in⁄ation, de⁄ation, and debt - booth school of business · interest rates 08-09 aug08 sep08...

TRANSCRIPT

Inflation, Deflation, and Debt

John H. Cochrane

University of Chicago Booth School of Business

October 14, 2010

Fiscal theory

I

# Shares × Price = Expected discounted dividends

I

Money + Gov’t DebtPrice level

= Expected discounted surpluses

I(Money+Deposits) × Velocity = Price × Income

Fiscal theory

I

# Shares × Price = Expected discounted dividends

I

Money + Gov’t DebtPrice level

= Expected discounted surpluses

I(Money+Deposits) × Velocity = Price × Income

Classic doctrines

Money + Gov’t DebtPrice level

= Expected discounted surpluses

I Money vs. Debt?I Inside vs. outside?I Peg rates, “provide liquidity.”I Deficits and inflation.

Interest rates 06-10

J u l06 J an07 J u l07 J an08 J u l08 J an09 J u l09 J an10 J u l100

1

2

3

4

5

6

7

8

9

10

10 y gov t3 mo gov t

BAA

AAA

FF

Interes t R ates

Long rates, TIPS, inflation and expected inflation

Mar05 Oc t05 May 06 N ov 06 J un07 D ec 07 J ul08 J an09 Aug09 Mar100

1

2

3

4

5

6C oreπ10 y ear treas .10 y ear index ed

Fighting recessions and deflations

Money+Gov’t DebtPrice level

= Expected discounted surpluses

I Cause? Discounted.I Tools?

1. Rates = 0?2. Quantitative Easing I — short bonds.3. Quantitative Easing II — long bonds.4. Quantitative Easing III —private/government debt.5. Announcements: Desperation?6. Helicopter drops?

Quantitative easing I II III, Debt Operations

Jan08 Apr08 Jul08 Oct08 Jan09 Apr09 Jul09 Oct09 Jan10 Apr10 Jul100

0.5

1

1.5

2

Treasuries

Agencies

TALF, CP, Lending, etc. Mbs

Federal Reserve Assets

$,Tr

illion

s

Jan08 Apr08 Jul08 Oct08 Jan09 Apr09 Jul09 Oct09 Jan10 Apr10 Jul100

0.5

1

1.5

2

Currency

Treasury

Reserves

Other

Federal Reserve Liabilities

$,Tr

illion

s

Announcements

Fighting inflation

Money + Gov’t DebtPrice level

= Expected discounted surpluses

Real primary surplus / GDP

1950 1960 1970 1980 1990 2000 2010

6

4

2

0

2

4

6

Real Primary Surplus / GDP

Date

Per

cent

Fighting inflation

Money + Gov’t DebtPrice Level

= Expected discounted surpluses

I “Unsustainable” long-run deficitsI Nominal credit guarantees (houses), government salaries,pensions, state/country bailouts.

I Present value Laffer curve: slow growth is the enemy.

PVt =τYtr − g

∂ logPV∂ log τ

= 1+∂ logY∂ log τ

+1

r − g∂g

∂ log τ

I τ = 30→ 35% = 15% reduction in Y .,I τ = 30→ 35% = 0.3% reduction in g !

Inflation scenario

2007 2008 2009 2010 2011 2012 2013 2014 2015 20160

2

4

6

8

10

12

20

10

5

4

3 2 1

Inflation

← s shock

Bond yield reaction

Date

Yie

ld

Inflation scenario —New Keynesian+fiscal model

0 2 4 6 8 10 12 142

0

2

4

6

8

10

12

14Response to delayed inflation

time

perc

ent

y

r

π

i

Is the Fed Worried?

“Measures of underlying inflation have trended lowerin recent quarters and, with substantial resource slackcontinuing to restrain cost pressures and longer-terminflation expectations stable, inflation is likely to besubdued for some time.”

(FOMC August 10 2010)

Fed view

Fed r→other r→"demand"→ "slack," "gaps"→→ inflationOther shocks↗ expectations, costs↗

Phillips curves don’t work

4 5 6 7 8 9 10 110

1

2

3

4

5

6

84

8586

87

88

8990

91

92

93

949596

979899

4

5 6

7 8

910

Unemployment

Infla

tion

Inflation and unemployment, 19842009

Phillips curves don’t work —70s

3 4 5 6 7 8 9 10 110

2

4

6

8

10

12

14

66

6768

69

70 71

72

73

74

75

76

7778

79

8081

82

8384

Unemployment

Infla

tion

Inflation and unemployment, 19661984

I Inflation can break out despite “slack!”

Better monetary/fiscal arrangements

Money + Gov’t DebtPrice level

= Expected discounted surpluses

I New tools?

1. Modern Commodity standard?2. CPI futures/TIPS spread?3. Long term debt4. “Government equity”

More

“Fiscal theory of the price level”

1. “Understanding Policy”

2. “Money as Stock”

3. “Long Term Debt and Optimal Policy”

4. “Determinacy and Identification in New-Keynesian Models”

5. “A Frictionless view of US inflation”

6. Etc., Etc., Etc.

http://faculty.ChicagoBooth.edu/john.cochrane/research/Papers/

SPARE GRAPHS FOLLOW

Greece and Euro

Money + Gov’t DebtPrice Level

= Expected discounted surpluses

I Debt vs. Equity; inflation vs. defaultI Currency union and fiscal unionI “Optimal currency area”I Commitment to pay ex-post lets you borrow more ex-anteI “Capital ratios”— long term debtI “Government equity?”

Price levels 06-10

May06 Nov06 Jun07 Dec07 Jul08 Jan09 Aug09 Mar10195

200

205

210

215

220

225

Inde

x, 1

983

= 1

00

Price levels

AllCoreHousing

Note food&energy, housing

Inflation 06-10

May06 Nov06 Jun07 Dec07 Jul08 Jan09 Aug09 Mar103

2

1

0

1

2

3

4

5

6

Per

cent

, ch.

from

a y

ear a

go

Inflation

AllCoreHousing

Interest rates and inflation? Interest rates 08-09

Aug08 Sep08 Oc t08 N ov 08 D ec 08 J an09 Feb09 Mar09 Apr09 May 09 J un09 J u l090

1

2

3

4

5

6

7

8

9

10

10 y gov t

3 mo gov t

BAA

AAA

1 Mo fin . C P

1 Mo N F C P

FF

C r is is

C r is is ends , inflation?

Interes t R ates

Crisis/credit risk premium! Inflation? Low rates = loose policy?“Fed sets rates?”

Interest rates 06-10

J u l06 J an07 J u l07 J an08 J u l08 J an09 J u l09 J an10 J u l100

1

2

3

4

5

6

7

8

9

10

10 y gov t3 mo gov t

BAA

AAA

FF

Interes t R ates

Long rates, TIPS, inflation and expected inflation

Mar05 Oc t05 May 06 N ov 06 J un07 D ec 07 J ul08 J an09 Aug09 Mar100

1

2

3

4

5

6C oreπ10 y ear treas .10 y ear index ed

What do long rates tell us, really?

Oct65 Apr71 Oct76 Mar82 Sep87 Mar93 Sep98 Feb04 Aug090

2

4

6

8

10

12

14

1610 year treas.1 year treas

Usual cyclical pattern

Long rates do not forecast inflation!

Oct65 Apr71 Oct76 Mar82 Sep87 Mar93 Sep98 Feb04 Aug090

2

4

6

8

10

12

14

16Core π10 year treas.

Do long rates today tell you where future inflation will be?Long rates did not warn of 70s inflation, 80s disinflation “

Long rates do not forecast inflation!

2 4 6 8 10 12 14 161

2

3

4

5

6

7

8

9

10

10 Year Yield

5 ye

ar in

flatio

n

x: 10 year treasury y: inflation in next 5 years

Long rates do not forecast inflation!

4 3 2 1 0 1 2 3 48

6

4

2

0

2

4

6

101 Yield Spread

5 ye

ar c

hang

e in

infla

tion

Why not? 1) risk premium obscures inflation 2) inflation is notforecastableWe have to think! Pundits?

Different opinions? Different theories! You choose!I Fed view

Fed r→other r→"demand"→ "slack," "gaps"→→ inflationother shocks↗ costs, expectations↗

("Credit constraints" vs. "Old-Keynesian")I New-Keynesian view

πt ↑ =⇒ it ↑↑ =⇒ πt+1 ↑↑

“Coordinate expectations on unique local equilibrium”I Monetarist view

MV = PY

Today’s M → tomorrow’s P? Deficits → more M?I Fiscal theory

Money + Gov’t DebtPrice level

= Present value [Real primary surpluses ]

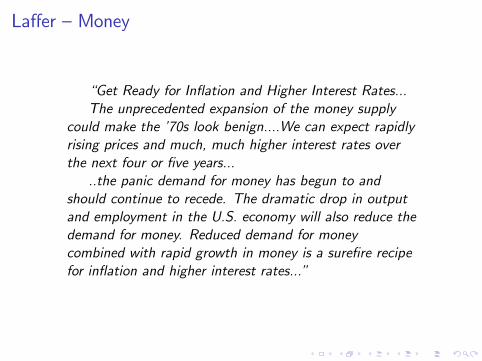

Laffer —Money

“Get Ready for Inflation and Higher Interest Rates...The unprecedented expansion of the money supply

could make the ’70s look benign....We can expect rapidlyrising prices and much, much higher interest rates overthe next four or five years.....the panic demand for money has begun to and

should continue to recede. The dramatic drop in outputand employment in the U.S. economy will also reduce thedemand for money. Reduced demand for moneycombined with rapid growth in money is a surefire recipefor inflation and higher interest rates...”

Laffer —Money

http://online.wsj.com/article/SB124458888993599879.html

Feldstein —Money, and deficits can tempt monetizationInflation is looming on America’s horizonThe unprecedented explosion of the US fiscal deficit

raises the spectre of high future inflation...There is amplehistoric evidence of the link between fiscal profligacy andsubsequent inflation....the large US fiscal deficits are being accompanied

by rapid increases in the money supply...The excessreserves of the banking system have ballooned from lessthan $3bn a year ago to more than $700bn (€536bn,£ 474bn) now.The money supply consists largely of

government-insured bank deposits that households andbusinesses are holding because of a concern about theliquidity and safety of other forms of investment. Butthis could change when conditions improve, turning thesemoney balances into sources of inflation.

http://belfercenter.ksg.harvard.edu/publication/18990/inflation_is_looming_on_americas_horizon.html

Krugman —Deflation!

“Deflation, not inflation, is the clear and presentdanger....why the inflation worries? Some claim that the

Federal Reserve is printing lots of money, which must beinflationary, while others claim that budget deficits willeventually force the U.S. government to inflate away itsdebt. The first story is just wrong. The second could beright, but isn’t....Banks aren’t lending out their extra reserves.

They’re just sitting on them – in effect, they’re sendingthe money right back to the Fed. So the Fed isn’t reallyprinting money after all

Krugman —Deflation and the usual insults

...Is there a risk that we’ll have inflation after theeconomy recovers? That’s the claim of those who look atprojections that federal debt may rise to more than 100percent of G.D.P. and say that America will eventuallyhave to inflate away that debt..Such things have happened in the past. For example,

France ultimately inflated away much of the debt itincurred while fighting World War I. But more modernexamples are lacking.If inflation isn’t a real risk, why all the claims that it

is?.. it’s hard to escape the sense that the currentinflation fear-mongering is partly political..

http://www.nytimes.com/2009/05/29/opinion/29krugman.html?_r=2

Bernanke/Fed —Credit channel; Phillips curve; “cost-push”

BB June 2009: Even after a recovery gets under way,the rate of growth of real economic activity is likely toremain below its longer-run potential for a while,implying that the current slack in resource utilization willincrease further. ...In this environment, we anticipatethat inflation will remain low.... cost pressures generallyremain subdued. As a consequence, inflation is likely tomove down some over the next year relative to its pace in2008. That said, improving economic conditions andstable inflation expectations should limit further declinesin inflation.FOMC March 16 2010: “With substantial resource

slack continuing to restrain cost pressures andlonger-term inflation expectations stable, inflation islikely to be subdued for some time.

Bernanke/Fed —Credit channel; Phillips curve; “cost-push”

FOMC August 10 2010: Measures of underlyinginflation have trended lower in recent quarters and, withsubstantial resource slack continuing to restrain costpressures and longer-term inflation expectations stable,inflation is likely to be subdued for some timeBB Aug 27: Recently, inflation has declined to a level

that is slightly below that which FOMC participants viewas most conducive to a healthy economy in the long run.With inflation expectations reasonably stable and theeconomy growing, inflation should remain near currentreadings for some time before rising slowly toward levelsmore consistent with the Committee’s objectives. At thisjuncture, the risk of either an undesirable rise in inflationor of significant further disinflation seems low.

I Internal: Big debate on how to stop deflation.

Low rates do not cause inflation

Oct65 Apr71 Oct76 Mar82 Sep87 Mar93 Sep98 Feb04 Aug090

2

4

6

8

10

12

14

163 month TBCore π

Phillips curves don’t work

4 5 6 7 8 9 10 110

1

2

3

4

5

6

84

8586

87

88

8990

91

92

93

949596

979899

4

5 6

7 8

910

Unemployment

Infla

tion

Inflation and unemployment, 19842009

Phillips curves don’t work —70s

3 4 5 6 7 8 9 10 110

2

4

6

8

10

12

14

66

6768

69

70 71

72

73

74

75

76

7778

79

8081

82

8384

Unemployment

Infla

tion

Inflation and unemployment, 19661984

I Inflation can break out despite “slack!”

2008-2010 —Money expands a lot!

Jan08 Apr08 Jul08 Oct08 Jan09 Apr09 Jul09 Oct09 Jan10 Apr10 Jul10

0

50

100

150

200

250

300

350

400

$ Bi

llion

Dollar increase in money from Jan 07

M1CurrencyDeposits

Jan08 Apr08 Jul08 Oct08 Jan09 Apr09 Jul09 Oct09 Jan10 Apr10 Jul10

0

10

20

30

40

50

60

Perc

ent

Percent increase in money from Jan 07

M1CurrencyDepositsGDP

Large increase

Balance sheet —Reserves expand more!

Jan08 Apr08 Jul08 Oct08 Jan09 Apr09 Jul09 Oct09 Jan10 Apr10 Jul100

0.5

1

1.5

2

Treasuries

Agencies

TALF, CP, Lending, etc. Mbs

Federal Reserve Assets

$,Tr

illion

s

Jan08 Apr08 Jul08 Oct08 Jan09 Apr09 Jul09 Oct09 Jan10 Apr10 Jul100

0.5

1

1.5

2

Currency

Treasury

Reserves

Other

Federal Reserve Liabilities

$,Tr

illion

s

But...Money has little actual correlation with inflation!

Jun90 Mar93 Dec95 Sep98 May01 Feb04 Nov06 Aug09 May128.6

8.7

8.8

8.9

9

9.1

9.2

9.3

9.4

9.5

9.6M1 and GDP

M1PY

And if it did, will smoking a cigar make you rich?

Money demand

0 1 2 3 4 5 6 79

10

11

12

13

14

15

16

17

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002200320042005

2006

20072008

2009

2010

3 month T bill rate

M1/

PY

, Per

cent

M1 Demand

At 0 rates, money demand is huge!

Does monetary expansion mean more inflation?

I Fed does not print money; “open market operations”; M&MsI Easy to reverse: As Md declines (panic, r), it’s easy for theFed to soak it up

I Conversely, at 0 rates Fed is powerless to stop deflation!I When interest rates are zero, buying and selling debt ofdifferent maturities has no effect.

Fiscal: inflation? M+B is rising a lot!

Money + Gov’t DebtPrice level

= Present value [Real primary surpluses ]

Jun07 Dec07 Jul08 Jan09 Aug09 Mar104000

5000

6000

7000

8000

9000

10000

$ B

illio

n

US debt

+ Pension, soc. sec., health,..??Including FedTreasury held by by public

Bottom lineI Why so much confusion/debate? Wildly different theories, fewof which work.

1. Fed view

Fed r→other r→"demand"→ "slack," "gaps"→→ inflation

2. New-Keynesian view3. Announcements “Coordinate expectations on unique localequilibrium”

4. Monetarist viewMV = PY

5. Fiscal theory

Money + Gov’t DebtPrice level

= Present value [Real primary surpluses ]

I To make a good forecast, understand mechanism!I You don’t know, but nobody else does either!