impact of research & innovation on profitable growth in ... · mckinsey & company | 13 in...

TRANSCRIPT

Impact of Research & Innovation on Profitable Growth in ChemicalsGPCA Research & Innovation Summit

Dubai, March 12, 2014

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

McKinsey & Company | 1

PPSPOMPARPTFEEPMEDPMiso.PPHOPEABSPANEpoxyPBTSilicone

LLDPEPEEKPESPIPEI LCP

UFPF

PEDPURPIBPETPASBBLDPEPMMABRPSPVC

Skeptics say the "good old times for innovation are over"

1900 1920 1940 1960 1980 2000

"There is an overwhelming consensus among analysts that chemical companies should not spend more on R&D"

European Chemical News

"Innovation will not be a primary growth and value driver in chemicals"

UBS Equity Research

"Lack of innovation has been one of the industry's greatest problems over the past decade"

Goldman Sachs

"Rapid product innovation may not confer a competitive advantage"

ING

SOURCE: McKinsey

Decline of monomer innovation

McKinsey & Company | 2

Enthusiasts see a different picture

New products/ technologies

Industrial enzymes

Liquid crystals

Agchem/GMO seeds

Cultures

Alternative feedstock Methanol to olefins

Coal to olefins

Biomass to chemicals, e.g., bioethanol to ethylene

Resource-efficient processes

New catalystsNew processes, e.g., HPPO, fermentation, electrolysis

Better and better solutions

Oilfield chemicalsFilms and coatingsfor electronics, etc.

... and many more

McKinsey & Company | 3

Beyond stories and opinions …

Top-down perspective Archetypes of successful companies in chemicals –Does Research & Innovation play a role?

Bottom-up perspective Value creation through innovation –What does McKinsey’s InnomaticsTM database say?

McKinsey & Company | 4

Beyond stories and opinions …

Top-down perspective Archetypes of successful companies in chemicals –Does Research & Innovation play a role?

Bottom-up perspective Value creation through innovation –What does McKinsey’s InnomaticsTM database say?

McKinsey & Company | 5SOURCE: Datastream, McKinsey

Chemicals has been capturing a disproportionate share of the valueTRS, indexed – 100 = December 31, 2000, USD

0

50

100

150

200

250

300

350

400

450

Global Market

Oil & Gas

ChemicalsConsumer GoodsConstruction

Automobile

Electronics

201312111009080706050403022001

Outlook on profitable growth?

McKinsey & Company | 6

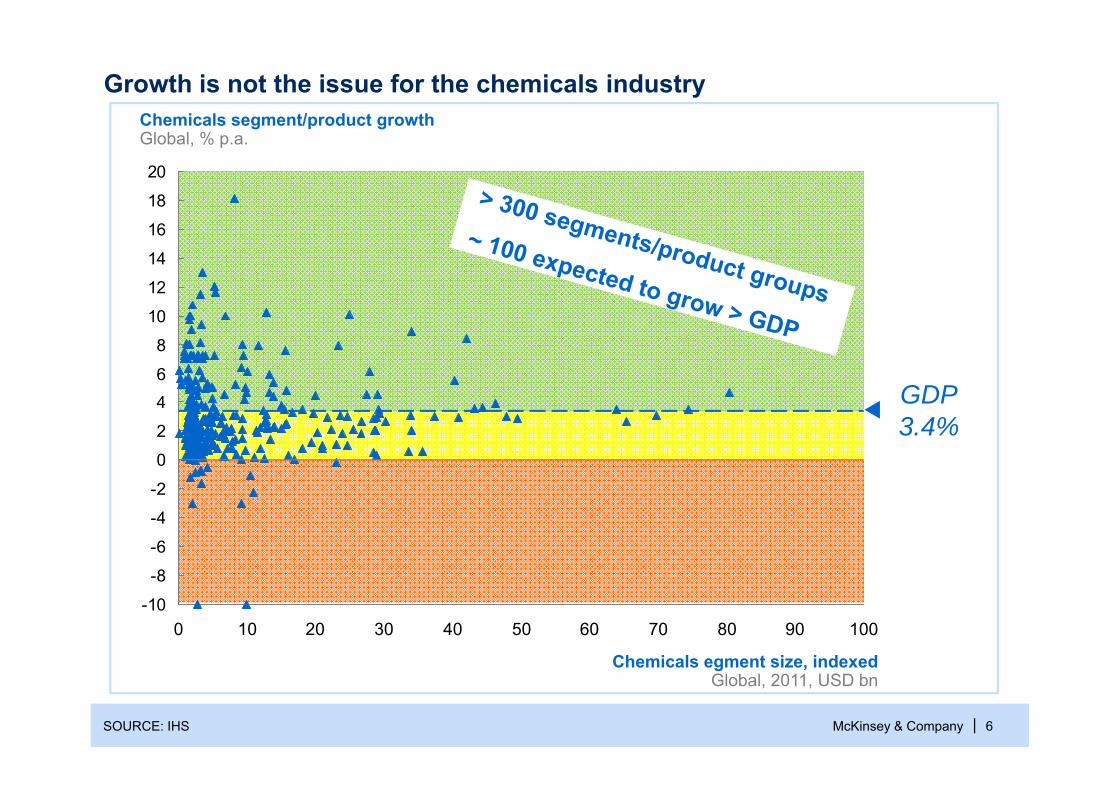

-10

-8-6

-4-2

0246

810

1214

1618

20

1009080706050403020100

Chemicals egment size, indexedGlobal, 2011, USD bn

Chemicals segment/product growthGlobal, % p.a.

Growth is not the issue for the chemicals industry

SOURCE: IHS

GDP3.4%

McKinsey & Company | 7

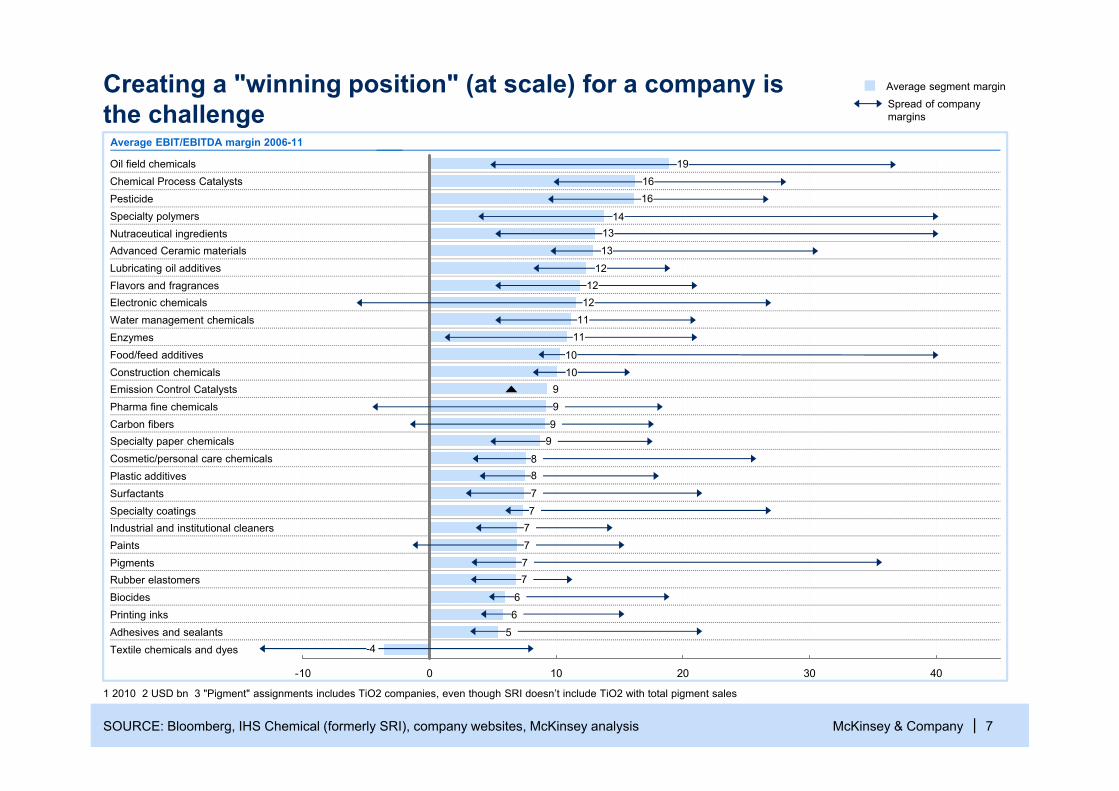

-10 0 10 20 30 40

PigmentsRubber elastomersBiocidesPrinting inksAdhesives and sealantsTextile chemicals and dyes

PaintsIndustrial and institutional cleanersSpecialty coatingsSurfactantsPlastic additivesCosmetic/personal care chemicalsSpecialty paper chemicalsCarbon fibersPharma fine chemicalsEmission Control CatalystsConstruction chemicalsFood/feed additivesEnzymesWater management chemicalsElectronic chemicalsFlavors and fragrancesLubricating oil additivesAdvanced Ceramic materialsNutraceutical ingredientsSpecialty polymersPesticideChemical Process CatalystsOil field chemicals

Creating a "winning position" (at scale) for a company is the challenge

1 2010 2 USD bn 3 "Pigment" assignments includes TiO2 companies, even though SRI doesn’t include TiO2 with total pigment sales

Average EBIT/EBITDA margin 2006-11

SOURCE: Bloomberg, IHS Chemical (formerly SRI), company websites, McKinsey analysis

Average segment marginSpread of company margins

191616

141313

1212

1211

11

1010

999

98877

7777

66

5-4

McKinsey & Company | 8

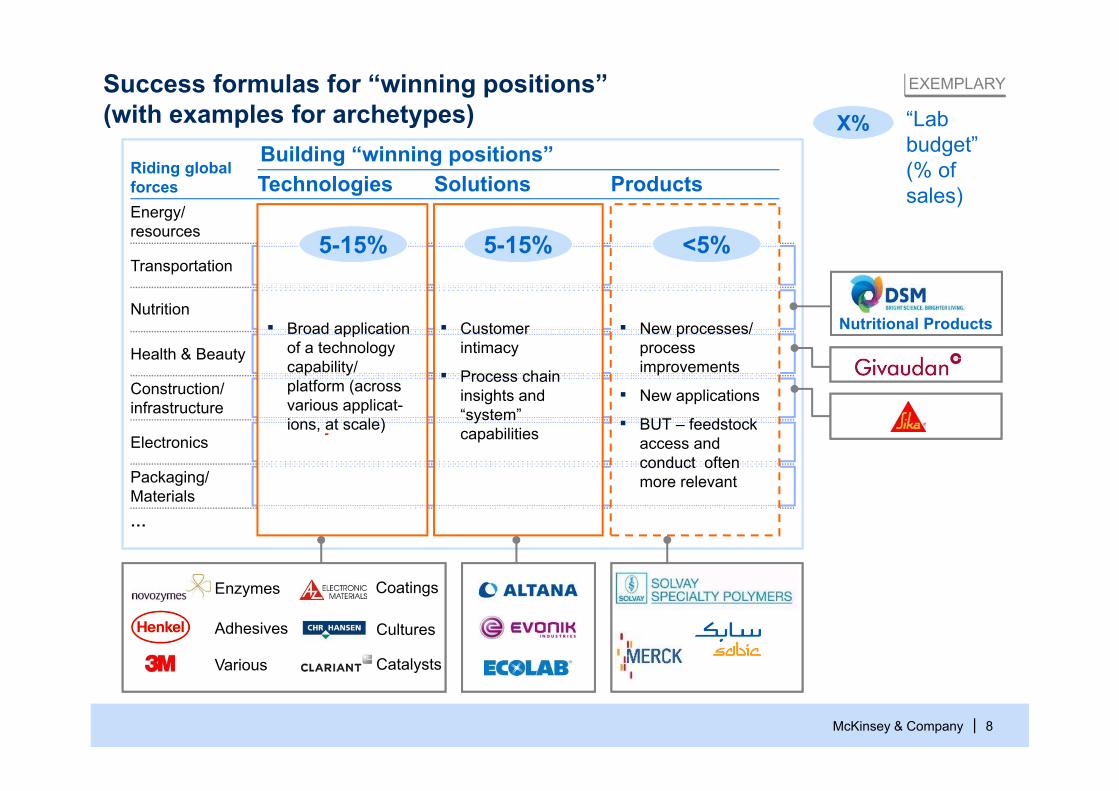

Success formulas for “winning positions” (with examples for archetypes)

EXEMPLARY

…

Energy/resources

Technologies SolutionsBuilding “winning positions”

Riding global forces Products

Nutrition

Transportation

Health & Beauty

Construction/ infrastructure

Electronics

Packaging/ Materials

Adhesives

Various

Enzymes

Cultures

Coatings

Catalysts

▪ Broad application of a technology capability/ platform (across various applicat-ions, at scale)

5-15%

▪ Customer intimacy

▪ Process chain insights and “system” capabilities

▪ New processes/ process improvements

▪ New applications

▪ BUT – feedstock access and conduct often more relevant

5-15% <5%

X% “Lab budget”(% of sales)

Nutritional Products

McKinsey & Company | 9

Beyond stories and opinions …

Top-down perspective Archetypes of successful companies in chemicals –Does Research & Innovation play a role?

Bottom-up perspective Value creation through innovation –What does McKinsey’s InnomaticsTM database say?

McKinsey & Company | 10

Innovation benchmarking – McKinsey's Innomatics™

SOURCE: McKinsey InnomaticsTM Innovation Benchmarking database 10

Examples (all or selected businesses)

Industry benchmarking with > 20 companies and > 100 businesses▪ Return on innovation ▪ Innovation best practices

McKinsey & Company | 11

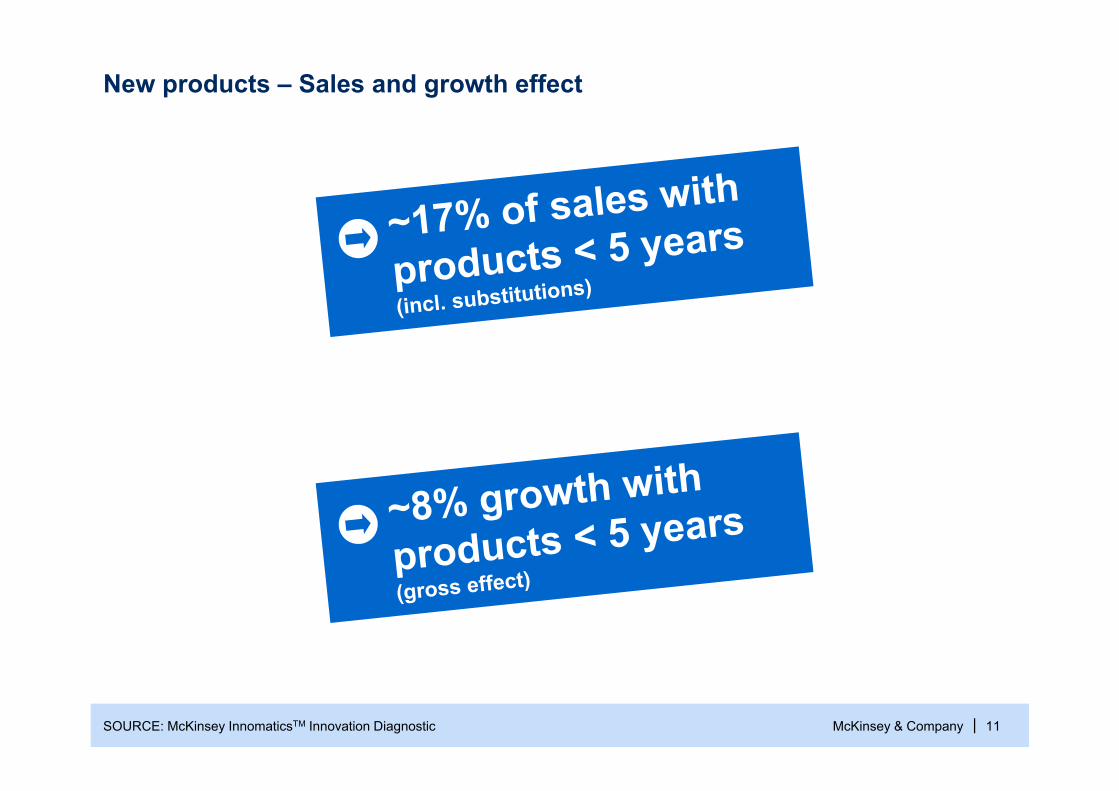

On-top sales from new products (gross effect), % of total sales

Sales from new products, % of total sales

New products – Sales and growth effect

SOURCE: McKinsey InnomaticsTM Innovation Diagnostic

010203040506070

10.09.59.08.58.07.57.06.56.05.55.04.54.03.53.02.52.01.51.00.50

R&D spend for new products/total sales, %

010203040506070

10.09.59.08.58.07.57.06.56.05.55.04.54.03.53.02.52.01.51.00.50

R&D spend for new products/total sales, %

17%

8%

McKinsey & Company | 12

-20

-10

0

10

20

30

40

50

60

70

5.0 5.5 6.0 17.54.54.03.53.02.52.01.51.00.50

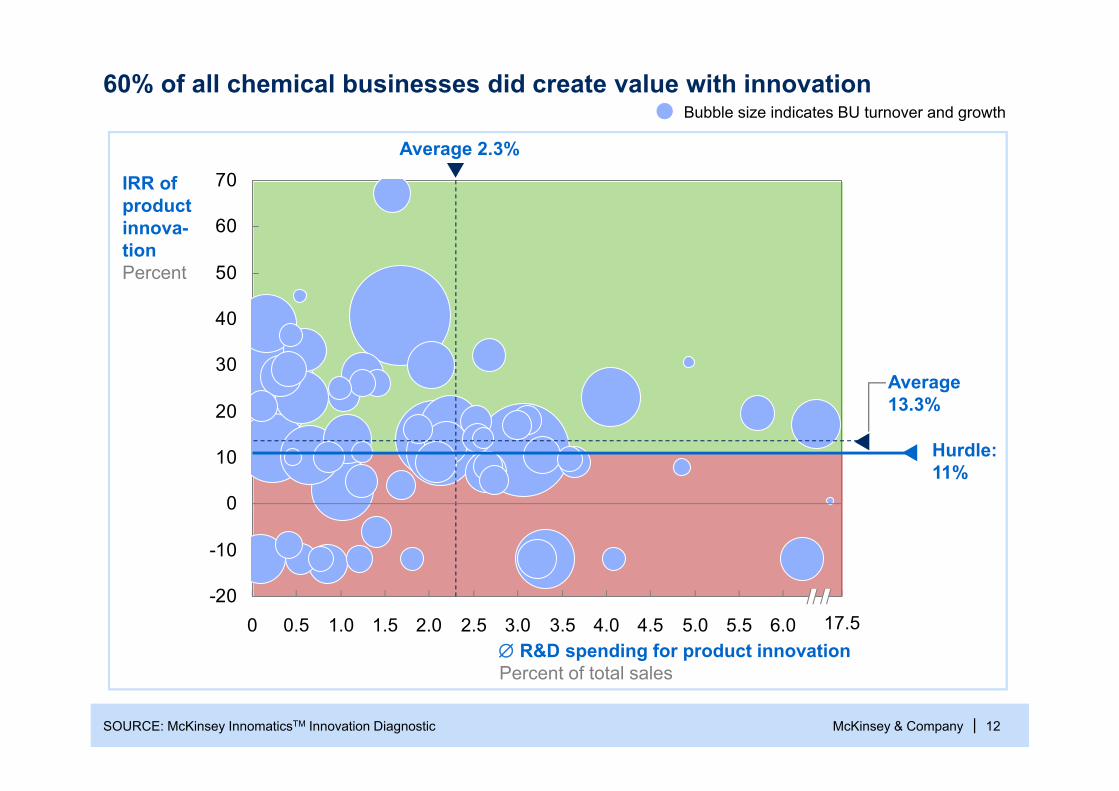

60% of all chemical businesses did create value with innovation

IRR of product innova-tionPercent

R&D spending for product innovationPercent of total sales

Hurdle:11%

Average13.3%

Average 2.3%

SOURCE: McKinsey InnomaticsTM Innovation Diagnostic

Bubble size indicates BU turnover and growth

McKinsey & Company | 13

In summary

Research & Innovation do contribute to growth and value creation of the industry –however, not necessarily for each company

There are very attractive “winning positions” that rely heavily on the ability to innovate at scale

Key observations/success factors for innovation▪ Strategy – reflecting innovation

headroom/tailwind and own capabilities▪ Scale (and/or patience to build) –

critical mass and focus▪ Lab efficiency (and spirit) – work flows,

automation/IT, etc.

McKinsey & Company | 14