ifrs news - grantthornton.cn ifrs news q3 2011.pdf · fair value hierarchy when measuring fair...

TRANSCRIPT

Quarter 3 2011

Our third edition of 2011 starts with alook at several important new Standardsthat have been issued since our lastquarterly edition. These include IFRS 13‘Fair Value Measurement’, a revisedversion of IAS 19 ‘Employee Benefits’and the new Standards on consolidations(which have already been featured in aspecial edition of IFRS News).

We go on to consider other items in the IASB’s pipeline including thereopening of the debates on revenuerecognition and the effective date of IFRS 9. We then turn to IFRS-relatednews at Grant Thornton, as well as amore general round-up of activitiesaffecting the IASB. We end with anoverview of the proposals that the IASBcurrently has out for comment, and theimplementation dates of newer Standardsthat are not yet mandatory.

Welcome to IFRS News – a quarterly update from the Grant ThorntonInternational IFRS team.IFRS News offers asummary of the moresignificant developments in International FinancialReporting Standards (IFRS) along with insightsinto topical issues andcomments and views from the Grant ThorntonInternational IFRS team.

IFRS News

2 IFRS News Quarter 3 2011

IFRS 13 Fair Value Measurement

New Standard provides guidance onhow to measure fair values for alltypes of items

The IASB has published IFRS 13 ‘FairValue Measurement’. The Standardexplains how to measure fair value forfinancial reporting and introducessignificantly enhanced disclosures aboutfair values. It does not address or changethe requirements on when fair valuesshould be used.

IFRS 13 has been issued in order toprovide a single source of guidance forall fair value measurements and to clarifythe definition of fair value. Prior to itspublication, the guidance on fair valuewas distributed across many IFRSs, withsome containing quite limited guidancewhile others contained extensiveguidance that was not always consistent.The global financial crisis highlighted theneed to improve the transparency ofhow fair value is measured and also howfair value should be measured when themarket for an asset or liability becomesless active. While the measurementprinciples will be unchanged in manysituations, there will be individualscenarios where the effects of IFRS 13could be significant.

New definition of fair valueIFRS 13 defines fair value as the pricethat would be received to sell an asset orpaid to transfer a liability in an orderlytransaction between market participantsat the measurement date (ie an exitprice).

The Standard clarifies that fair valueis based on a transaction taking place inthe principal market for the asset orliability or, in the absence of a principalmarket, the most advantageous market.The principal market is the market withthe greatest volume and level of activityfor the asset or liability. The applicablemarket should in either case be one towhich the entity has access however. Forinstance, in valuing a derivative a bankthat trades in such instruments mightlook to the dealer (inter-bank) market,whereas a commercial entity is unlikelyto have access to that market.

Practical insight: IFRS 13 addresses almost all fair value and ‘fair value-based’ measurements –including those for both financial and non-financial items. Fair values that arerequired to be disclosed in the notes are also captured.

Practical insight: Using an exit price definition of fair value has the benefit of removing entity-specificfactors that might exist in an entry price. It will however have implications for someentities, in particular those that acquire assets (or incur liabilities in one market) andsell or transfer them in another. Similarly, a transaction price or entry price may notnecessarily represent fair value where related parties are involved or a transactiontakes place under duress.

IFRS News Quarter 3 2011 3

For liabilities, the Standard providesextensive guidance to deal with theproblematic issue of measuring the fairvalue of a liability in the absence of aquoted price in an active market totransfer an identical liability. Forliabilities with a corresponding asset(such as loans payable), fair value ismeasured from the perspective of theasset holder. Accordingly, the credit riskof the borrower is implicitly taken intoaccount. Guidance is also given formeasuring fair value and addressingvaluation uncertainty in markets that areno longer active.

Fair value hierarchyWhen measuring fair value, an entity isrequired to use valuation techniques thatmaximise the use of relevant observableinputs and minimise the use ofunobservable inputs. IFRS 13 establishesa fair value hierarchy for doing this,which is set out below:• Level 1: Quoted prices (ie

unadjusted prices) in active marketsfor identical assets or liabilities thatthe entity can access at themeasurement date

• Level 2: Inputs other than quotedprices included within Level 1 thatare observable for the asset orliability, either directly or indirectly

• Level 3: Unobservable inputs for theasset or liability.

Significant differences in disclosurerequirements apply to each level withinthe hierarchy to provide users withinsight into the reliability of the fairvalue measurement (IFRS 13’sdisclosures do not however apply to fairvalues that arise only on initialrecognition – such as fair valuesdetermined for acquisition accountingunder IFRS 3).

These disclosures could be achallenge for some entities. For example,real estate valuations may end up beingclassified in Level 3 of the hierarchywhere the valuation takes place in aninactive or less transparent real estatemarket, leading to extensive disclosuresas to how the valuation has beenproduced.

ConvergenceThe US Financial Accounting StandardsBoard has also issued updated guidanceon fair value measurement. As a result,the IFRS and US GAAP requirementson fair value measurement are nowlargely identical.

Effective dateThe IFRS is to be applied for annualperiods beginning on or after 1 January2013. Earlier application is permitted.The new disclosure requirements areonly required for periods beginning afterIFRS 13 is adopted, ie comparativedisclosures for prior periods are notrequired.

Practical insight:IFRS 13 helpfully presumes that the principal market is the market in which an entitynormally enters into transactions for the asset or liability unless there is evidencethat another market has a greater volume and level of activity. Such a situationcould for example occur where an entity has measured fair value based on its localmarket but a deeper and more liquid market exists and the costs to access it(transport costs, etc) are not prohibitive. For a non-financial asset, IFRS 13 requires an entity to consider the highest and

best use of the asset. For example, in valuing land currently used for agriculturalpurposes an entity should consider alternative uses such as commercialdevelopment – but only if this is legally possible, financially feasible and there isevidence that a different use would maximise value to market participants. IFRS 13’s ‘exit value’ approach might suggest that some highly specialised

assets and items such as work-in progress would be valued on a scrap basis.However, the Standard avoids this outcome by requiring fair value to be measuredon the premise that market participants have access to the complementary assetsnecessary to maximise value where applicable. Entities employing outside valuation experts will need to ensure the valuations

provided are compliant with the requirements of IFRS 13.

Other issues covered in IFRS 13At over 100 pages in length, IFRS 13 is a comprehensive Standard containingdetailed guidance on many issues. Listed below are some of the important issuescovered in the Standard: • bid-ask spreads• the effect of restrictions on fair value measurement• transport costs where fair value is location-specific • blockage factors resulting from the size of an entity’s holding • liability valuation • the relationship between transaction prices and initial fair values.

IASB makes changes to accountingfor defined benefit plans

The IASB has issued an amendedversion of IAS 19 ‘Employee Benefits’which changes the way defined benefitplans are accounted for. Theamendments that have been made areintended to improve the recognition,presentation, and disclosure of definedbenefit plans. They do not address themeasurement of defined benefit planshowever.

the amendments eliminatethe ‘corridor’ method,under which it was possibleto defer gains or losses on a defined benefit plan

The changes made in the amendedversion of the Standard will result in: • immediate recognition of all

estimated changes in the cost ofproviding defined benefits and allchanges in the value of plan assets.The various methods which alloweddeferral of some of those gains orlosses under the previous version ofIAS 19, including the ‘corridor’method, have been eliminated

• a new presentation approach todistinguishing the different types ofgains and losses arising from definedbenefit plans. The table above setsout the changes in benefit costswhich are to be presented separatelyunder the new approach.

The effect of presenting these itemsseparately is to remove from IAS 19 theoption for entities to recognise in profitor loss all changes in defined benefitobligations and in the fair value of planassets.

One controversial change is thatpreparers will no longer be able toinclude the expected return on planassets in the profit and loss account. The return on plan assets will insteadrepresent interest, dividends and otherincome derived from the plan assets,together with realised and unrealisedgains or losses on the plan assets, lesscertain costs. The change means thatinstead of crediting the expected returnon pension plan assets separately andcharging the calculated interest cost onthe pension provision, the amendedstandard requires a charge or credit to becalculated by applying a AA rated bondinterest rate to the net pension deficit or surplus. This is likely to reduce thereported profit for many companies.

4 IFRS News Quarter 3 2011

Revised version of IAS 19 issued

Changes in benefit costs

Type of gain or loss Recognition

service cost in profit or loss

net interest on the net defined benefit liability or asset in profit or loss

remeasurement of the defined benefit liability or asset in other comprehensive income

IFRS News Quarter 3 2011 5

Amendments to IAS 1

The IASB has published amendments toIAS 1 ‘Presentation of FinancialStatements’. The main change is arequirement for entities to group itemspresented in other comprehensive income(OCI) on the basis of whether they are

potentially reclassifiable to profit or loss.The amendments also highlight theimportance that the IASB places onpresenting profit or loss and OCItogether and with equal prominence. Theamendments do not affect which items are

presented in OCI however, nor do theychange the rules on when OCI isreclassified.

SMEIG finalises its first guidance

Further to our article in last quarter’sedition of IFRS News, the SMEImplementation Group (SMEIG),responsible for assisting the IASB onmatters related to the implementation ofthe International Financial ReportingStandard for Small and Medium-sizedEntities (IFRS for SMEs), has publishedits first question and answer guidance onthe IFRS for SMEs.

Q&A 2011/01 addresses whether aparent entity that itself does not havepublic accountability may present itsseparate financial statements inaccordance with the IFRS for SMEs if it is part of a group that is required (orelects) to present consolidated financialstatements in accordance with fullIFRSs. The final guidance confirms thatif a parent entity does not have public

accountability, it may present its separatefinancial statements in accordance withthe IFRS for SMEs.

In addition to these changes, theamendments also introduce improveddisclosures relating to the followingareas: • the characteristics of the company’s

defined benefit plans • the amounts recognised in the

financial statements• risks arising from defined benefit

plans• participation in multi-employer

plans.

Comment:We support the elimination of the ‘corridor’ mechanism for smoothing the impact of actuarial gains or losses. We also support the recognition of service cost and finance cost in profit and

loss with the remeasurement components to be recognised in other comprehensiveincome (OCI). Having said this, our support is in the context of this being a short-term measure to improve the current Standard, as we currently see no clearconceptual basis to determine which gains and losses should be recognised in OCI rather than through profit or loss.

6 IFRS News Quarter 3 2011

New Standards on Consolidationpublished

As predicted in our last edition of IFRSNews, the IASB published the followingfive new Standards in May, dealing withgroup issues and off-balance sheet activity:• IFRS 10 ‘Consolidated Financial

Statements’• IFRS 11 ‘Joint Arrangements’• IFRS 12 ‘Disclosure of Interests in

Other Entities’• IAS 27 (Revised) ‘Separate Financial

Statements’• IAS 28 (Revised) ‘Investments in

Associates and Joint Ventures’.

We have published a special edition of IFRSNews which informs you about the newStandards and the implications they mayhave. The table opposite is reproduced fromthat special edition, and shows the mainpoints in the new Standards. If you havenot already received the special edition,please get in touch with your local IFRSrepresentative to request a copy.

Summary

Standard Significance

IFRS 10 Consolidated • supersedes IAS 27 ‘Consolidated and Separate Financial Statements’

Financial Statements and SIC-12 ‘Consolidation – Special Purpose Entities’

• changes the definition of control and applies it to all investees to

determine the scope of consolidation

• has the potential to affect the outcome of many borderline and

judgemental control assessments

• expected to lead to few changes for conventional group structures

based on majority share ownership

• where such a change does arise, however, the impact could be very

significant.

IFRS 11 Joint • supersedes IAS 31 ‘Interests in Joint Ventures’

Arrangements • eliminates the option of using proportionate consolidation for joint

ventures

• eliminates IAS 31’s ‘jointly controlled operations’ and ‘jointly controlled

assets’ categories

• most of the arrangements that would have been classified under those

categories will fall into the newly defined category ‘joint operation’.

IFRS 12 Disclosure of • combines the disclosure requirements for subsidiaries, joint

Interests in Other Entities arrangements, associates and structured entities within a

comprehensive disclosure standard

• provides more transparency on ‘borderline’ consolidation decisions

• enhances disclosures about unconsolidated structured entities in which

an investor or sponsor has involvement

• will help investors to assess the extent to which a reporting entity has

been involved in setting up special structures and the risks to which it is

exposed as a result.

IAS 27 (Revised) Separate • consequential changes arising from the publication of the new IFRSs

Financial Statements • IAS 27 will now solely address separate financial statements, the

requirements for which are substantially unchanged.

IAS 28 (Revised) • changes in scope arising from the publication of IFRS 11

Investments in Associates • continues to prescribe the mechanics of equity accounting.

and Joint Ventures

SMEIG publishes more draft guidance

The SME Implementation Group(SMEIG) has published for publiccomment three more question andanswer documents (Q&As) on the IFRSfor SMEs.

The new Q&As consider thefollowing issues:• whether a captive insurance

company is a publicly accountableentity, and whether a groupcontaining such an entity canproduce consolidated financialstatements in accordance with theIFRS for SMEs?

• how broadly should the phrase‘traded in a public market’ beinterpreted in the definition of publicaccountability? (eg does it includeover-the-counter markets?)

• in view of the Standard’s criterion thatan entity is publicly accountable if itholds assets in a fiduciary capacity fora broad group of outsiders, whetherinvestment funds that restrict theirownership to only a few participantsare not publicly accountable?

The SMEIG is responsible for assistingthe IASB on matters related to theimplementation of the IFRS for SMEs.Frank Timmins, a partner in our SouthAfrican member firm, represents GrantThornton on the Group.

IFRS News Quarter 3 2011 7

Comment:Take care not to overlook IFRS 12’s new disclosure requirements. Following the publication of the new consolidations Standards,most of the headlines have been given over to IFRS 10’s new definition of control and IFRS 11’s elimination of proportionateconsolidation. While these are very significant changes, they will not affect everyone. In contrast IFRS 12’s disclosurerequirements can be expected to have an effect on all entities. Some of the information required to meet the disclosure requirements will be new and its preparation will require planning.

One example is the requirement to provide summarised financial information about the assets, liabilities, profit or loss and cashflows of each subsidiary that has non-controlling interests that are material to the reporting entity. Another example is therequirement for an entity to disclose the nature of its interests in unconsolidated structured entities and the nature of the risks it is exposed to as a result. System modifications and enhancements may be required to address the change in guidance and to provide the necessary

information for the new disclosure requirements.

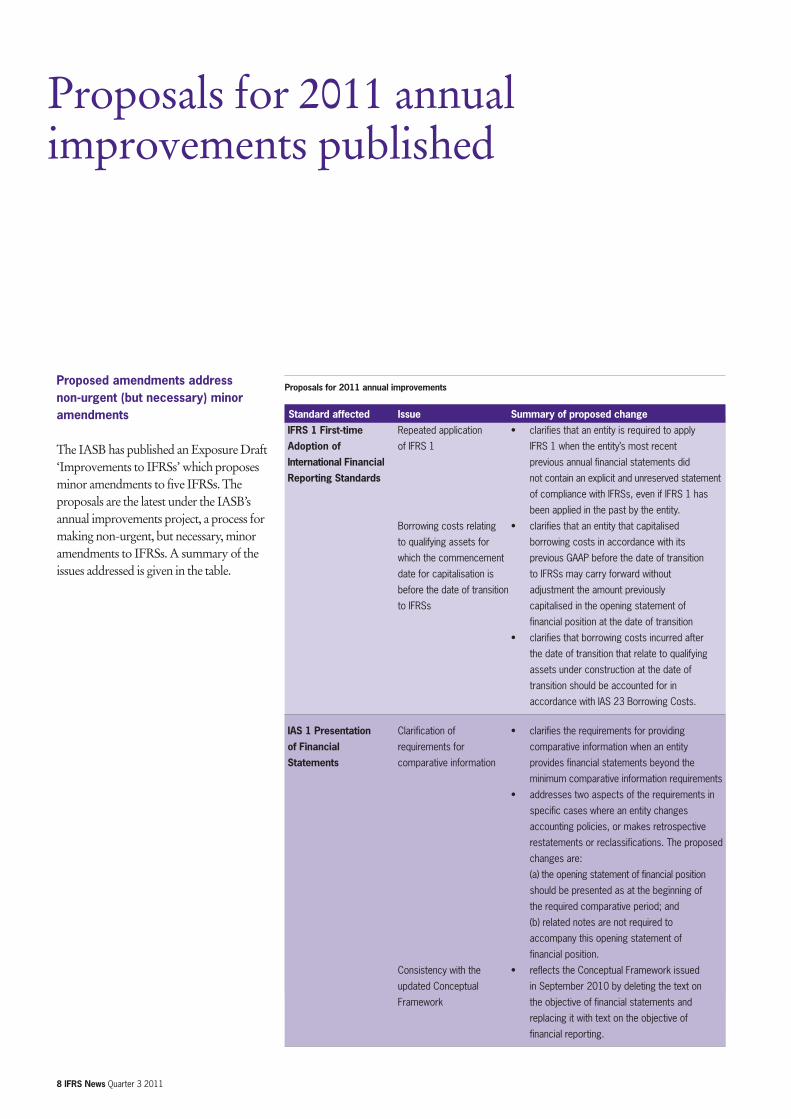

Proposals for 2011 annualimprovements published

Proposed amendments address non-urgent (but necessary) minoramendments

The IASB has published an Exposure Draft‘Improvements to IFRSs’ which proposesminor amendments to five IFRSs. Theproposals are the latest under the IASB’sannual improvements project, a process formaking non-urgent, but necessary, minoramendments to IFRSs. A summary of theissues addressed is given in the table.

Proposals for 2011 annual improvements

Standard affected Issue Summary of proposed change

IFRS 1 First-time Repeated application • clarifies that an entity is required to apply

Adoption of of IFRS 1 IFRS 1 when the entity’s most recent

International Financial previous annual financial statements did

Reporting Standards not contain an explicit and unreserved statement

of compliance with IFRSs, even if IFRS 1 has

been applied in the past by the entity.

Borrowing costs relating • clarifies that an entity that capitalised

to qualifying assets for borrowing costs in accordance with its

which the commencement previous GAAP before the date of transition

date for capitalisation is to IFRSs may carry forward without

before the date of transition adjustment the amount previously

to IFRSs capitalised in the opening statement of

financial position at the date of transition

• clarifies that borrowing costs incurred after

the date of transition that relate to qualifying

assets under construction at the date of

transition should be accounted for in

accordance with IAS 23 Borrowing Costs.

IAS 1 Presentation Clarification of • clarifies the requirements for providing

of Financial requirements for comparative information when an entity

Statements comparative information provides financial statements beyond the

minimum comparative information requirements

• addresses two aspects of the requirements in

specific cases where an entity changes

accounting policies, or makes retrospective

restatements or reclassifications. The proposed

changes are:

(a) the opening statement of financial position

should be presented as at the beginning of

the required comparative period; and

(b) related notes are not required to

accompany this opening statement of

financial position.

Consistency with the • reflects the Conceptual Framework issued

updated Conceptual in September 2010 by deleting the text on

Framework the objective of financial statements and

replacing it with text on the objective of

financial reporting.

8 IFRS News Quarter 3 2011

Proposals for 2011 annual improvements

Standard affected Issue Summary of proposed change

IAS 16 Property, Classification of servicing • clarifies that servicing equipment should be

Plant and Equipment equipment classified as property, plant and equipment

when it is used during more than one period

and as inventory otherwise.

IAS 32 Financial Income tax consequences • amends IAS 32 to clarify that income tax

Instruments: of distributions to holders relating to distributions to holders of an equity

Presentation of an equity instrument, instrument and income tax relating to

and of transaction costs transaction costs of an equity transaction should

of an equity transaction be accounted for in accordance with IAS 12

‘Income Taxes’.

IAS 34 Interim Interim financial reporting • clarifies the requirements in IAS 34 relating to

Financial Reporting and segment information segment information for total assets for each

for total assets reportable segment in order to enhance

consistency with the requirements in IFRS 8

‘Operating Segments’.

Proposed effective dateThe proposed effective date for theamendments is annual periods beginning onor after 1 January 2013. Earlier applicationwould be permitted.

IASB to re-expose revenuerecognition proposals

The IASB and the US FinancialAccounting Standards Board (FASB)have agreed to re-expose their revisedproposals for a common revenuerecognition standard.

The Boards had originally intendedto publish a final Standard by the end of June 2011. Given the importance ofthe revenue number to all companieshowever, they decided that it wasimportant to give interested parties the

opportunity to comment on the changesto the Board’s thinking since the June2010 exposure draft was published. Anew exposure draft is now planned forthe third quarter of 2011. It is expectedto have a comment period of 120 days.

Investment entities

Following the release of the new IFRSson Consolidation (see page 6 and ourSpecial Edition of IFRS News), theIASB is planning to issue an exposuredraft dealing with investment entities.

The objective of the project is toidentify particular types of investmententity that will be exempt from thegeneral requirement to consolidateentities that they control. Instead such

an entity would measure its investmentsat fair value, with changes in fair valuerecognised in profit or loss.

The IASB expects to issue theexposure draft in the current quarter.

IFRS News Quarter 3 2011 9

10 IFRS News Quarter 3 2011

Raymond Chabot Grant Thornton, oneof our Canadian member firms, has beenworking hard auditing the IFRStransition adjustments of its larger publiccompany clients and reviewing their firstquarterly financial statements underIFRS. Even though many clients havebeen preparing for transition for up totwo years, many issues were still onlyfinally resolved in the spring of 2011.Furthermore, the interim reports forsome clients expanded to up to 70 or sopages, which significantly increased thetime needed for preparation, for reviewby the firm and review by the auditcommittee.

the most significant changehas been in the area ofaccounting for definedbenefit plans

The most significant change forCanadian companies has been in the areaof accounting for defined benefit plans,where previously large deficits weredisclosed only in the notes, and wherecumulative actuarial losses had appearedcounter-intuitively as assets on thebalance sheet.

IFRS 1 ‘First-time Adoption ofInternational Financial ReportingStandards’ allows first-time adopters towrite-off any unamortised actuarialgains or losses at the time of transition.Since the performance of the stockexchange over the past few years hasbeen somewhat unfavourable, manyCanadian companies had largecumulative actuarial losses at thetransition date. The transition exemptionhas therefore allowed them to reset theirfinancial situation and remove largeamounts of future amortisation costs.IAS 19 furthermore allows companies tochoose a policy of recognising annualactuarial gains or losses in othercomprehensive income in the year thatthey arise, rather than recognising only a portion of these losses or gains basedon the corridor method. This changesimplifies the notes and improves thepresentation in the statement of financialposition for companies using it. It doeshave the drawback of increasingvolatility however.

A successful transition to IFRS in Canada

Canadian model IFRS financial statements for mining and explorationcompaniesRaymond Chabot Grant Thornton issued model financial statements for miningexploration companies in early 2011 which were very helpful to both clients andstaff. As clients have filed their actual financial statements, the firm has worked tofurther improve the model financial statements. This is another example of how thefirm is working to ensure a smooth and successful move to IFRS for its clients.

IFRS News Quarter 3 2011 11

After the larger companies had filedtheir first IFRS financial statements, thefirm had to regroup and prepare for thesmaller companies, including the mining exploration companies. Smaller miningcompanies have provided the firm with a unique challenge. Just because they are small does not mean that they are not complex. Like other Canadianaccounting firms, Raymond ChabotGrant Thornton have found that theyface a number of issues that are notnecessarily addressed clearly by IFRS.

As a result, our Canadian memberfirms have worked alongside the CanadianInstitute of Chartered Accountants(CICA), the Prospectors and DevelopersAssociation of Canada and the other largeaccounting firms, to develop a number ofdocuments providing non-authoritativeguidance on mining related issues (thedocuments produced by the workinggroup can be found on the CICA websiteat http://www.cica.ca/ifrs/ifrs-transition-resources/index.aspx). John Cochrane,delegate partner at Raymond Chabot

Grant Thornton and IFRS champion, isthe Canadian member firms’representative on this group. He issupported by Raymond Chabot GrantThornton’s accounting research team and a number of practitioners.

IASB discusses the mandatoryeffective date of IFRS 9

The IASB is considering delaying theeffective date of IFRS 9. Followingdelays in the completion of the differentphases to replace IAS 39, the IASB staffhave prepared a paper for the Board’sJuly meeting which addresses whetherthe Board should amend the mandatoryeffective date of IFRS 9 and, if so, whatthe effective date should be. The papercontains two possible alternatives. Theseare to:• retain the mandatory effective date

currently in the Standard (annualperiods beginning on or after 1 January 2013); or

• change the mandatory effective dateto annual periods beginning on orafter 1 January 2015.

Many external commentators havecommented that having a single effectivedate for all phases of the project toreplace IAS 39 (and also for the IASB’sprojects on insurance contracts, revenuerecognition and leases) would be themost cost-effective option. .

Regardless of which alternative theBoard decides upon, it will still bepossible for entities to early adopt IFRS 9 if they so wish.

12 IFRS News Quarter 3 2011

The US Securities and ExchangeCommission (SEC) has issued a StaffPaper exploring a possible method ofincorporation of IFRS into the financial system for US issuers.

The incorporation methodconsidered has been colloquially referredto as ‘Condorsement’, in that itcombines elements of both aconvergence approach to theincorporation of IFRS into USaccounting standards and anendorsement approach, such as that used in Europe. Under this approach: • US GAAP would be retained, but

the US Financial AccountingStandards Board (“FASB”) wouldincorporate IFRS into US GAAPover a defined period of time

• this would involve a transitionalperiod during which existingdifferences between IFRS and USGAAP would be eliminated throughongoing FASB standard-settingefforts

• during this period there would be afocus on minimizing transition costs,particularly for smaller issuers

• newly issued or amended IFRSswould be incorporated into USGAAP pursuant to an establishedendorsement protocol which wouldgive FASB or the SEC the ability tomodify or supplement IFRS when inthe public interest.

The idea of introducing an endorsementprotocol would necessitate a move awayfrom the FASB’s current standard-setting role and responsibilities. Mostsignificantly, the FASB would participatein the process for developing IFRS,rather than serving as the principal bodyresponsible for developing newaccounting standards or modifyingexisting standards under US GAAP.

‘Condorsement’ combineselements of both aconvergence approach andan endorsement approach

Feedback on the potential approachare requested in the Staff Paper by 31 July. The Staff Paper also notes thatthe approach set out in it represents justone possible approach to incorporationof IFRS and that several otherapproaches exist.

US explores ‘condorsement’ approachto adoption of IFRS

IFRS News Quarter 3 2011 13

Implications of leasing proposals for the Real Estate industry Grant Thornton International’s RealEstate and Construction group has issueda thought leadership piece called‘Preparing for global lease accountingstandards’.

The report examines the status of thejoint IASB and US Financial AccountingStandards Board proposals on leaseaccounting standards and offers real estateexecutives’ perceptions – from Australia,Canada, India, the United Kingdom andthe United States – on their potentialimpact.

To obtain a copy of the report, pleaseget in touch with your local IFRS contact.

Grant Thornton Japan publishesIFRS bookGrant Thornton Japan has published abook to provide Japanese companieswith guidance on how to apply IFRS.The book, which is available in Japanesebookstores, explains the requirements ofthe individual Standards, how they differfrom Japanese GAAP, and practicalpoints to consider in implementingthem.

Spotlight on our IFRS InterpretationsGroupGrant Thornton International’s IFRSInterpretations Group (IIG) consists of arepresentative from each of our memberfirms in the United States, Canada,Singapore, Australia, South Africa, India,the United Kingdom, France, Swedenand Germany as well as members of theGrant Thornton International IFRSteam. It meets in person three times ayear to discuss technical matters whichare related to IFRS.

Each quarter we throw a spotlight on one of the members of the IIG. This quarter we focus on Germany’s representative:

Thomas Senger, GermanyThomas is Warth & Klein GrantThornton Germany’s head of assurancefor public interest entities.

Thomas joined our German memberfirm in 1991, and has over 20 years ofexperience as a specialist in financialreporting. He is a member of theGerman Institute’s IFRS working group,which he has served for more than 13 years, and was head of its IFRS for SMEs working group.

Thomas is also a member of the Tax Advisory Panel, which has beenestablished by the UK and Germanaccounting standard setters as part ofEFRAG’s pro-active project on theaccounting for corporate income taxes.

Grant Thornton UK named Auditor of the YearOur UK member firm, Grant ThorntonLLP, has been declared the top auditoramong the six largest UK firms for thesecond year running.

The firm was announced as thewinner of the Auditor of the Year (LargeSix) category at The FDs’ ExcellenceAwards. The FDs’ Excellence Awards isthe largest independent poll of UKfinance directors (FDs) into the servicesprovided by auditors, banks, law firmsand technology firms. The results werebased on the responses of over 900 FDs.

FDs who took the survey describedour UK member firm as “verysupportive”, with one particularrespondent being quoted on the night,saying, “They demonstrate a clearunderstanding of our business and our direction. The audit was testing,extremely thorough – but balanced.”

14 IFRS News Quarter 3 2011

Grant Thornton’s International IFRSInterpretation Group meetsIn April, the Grant ThorntonInternational IFRS Interpretation Group(IIG) met in the Virginian office of ourUS member firm.

During the meeting they were joinedby staff from the US Securities andExchange Commission (SEC) as part ofthe SEC’s outreach activities for the IFRSWork Plan in the US.

Paul Beswick, Deputy ChiefAccountant, Office of the ChiefAccountant and Shelly Luisi, SeniorAssociate Chief Accountant, Office of theChief Accountant, discussed the status ofthe IFRS work plan with the members ofthe IIG, as well as the experiences ofdifferent jurisdictions with IFRSconvergence/adoption and issues such aspromoting the consistent application ofIFRS across jurisdictions.

Grant Thornton Australia launchessurveyOur Australian member firm haslaunched a survey under the title“Simplifying financial reporting: Fact or fiction?”.

The survey is designed to seewhether recent changes to financialreporting requirements have actuallyreduced compliance costs, whether

further improvements are needed, andwhat lessons can be learned for thefuture.

IFRS News Quarter 3 2011 15

Grant Thornton Ecuador

Our new member firm in Ecuador hashosted a conference on the application ofIFRS and its commercial impact.

The conference generated a greatdeal of interest in the cities of Quito andGuayaquil, and demonstrates ourambition of building our organisation inkey emerging locations.

New IASB chairmanHans Hoogervorst has assumed the roleof IASB chairman following Sir DavidTweedie’s retirement from the role at theend of June 2011. Under the 10-yearleadership of Sir David Tweedie, the IASBsucceeded in establishing IFRS as theaccepted set of financial reportingstandards in more than 100 countries.Prior to taking up the role,

Mr Hoogervorst was chairman of theNetherlands Authority for the FinancialMarkets (AFM), the Dutch securities andmarket regulator, chairman of theTechnical Committee of the InternationalOrganization of Securities Commissions(IOSCO) and co-chair of the FinancialCrisis Advisory Group (FCAG), anindependent body of senior leadersformed to advise accounting standard-setters on their response to the globalfinancial crisis.Ian Mackintosh has assumed the role

of vice-chairman of the IASB. Prior totaking up the role, Mr Mackintosh waschairman of the UK Accounting StandardsBoard and chairman of the group ofnational accounting standard-setters, abody in which more than 20 national andregional accounting standard-settingorganisations participate. His significantexperience in the standard-setting field willassist both Mr Hoorgervorst and the IASBas it seeks to establish IFRSs as theglobal standard.

Request for views on IASB agendaThe IASB will be publishing for the firsttime in Q3 2011 a Request for Views onthe future strategic direction and overallbalance of its agenda.The objective is to enhance the IASB’s

agenda setting process by providing aformal channel for public input on theoverall strategic direction and balance ofthe IASB’s agenda. More details will followin next quarter’s edition of IFRS News.

International Valuation StandardsThe International Valuation StandardsCouncil (IVSC) has published an ExposureDraft of proposed new “InternationalValuation Standards”. The Exposure Draft covers valuations

for most types of asset, including for thefirst time a proposed standard forfinancial instruments. The proposals onfinancial instruments are part of the IVSC’sattempt to rebuild confidence in thevaluations of financial products. In theirexamination of the causes of the2007/2008 financial crisis, politicians andfinancial regulators had identified thatvaluation, and in particular a lack ofunderstanding of the valuations ofcomplex financial instruments by investorsand other users of financial information,had been a significant contributory factorto the crisis. The proposals also reflect current

developments in IFRS, which increasinglyrequire valuations for assets and liabilities.

IASB and FASB extend timeline forcompleting the convergence programIn a podcast released in April 2011, theIASB and the FASB announced that theywill be extending by a few months thetimeline for their joint projects on revenuerecognition, leases, financial instruments,and insurance contracts. The projectswere originally intended to be completedby 30 June 2011. In the podcast, outgoing IFRS

Chairman Sir David Tweedie and his UScounterpart Leslie Seidman emphasisedthe importance of reaching high qualitysolutions on the projects before issuingfinal Standards. Since the podcast wasreleased, the IASB has issued a revisedwork plan showing a target date of thefirst half of 2012 for the completion of theStandards on revenue recognition, leasesand insurance contracts.

FEE discussion paper on combinedfinancial statementsThe Fédération des Experts ComptablesEuropéens (FEE) has issued a discussionpaper aimed at enhancing the publicdebate on the preparation of combinedfinancial statements under IFRS. At present, IFRS do not provide a

specific standard for the preparation ofcombined financial statements. FEE,which is the representative organisationfor the accountancy profession in Europe,has noted that as a result there appearsto have been diversity in practice inpreparing such financial information. Thecomment period for the discussion paperends 30 September 2011.

Round-up

16 IFRS News Quarter 3 2011

Preliminary conclusions of strategyreview published The Trustees of the IFRS Foundation, the oversight body of the IASB, have published for public comment thepreliminary conclusions of their strategyreview. The conclusions cover a number of

areas, including defining the publicinterest to which the IFRS Foundation iscommitted; governance; the process forensuring that the IASB’s standards are ofhigh quality, meet the requirements of awell-functioning capital market and areimplemented consistently across theworld; and ensuring the organisation isfinanced in a manner that permits it tooperate effectively, efficiently andindependently.

Cutting Clutter from Annual ReportsThe UK Accounting Standards Board haspublished a report entitled ‘Cutting Clutter:Combating clutter in annual reports’. The report looks at the problem of

clutter in annual reports, which canobscure relevant information and make it harder for users to analyse theperformance and prospects of abusiness.The report provides preparers of

annual reports with practical aids forreducing clutter, giving ideas for howdisclosures might look without the clutter,and factors to consider when planning theannual report process.

Considering the Effects of AccountingStandardsThe European Financial ReportingAdvisory Group (EFRAG) and the UKAccounting Standards Board havepublished a Discussion Paper,‘Considering the Effects of AccountingStandards’.

The proposals call on standard settersto consider the effects of accountingstandards throughout their due process,from start to finish, the overall objectivebeing to contribute to improving the wayin which accounting standard settersdevelop and implement standards. Feedback from the Discussion Paper,

which is open for comment until 31August 2011, will be used to assesssupport for the proposals and enhancethem, so that they can form the basis ofpossible improvements to the IASB’s dueprocess.

IASB and Japanese AccountingStandards Board meetThe IASB and the Japanese AccountingStandards Board met in Tokyo in June.During the meeting they announced theirintention to deepen their co-operation inpreparation for a decision around 2012on the mandatory application of IFRSs inJapan.

Proposed IFRS TaxonomyenhancementsThe IFRS Foundation has published anexposure draft of the IFRS Taxonomy2011 interim release ‘Common-practiceconcepts’. The IFRS Taxonomy is a translation of

IFRS into eXtensible Business ReportingLanguage (XBRL). The proposed interimrelease contains supplementary tags forthe IFRS Taxonomy that reflect disclosuresthat are commonly reported by entities intheir IFRS financial statements.

AppointmentsSimon Carey, New ZealandSimon Carey, a partner in ourChristchurch office, has been appointedas a member of the Accounting StandardsReview Board (ASRB) of New Zealand.The ASRB consists of between four

and seven members appointed on therecommendation of New Zealand’sMinister of Commerce. Its primaryfunctions are to set some aspects of thestrategy for financial reporting, and toreview and approve financial reportingstandards in New Zealand. It also seeks toinfluence the development of internationalstandards and has close linkages withAustralian financial reporting bodies.

John C. Cheng, PanamaCongratulations to John C. Cheng fromGrant Thornton Panama who takes officeas President of the Institute of CertifiedPublic Accountants of Panama with effectfrom 1 July.

IFRS News Quarter 3 2011 17

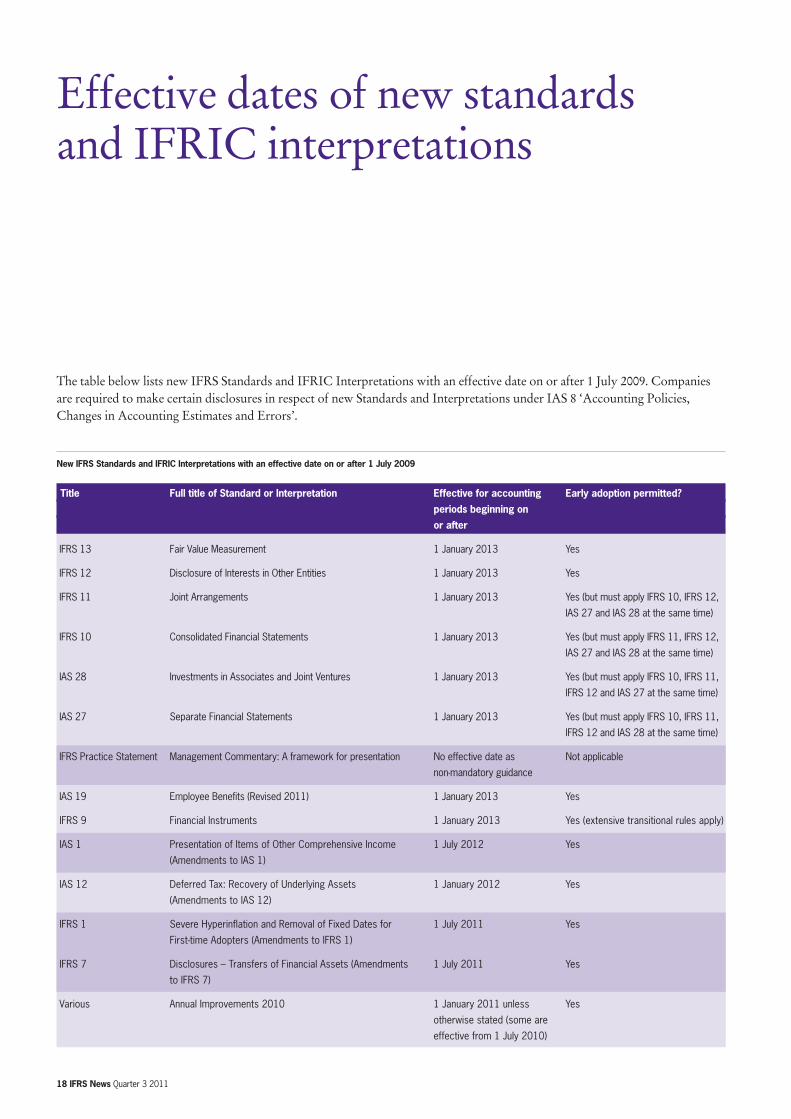

The table below lists new IFRS Standards and IFRIC Interpretations with an effective date on or after 1 July 2009. Companiesare required to make certain disclosures in respect of new Standards and Interpretations under IAS 8 ‘Accounting Policies,Changes in Accounting Estimates and Errors’.

Effective dates of new standards and IFRIC interpretations

New IFRS Standards and IFRIC Interpretations with an effective date on or after 1 July 2009

Title Full title of Standard or Interpretation Effective for accounting Early adoption permitted?

periods beginning on

or after

IFRS 13 Fair Value Measurement 1 January 2013 Yes

IFRS 12 Disclosure of Interests in Other Entities 1 January 2013 Yes

IFRS 11 Joint Arrangements 1 January 2013 Yes (but must apply IFRS 10, IFRS 12,

IAS 27 and IAS 28 at the same time)

IFRS 10 Consolidated Financial Statements 1 January 2013 Yes (but must apply IFRS 11, IFRS 12,

IAS 27 and IAS 28 at the same time)

IAS 28 Investments in Associates and Joint Ventures 1 January 2013 Yes (but must apply IFRS 10, IFRS 11,

IFRS 12 and IAS 27 at the same time)

IAS 27 Separate Financial Statements 1 January 2013 Yes (but must apply IFRS 10, IFRS 11,

IFRS 12 and IAS 28 at the same time)

IFRS Practice Statement Management Commentary: A framework for presentation No effective date as Not applicable

non-mandatory guidance

IAS 19 Employee Benefits (Revised 2011) 1 January 2013 Yes

IFRS 9 Financial Instruments 1 January 2013 Yes (extensive transitional rules apply)

IAS 1 Presentation of Items of Other Comprehensive Income 1 July 2012 Yes

(Amendments to IAS 1)

IAS 12 Deferred Tax: Recovery of Underlying Assets 1 January 2012 Yes

(Amendments to IAS 12)

IFRS 1 Severe Hyperinflation and Removal of Fixed Dates for 1 July 2011 Yes

First-time Adopters (Amendments to IFRS 1)

IFRS 7 Disclosures – Transfers of Financial Assets (Amendments 1 July 2011 Yes

to IFRS 7)

Various Annual Improvements 2010 1 January 2011 unless Yes

otherwise stated (some are

effective from 1 July 2010)

18 IFRS News Quarter 3 2011

New IFRS Standards and IFRIC Interpretations with an effective date on or after 1 July 2009

Title Full title of Standard or Interpretation Effective for accounting Early adoption permitted?

periods beginning on

or after

IFRIC 14 Prepayments of a Minimum Funding Requirement 1 January 2011 Yes

– Amendments to IFRIC 14

IAS 24 Related Party Disclosures 1 January 2011 Yes (either of the whole Standard or

of the partial exemption for

government-related entities)

IFRS 1 Limited Exemption from Comparative IFRS 7 Disclosures 1 July 2010 Yes

for First-time Adopters (Amendment to IFRS 1)

IFRIC 19 Extinguishing Financial Liabilities with Equity Instruments 1 July 2010 Yes

IAS 32 Classification of Rights Issues (Amendment to IAS 32) 1 February 2010 Yes

IFRS for SMEs International Financial Reporting Standard for Small and Immediately subject to approval N/A

Medium-sized Entities within the individual jurisdiction

Various Annual Improvements 2009 1 January 2010 unless Yes

otherwise stated (some are

effective from 1 July 2009)

IFRS 1 Additional Exemptions for First-time Adopters (Amendments 1 January 2010 Yes

to IFRS 1)

IFRS 2 Group Cash-settled Share-based Payment Transactions 1 January 2010 Yes

(Amendments to IFRS 2)

IFRS 1 First-time Adoption of International Financial Reporting 1 July 2009 Yes

Standards (Revised 2008)

IAS 39 Amendment to IAS 39 Financial Instruments: Recognition 1 July 2009 Yes

and Measurement: Eligible Hedged Items

IFRIC 17 Distributions of Non-cash Assets to Owners 1 July 2009 Yes (but must also apply IFRS 3

Revised 2008, IAS 27 Revised 2008

and IFRS 5 (as amended by IFRIC 17))

IFRS 3 Business Combinations (Revised 2008) 1 July 2009 Yes (but only for periods beginning on

or after 30 June 2007, and in

conjunction with IAS 27 Revised 2008)

IAS 27 Consolidated and Separate Financial Statements 1 July 2009 Yes (but must be applied in

(Revised 2008) conjunction with IFRS 3 Revised 2008)

IFRIC 18 Transfers of Assets from Customers Transfers of assets on or Yes provided the valuations and other

after 1 July 2009 information needed to apply the

Interpretation to past transfers were

obtained at the time those transfers

occurred

IFRS News Quarter 3 2011 19

www.gti.org

© 2011 Grant Thornton International Ltd. All rights reserved.Grant Thornton International Ltd (Grant Thornton International) and the member firms are not a worldwide partnership. Services are delivered independently by the member firms.

This table lists the documents that theIASB currently has out to comment andthe comment deadline. Grant ThorntonInternational aims to respond to each ofthese publications.

Open for comment

Current IASB documents

Document type Title Comment deadline

Exposure Draft Improvements to IFRSs 21 October 2011

IFRS Foundation IFRSs as the Global Standard: Setting a Strategy for the 25 July 2011

Consultation Foundation’s Second Decade

document