehicles in India increased by 147 %

arriving at roughly three million units in 2010.7 However, despite the strong interests of foreign

1 Ministry of Statistics and Program Implementation (MOSPI), 2009. 2 Organization for Economic Co-operation and Development (OECD), 2008. 3 Increase from 2004-2008 in current prices, MOSPI (2009). 4 Society of Indian Automotive Manufacturers (SIAM), 2011. 5 SIAM (2011). 6 Increase from 2004-2010, SIAM (2011). 7 Increase from 2004-2010, SIAM (2011).

2

automotive firms in the Indian market, primarily domestic firms such as Maruti-Suzuki8 and

Tata Motors dominate India’s passenger (small) car market.9

India’s increasing relevance for the global automotive industry requires from local as well as

global decision makers to rethink their strategies for the Indian (small) car market in order to

benefit from the tremendous growth potentials. We have therefore initiated an industry

intelligence research program to support decision makers of automotive companies in their

strategy development for the Indian (small) car market. In its essence, the program develops

scenarios for India’s automotive industry future with an emphasis on the small car segment as

well as industry dynamics analyses to better understand the impact and interdependences

among relevant formal and informal institutions for the Indian automotive industry. The insights

of this “Scenario 2020 Report” are based on an extensive Delphi-study carried out with local

automotive industry experts in India in 2010/2011. The experts evaluated 20 projections for the

year 2020: eight Industry Environment Projections comprising ideas for future political,

(economic) value chain, social and (soft/hard technological) infrastructure (PEST) environments

and twelve Industry Stakeholder Projections serving as a foundation to outline behaviors of

industry stakeholders that affect the future PEST environment of India’s automotive industry

(emphasis on the small car segment).

The remainder of this “Scenario 2020 Report” is structured as follows. First, the Delphi

methodology as applied in the study is briefly explained. Second, an overview of the examined

projections is provided and the quantitative results of the Delphi survey are discussed. Third, the

scenarios are developed by matching the two Industry Environment Projections related to each

PEST environment explaining potential consequences for the industry’s stakeholders based

upon an expert-workshop held on the IIM Bangalore campus in 2010. Then, each Industry

Environment Projection is analyzed referring to probability of occurrence, impact on and

desirability for the Indian automotive industry. Afterwards, potential effects on each Industry

Environment Projection are outlined by drawing on the Industry Stakeholder Projections.

8 Although Suzuki Motor Corporation holds a 54 % equity stake of Maruti Suzuki India Ltd. (MSIL) Maruti-Suzuki is rather perceived by the authors and many experts as a domestic company (MSIL, 2011). 9 Passenger Vehicle market shares in 2008: Maruti Suzuki 46 % and Tata Motors 16.5%, SIAM (2009).

3

Figure 1: Study approach for “Scenario 2020 Report”

The “Scenario 2020 Report” is intended to support senior executives and corporate strategy

managers in the development or re-evaluation of their current plans for India’s (small car)

automotive industry. This “Scenario 2020 Report” primarily serves as input for further workshop

discussions among the experts in automotive companies to analyze and identify necessary

actions to be taken: Be prepared for the future of “Incredible India”.

4

2 Methodology

Heraclitus noted approximately 2.500 years ago: “panta rhei” (everything flows). His conception

characterizes the world as a dynamic and complex environment, continuously undergoing a

process of change. In today’s globalized world, the future seems even more uncertain than ever:

Hardly anybody is able to grasp a sharp picture of how tomorrow will look like – especially not

with respect to mobility challenges in emerging markets like India. This is what makes the future

not only interesting, but also challenging. However, every challenge also provides a chance for

those who master this challenge better than others – and this is where our “Scenario 2020

Report” intends to support senior executives as well as corporate strategy managers.

Especially in emerging markets such has India, the perceived uncertainty regarding future

developments is high. This may be due to the strong economic growth, the changing society, and

the way domestic institutions frame the “rules of the game” (North, 1990: 3) for these markets

(Khanna & Palepu, 1997). This is particularly challenging for senior executives: they are

responsible not only for the tactical but also for the long-term planning and need to take various

and diverse possible influences into account that may be of relevance prior to their occurrence:

Strategic and operational flexibility as key competitive factors in markets like India.

Scenario planning is a commonly accepted method to identify possible futures that need to be

considered by strategic planning (Alsan, 2008). To develop sound scenarios, this study draws on

the Delphi method and expert discussions. The Delphi method is suitable for the collection of

both qualitative and quantitative data on projections for possible futures and has gained a solid

reputation for collecting disputed expert opinions (Nielsen & Thangadurai, 2007). Capturing

disputed judgments as well as interpreting qualitative data is imperative for this study’s

character: it explores the uncertain.

The Delphi method is a multi-level group-based information-sharing survey tool (Czinkota &

Ronkainen, 2005). The application of the Delphi method is structured in three main phases

(Nielsen & Thangadurai, 2007):

1. Identification of relevant topics and issues.

2. Sharing of perspectives based upon each participant’s experiences.

3. Analysis and synthesis of the shared knowledge and perspectives.

For this report, an extensive desk research was first completed to identify relevant topics.

Second, the topics identified were further evaluated and modified during interviews with several

industry experts. Last, the affirmed topics were merged into twenty projections: Eight Industry

Environment Projections, structured along the political, (economic) value chain, social and

(soft/hard technology) infrastructure environment (PEST); and twelve Industry Stakeholder

5

Projections, structured along relevant stakeholders (customers, suppliers, OEMs/competitors,

government and the society at large). The Industry Environment Projections curtail the future

environment along the PEST framework and the Industry Stakeholder Projections delineate

potential stakeholder activities that may influence the Industry Environment Projections’

occurrence.

Two Industry Environment Projections represent each PEST environment and two Industry

Stakeholder Projections examine each stakeholder group. An additional Industry Stakeholder

Projection was integrated in the survey for the Government of India and the automotive

suppliers based on the significant impact identified for those two stakeholder groups on the

future industry environment.

The Delphi tool used in the study allowed then the 43 participating industry experts to assess

the projections, share their reasoning with other experts, review the other experts’ arguments,

and reconsider their own assessments. The experts rated the 20 projections regarding the

probability of occurrence (0-100 %), impact on the industry (5 point Likert-Scale) and

desirability for the industry (5 point Likert-Scale) and underlined their assessment with

individual statements.

The Industry Environment Projections were evaluated based on both the experts’ quantitative

and qualitative assessment. Correlation analyses revealed interrelations between Stakeholder

and Industry Environment Projections to enable the development of a “Roadmap” for each

Industry Environment Projection. Besides, all expert statements were analyzed and consolidated

for each projection to provide for a sound fundament for further interpretation and evaluation.

The two Industry Environment Projections for each PEST environment were matched and four

scenarios developed for each environment. Each of the 16 scenarios developed were presented

and evaluated with regards to potential consequences for the five stakeholder groups during a

workshop with 25 industry experts on the campus of IIM Bangalore. In addition, each expected

probability of occurrence of a scenario was rated and important events between 2011 and 2020

were identified (back-casting).

6

GETTING STARTED:

A Guide to Understand the Quantitative Results of Delphi Studies

The results of Delphi studies contain both quantitative data (experts’ assessments on

probabilities, impact, and desirability) and qualitative data (arguments of the experts why there

is a high/low probability, impact or desirability). While the evaluation of the qualitative data is

based on the content analysis of the written expert statements, the evaluation of the quantitative

data requires some additional information in order to interpret the figures on probability,

impact and desirability correctly.

Probability

The purpose of Delphi studies – as conducted – is in this study’s context to increase

transparency on the future business environment of a specific industry (segment) in India. In

such a context, projections where each industry expert either agrees on 90%+ or 10%-

probabilities are easy to interpret and use but will unfortunately not result in an opportunity to

gain insights that might lead to future competitive advantages. Projections that are so clear with

respect to their probabilities can be considered common knowledge in the industry. It is

therefore more important to understand the relative distribution of the expert judgments

between 0% and 100% probability.

This is why we display in this report always the probability and the degree of consensus among

the experts as a first indicator for what a 65% or 42% probability actually means. If there is a

high degree of consensus for a specific probability among the experts it is quite useful to look at

their qualitative arguments to understand why they believe in a relatively high or low

probability. If there is a high degree of dissent among the experts we further need to evaluate

whether this is due to a “flat” distribution of the probability opinions between 0% and 100% or

whether there are, for example, two culminations around 10% probability and around 90%

probability and then evaluate which specific arguments the two groups of experts use to justify

their rather low or high probability assessment.

Impact

The impact of a projection is important to ensure that the assessed projections are relevant for

the future industry development. In combination with the probability value it is possible to

illustrate which projections have a high impact and either a very low or very high probability.

Those projections with a very high probability need to be seriously considered for the further

strategy development process while the high impact/very low probability projections need to be

treated in such a way that the company should at least have a pre-defined (re)action strategy in

case it actually becomes true.

7

Desirability

The desirability of a projection is relevant to evaluate as prior research has shown that

projections with a high desirability are prone to be biased in their probability value. In short,

projections with a high desirability tend to display in general a higher probability due to

psychological reasons which are beyond the scope of this short introduction to discuss. As the

bias in this study is only minimal we have not recalculated the probability values as they are

more efficient to interpret this way.

8

3 Quantitative Results: The Perspective of (Re)Action

The analysis framework is primarily based on the PEST analysis for the Industry Environment

Projections and the stakeholder concept for the Industry Stakeholder Projections. This section

introduces the twenty projections (8 Industry Environment Projections and 12 Industry

Stakeholder Projections) evaluated by local industry experts and offers first quantitative insights

as a basis for the scenario development in Section 4.

3.3 Curtailing the PEST-Environment

In the following, each of the two Industry Environment Projections along the political, economic,

social, and technological environment are described and the quantitative results of the Delphi

are outlined (cf. Table 1, Figure 2).

Political

Environment

India’s future political environment is examined with respect to

Government subsidies for small car purchases and intensified

emission regulations. Whereas the first projection reflects a

significantly reduced Goods & Service Tax (GST) rate (PP1) and

therefore as support for industry growth, the second projection

renders fortified CO2 emission regulations across India – even

comparable to European standards (PP2) and is therefore rather

seen as a hindrance for further industry growth.

Economic Value Chain

Environment

The (economic) value chain environment for India’s automotive

industry is assessed by two projections as well. On the one hand,

the dispersion of market shares among domestic and foreign

OEMs is accounted for (VP1) to identify the future major players.

On the other hand, an OEM’s relationship with suppliers is

depicted by posting an optional integration of domestic suppliers

into a supplier network that is accessible for one OEM exclusively

(VP2) to better understand how the relationships between buyers

and suppliers are primarily characterized.

9

Social Environment

The projections on India’s social environment comprise

tendencies that influence purchasing behavior in the small car

segment. The first projection concerns the society’s

environmental awareness and the demand for low-emission

vehicles (SP1) to integrate the general view of the society on the

analyzed subject; the second projection refers to car buyers’ cost-

awareness and the relevance of prices for consumers’ purchasing

decisions (SP2) to reflect the direct purchasing behavior of the

most important customer group for the automotive industry in

India.

Technological

Infrastructure

Environment

The (soft/hard technological) infrastructure environment accounts

for India’s education system (“soft technology”) and mobility

infrastructure (“hard technology”). The former aspect concerns

the availability of local engineers (graduates from India’s

universities) and their familiarity with advanced automotive

technologies (IP1) – as the soft infrastructure of India in the

context of this study. The latter aspect picks up on the

transportation infrastructure development, especially referring to

road construction (IP2) to account for the hard infrastructure in

this study’s context.

Table 1 illustrates the quantitative results for the PEST Industry Environment Projections

assessed in terms of probability, consensus among the experts, impact on and desirability for the

Indian small car industry. Additionally, the right column depicts the utilized markers for Figure

2.

Overall, the average impact (3.5) as well as desirability (3.4) of the projections is rated high.

Although the industry experts vary strongly in their assessments (Consensus Distance: Ø 30.9),

four out of the eight Industry Environment Projections are considered at least likely (Probability

> 50%). The Delphi participants’ lack of a common opinion regarding any Industry Environment

Projection indicates a high degree of uncertainty about future industry developments and

affirms the relevance of such studies for senior executives.

10

No Industry Environment Projections Probability Consensus Impact Desirability Symbol

Po

liti

cal

1

(PP1) “Harmonization of Emissions” in 2020: The GST for small cars in India is a third of the tax rate for all other kinds of passenger cars.

46% 32.5 3.4 3.3

■

Unlikely Strong Dissent

High High

2

(PP2) “Reduced Tax Rates” in 2020: The emission regulations in all regions of India are the same as in Europe.

47% 30 3.4 3.6

Unlikely Strong Dissent

High High

Eco

no

mic

Va

lue

Ch

ain

3

(VP1) “Foreign Dominance” in 2020: Foreign automotive OEMs have more than a 75% market share of the small car segment in India.

58% 40 3.3 2.9

▲

Likely Very Strong

Dissent High Medium

4

(VP2) “Exclusive Supplier Networks” in 2020: Each automotive OEM has its proprietary domestic supplier network in India.

52% 35 3.5 3

Likely Strong Dissent

High Medium

So

cia

l

5

(SP1) “Green Society” in 2020: Small cars are only socially accepted as a means of transportation if they fulfill the strictest emission standards in India.

44% 20 3.4 3.5

∆

Unlikely Moderate Consensus

High High

6

(SP2) “Reasonable Cars” in 2020: The only buying criteria for small cars in India is their “TCO” (Total Cost of Ownership = Purchase Cost + Maintenance Cost – Resale Value).

59% 25 3.4 2.9

Likely Moderate

Dissent High Medium

Te

chn

olo

gic

al

Infr

ast

ruct

ure

7

(IP1) “Local High-Tech Engineers” in 2020: The education system in India provides sufficient engineers with advanced innovation capabilities in automotive core technologies (engine, materials, etc.).

54% 42.5 4 4

□

Likely Very Strong

Dissent High High

8

(IP2) “Mobility Infrastructure” in 2020: The development of new small car concepts for India and major transportation infrastructure development projects in India are strongly aligned.

48% 22.5 3.5 3.7

Unlikely Moderate

Dissent High High

Table 1: Industry Environment Projections: Overview Quantitative Results

The average probability of the Industry Environment Projections is 51%. The occurrence of SP2

(“Cheap Cars”) is considered the most likely among the assessed projections (cf. Figure 2)

whereas the second societal Industry Environment Projection SP1 (“Green Society”) is considered

the least likely. Yet, since the Impact of both projections on the industry is rated equally (3.4),

both aspects should be kept in mind for long-term planning.

11

Industry Environment Projections

Mobility

Infrastructure

Red

uce

d

Tax

Rat

es

Har

mo

niz

atio

n

of

Em

issi

on

s

Foreign Dominance

Exclusive Supplier

NetworksGreen Society Reasonable Cars

Local High-Tech

Engineers

3,0

3,2

3,4

3,6

3,8

4,0

4,2

40% 45% 50% 55% 60%

Probability

Imp

act

Figure 2: PEST-Industry Environment Projections: Probability and Impact

The impact of each Industry Environment Projection is well above 3.0 which further confirms the

relevance of the selected projections during the desktop research and initial expert interviews

(cf. Figure 2). The projection IP1 seems to form an exception since the capabilities of India’s

engineering graduates can be expected to substantially contribute to India’s development

beyond a country of mere assemblers – India might become a market hub for the global small

car industry.

3.4 Anticipating the Industry Stakeholders’ Behavior

The applied industry stakeholder approach includes five groups: Customers, Suppliers,

OEMs/Competitors, the Government of India and India’s Society at large. Each stakeholder

group is addressed by at least two Industry Stakeholder Projections. Due to particular interest in

the development of the domestic automotive supplier industry and the considerable influence of

the Government of India (GOI) on India’s future, an additional Industry Stakeholder Projection

examines each of these two stakeholder group’s activities.

In the following, the Industry Stakeholder Projections are described and the quantitative results

of the Delphi study are outlined (cf. Table 2, Figure 3). All Industry Stakeholder Projections were

developed in a structured approach that ensures that those stakeholder behaviors are evaluated,

which are supposed to have the strongest impact on the evaluated Industry Environment

Projections in total.

12

Customers

The Indian customer’s perspective is examined by two

aspects which have a high momentum in current

discussions, too. The first projection refers to customers’

education in terms of traffic / car safety. This ties strongly

in with today’s traffic situation in India (CuP1). The second

projection refers to an increased usage of public

transportation as an alternative to individual

transportation in metropolitan areas and Tier 1-3 cities

(CuP2).

Suppliers

The domestic automotive supplier industry projections

account for three major aspects: fragmentation of the

supplier market with respect to the number of competitors;

motivation for preferring specific OEMs; and technological

know-how. The first dimension deliberates whether the

domestic automotive supplier industry has gone through a

consolidation process by the year 2020 in order to achieve

necessary economies of scale (SuP1). This projection may

also indicate increased financial resources for Research and

Development activities (R&D) among others. Whether or

not suppliers make effective use of financial resources and

invest continuously into technological upgrading is the

focus of the third projection, which refers to the Indian

suppliers’ technological competitiveness on international

level (SuP3). The second projection accounts for domestic

suppliers’ internationalization strategies to profit from an

OEM’s international positioning unveiling global growth

potentials (SuP2).

OEMs / Competitors

The OEMs / competitor perspective extends the R&D topic

beyond firm / private efforts and accounts for the potential

of public–private “Research Centers of Excellence” for

automotive technologies (CoP1). Moreover, a strong market

segmentation referring to particular products for clearly

differentiated consumer groups (e.g., some customers may

particularly desire innovative environmental technologies)

and its possible implications are incorporated in the second

projection for this stakeholder group (CoP2).

13

The Government

of India

Potential actions from the Government of India (GOI) are not

only partially in line with the suppliers’ and OEMs’ Industry

Stakeholder Projections, but may be seen as the institutional

way to fortify necessary or desirable developments. The first

projection focuses on incentives for exports by tax reductions

(GoP1). The second projection considers fortified

environmental standards with respect to production and the

lifecycle of a small car (GoP2). The third projection accounts

for public transportation considerations and considers

innovative multimodal transportation systems especially for

metropolitan areas (GoP3).

India’s Society

The frame of India’s Society as a stakeholder is delineated by

an economic component as well as an environmental

component. Whereas the former confines labor market

characteristics – in particular wages of blue-collar workers

(SoP1) – the latter pictures the relevance of environmental

awareness in particular to one’s choice of transportation

(SoP2).

In comparison to the quantitative results of the Industry Environment Projections, the average

probability (48 %), impact (3.5) and desirability (3.5) of the Industry Stakeholder Projections do

not differ substantially for any of the five stakeholder groups (cf. Table 2).

However, the experts have a much lower average consensus distance (Ø 19.6). This delivers

additional implications for the accurate design of roadmaps regarding stakeholder activities (cf.

PEST Roadmaps in the upcoming Chapters 4-7) as one may further elaborate each Stakeholder

Projection’s probability and consensus (cf. Appendix D).

14

No Industry Stakeholder Projections Probability Consensus Impact Desirability Symbol

Cu

sto

me

rs

9

(CuP1) “Safety Perception” in 2020: More than 90% of the current and potential buyers of small cars in India perceive their safety to other passenger cars as equal.

53% 10 3.4 3.4

Likely Strong

Consensus High High

10

(CuP2) “Public Transport” in 2020: Current or potential buyers of small cars in India perceive in 90% of the Metros and Tier1-3 Cities in India public transportation as a convenient alternative.

46% 30 3.7 3.6

Unlikely Strong Dissent

High High

Su

pp

lie

rs

11

(SuP1) “Supplier Consolidation” in 2020: The domestic automotive supplier base (Tier 1-3) has gone through a substantial consolidation process increasing the average turnover of a supplier compared to 2010 by the factor 4.

59% 20 3.6 3.7

▲

Likely Moderate Consensus

High High

12

(SuP2) “Focus: Export Opportunities” in 2020: Domestic automotive suppliers in India prefer foreign automotive OEMs operating in India over domestic OEMs due to higher global market volumes and potential growth opportunities.

53% 17.5 3.3 3.1

Likely Strong

Consensus High High

13

(SuP3) “Technological Upgrading” in 2020: Domestic automotive suppliers in India invest continuously into their technological upgrading and are technologically at par with their European, US or Japanese competitors.

48% 20 3.6 3.8

Unlikely Moderate Consensus

High High

Ind

ust

ry/

OE

Ms 14

(CoP1) “Centers of Excellence” in 2020: The automotive associations in India and the GOI have established public-private partnerships to establish research centers of excellence for all major automotive technology areas.

54% 15 3.7 3.9

∆

Likely Strong

Consensus High High

15

(CoP2) “Differentiated Customers” in 2020: All OEMs selling small cars in India are serving clearly differentiated consumer groups.

37% 25 3.2 2.9

Unlikely Moderate

Dissent High Medium

15

Go

ve

rnm

en

t

16 (GoP1) “Export Promotion” in 2020: The GOI provides 100% tax deductions on export profits.

44% 25 3.7 3.2

■

Unlikely Moderate

Dissent High High

17

(GoP2) “Environmental Organizations” in 2020: The GOI has established a powerful governmental organization that regulates all environmental matters of the production and consumption life cycle of small cars.

49% 20 3.5 3.4

Unlikely Moderate Consensus

High High

18

(GoP3) “Integrated Transport” in 2020: The GOI is actually implementing a total mobility strategy integrating individual and public transportation as well as related infrastructure investments.

42% 20 3.5 3.7

Unlikely Moderate Consensus

High High

So

cie

ty

19

(SoP1) “Labor Laws” in 2020: The Indian society has accepted that more flexible labor laws support the economic growth of the country in general and increased wealth of blue-collar workers in particular.

48% 12.5 3.5 3.3

◊

Unlikely Strong

Consensus High High

20

(SoP2) “Pollution Attitude” in 2020: The Indian society is very sensitive towards any kind of pollution through individual or corporate mobility requirements.

41% 20 3.3 3.6

Unlikely Moderate Consensus

High High

Table 2: Industry Stakeholder Projections: Overview Quantitative Results

In sum, the experts rated the Industry Stakeholder Projections’ probability within a relatively

large range (cf. Figure 3). Also within some stakeholder groups, the experts’ assessments varied

strongly among the corresponding Industry Stakeholder Projections. According to the Delphi

results, experts expect “Differentiated customers” (CoP2) to have neither a high impact nor a

high probability which indicates a lower priority for strategic planning. Yet, increasing efforts in

technological upgrading – which may be concentrated in public-private automotive research

“Centers of Excellence” (CoP1) – seems to be attended by India’s path towards a small car

market hub.

16

Industry Stakeholder Projections

Supplier

Consolidation

Technology

Investments

Pollution Attitude

Differentiated

Customers

Safety Perception

Public Transport

Focus: Export

Opportunities

Centers of ExcellenceExport Promotion

Integrated Transport

Lab

or L

aws

Environmental

Organisations

3,0

3,2

3,4

3,6

3,8

35% 40% 45% 50% 55% 60% 65%

Probability

Imp

act

Figure 3: Industry Stakeholder Projections: Probability and Impact

17

4 Scenario Development for the Political Environment of India’s (Small Car) Automotive Industry in 2020

The political environment is examined referring to GST tax reductions through the Government

of India (GOI) and stricter emission regulations. The first projection concerns a significantly

reduced Goods & Services Tax (GST) rate particularly for the small cars. The latter projection

expects emission regulations across India similar to European standards. At first, both political

projections are matched to create four scenarios for the political environment based on the

input from the scenario development workshop on IIM Bangalore campus. Then, each Industry

Environment Projection is analyzed separately, integrating the various qualitative comments of

the experts and subsequently analyzing why each projection is expected to occur/not to occur in

its respective ‘Roadmap’.

4.1 Political Environment Scenarios

The two Political Environment Projections are combined as two axes in a coordinate system to

sketch four potential scenarios for the political environment of the automotive industry in 2020.

While the x-axis was used to consider the occurrence (right-end) and non-occurrence (left-end)

of the first projections, the y-axis represented the occurrence (upper-end) and non-occurrence

(lower-end) of the corresponding second projection. Each of the four scenarios was jointly

developed and evaluated with regard to its probability of occurrence and potential

consequences for the five industry stakeholder groups during a workshop with local industry

experts on the campus of IIM, Bangalore.

Figure 4 illustrates four scenarios derived from matching the two Industry Environment

Projections for the political environment. According to the Delphi participants’ assessment of the

two Political Environment Projections, the “Costly & Dirty” scenario is the most probable to occur

– both projections were considered improbable. However, in a discussion of the study’s results

with industry experts, the scenarios “Green & Affordable” and “Cheap & Dirty” were rated with a

relatively higher probability to occur (30-40 %). Table 3 summarizes the main results of the

expert discussion and the main consequences of each scenario on the small car industry’s

stakeholders.

18

PP

2: “

Ha

rmo

niz

ati

on

of

Em

issi

on

s”

Hig

h

SCENARIO 1

20% Probability

“GREEN & EXPENSIVE”

SCENARIO 2

30-40% Probability

”GREEN & AFFORDABLE” L

ow

SCENARIO 3

10% Probability

“COSTLY & DRITY”

SCENARIO 4

30-40% Probability

”CHEAP AND DIRTY”

Low High PP1: “Reduced Tax Rates”

Figure 4: Political Environment Scenario Matrix

Scenarios for the Political Environment affecting the (Small Car) automotive industry in India 2020

19

Emission regulations are the same all over India following European standards and small cars are NOT fiscally preferred.

Customers A differentiation between urban and rural car buyers (or any other differentiation) is

necessary. The promotion of small cars will be difficult due to the required higher investments into

low-emission technology. Many low-income buyers might rather invest into other forms of mobility.

Social benefits from the status of owning a “Green” car might be gained for some buyer groups.

Customers have to face higher operating and maintenance costs. Suppliers The harmonized emission standards will require more investments into technology. Higher investments into clean technologies will increase the export potential for the

affected suppliers. OEMs Foreign OEMs have an advantage as they already own the necessary technologies while

domestic players might have higher R&D costs. However, many domestic players have access to the required technologies via collaborations or acquisitions.

All OEMs need to develop only one combined small car strategy for India and the Western markets.

The current collaboration level of OEMs and Associations in India will increase. The application of harmonized standards will improve the global image of the Indian

automotive industry. OEMs will have lower margins as R&D and other related costs to higher emission

standards will not be transferred to consumers. Government The Government of India can set a positive signal towards the global community by

pushing forward the harmonization of emission standards at a high level. On the other hand, the Government of India drives prices up in rural areas through the harmonization, which might not be understood by the rural population.

The Government of India will have to invest significantly to provide the required infrastructure, especially regarding the provision of the suitable petrol/diesel etc.

Society The ecological environment will benefit in the long-run through less emissions. The transportation infrastructure will be negatively affected through slowly growing

numbers of cars on the road leading to even more congestions especially in the urban areas. Moreover, the general availability of cheap small cars will make it even harder to further develop and promote public transportation in urban and rural areas.

Emission regulations are the same all over India following European standards and small cars are fiscally preferred.

Customers A differentiation between urban and rural car buyers (or any other differentiation) is

necessary. The promotion of small cars through tax benefits might only be marginal due to the

required higher investments into low-emission technology. Social benefits from the status of owning a “Green” car might be gained for some buyer

groups. Customers have to face higher operating and maintenance costs. Suppliers The harmonized emission standards will require more investments into technology. Reduced GST (and other taxes) are unlikely to significantly benefit suppliers. Higher investments into clean technologies will increase the export potential for the

affected suppliers. OEMs Foreign OEMs have an advantage, as they already own the necessary technologies while

domestic players might have higher R&D costs. However, many domestic players have access to the required technologies via collaborations or acquisitions.

All OEMs need to develop only one combined small car strategy for India and the Western markets.

The current collaboration level of OEMs and Associations in India will increase. The application of harmonized standards will improve the global image of the Indian

automotive industry while the reduced taxes will lead to higher sales of small cars leading to improved economies of scale

Government Decrease of tax revenues due to lower taxes for small cars might be partially

compensated by the higher number of small cars sold. The Government of India can set a positive signal towards the global community by

pushing forward the harmonization of emission standards at a high level. On the other hand, the Government of India drives prices up in rural areas through the harmonization which might not be understood by the rural population.

The Government of India will have to invest significantly to provide the required infrastructure, especially regarding the provision of the suitable petrol/diesel etc.

Society The ecological environment will benefit in the long-run through less emissions. The transportation infrastructure will be negatively affected through even higher

numbers of cars on the road leading to even more congestions especially in the urban areas. Moreover, the availability of cheap small cars will make it even harder to further develop and promote public transportation in urban and rural areas.

Scenarios for the Political Environment affecting the (Small Car) automotive industry in India 2020

20

Emission regulations in India are NOT following the higher European standards and small cars are fiscally NOT preferred.

Customers The demand for small cars is not specially promoted. Smaller consumer groups in urban areas might offer a niche for low-emission cars in

India. Suppliers The lower emission standards do not require additional investments into clean

technology development nor force domestic suppliers into collaborations with foreign players.

The missing investments into clean technologies will keep suppliers away from exporting to Western markets but might lead to interesting business opportunities in South-East Asia.

OEMs OEMs, if they want to export as well and increase their economies of scale, will have to

handle their operations with two different standards – the “Indian” and the “Western (e.g. European)” emission norms. This creates severe challenges to the supply chain, operations and supplier network management that might neutralize the benefits from the increased economies of scale.

All OEMs need to develop then different small car strategies for the high-emissions mass market in India and maybe South-East Asia, the low-emissions driven Western markets and the low-emission niche market in India.

In the short-to mid-term the margins and sales volume in India will be more attractive but the lower investments into technologies will affect the technological competitiveness of domestic OEMs in the long run.

Government Tax revenues stay stable and fuel the Government of India’s bank account. The Government of India faces significant pressure from the global community and

domestic “green” interest groups to follow “Western (e.g. European)” standards. Society The ecological environment will get affected in the long-run through more emissions. The transportation infrastructure will be slowly negatively affected through the

growing number of cars.

Emission regulations in India are NOT following the higher European standards and small cars are fiscally preferred.

Customers The promotion of small cars through tax benefits will lead to increased demand

especially in rural or semi-urban areas because consumers have the lowest possible buying and operating/maintenance costs.

Smaller consumer groups in urban areas might offer a niche for low-emission cars in India.

Suppliers The lower emission standards do not require additional investments into clean

technology development nor force domestic suppliers into collaborations with foreign players.

The missing investments into clean technologies will keep suppliers away from exporting to Western markets but might lead to interesting business opportunities in South-East Asia.

Reduced GST (and other taxes) are unlikely to significantly benefit suppliers. OEMs OEMs, if they want to export as well and increase their economies of scale, will have to

handle their operations with two different standards – the “Indian” and the “Western (e.g. European)” emission norms. This creates severe challenges to the supply chain, operations and supplier network management that might neutralize the benefits from the increased economies of scale.

All OEMs need to develop then different small car strategies for the high-emissions mass market in India and maybe South-East Asia, the low-emissions driven Western markets and the low-emission niche market in India.

In the short-to mid-term the margins and sales volume in India will be more attractive but the lower investments into technologies will affect the technological competitiveness of domestic OEMs in the long run.

Government Decrease of tax revenues due to lower taxes for small cars might be partially

compensated by the higher number of small cars sold. The Government of India faces significant pressure from the global community and

domestic “green” interest groups to follow “Western (e.g. European)” standards. The Government of India sets clear focus on cheap individual mobility despite the

existing traffic congestion problems and the impact on the ecological environment. Society The ecological environment will get affected in the long-run through more emissions. The transportation infrastructure will be negatively affected through even higher

numbers of cars on the road leading to even more congestions especially in the urban areas. Moreover, the availability of cheap small cars will make it even harder to further develop and promote public transportation in urban and rural areas.

Table 3: Political Environment Scenarios: Consequences for Industry Stakeholders

21

4.2 Reduced Tax Rates for Small Cars in 2020 (PP1)

The industry experts rate the average probability of the “Reduced Tax Rates” projection at 46 %

(cf. Table 4): the Government of India is not expected to implement a reduced Goods & Services

Tax (GST) rate for small cars. The experts are at odds regarding this judgment. Impact and

desirability are both considered high.

No Industry Environment Projections Probability Consensus Impact Desirability

1 (PP1) 2020: The GST for small cars in India is

a third of the tax rate for all other kinds of passenger cars

46% 32.5 3.4 3.3

Unlikely Strong Dissent

High High

Table 4: Political Industry Environment Projection PP1

The consensus analysis reveals that the experts slightly converge with their probability ratings

towards 40-60 % (cf. Figure 5) and two out of five experts do not expect the “Reduced Tax

Rates” projection to occur.

Reduced Tax Rates

0%

10%

20%

30%

40%

50%

60%

0% < 20% 20% < 40% 40% < 60% 60% < 80% 80% → 100%

Probability

Delp

hi P

art

icip

an

ts

Figure 5: Consensus Analysis for “Reduced Tax Rates” Projection PP1

4.2.1 Analysis of the Industry Expert’s Arguments on Projection PP1 (Reduced Tax Rates)

(PP1) 2020: The GST (Goods & Service Tax) for small cars in India is a third of the tax rate for all

other kinds of passenger cars

A reduced Goods & Service Tax (GST) exclusively for small cars is considered rather unlikely

(Probability 46 %), but with a strong dissent among experts (Consensus Distance: 32.5).

22

Probability

Given that the small car market in India is expected to continuously experience high compound

annual growth rates (CAGRs), the experts do not expect any governmental support in terms of

reduced tax rates to further boost this industry. Moreover, since a main idea of the GST is to

implement a single tax rate along several consumption areas and products, the Government of

India (GOI) does, according to the experts, not consider an exclusive treatment of small cars as

feasible. In addition, a reduced GST would most probably influence not only new car purchases,

but the domestic resale-market, too. The consequences of such a market intervention are highly

insecure and will probably lead to negative side effects that have not been considered yet.

However, the implementation of a reduced tax rate for a limited time frame of 5 years with a

moderate tax reduction (less than one third) might propel the industry according to some

experts. The GOI could benefit from additional tax revenues from the small car market since the

increase in demand could be high in both rural and urban areas. Therefore, a tax reduction could

balance or even increase total tax revenues due to higher sales volumes of small cars. Moreover,

subsidies via a reduced GST also support the automotive industry to achieve higher volumes and

might thereby increase affordability of small cars for a larger percentage of the Indian

population and make their domestically produced cars more competitive in other markets.

Another positive side effect of a reduced GST for small cars in 2020 is the potential motivation

for consumers to purchase car models with comparable lower fuel-consumption per mile.

Thereby, potential shortages in fuel imports can be counteracted proactively as well as overall

CO2 emissions per mile may be reduced. However, detailed calculations with respect to fuel

savings through cars with smaller engines as compared to the increased number of cars have to

be executed in the future.

Impact

According to some experts, a reduced tax rate for small cars can have a positive impact on a

sustainable industrial growth of India’s economy. The impact on the industry is thus considered

high among experts – especially manufacturers of small cars are expected to benefit significantly

from the reduced GST. Furthermore, the increase in new car registrations and total car

penetration rate in India is assumed to induce a further step for the development of the

domestic automotive industry’s competitiveness to finally aim for the international market.

Desirability

Since the GOI’s vision is to become a small car market hub, a reduced GST is highly desirable. An

implementation supports not only further growth of the small car segment but also affordability

for consumers. As mentioned, there might even be a positive environmental impact since small

cars have comparable lower emissions than large sedans.

23

4.2.2 Roadmap for Projection PP1 (Reduced Tax Rates)

Figure 6 illustrates the influences of different Industry Stakeholder Projections on the Industry

Environment Projection PP1 “GST Reduction” based on significant correlations identified by the

quantitative analysis using SPSS (cf. Appendix A). The potential influences on PP1 are structured

along the five stakeholder groups (Government, Customers, Suppliers, Industry, and Society).

Each arrow’s color in Figure 6 indicates the influence in respect of the Industry Environment

Projection’s probability (green for enabling; yellow for hindering).

PP1: 2020: The Government of India (GOI) has introduced a reduced GST for small cars.

An Analysis why it is unlikely to happen (PP1 Probability: 46 %)

Figure 6: Influences on Political Industry Environment Projection 1 (PP1)

Projections involved Enabling: SuP2, CoP1, GoP1 Hindering: CuP1, SuP3, GoP2, GoP3, SoP2 The following analysis is based on a quantitative correlation analysis as well as qualitative content

analysis between the Industry Environment Projection PP1 and all other projections of the study.

The roadmap draws on both the experts’ input and additional desktop research.

24

New car registrations in India experience impressive CAGRs and especially in metropolitan

areas the hitherto infrastructure capacity is often insufficient to cope with the rise in traffic. The

GOI (Government of India) is unable to cope adequately with the resulting rise in traffic

congestion and CO2 emissions. As a consequence, the society in the urban areas of India has

become more sensitive towards any kind of pollution (SoP2) and in general prefers to purchase

small cars due to their perceived lower emissions. Furthermore, the insufficient infrastructure

provision negatively affects the transportation sector and, as a result, the economic development

in general. The GOI thus experiences increased pressure especially from the manufacturing and

retail sector to improve the situation.

Therefore, the GOI not only clearly regulates the environmental impact of the production and the

lifecycle management for cars in India (GoP2) to achieve maximum efficiency but also

substantially invests in infrastructure development to alleviate the traffic situation in

metropolitan areas and Tier 1-3 cities (GoP3). In addition, the GOI introduces increased safety

standards for cars to lower the number and severity of traffic accidents as the Indian car buyers

are not sufficiently aware of the relatively low safety standards and features of the popular small

cars (CuP1) – as compared to trucks and buses. These new safety regulations enforce domestic

firms to invest in technological upgrading along the value chain (SuP3). However, the increased

infrastructure investments and the new regulations prove insufficient to manage the traffic and

emission situation in most metros and Tier 1-3 cities. The GOI has to acknowledge that this is

primarily due to the absolute number of cars on the streets. Although small cars produce

relatively lower emissions and may be preferred by many consumers, the GOI is therefore highly

unlikely to subsidize those purchases (PP1).

As a consequence, Indian automotive firms have to comply with new regulations (on

environment & safety). At the same time domestic suppliers are quite successful in technological

upgrading – they even are at par with their international competitors (SuP3). This enables

domestic suppliers to explicitly target foreign OEMs in order to benefit from potential growth

opportunities in the international market (SuP2). The global market seems additionally

attractive, since the GOI has introduced tax deductions on export profits (GoP1) in order to

incentivize domestic firms to compete on international level.

Overall, the GOI has a focus on the long-term competitiveness of the domestic industry – and

even funds public-private research centers to support technological upgrading (CoP1). This

again implies subsidies to support short-term domestic growth of new small car registrations to

be very unlikely (PP1).

25

4.3 Harmonization of Emission Standards (PP2)

The industry experts rate the average probability of the “Harmonization of Emission Standards”

projection at 47% (cf. Table 5): the Government of India is not expected to implement

standardized emission regulations all over India comparable to European norms. The experts

are at odds regarding this judgment. Impact and desirability are both considered high.

No Industry Environment Projections Probability Consensus Impact Desirability

2 (PP2) 2020: The emission regulations in all regions of India are the same as in Europe

47% 30 3.4 3.6

Unlikely Strong Dissent

High High

Table 5: Political Industry Environment Projection PP2

The consensus analysis reveals that the experts slightly converge with their probability ratings

towards 40-60 % (cf. Figure 7) and nearly two out of five experts do not expect the

“Harmonization of Emissions” projection to occur.

Harmonization of Emissions

0%

10%

20%

30%

40%

50%

60%

0% < 20% 20% < 40% 40% < 60% 60% < 80% 80% → 100%

Probability

Delp

hi P

art

icip

an

ts

Figure 7: Consensus Analysis for “Harmonization of Emissions” Projection PP2

26

4.3.1 Analysis of Expert’s Argument on Projection PP2

(PP2) 2020: The emission regulations in all regions of India are the same as in Europe.

A consistent nationwide upgrade of the emission regulations towards European standards is

neither considered probable (Probability: 47 %), nor do experts share a consensus (Consensus

Distance: 30.0) on this aspect.

Probability

A main concern is that the timeframe is too short since the GOI has not even been able to

harmonize the emission norms across the country so far. Besides, emission norms are in many

cases simply not abided to in India. The enormous geographical size makes India rather a

continent than a country, which seems to posit quite a few challenges. For example, fuel quality

also varies considerably among geographical regions.

Moreover, a raise of emission standards induces a rise in purchase prices due to more expensive

low-emission technologies – which the domestic automotive industry is not able to offer yet.

Therefore, the GOI is expected to prevent a harmonization of emission regulations with

European standards even though this might be desirable in terms of environmental protection

and potential increases in tax revenues (by taxing vehicles with higher emissions higher).

According to the experts, the GOI seems to be under pressure by civil and environmental

protection organizations which might lead to a change at least in the policy till 2020: Rising

environmental awareness obligates the GOI to reduce the gap to Euro-Norms at a rapid pace.

This is the opinion of a few experts. Historically, India is behind Europe on emission norms,

which were implemented in 1984 for the first time, followed by specifications for petrol vehicles

in 1991 and for diesel vehicles in 1992. Moreover, the GOI has already enforced emission

standards and aims to follow European standards and test procedures for cars. As of today,

many of the metropolitan cities have implemented Euro 4 and have additionally outlined a road

map for lowering emissions. In the long run, the GOI has no other option but to fortify

environmental regulations since also emerging economies will have to comply with

environmental norms as per WTO agreements. Furthermore, a future scarcity of natural

(energy) resources demands a sustainable perspective, which may also be emphasized by a

much stronger environmental awareness of India’s society.

Impact

In this respect, higher emission norms have a high impact on the vehicle production cost and

technological requirements due to the necessary utilization of advanced low-emission

27

technologies that are currently not yet locally produced. Customers may perceive an increase in

ownership quality although risen purchase prices place additional burdens on the majority of

car buyers that will by far outweigh the perceived contribution to “saving the planet”.

With regard to the domestic automotive industry, emission regulations towards European

standards imply substantial R&D investments at an early stage to achieve technological

upgrading in order to comply and to offer the required components and end products. Since this

may unveil potential growth opportunities in the global market, the GOI is likely to oblige the

domestic industry to invest a remarkable percentage of revenues in R&D – but thereby lowering

domestic firms’ margins for other investments. Domestic automotive firms are required to

change their entire positioning (e.g., product portfolio, manufacturing processes, and marketing

strategies).

The costs of technological development are a major concern for the industry and are estimated

to result in Joint Ventures, Alliances, or Mergers and Acquisitions. On the flipside, alternative

propulsion systems may be additionally promoted by the GOI to support the development of a

technological competitive domestic industry.

Desirability

Nevertheless, this outcome is highly desirable because the continuously increasing car

penetration rate induces more environmental pollution. It is considered essential to reduce

emissions per unit sold – at least. Furthermore, enforcing technological upgrading of the

domestic automotive industry at an early stage will support a positioning in the global car

market with high-quality Indian products.

4.3.2 Roadmap for Projection PP2

Figure 8 illustrates the influences on the “Harmonization of Emissions” Projection based on

significant correlations assessed by quantitative analysis (cf. Appendix A). The potential impacts

on PP2 are structured along the five stakeholder groups (Government, Customers, Suppliers,

Industry, and Society). Each arrow’s color in Figure 8 indicates the influence in respect of the

Industry Environment Projection’s probability (green for enabling; yellow for hindering).

PP2: 2020: The emission regulations in all regions of India are the same as in Europe.

An Analysis why it is unlikely to happen (PP2 Probability: 47 %)

28

Figure 8: Influences on Political Industry Environment Projection (PP2)

Projections involved Hindering: CuP2, SuP3, CoP2, GoP2, GoP3, SoP1; VP2, SP1, IP1, IP2

The following analysis is based on a quantitative correlation analysis as well as qualitative content

analysis between the Industry Environment Projection PP2 and all other projections of the study.

The roadmap draws on both the experts’ input and additional desktop research.

CO2 emissions in India are rising considerably due to the increase of industrial growth and

traffic. In the long-term, this may become a challenging aspect and the Government of India is

likely to experience pressure to take responsibility and implement strict environmental

regulations.

By 2020, the economic growth in India has continued at an impressive pace and has led to an

overall increase in the society’s wealth – but environmental pollution has risen as well. Due to an

early implementation of flexible labor laws, the GOI manages to support not only economic

growth but also the increase of society’s wealth (SoP1). India’s society has become increasingly

aware of environmental pollution and adapts a lifestyle towards a “Green Society” – even the

social acceptance of small cars depends on whether they comply with low-emissions standards

29

or not (SP1). Quite a few consumers are also willing to pay a higher price for a car to fit their

specific requirements via additional features, luxurious extras, fuel-efficiency, or a high safety

standard. Consequently, the small car market is clearly split into a low-cost/high-emission and a

high-cost/low-emission segment (CoP2).

In order to deliver the required high-quality (-technology) components, domestic suppliers have

to invest increasingly in technological upgrading (SuP3). In this context, the GOI realizes the

importance of human capital at an early stage and it ensures that the established education

system provides sufficient engineers to advance the domestic (automotive) industry’s

technological competence (IP1); domestic suppliers are able to succeed in their technological

upgrading and can compete on an international level (SuP3).

However, some of the domestic suppliers may lack financial capabilities and are tempted to

benefit from a strong integration into a foreign OEM’s domestic supplier network with respect to

technological spill-overs (VP2). In parallel, the considerable growth of the small car market has

intensified an overall shortage in resources; and the GOI acknowledges that this situation should

be improved by demanding higher efficiency in production and recycling. Besides, pressure from

international organizations has increased. As a result, the GOI implements an organization to

assure overall efficiency of production and life cycle of small cars – additionally regulating the

environmental impact (GoP2).

Furthermore, the GOI starts implementing a multi-modal passenger transportation system

(GoP3) and increases infrastructure investments (IP2) to ensure sufficient transportation

capacity required for further economic growth. Especially in metropolitan areas, inhabitants

benefit from these infrastructure investments. They perceive public transportation increasingly

as a convenient alternative to car ownership (CuP2).

Still, the GOI has so far been primarily driven by economic interests and not by society’s

environmental interests. The implementation of strict emission regulations is rather seen as a

hindrance for economic development and the GOI does not consider drastic steps required to

protect the environment – such as raising the emission regulations to European standards (PP2).

30

5 Scenario Development for the Economic Value Chain of India’s (Small Car) Automotive Industry in 2020

The economic perspective of the small car industry in India is examined in the light of the

market structures on OEM and supplier level. The first projection evaluates a dominant position

of foreign OEMs in the Indian small car market, whereas the second projection refers to the

establishment of proprietary domestic supplier networks. At first, both Value Chain Projections

are matched to create four scenarios for the economic value chain based on the input from the

scenario development workshop on IIM Bangalore campus. Then, each projection is analyzed

separately, integrating the various qualitative comments of the experts and subsequently

analyzing why each projection is expected to occur/not to occur in its respective ‘Roadmap’.

5.1 Economic Value Chain Scenarios

The two Value Chain Projections are combined as two axes in a coordinate system to sketch four

potential scenarios for the economic value chain of the automotive industry in 2020. While the x-

axis was used to consider the occurrence (right-end) and non-occurrence (left-end) of the first

projections, the y-axis represented the occurrence (upper-end) and non-occurrence (lower-end)