in the line of fire - agn international · < create a business case for social media in your...

TRANSCRIPT

September 2011 Issue 495-496 www.InternationalAccountingBulletin.com

In the line of fireLeaked: who are the winners and

losers of Barnier’s vision for audit?

● Deloitte Global reports record annual revenue● Exclusive research: how diversity varies in firms

● India survey: strong growth despite Satyam hangover● Japan survey: firms back on track

Gauging the effectiveness of social media in financial services

The use of social media has changed the way consumers interact with their service providers. A more personal and targeted approach is preferred to traditional advertising and direct marketing. In the financial services industry however, social media presents a minefield of risk factors and it is difficult to measure return on investment.Written specifically for the communications, sales, and customer services departments in financial organisations, this report provides expert advice on using social media to increase customer acquisition and loyalty and will enable you to reduce the risks associated with its use in financial services.

For full details visit www.vrl-financial-news.comPlease quote reference code: APC2/Ad

EMEA [email protected]

+44 (0) 20 7563 5605

Asia [email protected]

+ 65 6383 4688

< Estimate the ROI of your social media strategy< Understand which is the most appropriate social media platform

for your customers

< Create a business case for social media in your organisation< Use social media to increase customer acquisition and retention< Minimise the risks associated with social media

Read this report to:

New

indust

ry

report

September 2011 y 1

If there were ever any doubts about Michel Barnier’s conviction to revolutionise the

audit industry they have now been put to bed.

Leaked draft proposals on audit industry reform could threaten the Big Four business model while provide mid-tier firms with greater opportunities.

The proposals recommend mandatory audit firm rotation, the banning of non-audit services, joint audits, audit quality certifica-tion, expanded audit reports and EU over-sight reform.

Although more hard-hitting than first anticipated, it is important to remember that these are draft proposals and are still being worked on before they are made public in November.

After this stage, the regulation must then navigate a path through the EU’s council and parliament, where further horse trading is likely to take place before a watered down version becomes law. In other words, it’s still early days.

Some of the proposals will be welcomed by mid-tier firms, such as the abolition of restric-tive lending clauses and joint audits. But the major reforms strike at the heart of the four largest networks – Deloitte, PwC, Ernst & Young and KPMG.

Proposals on the provision of non-audit services could lead to Big Four firms being forced to shed audit clients or risk losing their consultancy businesses, which after years of building (and re-building in some cases) is a huge blow.

Mandatory rotation not the answerBarnier’s proposal on mandatory firm rota-tion is an attempt to improve auditor inde-pendence and scepticism. It’s due to a percep-tion that some audit firms are too cosy with management.

When you consider some firms have audit relationships with companies for more than 100 years, it is easy to see why capital market stakeholders could form that view.

However, mandatory audit firm rotation every nine years and mandatory re-tendering every five years, in addition to current rules on mandatory partner rotation, could prove a real headache for firms and companies.

This proposal sounds unlikely to navigate a path through EU council and parliament because it’s not practical.

Not only will it place a huge cost burden on companies, which in times of recession is par-

ticularly unpopu-lar, it will have an affect on the audit procedure and pro-ductive auditor/cli-ent relationships, which take many years to build in the largest compa-nies. Research on mandatory firm rotation shows it undermines audit quality.

There’s nothing wrong with exploring a mechanism to shorten audit engagements that span many decades but firm rotation must be considered in the context of current policies on partner rotation and retendering.

Too much change too soon in the name of independence will affect quality and compro-mise the role of the auditor.

Non-audit ban makes no senseBarnier is planning to abolish a broad range of non-audit services on tax, consulting, actu-ary, risk management, valuations and book-keeping for networks that generate a signifi-cant proportion of their European audit rev-enue from large public companies or ‘public interest entities’ (PIEs).

Let’s not kid ourselves, this is a direct attack on the Big Four and it is unwarranted.

To fall under the non-audit ban, firms must generate a third of their audit revenue from large public companies and belong to net-works that have revenue in excess of €1.5bn ($2bn).

The Big Four certainly fall into the latter but where it is hazy is how much audit rev-enue they receive from large PIEs – defined as the 10 largest public companies in country by market capitalisation and PIEs that have market capitalisation of more than €1bn.

Just this week, the world’s largest network Deloitte announced its global revenues soared by more than 8% to a record $28.8bn, with nearly 38% of revenue in consulting and financial advisory services (see p4).

If Barnier’s proposals are passed, it would threaten the growth of Deloitte and its rivals.

If Big Four firms were to be affected by this regulation they would mostly likely need to assess whether to drop audit clients in order to redress the amount of revenue they obtain from large public companies or split their operations altogether.

Importantly, having ‘audit only’ firms

www.InternationalAccountingBulletin.com

coMMeNt: ec draft proposalsInternational Accounting Bulletin

coNteNts02-03 NeWs

• DeloitteUSsuedforbillions • PKFDenmarkmergeswith

GrantThornton • NusbaumsaysC-suitepay

shouldmatchperformance

04 aNalYsIs

DeloitteglobalchiefexecutiveBarrySalzbergdiscussesperformanceandstrategyaftertheglobalnetworkreportedrevenueof$28.8bn

09-13 INdUstrY cHalleNGe: dIVersItY

Theaccountingprofessionisbreakingfreefromstereotypesthathavesurroundeditforyearsasfirmsstrivetodiversifytheirworkforce.ana GyorkosanalyseshowdiversityhasbeenaddressedacrosstheworlddrawingonexclusiveIAB research

14-18 coUNtrY sUrVeY: JapaN

AsJapanrebuildsfollowingtheMarchearthquake,accountingfirmsareunderimmensefeepressureandIFRSadoptionisinlimbo.david Hayesandana Gyorkosreport

19-24 coUNtrY sUrVeY: INdIa

Regulationsinaudit,accountingandtaxhaveledtoincreasedopportunitiesinIndiaasfirmsenjoybumpergrowthonthebackofastrongeconomy.Despitethis,thereisstillmuchsoulsearchinginthewakeoftheSatyamfraudandsignsofadividedprofession.swati prasadreports

editorial advisory Boardfrank arford,CroweHorwathInternationalCEOGeoff Barnes,BakerTillyInternationalpresidentandCEOJon lisby,KrestonInternationalexecutivedirectorJames Mendelssohn,MSIGlobalAllianceCEOchristian Mouillon,Ernst&Youngglobalvice-chair,assuranceJeremy Newman,BDOInternationalCEOed Nusbaum,GrantThorntonInternationalCEOliza robbins,MorisonInternationalCEOJean stephens,RSMInternationalCEOrobert tautges,HLBInternationalCEOpauline Wallace,PwCheadofpublicpolicyandregulatoryaffairs

Barnier’s vision good and bad

edItor’s letter

4p5

2 y September 2011 www.InternationalAccountingBulletin.com

NeWs: dIGest International Accounting Bulletin

leGal

KPMG to investigate $2bn UBS fraudKPMG has been appointed by the UK Financial Services Authority and Swiss Financial Market Supervisory Author-ity to investigate the events that lead to rogue trader Kweku Ado-boli losing $2bn in unauthorised trading at the Swiss investment bank UBS.

KPMG will investigate the details of the unauthorised trading and the control failures which permitted the activity to remain undetected. The investi-gation will also assess the overall strength of UBS’s controls to pre-vent unauthorised or fraudulent trading activity in its investment bank.

UBS’s board of directors have set up a separate internal investi-gation to be led by the former JP Morgan CFO David Sidwell.

strateGY

Former PKF Denmark firm joins GT

Grant Thornton International has added PKF Kresten Foged as the network’s new member firm in Denmark after PwC acquired its former member in May.

PKF Kresten Foged, which will change its name to Grant Thornton, has nine partners and 50 staff.

Grant Thornton International chief executive Ed Nusbaum said the network believes this addition is a “ground-breaking move” to create a strong pres-ence in Denmark.

The Grant Thornton leader previously expressed concerns about PwC’s acquisition reduc-ing competition in the market.

PKF Kresten Foged senior partner Jørgen Anker Nielsen said Grant Thornton has a very strong reputation in Denmark and is proud to have been select-ed to join the network.

“This puts us in a unique posi-tion to provide distinctive client service to clients as well as chal-lenging careers for ambitious professionals,” Nielsen said.

“We have already commit-

ted to building our presence in Copenhagen to 125 people with-in the next 12 months and will expand in other locations over the next three years.”

fINaNcIal resUlts

PwC UK increases revenue 6%

PwC UK has reported 6% growth in revenue to £2.46bn ($3.79bn) in the year to 30 June 2011. This follows solid 7% growth by Deloitte UK, indicat-ing some positive results for the Big Four.

Elsewhere in the market, fiscal 2011 results have been mixed with Grant Thornton and Baker Tilly reporting contractions while RSM Tenon and Smith & Williamson posted growth.

PwC UK’s fiscal year high-lights included recruiting 3,200 people, appointing 81 new part-ners, investing in a new London office and acquiring Diamond consulting.

PwC UK chairman and sen-ior partner Ian Powell said despite the challenging environ-ment “our assurance business performed well competitively winning the Aviva, TUI and IG Holdings audits and achiev-ing turnover growth of 6% to £909m”.

The firm reported growth of 8% to £907m in advisory serv-ices, including a 10% increase in consulting. Tax grew by 2% to £645m.

PwC’s average profit per partner increased marginally to £763,000 compared to £759,000 last year, and the bonus pool paid to staff increased by 10% to £89m.

fINaNcIal resUlts

RSM Tenon reports 31% growth

RSM Tenon’s revenue has increased by 31% to £249m ($394m) in the year to 30 June. The sharp increase is partly due to the firm’s 2009 acquisition of Bentley Jennison.

RSM Tenon’s underlying profit, before amortisation of acquired intangibles, deferred

consideration interest and excep-tional items, increased by 14% to £30m.

The firm’s operating profit rose 57% to £14m.

In the coming year, the firm plans to focus on driving organic development after a couple of years of significant acquisitions, including Bentley Jennison and parts of the former consolidator Vantis.

leGal

Deloitte US sued for billions

Deloitte US is being sued for $7.6bn by investors who have alleged the firm failed to detect fraud at defunct Florida mort-gage company, Taylor Bean & Whitaker (TB&W), one of the biggest private mortgage firms that collapsed during the US housing crash.

A trustee overseeing TB&W’s bankruptcy and one of the com-pany’s subsidiaries, Ocala Fund-ing, filed two separate lawsuits at the Miami-Dade Circuit Court this week.

Deloitte spokesman Jonathan Gandal told the media the com-pany rejects the claims and they are “utterly without merit”.

Gandal said the blame for the fraud and losses should rest squarely on TB&W, Ocala Fund-ing and Lee Farkas, the TB&W chairman who was sentenced to 30 years in prison for fraud.

leGal

Deloitte blocked from Longtop probe

Deloitte China claims Chinese authorities are preventing it from complying with a US Secu-rities and Exchange Commission (SEC) investigation into former client Longtop Financial Tech-nologies as the US regulator turns up the heat on the audit firm.

The SEC has asked a US federal court to force the Chinese affili-ate of Deloitte, D&T Shanghai, to disclose documents relating to Longtop after the firm failed to respond to a US District Court of Columbia subpoena that set an 8 July deadline.

“We have passed on the SEC’s requests to the regulators in China, as we are required to, but so far the China regulators have not given us permission to pro-vide papers to the SEC,” Deloitte said.

“We hope that a mechanism will be found shortly so that the matter can be resolved in compli-ance with the laws in both juris-dictions.”

Authorities of the two coun-tries have been at loggerheads over cross-border inspections because US regulators are not allowed to inspect China-based firms.

In a fresh court application to try and force Deloitte’s compli-ance, the SEC said: “Although D&T Shanghai is in possession of vast amounts of documents responsive to the subpoena, it has not produced any documents to the SEC to date. As a result, the commission is unable to gain access to information that is crit-ical to an investigation that has been authorised for the protec-tion of public investors.”

leGal

E&Y faces Anglo-Irish complaint

A formal complaint is expected to be filed to the Irish accounting watchdog against Ernst & Young Ireland (E&Y) over its role as auditor of Anglo Irish Bank.

The formal complaint follows an investigation by Chartered Accountants Regulatory Board (CARB) former auditor general John Purcell.

Purcell told the watchdog his investigation has found “prima facie cases against E&Y in respect of their role as auditors to Anglo Irish Bank”.

Purcell claimed E&Y failed to detect the scale of Sean Fitz-Patrick’s loans and their system-atic refinancing over year ends and a lack of appropriate dis-closure in the first set of Anglo’s financial statements in the year to 30 September 2008. E&Y said in statement it fundamentally disagrees there is a prima facie case to answer on three points under investigation. <

September 2011 y 3

NeWs: aNalYsIsInternational Accounting Bulletin

www.InternationalAccountingBulletin.com

Grant Thornton International chief executive Ed Nusbaum described generous C-suite pay rises at times when companies perform badly as “frankly insane” and poor corporate gov-ernance.

Nusbaum believes senior executive pay should be pegged against a company’s per-formance and to do otherwise “sends a ter-rible message to the marketplace”.

Nusbaum was commenting on remunera-tion packages in the broader context of cor-porate governance reform. Grant Thornton has tabled several recommendations to improve corporate governance as part of an EC consultation.

This includes shareholders being able to vote on executive and director compensa-tion, the annual public disclosure of senior executive compensation, a triennial external board evaluation for listed companies and ensuring that CEO/chairman responsibilities are not held by one person.

Grant Thornton believes any EU corporate governance code should be based on a ‘com-ply or explain’ framework due to the vary-ing stages of maturity between member state economies.

C-suite remuneration has been a contro-versial topic in recent years due to the soaring packages enjoyed by top earners while aver-age workers endure pay freezes and cuts.

Twenty years ago, FTSE 100 company chiefs earned 17 times the average employee’s pay packet but today it is more than 75 times. This month, it was revealed that pension pots of the leading corporate chiefs soared by 70 per cent in less than a decade and the average value of a FTSE 100 chief’s fund is £3.9m ($6m) – 130 times greater than the £30,000 fund of an average employee.

Nusbaum accepts the pay packets of C-level executives in relation to the average worker will always cause some “controver-sy” but where resentment boils over is when

remuneration packages are not linked to per-formance.

“This [issue] goes to the [heart] of the board of directors, corporate governance and independent thinking,” he said. “If you have a good chairman of the board, [he will] say, ‘what are you guys thinking? What’s going through your minds if we are asking our line workers to take cuts in pays while our com-pany is hurting and you want to give yourself a big raise?’ It’s frankly insane. It sends a ter-rible message to shareholders [and] it sends a terrible message to the workers.”

Nusbaum points out he does not have a problem with CEOs making “ridiculously high amounts of money” if their performance is helping the company to be successful.

The EC is expected to issue a feedback statement on responses to its corporate gov-ernance framework consultation within the next couple of months. <

Arvind Hickman

corporate GoVerNaNce

Nusbaum: remuneration must be linked to performance

4 y September 2011 www.InternationalAccountingBulletin.com

NeWs: aNalYsIs International Accounting Bulletin

Deloitte, the world’s largest accounting network, has increased global revenues by 8.4% to a record $28.8bn – laying down a marker to its Big Four rivals.

Growth of 7.7% in local currencies underlines a solid performance across most regions and is the network’s strongest growth since 2008.

Last year, Deloitte overtook PwC for the first time, bringing in $9m more in revenue. PwC would need to increase revenue by at least 9% to regain top position.

Deloitte’s success in recent years is due to building its consulting business, which dwarves that of its rivals. While PwC is a larger audit and tax network, Deloitte earns nearly 3.5bn more in consulting and advi-sory revenue alone.

Audit and tax have been less profitable businesses than consulting in recent years due to enormous pressure on fees. Audit also has a higher man-hours to billable fees ratio than many advisory services.

In addition, there is more headroom to grow consulting and advisory services than audit as the blue chip company audit mar-ket is saturated and clients often hold onto audit firms for several years.

The network’s global workforce reached 182,000, a net increase of 12,000, and is expected to grow more than 35% to 250,000 by FY2015.

Deloitte global chief executive Barry Salz-berg told International Accounting Bulletin Deloitte’s growth was mostly organic.

“Obviously we have made many acqui-sitions in the course of many years but it is now embedded in our system and in the past year it is almost all organic growth,” Salzberg said.

Salzberg said the economy has allowed the firm to drive advisory services, which contributed to growth of 15.1% in financial advisory and 14.8% in consulting.

“Going forward, with the concern over the economy,” Salzberg added. “We are guarded about our future growth but we believe we have a sufficient platform and are prepared to enjoy growth very similar to the growth we enjoyed this past year.

“In the area of services lines, our focus will be on data analytics. We are currently very significantly invested in advance capa-bilities and we are looking to invest more in that area organically and inorganically.”

Deloitte reported more moderate increas-es in audit (4.7%) and tax (5.2%).

Salzberg said the firm’s response to global fee pressure is to promote a more complete audit service.

“While we maybe seeing a slower growth in those businesses than our other busi-nesses, it’s clearly a growing and significant piece of our business, and we’ll continue to invest in it,” Salzberg added.

strong in asiaDeloitte’s Asia-Pacific region, which grew combined revenue by 15.8%, was the best-performing region for the seventh consecu-tive year with nearly all Deloitte member firms growing by double-digit figures.

Deloitte China grew 8.3% while mem-ber firms in Australia and India achieved growth in excess of 25%.

Salzberg said the growth could be attrib-uted in part to emerging markets and the growth potential of both China and India. The high growth in Australia was led by a 28% increase in consulting services.

“The Australian firm is one of the most innovative firms [in our network],” he said. “They have a very serious investment and commitment to an innovation platform and analytics capabilities, and both of those areas did superbly in that market. [When you] combine that with a robust consulting business, they did very well.”

Elsewhere, the Americas region grew 10.4%, led by firms in Brazil and Chile, which grew in excess of 20%.

Europe, Middle East and Africa revenues increased by 3.2%, with member firms in

the Middle East, Sweden, Turkey and Nor-way experiencing double-digit growth.

“European countries like Germany with opportunities to leverage the market in a place like Turkey,” Salzberg said.

Deloitte is halfway through a four-year $1bn investment programme. This includes investing $500m in FY2012 in priority mar-kets: Brazil, India, Russia, China, Japan, Middle East and South-East Asia.

The network will also pour $300m in Deloitte Audit, a new audit delivery tool, and build member firms’ analytics capabili-ties, which is expected to grow by more than 40% in FY2012.

Deloitte is building professional service capabilities for medium-sized companies, including private companies, mid-sized pri-vate equity firms, next-gen companies and mid-cap multinational companies.

The network will also invest millions in sustainability services.<

Ana Gyorkos and Arvind Hickman

fINaNcIal resUlts

Deloitte grows global revenue by 8% to $28.8bn

n BIG foUr

revenue timeline: 2006-2011

Source:International Accounting Bulletin

20062007

15

20

25

30

PwC

Deloitte

Ernst & Young

KPMG

20082009

20102011

bn

n deloItteregional breakdown

region revenue ($bn)

local growth

% of revenue

NorthAmerica 13.1 9.1 45.4

LatinAmerica 1.3 10.6 4.4

Asia-Pacific 4.2 8.5 14.6

Europe 9.5 5.2 32.8

MiddleEast 0.3 12.4 0.9

Africa 0.6 2.2 1.9

Source:Deloitte

Consulting29.7%Financialadvisory8.1%

Tax19.6%Audit&enterpriseriskservices42.6%

Source:Deloitte

n deloItte

service line fee split

September 2011 y 5www.InternationalAccountingBulletin.com

would affect the ability of firms to attract the diverse range of skills that make them important service providers to business.

Breaking up the Big Four would mean destroying the largest and most effective business graduate training grounds in the world.

One immediate question that springs to mind – what is the justification for all this?

There are already quite strong independ-ence requirements on non-audit services in many markets, such as the UK, so a lot of services that would impede audit independ-ence are already banned.

The basic litmus test of independence is that a firm should not be able to audit the financial statements of a client if its non-audit services influence reporting.

In layman’s terms, you shouldn’t audit your own work.

The case for audit firms providing certain non-audit services to clients is that auditors are best placed to provide them and to hire an external provider would be a waste of money and a repetition of work.

At a time when business leaders ponder a double dip recession, shouldn’t the EC look to remove unnecessary cost rather than increase it?

Joint audits should be consideredOn the positive side, there is merit in at least exploring joint audits on a broader scale than France.

Whether it works or not is open to debate, depending on who you talk to, but if it does help dynamise the market without affecting audit quality it is worth a shot.

Although the Big Four will contend there is plenty of competition between them, it wouldn’t hurt for other firms to gain experi-ence and market share auditing the largest companies provided it does not lead to inef-ficiencies and reduced quality.

Barnier must also be given credit for abol-ishing restrictive lending clauses and pro-moting an ‘EU audit passport’ that cuts red tape. Strengthening the tendering processes, ensuring greater transparency around audi-tor appointments and an enhanced dialogue between auditors and prudential supervisors are also sensible initiatives.

A major fallacy of the draft is its tone. Barnier implies ‘robust audit’ is the key to

re-establishing trust and market confidence after taxpayers have spent billions bailing out banks during the financial crisis.

Such a statement is worrying because it implies auditors are partly responsible for allowing the financial crisis to occur. Surely Barnier must know better.

If Barnier is fishing for reasons to change the audit industry, he ought to cast his rod in a different pond.

Auditors did not cause the financial cri-sis and any reform to the industry should be made for the right reasons and focus on audit quality.

It is the perception gap of what people believe auditors do compared to reality that has not adequately been addressed.

What must also come into question is the consultation process itself. Are these rec-ommendations really what capital markets stakeholders want? In some of the more con-troversial proposals, I suspect not.

The draft proposals still have a consider-able journey before they are enshrined in law but Barnier’s mission is clear for all to see – the status quo is no longer acceptable. <

Arvind [email protected]

p14

Mid-tier firms have largely welcomed EC draft proposals on audit while the Big Four warned some of the proposals could affect audit quality.

The draft proposals, widely leaked to the media this week, recommend mandatory audit firm rotation, the banning of non-audit services, joint audits, audit quality certifica-tion, expanded audit reports and EU oversight reform.

Some of the draft proposals have been wide-ly welcomed, such as the abolition on restric-tive lending clauses, an EU audit passport and improved transparency in the tendering proc-ess. Other proposals on mandatory re-tender-ing and the banning of non-audit services are far less popular, while there is a split between the Big Four and mid-tier on joint audits.

The proposal on non-audit services to audit clients could threaten the future of the Big Four as multi-service entities. It could force firms to drop audit clients or operate as audit-only firms.

PwC UK head of regulatory policy Pauline Wallace told the International Accounting Bulletin some of the more radical proposals could endanger audit quality.

“You have to ensure you have confidence in the market that a strong high-quality audit can provide. Most of the proposals in there at the moment will impair audit quality not improve it,” Wallace said, while stressing the proposals are only drafts and it is not time to panic.

Deloitte UK said any changes to the audit market must not be detrimental to audit qual-ity and should focus on economic growth.

“We believe the costs of any proposals for audited entities should not outweigh the ben-efits derived from improved audit quality and auditor choice,” Deloitte said.

While he welcomed the proposals, BDO International chief executive Jeremy Newman expressed some concern on his understanding of the details.

“I am concerned by the range and extent and inter-relationship of some of the propos-als,” Newman said.

“If I understand correctly what has been presented to me, the logistics of having a nine year mandatory rotation of firms, seven year rotation of partners, five year tendering and doing it with joint auditors could become very challenging.

“If you look at the combination of all those things it may be going too far. I think it could just be too much for corporates [to cope with].”

RSM International chief executive Jean Stephens said the process still has some way to go but broadly she is pleased with the overriding sentiment of the draft proposals.

“We are pleasantly surprised at the ambi-tions of the commission’s proposals that will go through discussion,” she said.

“What remains after the discussion process is going to be quite interesting. I think many ways the discussion has evolved and hope-fully some measures, such as the ban on Big Four only clauses are going to stick.”

Crowe Horwath International has also backed joint audits and periodic tendering but believes mandatory firm rotation will affect audit quality.

It is too early to speculate on who will be the winners and losers of Barnier’s vision, but a common view from the profession is that any changes must not compromise audit quality or further destabilise the econ-omy. <

Ana Gyorkos

INdUstrY reactIoN

Profession divided over Barnier’s EC draft

Barnier’s vision good and bad

NeWs: ec draft proposalsInternational Accounting Bulletin

International Accounting Bulletin

6 y September 2011 www.InternationalAccountingBulletin.com

Mandatory audit firm rotation

Barnier recommends large public-interest enti-ties cannot have the same auditor for more than nine years with a minimum engagement period of two years.

The draft regulation also requires audit partners carrying out a statutory audit to rotate every seven years. After a break of at least two years they can return to the engage-ment.

The gradual rotation required of auditors refers to individuals rather than entire teams.

Barnier bases these recommendations on the assumption that a ‘lack of change in audi-tors has created a perverse pressure on the incoming partner not to lose long standing audit clients’.

“The introduction of mandatory rota-tion of audit firms combined with tendering would deal with that problem,” the document states.

“Mandatory rotation of audit firms would also ensure that there would be new audit mandates available in the market for audits of public interest entities.”

To try and safeguard against concerns regu-lar rotation affects audit quality, auditors must hand over a file containing relevant informa-tion concerning the audited entity so the nature of the business and the internal organisational knowledge is not lost. This should help ensure continuity and comparability with the audits carried out in previous years.IAB verdict: Unlikely to make it into legisla-tion. This proposal will place a great burden on firms and companies.

It is not popular. Mandatory retendering after five years, partner rotation after seven years and firm rotation after nine years will become too onerous and costly for firms and companies of this size. It is also widely believed that mandatory rotation will have a negative affect on audit quality. This should be scraped.

Non-audit services

One of the most concerning recommendations for the Big Four, who have been building their non-audit capabilities for years, is the require-

ment to separate the audit from non-audit services to ensure greater auditor independ-ence.

The recommendation is subject to an audit firm generating more than a third of its annual audit revenues from large public interest enti-ties that belongs to a network whose Euro-pean members have combined annual audit revenues in excess of €1.5bn ($2bn) within the EU.

Large public interest entities are defined as the 10 largest public companies in country by market capitalisation and ‘public interest enti-ties’ (PIEs) that have market capitalisation of more than €1bn.

Barnier’s list of non audit services includes bookkeeping, valuation, tax consulting, actu-arial services, designing and implementing financial systems, internal control and risk management.

The list also includes internal audit for audit clients, litigation support, legal serv-ices, human resources, risk advice, manage-ment consultancy, dues diligence on potential M&As and other expert services with no rela-tion to audit.

The draft states non-audit services have effectively led to a situation where “an audi-tor cannot be demonstrably independent if professional scepticism is compromised by conflicting commercial interests”.

As most of the Big Four firms in the EU would be affected by this, it means they would either need to become audit-only firms or drop audit clients to fall outside the scope of an audit-only firm.IAB verdict: Terrible idea that is based on a perception that firms who provide non-audit services to audit clients have a conflict of inter-est that could affect the quality of their work.

There is no proof that such a conflict exists and current rules on non-audit services in countries like the UK provide sufficient safe-guards. These rules could effectively break up the Big Four and change the professional serv-ices firm model as we know it. It could also make recruitment more difficult as it would narrow the skill sets being sought in the pro-fession.

Businesses will also incur more costs by employing several suppliers to provide the services that could be done by one firm. This could be one of the first proposals to be nego-tiated out of the regulation.

Joint audits

To help increase the choice of audit firms Barnier has recommended large public inter-est entities should be required to appoint more than one audit firm to carry out its statutory audit.

Additionally, in this case at least one of the firms will have to be outside of the largest audit firms in a country and local regulators will be required to produce an annual public list of the largest audit firms.

A corporate could only appoint two of the largest firms when an audit would require in-depth and very specific knowledge of a field of activity and or geographical cover-age, which must be justified to the relevant regulator.IAB verdict: Joint audits should be considered provided they do not affect audit quality and help dynamise the market.

It is worth testing this idea in a broader region than France. It could potentially provide a greater number of firms with the opportunity to gain experience and market share serving large PIEs.

Questions still remain over whether this

What’s inside the Barnier draft?InaleakedECdraftregulationonaudit,ECInternalMarketsCommissionerMichelBarniermapsouthisvisionforthefutureoftheindustryandtheroleoftheauditor.International Accounting Bulletinhandsdownitsverdictonsomeofthekeydraftrecommendations

NeWs: ec draft proposals

September 2011 y 7www.InternationalAccountingBulletin.com

could lead to inefficiencies, but its worth exploring.

Strengthening audit committeesThe draft strengthens audit committees by requiring at least one of the committee members to have competence in auditing and at least two members have competence in accounting and/or auditing. The current Audit Directive only requires one committee member to have competence in auditing and accounting.IAB verdict: Any initiatives to strengthen the competence should be welcome.

EU audit passport

Such a passport would enable audit firms to carry out statutory audits in all EU member states, provided that the key audit partner leading the audit is approved as an auditor in the concerned member state.

In addition to the firm passport the com-mission draft sets forward a similar red-tape cutting measure for auditors. The ‘passport’ will enable statutory auditors to provide cross-border statutory audit services on a temporary or occasional basis.

An audit firm passport might also enable

the emergence of more pan-European audit firms.IAB verdict: Any measures that cut red tape and reduce the burden of multiple oversight systems within the single market is a wel-come move. Should make it easier for audit firms and auditors to operate on cross-border engagements.

Big Four only clauses

The draft directive clearly prohibits contrac-tual clauses or as more commonly known Big Four only clauses.

The draft states the existence of such claus-es has led to increased market concentration and is preventing some auditors from enter-ing the top segment of the market. IAB verdict: A sensible proposal and long overdue. This should reduce one competi-tion barrier.

Transparency reports

The draft legislations require all audit firms of large PIEs to make annual transparency reports public.

Transparency reports must include: a description of the legal structure and owner-ship of the audit firm; network affiliation of

the audit firm; description of the governance structure; description of the internal quality control system of the audit firm and a state-ment by the administrative or management body; indication of the last quality assurance review; partner remuneration information.

There is a separate proposal that requires firms to publish revenue information.IAB verdict: There’s conjecture over whether audit firms of PIEs should be as transparent as the companies they audit. This publication believes they should lead by example when it comes to transparency.

European Quality Certificate

The European Securities and Markets Authority is to develop draft regulatory tech-nical standards in order to obtain a European quality certificate for statutory auditors and audit firms carrying out statutory audits of public-interest entities. IAB verdict: Provided criteria to obtain the certificate is not too onerous, this could be viewed as a ‘kitemark’ of quality.

It could help change perceptions in the market about the audit quality of different firms, or become an unnecessary burden that companies will ignore. An idea worth consid-ering but implementation will be key. <

ec Internal Markets commissioner Michel Barnier is mapping out his vision for the future of the accounting industry

NeWs: ec draft proposalsInternational Accounting Bulletin

8 y September 2011 www.InternationalAccountingBulletin.com

International Accounting Bulletin

The European Commission’s draft regu-lations are now in the public domain and, in our view, the solutions pro-posed should apply to large public

companies. We believe the debate over expectations

and the structure of the market has not extended to the audit of other public com-panies, private companies and other sectors, and there is no case for change beyond the large public company sector.

The EC has encouraged discussion regard-ing the expectations of the audit of large pub-lic companies. The traditional format of the audit report was questioned. A more detailed ‘long form’ audit report is now proposed.

We agree with this proposal for large pub-lic companies as it is important stakeholders have more information about the conduct and outcome of the audit.

The EC has expressed concerns there is a concentration and competition issue in the market for large public company audit serv-ices in Europe. The public audit market is deemed not to be competitive and there are barriers to entry by new participants.

Ninety-nine of the FTSE 100 companies in the UK are audited by the Big Four audit firms and 27 of the DAX 30 in Germany are audited by two firms.

There is a view the UK Office of Fair Trad-ing (OFT) has reported that the average peri-od of appointment of an auditor of a FTSE 100 company is 43 years.

The EC has proposed joint audit for large public companies involving a Big Four firm and a non-Big Four firm. This will increase participation in the public company audit market by non-Big Four firms.

We believe that joint audit of large pub-lic companies can make a real change, as it will enable more audit firms to participate in the audit of larger public companies. This is clearly the case in France where joint audit is a legal requirement.

This reform will make the market more competitive and reduce the risk of the mar-ket being dependent on a small group of very large providers.

Joint audit has the potential to enhance audit quality as the two audit firms will co-

operate and work together to form an opin-ion. They will review each other’s work and test each other’s views and conclusions.

periodic tendering, mandatory rotationMany large European listed companies appear to have rarely, if ever, put their exter-nal audits out to open tender. A discussion prepared by the UK OFT supports this view in the context of the UK market.

The commission is proposing to make periodic tendering for public companies a requirement along with greater disclosure about the process. Open and transparent tendering, at periodic intervals, will enhance confidence in the process of appointing the auditor, particularly where the incumbent is reappointed.

This proposal could help to widen the market for audits. Greater competition has the potential to enhance audit qual-ity as quality should be one of the criteria assessed by audit committees when making an appointment.

The EC is proposing mandatory rotation with a maximum tenure by an auditor of nine years. Research has demonstrated that frequent rotation has undermined quality and we do not believe mandatory rotation will enhance audit quality.

Another proposal is a total prohibition of non-audit services. This has attracted head-lines because the EC is proposing the Big

Four firms split their audit and non-audit businesses.

We do not agree that there should be a total prohibition on the provision of non-audit services or a breakup of existing firms. There are perception issues but we do not believe the provision of non-audit services should be prohibited outright.

We propose auditors should not be permit-ted to provide non-audit services of an aggre-gated value which substantially exceeds the audit fee.

can the middle market networks deliver?If the proposals to change the market are to win stakeholder approval and maintain, if not enhance, audit quality, then the middle market networks of audit firms have to dem-onstrate they are willing and able to service larger listed companies.

The middle market networks have the required global reach needed to service this market. The networks have implemented pol-icies and procedures to ensure their members have the skills needed to service the clients of the network, whether present or future.

These include global quality control stand-ards, global audit processes and global train-ing programmes which apply global account-ing, auditing, and quality standards.

Many network member firms are already subject to the top level of regulatory compli-ance in their own countries, and provide the audit capabilities and quality comparable to their larger competitors.

Market change will need to take place over time as large public company audit arrange-ments cannot be changed immediately.

As the debate on the proposals begins, it is essential that, whatever the final form the regulations take, the solutions enhance stake-holder’s confidence in auditors and enhance the quality of audit work.

This outcome will make the discussion, debate and controversy over some of the proposals worthwhile. <

The views expressed are the personal per-spectives of the authors and do not reflect the official position of Crowe Horwath Interna-tional

The future of public company auditTheEC’sdraftregulationonaudithasanumberofrecommendationsthataredesignedtopromotegreatercompetitionintheauditmarket.CroweHorwathInternationalchiefexecutivefrank arford andinternationalA&Adirectordavid chitty sharetheirviewsontheproposals

Stakeholder confidence key: Crowe Hor-wath International’s Frank Arford (left) and international A&A director David Chitty

ec draft proposals: coMMeNt – fraNK arford & daVId cHIttY

September 2011 y 9

INdUstrY cHalleNGe: dIVersItYInternational Accounting Bulletin

www.InternationalAccountingBulletin.com

The days when the first women and people of varying races and back-grounds entered the profession are not as distant as one would imagine,

with most changes occurring place in the past two decades.

The profession globally has acknowl-edged that staff diversity is essential for future business success. However, firm lead-ers tell the International Accounting Bulletin there is still a way to go before diversity will be at a sufficient level and fully reflect the demographics.

A survey conducted by this publication to accompany the report saw 308 accounting firms respond from around the world. The findings paint an interesting picture as we see how different continents approach diversity and where their priorities lay.

In order to better understand how different regions and countries approach diversity we have interviewed firms leaders and profes-sional bodies across the world to cover some of the diversity basics: gender, race, mobility and educational background.

cracking the glass ceilingGlobally, there are more women entering the accounting profession each year and in some firms they outnumber male colleagues.

However, seeing women take on leader-ship positions in the profession is still rare and has been flagged as one of the important areas needing improvement.

At present, only one of the 10 largest glo-bal accounting networks has a female at the

helm – RSM International’s Jean Stephens.The Grant Thornton International Busi-

ness Report 2011 found women currently hold 20% of senior management positions globally in privately held business, down from 24% in 2009, and up just 1% from 2004. The mid-tier firm’s research attributed the decline to difficult economic conditions.

The International Accounting Bulletin’s diversity survey found only a third of firms across the world have a workforce with fewer than 45% women, with firms from the Middle East having the lowest proportion of women. Some 40% of the Middle Eastern firms surveyed had fewer than 10% female staff.

North American and European firms have the highest proportion of women. In North America, 84% of firms having at least 45% women, while in Europe it is 72% of firms.

In the Asia-Pacific region, 44% of firms have more than 45% women.

At Singaporean firm Foo Kon Tan Grant Thornton, 70% of staff are women, which is relatively high in Asia. HR managwer Dolly Ng Soon Cheng said the female-friendly hir-ing policy is due to programmes to encourage women to come back into profession after a career break.

“As the birth rate is low in Singapore, to encourage working women to return to the workforce after giving birth, employers pro-vide paid maternity leave of between 12 and 16 weeks,” Ng Soon Cheng says.

“Of this, four weeks of salary is reim-bursed by the government.”

BDO Brazil chairman and chief executive Raul Correa da Silva says his firm has been trying to keep the gender recruitment ratio for entry level at 50:50, however at manag-ment level the numbers of females signifi-cantly drops.

“In our profession, the number of women was small 15 years ago, but it has been grow-ing in the past few years,” Correa da Silva says.

“So, now I would say the percentage of women in our company – senior level profes-sionals – is of about 20%, but considering the current recruitment processes, it will start to increase fast.”

Da Silva says when he qualified there were only a handful of women in the profession; he married Brazil’s second female auditor.

KPMG UK head of recruitment Iain McLaughlin says the firm’s gender ratio is at about 50:50 “but there is considerable vari-ety by grade and function”.

“Of course we would like to see more women at senior levels,” McLaughlin says.

“There are things that we are doing, one of them is our Reach programme. This three-month programme allows women to articu-late their career goals, provides inspiration from various internal and external leaders, feedback on their leadership style, opportu-nity to build their networks, sponsorship and other support.

“We recognise we need to better represent-ative of females at a senior level.”

PwC US diversity leader Maria Castañón Moatscould points out that, while her

Getting the balance rightTheaccountingprofessionisbreakingfreefromtheshacklesofstereotypesthathavesurroundeditforyears,asfirmsgloballystrivetodiversifytheirworkforceandcreateanew,morecontemporaryimageofanaccountant.ana Gyorkosinvestigateshowdiversityhasbeenaddressedacrosstheworld

4p12

10 y September 2011 www.InternationalAccountingBulletin.com

INdUstrY cHalleNGe: dIVersItY International Accounting Bulletin

n dIVersItY

age chart – firms from different regions select the average age of staff. african firms have the youngest workforce, 76% have an average age of 25-35 years

Source:International Accounting Bulletin

Africa

Asia-Pacific

Europe0

10

20

30

40

50

60

70

80

blurb

North

America

Middle EastLatin

America

Age

25-35 years 36-45 years 46-55 years >55 years

n dIVersItY

Higher education – in most regions, business degrees are the most common form of tertiary education for accountants

Source:International Accounting Bulletin

Middle East

Asia-Pacific

Europe

North Americ

aAfri

ca

Latin Americ

a 0

20

40

60

80

100

Social studiesScienceOther

Mathematics

Business/Economics%

SouthandCentralAmerica11%

Europe46%

Asia-Pacific15%MiddleEast6%

Africa6%

Source:International Accounting Bulletin

n dIVersItY sUrVeY

regional breakdown of participating firms

“Ithinkinfiveyears’timewe’llseeamuchimprovedsituationintermsofchangingthedemographicsoftheprofessiontocloselyresemblethedemographicsofthecountry.Ithinkthere’sstillcommitment,andthecom-mitmentisreflectedbythefinancialresourcesthatareputaside”Victor sekese, ceo, sizweNtsaluba Gobodo

“Ithinkdiversity,whetherit’sbeenforcedupontheaccountancyprofessionI’mnottoosure,butit’scertainlyhighontheagendaofallaccountancyfirmsandorganisations”tony White, Hr & recruitment director, rsM tenon

IAB global diversity survey:

5%-20%,6%

20%-40%,11%

<40%,44%

>5%,6%

None33%

Source:International Accounting Bulletin

n dIVersItY

Middle east expats – firms in the Middle east report the largest number of expats

41-55%,35%55-65%,19%

<65%,24%

>20%,6%

21-40%,16%

Source:International Accounting Bulletin

n dIVersItY

europe gender balance – european firms have some of the most gender balanced workforces. 45% of firms surveyed reported female workforces greater than 55% of staff

September 2011 y 11

INdUstrY cHalleNGe: dIVersItYInternational Accounting Bulletin

www.InternationalAccountingBulletin.com

n dIVersItY

female friendly firms – Western economies have the most gender balanced workforce

Source:International Accounting Bulletin

North

America

Europe

Latin Americ

aAfric

a

Middle-East

Asia-Pacific0

20

40

60

80

100

%>10% 10-30% 31-45% >65%46-65%

n dIVersItY

expat barometer – firms highlight the percentage of expats within their workforce. latin america has the smallest proportion of foreign employees

Source:International Accounting Bulletin

Middle East

Asia-Pacific

Europe

North Americ

aAfri

ca

Latin Americ

a 0

20

40

60

80

100

20% - 40%>40%

1% - 20%None

%

n dIVersItY

Qualified breakdown – nearly a third of firms have a workforce with 60% or more qualified accountants

Source:International Accounting Bulletin

0

20

40

60

80

100

>20%

20%-50%

60%-75%>75%

50%-60%

Firms

n dIVersItY

Work experience – percentage of firms offering internships and graduate programmes

Source:International Accounting Bulletin

Internship

Graduate

programme 0

20

40

60

80

100

No

Yes%

n dIVersItY sUrVeY

Workforce size of participating firms

Source:International Accounting Bulletin

0

50

100

150

200

<50 employees

50-100 eemployees

200-500 employees

>500 employees

100-250 employees

Firms

“Ithinkdiversityisaveryhealthythingandit’scommercialbeneficial.Youknowwedon’tmakeanything,we’renotamanufacturingfirm,ourfirmisbuiltonitspeople,anddiversityinthinkingwillproduceadriveinnovationandgrowthwithourclients”Iain Mclaughlin, head of recruitment, KpMG UK

“Whatdiversitymeansforusinourcon-texthavingmovedawayfromanapartheidsystem,ourbigdriverischangethedemo-graphicofourmembershiptorepresentthedemographicofthecountry”Nazeer Wadee, chief operating officer, south african Institute of chartered accountants

Still room for improvement

12 y September 2011 www.InternationalAccountingBulletin.com

INdUstrY cHalleNGe: dIVersItY International Accounting Bulletin

firm may recruit 50% women, “as women advance in their careers, those numbers change”.

“Perhaps women begin to make choices around juggling career, family, etc. By the time you get to the manager level you are not at 50%,” Castañón Moatscould explains.

“So we really invest in supporting working parents and we have put in place things like Full Circle.

“This is [a programme] where we assign women to a PwC coach – someone they can still have a relationship with even when they are not with the firm because they are taking time off.

“It also gives them access to our firm’s training to keep their skills current.”

As women slowly make their mark, firm leaders accept there is still a way to go before women well and truly break the glass ceil-ing.

racial diversityRacial diversity is another area that has improved in recent years for several rea-sons.

Businesses want to better reflect the cross-section of people in the societies they operate, while globalisation and improved mobility of the profession has led to a rise in secondments.

In some countries, such as South Africa, racial diversity is an important issue due to relatively low proportion of black Afri-can accountants compared to the countries demography.

South African Institute of Chartered Accountants (SAICA) chief operating officer Nazeer Wadee recalls that, when he quali-fied in 1998-99, South Africa was moving out of the racist and suppressive apartheid regime that stifled opportunities for black accountants.

“For me personally, the difficulty back then was finding employment,” Wadee says.

“Unless you were white, finding employ-ment was really difficult, especially at the Big Five.

“What you then struggled with was getting somebody to believe that somebody who was

not white could do the job. It just meant you probably had to work 40% to 50% harder than anyone else.”

Racial diversity has changed significantly in recent years and this is partly due to the Black Economic Empowerment Act, which imposes a quota of black employees per com-pany.

So much so, Wadee says, that it has become difficult to satisfy the demand for qualified black accountants, particularly female black accountants.

Morison International member SizweNt-saluba Gobodo is the largest firm outside of the Big Four.

A forerunner firm, SizweNtsaluba was one of the first ‘black firms’ – a firm largely com-posed of black Africans. Chief executive Vic-tor Sekese says when he did his professional training in the late 1980s and the early 1990s you could literally count the number of black chartered accountants.

“You sort of knew everybody because there were so few of us,” Sekese points out.

Prior to the merger of SizweNtsaluba and Gobodo earlier this year, the firms were known as black firms.

“Because of us having a majority of black staff you might say we are a black firm but that doesn’t mean we only employ black peo-ple,” Sekese says.

“At partner level we have representatives of the racial group: African black, coloured, Indians and whites, both male and female.”

Sekese says SizweNtsaluba Gobodo closely reflects the demographic of the country.

Across the Atlantic, Castañón Moatscould explains that PwC takes high-performing employees from minority backgrounds and matches them with an advocate at senior partner level to encourage them to progress within the firm.

“We have affinity groups – we refer to them as ‘circles’ – not only for women, but also minorities such as Asian Americans, African Americans as well as Hispanics,” she says.

“We also reach out to minority high school students and parents on navigating the col-lege choice decision.”

Despite efforts such as these, Castawñón Moatscould adds: “My personal feeling is that our African-American and Latino students are still under-represented in the accounting programmes nationwide.”

professional mobilityAnother way firms are becoming more diverse is through secondments and other programmes that allow accountants to work abroad.

International Accounting Bulletin research revealed that Latin America employs the lowest number of people from abroad, with 74% of responding firms saying they have no expats.

Middle East is the region with the highest number of expats, with 44% of firms saying they have more than 40% foreign workforce. More then half of respondents from North America and Europe also said they have no expats working for their firm.

In Asia-Pacific. 50% of responding firms have between a 1% and 40% foreign work-force.

HLB International US member firm Anch-in, Block & Anchin is increasingly recruiting and sponsoring accountants from the Philip-pines, South Africa and Asian countries such as China and Korea.

“We have always been open to hiring what we think are the best and the brightest,” human resources director David Finkelstein says.

“At the time when it was hard to get the quality we wanted from the US workforce, we heard that people coming over from Phil-ippines, for example, were very talented and we decided to look at recruiting from over-seas.”

Another firm with an internationally diverse work force of more than 18 nation-alities is Foo Kon Tan Grant Thornton.

“As there is a shortage of local talent in the industry, foreign talent helps to complement the workforce,” Ng Soon Cheng says.

“On top of this, the special richness that foreign talent brings and blends provide us with a different perspective at work.”

p94

n dIVersItYeducation – in most regions, firms have two thirds of the work force with a university degree

africa asia-pacific Middle east europe North america

latin america

Lessthan20% 11 2 0 7 0 3

20%-50% 17 10 0 28 4 17

50%-60% 11 2 5 12 11 23

60%-75% 17 23 11 13 13 17

Morethan75% 44 63 84 40 72 40

Source:International Accounting Bulletin

“Unless you were white, finding employment was really difficult, especially at the Big five... It just meant you probably had to work 40% to 50% harder than anyone else” NazeerWadee,SAICA

September 2011 y 13

INdUstrY cHalleNGe: dIVersItYInternational Accounting Bulletin

www.InternationalAccountingBulletin.com

Most foreign employees at the firm are from other Asian countries as well as the US and UK.

Professional accountancy body CPA Aus-tralia says that, in Australia, accounting is on the government’s skills shortage list, which provides an easy passage for migrant accountant workers to enter the country.

“The main countries of origin are China and India,” CPA Australia executive general manager for member engagement Jeff Hugh-es explains.

The UK has always been known for recruiting from abroad, however, recent gov-ernment restrictions to lower immigration levels is likely to stem the flow of migrant workers entering the country and have an impact upon diversity.

“As a company, we have visa programmes and we have our allocation on the number of people we can bring in but there are so many hurdles now,” RSM Tenon HR & recruit-ment director Tony White.

“It is very difficult to do that now.”To get around the restrictions, RSM Tenon

has started to do intercompany transfers within the RSM International network.

“We have intercompany transfers where our people will go over to South Africa, America, Australia and will do anything from three months to two years,” White says.

“Then, on the flip side, we will get people coming to the UK to do that. So it is almost like a work exchange programme that is quite sophisticated.”

McLaughlin, from KPMG UK, says the firm is working with the UK government to better understand the regulation. As yet, it has not yet affected the firm’s recruitment strategy.

the next generationTraditionally, firms have sought accounting talent from business degree backgrounds but this is not necessarily the case in every country.

In regions where the talent pool is small or there is fierce competition from other sectors, firms have broadened the educa-tion criteria of candidates. Larger firms that provide a myriad of consulting services are also seeking professionals with backgrounds in IT, climate change, engineering and other industry sectors.

The most common degree of accounting recruits, according to International Account-ing Bulletin survey respondents is a business and economics degree. In North America, 91% of recruits without an accountancy degree have a business or economics degree.

Some 27% of respondents from Africa also said they look at social studies degrees, While only 3% of respondents from North

America said they would hire people with those qualifications.

Most firm leaders explain that, while there is a growing interest in other educational backgrounds, most recruitment activity is focused on business graduates.

Finkelstein says, for Anchin, Block & Anchin, most graduates have a master’s degree and majored in accounting.

“The pool is large enough that you don’t need to go outside accounting,” he says.

Sekese says, in the SizweNtsaluba Gobodo audit practice, most recruits have an account-ing degree due to the way the profession has been structured historically.

“However, lately we are now employing non-accounting graduates to work in other divisions that we have,” he adds.

“For example, the next group of graduates we have are graduates in the IT space so we have got a number of people that are quali-fied from an IT point of view.

“But, to a very large extent, it is still accounting degrees. We find ourselves with teams of various skills, legal skills, investiga-tive skills and accounting skills.

“With the new green economy, we are looking for people who have an understand-ing of environmental law and environmental issues.”

UK firms, however, are more open to peo-ple with non-traditional higher education qualifications. White says academic perform-ance is as important as academic pursuit.

“Our policy would be to take people from a wide range of courses from politics, histo-ry, sociology, geography, maths, whatever,” White says.

“It doesn’t matter. What matters is seeing on the graduate assessment days why people want to be an accountant. What is their hun-ger, rather than have they have got a distinc-tion in accountancy at XYz university.”

ICAEW head of member services Sharon Gunn says the institute is also looking to take in more students from non-accounting backgrounds.

“That is actually very typical of the make-up of our profession right now – we don’t just take relevant accounting graduates, but

a really diverse mix,” she explains.The survey accompanying this report

found the majority of responding firms from around the world had more than 75% of workforces university educated.

The Middle East has the highest number of university educated professionals, with more than 84% of responding firms having more 75% of the workforce with a university edu-cation. In Europe, 40% or responding firms have more then 75% university educated staff.

room for improvementAlthough firm leaders have seen enormous changes in diversity there is still a way to go.

KPMG’s McLaughlin says the profes-sion “probably isn’t quite diverse enough, there probably is a lot of room for improve-ment”.

“I think the profession overall, and frank-ly the service we provide the clients, would definitely benefit from increased diversity,” he adds.

“It is an industry challenge we recognise now. Our peer group recognise that now.”

Sekese says: “I think in five years’ time we’ll see a much improved situation in terms of changing the demographics of the profes-sion to closely resemble the demographics of the country. I think there is still commitment and the commitment is reflected by the finan-cial resources that are put aside.”

Firm and professional body heads agree diversity is an area that needs to be closely monitored and resources invested in order to improve the demographics of the profes-sion.

Perhaps in certain areas additional regula-tion is required to bring along the next level of changes. For example, mandatory female quotas at management level might bring the additional push women need to break the glass ceiling in financial services.

Regardless of regulatory intervention the profession globally is aware of the impor-tance of diversity; however there is still a way to go before firms are able to put this challenge behind them. <

n dIVersItYQualified accountants – in most regions, firms have between 20% - 50% qualified workforce

africa asia-pacific Middle east europe North america

latin america

Lessthan20% 39 27 0 18 0 11

20%-50% 39 19 37 40 25 23

50%-60% 10 19 16 20 25 31

60%-75% 6 19 21 11 30 9

Morethan75% 6 16 26 11 20 26

Source:International Accounting Bulletin

14 y September 2011

Japan’s accounting profession has had to deal with exceptional operational circumstances this year following a 9.0 magnitude earthquake that sent a

Tsunami hurtling towards North-East Japan on 11 March.

Earthquake damage occurred in an area stretching about 350km north to south from Sendai to Tokyo along the East Japan coast-line and up 100km inland in some areas just north of Tokyo. It is one of the worst natural disasters in modern Japanese history.

According to the Japanese National Police Agency, 15,782 people died and 4,086 peo-ple are missing, while 270,000 buildings were either damaged or destroyed. And, while a nuclear power plant catastrophe stole much of the headlines, it is the destruc-tion of lives and businesses that will have a lasting legacy.

Today, six months after the earthquake struck, damage to factories and other indus-trial facilities still affect the supply of auto-motive parts, electronic components and cigarettes, as well as fishery and agricul-tural products. This all has a run-on effect for Japan’s accounting firms, says RSM Sawamura & Co managing partner Aki Murayama.

“We are strongly related with each other and the disaster has hit our life and economy significantly,” Murayama says.

“Although it does not directly affect our business, we realise some industries have been suffering from nuclear crisis, lack of materials and facilities, electrical shortages, bad communication as well as slow politi-cal decision and emergent appreciation in Japanese currency. It affects our business in the end.”

Grant Thornton Japan senior partner Satoru Endo says the firm hasn’t felt any direct effect from the disaster.

“However, indirectly we think we have felt the effect. It has caused even more fee pressure and affected our IPO related work. There has been a lot of postponing of IPOs,” Endo says.

In spite of the devastation caused to the Tohoku region, the rest of Japan was large-ly unaffected and industrial recovery since March has been faster than many people originally expected.

“After the earthquake people said there would be serious damage affecting industry until November or December but against this forecast we have seen a quick recovery. However, there is still a problem due to the serious appreciation of the yen,” KPMG Japan executive board member and Tokyo office managing partner Tsutomu Takahashi says.

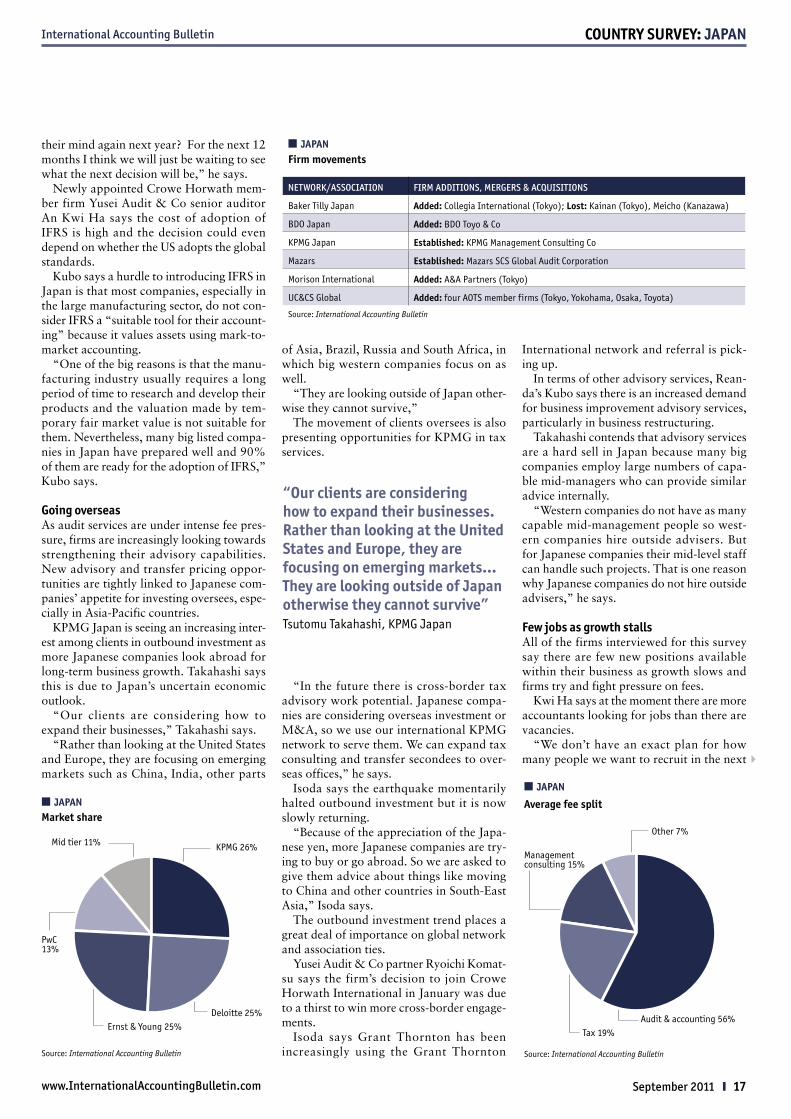

KpMG on topThe Japanese accounting market has grown 2% as most firms have not yet felt the full business effects of the earthquake and tsu-nami on their balance sheet. Although this is an improvement on fiscal 2009/2010 – it is a far cry from the hefty growth experienced prior to the global financial crisis.

The market leader KPMG has grown rev-enue 2% to ¥109bn in the year to 30 June 2011.

KPMG is closely followed by Deloitte Japan, which reported similar revenue growth to ¥108bn in the year to 31 May 2011.

The fourth largest firm, PwC Japan, reported a 1% decline, following last year’s

staggering growth of 20%. PwC Japan is rel-atively small compared to its rivals, report-ing ¥58.3bn in the year to 30 June 2011. This is due to the demise of its previous Japanese member, Misuzu Audit Corpora-tion, which dissolved in 2007 after account-ing scandals.

The firm with the highest growth is BDO Japan, which grew by 135% due to the addi-tion of BDO Toyo & Co, a former Crowe Horwath Japan member. The new addition makes BDO the largest mid-tier firm with annual revenues of ¥6.69bn.

The loss of Toyo & Co led to Crowe Hor-wath Japan reporting a 55% decrease in rev-enue to ¥1.89bn.

As audit is the predominant service line for firms, bringing in 56% of annual income, firms are feeling the pinch of fee pressure and looking to grow via M&As and advi-sory services. A delay on the adoption of IFRS will also have an impact on consulting services.

audit under pressureAside from the natural disaster, fee pressure has been a challenge for Japan’s accounting firms.

“At the moment our clients are very price

www.InternationalAccountingBulletin.com

coUNtrY sUrVeY: JapaN International Accounting Bulletin

Earthquake, IFRS shockwaves strikeAsJapanrebuildsfollowingtheMarchearthquake,accountingfirmsareunderimmensefeepressureandIFRSadoptionisinlimbo.david Hayesandana Gyorkosfindfirmleadersinpursuitofopportunitiesabroadwhiledomesticmarketstakeatumble

n JapaN

Accountancy market at a glance revenue largest by revenue:KPMG,¥109bn smallest by revenue:Mazars,¥88mHighest growth rate:BDOJapan,132%lowest growth rate: CroweHorwathJapan,-55%

stafflargest workforce:DeloitteJapan,7,851smallest workforce: Mazars,18Most professionals: DeloitteJapan,6,318Most partners:KPMG,735Most admin staff:DeloitteJapan,842Most offices:DeloitteJapan,38Source:International Accounting Bulletin

0

100

200

300

400

500

20072008

20102011

2009

¥bn

0

5

10

15

20

25%

Total revenue

Market growth

n JapaNtotal revenue vs market growth (2007-2011)

Source:International Accounting Bulletin

September 2011 y 15

coUNtrY sUrVeY: JapaNInternational Accounting Bulletin

conscious and we have very big pressures from our audit clients. Another thing is that we have increased competition from other firms – from Big Four firms to other mid-tier players. It’s hard to compete for new clients,” Grant Thornton Japan partner and audit leader Taro Isoda explains.

Takahashi says that KPMG has seen tight fee competition from medium and small accounting firms.

“Audit fees are about the same as last year. Competitors approach our clients and offer

a lower fee, and then clients approach us to offer them a more attractive fee,” Takahashi says.

Takahashi says a dearth of IPOs and the merging of listed companies is contracting the market for audit.

“The trend for listed companies in Japan to merge as a way to increase their opera-tional efficiency is one that concerns many accounting firms,” he says.

“Each merger results in the loss of an audit client for one accounting firm. The

current shortage of IPOs means the number of listed companies in Japan has started to decrease.”

Isoda says Grant Thornton has tried to manage fee pressure by cutting the over-heads and fixed cost.

Tax services have also been exposed to fee pressure. Mid-tier leaders observe fee cut-ting on services such as transfer pricing.

“Tax has potential, but we have seen severe competition from the Big Four in terms of transfer pricing. The Big Four are

www.InternationalAccountingBulletin.com

n JapaNleading accounting firms, networks and associations: fee data

rank Namefee

income (¥m)

Growth rate (%)

fee split (%)

Year-endaudit &

accounting tax services Management consulting

corporate finance

corporate recovery/ insolvency

litigation support other

FIRM/INTERNATIONAL AFFILIATE

1 KPMG*†(1) 108,638.0 2 81 10 – – – – 9 Jun11

2 DeloitteJapan*†(2) 108,234.0 2 73 8 15 4 – – – May11

3 Ernst&Young*†(e) 107,729.3 2 – – – – – – – Jun11

4 PwCJapan*†(3) 58,300.0 -1 50 17 – – – – 33 Jun10

5 BDOJapan*†(4) 6,696.2 132 91 5 3 – 1 – – Jun11

6 GrantThorntonJapan*† 6,145.0 -5 79 13 4 2 0 0 0 Sep10

7 MiraiGroup/ReandaInternational*†

1,598.0 -1 22 18 36 – 22 – 2 Jun11

8 Seishin&Co/MooreStephensInternational*

511.6 2 65 26 – – – – 9 Dec10

9 Nakamoto&Company/PKFInternational*†

325.1 26 36 5 59 – – – – Dec10

10 Mazars†(5) 88.0 -23 85 11 1 1 – – 2 Aug11

total revenue/growth 398,265.2 2

NETWORK/ASSOCIATION OF INDEPENDENT FIRMS

1 RSMJapan*† 3,659.0 37 27 19 54 – – – – Jun10

2 BakerTillyJapan*† 2,442.7 -4 68 22 4 1 1 – – May11

3 CroweHorwathJapan*†(6) 1,890.5 -55 65 6 29 – – – – Mar11

4 NexiaInternational*† 1,629.0 8 78 – 20 0 0 0 2 Jun10

5 HLBJapan*† 1,490.1 -5 39 37 – 6 12 – 6 Dec11

6 ECOVISJapan* 1,442.3 58 62 38 – – – – – Aug11

7 IntegraInternational* 1,400.0 0 15 75 10 – – – – Dec10

8 UC&CSGlobal* 1,221.4 – 20 – 80 – – – – Dec10

9 INPACTAsiaPacific* 899.2 1 29 66 5 – – – – Dec11

10 MorisonInternational* 769.4 – 88 – 11 – – – 1 Jul11

11 Praxity(7) 688.0 -6 64 23 1 1 0 0 11 n/a

12 DFKInternational* 516.8 14 37 31 26 6 – – – Sep10

13 MGI* 503.3 13 – – – – – – – Jun11

14 IGAFPolaris* 498.8 – 83 – 11 6 May11

15 KrestonInternational*†(8) 469.0 2 31 50 12 – – – 7 Oct10

total revenue/growth 15,860.5 2

Notes:*Disclaimer=Onlydatafromthenamedmemberfirmortheexclusivememberfirmswithinanetwork/associationisincluded.Datarelatingtocorrespondentandnon-exclusivememberfirmsisnotincluded.†TheseorganisationscomeundertheIFACdefinitionofanetworkornetworkfirm;(e)IABestimate(1)Taxservicelinefiscalyearends31December2010.Otherincludesadvisory;(2)Theyear-endisforglobalreportinguseonly;(3)Otherincludesincomefrom:managementconsulting,corporatefinanceandcorporateRecovery/Insolvency;(4)In2010theyear-endwasMarch;(5)Feeincomedoesnotincludeincomefromcorrespondentfirmsandnon-exclusivemembers.Ifitwereto,totalfeeincomewouldbe¥178m;(6)In2009theyear-endwasDecember;(7)Praxityyear-endisthelatestpossibleyear-endofitsmemberfirms.Feeincomedoesnotincludeincomefromcorrespondentfirmsandnon-exclusivemembers.Ifitwereto,totalfeeincomewouldbe¥848m;(8)Feeincomedoesnotincludeincomefromcorrespondentfirmsandnon-exclusivemembers.Ifitwereincludingitthetotalfeeincomewouldbe¥5.2bn.Source:International Accounting Bulletin

4

International Accounting Bulletin

16 y September 2011

coUNtrY sUrVeY: JapaN

offering big discounts for those engagements and it’s hard for us to offer the same when tendering for new clients. Existing clients were not affected by this,” Isoda says.

Reanda Japan managing director Mitsuo Kubo says his firm is focused on providing tax as a stable source of income.

“We are thinking of expanding our tax service in the coming future by adding transfer pricing planning and international tax service into our tax service line,” Kubo explains.

Ifrs U-turnThree months after the earthquake, account-ing firms received another shockwave when the government announced plans to delay the introduction of IFRS.

Japanese Minister for Financial Services Shozaburo Jimi said, on 21 June, the manda-tory introduction of IFRS will be reconsid-ered due to concerns over the additional cost for already struggling Japanese companies.

At the time, the FSA said if Japan decides to make IFRS mandatory there will be a non-mandatory lead-in period of five to seven years to allow companies time to pre-pare for the new standards. This means the earliest date IFRS could become mandatory is from 2017.

There are about 3,700 listed companies in Japan and 40% are small- to medium-sized entities that are not expected to implement IFRS until it becomes mandatory. These are largely served by small- and medium-sized accounting firms.

Japan Institute of Certified Public Accountants says 60% of listed companies are Big Four clients and most are expected to use IFRS on a voluntary basis, adhering to the previous IFRS adoption schedule. Taka-hashi points out that most large listed Japa-nese companies his firm serves will go on to implement IFRS as originally scheduled.

Small- and medium-sized listed companies may delay their previous plans to implement IFRS until the government makes further announcements.

Endo says the IFRS delay has created an impact on Grant Thornton’s fees because of the loss of IFRS consulting projects.

“Our clients don’t really know what the government will do next; have they stopped the adoption indefinitely or will they change

www.InternationalAccountingBulletin.com

n JapaNleading accounting firms, networks and associations: staff data

rank Nametotal staff partners professional staff administrative staff offices

2011 2010 2011 2010 2011 2010 2011 2010 2011 2010

FIRM/INTERNATIONAL AFFILIATE

1 DeloitteJapan*† 7,851 7,753 691 679 6,318 6,289 842 785 38 38

2 Ernst&Young*†(e) 7,391 7,247 – – – – – – – 35

3 KPMG*† 6,772 6,593 735 714 5,314 5,182 723 697 34 32

4 PwCJapan*† 3,959 2,083 215 82 3,218 1,726 526 275 8 4