impact of airline market consolidation towards air traffic ... · impact of airline market...

TRANSCRIPT

UNIVERSITY OF SOUTH FLORIDA

IMPACT OF AIRLINE MARKET CONSOLIDATION TOWARDS AIR TRAFFIC IN

FLORIDA TTE 5620 | TERM PROJECT

MENON, NIKHIL

5/2/2014

1 INTRODUCTION

The US domestic airline passenger market has undergone tremendous amount of change since

the deregulation of 1978. Airlines have repeatedly merged to exploit and scale network

economies of scale. As of now, the latest merger to have hit the ground running is the merger

between American Airlines and US Airways, the merger of which, when successful will create

the biggest airline in the US.

There has been a massive spurt in airline market consolidation over the last decade. According to

Perry Flint (Air Transport World), “The US airline industry has always wanted to consolidate. It

tends to happen in bunches, until Washington becomes concerned and tries to block it.” The

airline market consolidation phenomenon is known to be a mixed blessing with the majority of

the upper hand at the hands of the airline companies and the consumers (airline passengers) on

the other side of the debate.

1.1 MOTIVATIONS FOR CONSOLIDATION The motivations for consolidation are often complex and manifold. Some of them are as under:

i. Airlines consolidate for maintaining cost efficiency. It is also a way in which they

extend the foothold on the market.

ii. It is usual for airlines to enter into agreements with other airlines that operate on

different markets from themselves. In doing so, they have a complimentary effect than

that of a competitive one. This leads to network expansion.

iii. A third reason why some airlines consolidate is to improve their brand image or quality

of service. These kinds of steps can usually lure rival airlines from entering into

codeshare agreements.

1.2 EFFECTS OF CONSOLIDATION Some effects of consolidations are as follows:

i. Airline mergers and/ or consolidation usually lead to lesser competing entities for a

particular market. This leads to lesser options for the customer and in such a situation,

he/ she is forced to pay a higher price for using the service.

ii. Consolidation in one end can cause a possible coordinated behaviour among the

remaining network airlines, which shall also lead to higher fares, higher fees and

limited services.

iii. Smaller markets are usually the most affected due to consolidation. It is usual to

observe a scenario where the merging airlines are both dominating that small region

and a merger leads to severe reduction in the number of flights.

1.3 RESEARCH OBJECTIVE The objective of this term paper shall be to analyze the impact of airline mergers and market

consolidation towards air traffic in Florida airports. In saying so, the term paper shall aim to

address the overall airline mergers and acquisition scenario over the last decade in the United

States. As a second stage to the paper, there shall be an attempt to assess the impact of these

mergers and acquisitions on the market – both at an overall airport level as well as at an airline

route level.

1.4 CASE STUDY & DATA SOURCE The case studies adopted for the course of this term paper are the 4 major airports in the state of

Florida. They are:

i. Miami International Airport (MIA)

ii. Orlando International Airport (MCO)

iii. Fort Lauderdale Hollywood International Airport (FLL)

iv. Tampa International Airport (TPA)

The data sources that have been referre3d to for the completion of this term paper are mainly

two:

i. Bureau of Transportation Statistics (BTS) – T100 database (accessible at:

http://www.transtats.bts.gov/DL_SelectFields.asp?Table_ID=258)

ii. Bureau of Transportation Statistics (BTS) – Airline Passengers & Traffic Data

(accessible at:

http://www.rita.dot.gov/bts/data_and_statistics/by_mode/airline_and_airports/airline_pas

sengers.html)

2 AIRLINE MERGERS AND ACQUISITIONS

Table 1 below lists all the mergers and acquisitions that have taken place in the United States

since year 2005.

TABLE 1 – LIST OF AIRLINE MERGERS

As can be seen from Table 1, a lot of mergers took place in the last 10 years, starting from year

2005. Some of the biggest legacy carrier mergers that took place in this period were the Delta –

Northwest merger of 2008 and the United – Continental merger of 2010. Both these mergers

produced airlines which were at that point, the biggest airlines in the United States. Several low

cost carriers (LCCs) merged along the same time though their effects were far lesser than that

observed with the legacy carriers.

For the purpose of this term paper, the two mergers that are going to be focused in detail are the

Air Tran – Southwest merger of 2010 and the recently announced US Airways – American

Airlines merger of 2013.

3 METHODOLOGY

The methodology adopted for the course of this term paper can be divided into the following

stages:

i. The impact of airline market consolidation will be assessed at two levels – individual

airport level in terms of the passenger and load factors; and the individual airline route

level in terms of the total passengers.

a. The main objective of this exercise shall be to see whether airline mergers have

led to highly concentrated markets at the airport or the airline route level.

ii. The evidence for market power shall be established by the Herfindahl Hirschman Index

(HHI), which will be calculated at the overall airport and route levels.

3.1 HERFINDAHL HIRSCHMAN INDEX (HHI) The Herfindahl Hirschman Index (HHI) is a commonly used tool to analyze competition by

measuring market competition. It is a tool that is not only used in the airline industry, but also

used in a variety of other fields such s marketing, business and operations research.

It is calculated by summing up the square of the market shares for firms competing in the

marker. The Herfindahl Hirschman Index can be calculated as shown below:

The commonly used yardstick for measuring HHI is as given below:

3.2 AIRPORT LEVEL CONCENTRATION For the analysis at the airport level, several assumptions are made for the course of this term

paper. The assumptions have been taken in order to simplify the analysis procedures in the wake

of time limitations. They are as under:

i. Airlines Analyzed: Delta, American Airlines, United Airlines, Air Tran, Southwest, US

Airways.

ii. All the other airlines, not listed in the (i) have been categorized as being in the ‘others’

category for the purpose of analysis.

iii. The first year of the AirTran – Southwest merger announcement (2010) has been taken as

the first year of the combined market share.

iv. In order to assess the impact of the proposed US Airways – American Airlines merger for

year 2013, year 2011 has been taken as the first year of the combined market share. This

has been done in order to check for the impact, as data for year 2013 is still not fully

available.

The results of the analysis conducted are as shown in the next section. Some of the results have

been shown in the next section

3.3 AIRLINE ROUTE LEVEL CONCENTRATION For the analysis at the airport level, several assumptions are made for the course of this term

paper. The assumptions have been taken in order to simplify the analysis procedures in the wake

of time limitations. They are as under:

i. Airlines Analyzed: Delta, American Airlines, United Airlines, Air Tran, Southwest, US

Airways.

ii. The first year of the AirTran – Southwest merger announcement (2010) has been taken as

the first year of the combined market share.

iii. In order to assess the impact of the proposed US Airways – American Airlines merger for

year 2013, year 2011 has been taken as the first year of the combined market share. This

has been done in order to check for the impact, as data for year 2013 is still not fully

available.

Analyzing at the airline route level, there are two possible scenarios concerning market

concentration:

i. Two airlines serving a market merge, with no other competing airlines. This leads to a

monopoly on that particular route by the merging airlines.

ii. Two airlines serving a market merge, with the existence of other competitors.

Depending on the market concentration of the merging entities, this scenario could lead

to possible market concentration effects.

The results of the analysis conducted are as shown in the next section. Some of the results have

been shown in the next section while the rest of the routes analyzed have been presented in the

appendix.

4 RESULTS

4.1 AIRPORT LEVEL CONCENTRATION At the airport level, the analysis was done in order to calculate the HHI of the airlines studied for

the purpose of this term paper. In order to do this, the market shares of each airline have been

estimated from year 2003 to 2012. The market shares have been converted into corresponding

HHI values. Once that is done, the airport level HHI is calculated for each year. Once the first set

of HHIs are generated, new HHI values with the combined market share (accounting for the

mergers) are generated. The airport level HHIs are then calculated and then the difference in HHI

is analyzed.

TABLE 2 – AIRPORT LEVEL HHI – MIA

From the first table, it can be seen that MIA has a very high HHI index. This is primarily due to

the fact that 75% of all flight operations from MIA are by American Airlines (~ 75%). A HHI

index in the excess of 6000 is an indicator of high concentration (HHI > 2500). As can be seen

from the second table, the difference in HHI [D(HHI)] at MIA is almost negligible with the

AirTran – Southwest merger, but this becomes more and more relevant with the proposed

American – US Airways merger. A difference in HHI of more than 200 is considered to be

significant.

TABLE 3 - AIRPORT LEVEL HHI – MCO

As can be seen for MCO, the change in HHI is in the range of 650, which is a significant change

that can be observed with the proposed mergers.

TABLE 4 - AIRPORT LEVEL HHI – FLL

FLL indicates concentration even before the mergers are proposed, but the proposed mergers are

set to increase the HHIs beyond the significant thresholds by only a very low margin.

TABLE 5 - AIRPORT LEVEL HHI – TPA

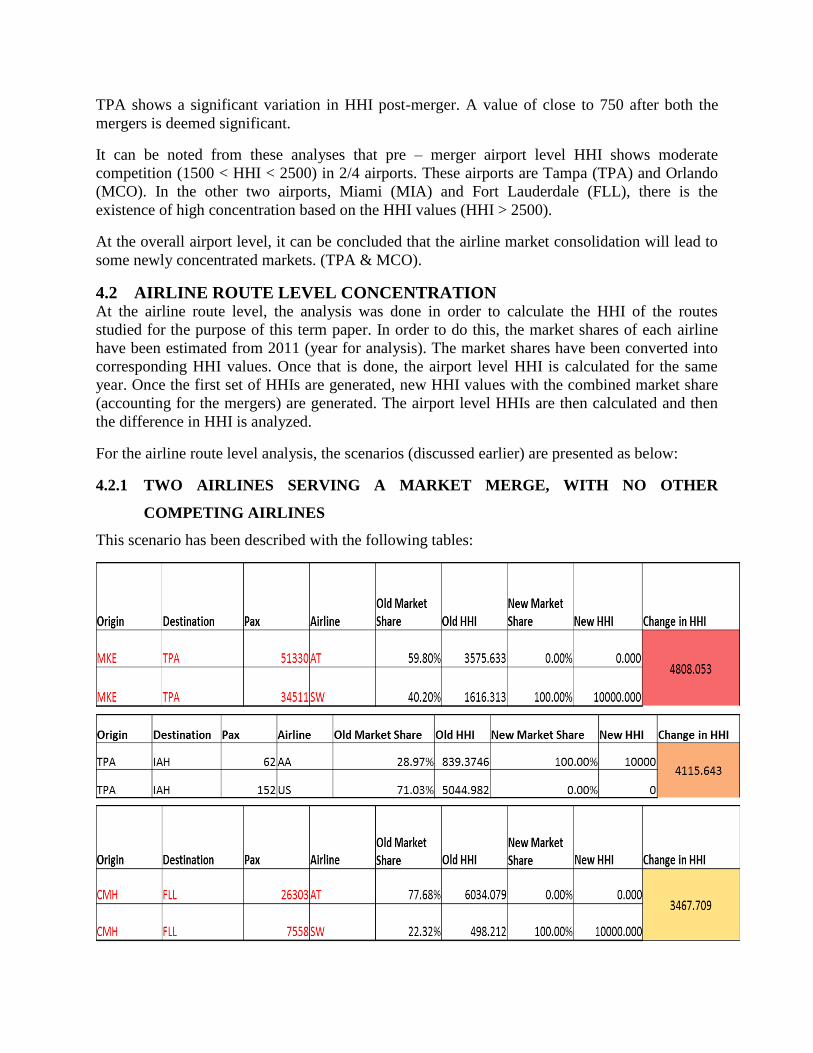

TPA shows a significant variation in HHI post-merger. A value of close to 750 after both the

mergers is deemed significant.

It can be noted from these analyses that pre – merger airport level HHI shows moderate

competition (1500 < HHI < 2500) in 2/4 airports. These airports are Tampa (TPA) and Orlando

(MCO). In the other two airports, Miami (MIA) and Fort Lauderdale (FLL), there is the

existence of high concentration based on the HHI values (HHI > 2500).

At the overall airport level, it can be concluded that the airline market consolidation will lead to

some newly concentrated markets. (TPA & MCO).

4.2 AIRLINE ROUTE LEVEL CONCENTRATION At the airline route level, the analysis was done in order to calculate the HHI of the routes

studied for the purpose of this term paper. In order to do this, the market shares of each airline

have been estimated from 2011 (year for analysis). The market shares have been converted into

corresponding HHI values. Once that is done, the airport level HHI is calculated for the same

year. Once the first set of HHIs are generated, new HHI values with the combined market share

(accounting for the mergers) are generated. The airport level HHIs are then calculated and then

the difference in HHI is analyzed.

For the airline route level analysis, the scenarios (discussed earlier) are presented as below:

4.2.1 TWO AIRLINES SERVING A MARKET MERGE, WITH NO OTHER

COMPETING AIRLINES

This scenario has been described with the following tables:

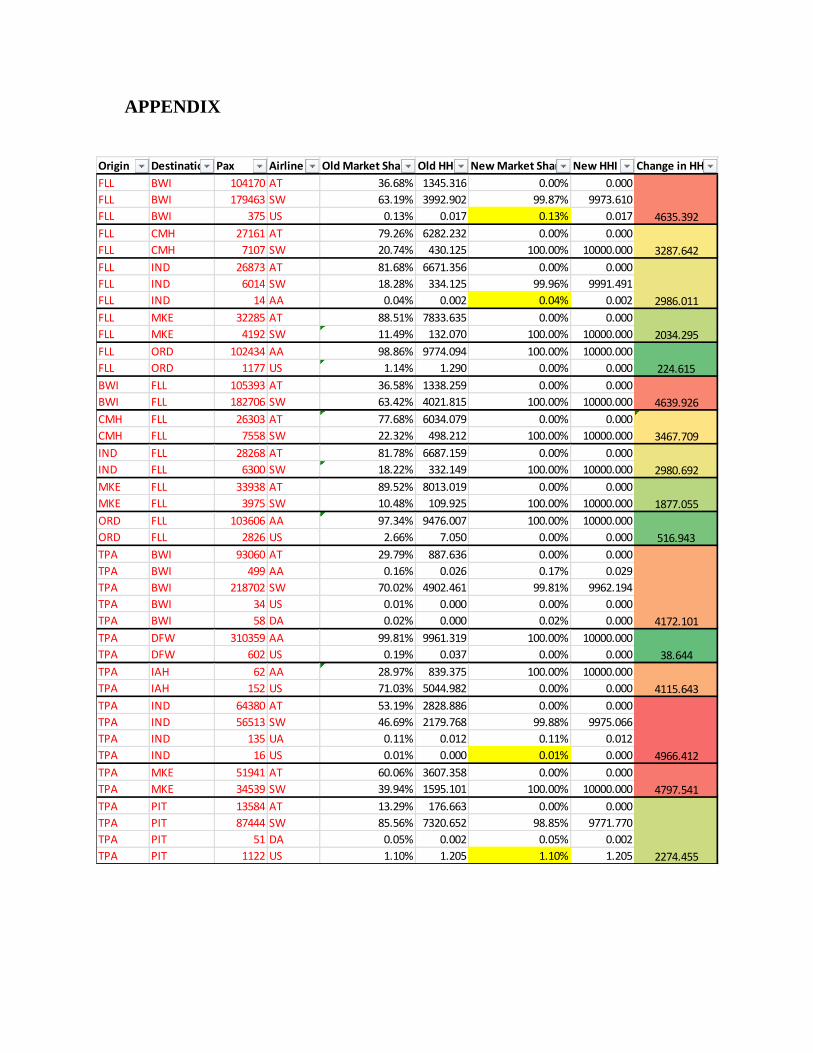

FIGURE 1 – HHI INDEX ON ROUTES WITH ONLY TWO MERGING AIRLINES OPERATING

As can be seen, the change in HHI in these select route pairs shows various levels of impacts of

the proposed merger. As can be seen, the proposed merger can be “presumptively illegal” (all

else remaining the same) if the HHI is above 2500. But in some of these cases, the proposed

change in HHI is in the tune of 4000s.

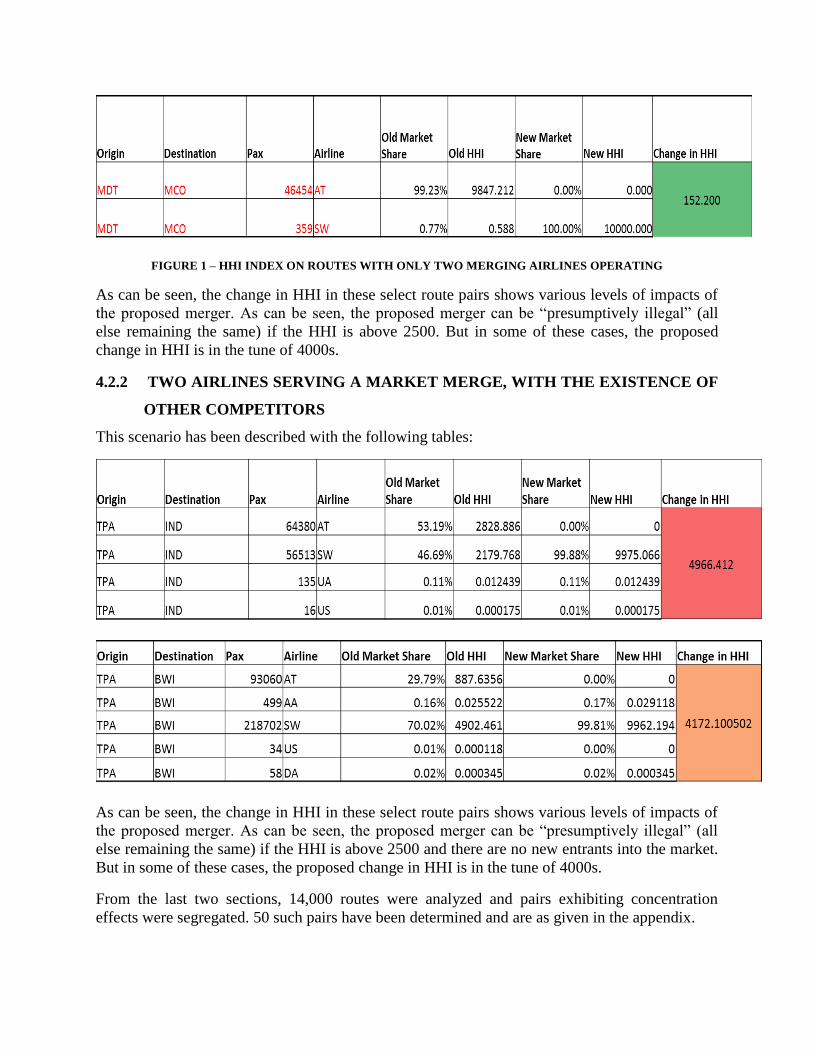

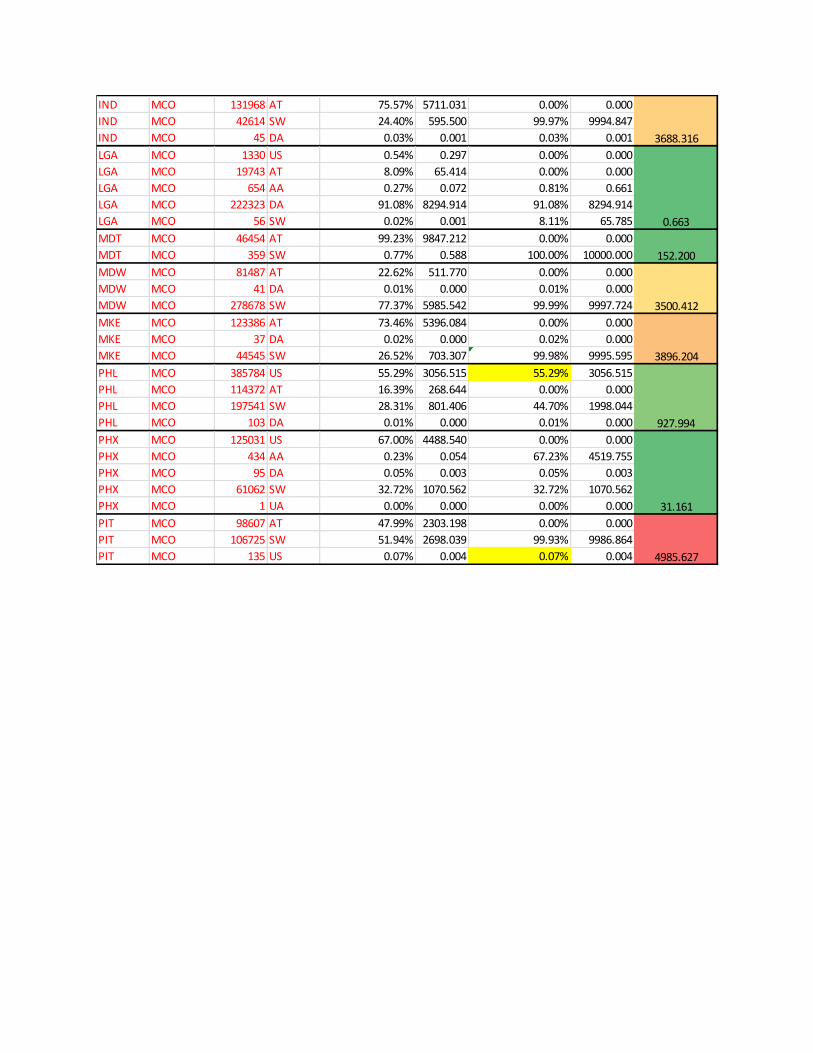

4.2.2 TWO AIRLINES SERVING A MARKET MERGE, WITH THE EXISTENCE OF

OTHER COMPETITORS

This scenario has been described with the following tables:

As can be seen, the change in HHI in these select route pairs shows various levels of impacts of

the proposed merger. As can be seen, the proposed merger can be “presumptively illegal” (all

else remaining the same) if the HHI is above 2500 and there are no new entrants into the market.

But in some of these cases, the proposed change in HHI is in the tune of 4000s.

From the last two sections, 14,000 routes were analyzed and pairs exhibiting concentration

effects were segregated. 50 such pairs have been determined and are as given in the appendix.

FIGURE 2 - HHI INDEX ON ROUTES WITH MORE THAN THE TWO MERGING AIRLINES OPERATING

5 CONCLUSION

The main objective of assessing the market concentration at the airport and airline route level has

been done and the following conclusions can be summarized:

i. At the overall airport level, it can be concluded that the airline market consolidation will

lead to some newly concentrated markets. (TPA & MCO).

ii. 50 routes of 14,000 (0.357 %) routes were found to have concentration effects as a

consequence of the market consolidation.

iii. Out of these 50 routes, 29 (58%) have a HHI > 2500 which means that across these

routes, the merger is “presumptively illegal”.

iv. Airline mergers, if they increase, market concentration levels experienced by the

passengers, should be discouraged by the Department of Justice (DoJ).

6 FUTURE WORK

As part of the future work on this regard, there is a lot that could be done to enrich the research.

i. The analysis of post – merger HHI across years (with the 2012 data) to ascertain the

change in market concentration patterns (if any).

ii. Expansion from the four major airports in Florida to the rest of the airports in the state as

well. As has been discussed earlier, smaller airports have higher chances of concentration

post – merger.

iii. Expansion from single airport pair levels to city levels, encompassing all airports around

a city instead of analyzing flows from that particular airport.

7 REFERENCES

1. Schabas, M (2014). Have Airline Mergers in the United States Reduced Domestic Market

Concentration? Transportation Research Board 2014. Washington DC.

2. US Airways – American Airlines Complaint http://www.scribd.com/doc/159988211/US-

Airways-American-Airlines-Complaint

3. HHI Analysis – an Indicator of Monopoly or Fragmented Industry

http://www.danielihliu.com/blog/2012/04/03/79/

4. Bilotkach, V. Multimarket Contact and Intensity of Competition: Evidence from an Airline

Merger. Review of Industrial Organisation, 2011.

5. The Points Guy (2013). Past and Future Airline Mergers: A Brief History and

Predictions http://thepointsguy.com/2013/02/past-and-future-airline-mergers-a-brief-

history-and-predictions/

6. Airlines for America. US Airlines Mergers and Acquisitions

http://www.airlines.org/Pages/U.S.-Airline-Mergers-and-Acquisitions.aspx

7. Brumbaugh Wealth Management. Big Birds: The Potential Effects of Airline

Consolidation http://www.brumbaughwealth.com/HOT-TOPIC-Airline-

Consolidation.c4784.htm

8. Huschelrath, K., and K. Muller. Market Power, Efficiencies, and Entry - Evidence from an

Airline Merger. Undated.

APPENDIX

Origin Destination Pax Airline Old Market Share Old HHI New Market Share New HHI Change in HHI

FLL BWI 104170 AT 36.68% 1345.316 0.00% 0.000

FLL BWI 179463 SW 63.19% 3992.902 99.87% 9973.610

FLL BWI 375 US 0.13% 0.017 0.13% 0.017

FLL CMH 27161 AT 79.26% 6282.232 0.00% 0.000

FLL CMH 7107 SW 20.74% 430.125 100.00% 10000.000

FLL IND 26873 AT 81.68% 6671.356 0.00% 0.000

FLL IND 6014 SW 18.28% 334.125 99.96% 9991.491

FLL IND 14 AA 0.04% 0.002 0.04% 0.002

FLL MKE 32285 AT 88.51% 7833.635 0.00% 0.000

FLL MKE 4192 SW 11.49% 132.070 100.00% 10000.000

FLL ORD 102434 AA 98.86% 9774.094 100.00% 10000.000

FLL ORD 1177 US 1.14% 1.290 0.00% 0.000

BWI FLL 105393 AT 36.58% 1338.259 0.00% 0.000

BWI FLL 182706 SW 63.42% 4021.815 100.00% 10000.000

CMH FLL 26303 AT 77.68% 6034.079 0.00% 0.000

CMH FLL 7558 SW 22.32% 498.212 100.00% 10000.000

IND FLL 28268 AT 81.78% 6687.159 0.00% 0.000

IND FLL 6300 SW 18.22% 332.149 100.00% 10000.000

MKE FLL 33938 AT 89.52% 8013.019 0.00% 0.000

MKE FLL 3975 SW 10.48% 109.925 100.00% 10000.000

ORD FLL 103606 AA 97.34% 9476.007 100.00% 10000.000

ORD FLL 2826 US 2.66% 7.050 0.00% 0.000

TPA BWI 93060 AT 29.79% 887.636 0.00% 0.000

TPA BWI 499 AA 0.16% 0.026 0.17% 0.029

TPA BWI 218702 SW 70.02% 4902.461 99.81% 9962.194

TPA BWI 34 US 0.01% 0.000 0.00% 0.000

TPA BWI 58 DA 0.02% 0.000 0.02% 0.000

TPA DFW 310359 AA 99.81% 9961.319 100.00% 10000.000

TPA DFW 602 US 0.19% 0.037 0.00% 0.000

TPA IAH 62 AA 28.97% 839.375 100.00% 10000.000

TPA IAH 152 US 71.03% 5044.982 0.00% 0.000

TPA IND 64380 AT 53.19% 2828.886 0.00% 0.000

TPA IND 56513 SW 46.69% 2179.768 99.88% 9975.066

TPA IND 135 UA 0.11% 0.012 0.11% 0.012

TPA IND 16 US 0.01% 0.000 0.01% 0.000

TPA MKE 51941 AT 60.06% 3607.358 0.00% 0.000

TPA MKE 34539 SW 39.94% 1595.101 100.00% 10000.000

TPA PIT 13584 AT 13.29% 176.663 0.00% 0.000

TPA PIT 87444 SW 85.56% 7320.652 98.85% 9771.770

TPA PIT 51 DA 0.05% 0.002 0.05% 0.002

TPA PIT 1122 US 1.10% 1.205 1.10% 1.205

4639.926

4635.392

3287.642

2986.011

2034.295

224.615

3467.709

2980.692

1877.055

516.943

4172.101

38.644

4115.643

4966.412

4797.541

2274.455

BWI TPA 210988 SW 69.01% 4763.047 99.85% 9969.994

BWI TPA 94267 AT 30.84% 950.799 0.00% 0.000

BWI TPA 103 DA 0.03% 0.001 0.03% 0.001

BWI TPA 356 US 0.12% 0.014 0.12% 0.014

DFW TPA 302921 AA 99.94% 9987.929 100.00% 10000.000

DFW TPA 183 US 0.06% 0.004 0.00% 0.000

IND TPA 56246 SW 46.51% 2163.006 99.89% 9979.009

IND TPA 64565 AT 53.39% 2850.157 0.00% 0.000

IND TPA 127 US 0.11% 0.011 0.11% 0.011

MKE TPA 51330 AT 59.80% 3575.633 0.00% 0.000

MKE TPA 34511 SW 40.20% 1616.313 100.00% 10000.000

PIT TPA 90066 SW 86.23% 7435.409 99.17% 9835.056

PIT TPA 13519 AT 12.94% 167.522 0.00% 0.000

PIT TPA 18 UA 0.02% 0.000 0.02% 0.000

PIT TPA 847 US 0.81% 0.658 0.81% 0.658

MIA PHL 122056 US 49.44% 2444.552 0.00% 0.000

MIA PHL 124686 AA 50.51% 2551.035 99.95% 9990.038

MIA PHL 123 DA 0.05% 0.002 0.05% 0.002

PHL MIA 125911 US 50.82% 2582.334 0.00% 0.000

PHL MIA 121519 AA 49.04% 2405.323 99.86% 9972.172

PHL MIA 345 DA 0.14% 0.019 0.14% 0.019

MCO BOS 48536 AT 34.27% 1174.205 0.00% 0.000

MCO BOS 740 AA 0.52% 0.273 0.53% 0.277

MCO BOS 90718 DA 64.05% 4102.068 64.05% 4102.068

MCO BOS 1642 SW 1.16% 1.344 35.43% 1254.997

MCO BOS 6 US 0.00% 0.000 0.00% 0.000

MCO BUF 35877 AT 23.25% 540.616 0.00% 0.000

MCO BUF 116173 SW 75.29% 5668.489 98.54% 9710.235

MCO BUF 2242 US 1.45% 2.111 1.45% 2.111

MCO BUF 10 UA 0.01% 0.000 0.01% 0.000

MCO BWI 169800 AT 36.46% 1329.639 0.00% 0.000

MCO BWI 295485 SW 63.45% 4026.515 99.92% 9983.815

MCO BWI 6 UA 0.00% 0.000 0.00% 0.000

MCO BWI 371 US 0.08% 0.006 0.08% 0.006

MCO CMH 109426 SW 74.30% 5520.258 100.00% 10000.000

MCO CMH 37853 AT 25.70% 660.570 0.00% 0.000

MCO DTW 4304 SW 0.89% 0.785 15.45% 238.753

MCO DTW 70750 AT 14.57% 212.155 0.00% 0.000

MCO DTW 410681 DA 84.55% 7148.426 84.55% 7148.426

MCO IND 130632 AT 76.26% 5816.144 0.00% 0.000

MCO IND 40570 SW 23.68% 560.978 99.95% 9989.728

MCO IND 88 DA 0.05% 0.003 0.05% 0.003

MCO LGA 19054 AT 8.35% 69.781 0.00% 0.000

MCO LGA 489 SW 0.21% 0.046 8.57% 73.409

MCO LGA 545 AA 0.24% 0.057 1.15% 1.315

MCO LGA 205937 DA 90.29% 8151.423 90.29% 8151.423

MCO LGA 2071 US 0.91% 0.824 0.00% 0.000

MCO MDT 44494 AT 99.20% 9840.562 0.00% 0.000

MCO MDT 359 SW 0.80% 0.641 100.00% 10000.000

12.068

4256.149

4.016

4965.846

4808.053

2232.125

4994.451

4984.515

79.452

3501.130

4627.661

3819.172

25.812

3612.606

158.797

MCO MDW 281461 SW 77.13% 5948.374 100.00% 10000.000

MCO MDW 83477 AT 22.87% 523.233 0.00% 0.000

MCO MKE 11577 AT 19.72% 388.930 0.00% 0.000

MCO MKE 47126 SW 80.28% 6444.668 100.00% 10000.000

MCO PHL 115803 AT 16.51% 272.653 0.00% 0.000

MCO PHL 200235 SW 28.55% 815.176 45.06% 2030.719

MCO PHL 385070 US 54.91% 3014.745 54.91% 3014.745

MCO PHL 209 DA 0.03% 0.001 0.03% 0.001

MCO PHX 169 DA 0.09% 0.009 0.09% 0.009

MCO PHX 176 AA 0.10% 0.009 66.91% 4476.467

MCO PHX 59824 SW 32.65% 1065.699 32.65% 1065.699

MCO PHX 653 UA 0.36% 0.127 0.36% 0.127

MCO PHX 122434 US 66.81% 4463.625 0.00% 0.000

MCO PIT 97931 AT 47.98% 2302.260 0.00% 0.000

MCO PIT 105273 SW 51.58% 2660.406 99.56% 9912.393

MCO PIT 896 US 0.44% 0.193 0.44% 0.193

MCO SAN 285 AA 3.90% 15.171 44.03% 1939.032

MCO SAN 4005 SW 54.74% 2995.980 54.74% 2995.980

MCO SAN 90 UA 1.23% 1.513 1.23% 1.513

MCO SAN 2937 US 40.14% 1611.172 0.00% 0.000

BOS MCO 9 US 0.01% 0.000 0.00% 0.000

BOS MCO 50563 AT 35.33% 1247.988 0.00% 0.000

BOS MCO 1109 AA 0.77% 0.600 0.78% 0.610

BOS MCO 90144 DA 62.98% 3966.600 62.98% 3966.600

BOS MCO 1304 SW 0.91% 0.830 36.24% 1313.188

BUF MCO 122991 SW 77.73% 6041.303 99.94% 9988.881

BUF MCO 35158 AT 22.22% 493.665 0.00% 0.000

BUF MCO 12 US 0.01% 0.000 0.01% 0.000

BUF MCO 76 UA 0.05% 0.002 0.05% 0.002

BWI MCO 169 US 0.04% 0.001 0.04% 0.001

BWI MCO 168071 AT 35.52% 1261.990 0.00% 0.000

BWI MCO 304873 SW 64.44% 4152.486 99.96% 9992.857

CMH MCO 37398 AT 24.64% 607.350 0.00% 0.000

CMH MCO 114335 SW 75.34% 5676.766 99.99% 9997.760

CMH MCO 17 UA 0.01% 0.000 0.01% 0.000

DTW MCO 70181 AT 14.43% 208.328 0.00% 0.000

DTW MCO 411753 DA 84.68% 7171.023 84.68% 7171.023

DTW MCO 4288 SW 0.88% 0.778 15.32% 234.563

DTW MCO 13 UA 0.00% 0.000 0.00% 0.000 25.457

3528.392

3166.402

942.890

12.833

4949.726

312.689

64.380

3453.913

4578.382

3713.643

IND MCO 131968 AT 75.57% 5711.031 0.00% 0.000

IND MCO 42614 SW 24.40% 595.500 99.97% 9994.847

IND MCO 45 DA 0.03% 0.001 0.03% 0.001

LGA MCO 1330 US 0.54% 0.297 0.00% 0.000

LGA MCO 19743 AT 8.09% 65.414 0.00% 0.000

LGA MCO 654 AA 0.27% 0.072 0.81% 0.661

LGA MCO 222323 DA 91.08% 8294.914 91.08% 8294.914

LGA MCO 56 SW 0.02% 0.001 8.11% 65.785

MDT MCO 46454 AT 99.23% 9847.212 0.00% 0.000

MDT MCO 359 SW 0.77% 0.588 100.00% 10000.000

MDW MCO 81487 AT 22.62% 511.770 0.00% 0.000

MDW MCO 41 DA 0.01% 0.000 0.01% 0.000

MDW MCO 278678 SW 77.37% 5985.542 99.99% 9997.724

MKE MCO 123386 AT 73.46% 5396.084 0.00% 0.000

MKE MCO 37 DA 0.02% 0.000 0.02% 0.000

MKE MCO 44545 SW 26.52% 703.307 99.98% 9995.595

PHL MCO 385784 US 55.29% 3056.515 55.29% 3056.515

PHL MCO 114372 AT 16.39% 268.644 0.00% 0.000

PHL MCO 197541 SW 28.31% 801.406 44.70% 1998.044

PHL MCO 103 DA 0.01% 0.000 0.01% 0.000

PHX MCO 125031 US 67.00% 4488.540 0.00% 0.000

PHX MCO 434 AA 0.23% 0.054 67.23% 4519.755

PHX MCO 95 DA 0.05% 0.003 0.05% 0.003

PHX MCO 61062 SW 32.72% 1070.562 32.72% 1070.562

PHX MCO 1 UA 0.00% 0.000 0.00% 0.000

PIT MCO 98607 AT 47.99% 2303.198 0.00% 0.000

PIT MCO 106725 SW 51.94% 2698.039 99.93% 9986.864

PIT MCO 135 US 0.07% 0.004 0.07% 0.004

31.161

4985.627

3688.316

0.663

152.200

3500.412

3896.204

927.994