impact of branchless banking on customer satisfaction

TRANSCRIPT

The main objective of this research

is to establish how Branchless

banking has impacted on customer

satisfaction in Pakistan. A rapid

evolution in technology over the

past decade has brought

unprecedented changes in the

Pakistan banking industry.

“Impact of

Branchless Banking

on Customer

satisfaction”

Rashid Ali Soomro

DECLARATION

I hereby declare that the project work entitled

“Impact of Branchless Banking on Customer Satisfaction”

Submitted to the KASB Institute of technology, is a record of an original work done by me

under the guidance of Assistant Professor Umer Farooq,a n d t h i s p r o j e c t w o r k i s

s u b mi t t e d i n t h e p a r t i a l f u l f i l l m e n t o f t h e requirements for the award of the

degree of bachelors of Business Administration. The results embodied in this Research

report have not been submitted to any other University or Institute for the award of any

degree or diploma.

Author:

Rashid Ali Soomro

Checked and Approved by

__________________ ____________ Assistant Professor Umer Farooq

Course Supervisor

Faculty of Management Sciences (FMS)

KASBIT

BBA VIII

Page 3 of 19

Acknowledgements

In the Name of Allah, who is the Most Gracious and the Most Merciful, I give thanks to my

creator, the able and powerful Almighty Allah for his help in seeing me through my

Bachelor program. It would not have been an easy achievement if not for His love and

mercy on me. Firstly and foremost, I am grateful to Allah the Almighty for everything He

has granted me, the Most Merciful who has granted me the ability and willing to start and

complete this study. I do pray to His Greatness to inspire and enable me to finish this

dissertation on the required time. Without his permission, for sure I cannot make it possible.

My most profound thankfulness goes to my supervisor, Sir Umar for all his patience,

creativity encouraging guidance, and many discussions that made this study to what it is.

Without his understanding, consideration and advice, this dissertation would not have been

completed successfully my thanks and gratitude goes to all my dearest family members

especially my Brother for being by my side since I left home. Lastly, I am thankful to my

dignified institute KASBIT for giving me the opportunity to carry out this research in a very

conducive environment

Abstract

The purpose of this study is to find the Branchless banking service dimensions through

Internet that will have the impact on customer satisfaction. Many Banks are working in the

Pakistan but I have worked on Silk Bank Pakistan. Questionnaires were used to collect data

from 50 respondents by using convenience sampling. And regression analysis that helps to

obtain the important of branchless banking service dimensions that have the impact on

customer satisfaction. Results showed that providing 24hours-7days services to the

customer, completing each task accurately, contacting staff to check immediately, and

providing accurate information & up to date, transaction process is fast, and providing

online registration times were the important factors that have the impact on customer

satisfaction.

.

Page 5 of 19

(i) TABLE OF CONTENTS Approval &Declaration------------------------------------------------------------------------------------------------ (2)

Acknowledgements ---------------------------------------------------------------------------------------------------- (3)

Abstract ------------------------------------------------------------------------------------------------------------------ (4)

Table of Contents------------------------------------------------------------------------------------------------------- (5)

Chapter No. 1 --- Introduction to Research -------------------------------------------------------------------------------------- (6)

Introduction& Background-------------------------------------------------------------------------------------------- (6)

Research Problem------------------------------------------------------------------------------------------------------- (7)

Research Objectives --------------------------------------------------------------------------------------------------- (8)

Research Question & Key--------------------------------------------------------------------------------------------- (8)

Limitations--------------------------------------------------------------------------------------------------------------- (8)

Scope of study----------------------------------------------------------------------------------------------------------- (8)

Chapter No. 2 --- Literature Review---------------------------------------------------------------------------------- (8)

Overview of Branchless Banking------------------------------------------------------------------------------------- (8)

International Background---------------------------------------------------------------------------------------------- (9)

Customer Satisfaction with Branchless Banking------------------------------------------------------------------- (9)

National Background -------------------------------------------------------------------------------------------------- (9)

Reliability--------------------------------------------------------------------------------------------------------------- (10)

Fees and Charges------------------------------------------------------------------------------------------------------ (10)

Response---------------------------------------------------------------------------------------------------------------- (10)

Customer Support----------------------------------------------------------------------------------------------------- (11)

Privacy security-------------------------------------------------------------------------------------------------------- (11)

Website layout--------------------------------------------------------------------------------------------------------- (12)

Chapter No. 3Research Design-------------------------------------------------------------------------------------- (12)

Hypotheses Development-------------------------------------------------------------------------------------------- (13)

Chapter No. 4 --- Research Methodology-------------------------------------------------------------------------- (14)

Sampling Method and Sample Size--------------------------------------------------------------------------------- (14)

Target population------------------------------------------------------------------------------------------------------ (14)

Data Collection and analysis----------------------------------------------------------------------------------------- (14)

Data Collection Technique------------------------------------------------------------------------------------------- (14)

Chapter No. 5 --- Research Results--------------------------------------------------------------------------------- (15)

Reliability--------------------------------------------------------------------------------------------------------------- (15)

Responsiveness-------------------------------------------------------------------------------------------------------- (15)

Fees And Charge------------------------------------------------------------------------------------------------------ (16)

Privacy Security------------------------------------------------------------------------------------------------------- (16)

Customer Support----------------------------------------------------------------------------------------------------- (16)

Chapter No. 6 --- Conclusion---------------------------------------------------------------------------------------- (17)

Conclusion-------------------------------------------------------------------------------------------------------------- (17)

Recommendations for Future Research---------------------------------------------------------------------------- (17)

References-------------------------------------------------------------------------------------------------------------- (18)

Questionnaire---------------------------------------------------------------------------------------------------------- (20)

Chapter No. 1 --- Introduction

Introduction

The focus of this chapter is to provide a

selective review of the past research works

related to the Branchless banking study. A

lot of research will have done but (as a

sample) very few are related with this

unique one.

In fast moving world of competition the

key advantage for all the organization is to

delivered a maximum kind of new

services to the customers and diverting

customers mind into the satisfaction to

become this advantage for the profit of

organization (Ismail, Madi and

Francis,2009; Shemwell, Yavas and

Bilgin, 1998). A new change of

technology in this country brought

unprecedented changes in the banking

sectors. Information technology playing a

main role in all activities of branchless

banking with the help of advance mode of

technology each individual can do all their

banking activities through the internet

(Young, 2001) Branchless banking is the

self service delivery of channels that

allows banking sector to provide financial

services to their customers in a easy way

that a customer can easily understand the

Branchless banking. Basically this world

is moving with the advantages of advance

technology which is specifically related to

the internet. And the Internet is a powerful

tool that can make businesses more

productive and profitable and has lead to

fundamental changes in how banking

sector save their customers. Now a day’s

many banking sectors are the customer

focused with less customer contact use of

branchless banking through internet

banking. The financial institutions are one

of the most important service providers for

a nation’s economy. Use of Internet

banking is expected to lead to reduced

costs and improved institutions culture and

competitiveness. Through internet the

service delivery channel is seen as

powerful because it can retain young

generation, businessman, who knows

about Branchless banking, and who

continue using banking services from all

locations through internet and advance

technology. Moreover, Internet banking

provides opportunities for a bank to

develop its market by creating a new

customer base from existing Internet users

who can access branchless activities from

any where

The main objective of this research is to

establish how Branchless banking has

impacted on customer satisfaction in

Pakistan. A rapid evolution in technology

over the past decade has brought

unprecedented changes in the Pakistan

banking industry (Reserve Bank of

Pakistan, 2010). According to SBP’s

policy environment for branchless banking

these services are being offered through

alternative delivery channels in the form

of agent network, Telecommunication

Networks, alternate teller machines

(ATMs), and point of sale (PoS), etc

through online banking all type of

transaction can be done in a easy way with

a help of advance mood of technology this

is a key benefit for those who used the

Page 7 of 19

branchless banking it save the customers

to go to a bank physically and complete

the transaction and stand in the lines

through branchless banking people access

banking and complete their transaction.

1.1Background of the Study

Branchless banking is Virtual banking

(Carmel and Scott, 2009). According to

Carmel and Scott (2009), branchless

banking is the delivery of financial

services outside conventional bank

branches using information and

communication technologies. In Pakistan,

banking started with free banking as early

as 2002. Throughout the 1980s the

financial sector was tightly controlled and

highly oligopolistic, with multinational

banks (Barclays and Standard Chartered

Bank) dominating the sector globally.

Presently, the financial sector comprises

the Reserve Bank of Pakistan.

Commercial banks, merchant banks,

building societies, the People's Own

Savings Bank (POSB), insurance

companies, asset management companies,

developmental financial institutions, the

Karachi stock exchange, microfinance

institutions and money transfer agencies.

Most institutions have the majority of their

branches in major cities, Branchless

Banking industry has operated in a

relatively stable environment from some

periods. However, with the advent of

Internet banking, the industry is

characterized by dramatically aggressive

competition. The shift from traditional

branch banking to Internet banking has

meant that new strategies to attract new

customers and retain existing ones have

become critical called as Branchless

Banking (Wong, 2005). Branchless

Banking allows customers to access

banking services 24 hours a day, 7 days a

week. Like ATMs, Point of sale POS

devices, EFTPOS devices and mobile

phones Branchless or internet banking

empowers customers to choose when and

where they conduct their banking

transactions. The long queues and huge

crowds are highly devastating and

discouraging most times, especially when

the weekend is near. Most times, these

long queues are as a result of the

breakdown of the computers used by the

Bank tellers, sometimes it occurs as a

result of the Bank tellers absolving them

from duty and passing the bulk to

someone else.

1.2 Problem statement

Branchless banking is a fastest and

economically feasible route to distribute

financial services without depending

on bank branches. It is a type of banking

where the banking customer does not need

to visit a branch or central site of the bank.

. Due to economic ups and downs the

banking sector of Pakistan faces UN

stability although it is backbone of our

economy. To flourish this new system

were lunched as far as technology is

concern. Time is very important element

in the life of business men. The new

Page 8 of 19

concept of branchless banking helps them

to save their time. For this we have to

examine impact of branchless banking on

customer satisfaction

1.3 Research Objective

Customer satisfaction is ultimate objective of

any business. In this study I am going to

examine the methods of delivering branchless

banking services to customer effectively which

ultimately leads to customer satisfaction and

retention

1.3.1 Research Question

What are the major factors affecting

customers’ satisfaction with Branchless

Banking or internet banking

1.3.2 Key Research Question

What are the procedures of developing an

efficient branchless banking system

(identify weakness)?

What will be the future of branchless

banking in Pakistan (technological

developments)?

How is the branchless banking organize

all over the Pakistan (rural and urban both

areas)?

1.4 Limitations

Customer knowledge, trust on technology,

proper reply from banks and customers,

technological knowhow these all are the

limitations other than that time, finance,

city law and order situations also impact

on the working. This study is not covering

all the cities of Pakistan. I can only work

in Karachi and study the impact on

customer satisfaction. The reason is that

this city is business hub.

1.5 Scope of study

This study focuses on the customer

satisfaction due to branchless banking.

The study provides proper evidence to

those concern people who can get benefit.

This study also provide them the way that

customer can save not their time but also

save opportunity cost. Also for banking

sector it leads to growth and profitability.

Chapter No 2--- Literature Review:

Overview of Branchless Banking:

Branchless banking is a type of banking

that takes place where the banking

customer does not need to visit a branch or

central location of the bank physically.

Financial institution business may be

completed through technological services,

such as online Banking transactions, over

the Mobile phone, or through an ATM

(Automated Teller Machine) Now a day’s

Branchless banking is very common

activity, and many people are able to

complete all their banking online without

ever having to visit the bank. There are

many benefits to branchless banking to the

customers. There is no need for the human

Page 9 of 19

to take time out of the day to physically

visit the bank in order to withdraw or

deposit money these activities customer

can do through branchless banking easily

Examples of branchless banking

technologies are the Technology, Internet,

automated teller machines (ATMs), Point

of sale POS devices, and mobile phones

etc. Each of these technologies serves to

deliver a set of branchless banking

services to the customers

International Background of the

Branchless Banking:

The concept of branchless banking first

introduced by United Kingdom after that a

Midland bank has started this concept in

with more futures. At that time Midland

Bank was one of the Big Four banking

groups in the United Kingdom for most of

the 20th century. It is now part of HSBC.

HSBC is a British multinational banking

and financial services company and the

headquartered in London United

Kingdom. It is the world's second largest

bank providing financial services to the

customers. It was founded in London in

1991 by the Hongkong and Shanghai

Banking Corporation to act as a new group

holding company

National Background of the Branchless

Banking:

Pakistan has been declared as a ground

innovation in branchless banking and has

been successful in developing a variety of

business models involving a wide range of

players many banks has played a role in

activities of branchless banking, including

mobile network operators (MNOs),

technology companies and even courier

businesses etc. According to history

Branchless banking concept was first

introduced in Pakistan in April 2008 under

the regulation of State Bank of Pakistan

Government has provided clear guidance

to the financial institutions. (Weijters et

al., 2005, p. 9)

Customer Satisfaction with Branchless

Banking:

In this world all knows that customers

place great importance on the value and

Convenience offered by financial

institutions (Lewis and Soureli, 2006) and

that customer satisfaction (which is

affecting on the service quality

perceptions) Many Research create

confusion and gaps in understanding the

nature of online service quality process,

and how it operates within the financial

institution it depends upon customer lack

of specific knowledge as to how the

quality of Branchless Banking web sites

impacts on customers mentality it all

depends upon customer satisfaction with

their bank (Carmel and Scott, 2009).

Automated transaction of services has the

potential to make customers enthusiastic

about their financial institution. and to tell

other potential customers about its

advantages. After that, automated service

users would be more likely to comment

positively about their bank to other

potential customers, recommending the

bank encouraging and motivating others to

Page 10 of 19

do business with it (Joseph and Stone,

2003) Vol. 1 | No. 2 | August 2012

Reliability

Reliability involves consistency of

performance and dependability of silk

bank branchless banking activities. It

means that the silk bank performs the

service right the first time to their

customers. It also means that the silk bank

honors its promises with in Pakistan.

Specifically silk bank involves accuracy in

billing in all departments, keeping records

correctly and performing the service at

proper time. (ISSN 2319–6912 (March

2013, issue 2 volume 3) Reliability also

“refers to the correct technical functioning

of a silk bank technology and the accuracy

of service delivery to their customer at a

time with proper management” customers

should be specifically influenced by the

reliability of advance technology because

they might be associated with risks such as

the technology malfunctioning

(Shamdasani 2008)

Fees and Charges:

Fees and charges of every online

transaction impacts on Service quality in

branchless banking financial institution

are important when human internet

interaction is the main service delivery

and communication strategy with their

potential customers. After introducing

branchless banking Silk bank offering

high quality services to satisfy potential

consumers but it needs, that at lower costs,

because it is competitive advantage of silk

bank. Online banking has successfully

reduced operating administrative costs and

other costs In this world every person

want to save money when a silk bank

provides a lower cost services as

compared to other financial institution in

Pakistan result customers prefer a lower

cost bank easily it shows that Cost savings

have helped online based banks offering

lower or no service fees it’s a advantage

for the financial institution for diverting

customers expectation to the online banks,

it means it is hypothesized that fees and

charges have positive impact on customer

satisfaction

Response

Response means Customers are

particularly interested in the speed with

which a service is offered or delivered to

their potential customers (The Wall Street

Journal, 1990). Most researches have

indicated that few customers overrate the

processing time of a services especially in

Pakistan According to employees of silk

bank on certain occasion customers has a

strong liking to carry out the service by

them. This activity is particularly justified

by the willingness of the customers to up

the speed of delivery it is mandatory for

the silk bank to upgrade system and

manage delivery time and follow advance

mood of technology. Because slow service

delivery has a negative effect on few

customers if customers are expecting a

Page 11 of 19

fast service delivery it is clear that

customers using the service more

positively. That time was an important

factor for each individual in using a new

service or advance technology in banks. In

this fast moving world time savings were

essential for each individual who use

online banking and online shopping

(Hornik, 1984)

Customer Support Customer support including before sell

support or before doing any transaction

and after sell supports or after doing any

transaction. Before doing any activity

customer make decisions, at that time the

financial institution should give some

support to attract potential customer,

because the customers want to fulfill the

communication gap for example let

customers feel that they are at own place.

The relationship between customers is like

a good friend not like a business person.

After customers buy the services or

products from bank, Bank should solve the

problem that customers have in their mind

and few questions according to the

problems bank needs to communicate with

customer and provide better solution and

easily attract customer through

communication style, in the branchless

banking support is also important for

everyone. Because Not everyone good at

the computer and not everyone now about

branchless banking usage so they need

guide how to use branchless banking. And

maybe someone good at computer but still

have problems and then they also need

support it’s a opportunity for the bank to

communicate with customer and easily

attract them after buying some services

through the internet customers might have

questions in their mind and waiting to

answer so he or she also needs support

from financial institution. So support is

very important for satisfying the

customers

Privacy security

This is the guarantee from the state bank

of Pakistan that the record showing

banking activities and security of account

information is not shared to everyone

(Yang and Fang 2004; Saha and Zhao,

2005). Security and privacy is important in

the decision of consumers to use online or

Internet banking. When the security is

improved in financial institutions then

more customers would be willing to

conduct their transactions over the Internet

(branchless banking). When the security is

not properly provided to the customers it

shown to slow growth of Internet banking

in the country most individuals had

unclear knowledge and understanding of

online banking after using online banking

he knows about the risk and they avail

online baking. Some time individuals are

aware that their bank will protect their

privacy and security and also have strong

confidence in their bank but have a weak

confidence in technology use for online

banking services. Security and privacy

issues are the major factor preventing

customers from using the Internet for

financial transactions finally one of the

most important future challenges facing

each customers of a silk bank is the fear of

higher risks from each online transaction

associated with using the Web branchless

banking and financial transaction over the

bank.

Page 12 of 19

Website layout It is necessary for the financial institution

to design a web site visually more

attractive and enjoyable. Discussed

website must content its four aspects about

us, Vision/Mission, information

organization, and structure of all activities.

Silk bank is testing accessibility of their

customer websites with automated tools

advance technology and user accessibility

trials to their website. It is clearly

hypothesized that website layout has a

positive effect on quality of banks to

customer satisfaction. Content on the web

site of the bank is one of the factors

influencing on branchless banking

acceptance. On the other hand, quality of

portal, designs, graphics, Writing or colors

these things identify the good image of the

bank and enhance efficient use of potential

customers. Discuss that such website

features as website speed, Browsing, web

site content and design, navigation,

interactivity privacy and security all

influence on customers satisfaction the

level and nature of customer participation

had the more impact on the quality of the

service experience provided by silk bank

to their customers and issues such as

customers' zone of tolerance, and the

degree of understanding the customer’s

needs and emotional response to their

customers, these impact on service quality

and customer satisfaction in this variable it

is Identified five quality dimensions that

have an impact on “customers”

satisfaction in an using branchless

banking: content of website, accuracy,

format, ease of use, timeliness. It is

hypothesized that website layout has

positive effect on customer satisfaction

Chapter No. 3 --- Research design

The research design was a combination of

quantitative and qualitative research

design so as to obtain detailed information

that helped me to establish the relationship

between Branchless banking and customer

satisfaction.

Reliability

Fees and

charges

Response

Customer

Support

Privacy

Security

Website

Layout

Service

Quality

Customer

Satisfaction

Page 13 of 19

Hypothesis Development:

Reliability

H1

Reliability has relationship with service

quality in Branchless Banking & impact

on Customer Satisfaction.

Ho

Reliability has no relationship with service

quality in Branchless Banking & impact

on Customer Satisfaction.

Fees and charges

H1

Fees and charges have relationship with

service quality in branchless banking &

impact on customer satisfaction.

Ho

Fees and charges have no relationship

with service quality in branchless banking

& impact on customer satisfaction.

Response

H1

Response has relationship with service

quality in branchless banking & impact on

customer satisfaction.

Ho

Response has no relationship with service

quality in branchless banking & impact on

customer satisfaction.

H1

Customer Support has relationship with

service quality in branchless banking &

impact on customer satisfaction.

Ho

Customer Support has No relationship

with service quality in branchless banking

& impact on customer satisfaction.

Privacy/Security

H1

Privacy/Security has relationship with

service quality in branchless banking &

impact on customer satisfaction.

Ho

Privacy/Security has No relationship with

service quality in branchless banking &

impact on customer satisfaction

Website layout

H1

Website layout has relationship with

service quality in branchless banking &

impact on customer satisfaction.

Ho

Website layout has No relationship with

service quality in branchless banking &

impact on customer satisfaction

Page 14 of 19

Chapter No 4--- Research

Methodology:

Overview

Research Methodology chapter presents

the methodological concerns used in

conducting this research and provides a

justification for steps taken. It covers the

general research perspectives, data

collection summary, statistical

measurement methods, access strategies

and credibility of the research in this

article

Sampling Method and Sample Size:

The study is about impact of branchless

banking service quality on customer

satisfaction of banks online services

provided to the customers, in this study 50

respondents of only Bank AL Habib ltd

have been selected by using convenience

sampling method. Basically Convenience

sampling is a non-probability sampling

technique where respondents are selected

because of their convenient accessibility

and proximity to the researcher.

Target population

The study is depending up on Bank Al

Habib LTD Head office. The target

population for the study is to be 50

Account Holders of the Bank AL Habib

LTD, from them 12 employees of Bank

AL Habib.

Data Collection and analysis

This survey is conducted on Bank AL

Habib LTD in Pakistan city to collect

primary data by using structured

questionnaire; Qualitative approach with

convenience sampling process has been

used to collect data for this research. And

this study called as Case study. All

questions are closed-ended because all

possible answers were given to the

respondents. In the Likert scale (where 1=

strongly disagree to 5 = strongly agree)

has been used for the main research

questions. After data collection, by using

PH state (17.0 versions), analyzing

interpretation have been conducted to test

the strength of associations between the

study and variables

Data Collection Technique

Data collection technique I have used

structured type of questionnaire.

Questionnaire is easy and understandable

for everyone. None of technical terms

used in questionnaire, basically the

Questionnaire is based on some specific

questions related to the dependent variable

and independent variables which can

easily identified a result.

Page 15 of 19

Chapter No. 5 --- Research Results

HP1 Reliability

Data

Null Hypothesis

= 3

Level of Significance 0.05

Population Standard Deviation 1.019

Sample Size 50

Sample Mean 3.95

Intermediate Calculations

Standard Error of the Mean 0.144108362

Z Test Statistic 6.592261454

Two-Tailed Test

Lower Critical Value -

1.959963985

Upper Critical Value 1.959963985

p-Value 4.33178E-11

Reject the null hypothesis

Interpretation:

In this analysis we have put 5 options

Likert scale. We have value of =3 which

is mid-value of the scale. Because system

only find out the middle value.

We put 0.05 as the level of significance

due to management sciences studies.

Following are the interpretation of the

hypothesis.

We use 50 questionnaires of data sample

size is 50

Interpretation hp 1:

The p- value 4.33178E-11 is less

than 0.05. It means that null

hypothesis is rejected.

The value of standard deviation comes

out to be 1.019 which can deviate from

its actual value of mean 3.95

Sample mean is 3.95 which is nearest

to 4. It means that more respondents

are agreed with this statement that’s

why null hypothesis is rejecting.

Reliability impacts on Customer

Satisfaction.

HP2 Responsiveness

Data

Null Hypothesis

= 3

Level of Significance 0.05

Population Standard Deviation 1.062401

Sample Size 50

Sample Mean 3.78

Intermediate Calculations

Standard Error of the Mean 0.15024619

Z Test Statistic 5.191479388

Two-Tailed Test

Lower Critical Value -

1.959963985

Upper Critical Value 1.959963985

p-Value 2.0863E-07

Reject the null hypothesis

Interpretation hp 2:

The p- value 2.0863E-07 is less

than 0.05. It means that null

hypothesis is rejected.

The value of standard deviation

comes out to be 1.062401 which

can deviate from its actual value of

mean 3.78.

Sample mean is 3.78 which is

nearest to 4. It means that more

respondents are agreed with this

statement that’s why null hypothesis

Page 16 of 19

is rejecting. Responsiveness is

impact on Customer Satisfaction.

HP3 Fees and Charge

Data

Null Hypothesis

= 3

Level of Significance 0.05

Population Standard Deviation 1.0953

Sample Size 50

Sample Mean 3.715

Intermediate Calculations

Standard Error of the Mean 0.154898811

Z Test Statistic 4.615916631

Two-Tailed Test

Lower Critical Value -

1.959963985

Upper Critical Value 1.959963985

p-Value 3.91364E-06

Reject the null hypothesis

Interpretation hp 3:

The p- value 3.91364E-06 is less

than 0.05. It means that null

hypothesis is rejected.

The value of standard deviation

comes out to be 1.0953 which can

deviate from its actual value of

mean 3.715

Sample mean is 3.715 which is

nearest to 4. It means that more

respondents are agreed with this

statement that’s why null hypothesis

is rejecting. Fees and Charge is

impact on Customer Satisfaction

HP4 Customer Support

Data

Null Hypothesis

= 3

Level of Significance 0.05

Population Standard Deviation 1.0774

Sample Size 50

Sample Mean 3.56

Intermediate Calculations

Standard Error of the Mean 0.152367369

Z Test Statistic 3.675327617

Two-Tailed Test

Lower Critical Value -

1.959963985

Upper Critical Value 1.959963985

p-Value 0.000237544

Reject the null hypothesis

Interpretation hp 4:

The p- value 0.000237544 is less

than 0.05. It means that null

hypothesis is rejected

The value of standard deviation

comes out to be 1.0774 which can

deviate from its actual value of

mean 3.56.

Sample mean is 3.56 which is

nearest to 4. It means that more

respondents are agreed with this

statement that’s why null hypothesis

is rejecting. Customer support is

impact on Customer Satisfaction

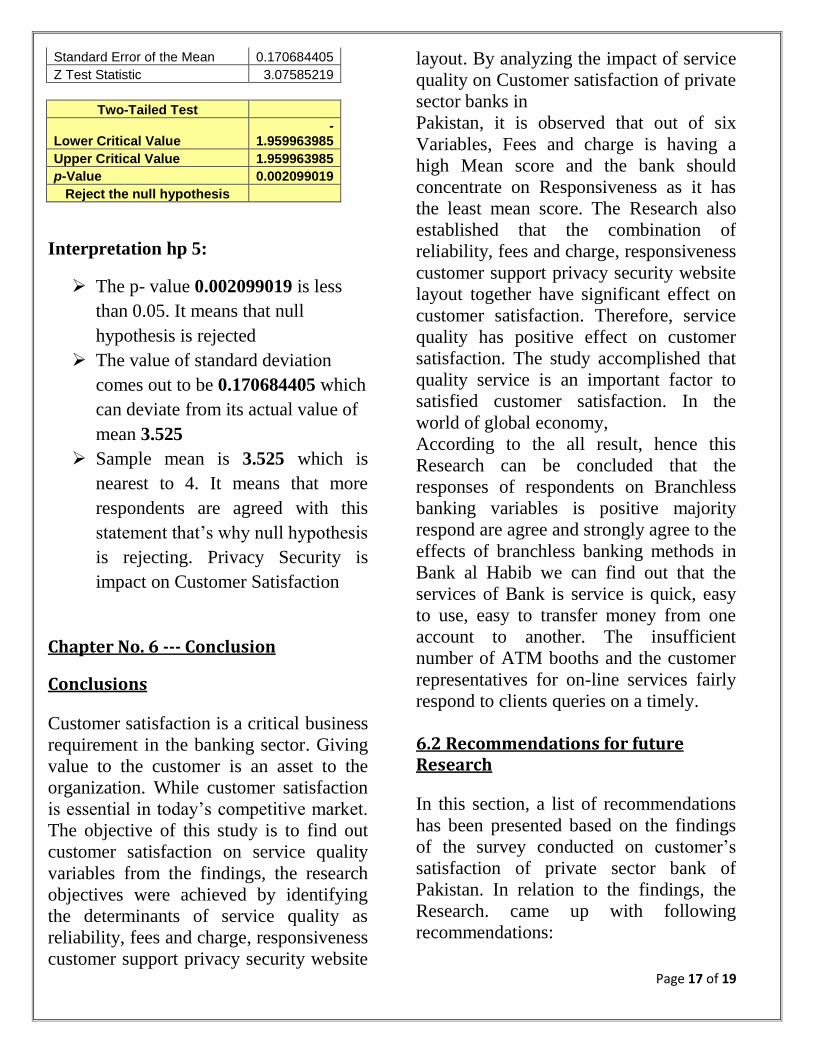

HP5 Privacy Security

Data

Null Hypothesis

= 3

Level of Significance 0.05

Population Standard Deviation 1.206921

Sample Size 50

Sample Mean 3.525

Intermediate Calculations

Page 17 of 19

Standard Error of the Mean 0.170684405

Z Test Statistic 3.07585219

Two-Tailed Test

Lower Critical Value -

1.959963985

Upper Critical Value 1.959963985

p-Value 0.002099019

Reject the null hypothesis

Interpretation hp 5:

The p- value 0.002099019 is less

than 0.05. It means that null

hypothesis is rejected

The value of standard deviation

comes out to be 0.170684405 which

can deviate from its actual value of

mean 3.525

Sample mean is 3.525 which is

nearest to 4. It means that more

respondents are agreed with this

statement that’s why null hypothesis

is rejecting. Privacy Security is

impact on Customer Satisfaction

Chapter No. 6 --- Conclusion

Conclusions

Customer satisfaction is a critical business

requirement in the banking sector. Giving

value to the customer is an asset to the

organization. While customer satisfaction

is essential in today’s competitive market.

The objective of this study is to find out

customer satisfaction on service quality

variables from the findings, the research

objectives were achieved by identifying

the determinants of service quality as

reliability, fees and charge, responsiveness

customer support privacy security website

layout. By analyzing the impact of service

quality on Customer satisfaction of private

sector banks in

Pakistan, it is observed that out of six

Variables, Fees and charge is having a

high Mean score and the bank should

concentrate on Responsiveness as it has

the least mean score. The Research also

established that the combination of

reliability, fees and charge, responsiveness

customer support privacy security website

layout together have significant effect on

customer satisfaction. Therefore, service

quality has positive effect on customer

satisfaction. The study accomplished that

quality service is an important factor to

satisfied customer satisfaction. In the

world of global economy,

According to the all result, hence this

Research can be concluded that the

responses of respondents on Branchless

banking variables is positive majority

respond are agree and strongly agree to the

effects of branchless banking methods in

Bank al Habib we can find out that the

services of Bank is service is quick, easy

to use, easy to transfer money from one

account to another. The insufficient

number of ATM booths and the customer

representatives for on-line services fairly

respond to clients queries on a timely.

6.2 Recommendations for future Research

In this section, a list of recommendations

has been presented based on the findings

of the survey conducted on customer’s

satisfaction of private sector bank of

Pakistan. In relation to the findings, the

Research. came up with following

recommendations:

Page 18 of 19

Since Bank Al Habib is a service

oriented Financial Institution hence

providing continuous training to the

employees on issues like courtesy,

Behavior and communication skills

while dealing with customers is

more importance.

And also Bank Al Habib is a

customer oriented organization

hiring potential human resource is a

must. And for this reason, the bank

should hire self-motivated,

enthusiastic employees who will

like to deal with customer and will

try to solve customer complaints

and other issues in an effective

manner. Only then the bank can

render superior customer services

and enjoy the benefit in the long

run.

In order to retain the existing

customers and to improve service

quality, the Bank Al Habib should

continuously maintain error-free

transactions, since bank accounts

and figures are very sensitive for

each and every customer.

The Bank Al Habib management

needs to improve quality services so

as to satisfy customer’s needs. The

bank needs to pay much attention

on the customer complaints in order

satisfy the customer’s expectation.

Individual attention should be given

to customers in order to better

understand their needs and better

satisfy them for solving all the

issues of Banks.

References

International Journal of Humanities and

Management Sciences (IJHMS) Volume

1, Issue 1 (2013) ISSN 2320–4044

(Online)

Mohamad Rizal Abdul Hamid,

HanudinAminSuddinLada, and Noren

Ahmad (2007), A comparative analysis of

Internet banking in Malaysia

and Thailand, Journal of Internet business

vol4, 2007.

Muffatto, M. & Panizzolo, R. (1995). A

process based view for customer

satisfaction. International Journal of

Quality & Reliability Management,

12(9): pp. 154-169.

Oliver, R.L., (1997). Satisfaction: A

Behavioral Perspective on the

Consumer, McGraw-Hill, New York

International journal of Innovative

Research in Management ISSN 2319–

6912 (March 2013, issue 2 volume 3)

International Journal of Advanced

Research in Management and Social

Sciences ISSN: 2278-6236

Banking Survey. (2011). Annual survey

Results, Harare, Zimbabwe.

Khan. (2007). The effects of trust and

interdependence on relationship

commitment: a trans- Atlantic study.

International Journal of Research in

Marketing, Vol.13 No. 4, pp. 303-17.

Page 19 of 19

http://www.garph.co.uk/IJARMSS/Aug20

12/18.pdf

http://www.isaet.org/images/extraimages/I

JHMS%200101224.pdf

http://www.tjmcs.com/includes/files/articl

es/Vol9_Iss1_3340_The_Impact_of_Servi

ce_Quality_on_Cu.pdf

http://www.iosrjournals.org/iosr

jhss/papers/Vol18-issue5/F01853944.pdf

http://www.distance.mak.ac.ug/sites/defau

lt/files/publications/NAKANJAKKO.pdf

Zhilin Yang, Xiang Fang, “Online service

quality dimensions and their relationships

with satisfaction: A content analysis of

customer reviews of securities brokerage

services”, “International Journal of

Service Industry Management”, MCB UP

Ltd: Emerald Group Publishing Limited,

vol. 15, no. 3, pp. 85-97, 2004.

Ishfaq Ahmed, Shafiq Gul, Umer Hayat,

Mohammad Qasim, “Service quality,

service features and customer complaint

handling as the major determinants of

customer satisfaction in banking sector: A

case study of National Bank of Pakistan”,

2001.Available:http://www.wbiconpro.co

m/5[1].ISHFA.pdf.

E.M. Awad, The Structure of E-commerce

in the Banking industry: An Empirical

Investigation, SIGCPR2000 Evanston

Illinois USA.

M.M Anuar, F. Adam, and Z. Mohammad,

Muslim consumers’ perception on Internet

Banking services, International Journal of

Business and social Science, Vol. 3, No. 5,

(2012) 63-71.

S. F. Sakhaei, A. J. Afshari, E. Esmaili / J.

Math. Computer Sci.9 (2014),33-40