inclusive international agricultural value chains: the case of coffee in ethiopia

TRANSCRIPT

Inclusive international agricultural value chains: The case of coffee in Ethiopia

Bart Minten

Geneva – WTO September 29, 2016

1

Outline

1. Gender and agriculture in Ethiopia

2. Gender and coffee

3. The potential of certification

1. Gender and agriculture in Ethiopia

• 80 percent of the population residing in rural areas

• Women majority of the agricultural labor in these communities.

• Women’s access to resources and community participation are usually mediated through men, either their fathers or husbands

• When women have access to their own income, they are more likely than men to spend it on the betterment of their families and successfully participate in village savings or pay school fees for their children.

• Higher empowerment of women also linked to better nutrition

1. Gender and agriculture in Ethiopia

WEAI=1: Women completely empoweredWEAI=0: Women completely disempowered

[production; resources; income; leadership; time]

0.60.70.80.9

1

Women Empowerment Agriculture Index

1. Gender and agriculture in Ethiopia

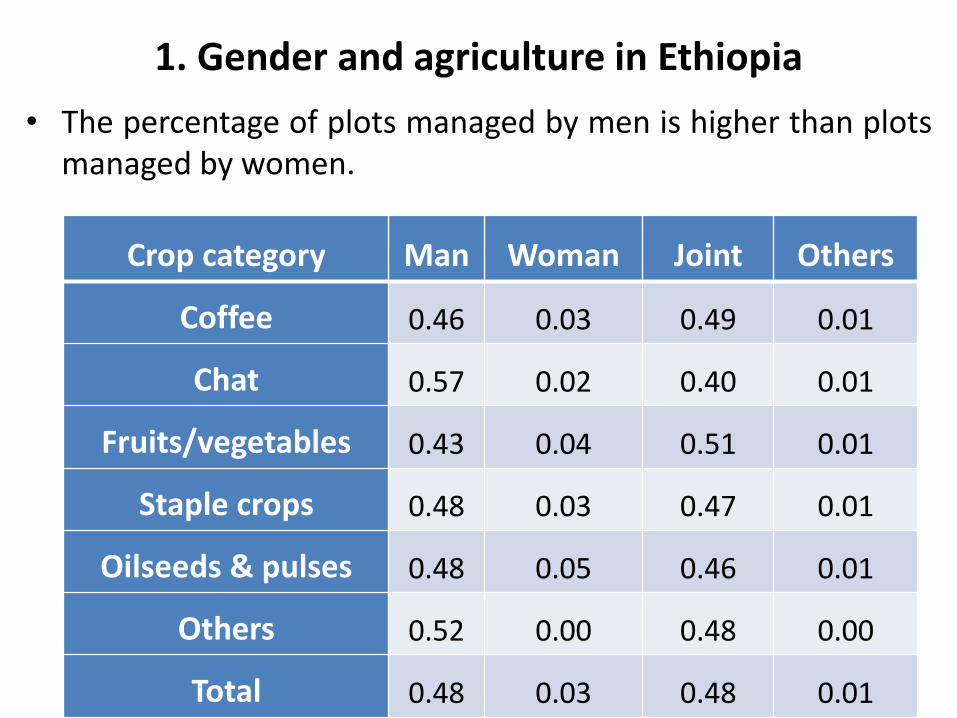

• The percentage of plots managed by men is higher than plotsmanaged by women.

Crop category Man Woman Joint Others

Coffee 0.46 0.03 0.49 0.01

Chat 0.57 0.02 0.40 0.01

Fruits/vegetables 0.43 0.04 0.51 0.01

Staple crops 0.48 0.03 0.47 0.01

Oilseeds & pulses 0.48 0.05 0.46 0.01

Others 0.52 0.00 0.48 0.00

Total 0.48 0.03 0.48 0.01

6

2. Gender and coffee

• Coffee in Ethiopia:- Most important African coffee exporter; 10th biggest

coffee exporter in the world; 3% of the internationalmarket

- Coffee about a quarter of the value of Ethiopia’s exports- Income for over 4 million farmers- Important role in social gatherings as well as for local

consumption (half of production consumed locally)

2. Gender and coffee

53%

3%

44%

Responsibility of farming on the plot

Man Woman Both

47%48%

3%

2%

Right to decide what to grow on parcel

Man Both Woman Community(outside hh)

2. Gender and coffee

• Labor:- men are highly engaged in most of the coffee production

activities- women are mainly engaged in harvesting and post-harvesting

activities

Male-Adult Female-Adult Child

Tree management 88 8 4

Mulching 84 12 5

Tilling/ hoeing 91 5 4

Manure and compost application 63 30 8

Weeding 86 8 5

Chemical fertilizer 90 8 3

Harvesting 68 24 8

Post-harvest activities 58 37 5

Total time 78 16 6

• Sales mostly done by men; they control income (as is the caseof most cash crops in developing countries).

2. Gender and coffee

0

20

40

60

80

Adult men Adult woman Child Mix

Dry cherry Red cherry

3. The potential of certification

• Growing emphasis on Voluntary SustainabilityStandards (VSS) practices globally, inresponse to social/environmental pressure

• VSS rapidly taking off in the world

0

5

10

15

20

2005 2010 2015

%

Ethiopia World

3. The potential of certification

• One desired impact for sustainability standards systems is sometimes gender equality.

• These standards systems track gender equality and female representation through the supply chain.

• For example, a critical criterion for certification to the Sustainable Agriculture Network standard, (which forms the backbone of the Rainforest Alliance ecolabel): workers cannot be discriminated against on the basis of religion, gender or race.

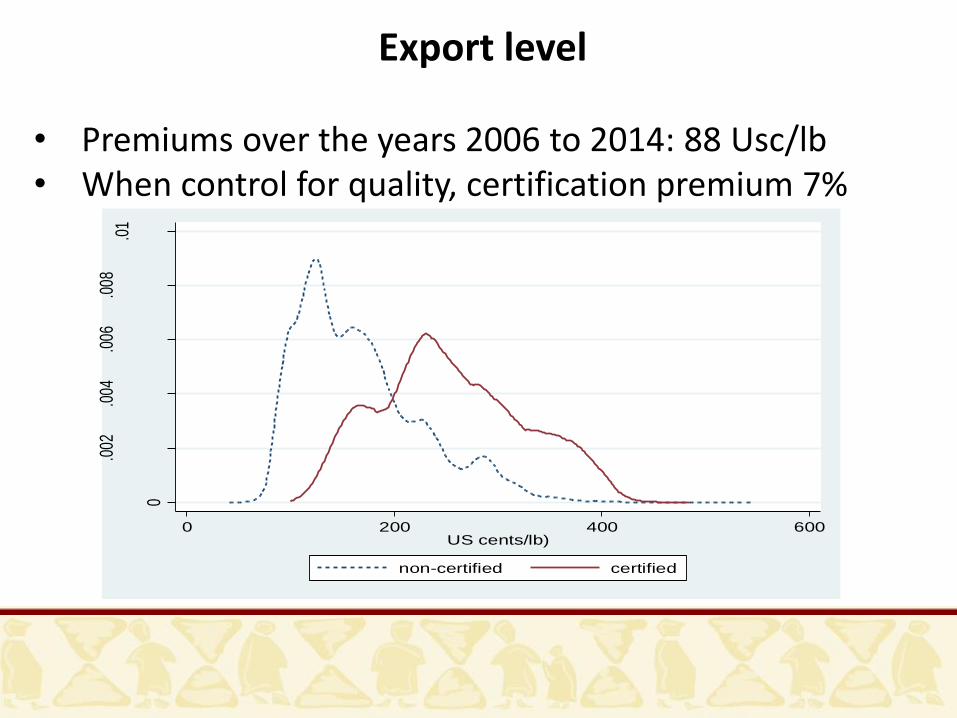

Export level

• Premiums over the years 2006 to 2014: 88 Usc/lb• When control for quality, certification premium 7%

0

.002

.004

.006

.008

.01

Den

sity

0 200 400 600US cents/lb)

non-certified certified

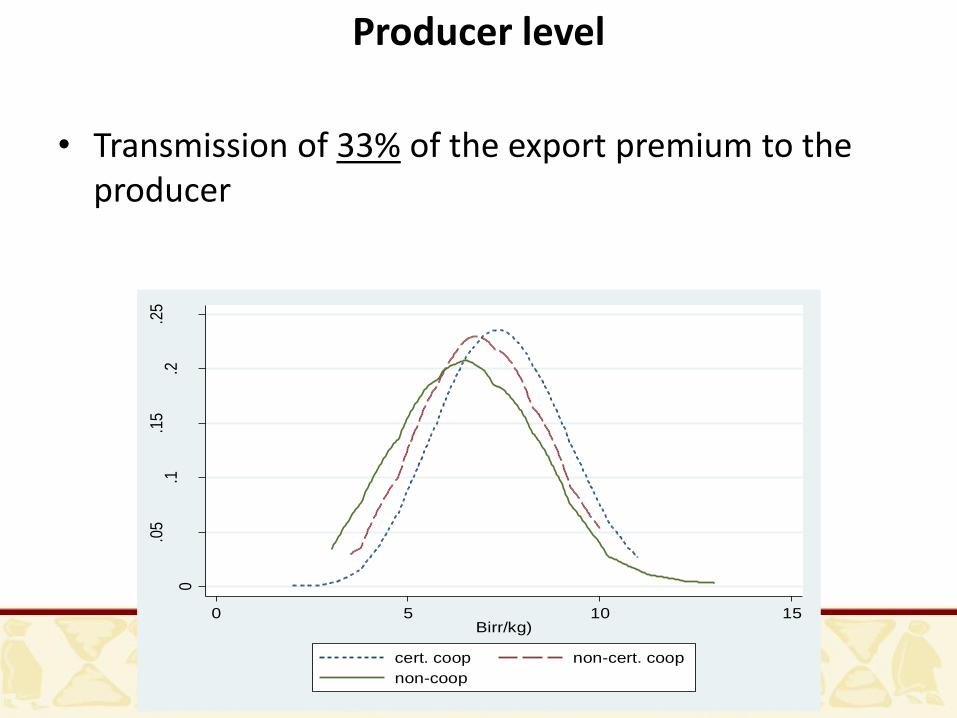

• Transmission of 33% of the export premium to the producer

Producer level

0

.05

.1.1

5.2

.25

Den

sity

0 5 10 15Birr/kg)

cert. coop non-cert. coop

non-coop

• Two-thirds of the quality premium not transmitted. Where did it go?

1. Overheads. 30% of premiums goes to unions, to pay for doing deals, aggregation, etc. Certification costs. 3 USc/lb (about 20% of the premium). Sometimes paid by unions; sometimes by primary cooperatives.

2. Cooperative use of premiums. Mostly investments in communal assets such as schools, roads, etc. but also offices, cars, etc.

3. Repayments of debts. Bought coffee at too high a price; price dropped and losses were incurred. Also loans for wet mills that have to be repaid.

What explains the gap?

Potential of certification

• Median coffee farmer in Ethiopia sells 400 kgs of red cherries equivalent; If all sold certified and all sold as red cherries, it would increase his income with 144 Birr per year or 7.5 USD per year…; Even if assumed complete efficiency (100% transmission), increased annual income of 20 USD per year…

• In current form, little incentives to change practices; explains slow growth of VSS in Ethiopia

Potential of certification

• Test if desired indicators of certification are really different (technology adoption; organic practices; labor of children; schooling of children);

[In tested certification schemes unfortunately no explicit gender target]

• In general, some evidence that there are benefits on these indicators from being a member but results not that strong

• Therefore, still issues with implementation of these certification schemes in these settings