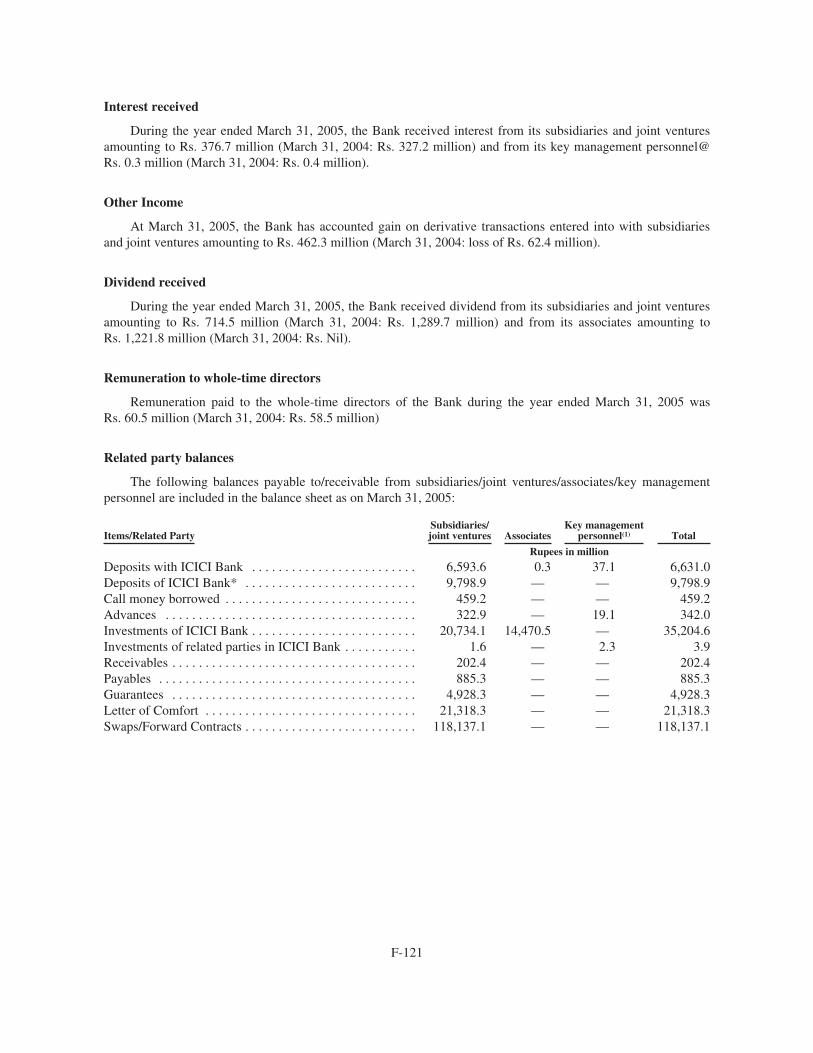

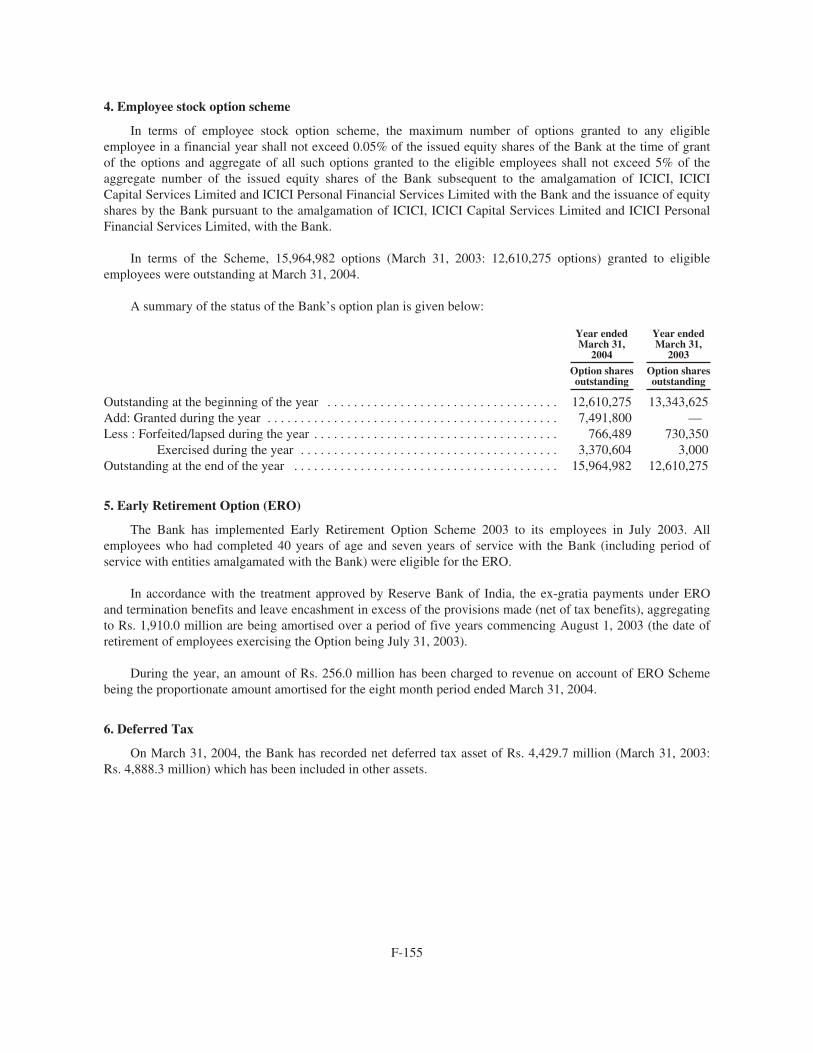

icici bank notes maturity date

TRANSCRIPT

The Offering

Issuer . . . . . . . . . . . . . . . . . . . . . . . . . . . ICICI Bank Limited, a public limited company incorporated under thelaws of the Republic of India (“ICICI Bank”).

Notes Offered . . . . . . . . . . . . . . . . . . . . . 6.375% Fixed to Floating Rate Subordinated Notes due April 30,2022 issued by ICICI Bank in an aggregate principal amount of US$750,000,000 (the “notes”).

Maturity . . . . . . . . . . . . . . . . . . . . . . . . . The notes will mature on April 30, 2022 (the “Maturity Date”).

Trustee . . . . . . . . . . . . . . . . . . . . . . . . . . The Bank of New York

Interest . . . . . . . . . . . . . . . . . . . . . . . . . . Interest will be payable on the outstanding principal amount of thenotes from January 12, 2007 (the “Issue Date”) (i) semi-annually inarrears on April 30 and October 31 of each year, at a fixed rate perannum equal to 6.375%, during the period from (and including) theIssue Date to (but excluding) April 30, 2017, and (ii) thereafter semi-annually in arrears on April 30 and October 31 of each year, at avariable rate per annum equal to the 6-month LIBOR plus a margin of2.28%. The first payment of interest will be made on April 30, 2007in respect of the period from (and including) the Issue Date to (butexcluding) April 30, 2007. See “Description of the Notes—Interest”.Each such date is an “Interest Payment Date”.

Each period from and including an Interest Payment Date or the IssueDate, as applicable, to but excluding the next Interest Payment Dateuntil April 30, 2017 is called a “Fixed Interest Period”. The periodfrom and including April 30, 2017, to but excluding the nextfollowing Interest Payment Date, and each successive period fromand including an Interest Payment Date to, but excluding, theMaturity Date is called a “Floating Interest Period”. Each FixedInterest Period and Floating Interest Period is referred to as an“Interest Period”.

If and to the extent that, on any Interest Payment Date, ICICI Bankhas:

• a Capital Deficiency (as defined below), then ICICI Bank shallnot pay any principal or interest on such date and (i) with respectto any Interest Payment Date other than the Maturity Date, theinterest payable on such date shall be deferred until the nextsucceeding date on which interest is payable under the notes, and(ii) with respect to the Maturity Date, any interest (includingInterest Arrears and Additional Interest (each as defined below))and principal payable on such date shall be deferred until theCompulsory Payment Date (as defined below); or

• a Net Loss (as defined below) or increase in Net Loss without aCapital Deficiency, then ICICI Bank shall not pay any principalor interest on such date except that it may pay interest with theprior approval of the Reserve Bank of India (“RBI”) and, in theevent that the RBI does not grant approval for payment of interest(i) with respect to any Interest Payment Date other than the

3

Maturity Date, the interest payable on such date shall be deferreduntil the next succeeding date on which interest is payable underthe notes, and (ii) with respect to the Maturity Date, any interest(including Interest Arrears and Additional Interest (each asdefined below)) and principal payable on such date shall bedeferred until the Compulsory Payment Date (as defined below).

“Capital Deficiency” means, for any Interest Payment Date, thatICICI Bank determines that its capital to risk assets ratio (“CRAR”)has declined below the minimum regulatory requirement prescribedby the RBI from time to time, (i) as at the immediately precedingMarch 31 in the case of the Interest Payment Date in April and (ii) asat the immediately preceding September 30 in the case of the InterestPayment Date in October.

“Compulsory Payment Date” means, in the case of principal andinterest (including Interest Arrears and Additional Interest), a dateafter the Maturity Date following deferral of the payment of principaland interest which is one business day after the first date on whichICICI Bank determines that it has (i) neither a Capital Deficiency nora Net Loss or (ii) no Capital Deficiency, but a Net Loss or increase inNet Loss and has received approval from the Reserve Bank of India tomake the payment of principal and interest, provided that any suchpayment will not cause ICICI Bank to have a Capital Deficiency or inthe case of (i) a Net Loss.

“Net Loss” means, for any Interest Payment Date, a determinationmade by ICICI Bank as per (a) unconsolidated Indian GAAP financialstatements that it has either (i) a negative balance reported in thebalance in the profit and loss account line item in its Balance Sheet,or (ii) a net loss reported in its profit and loss account, as at and forthe 12 month period ended on the immediately preceding March 31 inthe case of the Interest Payment Date in April or as at and for the sixmonth period ended on the immediately preceding September 30 inthe case of the Interest Payment Date in October, or (b) regulations orguidelines prescribed by Reserve Bank of India from time to time inthis regard. In case of any conflict between the determination madeunder (a) and (b) hereinabove, the determination made under (b) shallprevail.

If, as a consequence of a Capital Deficiency or a Net Loss, ICICIBank shall not pay principal or interest on an Interest Payment Datethen, no later than the 5th day prior to the relevant Interest PaymentDate, it shall deliver to the Trustee a notice indicating the existence ofsuch Capital Deficiency or Net Loss and that it will as a consequencethereof not pay principal or interest on such Interest Payment Date (a“Payment Suspension Notice”). A Payment Suspension Notice willhave no force or effect unless ICICI Bank has delivered it to theTrustee in accordance herewith.

4

Interest on the notes will be cumulative. This means that, if interest isnot paid on the notes on any Interest Payment Date, holders of thenotes will have the right to receive those interest payments on thenext succeeding date on which interest is payable under the notes.

In the event that ICICI Bank determines there is a Net Loss without aCapital Deficiency for any Interest Payment Date, ICICI Bank shallapply to the RBI for permission to pay interest which wouldotherwise be due on such Interest Payment Date. If the RBI grantssuch permission, notwithstanding any prior delivery of a PaymentSuspension Notice in relation to such Interest Payment Date, ICICIBank shall, subject to compliance with such conditions as may bestipulated by the RBI while granting its approval, proceed to pay theinterest due on such Interest Payment Date, either (i) on such InterestPayment Date, if approval from the RBI is received in advancethereof, or (ii) within 1 business day of receipt of the approval fromthe RBI if such approval is received after the date which is 1 businessday prior to the relevant Interest Payment Date.

In the event that any interest in respect of the notes is not paid on anInterest Payment Date (any such amount, “Interest Arrears”), suchInterest Arrears shall bear interest (“Additional Interest”) from theInterest Payment Date on which the interest first became due to (andincluding) the actual date of payment. Additional Interest shall becalculated at the interest rate payable on the notes. Additional Interestaccrued to any Interest Payment Date shall be added, for the purposeonly of calculating the Additional Interest accruing thereafter, to theamount of Interest Arrears remaining unpaid on such InterestPayment Date.

Dividend and Capital Restriction . . . . So long as any Interest Arrears or Additional Interest thereon remainunpaid, ICICI Bank will not (i) other than to the holders of ExistingPreference Shares to the extent permissible and subject to prevailingIndian laws, declare or pay any dividend, distribution or otherpayment in respect of its Ordinary Shares, any other security orobligation of ICICI Bank ranking junior to the notes, or any OtherPari Passu Claims (other than as required under the terms of anypreference shares or other security or obligation ranking junior to thenotes (but not including Ordinary Shares) or Other Pari PassuClaims), or (ii) other than as required under the terms of such securityor obligation, effect any repurchase or redemption of any of itsOrdinary Shares, any other security or obligation of ICICI Bankranking junior to the notes or any Other Pari Passu Claims, (orcontribute any moneys to a sinking fund for the redemption of anysuch shares, securities or claims).

“Ordinary Shares” means ordinary shares of ICICI Bank.

“Existing Preference Shares” means the three hundred fifty 0.001%preference shares of Rs. 10,000,000 each of ICICI Bank allotted asfully paid preference shares to preference shareholders of erstwhileICICI Limited, redeemable at par on April 20, 2018.

5

Subordination . . . . . . . . . . . . . . . . . . . . The payment obligations of ICICI Bank under the notes constituteunsecured subordinated obligations of ICICI Bank and will rank(i) behind (junior to) the claims of holders of Senior Indebtedness,(ii) pari passu with Other Pari Passu Claims and (iii) before (seniorto) (x) the claims for payment of any obligation that, expressly or byapplicable law, is subordinated to the notes, (y) the claims of holdersof preference and equity shares of ICICI Bank and (z) the claims ofinvestors in instruments eligible for inclusion in Tier I capital ofICICI Bank, in accordance with the subordination provisions of theIndenture.

“Other Pari Passu Claims” means claims of creditors of ICICI Bankwhich are subordinated so as to rank pari passu with claims in respectof the notes.

“Senior Indebtedness” means all deposits and other senior liabilitiesof ICICI Bank (including those in respect of bonds, notes anddebentures), and debt instruments constituting “lower Tier II” capitalof ICICI Bank from time to time, other than liabilities of ICICI Bankunder the notes. For the avoidance of doubt, Senior Indebtedness shallnot include any other debt securities of ICICI Bank which qualify forUpper Tier II treatment under the RBI guidelines.

Additional Amounts . . . . . . . . . . . . . . . All payments of principal and interest in respect of the notes will bemade without withholding or deduction for any taxes or othergovernmental charges imposed by a Taxing Jurisdiction, unless suchwithholding or deduction is required by law. In the event ICICI Bankis required by law to withhold or deduct amounts for any such taxesor other governmental charges, ICICI Bank will pay such additionalamounts so that the holders of the notes will receive the sameamounts as they would have received without such withholding ordeduction, subject to certain exceptions. ICICI Bank will pay anystamp, administrative, court, documentary, excise or property taxesimposed on the initial issuance and delivery of the notes in a TaxingJurisdiction and will indemnify the holders of the notes for any suchtaxes paid by the holders of the notes, excluding any such duties ortaxes which may relate to any transfer or transmission of the notesfollowing their initial issuance and delivery by us. See “Descriptionof the Notes—Additional Amounts.”

“Taxing Jurisdiction” means India, or any political subdivisionthereof or any authority or agency therein or thereof having the powerto tax, or any other jurisdiction or any political subdivision or anyauthority or agency therein or thereof having the power to tax towhich ICICI Bank becomes subject in respect of payments made by itof principal or interest on the notes.

Optional Redemption . . . . . . . . . . . . . . The Notes are not redeemable at the option of the holders thereof atany time and are not redeemable at the option of ICICI Bank prior to

6

April 30, 2017 (the “First Call Date”), except in certaincircumstances in the event of certain changes in withholding taxes(see “Description of Notes—Optional Tax Redemption”) or upon theoccurrence of a Regulatory Event (see “Description of the Notes—Redemption Upon a Regulatory Event”).

The notes may be redeemed at the option of ICICI Bank, in whole(and not in part), on the First Call Date or on any subsequent InterestPayment Date; provided that ICICI Bank will give notice to holdersof notes not less than 15 business days but not more than 30 businessdays prior to any such redemption. This notice will be published inaccordance with the notice provisions described under “Descriptionof the Notes—Notices”.

The redemption price for any redemption of the notes will be 100% ofthe principal amount of the notes then outstanding, plus InterestArrears (if any) and Additional Interest (if any) on the principalamount being redeemed to (but excluding) the redemption date (the“Base Redemption Price”).

Any optional redemption of notes is subject to compliance withapplicable regulatory requirements, including the prior approval ofthe RBI. The RBI, whilst considering the request of ICICI Bank to soredeem the notes, may take into consideration, among other things,ICICI Bank’s CRAR position both at the time of the proposedredemption and thereafter.

Optional Tax Redemption . . . . . . . . . . In the event ICICI Bank determines that, as a result of certain changesin or amendments to the laws or regulations of a Taxing Jurisdiction(as defined above) ICICI Bank has been or will be required to payadditional amounts as described under “Description of the Notes—Additional Amounts,” ICICI Bank may, at its option, but subject toapproval by the Reserve Bank of India, redeem the notes at aredemption price equal to the Base Redemption Price. See“Description of the Notes—Optional Tax Redemption”.

Redemption Upon a RegulatoryEvent . . . . . . . . . . . . . . . . . . . . . . . . . . Upon the occurrence of a Regulatory Event, and subject to the

conditions (see “Description of the Notes”), ICICI Bank, upon thereceipt of prior permission from the RBI, will have the right toredeem the notes in whole (and not in part) at a redemption priceequal to (A) in the case of redemption prior to April 30, 2017, thehigher of the Base Redemption Price and the Make Whole Amount(as defined herein), or (B) in the case of a redemption on or afterApril 30, 2017, the Base Redemption Price.

“Regulatory Event” means the receipt by ICICI Bank of an opinion,declaration, rule or decree of the RBI or any other regulatory or

7

governmental authority succeeding to the authority of the RBI asregards monitoring of capital adequacy of Indian banks, to the effectthat there has been either (i) a change in the law or regulation or (ii) achange in the interpretation thereof, resulting in more than aninsubstantial risk that the notes (or any portion thereof) will not beeligible to be included in calculating the Upper Tier II capital ofICICI Bank, other than as a result of such notes exceeding thepermitted basket for notes eligible for inclusion as Upper Tier IIcapital.

Form and Denomination . . . . . . . . . . . The notes will be in fully registered form without interest couponsattached. The notes sold in reliance on Rule 144A under theSecurities Act (“Rule 144A”) will be issued in the form of a restrictedglobal note (the “Restricted Global Note”) and the notes sold inreliance on Regulation S under the Securities Act (“Regulation S”)will be issued in the form of a Regulation S global note (the“Regulation S Global Note”). The Restricted Global Note and theRegulation S Global Note will be registered in the name of Cede &Co. as nominee for, and deposited with the trustee as custodian for,DTC. The notes offered and sold in reliance on Rule 144A will beissued in minimum denominations of US$ 100,000 and integralmultiples of US$ 1,000 in excess thereof. Notes offered and sold inreliance on Regulation S will be issued in minimum denominations ofUS$ 100,000 and integral multiples of US$ 1,000 in excess thereof.See “Form, Denomination and Transfer.”

Use of Proceeds . . . . . . . . . . . . . . . . . . . ICICI Bank will use the proceeds of the issue and sale of the notes tosupport growth of ICICI Bank and its subsidiaries, to increase theUpper Tier II capital of ICICI Bank and for general corporatepurposes, including to pay certain expenses relating to the offering.

Resale Restrictions . . . . . . . . . . . . . . . . The notes have not been and will not be registered under theSecurities Act and may not be offered, sold, pledged or otherwisetransferred except in a transaction pursuant to the exemption providedby Regulation S, Rule 144A or such other available exemption fromthe registration requirements of the Securities Act. The notes may betransferred only as described under “Transfer Restrictions”.

Substitution of Entity or Branch . . . . . ICICI Bank may at any time, subject to any regulatory approvals asmay be required, elect to have the liability to pay the amounts dueunder the terms of the notes transferred, in whole or in part, to anentity controlled by ICICI Bank or a branch of ICICI Bank other thanthe Issuer. Any such transfer to an entity might be deemed for U.S.federal income tax purposes to be an exchange of the notes for newnotes by the holders thereof, resulting in the recognition of taxablegain or loss for such purposes and possibly certain other adverse taxconsequences.

Listing and Trading . . . . . . . . . . . . . . . Approval-in-principle has been obtained for listing of the notes on theSingapore Exchange. The approval-in-principle for the listing, and theadmission to the Official List of the Singapore Exchange, of the notes

8

is not to be taken as an indication of any of the merits of ICICI Bankor the merits of the notes. The notes will be traded on the SingaporeExchange in a minimum board lot size of US$ 200,000 for so long asthe notes are listed on the Singapore Exchange.

Clearance and Settlement . . . . . . . . . . The notes will be issued in book-entry form through the facilities ofDTC, on the one hand and Euroclear and Clearstream, Luxembourg,on the other, each with respect to their respective participants.Holders of beneficial interests in notes held in book-entry form willbe entitled to receive physical delivery of certificated notes onlyunder certain circumstances. For a description of certain factorsrelating to clearance and settlement, see “Form, Denomination andTransfer.”

Governing Law . . . . . . . . . . . . . . . . . . . The Indenture, the notes and the Calculation Agency Agreement aregoverned by the laws of the State of New York, United States ofAmerica, except that the subordination provisions of the Indentureand the notes are governed by the laws of India.

Security CodesRule 144A Regulation S

ISIN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . US45104GAE44 USY38575DE68CUSIP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45104GAE4 Y38575DE6Common Code . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 028219539 028219628

9

RISK FACTORS

Prospective investors should carefully consider the risks described below, together with the risks describedin the other sections of this offering memorandum before making any investment decision relating to our notes.The occurrence of any of the following events could have a material adverse effect on our business including ourability to grow our asset portfolio, the quality of our assets, our liquidity, our financial performance, ourstockholders’ equity, our ability to implement our strategy and our ability to repay the interest or principal onthe note in a timely fashion or at all.

Before making an investment decision, prospective investors should carefully consider all of the informationcontained in this offering memorandum, including the financial statements included in this offeringmemorandum.

Risks Relating to India

A slowdown in economic growth or rise in interest rates in India could cause our business to suffer.

Any slowdown in the Indian economy or volatility of global commodity prices, in particular oil and steelprices, could adversely affect our borrowers and contractual counterparties. Because of the importance of ourcommercial banking operations for retail customers and the increasing importance of our agricultural loanportfolio to our business, any slowdown in the growth of the housing, automobiles and agricultural sectors couldadversely impact our business. Since 2004, interest rates in the Indian economy have increased significantly.Slowdown in demand for loans from corporate customers, retail customers and customers in the agriculturalsector, including due to higher interest rates, could adversely impact our business.

A significant increase in the price of crude oil could adversely affect the Indian economy, which couldadversely affect our business.

India imports approximately 70.0% of its requirements of crude oil, which were approximately 31.3% oftotal imports in fiscal 2006. For example, the sharp increase in global crude oil prices during fiscal 2001adversely affected the Indian economy in terms of volatile interest and exchange rates. This adversely affectedthe overall state of liquidity in the banking system leading to intervention by the Reserve Bank of India. Since2004, there has been a sharp increase in global crude oil prices due to both increased demand and pressure onproduction and refinery capacity, and political and military tensions in key oil-producing regions. The full burdenof the oil price increase has not been passed to Indian consumers and has been substantially absorbed by thegovernment and government-owned oil marketing companies. While global crude prices have moderatedrecently, sustained high levels, further increases or volatility of oil prices and the pass-through of increases toIndian consumers could have a material negative impact on the Indian economy and the Indian banking andfinancial system in particular, including through a rise in inflation and market interest rates and a higher tradedeficit.

A significant change in the Indian government’s economic liberalization and deregulation policies couldadversely affect our business and the price of our notes.

Our assets and customers are predominantly located in India. The Indian government has traditionallyexercised and continues to exercise a dominant influence over many aspects of the economy. Governmentpolicies could adversely affect business and economic conditions in India and our business.

Financial instability in other countries, particularly emerging market countries and countries where wehave established operations, could adversely affect our business and the price of our notes.

The Indian economy is influenced by economic and market conditions in other countries, particularlyemerging market countries in Asia. We have also established operations in several other countries. A loss of

17

investor confidence in the financial systems of other emerging markets and countries where we have establishedoperations or any worldwide financial instability may cause increased volatility in the Indian financial marketsand, directly or indirectly, adversely affect the Indian economy and financial sector and our business.

If regional hostilities, terrorist attacks or social unrest in some parts of the country increase, our businessand the price of our notes could be adversely affected.

India has from time to time experienced social and civil unrest and hostilities both internally and withneighboring countries. In the past, there have been military confrontations between India and Pakistan. India hasalso experienced terrorist attacks in some parts of the country. These hostilities and tensions could lead topolitical or economic instability in India and adversely affect our business.

Trade deficits could adversely affect our business and the price of our notes.

India’s trade relationships with other countries and its trade deficit, driven to a major extent by global crudeoil prices, may adversely affect Indian economic conditions. If trade deficits increase or are no longermanageable because of the rise in global crude oil prices or otherwise, the Indian economy, and therefore ourbusiness, could be adversely affected.

Natural calamities could adversely affect the Indian economy, our business and the price of our notes.

India has experienced natural calamities like earthquakes, floods and drought in the past few years. Theextent and severity of these natural disasters determine their impact on the Indian economy. For example, infiscal 2003, many parts of India received significantly less than normal rainfall. As a result of the droughtconditions in the economy during fiscal 2003, the agricultural sector recorded a negative growth of 7.0%. Also,the erratic progress of the monsoon in fiscal 2005 adversely affected sowing operations for certain crops andresulted in a decline in the growth rate of the agricultural sector from 9.6% in fiscal 2004 to 0.7% in fiscal 2005.The agricultural sector grew by 3.9% in fiscal 2006 and by 2.6% in the first half of fiscal 2007. Further prolongedspells of below or above normal rainfall or other natural calamities could adversely affect the Indian economyand our business, especially in view of our strategy of increasing our exposure to rural India.

Financial difficulty and other problems in certain financial institutions in India could adversely affect ourbusiness and the price of our notes.

As an Indian bank, we are exposed to the risks of the Indian financial system which may be affected by thefinancial difficulties faced by certain Indian financial institutions because the commercial soundness of manyfinancial institutions may be closely related as a result of credit, trading, clearing or other relationships. This risk,which is sometimes referred to as “systemic risk”, may adversely affect financial intermediaries, such as clearingagencies, banks, securities firms and exchanges with whom we interact on a daily basis. Any such difficulties orinstability of the Indian financial system in general could create an adverse market perception about Indianfinancial institutions and banks and adversely affect our business. See also “Overview of the Indian FinancialSector”. As the Indian financial system operates within an emerging market, it faces risks of a nature and extentnot typically faced in more developed economies, including the risk of deposit runs notwithstanding the existenceof a national deposit insurance scheme. For example, in April 2003, unsubstantiated rumors, believed to haveoriginated in Gujarat, a state in India, alleged that we were facing liquidity problems. Although our liquidityposition was sound, we witnessed higher than normal deposit withdrawals on account of these unsubstantiatedrumors for several days in April 2003. We successfully controlled the situation in this instance, but any failure tocontrol such situations in the future could result in high volumes of deposit withdrawals which would adverselyimpact our liquidity position.

A decline in India’s foreign exchange reserves may affect liquidity and interest rates in the Indian economywhich could adversely impact us.

A decline in India’s foreign exchange reserves could result in reduced liquidity and higher interest rates inthe Indian economy, which could adversely affect our business. See also “—Risks Relating to Our Business”.

18

Any downgrading of India’s debt rating by an international rating agency could adversely affect ourbusiness and our liquidity.

Any adverse revisions to India’s credit ratings for domestic and international debt by international ratingagencies may adversely affect our business and limit our access to capital markets and decrease our liquidity.

Uncertain enforcement of civil liabilities.

We are incorporated under the laws of India and all of our directors and executive officers reside outside theUnited States. In addition, a substantial portion of our assets are located outside the United States. As a result,you may be unable to:

• effect service of process within the United States upon us and other persons or entities; or

• enforce in the U.S. courts judgments obtained in the U.S. courts against us and other persons orentities, including judgments predicated upon the civil liability provision of the federal securities lawsof the United States.

The United States and India do not currently have a treaty providing for reciprocal recognition andenforcement of judgments (other than arbitration awards) in civil and commercial matters. Therefore, a finaljudgment for the payment of money rendered by any federal or state court in the United States for civil liability,whether or not predicated solely upon the general securities laws of the United States, would not be enforceablein India.

However, the party in whose favor such final judgment is rendered may bring a new suit in a competentcourt in India based on a final judgment that has been obtained in the United States within three years ofobtaining such final judgment. If and to the extent that Indian courts were of the opinion that fairness and goodfaith so required, they would, under current practice, give binding effect to the final judgment which had beenrendered in the United States, unless such a judgment contravened principles of public policy of India. It isunlikely that an Indian court would award damages on the same basis as a foreign court if an action is brought inIndia. Moreover, it is unlikely that an Indian court would award damages to the extent awarded in a finaljudgment rendered in the United States if it believed that the amount of damages awarded were excessive orinconsistent with Indian practice. In addition, any person seeking to enforce a foreign judgment in India isrequired to obtain prior approval of the Reserve Bank of India to execute such a judgment or to repatriate anyamount recovered. For more information, see “Enforceability of Civil Liabilities” in this offering memorandum.

Risks Relating to Our Business

Our business is particularly vulnerable to interest rate risk and volatility in interest rates could adverselyaffect our net interest margin, the value of our fixed income portfolio, our income from treasury operationsand our financial performance.

As a result of certain reserve requirements of the Reserve Bank of India, we are more structurally exposed tointerest rate risk than banks in many other countries. See “Supervision and Regulation—Legal ReserveRequirements”. These requirements result in our maintaining a large portfolio of fixed income Government ofIndia securities, and we could be materially adversely impacted by a rise in interest rates, especially if the risewere sudden or sharp. These requirements also have a negative impact on our net interest income and net interestmargin because we earn interest on a portion of our assets at rates that are generally less favorable than thosetypically received on our other interest-earning assets. If the yield on our interest-earning assets does not increaseat the same time or to the same extent as our cost of funds, or if our cost of funds does not decline at the sametime or to the same extent as the yield on our interest-earning assets, our net interest income and net interestmargin would be adversely impacted. We are also exposed to interest rate risk through our treasury operationsand our subsidiary, ICICI Securities, which is a primary dealer in Government of India securities. A rise ininterest rates or greater interest rate volatility could adversely affect our income from treasury operations or the

19

value of our fixed income securities trading portfolio. Sharp and sustained increases in the rates of interestcharged on floating rate home loans, which are a material proportion of our loan portfolio, would result inextension of loan maturities and higher monthly installments due from borrowers, which could result in higherrates of default in this portfolio.

A large proportion of ICICI’s loans consisted of project finance assistance, a substantial portion of which isparticularly vulnerable to completion and other risks.

Long-term project finance assistance was a significant proportion of ICICI’s asset portfolio and continues tobe a part of our loan portfolio. The viability of these projects depends upon a number of factors, including marketdemand, government policies and the overall economic environment in India and the international markets.These projects are particularly vulnerable to a variety of risks, including completion risk and counterparty risk,which could adversely impact their ability to generate revenues. We cannot be sure that these projects willperform as anticipated. In the past, we experienced a high level of default and restructuring in our project financeloan portfolio as a result of the downturn in certain global commodity markets and increased competition inIndia. Future project finance losses or high levels of loan restructuring could have a materially adverse effect onour profitability and the quality of our loan portfolio.

We have a high concentration of loans to certain customers and sectors and if a substantial portion of theseloans become non performing, the overall quality of our loan portfolio, our business and the price of ournotes could be adversely affected.

Our loan portfolio and non-performing asset portfolio have a high concentration in certain customers andsectors. See “Business—Asset Composition and Classification—Loan Concentration”. In the past, certain ofthese borrowers and sectors have been adversely affected by economic conditions in varying degrees. Creditlosses or financial difficulties of these borrowers and sectors in the future could adversely affect our business, ourfinancial performance, our shareholders’ equity and the price of our notes.

If we are not able to control the level of non-performing assets in our portfolio, our business will suffer.

We have experienced rapid growth in our retail loan portfolio. See “Business—Asset Composition andClassification—Loan Concentration”. Various factors, including a rise in unemployment, prolonged recessionaryconditions, a sharp and sustained rise in interest rates, developments in the Indian economy, movements in globalcommodity markets and exchange rates and global competition could cause an increase in the level ofnon-performing assets on account of these retail loans and have a material adverse impact on the quality of ourloan portfolio. In addition, under the directed lending norms of the Reserve Bank of India, we are required toextend 50.0% of our residual net bank credit (excluding the advances of ICICI at year-end fiscal 2002) to certaineligible sectors, which are categorized as “priority sectors”. See “Business—Asset Composition andClassification—Loan Concentration—Directed Lending”. We may experience a significant increase innon-performing assets in our directed lending portfolio, particularly loans to the agricultural sector and small-scale industries, where we are less able to control the portfolio quality and where economic difficulties are likelyto affect our borrowers more severely. Any change by the Reserve Bank of India in the directed lending normsmay result in our inability to meet the priority sector lending requirements as well as require us to increase ourlending to relatively riskier segments and may result in an increase in non-performing assets in the directedlending portfolio. We may not be able to control or reduce the level of non-performing assets in our project andcorporate finance portfolio. We may not be successful in our efforts to improve collections and foreclose onexisting non-performing assets. We also have investments in security receipts arising out of the sale ofnon-performing assets by us to Asset Reconstruction Company (India) Limited, a reconstruction companyregistered with the Reserve Bank of India. See “Business—Asset Composition and Classification”. There can beno assurance that Asset Reconstruction Company (India) Limited will be able to recover these assets and redeemour investments in security receipts and that there will be no reduction in the value of these investments.

20

If we are not able to control or reduce the level of non-performing assets, the overall quality of our loanportfolio may deteriorate and our business may be adversely affected.

Further deterioration of our non-performing asset portfolio and an inability to improve our provisioningcoverage as a percentage of gross non-performing assets could adversely affect the price of our notes.

Although we believe that our total provisions will be adequate to cover all known losses in our assetportfolio, there can be no assurance that there will be no deterioration in the provisioning coverage as apercentage of gross non-performing assets or otherwise or that the percentage of non-performing assets that wewill be able to recover will be similar to our and ICICI’s past experience of recoveries of non-performing assets.In the event of any further deterioration in our non-performing asset portfolio, there could be an adverse impacton our business, our future financial performance, our stockholders’ equity and the price of our notes.

The value of our collateral may decrease or we may experience delays in enforcing our collateral whenborrowers default on their obligations to us which may result in failure to recover the expected value ofcollateral security exposing us to a potential loss.

A substantial portion of our loans to corporate and retail customers are secured by collateral. See“Business—Asset Composition and Clarification—Classification of Assets—Non-Performing Asset Strategy”.We may not be able to realize the full value of our collateral as a result of delays in bankruptcy and foreclosureproceedings, defects in the perfection of collateral, fraudulent transfers by borrowers and other factors, includinglegislative changes and judicial pronouncements. Failure to recover the expected value of collateral could exposeus to potential losses, which could adversely affect our business.

The failure of our restructured loans to perform as expected or a significant increase in the level ofrestructured loans in our portfolio could affect our business.

Our standard assets include restructured standard loans. Our borrowers’ requirements to restructure theirloans can be attributed to several factors, including increased competition arising from economic liberalization inIndia, variable industrial growth, a sharp decline in commodity prices, the high level of debt in the financing ofprojects and capital structures of companies in India and the high interest rates in the Indian economy during theperiod in which a large number of projects contracted their borrowings. These factors reduced profitability forcertain of our borrowers and also resulted in the restructuring of certain Indian companies in sectors includingiron and steel, textiles and cement. The failure of these borrowers to perform as expected or a significant increasein the level of restructured assets in our portfolio could adversely affect our business, our future financialperformance, our shareholders’ equity and the price of our notes.

We face greater credit risks than banks in developed economies.

Our credit risk is higher because most of our borrowers are based in India. Unlike several developedeconomies, a nationwide credit bureau has become operational in India only recently. This may affect the qualityof information available to us about the credit history of our borrowers, especially individuals and smallbusinesses. In addition, the credit risk of our borrowers, particularly small and middle market companies, ishigher than borrowers in more developed economies due to the greater uncertainty in the Indian regulatory,political, economic and industrial environment and the difficulties of many of our corporate borrowers to adapt toglobal technological advances. Also, several of our corporate borrowers suffered from low profitability becauseof increased competition from economic liberalization, a sharp decline in commodity prices, a high debt burdenand high interest rates in the Indian economy at the time of their financing, and other factors. This may lead to anincrease in the level of our non-performing assets and there could be an adverse impact on our business, ourfuture financial performance, our shareholders’ equity and the price of our notes.

21

Our funding is primarily short-term and if depositors do not roll over deposited funds upon maturity, ourbusiness could be adversely affected.

Most of our incremental funding requirements, including replacement of maturing liabilities of ICICI(which generally had longer maturities), are met through short-term funding sources, primarily in the form ofdeposits including inter-bank deposits. Our customer deposits generally have a maturity of less than one year.However, a large portion of our assets, primarily the assets of ICICI and our home loan portfolio, have mediumor long-term maturities, creating the potential for funding mismatches. Our ability to raise fresh deposits andgrow our deposit base depends in part on our ability to expand our network of branches, which requires theapproval of the Reserve Bank of India. In September 2005, the Reserve Bank of India replaced the existingsystem of granting authorisations for opening individual branches with a system of giving aggregated approvalscovering both branches and existing non-branch channels like ATMs, on an annual basis. While we have recentlyreceived the Reserve Bank of India’s authorizations for establishing new branches and additional off-site ATMs,there can be no assurance that these authorizations or future authorizations granted by the Reserve Bank of Indiawill meet our requirements for branch expansion to achieve the desired growth in our deposit base. High volumesof deposit withdrawals or failure of a substantial number of our depositors to roll over deposited funds uponmaturity or to replace deposited funds with fresh deposits as well as our inability to grow our deposit base, couldhave an adverse effect on our liquidity position, our business, our future financial performance, our stockholders’equity and the price of our notes. See also “—Financial difficulty and other problems in certain financialinstitutions in India could adversely affect our business and the price of our notes”.

We are subject to legal and regulatory risk which may adversely affect our business.

We are subject to a wide variety of banking and financial services laws and regulations and a large numberof regulatory and enforcement authorities in each of the jurisdictions in which we operate. The laws andregulations governing the banking and financial services industry have become increasingly complex governing awide variety of issues, including interest rates, liquidity, capital adequacy, securitization, investments, ethicalissues, money laundering, privacy, record keeping, and marketing and selling practices, with sometimesoverlapping jurisdictional or enforcement authorities.

Failure to comply with applicable regulations in various jurisdictions, including unauthorized actions byemployees, representatives, agents and third parties, suspected or perceived failures and media reports, andensuing inquiries or investigations by regulatory and enforcement authorities, has resulted, and may result inregulatory action including financial penalties and restrictions on or suspension of the related businessoperations. For example, in fiscal 2006, the Reserve Bank of India imposed a penalty of Rs. 0.5 million(US$ 10,881) on us in connection with our role as collecting bankers in certain public offerings of equity bycompanies in India.

In addition, a failure to comply with the applicable regulations in various jurisdictions by our employees,representatives, agents and third party service providers, either in or outside the course of their services, orsuspected or perceived failures by them, may result in inquiries or investigations by regulatory and enforcementauthorities, in regulatory or enforcement action against either us or such employees, representatives, agents andthird party service providers or both and such actions may, amongst other consequences, impact our reputation,result in adverse media reports, lead to increased or enhanced regulatory or supervisory concerns, lead toadditional costs, penalties, claims and expenses being incurred by us or impact adversely on our ability toconduct business owing to implications on business continuity, possible distraction, lack of proper attention ortime by such employees, representatives, agents and third party service providers to their official roles and duties,or suspension or termination by us of their services and having to find suitable replacements apart from personalliability, financial or other penalties and restrictions that may be imposed on or suffered by them, includingpersonal liability for criminal violation.

If we fail to manage our legal and regulatory risk in the many jurisdictions in which we operate, includingsome or all of the compliance failures, our business could suffer, our reputation could be harmed and we would

22

be subject to additional legal risk. This could, in turn, increase the size and number of claims and damagesasserted against us or subject us to regulatory investigations, enforcement actions or other proceedings, or lead toincreased regulatory or supervisory concerns. We may also be required to spend additional time and resources onany remedial measures which could have an adverse effect on our business.

Despite our best efforts to comply with all applicable regulations, there are a number of risks that cannot becompletely controlled. Our rapid international expansion has led to increased risk in this respect. Regulators inevery jurisdiction in which we operate or have listed our notes have the power to bring administrative or judicialproceedings against us (or our employees, representatives, agents and third party service providers), which couldresult, among other things, in suspension or revocation of one or more of our licenses, cease and desist orders,fines, civil penalties, criminal penalties or other disciplinary action which could materially harm our results ofoperations and financial condition.

We cannot predict the timing or form of any current or future regulatory or law enforcement initiatives,which we note are increasingly common for international banks, but we would expect to cooperate with any suchregulatory investigation or proceeding.

Regulatory changes in India or other jurisdictions in which we operate could adversely affect our business.

The laws and regulations or the regulatory or enforcement environment in any of those jurisdictions inwhich we operate may change at any time and may have an adverse effect on the products or services we offer,the value of our assets or our business in general. In its mid-term review of the annual policy statement for fiscal2005, the Reserve Bank of India increased the risk weight for the computation of capital adequacy from 50% to75% in the case of housing loans and from 100% to 125% in the case of consumer credit (including personalloans and credit cards) as a temporary counter-cyclical measure. In July 2005, the Reserve Bank of Indiaincreased the risk weight for capital market exposure and exposure to commercial real estate from 100% to125%. In October 2005, in its mid-term review of the annual policy statement for fiscal 2005, the Reserve Bankof India increased the requirement of general provisioning for standard advances from 0.25% to 0.40% exceptdirect advances to agriculture and small and medium enterprise sectors. In February 2006, the Reserve Bank ofIndia issued its final guidelines on securitization of standard assets under which we are, in respect of transactionsafter February 1, 2006, required to maintain higher capital for credit enhancement and also amortize the profit onsecuritization over the life of the related loans. In April 2006, the Reserve Bank of India increased therequirement of general provisioning for certain categories of advances from 0.40% to 1.00% and also increasedthe risk weight on exposures to commercial real estate from 125.0% to 150.0%. In its mid term review of theannual policy statement announced in October 2006, the Reserve Bank of India increased the repo rate by 25basis points from 7.0% to 7.25%. In December 2006, the Reserve Bank of India increased the cash reserve ratioby 50 basis points from 5.0% to 5.5%. Similar changes in the future could have an adverse impact on our capitaladequacy and profitability. Pursuant to the recent amendment to the Reserve Bank of India Act, no interest ispayable on cash reserve ratio balances, on which interest was hitherto paid by the Reserve Bank of India. Anychange by the Reserve Bank of India in the directed lending norms may result in our inability to meet the prioritysector lending requirements as well as require us to increase our lending to relatively riskier segments and mayresult in an increase in non-performing assets in the directed lending portfolio.

We have experienced rapid international growth in the last three years which has increased the complexityof the risks that we face.

Until very recently, we operated only in India. Beginning in fiscal 2004, we began a rapid internationalexpansion opening banking subsidiaries in the United Kingdom, Canada and Russia and branches in Hong Kong,Bahrain, Singapore, Sri Lanka and Dubai and representative offices in several countries. As of the six monthsended September 30, 2006, the assets of these banking subsidiaries and branches constituted approximately 16%of the consolidated assets of ICICI Bank and its banking subsidiaries. In addition, we have substantiallyexpanded, in a number of jurisdictions, our services to non-resident Indians for the remittance of funds to India.

23

This rapid international expansion into banking in multiple jurisdictions exposes us to a new variety ofregulatory and business challenges and risks, including cross-cultural risk and has increased the complexity ofour risks in a number of areas including currency risks, interest rate risks, compliance risk, regulatory andreputational risk and operational risk. See also “We are subject to legal and regulatory risk which may adverselyaffect our business”. The skills required for this business could be different from those required for our Indianbusiness and we may not be able to attract the required talented professionals. If we are unable to manage theserisks, our business could be adversely affected.

A determination against us in respect of disputed tax assessments may adversely impact our financialperformance.

We have been assessed a significant amount in additional taxes by the Government of India’s tax authoritiesin excess of our provisions. See “Business—Legal and Regulatory Proceedings”. We have appealed all of thesedemands. While we expect that no additional liability will arise out of these disputed demands, there can be noassurance that these matters will be settled in our favor or that no further liability will arise out of these demands.Any additional tax liability may adversely impact our financial performance and shareholders’ equity.

We are involved in various litigations and any final judgment awarding material damages against us couldhave a material adverse impact on our future financial performance, our stockholders’ equity and the priceof our notes.

We are often involved in litigations for a variety of reasons, which generally arise because we seek torecover our dues from borrowers or because customers seek claims against us. The majority of these cases arisein the normal course and we believe, based on the facts of the cases and consultation with counsel, that thesecases generally do not involve the risk of a material adverse impact on our financial performance orshareholders’ equity. Where we assess that there is a probable risk of loss, it is our policy to make provisions forthe loss. However, we do not make provisions or disclosures in our financial statements where our assessment isthat the risk is insignificant. See “Business—Legal and Regulatory Proceedings”. We cannot guarantee that thejudgments in any of the litigation in which we are involved would be favorable to us. If our assessment of therisk changes, our view on provisions will also change.

Our rapid retail expansion in India, our rural initiative and our insurance ventures expose us to increasedrisk that may adversely affect our business.

We have experienced rapid growth in our retail loan portfolio. Our joint ventures in life insurance andgeneral insurance have experienced rapid growth in their business volumes. Our branch network has alsosignificantly expanded and we are entering into new, smaller second tier cities within India as part of this growthstrategy. In addition, we are now beginning a rural initiative designed to bring our products and services intomany rural areas. This rapid growth of the retail loan business and the insurance businesses as well as the ruralinitiative exposes us to increased risks within India including the risk that our impaired loans may grow fasterthan anticipated, the risk that we may not be able to raise the substantial capital required for these businesses,increased operational risk, increased fraud risk and increased regulatory and legal risk. See also “We are subjectto legal and regulatory risk which may adversely affect our business”.

If we are not able to integrate any future acquisitions, our business could be disrupted.

We may seek opportunities for growth through acquisitions or be required to undertake mergers mandatedby RBI. On December 9, 2006, our board of directors and the board of directors of The Sangli Bank Limited, orSangli Bank, an unlisted private sector bank, approved an all-stock amalgamation of Sangli Bank with us. Atyear-end fiscal 2006, Sangli Bank had total assets of Rs. 21.51 billion, total deposits of Rs. 20.04 billion, totalloans of Rs. 8.88 billion and total capital adequacy of only 1.6%. In fiscal 2006, it incurred a loss of Rs. 0.29billion. The amalgamation is subject to the approval of the shareholders of both banks and the Reserve Bank of

24

India and there can be no assurance that such approval will be received. This and any future acquisitions ormergers may involve a number of risks, including deterioration of asset quality, diversion of our management’sattention required to integrate the acquired business and the failure to retain key acquired personnel and clients,leverage synergies or rationalise operations, or develop the skills required for new businesses and markets, orunknown and known liabilities, some or all of which could have an adverse effect on our business.

We are exposed to fluctuations in foreign exchange rates.

As a financial intermediary we are exposed to exchange rate risk. See “Risk Management—Quantitative andQualitative Disclosures About Market Risk—Exchange Rate Risk”. Adverse movements and volatility in foreignexchange rates may adversely affect our borrowers, the quality of our exposure to our borrowers and ourbusiness.

Our business is very competitive and our growth strategy depends on our ability to compete effectively.

Within the Indian market, we face intense competition from Indian and foreign commercial banks in all ourproducts and services. Foreign banks also operate in India through non-banking finance companies. Furtherliberalization of the Indian financial sector could lead to a greater presence or new entries of foreign banksoffering a wider range of products and services, which would significantly toughen our competitive environment.In addition, the Indian financial sector may experience further consolidation, resulting in fewer banks andfinancial institutions, some of which may have greater resources than us. The Government of India has indicatedits support for consolidation among government-owned banks. The Reserve Bank of India has announced a roadmap for the presence of foreign banks in India that would, after a review in 2009, allow foreign banks to acquireup to a 74.0% shareholding in an Indian private sector bank. See “Business—Competition” and “Overview of theIndian Financial Sector—Commercial Banks—Foreign Banks”. Due to competitive pressures, we may be unableto successfully execute our growth strategy and offer products and services at reasonable returns and this mayadversely impact our business.

In our international operations we also face intense competition from the full range of competitors in thefinancial services industry, both banks and non-banks and both Indian and foreign banks. We remain a small tomid-size player in the international markets and many of our competitors have resources much greater than ourown.

Fraud and significant security breaches in our computer system and network infrastructure could adverselyimpact our business.

Our business operations are based on a high volume of transactions. Although we take adequate measures tosafeguard against system-related and other fraud, there can be no assurance that we would be able to preventfraud. Our reputation could be adversely affected by fraud committed by employees, customers or outsiders.Physical or electronic break-ins, security breaches, other disruptive problems caused by our increased use of theInternet or power disruptions could also affect the security of information stored in and transmitted through ourcomputer systems and network infrastructure. Although we have implemented security technology andoperational procedures to prevent such occurrences, there can be no assurance that these security measures willbe successful. A significant failure in security measures could have a material adverse effect on our business.

System failures could adversely impact our business.

Given the increasing share of retail products and services and transaction banking services in our totalbusiness, the importance of systems technology to our business has increased significantly. Our principaldelivery channels include ATMs, call centers and the Internet. Any failure in our systems, particularly for retailproducts and services and transaction banking, could significantly affect our operations and the quality of ourcustomer service and could result in business and financial losses.

25

There is operational risk associated with our industry which, when realized, may have an adverse impact onour business.

We, like all financial institutions, are exposed to many types of operational risk, including the risk of fraudor other misconduct by employees or outsiders, unauthorized transactions by employees and third parties(including violation of regulations for prevention of corrupt practices, and other regulations governing ourbusiness activities), or operational errors, including clerical or record keeping errors or errors resulting fromfaulty computer or telecommunications systems. We use direct marketing associates for marketing our retailcredit products. We also outsource some functions to other agencies. Given our high volume of transactions,certain errors may be repeated or compounded before they are discovered and successfully rectified. In addition,our dependence upon automated systems to record and process transactions may further increase the risk thattechnical system flaws or employee tampering or manipulation of those systems will result in losses that aredifficult to detect. We may also be subject to disruptions of our operating systems, arising from events that arewholly or partially beyond our control (including, for example, computer viruses or electrical ortelecommunication outages), which may give rise to a deterioration in customer service and to loss or liability tous. We are further exposed to the risk that external vendors may be unable to fulfill their contractual obligationsto us (or will be subject to the same risk of fraud or operational errors by their respective employees as are we),and to the risk that its (or its vendors’) business continuity and data security systems prove not to be sufficientlyadequate. We also face the risk that the design of our controls and procedures prove inadequate, or arecircumvented, thereby causing delays in detection or errors in information. Although we maintain a system ofcontrols designed to keep operational risk at appropriate levels, like all banks we have suffered losses fromoperational risk and there can be no assurance that we will not suffer losses from operational risks in the futurethat may be material in amount, and our reputation could be adversely affected by the occurrence of any suchevents involving our employees, customers or third parties. For a discussion of how operational risk is managed,see “Business—Risk Management—Operational Risk”.

We are subject to credit, market and liquidity risk which may have an adverse effect on our credit ratingsand our cost of funds.

To the extent any of the instruments and strategies we use to hedge or otherwise manage our exposure tomarket or credit risk are not effective, we may not be able to mitigate effectively our risk exposures in particularmarket environments or against particular types of risk. Our balance sheet growth will be dependent uponeconomic conditions, as well as upon our determination to securitize, sell, purchase or syndicate particular loansor loan portfolios. Securitization is an important element of our funding and capital management strategy. TheIndian securitization market is still evolving in terms of asset classes, participants and regulations and there canbe no assurance of our continuing ability to securitize loan portfolios. In November 2006, CRISIL, an Indiancredit rating agency, lowered the rating of a personal loan receivables pool, securitized by us, by two notches dueto higher than anticipated utilization of the cash collateral stipulated at the initiation of the transaction. Ourtrading revenues and interest rate risk are dependent upon our ability to properly identify, and mark to market,changes in the value of financial instruments caused by changes in market prices or rates. Our earnings aredependent upon the effectiveness of our management of migrations in credit quality and risk concentrations, theaccuracy of our valuation models and our critical accounting estimates and the adequacy of our allowances forloan losses. To the extent our assessments, assumptions or estimates prove inaccurate or not predictive of actualresults, we could suffer higher than anticipated losses. See also “—Further deterioration of our non-performingasset portfolio and an inability to improve our provisioning coverage as a percentage of gross non-performingassets, could adversely affect the price of our notes”. The successful management of credit, market andoperational risk is an important consideration in managing our liquidity risk because it affects the evaluation ofour credit ratings by rating agencies. Rating agencies may reduce or indicate their intention to reduce the ratingsat any time. See also “—Any downgrading of India’s debt rating by an international rating agency couldadversely affect our business and the price of our notes”. The rating agencies can also decide to withdraw theirratings altogether, which may have the same effect as a reduction in our ratings. Any reduction in our ratings (orwithdrawal of ratings) may increase our borrowing costs, limit our access to capital markets and adversely affectour ability to sell or market our products, engage in business transactions, particularly longer-term and

26

derivatives transactions, or retain our customers. This, in turn, could reduce our liquidity and negatively impactour operating results and financial condition. For more information relating to our ratings, see “Business—Quantitative and Qualitative Disclosures About Market Risk—Liquidity Risk”.

We depend on the accuracy and completeness of information about customers and counterparties.

In deciding whether to extend credit or enter into other transactions with customers and counterparties, wemay rely on information furnished to us by or on behalf of customers and counterparties, including financialstatements and other financial information. We may also rely on certain representations as to the accuracy andcompleteness of that information and, with respect to financial statements, on reports of independent auditors.For example, in deciding whether to extend credit, we may assume that a customer’s audited financial statementsconform with generally accepted accounting principles and present fairly, in all material respects, the financialcondition, results of operations and cash flows of the customer. Our financial condition and results of operationscould be negatively affected by relying on financial statements that do not comply with generally acceptedaccounting principles or other information that is materially misleading.

Any inability to attract and retain talented professionals may adversely impact our business.

Attracting and retaining talented professionals is a key element of our strategy and we believe it to be asignificant source of competitive advantage. See “Business—Employees”. Our inability to attract and retaintalented professionals or the loss of key management personnel could have an adverse impact on our business.

If we are required to change our accounting policies with respect to the expensing of stock options, ourearnings could be adversely affected.

We currently deduct the expense of employee stock option grants from our income based on the intrinsicvalue method and not on the fair value method. Had compensation costs for our employee stock options beendetermined in a manner consistent with the fair value approach, our profit after tax for the six months endedSeptember 30, 2006 as reported would have been reduced to the pro forma amount of Rs. 13.30 billion (US$ 289million) from Rs. 13.75 billion (US$ 300 million) and for fiscal 2006, to Rs. 24.88 billion (US$ 541 million)from Rs. 25.40 billion (US$ 553 million).

Risks Relating to the Notes

A public market may not develop for the notes.

Prior to this offering there has been no trading market in the notes. Approval-in-principle has been obtainedfor the listing of the notes on the Singapore Exchange, but we cannot assure you that the listing will be obtained.The Initial Purchasers have advised us that one or more of their affiliates currently intends to make a market inthe notes. However, the Initial Purchasers’ affiliates are not obligated to make markets in the notes and maydiscontinue this market-making activity at any time without notice. In addition, market-making activity by theInitial Purchasers’ affiliates may be subject to limits imposed by applicable law. As a result, we cannot assureyou that any market in the notes will develop or, if it does develop, it will be maintained. If an active market inthe notes fails to develop or be sustained, you may not be able to sell the notes or may have to sell them at alower price.

The notes will be unsecured and deeply subordinated obligations.

The notes will be unsecured and deeply subordinated obligations. The notes are not deposits and are notinsured by any regulatory agency and they may not be used as collateral for any loan made by us. In the event ofa winding up of our operations, your claims will be subordinated in right of payment to the prior payment in fullof all of our other liabilities (whether actual or contingent, present or future) including all deposit liabilities andother liabilities and all of our offices and branches, except those liabilities which by their terms rank equal withor junior to the notes.

27

As a consequence of the subordination provisions, in the event of a winding up of our operations, you mayrecover less rateably than the holders of deposit liabilities or the holders of our other liabilities that rank senior tothe notes. The notes, the Indenture and the Calculation Agency Agreement do not limit the amount of theliabilities ranking senior to the notes which may be hereafter incurred or assumed by us.

You will have limited rights of acceleration if amounts are due but not paid on the notes.

In the event of a default in payment on the notes, you will have no right to accelerate payments on the notes,except if a court order is made or an effective resolution is passed for our winding-up.

The notes may not qualify as Upper Tier II capital.

There is no guarantee that the notes will qualify as Upper Tier II capital under the regulations published bythe Reserve Bank of India. See “Supervision and Regulation—Capital Adequacy Requirements”. The failure ofthe notes to qualify as Upper Tier II capital due to any reason (including changes in laws, regulations orinterpretations of the Reserve Bank of India or other government authorities) would adversely affect our capitaladequacy ratio.

The rating of the notes may be lowered or withdrawn depending on some factors, including the ratingagency’s assessment of our financial strength and Indian sovereign risk.

It is a condition to the issuance of the notes that they be rated at least “Baa2” by Moody’s or “BB-” by S&P.The rating addresses the likelihood of payment of principal on redemption and the timely payment of interest oneach payment date. The rating of the notes is not a recommendation to purchase, hold or sell the notes, and therating does not comment on market price or suitability for a particular investor. We cannot assure you that therating of the notes will remain for any given period of time or that the rating will not be lowered or withdrawn. Adowngrade in the rating of the notes will not be an event of default under the indenture. The assigned rating maybe raised or lowered depending, among other factors, on the rating agency’s assessment of our financial strengthas well as its assessment of Indian sovereign risk generally.

28

USE OF PROCEEDS

The net proceeds from the sale of the notes is approximately US$ 746,500,000 (after deducting fees,commissions and expenses) which we intend to use for general corporate purposes in accordance with anyapplicable rules or regulations.

29

CAPITALIZATION

The following table sets out our capitalization at September 30, 2006 derived from our auditedunconsolidated financial statements prepared in accordance with Indian GAAP. For additional information, seeour financial statements and accompanying schedules included elsewhere in this offering memorandum.

As of September 30, 2006

(Rs. inbillions)

(US$ inmillions)

Borrowings(1):Short-term debt(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 183.63 3,996Long-term debt(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 332.38 7,234

Total debts (A) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 516.01 11,230

Shareholders’ funds:Share capital(4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12.43 270Reserves . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 226.57 4,931Less : Unamortized deferred revenue expenditure(5) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.69 15

Total shareholders’ funds (B) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 238.31 5,186

Total capitalization (A) + (B) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 754.32 16,416Capital adequacy:Tier I (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9.38%Tier II (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.96%

Total (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14.34%

(1) Borrowings do not include deposits.(2) Short-term debt is debt maturing within the next one year from the date of above statement, which includes

bonds in the nature of subordinated debt (excluded from Tier II capital) of Rs. 5.56 billion.(3) Includes Rs. 150.39 billion of unsecured redeemable debentures and bonds in the nature of subordinated

debt eligible for inclusion in Tier II capital.(4) Includes preference share capital of Rs. 3.50 billion.(5) Unamortized expenses on account of the early retirement option scheme offered to the employees.(6) We are raising funds simultaneously with this issue via a two-tranche bond issue out of our Bahrain branch

in an aggregate amount of USD 1,250,000,000.

30

SELECTED FINANCIAL DATA

Our financial and other data for fiscal 2002 through fiscal 2006 and the six months ended September 30,2005 and 2006 included in this offering memorandum have been derived from our unconsolidated financialstatements prepared in accordance with generally accepted accounting principles in India, or Indian GAAP,guidelines issued by the Reserve Bank of India from time to time and practices generally prevailing in thebanking industry in India. These financial statements do not include the results of operations of our subsidiariesand other consolidating entities. The principal subsidiaries whose results are not included are: ICICI SecuritiesLimited, ICICI Prudential Life Insurance Company Limited, ICICI Lombard General Insurance CompanyLimited, ICICI Venture Funds Management Company Limited, ICICI Home Finance Company Limited,Prudential ICICI Asset Management Company Limited, ICICI Bank UK Limited, ICICI Bank Canada Limitedand ICICI Bank Eurasia Limited Liability Company.

The financial statements for fiscal 2002 were audited by S. B. Billimoria & Co., Chartered Accountants, forfiscal 2003 jointly by N. M. Raiji & Co., Chartered Accountants and S. R. Batliboi & Co., Chartered Accountantsand for fiscal 2004, 2005 and 2006 and the six months ended September 30, 2005 by S. R. Batliboi & Co.,Chartered Accountants and for the six months ended September 30, 2006 by BSR & Co., Chartered Accountants.You should read the following discussion and analysis of our selected financial and operating data with the moredetailed information contained in our audited unconsolidated financial statements. The following discussion isbased on our audited unconsolidated financial statements and accompanying notes prepared in accordance withIndian GAAP, while the financial information in our annual reports on Form 20-F for the fiscal year 2006 isbased on our audited consolidated financial statements and accompanying notes prepared in accordance withIndian GAAP with the net income and stockholders’ equity reconciled to US GAAP. Financial information in ourannual report on Form 20-F for the fiscal years 2000 to 2005 filed with the SEC was prepared in accordance withUS GAAP. US GAAP requires consolidation as a fundamental basis of accounting. For a discussion of thesignificant differences between Indian GAAP and US GAAP, see “Description of Certain Differences betweenIndian GAAP and US GAAP”.

The amalgamation of ICICI, ICICI Personal Financial Services and ICICI Capital Services with us wasaccounted for using the purchase method of accounting. The effective date of the amalgamation was May 3,2002. However, the date of the amalgamation for accounting purposes under Indian GAAP was the AppointedDate under the Scheme of Amalgamation approved by the High Courts of Bombay and Gujarat and the ReserveBank of India, which was March 30, 2002. Accordingly, our profit and loss account (hereinafter referred to asincome statement) for fiscal 2002 includes the results of operations of ICICI, ICICI Personal Financial Servicesand ICICI Capital Services for only two days, i.e., March 30 and 31, 2002, although our balance sheet for fiscal2002 reflects the full impact of the amalgamation. As a result of the above, the income statement for fiscal 2003is not comparable with the income statements for fiscal 2002 and prior years.

31

Operating Results Data

The operating results data for the fiscal years 2003, 2004, 2005 and 2006 and the six months endedSeptember 30, 2005 and September 30, 2006 are not comparable with the operating results data for fiscal 2002due to the amalgamation.

Year ended March 31, Six months ended September 30,

2002 2003 2004 2005 2006 2005 2006 2006

(Rupees in billions, except per share data)

(US$ in millions,except per share

data)Interest income

Interest on advances(1) . . . . . . . . . . Rs. 7.74 Rs. 61.73 Rs. 63.80 Rs. 71.22 Rs.102.07 Rs. 45.54 Rs. 72.27 US$ 1,573Income on investments(2) . . . . . . . . 12.34 29.10 25.40 22.29 36.93 16.86 28.27 615Interest on balances with Reserve

Bank of India and other inter-bank funds and others . . . . . . . . . 1.46 4.42 3.88 4.28 4.06 2.05 4.54 99

Total interest income . . . . . . . . . . . . Rs. 21.54 Rs. 95.25 Rs. 93.08 Rs. 97.79 Rs.143.06 Rs. 64.45 Rs.105.08 US$ 2,287Interest expense

Interest on deposits . . . . . . . . . . . . . Rs.(13.89) Rs.(24.80) Rs.(30.23) Rs.(32.52) Rs. (58.37) Rs.(26.29) Rs. (53.38) (1,162)Interest on Reserve Bank of India/

inter-bank borrowings . . . . . . . . (0.48) (1.83) (2.29) (2.53) (9.25) (3.87) (5.92) (129)Others (including interest on

borrowings of ICICI)(3) . . . . . . . . (1.22) (52.81) (37.63) (30.66) (28.35) (13.90) (15.26) (332)

Total interest expense . . . . . . . . . . . . Rs.(15.59) Rs.(79.44) Rs.(70.15) Rs.(65.71) Rs. (95.97) Rs.(44.06) Rs. (74.56) US$ 1,623

Net interest income . . . . . . . . . . . . . . Rs. 5.95 Rs. 15.81 Rs. 22.93 Rs. 32.08 Rs. 47.09 Rs. 20.39 Rs. 30.52 US$ 664Non-interest income

Commission, exchange andbrokerage . . . . . . . . . . . . . . . . . . Rs 2.30 Rs. 7.92 Rs. 10.72 Rs. 19.21 Rs. 30.02 Rs.12.52 Rs. 19.45 US$ 423

Profit/(loss) on sale of investments(net) . . . . . . . . . . . . . . . . . . . . . . 3.06 4.92 12.25 5.46 7.50 3.65 3.10 67

Profit/(loss) on foreign exchangetransactions (net) . . . . . . . . . . . . 0.37 0.10 1.93 3.15 4.73 1.83 1.60 35

Profit/(loss) on revaluation ofinvestments (net) . . . . . . . . . . . . (0.15) — — — (0.54) (0.07) 0.40 9

Lease income . . . . . . . . . . . . . . . . . 0.11 5.37 4.21 4.08 3.61 1.74 1.30 28Profit on sale of shares of ICICI

Bank held by ICICI . . . . . . . . . . — 11.91 — — — — — —Miscellaneous income(4) . . . . . . . 0.06 1.37 1.54 2.26 4.51 2.35 2.63 58